Man-Portable Air Defense Systems (MANPADS) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 5.34 Billion |

| Market Size (2030) | USD 6.97 Billion |

| Growth Rate (2025 - 2030) | 5.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Man-Portable Air Defense Systems (MANPADS) Market Analysis by Mordor Intelligence

The man-portable air defense systems (MANPADS) market size stood at USD 5.34 billion in 2025 and is forecast to reach USD 6.97 billion by 2030, expanding at a 5.47% CAGR. Escalating geopolitical tensions, record-high defense budgets, and spreading low-cost aerial threats reinforce procurement pipelines across mature and emerging defense economies.[1]Source: Stockholm International Peace Research Institute, “Global Military Expenditure Reaches New Record High in 2024,” sipri.org Defense ministries channel funds toward network-ready, soldier-portable interceptors that close coverage gaps left by fixed and vehicle-mounted short-range air-defense programs. Suppliers are layering artificial-intelligence-driven sensor fusion and modular open-architecture launchers onto proven missile bodies to stay competitive, even as stringent export controls and component bottlenecks complicate global supply chains. While traditional very-short-range interceptors dominate current inventories, incremental demand is tilting toward longer-reach missiles that push engagement to 10 km and above, reflecting the faster, higher-altitude profiles of modern aircraft and unmanned systems. Competitive intensity is rising as Eastern European and Asian manufacturers scale production capacity and forge cross-border ventures that challenge the incumbency of US and Western European primes.

Key Report Takeaways

- By range, very short-range systems held 63.74% of the MANPADS market share in 2024; Short-Range systems are projected to post the fastest 6.23% CAGR through 2030.

- By guidance technology, infrared homing captured 64.90% share of the MANPADS market size in 2024, while laser beam-rider solutions are on track for a 6.78% CAGR to 2030.

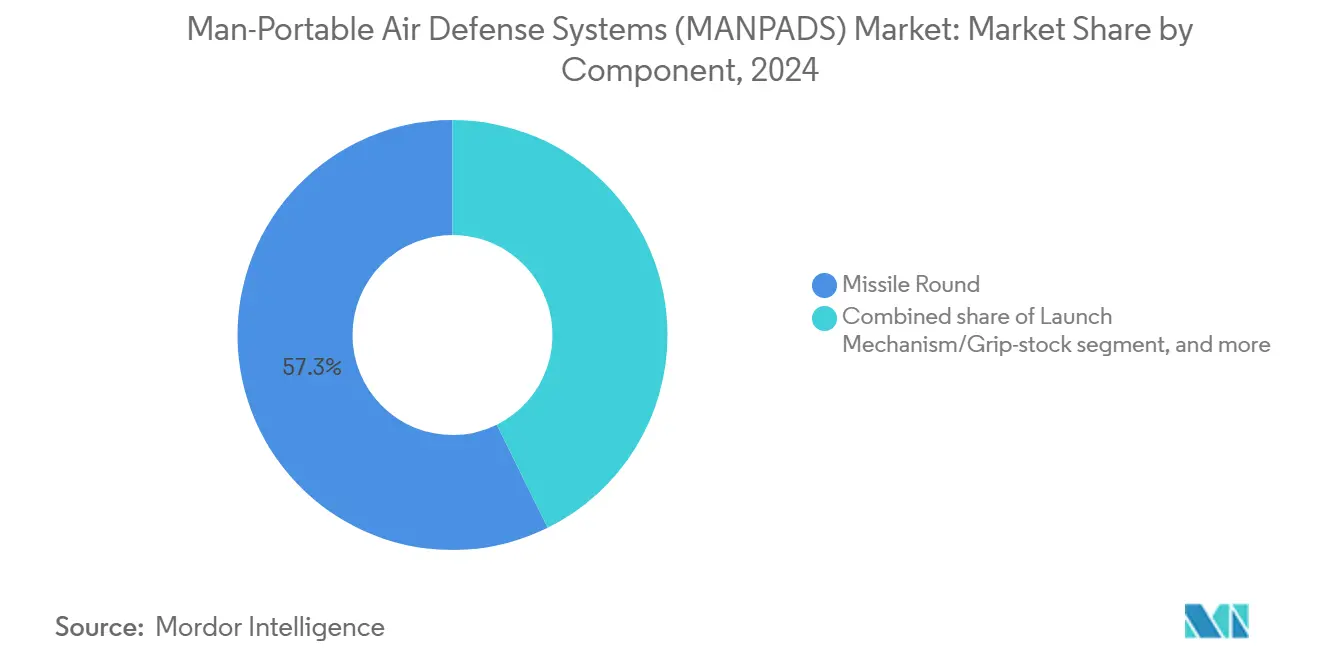

- By component, missile rounds accounted for 57.30% of revenue in 2024; fire-control and sighting units are set to expand at a 6.30% CAGR through 2030.

- By end-user, the military segment led with 86.70% share of the MANPADS market in 2024; homeland security demand is pacing a 7.40% CAGR to 2030.

- By geography, North America commanded 34.50% revenue share in 2024, whereas Asia-Pacific is advancing at a 7.21% CAGR to 2030.

Global Man-Portable Air Defense Systems (MANPADS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global defense budgets | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Surge in low-cost UAV and loitering-munitions threats | +0.9% | Middle East, Eastern Europe, Asia-Pacific | Short term (≤ 2 years) |

| Modernization programmes for short-range air-defense layers | +0.8% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Intensifying geopolitical conflicts | +0.7% | Eastern Europe, Middle East, South China Sea | Short term (≤ 2 years) |

| Modular open-architecture launchers enabling plug-and-play missiles | +0.5% | North America, Europe | Medium term (2-4 years) |

| AI-enabled sensor-fusion accelerating dismounted target acquisition | +0.4% | North America, Europe, select Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Defense Budgets

Global military expenditure hit USD 2.7 trillion in 2024, ushering in sizable procurement windows for MANPADS manufacturers. Germany earmarked EUR 395 million (USD 463 million) for 500 new Stinger missiles to be delivered between 2028 and 2029, while Norway placed a NOK 350 million (USD 35.42 million) order for Polish Piorun systems. Expanded budgets attract smaller contractors such as MESKO, which lifted annual Piorun output beyond 1,000 units in 2024, intensifying rivalry with established primes. The spending upcycle also encourages diversification of supplier bases as governments hedge geopolitical exposure by blending U.S., European, and indigenous solutions into their force structures.

Surge in Low-Cost UAV and Loitering-Munitions Threats

Cheap unmanned aerial vehicles (UAVs) capable of inflicting disproportionate damage are pushing militaries to field MANPADS optimized for small, low-signature targets. The US Marines deployed MADIS vehicles in December 2024, integrating sensors and kinetic effectors to counter group 1–3 drones.[2]Source: The War Zone, “Imaging infrared seeker for APKWS guided rockets is in the works,” twz.com Manufacturers are responding with multi-spectral seekers and AI-enabled discrimination algorithms that filter decoys without sacrificing lock-on speed. This evolution is tightening collaboration between missile houses and electronics firms specializing in machine-vision processors, spawning a new wave of joint-development agreements that accelerate feature rollouts while dispersing R&D risk.

Modernization Programs for Short-Range Air-Defense Layers

Armed forces are swapping legacy stand-alone tubes for networked systems that fit within broader layered-defense constructs. The US Army’s M-SHORAD combines radars, electronic warfare, and MANPADS to protect maneuver units, reinforcing demand for missiles that plug seamlessly into vehicle and command-and-control architectures. European counterparts showcase similar moves: MBDA’s Ground Warden AI module calculates real-time probability-of-kill data for integrated launchers. Resultant design priorities include open software standards, datalink compatibility, and cyber-secure firmware that can be patched in theater.

Intensifying Geopolitical Conflicts

The Ukraine conflict and South China Sea flashpoints are compressing procurement timelines as governments fast-track off-the-shelf buys. Germany’s EUR 780 million (USD 914.15 million) January 2024 Stinger replenishment underscores how conflict-driven donations create replenishment backlogs. Similar patterns are visible in Asia-Pacific, where Taiwan’s NASAMS acquisition in 2024 signaled urgency in bolstering point-defense layers. Compressed lead times reward vendors with surge-capacity production lines and proven export-license track records.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent export‐control/ITAR restrictions | -0.8% | Global, highest on U.S. systems | Long term (≥ 4 years) |

| High R&D and procurement costs for next-gen seekers and batteries | -0.6% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Supply-chain fragility for thermal batteries and IR detector chips | -0.5% | Semiconductor-dependent regions | Short term (≤ 2 years) |

| Adoption of low-cost aircraft DIRCM reducing perceived threat | -0.3% | Commercial and military fleets worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Export-Control/ITAR Restrictions

International Traffic in Arms Regulations (ITAR) complicate foreign sales of US-origin MANPADS, elongating negotiation cycles and elevating compliance costs. Allied customers frequently pivot toward European alternatives from MBDA or Saab AB to sidestep approval bottlenecks, fragmenting demand across multiple suppliers. Export-controlled components also oblige manufacturers to develop region-specific variants, diluting economies of scale and inflating unit costs, particularly for next-generation missiles that incorporate classified seekers or advanced cryptography.

High R&D and Procurement Costs for Next-Generation Seekers and Batteries

True multi-spectral seekers and long-life thermal batteries require niche semiconductor processes and exotic chemistries. Capital outlays for fab upgrades, prototype iterations, and software toolchains price smaller vendors out of the top tier, reinforcing a moderate but persistent consolidation trend. Customer agencies with limited budgets weigh capability advantages against life-cycle costs, encouraging modular upgrade paths that spread payments but extend total program timelines. Component suppliers can guarantee second-source resilience and domestic production footprints by capturing premium contract valuations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Range: Evolving from Point Defense to Extended Reach

Very short-range systems captured 63.74% of the MANPADS market in 2024, driven by entrenched infantry doctrines and low unit cost. Yet Short Range interceptors capable of 6-10 km engagements are projected to log a 6.23% CAGR, expanding the MANPADS market size within higher-altitude threat envelopes. Armed forces want earlier intercept windows against supersonic aircraft and fast drones, prompting rocket motors and trajectory algorithm design tweaks. Suppliers offering plug-and-play missile swap kits for existing grip-stocks are gaining traction, allowing units to tailor range profiles without retraining or new logistics footprints.

The shift also reflects operational lessons from recent conflicts, where dispersed forces confronted saturation attacks from loitering munitions launched beyond 5 km. Extended-reach MANPADS give platoon-level commanders more reaction time, feeding into broader kill-chain data that uplinks to artillery or electronic-warfare batteries. These requirements encourage missile houses to bundle telemetry packages within booster sections while preserving shoulder-fire weight limits below 20 kg.

By Guidance Technology: Infrared Maturity Meets Laser Resilience

Infrared homing retained 64.90% share of the MANPADS market size in 2024, favored for its cost-efficiency and proven reliability. However, laser beam-rider missiles are advancing at a 6.78% CAGR, propelled by their innate immunity to standard infrared flares and high accuracy against low-thermal drones. Field trials demonstrate sub-2 m miss distance against quadcopters, positioning laser solutions for expanded homeland-security adoption where collateral-damage tolerance is minimal.

Multinational development consortia inject AI object-classification into seeker software, allowing dual-mode heads that default to infrared but switch to laser guidance when spoofed. The hybrid approach hedges against proliferating aircraft DIRCM installations, such as the J-MUSIC suite now protecting German government A350s.

By Component: Electronics Drive Future Value Capture

Missile rounds continued to account for 57.30% of MANPADS market revenue in 2024 due to their consumable nature, but fire-control and sighting units are growing fastest at a 6.30% CAGR. Digitally networked optics feed threat data to higher echelons, achieving sensor-to-shooter closures under 5 seconds when integrated with vehicle or drone surveillance feeds. This connectivity transforms launchers from isolated tubes into nodes within composite air-defense grids, elevating software and cyber-hardening expenditures per unit.

Launch mechanisms and grip stocks remain capital goods with refresh cycles exceeding 10 years, but retrofit kits—Bluetooth telemetry pods, augmented-reality sights, and clip-on thermal imagers—are expanding aftermarket revenue streams. Vendors who certify cyber-secure firmware updates gain competitive leverage as militaries institutionalize zero-trust architectures.

By End-User: Homeland Security Accelerates

The military sector owned 86.70% of 2024 revenue, reflecting doctrinal reliance on soldier-portable interceptors. Nevertheless, homeland security agencies are poised for a 7.40% CAGR as airports, energy facilities, and border patrols confront elevated drone threats. Civil responders prefer rechargeable simulators and lock-out features that prevent unauthorized fire, driving an accessory ecosystem distinct from purely military kit.

Inter-agency procurement pools—spanning police, coast guards, and customs units—are scaling volumes sufficient to attract mainstream defense contractors, spurring tailored variants with geofenced engagement logic and lower flight-ceiling pre-sets. This civilian shift could ultimately seed domestic industrial bases in countries that previously imported all MANPADS.

Geography Analysis

North America held 34.50% of the MANPADS market share in 2024, anchored by US tri-service inventories and a well-funded modernization pipeline that stretches across Army, Marine Corps, and Special Operations units. Extensive export portfolios reinforce economies of scale, while newly announced US-based production joint ventures such as RAFAEL and Kratos’ USD 175 million Prometheus Energetics facility aim to secure solid-rocket-motor supply for allied buyers. Continued congressional support for Foreign Military Sales ensures the region’s output remains globally relevant despite rising international competition.

Europe occupies the second-largest revenue position, buoyed by NATO spending surges following Russia’s actions in Ukraine. Joint procurement under the EUR 300 million (USD 351.58 million) EDIRPA framework supports multinational economies of scale. At the same time, individual programs, Germany’s EUR 395 million (USD 462.91 million) Stinger buy and Norway’s NOK 350 million (USD 35.40 million) Piorun deal, bolster domestic stockpiles.[3]Source: European Security & Defence, “ESD Issue 5/2024,” euro-sd.com Emphasis on technology sovereignty is steering R&D toward indigenous seekers and open-system launchers, reducing dependency on ITAR-restricted components. By leveraging rapid-delivery reputations, Eastern European manufacturers are exporting competitively into NATO and beyond.

Asia-Pacific registers the fastest 7.21% CAGR as nations react to maritime disputes and rising great-power rivalry. India’s staggered Igla-S procurement, blending Russian imports with indigenous assembly, illustrates dual-sourcing strategies for capability and industrial self-reliance. Japan’s multibillion-dollar AMRAAM program and Taiwan’s NASAMS fielding underscore the scale of regional air-defense investment. Southeast Asian countries, from Indonesia to the Philippines, are instituting first-generation MANPADS deployments, often financed via offset credits and concessional defense loans.

Competitive Landscape

The man-portable air defense systems (MANPADS) market maintains a moderately consolidated structure where the top five suppliers control an estimated 55-60% of annual deliveries. Lockheed Martin and RTX Corporation remain leaders in the strength of established Stinger and Javelin franchises. Still, European and Asian houses are eating share through agile production and fewer export hurdles. MBDA leverages its Ground Warden AI platform to upsell integration services alongside missile hardware, while Saab positions the RBS 70NG laser system as an ITAR-free alternative for emerging markets.

Cross-border joint ventures are reshaping the value chain. RAFAEL’s partnership with Kratos establishes US rocket-motor capacity that secures eligibility for Pentagon and FMS orders, mitigating past dependency on overseas energetics. AeroVironment’s USD 4.1 billion acquisition of BlueHalo widens its counter-UAS and directed-energy portfolio, positioning the firm as a holistic provider of point-defense solutions. Turkish-origin Roketsan and South Korean LIG Nex1 are cultivating regional partner networks, translating lower labor costs into aggressive pricing.

Technology differentiation increasingly hinges on seeker software, data-link security, and compliance automation that eases export licensing. Vendors embedding artificial-intelligence processors and zero-trust encryption into new builds can renew mature missile designs without complete airframe redesigns, preserving sunk tooling while lifting gross margins. Market entry barriers persist around thermal-battery chemistry and classified algorithms, yet government investment in industrial diversification is opening footholds for smaller electronics and battery specialists.

Man-Portable Air Defense Systems (MANPADS) Industry Leaders

RTX Corporation

Saab AB

Lockheed Martin Corporation

MBDA

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thales and Bharat Dynamics Limited (BDL) delivered the first batch of Laser Beam Riding MANPAD (LBRM) Very Short-Range Air Defense (VSHORAD) missiles and launchers to the Indian Ministry of Defence (MoD), enhancing air defense capabilities with advanced, countermeasure-resistant technology. LBRM systems, including drones, are 60% locally manufactured and counter diverse aerial threats.

- January 2024: Romania signed a USD 96.5 million deal with South Korea for 54 Chiron (KP-SAM MANPADS) launchers, anti-aircraft missiles, and support services under its ‘Strategic Umbrella’ program.

Global Man-Portable Air Defense Systems (MANPADS) Market Report Scope

| Very Short Range (Less than 6 km) |

| Short Range (6 km to10 km) |

| Infrared Homing |

| Laser Beam-Rider |

| Command Line-of-Sight (CLOS) |

| Others |

| Missile Round |

| Launch Mechanism/Grip-stock |

| Fire-Control and Sighting Units |

| Military |

| Homeland Security |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Range | Very Short Range (Less than 6 km) | ||

| Short Range (6 km to10 km) | |||

| By Guidance Technology | Infrared Homing | ||

| Laser Beam-Rider | |||

| Command Line-of-Sight (CLOS) | |||

| Others | |||

| By Component | Missile Round | ||

| Launch Mechanism/Grip-stock | |||

| Fire-Control and Sighting Units | |||

| By End-User | Military | ||

| Homeland Security | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the MANPADS market?

The MANPADS market size reached USD 5.34 billion in 2025 and is projected to climb to USD 6.97 billion by 2030, expanding at a 5.47% CAGR.

Which regional market is growing fastest?

Asia-Pacific is forecasted to record a 7.21% CAGR through 2030 as countries expand air-defense postures.

Which range category is gaining traction?

Short Range MANPADS (6 km to 10 km) show the highest growth at 6.23% CAGR due to demand for longer engagement envelopes.

How are export regulations affecting suppliers?

ITAR and similar rules slow US system exports, steering some buyers toward European or indigenous alternatives.

What technologies are enhancing future MANPADS?

AI-enabled sensor fusion, multi-spectral seekers, and open-architecture launchers are key upgrade trends.

Page last updated on: