Aircraft Lightning Protection Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.89 Billion |

| Market Size (2031) | USD 6.57 Billion |

| Growth Rate (2026 - 2031) | 6.09% CAGR |

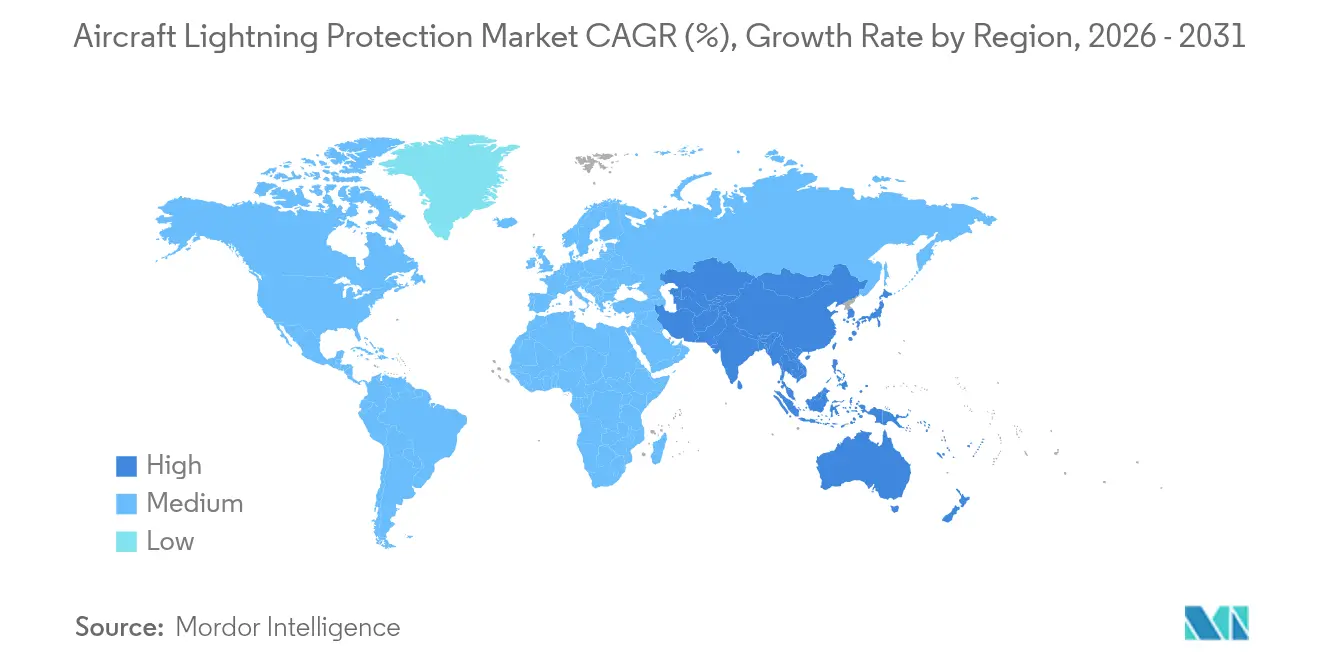

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

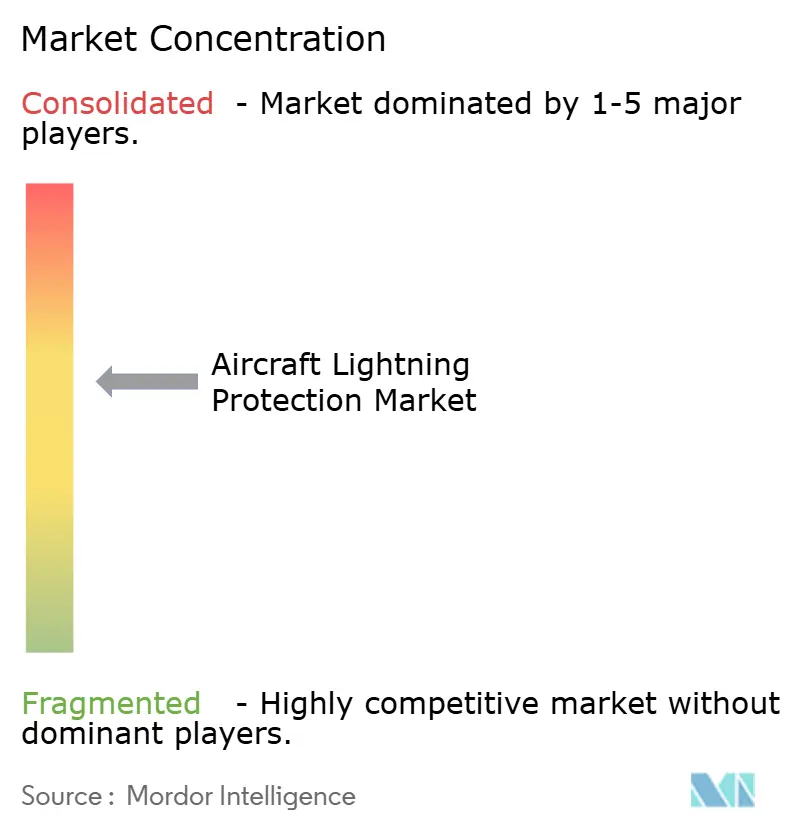

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Lightning Protection Market Analysis by Mordor Intelligence

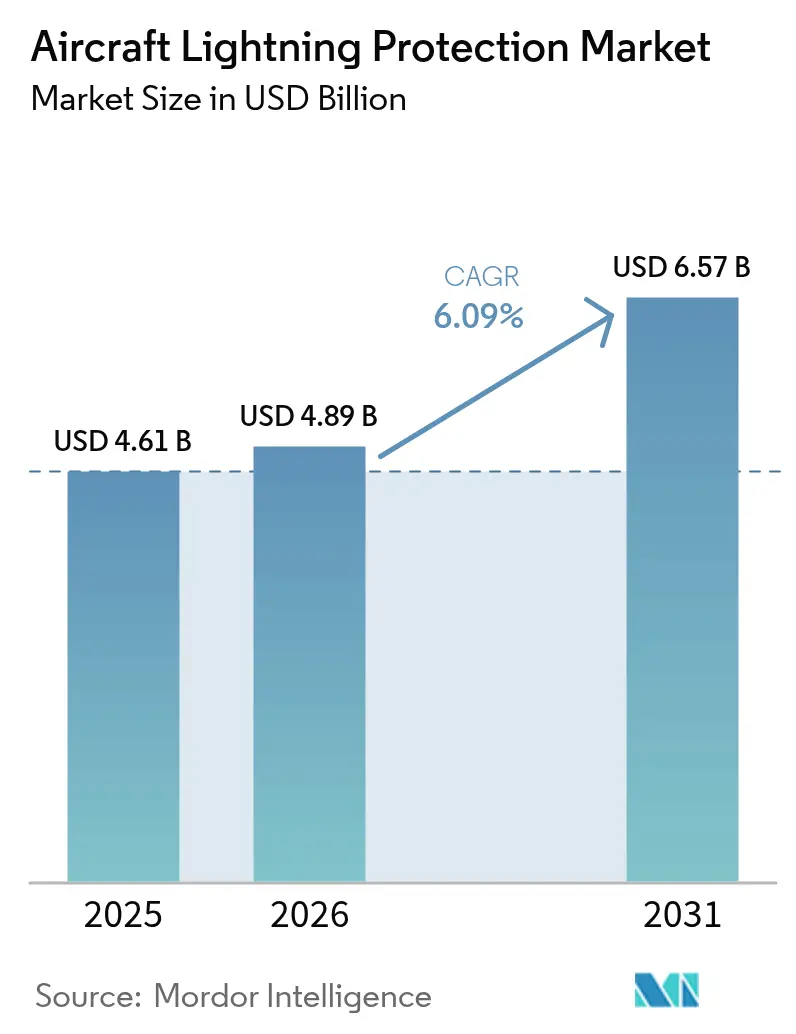

The aircraft lightning protection market size is expected to grow from USD 4.61 billion in 2025 to USD 4.89 billion in 2026 and is forecast to reach USD 6.57 billion by 2031 at 6.09% CAGR over 2026-2031. Growth aligns with two structural shifts: the widening application of carbon-fiber fuselages and the rapid emergence of electric air-taxi fleets. Composite airframes lack the built-in conductivity of traditional aluminum skins, so every new delivery increases demand for conductive foils, meshes, and nanomaterial coatings that safely channel strike energy. Tightening FAA and EASA certification rules intensify this pull, while record commercial aircraft backlogs push OEMs to secure a long-term supply of qualified protection materials.[1]Source: Franklin Fisher, “Lightning Protection of Aircraft Handbook,” Federal Aviation Administration, faa.gov Asia-Pacific’s airport boom, led by China’s target of 270 operational facilities by 2025, accelerates volume growth even as North America remains the technology nucleus.[2]Source: US Department of Commerce, “China - Aviation,” International Trade Administration, trade.gov Mid-sized suppliers face cost pressure from six-figure qualification tests on the competitive front, opening paths for larger firms to consolidate capabilities through M&A.

Key Report Takeaways

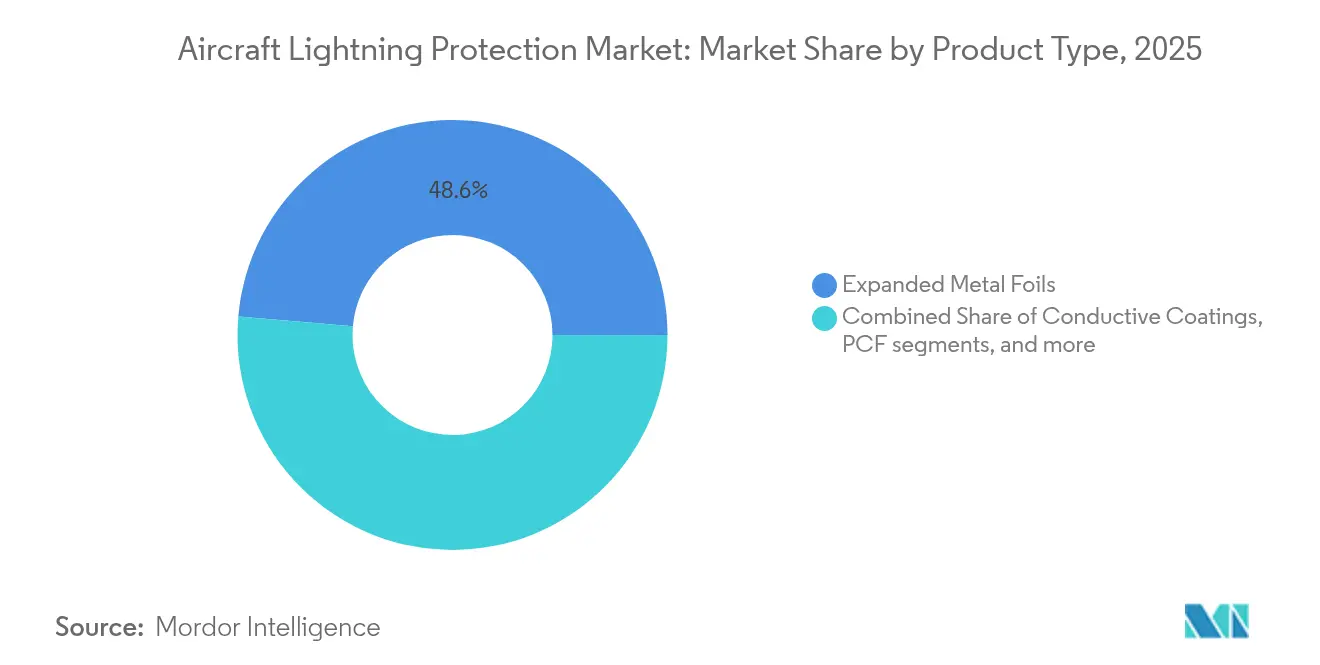

- By product type, expanded metal foils led with 48.62% of the aircraft lightning protection market share in 2025, while plated carbon fiber is advancing at a 7.33% CAGR through 2031.

- By aircraft type, fixed-wing platforms accounted for 58.10% of the aircraft lightning protection market size in 2025; eVTOL/urban air mobility is forecasted to expand at a 9.85% CAGR to 2031.

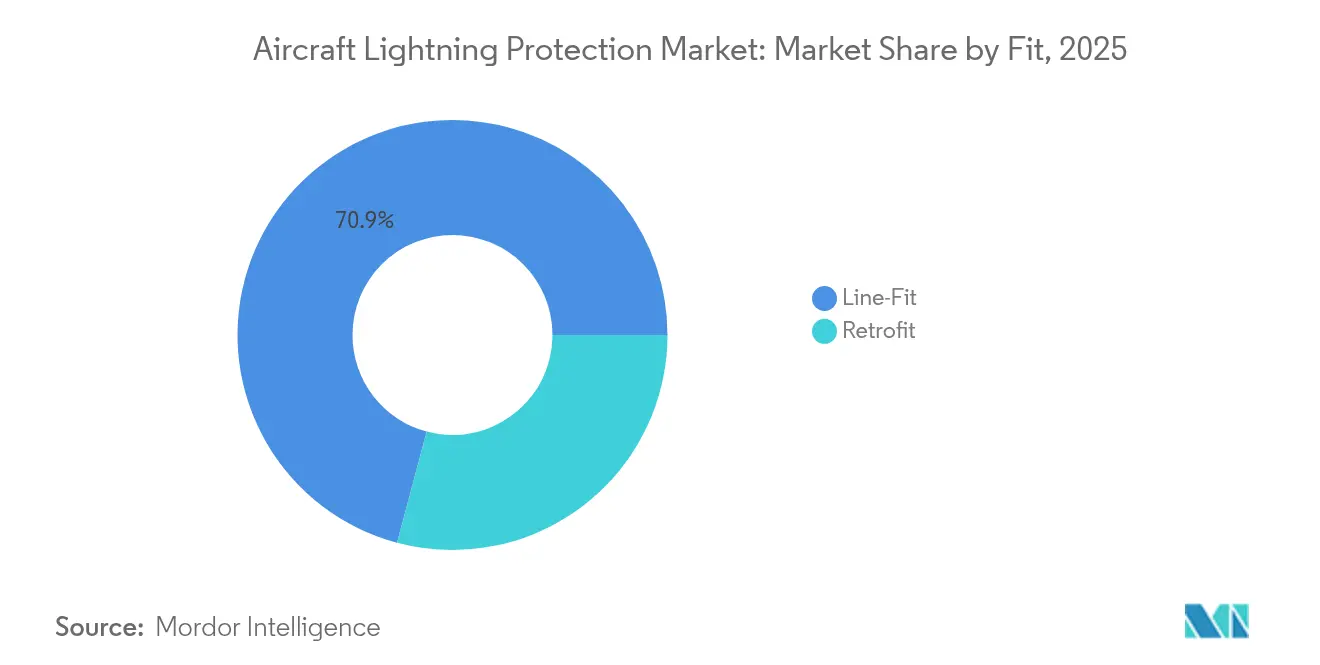

- By fit, line-fit installations captured 70.85% revenue share of the aircraft lightning protection market in 2025; retrofit demand trails but is growing 6.88% over the forecast period.

- By end user, naval forces held 64.55% of the aircraft lightning protection market share in 2025, whereas civil/commercial customers represent the fastest growth at 8.64% CAGR.

- By geography, North America retained 38.12% of 2025 revenue; Asia-Pacific is the fastest-growing region at 7.62% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Lightning Protection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in composite-airframe deliveries | +1.8% | North America and Europe, spreading worldwide | Medium term (2-4 years) |

| Increasing commercial aircraft backlogs | +1.2% | Asia-Pacific and North America | Short term (≤ 2 years) |

| Stricter FAA and EASA lightning-certification rules | +0.9% | North America and Europe with global spillover | Long term (≥ 4 years) |

| Growing retrofit programs for aging fleets | +0.7% | North America and Europe | Medium term (2-4 years) |

| On-board lightning detection and prognostic maintenance | +0.4% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Electrification of eVTOL/urban air-taxi fleets | +0.3% | Urban centers worldwide, led by North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Composite-Airframe Deliveries

B787 and A350 aircraft families rely on embedded copper or aluminum meshes to dissipate strike currents, marking a wholesale design departure from external bonding straps. Operators increasingly view integrated mesh as standard, and that expectation now cascades into narrow-body refresh programs and the latest regional jets. NASA test panels showed that lightweight non-metallic films can cut lightning damage depth by 79% while boosting post-strike compressive strength by 21%, encouraging OEMs to adopt thinner, lighter layers in forthcoming models. Material innovation thus compounds unit demand, as each new composite panel requires factory-installed conductive pathways. The driver delivers its strongest pull through 2027, stabilizing as composite penetration plateaus.

Increasing Commercial Aircraft Backlogs

Order books for single-aisle jets remain full well into 2031. Boeing and Airbus have publicly linked production-rate hikes to a reliable supply of specialty materials such as expanded metal foils. PPG’s USD 290 million aerospace-coatings backlog in Q3 2024 highlights the strain on supply chains already running at extended lead times.[3]Source: John Marshall, “PPG Q3 2024 Earnings Prepared Remarks,” PPG Industries, ppg.com Each backlog drawdown releases a wave of line-fit demand for lightning protection kits, while deferred deliveries translate into incremental retrofit opportunities as airlines stretch the life of older frames. Asia-Pacific fleets constitute a third of the global backlog, positioning the region as the volume growth engine through 2026.

Stricter FAA and EASA Lightning-Certification Rules

The FAA’s adoption of SAE ARP 5577 and EASA’s special conditions for battery-rich VTOL aircraft raise test-current thresholds and expand the zones classified as direct effects areas. Compliance costs soar because every new material stack-up must prove performance at 200 kA and beyond. Large vendors pass these costs across wider product portfolios, whereas start-ups often retreat to niche R&D contracts. Over time, standardization tightens switching costs, meaning certified incumbents enjoy a durable revenue stream as new aircraft families progress from prototype to production.

Growing Retrofit Programs for Aging Fleets

Military life-extension projects—such as A-10 wing replacements and F-16 avionics upgrades—routinely add conductive films or mesh during depot overhaul to protect new digital mission systems. Commercial operators replicated the practice in 1990s-vintage A320s to minimise lightning-induced dispatch delays. Retrofit kits typically command higher gross margins due to custom engineering, offsetting lower volume relative to line-fit. Demand peaks through 2028 as carriers align retrofit windows with heavy-check schedules.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High qualification-testing costs | -0.8% | Global, especially challenging for SMEs | Medium term (2-4 years) |

| Weight-penalty versus fuel-burn trade-offs | -0.6% | Global, acute in fuel-sensitive markets | Short term (≤ 2 years) |

| Volatile raw-material pricing for aluminum and copper | -0.5% | Global, most visible in commodity-importing regions | Short term (≤ 2 years) |

| Technical challenge of qualifying nanomaterial coatings | -0.4% | Global, with higher impact on early-stage suppliers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Qualification-Testing Costs

Lightning simulation labs capable of 200 kA impulses charge aerospace rates exceeding USD 40,000 per shot, and a full compliance program can require dozens of strikes across multiple coupon sizes. Start-ups developing graphene or CNT solutions often exhaust seed funding before clearing certification milestones, leaving their IP to be licensed by larger incumbents. The financial hurdle constrains overall technology diversity and slows price competition, trimming growth by an estimated 0.8 percentage points over the horizon.

Weight-Penalty Versus Fuel-Burn Trade-offs

Traditional copper mesh lifts OEW by up to 90 kg on a twin-aisle jet, translating into USD 3,000 in annual fuel per added pound across a 20-year life. Airlines, therefore, pressure OEMs to adopt lighter substitutes. Yet ultra-thin aluminum coatings can cost two to three times more per square foot than legacy mesh, creating procurement tension that defers wider adoption. Weight risk is most acute for eVTOL craft, where eve ry kilogram removes passenger range.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Composites Drive Innovation Beyond Traditional Foils

Expanded metal foils still held 48.62% of the aircraft lightning protection market share in 2025 due to their long service history and abundant certification data. Even so, plated carbon fiber is projected to capture a rising slice of the aircraft lightning protection market size as its 7.33% CAGR outpaces volume growth in legacy foils. The material embeds conductivity within structural plies, shaving weight while maintaining strike pathways, an advantage validated on 787 fuselage panels. Research panels with carbon nanotubes recorded 54.8% smaller strike scars, pointing to future gains as nano-reinforced plies move from lab to line.

Interwoven wire fabrics appeal to defense primes seeking proven survivability, particularly for rotorcraft operating low-level in storm-dense theaters. Conductive coatings fill retrofit niches where foil lay-up is impractical; however, studies show thick coatings can trap arc heat and enlarge delamination, limiting adoption. Though outside today’s revenue pie, early-stage graphene films attract R&D capital from Airbus and BAE because they promise step-changes in areal weight without expensive copper inputs.

By Aircraft Type: eVTOL Revolution Reshapes Protection Requirements

Fixed-wing jets generated 58.10% of 2025 revenue, cementing their role as the anchor of the aircraft lightning protection market. They also represent the majority of current certification knowledge, so material suppliers routinely validate new solutions on single-aisle structures before chasing emerging categories. In contrast, eVTOL airframes expand at a 9.85% CAGR and introduce distributed propulsion pods and high-energy batteries that create multiple strike entry points. EASA’s latest special conditions now require holistic system-level protection that addresses battery thermal runaway alongside structural current paths.

The aircraft lightning protection market size for eVTOL components is forecast to multiply as prototypes enter serial production from 2026 onward. Rotorcraft remain a steady niche because their rotating hubs naturally attract leaders, demanding robust rotor-tip bonding and blade protection layers mandated by 14 CFR 27.610. The segment tableau shows traditional line-fit volume in fixed-wing jets financing R&D for lightweight solutions poised to dominate the urban air-mobility fleet later in the decade.

By Fit: Line-Fit Dominance Masks Retrofit Complexity

Line-fit installations captured 70.85% of 2025 revenue and will remain the primary conduit for volume. OEM-specified mesh or foil is co-cured with composite skins at the autoclave stage, ensuring conductivity continuity and eliminating extra labor later. This integration underpins lower lifecycle cost and underwrites a 6.88% CAGR to 2031. Aircraft lightning protection market share in retrofit remains small, yet high-margin.

Airlines tackling cabin-upgrade checks green-light conductive paint or peel-and-stick foil patches that must dovetail with legacy wiring schemes, a task often requiring bespoke engineering teams. Retrofit, therefore, brightens revenue diversity but adds schedule risk, especially where panels are already RIBE-bonded to load-bearing frames.

By End User: Defense Spending Drives Naval Dominance

Naval aviation accounted for 64.55% of the aircraft lightning protection market share in 2025, owing to high per-aircraft system value and stringent MIL-STD requirements. Maritime fighters and rotorcraft experience harsher saline environments, so corrosion-resistant meshes and multi-coat sealants command premium pricing. Mitsubishi Heavy Industries booked a record JPY 791.5 billion (USD 5.45 billion) aerospace revenue in FY 2024 as Japan ramped up defense outlays, and each new patrol aircraft embeds advanced protection layers.

Civil/commercial fleets, while smaller today, grow at 8.64% CAGR as airlines replace aging narrow-bodies and eVTOL operators prepare for certification. The aircraft lightning protection industry increasingly leverages defense-funded R&D to mature graphene or CNT films before commercial rollout.

Geography Analysis

North America retained 38.12% of 2025 revenue because the region hosts the bulk of global composite-airframe assembly, high-energy certification labs, and tier-one suppliers. FAA collaboration eases qualification runs, allowing vendors to compress time-to-market. Canada’s niche suppliers feed resin-infusion foils, while Mexico’s maquiladoras machine bonding hardware for cabin zones. Ecosystem tightness supports premium pricing, though labor shortages risk schedule slip. Asia-Pacific posts the fastest 7.62% CAGR, underpinned by China’s intent to operate 270 airports by 2025, each driving fresh narrow-body orders. Domestic composites plants scale rapidly; however, intellectual-property safeguards remain a Western concern, slowing the transfer of the latest CNT-reinforced meshes. Japan’s orderbook surge to JPY 7.07 trillion in FY 2024 pairs with stringent MoD specifications, spurring local demand for high-amp foil and corrosion-resistant sealants. India’s Tata-Airbus line at Vadodara lays early groundwork for an indigenous lightning-protection supply but needs two decades to match Western volume. Europe continues as the technology vanguard. The EASA certification authority prompts early adoption of regulatory changes, and Horizon-funded labs pioneer ultra-thin aluminum coatings that cut mesh weight by 58%. The Middle East leverages fleet renewals at Gulf carriers, pushing retrofit demand. South America and Africa remain nascent, but Brazil’s regional jet exports seed future requirements for local foil conversion lines.

Competitive Landscape

Market structure is moderately concentrated. PPG captured a strong aerospace-coatings tailwind, with Q3 2024 order backlogs worth USD 290 million, providing clear revenue visibility. Amphenol’s USD 900 million purchase of Carlisle Interconnect Technologies extends the firm’s harsh-environment interconnect play into lightning-bonding straps, completing a vertically integrated offering. Mitsubishi Heavy Industries accelerates through defense contracts, channeling research funds into lighter copper-aluminum hybrid meshes for maritime patrol craft.

Innovation fronts emerge from smaller specialist houses. Haydale’s graphene-enhanced prepregs, funded under the UK NATEP program, promise equivalent strike performance at half the areal weight. ORNL’s 6.5-foot wind-turbine blade experiments corroborate cross-sector benefits, validating material behavior under 150 kA impulses relevant to eVTOL winglets. Certification barriers remain the chief moat; collaboration with tier-one OEMs is essential for lab-bench concepts to reach production. Consolidation is expected to continue as incumbents buy nascent technology rather than build from scratch.

Aircraft Lightning Protection Industry Leaders

PPG Industries, Inc.

Astroseal Products Manufacturing Corp.

Dayton-Granger, Inc.

Henkel Corporation

Amphenol Aerospace (Amphenol Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: NTT Corporation demonstrated a drone-based lightning-triggering system rated to 150 kA, opening use cases for aircraft ground-handling protection.

- December 2024: Oak Ridge National Laboratory validated new conductive inserts in a 6.5-ft blade tip, indicating cross-over potential for composite aircraft structures.

- May 2023: Satair, a subsidiary of Airbus Services, inked a multi-year distribution deal with Dayton-Granger, Inc., a leading aerospace manufacturer known for its antennas, static dischargers, and lightning protection equipment. This agreement paves the way for the worldwide distribution of Dayton-Granger's ELT-DT Blade Antenna. This innovative product boasts anti-disablement, lightning protection, and Global Navigation Satellite System (GNSS) location capabilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the aircraft lightning protection market as the value generated by materials, sub-systems, and integrated solutions that conduct, dissipate, or warn against strike energy on fixed-wing, rotary-wing, and unmanned airframes, including expanded metal foils, conductive coatings, static dischargers, diverter strips, and transient voltage suppressors installed during line-fit or retrofit programs.

Scope exclusion: Handheld lightning detectors used by ground staff, airport-mounted lightning safety hardware, and generic surge suppressors for non-aerospace vehicles are outside this analysis.

Segmentation Overview

- By Product Type

- Expanded Metal Foils

- Interwoven Wire Fabrics

- Conductive Coatings

- Plated Carbon Fiber (PCF)

- Others

- By Aircraft Type

- Fixed-Wing Aircraft

- Narrow-Body

- Wide-Body

- Regional and Business Jets

- Rotorcraft

- Civil Helicopters

- Military Helicopters

- Unmanned Aerial Vehicles (UAV)

- eVTOL/UAM Vehicles

- Fixed-Wing Aircraft

- By Fit

- Line-Fit

- Retrofit

- By End User

- Civil/Commercial

- Military

- By Region

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Israel

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Telephone discussions with certification engineers, MRO managers, composite suppliers, and avionics integrators across North America, Europe, and Asia helped us verify cost ranges, retrofit frequency, and regional regulation nuances, letting us stress-test desk findings before locking the model.

Desk Research

We began by extracting yearly aircraft deliveries, active-fleet mix, and strike-incident rates from FAA Service Difficulty Reports, EASA lightning guidance, ICAO registries, and IATA statistics. Our team then screened 10-Ks, investor decks, and press releases to map bill-of-material costs and replacement cycles. Patent analytics from Questel plus customs records on copper and aluminum mesh imports revealed material trends, while Dow Jones Factiva news feeds and IMTMA build logs added context.

Because no single source covers every niche, Mordor analysts broaden the net to additional open databases and association white papers; the sources named are illustrative, not exhaustive.

Market-Sizing & Forecasting

We apply a top-down build. Annual production and active-fleet counts are multiplied by protection penetration rates and average system spend, then cross-checked through sampled supplier revenues and MRO invoice reviews. Key drivers inside our multivariate regression plus exponential smoothing include composite share per new airframe, eVTOL launch schedules, fleet age, retrofit cycle length, copper prices, and FAA strike statistics. Gaps in bottom-up data are bridged with carefully interviewed ranges.

Data Validation & Update Cycle

Outputs pass two analyst reviews that flag anomalies against historic claim data and metal trade signals. Reports refresh each year, with interim updates when delivery forecasts or input costs shift materially. Before release, a fresh analyst pass ensures clients receive the latest view.

Why Mordor's Aircraft Lightning Protection Baseline Commands Reliability

Published estimates often diverge because firms vary component scope, treat retrofit revenue unevenly, or freeze currency at earlier rates.

By refreshing our segmentation annually, rebasing to current exchange averages, and pairing desk findings with field views, Mordor Intelligence narrows these gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.61 B (2025) | Mordor Intelligence | - |

| USD 3.10 B (2024) | Global Consultancy A | Conductive coatings omitted; limited interviews |

| USD 4.43 B (2024) | Industry Journal B | Retrofit revenue absent; older fleet outlook |

| USD 5.14 B (2024) | Regional Consultancy C | High ASP escalation; currency not rebased |

The comparison shows that our disciplined scope choices and verified inputs give decision-makers a balanced, transparent baseline they can trust.

Key Questions Answered in the Report

What is the current size of the aircraft lightning protection market?

The aircraft lightning protection market stands at USD 4.89 billion in 2026 and is projected to reach USD 6.57 billion by 2031, reflecting a steady 6.09% CAGR.

Which region is growing fastest in this market?

Asia-Pacific shows the highest growth, advancing at a 7.62% CAGR thanks to large aircraft backlogs and airport construction programs.

Why are composite airframes increasing demand for lightning protection?

Carbon-fiber structures lack the inherent conductivity of aluminum, so they require embedded foils or meshes to safely dissipate strike energy.

How do certification costs impact new material adoption?

High-current laboratory tests can cost hundreds of thousands of dollars, limiting smaller firms’ ability to bring innovations like graphene meshes to market.

Which product type is gaining momentum?

Plated carbon fiber is the fastest-growing product, registering a 7.33% CAGR because it integrates structural strength with conductivity while lowering weight.

How will eVTOL aircraft influence future demand?

EVTOL vehicles introduce multiple electric propulsion pods and batteries, driving demand for holistic, lightweight protection systems and boosting long-term market growth.

Page last updated on: