Aircraft Interface Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

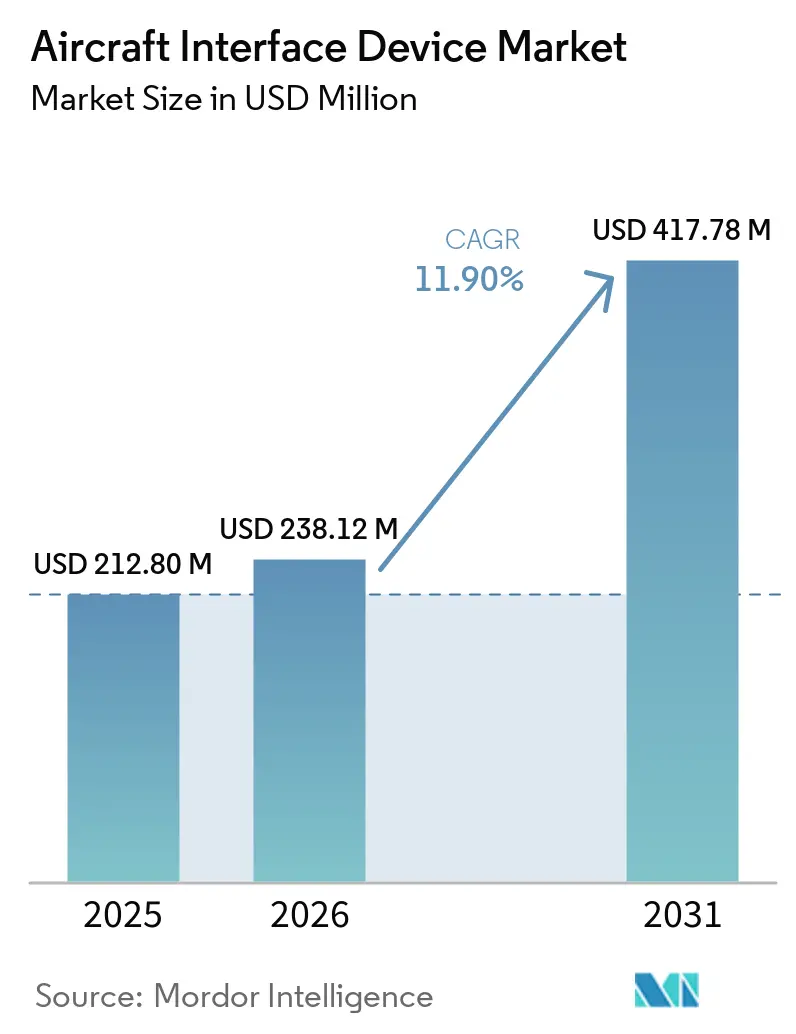

| Market Size (2026) | USD 238.12 Million |

| Market Size (2031) | USD 417.78 Million |

| Growth Rate (2026 - 2031) | 11.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Interface Device Market Analysis by Mordor Intelligence

The aircraft interface device market size in 2026 is estimated at USD 238.12 million, growing from 2025 value of USD 212.80 million with 2031 projections showing USD 417.78 million, growing at 11.90% CAGR over 2026-2031. Rising digital-first flight operations, real-time aircraft health monitoring programs, and the rapid rollout of high-throughput satellite networks are the primary forces propelling this expansion. Airlines and defense operators are replacing paper-based processes with connected electronic workflows relying on secure, high-bandwidth data gateways. At the same time, growing retrofit activity among aging commercial fleets and the accelerating adoption of open-architecture avionics standards have broadened the addressable customer base. Market participants differentiate on certification pedigree, cyber-resilience, and the ability to support multi-protocol data buses and multi-orbit connectivity pathways.

Key Report Takeaways

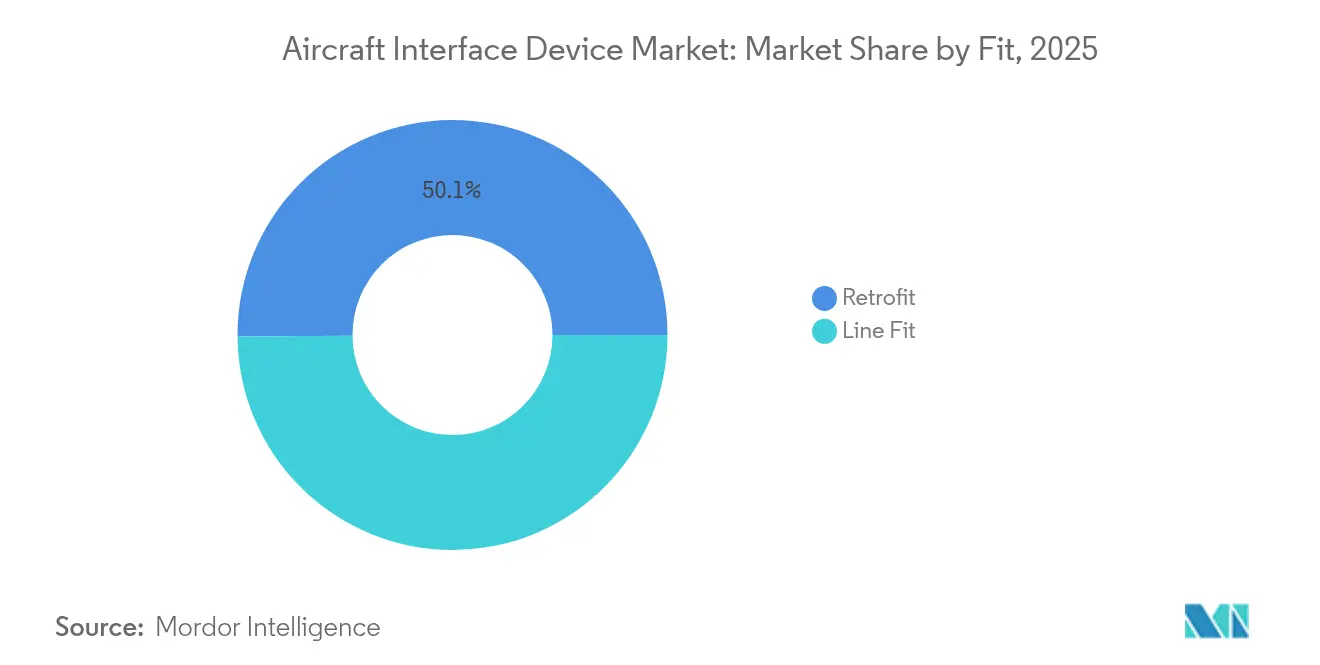

- By fit, line-fit installations held 49.89% of the aircraft interface device market share in 2025, while retrofit solutions are forecasted to post a 14.12% CAGR through 2031.

- By connectivity, wired systems led with 65.22% revenue share in 2025, whereas wireless solutions are anticipated to expand at a 16.10% CAGR to 2031.

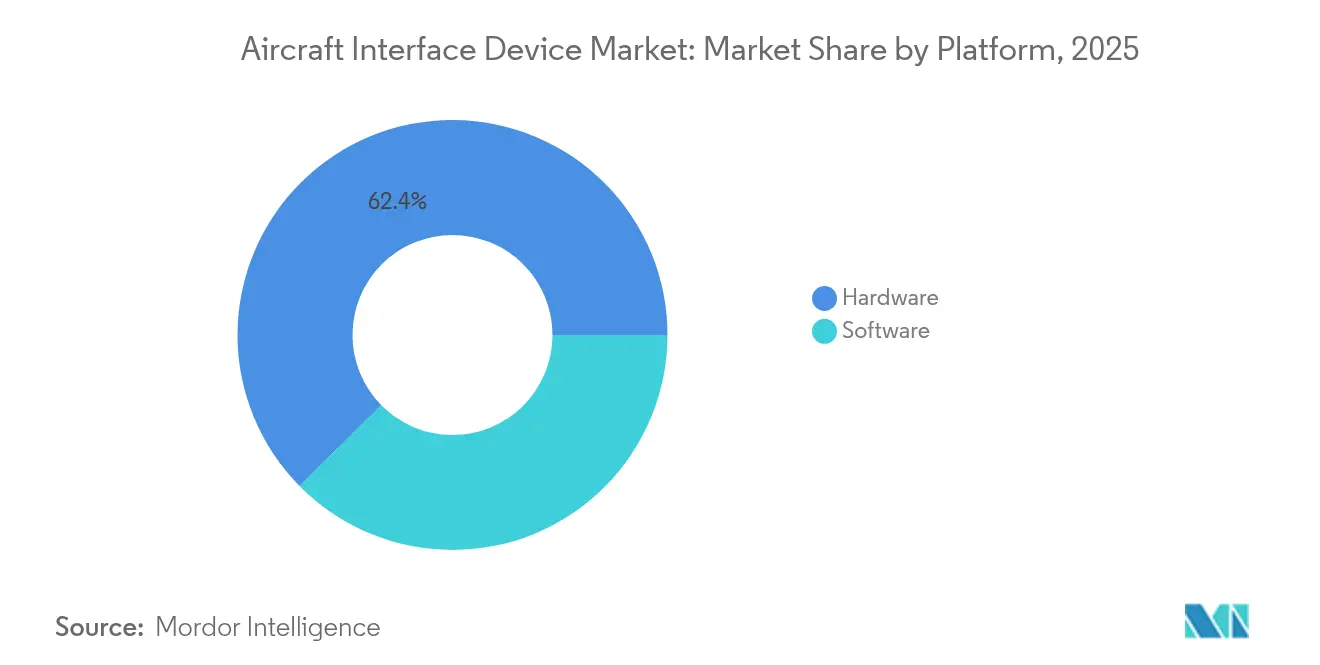

- By platform, hardware captured 62.40% of the aircraft interface device market size in 2025, yet software is growing fastest at 15.35% CAGR.

- By aircraft type, commercial aviation commanded 68.67% market share in 2025; unmanned systems registered the strongest outlook with an 17.30% CAGR.

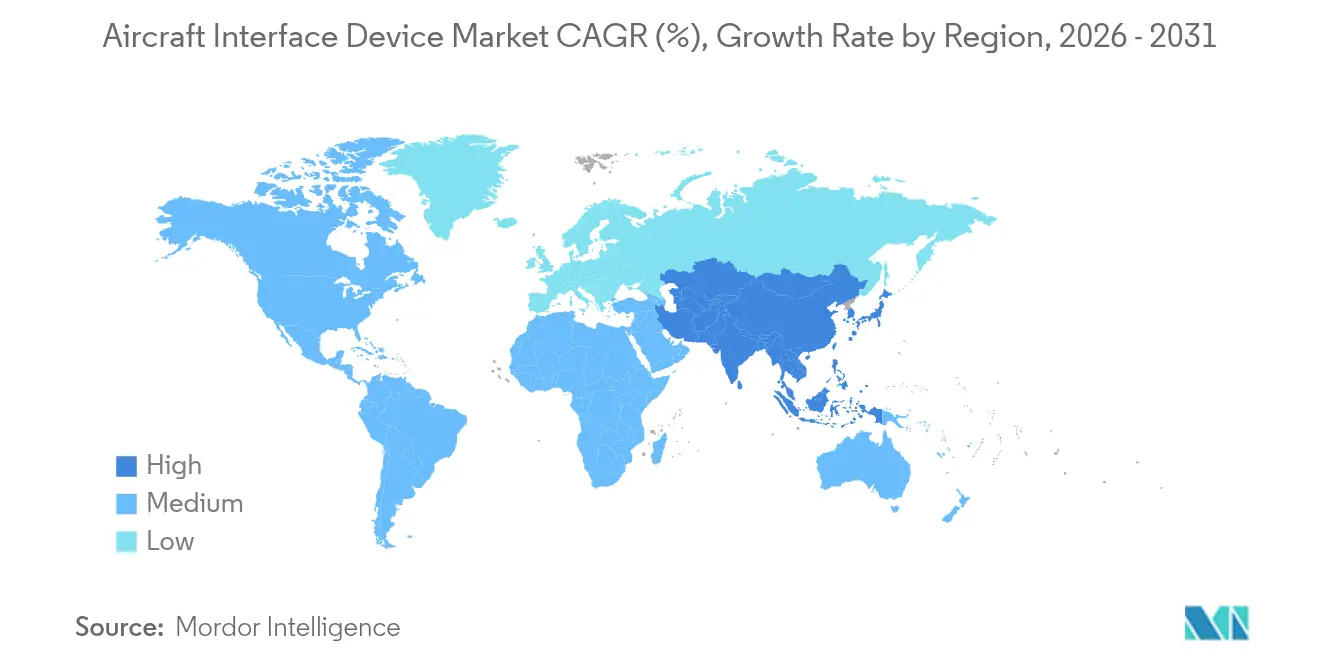

- By geography, North America dominated with 35.96% revenue share in 2025, while Asia-Pacific is projected to advance at a 13.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Interface Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitized flight operations elevates demand for AIDs | +2.8% | North America and Europe | Medium term (2-4 years) |

| Expansion of real-time aircraft health-monitoring and predictive-maintenance ecosystems | +2.1% | Global commercial fleets | Long term (≥ 4 years) |

| Military ISR platforms’ demand for high-speed data-exfiltration interfaces | +1.9% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Adoption of open-architecture avionics standards | +1.6% | Global, early uptake in defense | Long term (≥ 4 years) |

| Accelerating retrofit cycles for Electronic Flight Bag (EFB) upgrades | +1.4% | North America and Europe commercial aviation | Medium term (2-4 years) |

| Proliferation of high-throughput satellite constellations (GEO VHTS, LEO) | +1.2% | Global, with emphasis on remote route coverage | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digitized flight operations elevate demand for AIDs

Airlines have replaced paper charts and performance calculations with fully digital processes dependent on secure, high-capacity data bridges. Certified tablet interface modules like Collins Aerospace’s InteliSight suite stream real-time avionics data to cloud analytics platforms for flight-crew decision support.[1]Collins Aerospace, “InteliSight tablet interface modules,” collinsaerospace.com Predictive-maintenance dashboards now draw directly from onboard sensors, increasing the required processing power of each interface device. Airbus’s company-wide mandate for electronic flight bag usage accelerated global demand for certified gateways connecting legacy aircraft networks to modern apps. Operators also integrate these devices to comply with emerging performance-based navigation rules and real-time flight tracking initiatives.

Expansion of real-time aircraft health-monitoring and predictive-maintenance ecosystems

Edge-based computing capabilities inside modern AIDs filter and compress raw data before transmission to ground servers, reducing bandwidth costs while preserving diagnostic fidelity. Aireon’s space-based ADS-B data stream combines with Boeing’s analytics platform to monitor flight parameters beyond traditional maintenance limits, underscoring the strategic role of interface gateways in fleet-wide health programs. Astronics has responded with Smart Aircraft Interface Devices, integrating server and router functionality, incorporating Federal Information Processing Standards-level encryption to protect sensitive telemetry.

Military ISR platforms require high-speed data exfiltration

Armed forces deploy ever-larger sensor suites on crewed and uncrewed aircraft, producing terabytes of surveillance data per mission. L3Harris networking architectures employ cross-domain solutions to move multi-intelligence feeds over contested links without compromising security. NATO’s adoption of STANAG 4586 for unmanned control drives standard-form-factor AIDs with common middleware, enabling plug-and-play upgrades across diverse airframes.[2]NATO Science and Technology Organization, “STANAG 4586,” nato.int Contract awards for open-system avionics on rotary platforms illustrate sustained defense demand for cyber-hardened gateways.

Adoption of open-architecture avionics standards

The Future Airborne Capability Environment (FACE) Technical Standard now guides procurement policy across multiple Western defense programs, shifting value creation toward software portability. Suppliers like RTI have obtained DO-178C DAL A certification for FACE-conformant messaging layers, demonstrating how open standards can accelerate regulatory approvals. Civil transport OEMs mirror this approach in next-generation cockpits to shorten integration cycles and reduce vendor lock-in.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cybersecurity compliance burden | -1.8% | North America and Europe | Short term (≤ 2 years) |

| Supply-chain volatility in multi-protocol data-bus components | -1.5% | Global, acute in Asia-Pacific | Medium term (2-4 years) |

| Prolonged and expensive certification cycles (DO-178C/254, DO-160G, FAA/EASA STC) | -1.2% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Space-based ADS-B reducing need for on-board data gateways on new-gen aircraft | -0.9% | Global, with early impact on oceanic and remote routes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating cybersecurity compliance burden

DO-326A and DO-356A standards add rigorous design, verification, and penetration-testing steps that can extend certification schedules by over a year. The FAA’s Aircraft Network Security Program requires operators of connected aircraft to document threat models and mitigation strategies before receiving approvals, raising development costs for smaller suppliers. European research consortia such as AIDA are prototyping AI-driven cyber agents to monitor avionics networks in real time, reflecting the rapidly expanding scope of required defensive capabilities.

Supply-chain volatility in multi-protocol data-bus components

Shortfalls in ARINC 664 switches and specialty semiconductors have lengthened lead times to more than 50 weeks for certain part numbers. Aerospace demand represents less than 5% of the global chip market, limiting buyer leverage during allocation cycles. Tier-one suppliers respond with dual-sourcing strategies and vertical integration, yet smaller OEMs face production delays that ripple into airline retrofit schedules. Industry coalitions are drafting traceability frameworks to prevent counterfeit components from entering safety-critical supply chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fit: Retrofit acceleration drives market evolution

Retrofit programs are outpacing new-build deliveries with a 14.12% CAGR through 2031, even though line-fit options still held 49.89% of the aircraft interface device market share in 2025. Airlines view cockpit upgrade packages as a cost-effective alternative to new airframes, particularly for regional and business jets approaching mid-life checks. Collins Aerospace offers Pro Line Fusion conversions that deliver synthetic vision and advanced flight-management functions while satisfying next-generation airspace mandates. Regulatory ADS-B and FANS 1/A requirements further stimulate retrofit demand across every continent.

Line-fit retains scale advantage because OEMs embed gateways during assembly, avoiding additional downtime and ensuring tight integration with other avionics suites. Yet delivery backlogs push operators toward immediate capability gains through retrofit, reinforcing the long-term growth advantage in that channel. The aircraft interface device market size for retrofit solutions is forecast to approach USD 225.6 million by 2031, underscoring how modernization schedules and certification paths shape buyer behavior.

By Connectivity: Wireless revolution transforms interface architecture

Wired networks dominated with 65.22% revenue in 2025, benefitting from deterministic latency and proven electromagnetic compatibility. Nevertheless, wireless AIDs are growing at 16.10% CAGR as airlines adopt multi-orbit satellite and 5G air-to-ground links. Delta’s selection of the Hughes Fusion platform, which can blend low-earth and geostationary bandwidth, illustrates how carriers expect seamless roaming across diverse networks.

Bombardier’s continental 5G roll-out highlights a shift toward terrestrial links for high-density routes. Wireless gateways handle traffic prioritization, encryption, and antenna handovers that used to require multiple discrete boxes. Certification hurdles slow adoption for safety-critical applications, so wired backbones will remain essential inside fly-by-wire and navigation domains. The aircraft interface device market size attached to wireless solutions is projected to expand at double-digit rates through 2031, matching passenger demand for uninterrupted broadband.

By Platform: Software-defined architecture gains momentum

Hardware platforms accounted for 62.40% revenue share in 2025, yet software subscriptions are accelerating at 15.35% CAGR because they allow iterative feature releases. Thales’s FlytEDGE cloud-native platform demonstrates how content and functionality updates can occur during overnight layovers rather than during heavy checks. Software containers also lower the threshold for third-party innovation, aligning with MOSA and FACE principles.

High-bandwidth and deterministic workloads still demand specialized processors with real-time operating systems, ensuring that hardware remains indispensable for mission systems. Leading vendors, therefore, integrate multi-core CPUs and FPGA fabric that permit field-programmable protocol changes. The hybrid model underpins future growth: hardware provides secure compute foundations while software unlocks value through analytics and connected services.

By Aircraft Type: Unmanned systems drive innovation

Commercial airliners held 68.67% of 2025 revenue because of fleet volume, yet unmanned platforms are the fastest-growing category at 17.30% CAGR. NATO’s standardization of UAV command protocols creates unified interface requirements, opening a sizeable window for COTS device suppliers. Small tactical drones, large HALE vehicles, and optionally piloted aircraft each require rugged, low-SWaP interface boards to bridge sensor buses to satellite links.

Crewed business and regional jets drive limited-run retrofit projects, focusing on enhancing situational awareness and optimizing maintenance. Helicopter programs often mandate extreme vibration resistance and secure mission-equipment gateways, sustaining a steady niche. Overall, the aircraft interface device industry benefits from technological cross-pollination between manned and unmanned domains, with security and bandwidth demands rising in parallel.

Geography Analysis

North America led the aircraft interface device market with a 35.96% share in 2025, supported by large fleets, strict FAA connectivity mandates, and robust defense spending. Military modernization contracts such as the UH-60M avionics upgrade sustain high unit volumes and guarantee long-term support revenues. The region’s mature MRO ecosystem accelerates retrofit cycles, while the FAA’s roadmap for next-generation air-traffic management further stimulates demand for certified gateways.

Asia-Pacific registers the strongest growth outlook, with a 13.25% CAGR to 2031. Expanding middle-class travel, rapid low-cost carrier fleet additions, and heightened regional security considerations drive commercial and military aircraft procurement. Recent multi-year modernization programs for Mi-17 rotary fleets showcase how operators across Southeast Asia and India prioritize glass-cockpit conversions that depend on advanced interface devices. National airworthiness authorities in Japan, China, and Australia now recognize standards such as DO-178C, making it easier for suppliers to transfer products across borders.

Europe maintains measured growth through joint defense initiatives and sustainability commitments that rely on granular flight-data analytics. EASA guidance harmonizes certification pathways, enabling coordinated adoption of open-architecture avionics. Corporate consolidation, highlighted by Thales’s acquisition of Cobham Aerospace Communications, enhances local supply resilience and competitive positioning. South America, the Middle East, and Africa remain early-stage yet attractive, especially for retrofit solutions that extend asset life while meeting evolving navigation mandates.

Competitive Landscape

The aircraft interface device (AID) market is moderately consolidated, with a cohort of global avionics majors and a long tail of specialist hardware and software firms. Collins Aerospace (RTX Corporation), Astronics Corporation, Thales Group, and Honeywell International Inc. leverage wide product portfolios, DO-178C/DO-254 certification expertise, and embedded customer relationships to defend premium positions. Mid-tier companies pursue modular open-system designs to win niche programs, especially across unmanned and rotary segments.

Strategic acquisitions widen technology offerings and lock in intellectual property. Honeywell’s agreement to purchase Civitanavi bolsters its inertial navigation and autonomous operations credentials. Likewise, HEICO’s purchase of Rosen Aviation strengthens its cabin systems proposition, integrating in-flight entertainment with data-link gateways. Suppliers also partner on experimental blended-wing demonstrators, confirming a pivot toward distributed flight-control architectures requiring new generations of high-bandwidth, cyber-secure interfaces.

Intellectual-property filings highlight future differentiation. Meta’s patents on WLAN uplink scheduling methods may influence airborne Wi-Fi standards, potentially affecting future device logic layers. Meanwhile, open-standard adherence sets baseline requirements. Companies that achieve full FACE conformance gain privileged access to US defense program shortlists. At the same time, commercial carriers favor suppliers capable of a hybrid wired-wireless gateway design validated under DO-160G and DO-326A.

Aircraft Interface Device Industry Leaders

Astronics Corporation

Collins Aerospace (RTX Corporation)

Teledyne Technologies Incorporated

Honeywell International Inc.

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Curtiss-Wright won a USD 80 million IDIQ contract to supply high-speed data-acquisition systems for US Air Force flight-test programs.

- February 2025: Collins Aerospace rolled out Pro Line 21 upgrades for Cessna Citation business-jet cockpits, including ADS-B In weather display.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the aircraft interface device market as global sales revenue from certified hardware modules that bridge avionics data-buses (ARINC 429, 717, 664 or MIL-STD-1553) with pilot electronic flight bags and airline or military ground networks, covering fixed and rotary-wing fleets. According to Mordor Intelligence, this market is valued at USD 212.8 million in 2025.

Scope exclusion: We do not consider passenger Wi-Fi access points, in-seat entertainment servers, or unrelated cabin connectivity boxes.

Segmentation Overview

- By Fit

- Line Fit

- Retrofit

- By Connectivity

- Wired

- Wireless

- By Platform

- Hardware

- Software

- By Aircraft Type

- Commercial

- Narrowbody Aircraft

- Widebody Aircraft

- Regional Jets

- Military

- Combat

- Non-Combat

- General Aviation

- Business Jets

- Helicopters

- Unmanned Systems

- Commercial

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Israel

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with avionics architects, airline flight-ops managers, connectivity integrators, and MRO engineers across North America, Europe, the Middle East, and Asia-Pacific. These interviews clarified real-world penetration, pricing dispersion, and retrofit timing, allowing us to align model assumptions with operator practice.

Desk Research

We started by gathering fleet and production totals from FAA and EASA aircraft registries, ICAO traffic databases, and IATA World Air Transport Statistics; these sources shaped the initial demand pool. Trade data for avionics gateways were extracted from US ITC customs codes and Volza, while Form 10-K disclosures and investor decks clarified OEM attach rates and average selling prices. Subscriptions such as D&B Hoovers and Dow Jones Factiva helped us benchmark supplier revenue splits and validate price corridors.

A second sweep reviewed regulatory and technology triggers. Questel patent searches exposed innovation velocity in high-speed gateways, FAA airworthiness directives flagged likely retrofit cycles, and RTCA DO-178C approval lists provided certification queue insights. The sources noted are illustrative only; many other open records supported data collection, validation, and gap checks.

Market-Sizing & Forecasting

We built a top-down fleet-based pool from annual deliveries, active tail counts, and typical installation ratios, which was then cross-checked through sampled supplier revenue roll-ups and average selling price × volume estimates. Key variables like EFB adoption, satellite bandwidth costs, retrofit mandates, lead-time shifts, and aircraft retirements feed a multivariate regression that projects value through 2030. Scenario analysis adjusts for certification delays or bandwidth cost shocks, while regional channel checks fill any bottom-up gaps.

Data Validation & Update Cycle

Model outputs undergo automated variance scans, senior analyst logic checks, and peer sign-off. Reports refresh every year, with interim updates triggered by major regulatory or fleet events so clients receive our latest view.

Why Our Aircraft Interface Devices Aid Baseline Commands Reliability

Published estimates often diverge because firms pick different device definitions, currency bases, and refresh cadences; several even fold passenger connectivity boxes into AID totals, whereas we do not.

Key gap drivers include scope creep, optimistic retrofit penetration, list-price revenue calculations, and multi-year refresh cycles versus Mordor's yearly recalibration.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 212.8 million (2025) | Mordor Intelligence | - |

| USD 187.3 million (2024) | Global Consultancy A | Excludes military platforms and applies uniform 9 percent ASP growth |

| USD 160.5 million (2025) | Industry Journal B | Counts only line-fit deliveries, ignores retrofit pool |

| USD 167 million (2024) | Research Publisher C | Uses vendor list prices without currency normalization |

Taken together, the comparison shows that our disciplined scope selection, yearly updates, and dual-track validation offer decision-makers a transparent, reproducible baseline they can trust.

Key Questions Answered in the Report

What is the current value of the aircraft interface device market?

The aircraft interface device market size is USD 238.12 million in 2026.

Which segment is growing fastest within this market?

Unmanned systems lead growth with an 17.30% CAGR through 2031.

Why are retrofit programs so important for market growth?

Retrofit programs let operators modernize older aircraft quickly and cost-effectively, driving a 14.12% CAGR for retrofit AIDs through 2031.

How does cybersecurity regulation affect suppliers?

Compliance with DO-326A and related standards can extend certification by up to 18 months and add roughly 25% to development budgets.

Which region will contribute the most incremental revenue by 2031?

Asia-Pacific is forecast to expand at 13.25% CAGR, making it the largest contributor to new revenue during the forecast period.

Are wireless or wired connectivity solutions expected to dominate?

Wired solutions retain safety-critical applications, yet wireless interface devices will grow faster at 16.10% CAGR thanks to multi-orbit satellite and 5G networks.

Page last updated on: