Aircraft Brakes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.8 Billion |

| Market Size (2031) | USD 12.56 Billion |

| Growth Rate (2026 - 2031) | 5.11% CAGR |

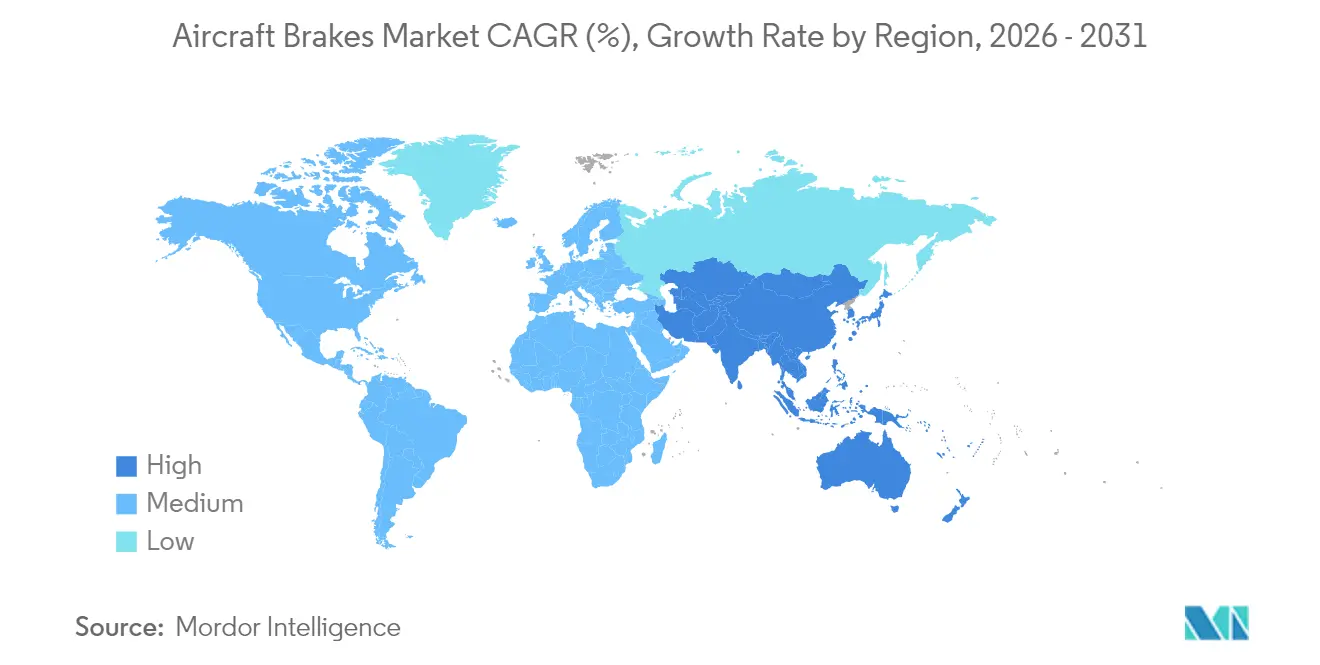

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Brakes Market Analysis by Mordor Intelligence

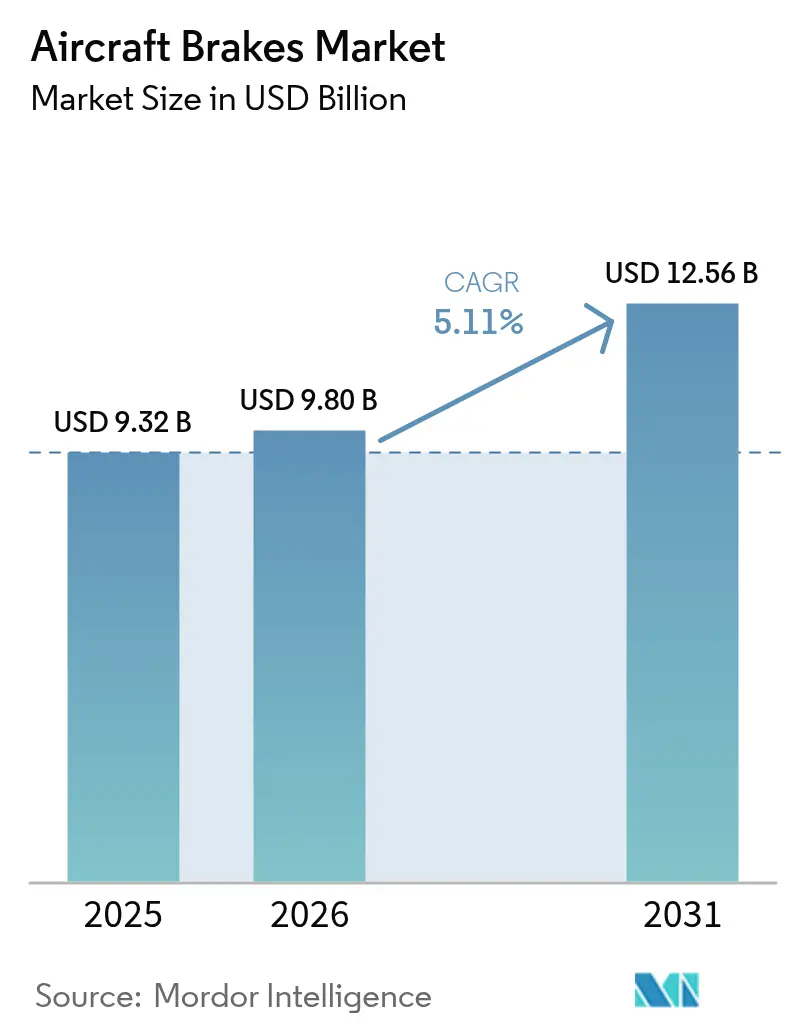

The aircraft brakes market size in 2026 is estimated at USD 9.8 billion, growing from 2025 value of USD 9.32 billion with 2031 projections showing USD 12.56 billion, growing at 5.11% CAGR over 2026-2031. Rising fleet deliveries, steady defense modernization programs, and the industry-wide pivot from steel to advanced carbon braking systems sustain momentum. Commercial airlines are lengthening aircraft retirement cycles, increasing maintenance, repair, and overhaul (MRO) demand; brake-by-wire technology is gaining traction as more electric aircraft architectures enter service. Carbon brakes dominate new installations because they cut weight, curb fuel burn, and last longer than steel alternatives, while breakthrough carbon-ceramic concepts promise even higher thermal tolerance. Regional market dynamics favor North America for installed base revenues, yet Asia-Pacific is expanding the fastest as low-cost carriers add narrowbody jets and regional regulators streamline certification pathways. Supply chain tightness in aerospace-grade carbon fiber and the rigorous certification regime for novel brake materials continue to cap near-term capacity additions. Still, OEM investments in new factories underscore confidence in multiyear demand.

Key Report Takeaways

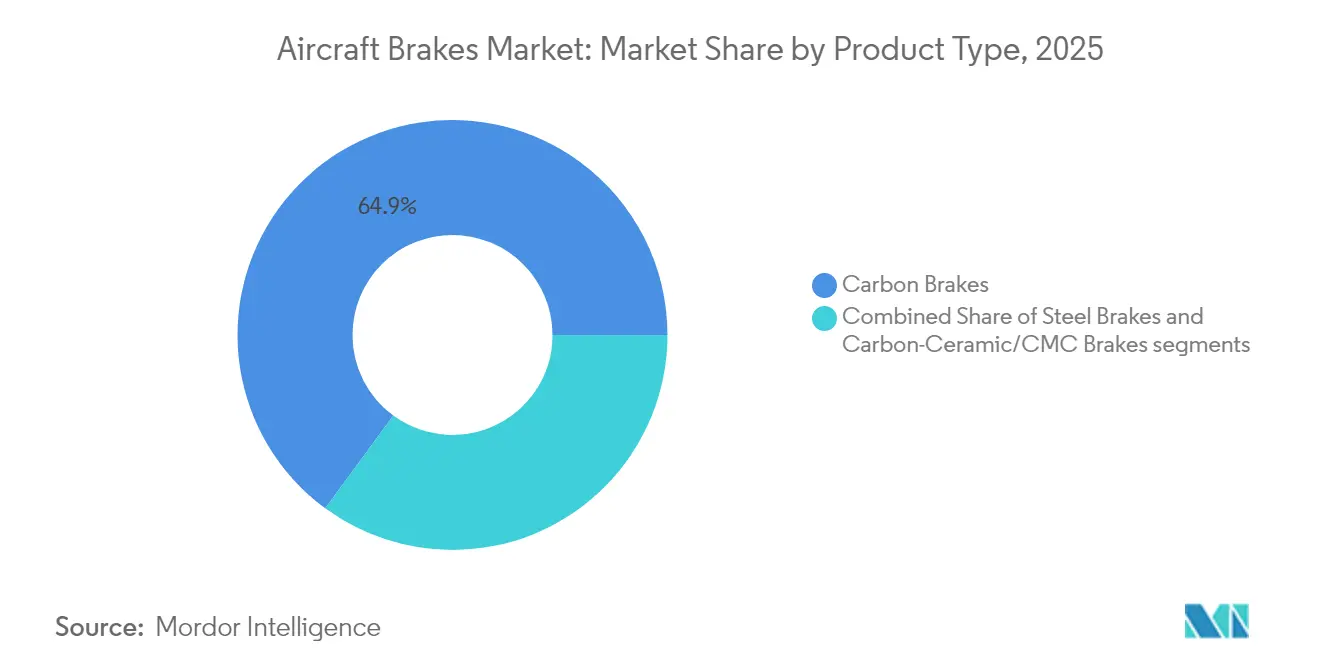

- By product type, carbon brakes led with 64.92% revenue share in 2025; carbon-ceramic/CMC brakes are projected to advance at a 7.55% CAGR to 2031.

- By actuation technology, conventional hydraulic systems held 75.60% share in 2025, whereas fully electric/brake-by-wire solutions are expected to grow at 6.29% CAGR through 2031.

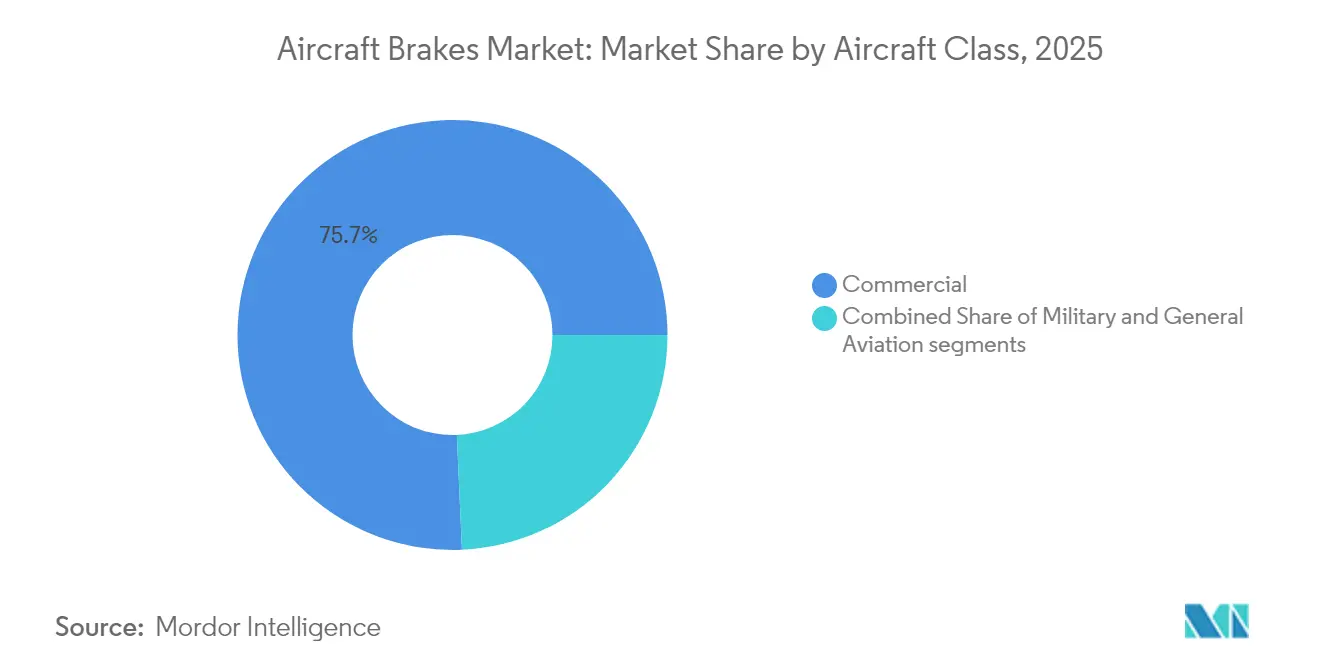

- By aircraft class, commercial held a 75.70% share in 2025, and is expected to grow at a 6.05% CAGR through 2031.

- By end user, linefit installations represented 54.10% of the aircraft brakes market share in 2025; retrofit activity is forecasted to rise at a 5.39% CAGR as operators upgrade aging fleets.

- By geography, North America accounted for 30.60% of the aircraft brakes market in 2025, while Asia-Pacific is poised to register the fastest regional CAGR at 6.72% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Brakes Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of worldwide aircraft fleet and sustained growth in deliveries | +1.8% | Global; strongest in Asia-Pacific and North America | Medium term (2-4 years) |

| Industry transition from steel brakes to advanced carbon braking solutions | +1.2% | North America and Europe, spreading to Asia-Pacific | Long term (≥ 4 years) |

| Global defense fleet modernization programs stimulating brake demand | +0.9% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rising MRO requirements from aging commercial aircraft fleets | +1.1% | North America and Europe | Short term (≤ 2 years) |

| Increasing adoption of brake-by-wire systems in more-electric aircraft architectures | +0.7% | Early uptake in North America and Europe | Long term (≥ 4 years) |

| Wider acceptance of PMA parts in cost-sensitive aviation markets | +0.4% | Strongest in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of worldwide aircraft fleets drives sustained brake demand

Boeing’s 2024 outlook calls for 43,975 new jet deliveries over 2024-2043, and 76% of them are single-aisle models that operate high landing-cycle missions, accelerating brake wear and replacement frequency.[1]Boeing, “Commercial Market Outlook,” boeing.com India’s traffic is expanding more than 7% annually, underpinning a need for 2,835 additional aircraft by 2045, which compounds brake demand in both the original-equipment and aftermarket channels. Aircraft retirements remain below historic norms, extending fleet average age and intensifying MRO cycles, including repetitive brake overhauls. Regulatory oversight by ICAO and national authorities standardizes global brake performance benchmarks, ensuring that every newly delivered or overhauled unit meets identical stopping-distance, thermal-fade, and wear-rate criteria.

Industry transition from steel to carbon braking solutions reshapes market dynamics

Operators value carbon brakes because they trim weight and last longer than steel sets; Collins Aerospace’s DURACARB® discs deliver about 35% extra lifespan on Boeing 737NG aircraft, translating into fewer shop visits and lower fuel burn. Safran’s Equipment & Defense division, which bundles landing and carbon-brake products, posted 17.70% organic revenue growth in 2024, a signal of shifting operator preferences toward premium carbon technology. Meanwhile, Mitsubishi Chemical Group has demonstrated carbon-fiber reinforced ceramic matrix composites (CMCs) capable of withstanding 1,500 °C, paving the way for next-generation brake discs that tolerate extreme heat without a mass penalty. New production capacity, such as Collins Aerospace’s USD 200 million Spokane expansion, will lift global carbon brake output by 50%, helping alleviate backlog pressure.

Global defense fleet modernization programs stimulate brake upgrades

The US Air Force’s F-16 brake control redesign pivots to Crane’s Mark V brake-by-wire architecture, removing single-point failures and elevating stopping-distance reliability. Similarly, the B-52J re-engining and drag-chute retrofit aim to cut landing-roll brake wear, spotlighting how propulsion upgrades trigger brake system redesign. FlightGlobal tallied 52,642 active military aircraft worldwide, and order books for 4,350 new fixed-wing combat platforms will require freshly certified brakes and long-term sustainment. NATO standardization aligns performance and maintenance metrics, creating a homogeneous defense aftermarket that encourages multi-country brake supply contracts.

Rising MRO requirements from aging commercial fleets bolster aftermarket revenue

Deferred retirements and delivery delays compel airlines to stretch legacy airframes, raising annual shop visit counts for wheels and brakes. North American and European MRO facilities report high utilization rates as airlines schedule proactive brake overhauls to mitigate operational disruptions. Line-replaceable overhaul kits centered on carbon stacks command premium pricing, so brake OEMs invest in additional field-stocking locations and digital tracking tools that precisely monitor heat-soak cycles and wear thickness to time part replacement. The Asia-Pacific maintenance market is projected to grow to USD 109 billion by 2043, and brake specialist capabilities are a critical slice of that expansion.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in global carbon fiber supply and rising energy costs | -0.8% | Highest in Asia-Pacific production hubs | Medium term (2-4 years) |

| Lengthy OEM certification processes and retrofit program backlogs | -0.6% | North America and Europe | Medium term (2-4 years) |

| Stricter international regulations on brake particulate emissions | -0.3% | Europe leading, global uptake | Long term (≥ 4 years) |

| Growing OEM vertical integration reducing tier-2 supplier participation | -0.4% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile carbon fiber supply constrains production scaling

Aerospace-grade carbon fiber capacity additions lag demand because qualification cycles stretch several years, and most new lines aim at lower-grade products for wind blades, not aircraft brakes.[2]CompositesWorld, “Carbon fiber’s changing global landscape,” compositesworld.com Heat-treatment furnaces and chemical vapor infiltration used to make carbon-carbon discs consume large amounts of electricity and natural gas; fluctuating utility prices squeeze suppliers’ margins and push brake selling prices upward. Extended lead-times for titanium, specialty stainless, and alloy castings—often 30 weeks or more—delay hub and torque-tube deliveries for brake assembly. Geopolitical shipping disruptions add further risk to trans-Pacific logistics, prompting OEMs to dual-source raw materials or consider in-region production shifts.

Certification bottlenecks delay technology implementation

EASA deferred its runway-overrun system mandate by 18 months because OEMs cited shortages of certified suppliers and lengthy test-data reviews. In August 2024, the FAA introduced System Safety Assessments that require every brake installation to demonstrate elimination of significant latent failures; complying with the new rule can prolong project timelines by a year or more. While a five-nation pact strives for harmonized powered-lift rules, brake suppliers still face duplicate audit burdens under FAA and EASA requirements, adding cost and complexity. For airframers racing to launch eVTOLs, a protracted brake qualification window can jeopardize entry-into-service targets, forcing some to select mature hardware over next-generation options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Carbon brakes anchor premium growth

Carbon technology commanded a 64.92% of the aircraft brakes market share in 2025 due to the strength of weight savings that cut fuel burn and increased payload capacity. Steel sets retain a niche in light aircraft and cost-constrained operators, yet carriers are quantifying whole-life savings and switching fleets to carbon at the next overhaul cycle. Carbon-ceramic/CMC variants are the fastest-growing sub-category at a 7.55% CAGR, driven by their 1,500 °C heat-resilience and outstanding fade resistance, critical for repeated short-haul missions.

Manufacturing investments mirror this shift. Collins Aerospace doubled Spokane output with a USD 200 million expansion, and Safran is building a new carbon brake plant in France to shore up European capacity. Certification protocols under FAA Part 25 require brake discs to withstand nine-stop rejected-takeoff tests without structural degradation, and carbon stacks routinely outperform steel in this regime. Environmental regulations favor carbon because it eliminates cadmium plating and reduces particulate emissions versus steel-based linings.

By Actuation Technology: Hydraulic dominance confronts an electric future

Traditional hydraulics represent 75.60% of the aircraft brakes market size, prized for proven reliability and global MRO familiarity. Electro-hydraulic hybrids add electronic precision while leveraging existing pumps and reservoirs, serving as a bridge technology for new-builds that still share line architecture with legacy fleets. Fully electric systems, or brake-by-wire, are accelerating at a 6.29% CAGR to 2031 as OEMs pursue all-electric secondary power architectures; Safran’s 787 unit sets the precedent, pairing smart-sensor wear gauging with cockpit annunciations.

Military programs expedite adoption: Crane’s Mark V architecture on the F-16 offers dual redundant signal paths that comply with MIL-HDBK-516C airworthiness criteria. Electric brakes reduce hydraulic fluid mass and eliminate thermal soak-back issues that raise wheel-well temperatures in composite fuselages. As battery-electric regional aircraft and eVTOL prototypes mature, lightweight distributed brake actuators with regenerative capabilities are emerging design baselines in preliminary certification packages.

By Aircraft Class: Commercial aviation underpins volume, defense accelerates technology

Commercial operators generated 75.70% of 2025 demand, led by narrowbody programs such as B737 and A320 lines that account for most annual landings. Widebodies contribute higher unit revenue per set due to larger disc diameters and more complex antiskid control valves. Regional jets and turboprops are converting to carbon brakes as airlines chase lower turnaround times and simplified stocking.

Defense fleets, although smaller in volume, drive frontier technology; the US Air Force (USAF) funds brake-by-wire retrofits, and NATO fleets align specification sheets to streamline coalition logistics. General aviation—including business jets—demands high-energy-absorption discs rated for steep-approach landing fields, a design requirement that increasingly tilts toward carbon. Rotorcraft applies mandatory rotor brakes under 14 CFR 27.921, a regulation that ensures safe rotor stoppage before ground personnel approach.

By End User: Line-fit secures early revenue, retrofit extends lifecycle value

Linefit contracts supplied 54.10% of the aircraft brakes market in 2025, embedding OEM hardware for decades of follow-on spares. Negotiated alongside airframe purchase agreements, these deals lock in brake specifications and often bundle maintenance packages that guarantee predictable cost per landing over a set horizon.

Retrofit demand grows at 5.39% CAGR through 2031 as carriers seek fuel savings and lower maintenance burden by replacing steel stacks with carbon during heavy checks; Copa Airlines’ B737NG upgrade to Collins carbon brakes is a recent reference. PMA alternatives intensify competition, letting operators mix OEM and non-OEM parts within the same assembly under approved engineering orders. Military life-extension programs recapitalize existing fleets rather than buy new airframes, elevating retrofit scope for brake control computers and high-temperature discs.

Geography Analysis

North America has the largest aircraft brakes market share, at 30.60%, because it combines the world’s biggest military inventory with the densest commercial traffic flows and a mature MRO network. US-based suppliers benefit from Buy-American preferences and a robust defense budget that accelerates brake modernization cycles on legacy platforms.

Asia-Pacific registers the steepest growth at 6.72% CAGR owing to prolific fleet additions and regulatory streamlining that shortens certification lead-times for new component entrants. Domestic production incentives in China and India foster local assembly of wheels-and-brake subcomponents, reducing import dependency and creating strategic partnerships with global OEMs. Europe remains pivotal through Airbus output and stringent environmental directives that steer early adoption of low-emission brake materials. The Middle East and Africa are growing from a small base as Gulf carriers upgrade fleets and African nations add connectivity under the Single African Air Transport Market protocols.

Competitive Landscape

Five integrated groups—Safran, Collins Aerospace, Honeywell International Inc., Crane Aerospace & Electronics, and Meggitt PLC—collectively command a majority share, underpinned by technology portfolios, established FAA/EASA approvals, and dense global service networks. Safran’s planned French carbon-brake plant and its USD 1.8 billion actuation acquisition underscore a strategy of deep vertical integration from design to aftermarket. Collins Aerospace is countering through capacity expansions and pioneering environmentally friendly carbon-stack chemistries that remove heavy metals.

Tier-2 suppliers face squeezed line-fit prospects but are carving niches in PMA and regional-aircraft programs. Rapco Fleet Support scaled carbon PMA offerings, while C&L Aero bundled PMA discs into Saab 340 overhauls, highlighting an aftermarket pivot. Digital twin initiatives are another battleground; proprietary algorithms predict heat-soak cycles and disc wear, letting airlines defer changes without safety compromise, a service differentiator that OEMs monetize through subscription models.

Electric-brake ecosystems attract new entrants from power electronics and software backgrounds. Start-ups collaborating with eVTOL OEMs are formulating lightweight electromechanical actuators rated for thousands of high-frequency landings. However, steep certification costs and protracted development timelines favor incumbents with existing DER staff and DER-approved test rigs, slowing disruptive threats.

Aircraft Brakes Industry Leaders

Honeywell International Inc.

Meggitt Ltd. (Parker-Hannifin Corporation)

Crane Aerospace & Electronics (Crane Company)

Collins Aerospace (RTX Corporation)

Safran SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Spirit Airlines and Safran Landing Systems renewed their agreement to supply and provide MRO services to wheels and carbon brakes for Spirit's Airbus A320 fleet.

- March 2023: AllClear Aerospace & Defense signed an exclusive distribution agreement with Aircraft Wheel and Brake LLC, a Kaman company, for wheels, brakes, and associated components supporting KT-1 and KT-100 platforms in specific international regions.

Global Aircraft Brakes Market Report Scope

Aircraft braking systems are used to slow down or stop aircraft movement. Aircraft brakes are disc brakes that operate hydraulically or pneumatically. There are different types of aircraft braking systems which include single-disc, double-disc, multi-disc, and rotor disc brakes. The aircraft brakes market includes the brakes used in military, commercial, and general aviation aircraft. The market study also includes brake components and brake support systems, like anti-skid brakes.

The aircraft brakes market is segmented based on type, end-user, and geography. By type, the market is segmented into electric brakes, carbon brakes, and steel brakes. By end user, the market is segmented into commercial, military, and general aviation. The report also covers the market sizes and forecasts for the aircraft brakes market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Carbon Brakes |

| Steel Brakes |

| Carbon-Ceramic/CMC Brakes |

| Conventional Hydraulic |

| Electro-Hydraulic |

| Fully Electric/Brake-by-Wire |

| Integrated Self-Powered Systems |

| Commercial | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military | Combat |

| Transport | |

| Special Mission | |

| Military Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters |

| Linefit |

| Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middile East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Product Type | Carbon Brakes | ||

| Steel Brakes | |||

| Carbon-Ceramic/CMC Brakes | |||

| By Actuation Technology | Conventional Hydraulic | ||

| Electro-Hydraulic | |||

| Fully Electric/Brake-by-Wire | |||

| Integrated Self-Powered Systems | |||

| By Aircraft Class | Commercial | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military | Combat | ||

| Transport | |||

| Special Mission | |||

| Military Helicopters | |||

| General Aviation | Business Jets | ||

| Commercial Helicopters | |||

| By End User | Linefit | ||

| Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middile East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the aircraft brakes market?

The aircraft brakes market was valued at USD 9.8 billion in 2026 and is projected to reach USD 12.56 billion by 2031, progressing at a 5.11% CAGR.

Which brake material dominates commercial fleets today?

Carbon brakes lead with 64.92% share owing to weight savings and extended service life.

Why are brake-by-wire systems gaining attention?

They fit more-electric aircraft architectures, cut hydraulic complexity, and enable real-time health monitoring.

Which region is expanding the fastest?

Asia-Pacific is forecasted to grow at a 6.72% CAGR through 2031 on the back of large narrowbody orders.

How do PMA parts affect brake procurement?

PMA-approved discs and linings give operators certified, lower-cost alternatives to OEM components.

Page last updated on: