Aircraft Braking Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 7.47 Billion |

| Market Size (2031) | USD 9.13 Billion |

| Growth Rate (2026 - 2031) | 4.07% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

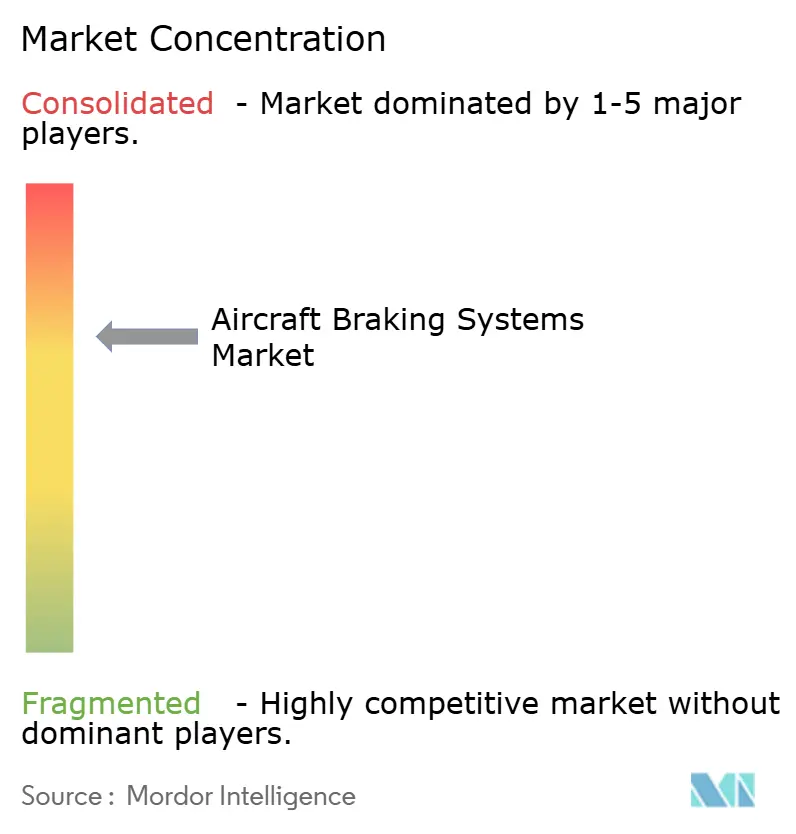

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Braking Systems Market Analysis by Mordor Intelligence

The aircraft braking systems market size is expected to grow from USD 7.19 billion in 2025 to USD 7.47 billion in 2026 and is forecast to reach USD 9.13 billion by 2031 at 4.07% CAGR over 2026-2031. Production gains in single-aisle programs are feeding directly into brake-set demand because both Boeing and Airbus continue to push narrowbody output higher, thereby raising factory-fit and future replacement volumes. Carbon brake adoption continues to strengthen as airlines increasingly weigh fuel use, fleet utilization, and overhaul intervals when choosing braking hardware, and suppliers respond with longer-life products for high-cycle fleets. Electric and hybrid brake architectures are also moving closer to mainstream specification on new aircraft programs as OEMs reduce hydraulic complexity and tie braking performance more closely to digital control systems. Asia-Pacific adds another layer of demand because traffic growth remained strong in 2025 and regional load factors reached record levels in March 2026, which keeps both new deliveries and brake overhaul cycles active.[1]Safran, “Airbus A320ceo/neo Long Life Carbon Brake,” Safran, safran-group.com Competition is still concentrated in carbon brakes for mainline commercial aircraft, but newer categories such as UAVs and eVTOL platforms leave more room for smaller specialists and technology entrants.

Key Report Takeaways

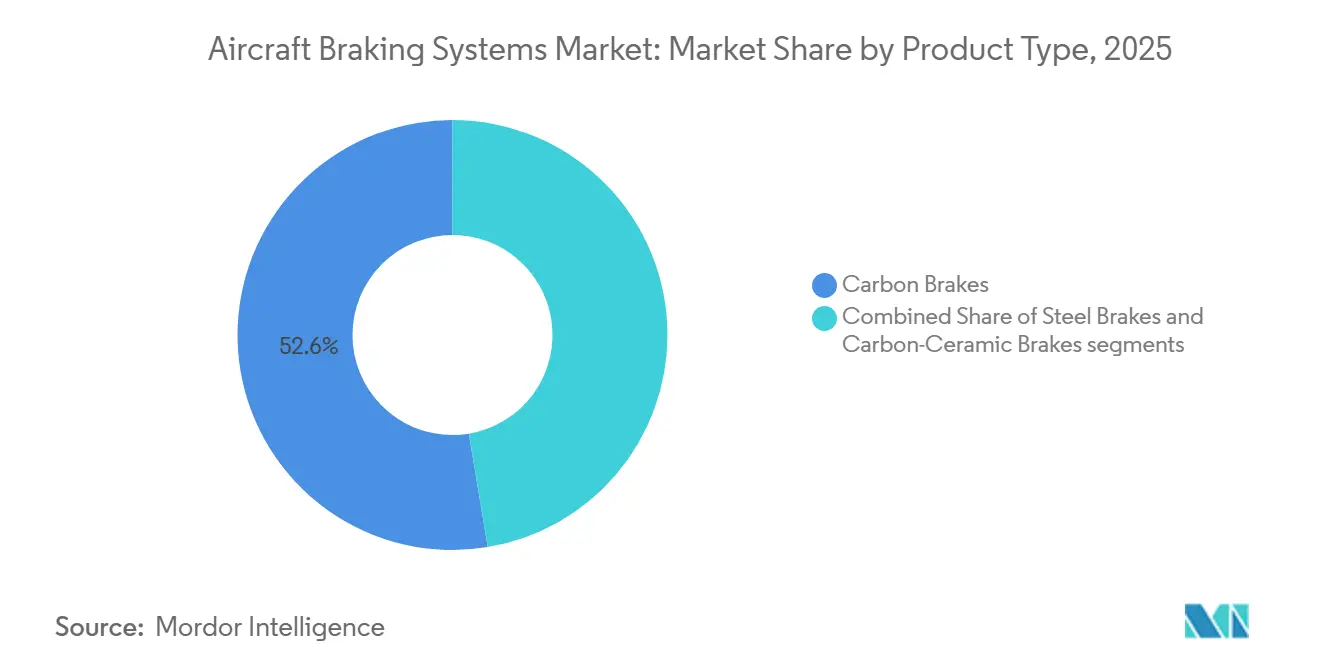

- By product type, carbon brakes led with 52.62% of revenue in 2025, while carbon-ceramic brakes are forecast to grow with a 7.29% CAGR through 2031.

- By actuation method, hydraulic systems accounted for 72.69% of revenue in 2025, while fully-electric braking systems are forecast to expand at a 8.29% CAGR through 2031.

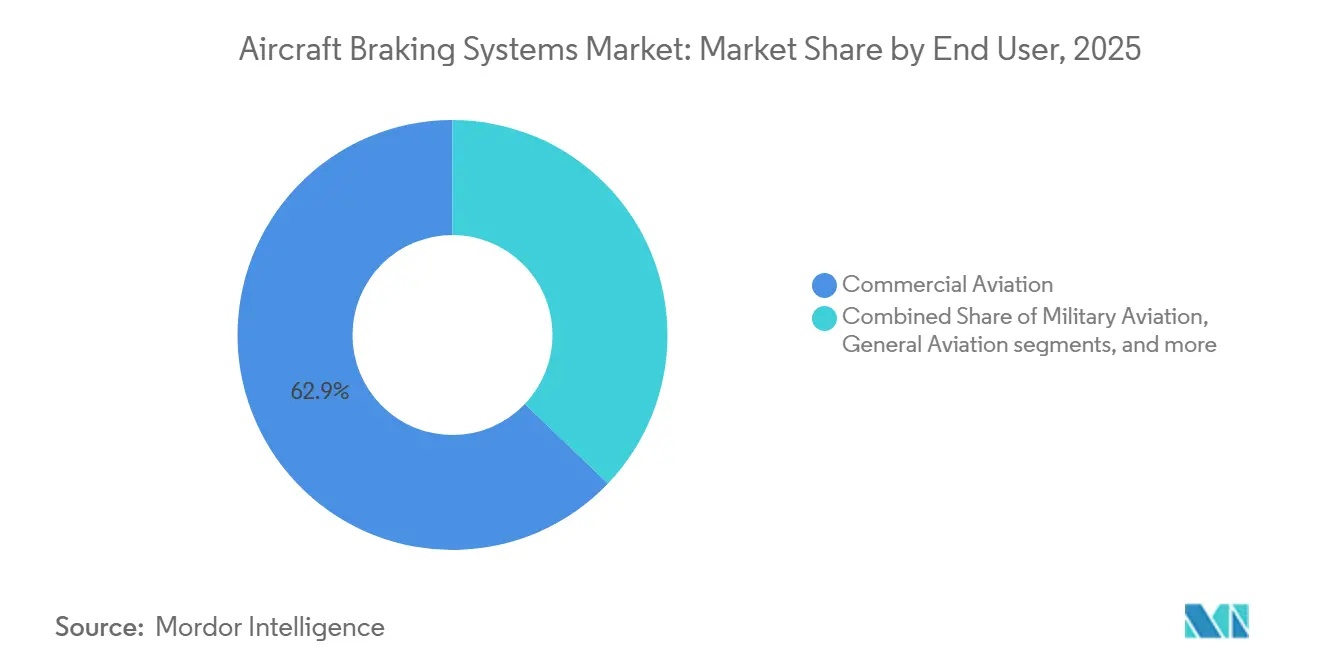

- By end user, commercial aviation accounted for 62.87% of revenue in 2025, while eVTOL/Urban Air Mobility is forecast to grow at a 9.98% CAGR through 2031.

- By component, brake discs accounted for 50.37% of revenue in 2025, while valves are forecast to advance at a 6.41% CAGR through 2031.

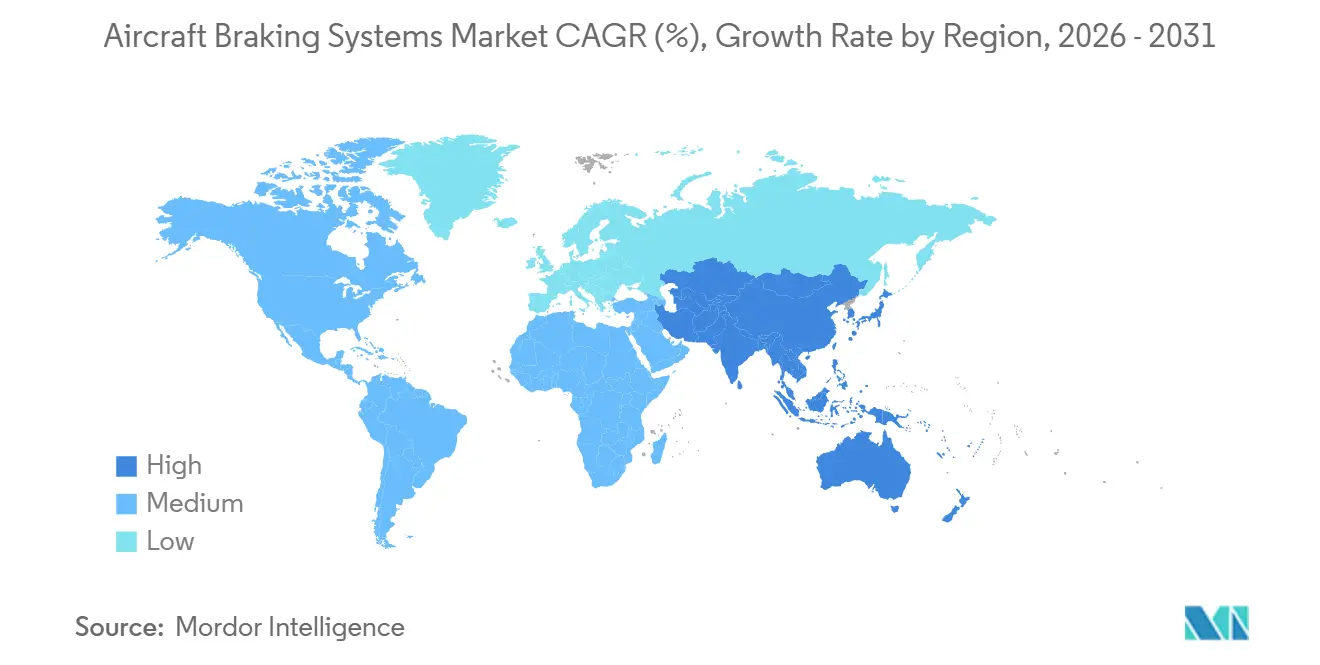

- By geography, North America accounted for 36.89% of revenue in 2025, while Asia-Pacific is forecast to record the highest regional CAGR of 5.84% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aircraft Braking Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising production of single-aisle aircraft | +1.2% | Global, with the strongest effect in North America and Europe, and spillover demand in Asia-Pacific MRO | Short term (≤ 2 years) |

| Mandatory shift to carbon brakes for fuel and weight savings | +0.9% | Global, with concentrated effect in Asia-Pacific and the Middle East due to high-cycle narrowbody use | Medium term (2-4 years) |

| Surge in eVTOL and Urban Air Mobility programs | +0.6% | North America, Europe, and the Middle East | Medium term (2-4 years) |

| Passenger traffic growth in emerging economies | +0.5% | Asia-Pacific core, with spillover to Latin America and Africa | Short term (≤ 2 years) to Medium term (2-4 years) |

| Defense carrier aircraft upgrade cycles | +0.3% | North America and Europe | Long term (≥ 4 years) |

| Predictive maintenance adoption for landing gear | +0.4% | Global, with early concentration in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Production of Single-Aisle Aircraft

The aircraft braking systems market is responding directly to the narrowbody production cycle, as each additional single-aisle delivery increases both immediate brake demand and the future overhaul base. Boeing delivered 447 B737 MAX aircraft in 2025, up from 260 in 2024, and it targeted a production rate of 47 aircraft per month by summer 2026 with plans to move toward 53 by year's end against a backlog of more than 4,800 orders. Airbus delivered 607 A320-family aircraft in 2025 and continued to target 75 aircraft per month by 2027. Those schedules lift annual brake-set requirements faster than new qualified furnace and finishing capacity can be added, because carbon-brake production plants take years to commission and certify. The aircraft braking systems market, therefore, continues to favor incumbents that already have qualified production footprints, OEM approvals, and established airline support networks.

Mandatory Shift to Carbon Brakes for Fuel and Weight Savings

The aircraft braking systems market is gaining support from airline fleet policies that now treat brake weight, maintenance intervals, and emissions goals as linked decisions rather than separate procurement items. Carbon brakes remain attractive because they improve operating economics over time through lower weight and longer service life when compared with steel alternatives. Safran states that its SepCarb IV Long Life carbon brake for the A320neo reaches 2,500 landings between overhauls, reducing downtime and spare parts inventory for airlines running dense short-haul schedules.[2]Safran, “Airbus A320ceo/neo Long Life Carbon Brake,” Safran, safran-group.com That performance supports retrofit demand on in-service narrowbody fleets and creates a demand stream that does not depend only on new aircraft deliveries. The aircraft braking systems market is therefore being strengthened by both factory-fit positions and aftermarket replacement programs that reward suppliers with broad OEM and MRO reach.

Surge in eVTOL/Urban Air Mobility Programs

The aircraft braking systems market is opening a structurally new demand pool as eVTOL/Urban Air Mobility programs move deeper into certification and pre-service preparation. Joby Aviation began power-on testing of its first FAA-conforming aircraft for Type Inspection Authorization in November 2025, and Dubai service launch plans were tied to 2026 timelines.[3]Grace Stubbins, “Joby eVTOL Moves Toward Final Stages of Certification, Builds Global AAM Framework,” CompositesWorld, compositesworld.com Archer Aviation had already received final FAA airworthiness criteria for its Midnight aircraft in 2024, which cleared the way for for-credit flight testing. EASA also advanced the regulatory framework in April 2026 with Certification Memorandum CM-21.A-P-002 under the SC-VTOL framework, while Embraer’s 2025 patent filing showed continued work on compact hybrid hydraulic-electric brake control layouts for novel aircraft packaging needs. The aircraft braking systems market will likely benefit from this category, as brake requirements differ materially from those of fixed-wing designs, forcing suppliers to rethink mass, friction surfaces, control logic, and packaging.

Predictive-Maintenance Adoption for Landing Gear

The aircraft braking systems market is also being shaped by predictive maintenance, as improved brake wear visibility can increase aircraft availability and alter service contract design. Safran Landing Systems uses digital twins and machine-learning wear models, while Boeing’s AnalytX platform applies flight and sensor data to forecast brake disc replacement intervals across fleets. The E-LISA project, documented in a 2025 SAE paper, developed an iron-bird test facility to validate electrically actuated landing gear and brake systems across normal, degraded, and failure conditions.[4]Andrea De Martin, Antonio Bertolino, and Giovanni Jacazio, “A New Test Rig for Electrically Actuated Landing Gear and Brake of a Small Transport Aircraft,” SAE Technical Paper 2025-01-0161, doi.org These tools reduce unplanned removals and help suppliers shift more aftermarket business toward performance-based service contracts. The aircraft braking systems market is therefore moving beyond hardware replacement alone and toward service models that tie brake health data to contract value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of carbon-composite materials | -0.5% | Global, with the strongest effect in OEM supply chains in North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Lengthy certification cycles for new brake technology | -0.4% | Global, with the strongest effect on eVTOL and electric-brake programs in North America and Europe | Medium term (2-4 years) to Long term (≥ 4 years) |

| Supply-chain fragility in niche friction materials | -0.3% | Global, with particular effect on Asia-Pacific MRO networks | Short term (≤ 2 years) to Medium term (2-4 years) |

| Additive-manufactured substitutes eroding aftermarket | -0.2% | North America and Europe | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Carbon-Composite Materials

The aircraft braking systems market remains exposed to raw-material cost swings because carbon-carbon brake production depends on specialized precursor and processing inputs that are difficult to replace quickly. Suppliers face the most pressure when fixed-price agreements with OEMs and airlines do not align with input costs. Capacity decisions are also affected because large new facilities require multi-year confidence in material economics before investment is approved. Safran’s planned fourth carbon-brake plant near Lyon carries an investment value of EUR 450 million (USD 523.90 million), underscoring how expensive it is to add qualified output in this segment. The aircraft braking systems market can therefore see short-term margin pressure and slower capacity additions when carbon-composite cost visibility remains weak.

Lengthy Certification Cycles for New Brake Tech

The aircraft braking systems market still faces long qualification timelines because braking remains a safety-critical landing system with little tolerance for incomplete validation. Safran’s electric brake system on the B787 remains a strong reference point for how deeply certification and reliability requirements can be, even after the technology concept has been proven. The challenge is greater for eVTOL and other new aircraft categories because authorities have less precedent data on brake thermal loads, control logic, and failure behavior in these platforms. A 2024 PHMS Society paper described electromechanical brake systems for new aircraft categories as relatively unproven and more complex than hydraulic solutions, which increases the need for dedicated validation rigs and health-monitoring evidence. The aircraft braking systems market will likely see slower adoption of new actuation methods wherever certification campaigns extend well beyond technology development milestones.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Carbon-Ceramic Innovation Pressures the Incumbent Carbon Duopoly

Carbon brakes held 52.62% of the aircraft braking systems market in 2025, maintaining their lead across product categories. Safran stated in 2025 that it equips over 70% of the global A320 family fleet, or around 5,100 aircraft, while Collins said its DURACARB technology is installed across more than 30,000 commercial and military aircraft. That installed base keeps replacement, overhaul, and support demand centered on carbon systems across large airline fleets. Steel brakes still retain a role in general aviation, regional turboprops, and selected military platforms where upfront acquisition cost remains a stronger buying factor than lifetime economics.

Carbon-ceramic brakes are the fastest-growing product category in the aircraft braking systems market because newer aircraft classes and selected defense applications value low mass and stable friction behavior. Wet-runway performance and thermal consistency continue to support interest in this material set, despite wide variations in mission intensity. The E-LISA program is also examining carbon-based brake materials for next-generation electrically actuated landing gear and braking systems, thereby keeping development aligned with broader electrification efforts. The aircraft braking systems market, therefore, remains anchored in conventional carbon products today, but the product roadmap is clearly widening as emerging platforms push different weight, packaging, and operating requirements.

By Actuation Method: Electrification Accelerates as the More Electric Aircraft Concept Matures

Hydraulic systems accounted for 72.69% of actuation revenue in 2025, reflecting the installed-base reality of the global fleet. The aircraft braking systems market, therefore, continues to rely on hydraulic support across current fleets even as new program architecture moves in a different direction. Fully-electric braking systems are projected to grow at an 8.29% CAGR between 2026 and 2031, the fastest pace among actuation methods in the aircraft braking systems market. Parker Aerospace states that its Ebrake system on the A220 can decelerate an aircraft weighing more than 60 tons at speeds above 200 mph within 3,280 feet while handling temperatures up to 2,000°C.

Electro-hydraulic systems sit in the middle of that transition because they allow OEMs to lower hydraulic dependence without requiring a complete redesign of aircraft systems, making them a practical option for programs that want some electrification benefits but still prefer familiar backup logic and maintenance practices. Liebherr Aerospace’s role in the Clean Sky 2 More Electric Wing project shows that high-power motor controllers and thermal management modules remain active areas of development for electric landing gear systems. The aircraft braking systems market is therefore likely to move through layered and hybrid architectures before fully-electric layouts become dominant across a wider range of aircraft classes.

By End User: eVTOL Structural Expansion Reshapes Brake Material Requirements

Commercial aviation held 62.87% of the aircraft braking systems market share in 2025, making it the largest end-user group. That position reflects fleet renewal activity, large installed narrowbody fleets, and recurring overhaul cycles on aircraft that remain in intensive service. Military demand also stays meaningful, supported by a USD 62.20 million contract modification for C-130 brake heat sinks and by AllClear’s May 2026 expansion of inventory investment in Honeywell Carbenix braking systems for F-15 and F-18 fleets. The aircraft braking systems market also keeps a steady, smaller-volume base in general aviation and UAV platforms, where proprietary designs and fragmented supplier positions shape replacement activity.

The eVTOL/Urban Air Mobility segment is projected to grow at a 9.98% CAGR through 2031, making it the fastest-growing end-user category in the aircraft braking systems market. Joby’s planned Dubai launch and Saudi Arabia’s memorandum with Joby to use FAA type-certification standards as the basis for Saudi approval both indicate that early commercial deployment will not be confined to the United States. These aircraft require brake systems designed for lower stop loads, tighter packaging, and different friction and control behavior compared to fixed-wing platforms. The aircraft braking systems market is therefore developing a parallel path in materials and hybrid control layouts rather than applying large-aircraft braking assumptions to a new category.

By Component: Valve Architecture Complexity Underpins MRO and OEM Revenue Growth

Brake discs accounted for 50.37% of the aircraft braking systems market size in 2025, giving them the largest revenue share among components. Their lead comes from high unit value and recurring replacement cycles, with Safran and CompositesWorld noting overhaul intervals of 2,000 to 2,500 landings for commercial carbon discs, depending on application. Valves are forecast to expand at a 6.41% CAGR between 2026 and 2031, the fastest growth rate among components in the aircraft braking systems market. The aircraft braking systems market is adding more pressure modulation, isolation, and emergency control hardware as electro-hydraulic and electric architectures become more complex.

Embraer’s 2025 hybrid hydraulic-electric brake patent specifically included dual-channel pressure transducers and normally closed solenoid valves for parking brake leak management, illustrating how valve density can increase as architecture evolves. That detail matters because component values can shift even when the aircraft platform itself is smaller than that of a conventional transport aircraft. Electronics and wheels continue to provide stable aftermarket revenue, while accumulators and brake housing remain more mature replacement-driven categories with slower innovation cycles. The aircraft braking systems market is therefore likely to create more incremental value in control hardware and supporting electronics than in mature structural elements alone.

Geography Analysis

North America accounted for 36.89% of the aircraft braking systems market share in 2025, making it the leading regional contributor. That position rests on the concentration of major OEM delivery programs, a large defense procurement base, and a dense MRO network serving the world's largest commercial fleet. Boeing delivered 447 B737 MAX aircraft in 2025 and aimed to reach a rate of 53 aircraft per month by the end of 2026, keeping brake-set demand concentrated in the regional supply chain. Safran's Walton, Kentucky, site produces more than 9,500 wheel and brake sets per year, while Collins expanded carbon-brake capacity in Spokane to support both commercial and military demand. The aircraft braking systems market in North America also benefits from advanced eVTOL certification activity, as Joby and Archer remain closely tied to FAA-led approval pathways.

Asia-Pacific is projected to grow at a 5.84% CAGR through 2031, making it the fastest-growing regional segment in the aircraft braking systems market. Higher aircraft utilization in that environment raises brake wear and accelerates overhaul demand even before new deliveries are counted. China is also expanding local capability through C919 brake-disc localization and through AVIC Xi'an Aviation Braking's maintenance cooperation across Boeing, Airbus, and Bombardier platforms, which adds a competitive manufacturing dimension to regional demand.

Europe held a significant share in 2025, supported by Airbus's delivery activity and Safran's French manufacturing base in aircraft braking systems. Brazil recorded 10.8% domestic RPK growth in March 2026, suggesting incremental narrowbody demand in South America, even though the region still relies heavily on imported brake components. Africa posted 20.6% RPK growth in March 2026 and remains small in fleet size, but rising intra-continental traffic still supports a longer-term MRO opportunity. The Middle East saw a 58.6% drop in RPK in March 2026 due to airspace disruptions. Yet, Saudi Arabia's aviation expansion and Riyadh Air's planned B787-9 fleet with Safran electric carbon brakes preserve medium-term demand.

Competitive Landscape

The aircraft braking systems market remains semi-consolidated in large commercial and military programs, where Safran SA, Collins Aerospace (RTX Corporation), and Honeywell International Inc. hold the strongest positions. Safran states that it equips more than 55% of commercial airliners with more than 100 seats and around 800 B787 aircraft with its electric carbon-brake system. Collins says its DURACARB technology is certified on more than 30,000 aircraft. Parker Aerospace also holds a visible position in electric braking through the Ebrake system on the A220. Concentration is strongest in mainline carbon brakes and clearly lower in general aviation, UAV, and eVTOL applications.

Capacity expansion is one of the clearest competitive tools in the aircraft braking systems market. Safran committed EUR 450 million (USD 523.90 million) to a fourth carbon-brake plant near Lyo. At the same time,e Collins broke ground on a USD 200 million expansion in Spokane to increase output for commercial and military programs. Long-term supply and service agreements reinforce that strategy, as shown by Safran’s renewed Spirit Airlines MRO deal in April 2025 and its November 2025 agreement to supply Riyadh Air’s future B787-9 fleet. These moves make scale, installed-base access, and service reach harder for smaller rivals to match.

The aircraft braking systems market is also shifting toward software-linked service models as suppliers combine hardware with diagnostics. Safran uses digital-twin brake-wear monitoring, and Boeing’s AnalytX platform forecasts replacement intervals, which support performance-based contracts and stronger aftermarket retention. Honeywell strengthened its military braking position in May 2026 when AllClear expanded inventory support for Carbenix systems across F-15 and F-18 fleets in more than 60 countries. The aircraft braking systems market still leaves open design space in eVTOL and UAV programs, where lower legacy lock-in gives smaller specialists a better chance to win positions than in the mainline commercial airliner segment.

Aircraft Braking Systems Industry Leaders

Safran SA

Honeywell International Inc.

Collins Aerospace (RTX Corporation)

Crane Aerospace & Electronics (Crane Co.)

Parker-Hannifin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: AllClear Aerospace & Defense (AllClear) announced an enhanced investment in Honeywell Aerospace’s wheels and brakes product line, underscoring its commitment to delivering reliable, mission-ready supplies to military operators amid ongoing global supply chain challenges.

- November 2025: Safran Landing Systems finalized a long-term agreement with Riyadh Air to deliver wheels and advanced electric carbon brakes for the airline's upcoming fleet of over 70 B787-9 aircraft. The agreement emphasizes the operational advantages of electric carbon brakes, particularly their suitability for high-altitude operations at King Khaled International Airport.

- July 2024: TT Electronics, a global leader in manufacturing solutions and engineered technologies, secured a significant contract with Parker at its Cleveland, Ohio, facility. This multi-million-pound deal, set to run through 2027, centers on the production of intricate electronic assemblies for commercial aircraft braking systems, reinforcing the enduring partnership between TT Electronics and Parker.

- January 2024: Crane Aerospace & Electronics secured a pivotal role as a supplier to Deutsche Aircraft for its D328eco regional turboprop. The eco-conscious aircraft will be outfitted with Crane A&E's advanced Mark V brake-by-wire control system.

Global Aircraft Braking Systems Market Report Scope

The aircraft braking systems market is experiencing steady growth, driven by rising aircraft production, increasing demand for lightweight, fuel-efficient braking technologies, and the growing adoption of electric brake-by-wire systems in modern aircraft. These systems are essential for ensuring safe landing, taxiing, and ground operations across commercial, military, and general aviation platforms. Additional factors contributing to market growth include advancements in carbon and carbon-ceramic brake materials, fleet modernization programs, and the emergence of eVTOL and urban air mobility platforms.

The aircraft braking systems market is segmented based on product type, actuation method, end user, component, and geography. By product type, the market is divided into carbon brakes, steel brakes, and carbon-ceramic brakes. Based on the actuation method, the market comprises hydraulic, electro-hydraulic, and fully electric braking systems. The end-user segment comprises commercial aviation, military aviation, general aviation, unmanned aerial vehicles (UAVs), and eVTOL/urban air mobility platforms. By component, the market encompasses wheels, brake discs, brake housing, valves, actuators, accumulators, and electronics. The report also covers market sizes and forecasts for the aircraft braking systems market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Carbon Brakes |

| Steel Brakes |

| Carbon-Ceramic Brakes |

| Hydraulic |

| Electro-Hydraulic |

| Fully-Electric |

| Commercial Aviation |

| Military Aviation |

| General Aviation |

| Unmanned Aerial Vehicles (UAVs) |

| eVTOL/Urban Air Mobility |

| Wheels |

| Brake Discs |

| Brake Housing |

| Valves |

| Actuators |

| Accumulators |

| Electronics |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Product Type | Carbon Brakes | ||

| Steel Brakes | |||

| Carbon-Ceramic Brakes | |||

| By Actuation Method | Hydraulic | ||

| Electro-Hydraulic | |||

| Fully-Electric | |||

| By End User | Commercial Aviation | ||

| Military Aviation | |||

| General Aviation | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| eVTOL/Urban Air Mobility | |||

| By Component | Wheels | ||

| Brake Discs | |||

| Brake Housing | |||

| Valves | |||

| Actuators | |||

| Accumulators | |||

| Electronics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the forecast for aircraft braking systems through 2031?

The aircraft braking systems market is projected to rise from USD 7.47 billion in 2026 to USD 9.13 billion by 2031 at a 4.07% CAGR.

Which actuation method is growing the fastest?

Fully electric braking systems are forecast to expand at an 8.29% CAGR through 2031 as aircraft architectures reduce hydraulic dependence.

Why are carbon brakes still leading adoption?

Carbon brakes led product revenue with 52.62% in 2025 and remain favored for lifetime operating economics and longer overhaul intervals, with Safran citing up to 2,500 landings between overhauls on its A320neo long-life brake.

Which region is expanding the fastest?

Asia-Pacific is projected to grow at a 5.84% CAGR through 2031, supported by 7.8% RPK growth in 2025 and an 87.2% load factor in March 2026.

Which end-user group contributes the most revenue today?

Commercial aviation remained the largest end-user segment with 62.87% of revenue in 2025 because of fleet renewals and recurring overhaul cycles on high-use aircraft.

What are the most important competitive moves to watch?

Capacity expansion and long-term service agreements stand out, including Safran's Lyon plant investment, Collins' Spokane expansion, and Safran's supply deals with Spirit Airlines and Riyadh Air .

Page last updated on: