Aircraft Band Clamp Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 267.44 Million |

| Market Size (2031) | USD 349.89 Million |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Band Clamp Market Analysis by Mordor Intelligence

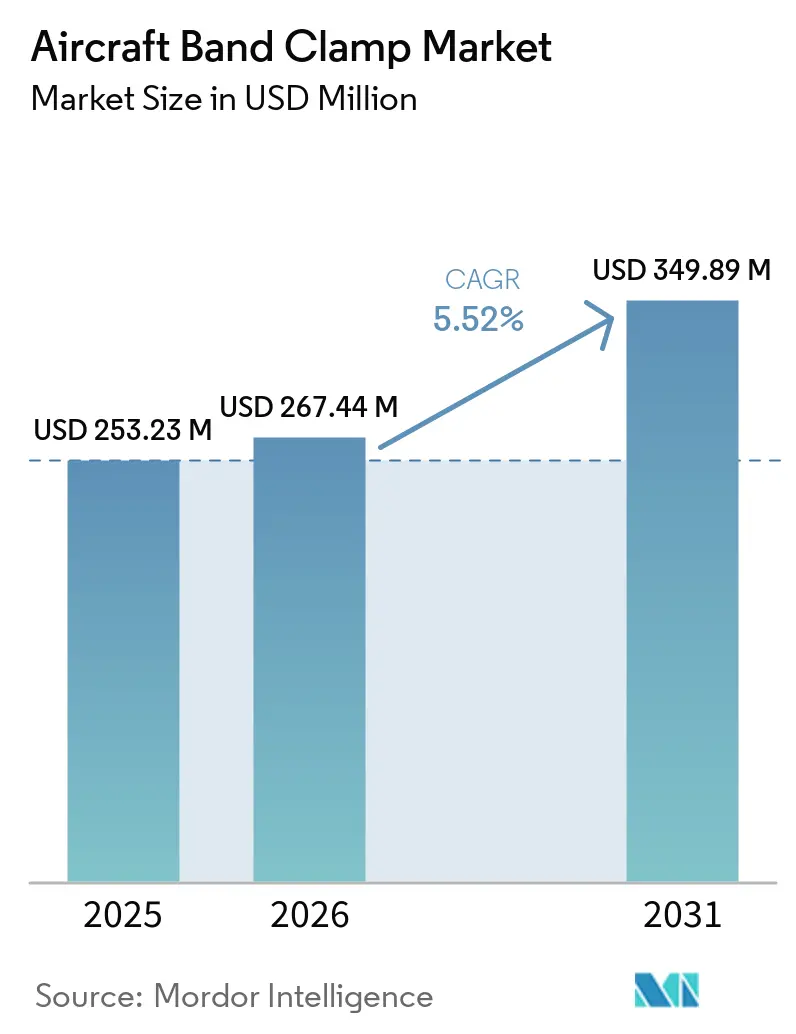

The aircraft band clamp market was valued at USD 253.23 million in 2025, and is projected to grow from USD 267.44 million in 2026 to USD 349.89 million by 2031, at a 5.52% CAGR over 2026-2031. This steady expansion is being supported by the strongest OEM production cycle in many years, with Airbus alone holding a commercial aircraft backlog of 9,037 units as of March 2026, while the combined Airbus and Boeing pipeline remained above 15,000 aircraft in 2026.[1]Airbus, “Q1 2026 Results,” Airbus, airbus.com Because each narrowbody aircraft uses close to 50 V-band and related clamps across engines, ducts, and airframe installations, those backlogs convert into recurring component demand over a long production horizon. The aircraft band clamp market is also being pushed by tighter environmental rules and fuel-efficiency goals, which are increasing interest in lighter materials and more integrated clamp designs across new aircraft programs. Replacement demand is adding a second layer of support, since the global fleet averaged 15.1 years of age in 2025, and older aircraft require more frequent inspection and replacement activity across clamp-intensive systems. Competition remains active rather than concentrated, as diversified aerospace suppliers and specialist clamp manufacturers compete through approved-vendor status, material expertise, and qualification depth, while long certification cycles still slow rapid new entry into the aircraft band clamp market.

Key Report Takeaways

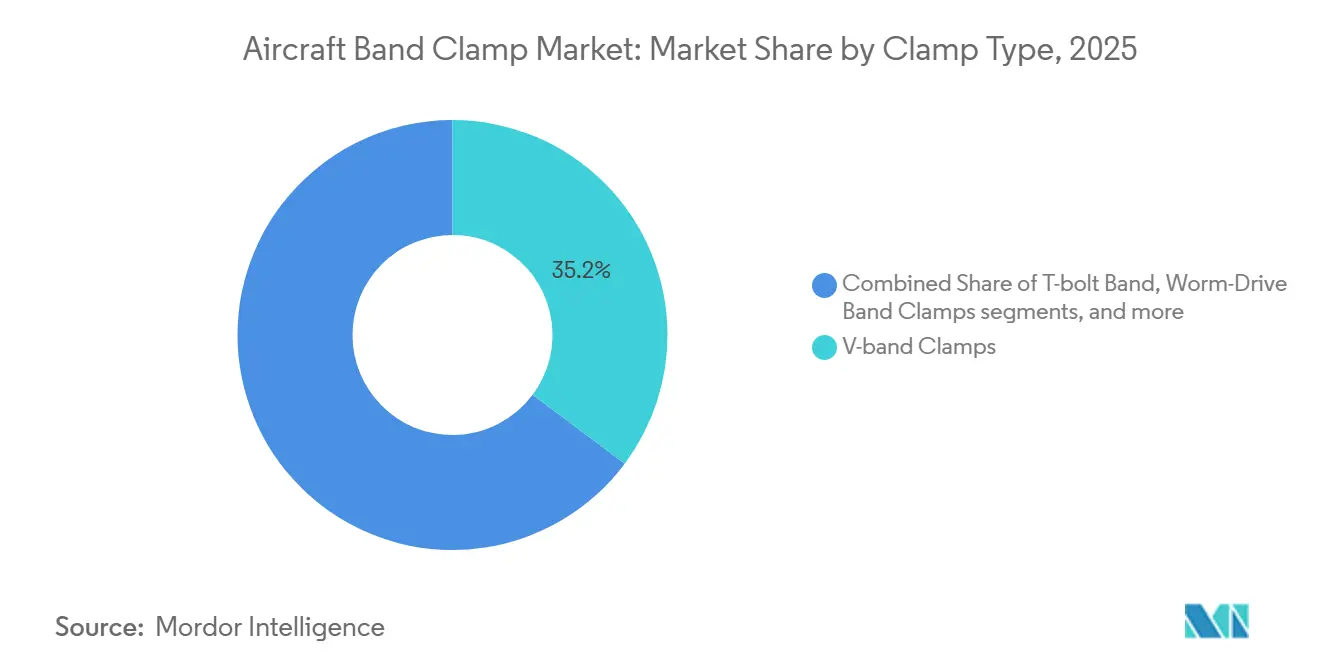

- By clamp type, V-band clamps accounted for 35.21% of the aircraft band clamp market in 2025, while cradle support latch clamps are projected to grow at a 6.83% CAGR through 2031.

- By material, stainless steel captured 46.65% share in 2025, while titanium is forecast to grow at 7.22% CAGR through 2031.

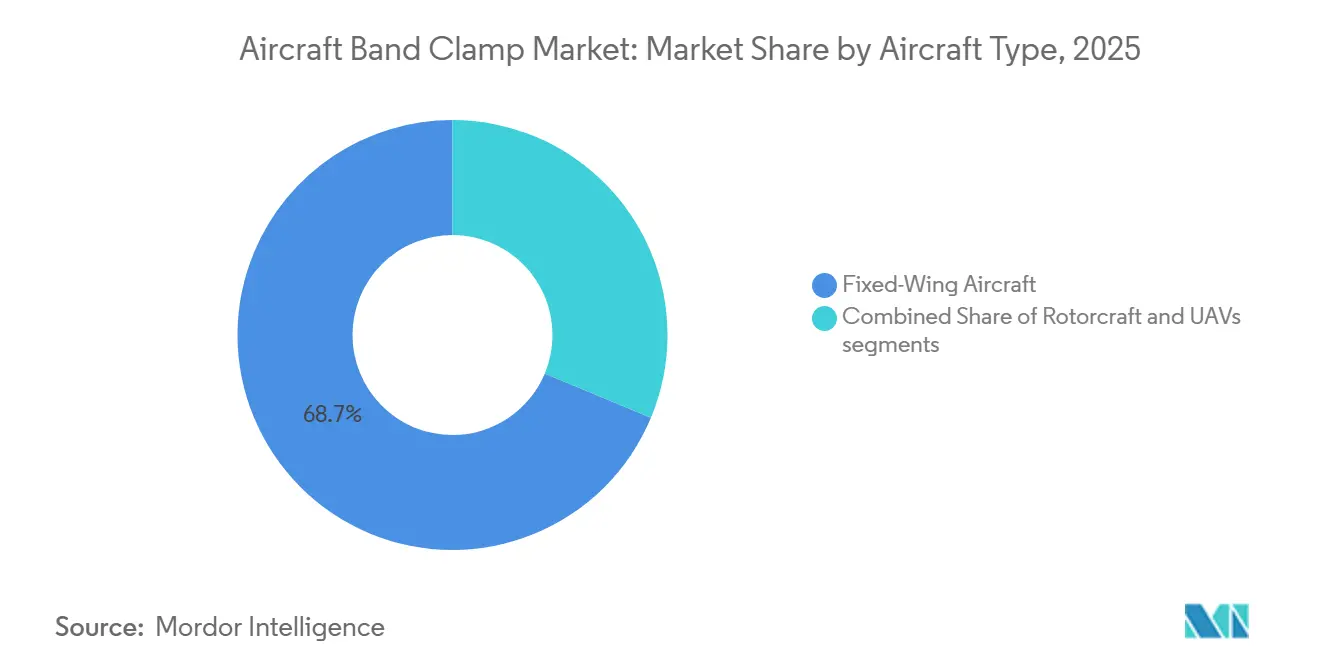

- By aircraft type, fixed-wing aircraft held 68.71% share in 2025, while UAVs are projected to expand at 8.42% CAGR through 2031.

- By application, airframe assemblies accounted for 38.32% of the aircraft band clamp market in 2025, while electrical systems are projected to grow at a 7.51% CAGR through 2031.

- By end-user, OEMs commanded a 69.91% share in 2025, while the aftermarket is forecast to grow at a 6.77% CAGR through 2031.

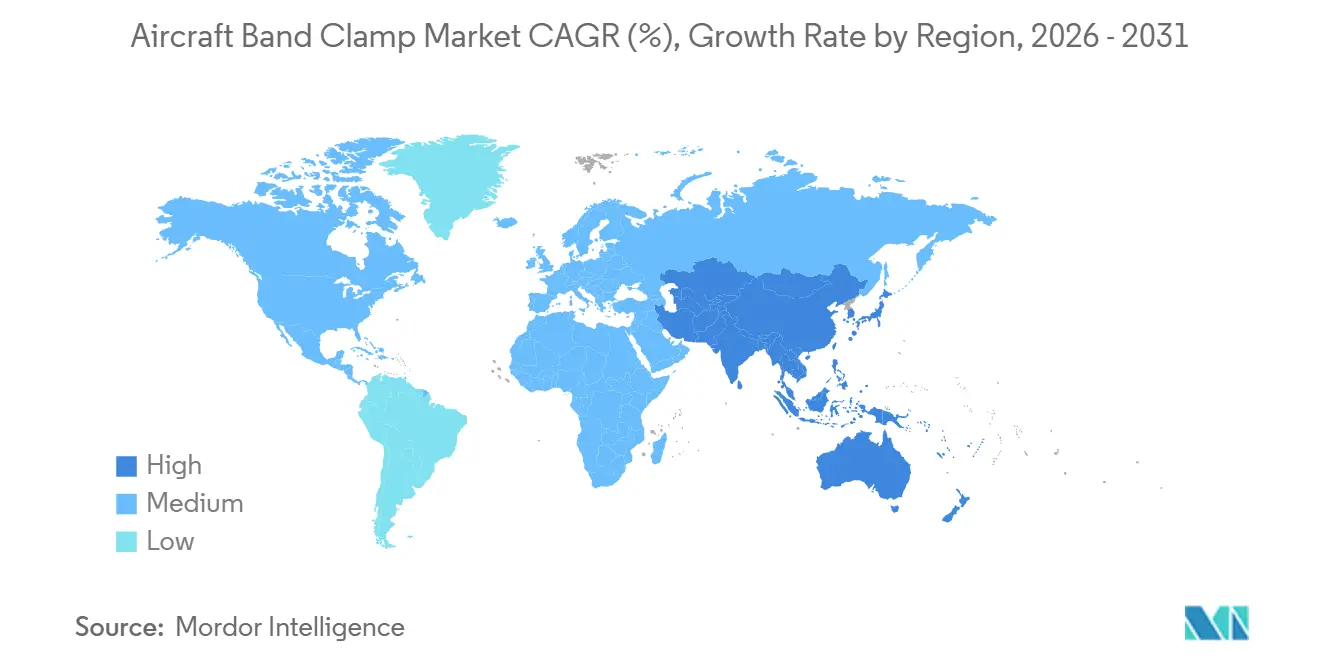

- By geography, Asia-Pacific held 34.45% of the aircraft band clamp market share in 2025, and the region is forecast to expand at 7.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aircraft Band Clamp Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising aircraft production backlog | +1.4% | Global, concentrated in North America, Europe, and APAC | Short term (≤ 2 years) |

| Expanding MRO clamp-replacement demand | +1.1% | Global, strongest in North America and APAC | Short term (≤ 2 years) |

| Higher defense aircraft procurements | +0.8% | North America, Europe, APAC | Medium term (2-4 years) |

| Stricter emission/fuel-efficiency norms | +0.7% | Global, with early regulatory application in EU and North America | Medium term (2-4 years) |

| Additive-manufactured titanium clamps | +0.5% | North America and Europe, with spillover to APAC | Long term (≥ 4 years) |

| Hybrid-electric thermal-cycling needs | +0.4% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Aircraft Production Backlog Sustaining OEM Component Pull

The aircraft band clamp market remains closely tied to aircraft build rates, as every new shipset requires OEM-qualified clamps during first assembly. Airbus held a commercial aircraft backlog of 9,037 units as of March 2026, and the combined Airbus and Boeing backlog remained above 15,000 aircraft in 2026, providing suppliers with clear visibility into future production demand. Airbus also delivered 793 commercial aircraft in 2025, which shows that the order pipeline is already translating into installed component volume across active programs.[2]Source: Airbus, “793 Commercial Aircraft Deliveries in 2025,” Airbus, airbus.com This backlog supports forward planning for materials, certification capacity, and long-run supply agreements across the aircraft band clamp market. At the same time, supply chain bottlenecks cost airlines more than USD 11 billion in 2025, keeping older aircraft in service longer and increasing replacement demand alongside new production demand. The result is a durable two-channel demand pattern in which new builds and prolonged fleet service keep clamp volumes elevated.

Stricter Emission And Fuel-Efficiency Norms Accelerating Lightweighting

The aircraft band clamp market is being reshaped by tighter environmental rules that reward lower weight and more efficient system design. ICAO adopted a CO2 standard in March 2026 that is 10% more stringent for new aircraft type designs from 2031, which increases pressure on manufacturers to reduce mass across structures and systems.[3]International Civil Aviation Organization, “New Aircraft Will Face Stricter Environmental Standards,” ICAO, icao.int CORSIA’s first phase, from 2024 to 2026, already requires 690 aircraft operators to monitor and offset emissions above 85% of 2019 levels, keeping fuel-burning reduction high on airline and supplier agendas. That policy setting improves the case for titanium and aluminum-alloy clamps in applications where stainless steel has long been the standard choice. It also supports multi-function clamp designs that reduce part count, simplify installation, and lower the weight burden of surrounding assemblies. Over the medium term, these rules are likely to shift more value toward lightweight materials, even if their unit costs remain above those of conventional options.

Expanding MRO Clamp-Replacement Demand From An Aging Global Fleet

The aircraft band clamp market is seeing stronger replacement demand as the global fleet ages and remains in service longer. IATA placed the average commercial aircraft age at 15.1 years in 2025, with passenger aircraft at 12.8 years and cargo aircraft at 19.6 years, thereby increasing maintenance intensity across clamp-heavy systems. In engine and hydraulic line applications, clamps require regular inspection and scheduled replacement, so mature fleets turn routine maintenance events into recurring demand. The supplied draft notes that a large part of the operating fleet renews its clamp inventory on a rolling 2-3-year cycle, helping keep service demand stable even when production schedules fluctuate, which is one reason the aftermarket channel in the aircraft band clamp market is projected to grow faster than the overall market through 2031. Asia-Pacific adds to this momentum, as expanding regional MRO capacity widens the base of approved buyers and certified replacement suppliers.

Higher Defense Aircraft Procurements Enlarging Addressable Platform Base

Defense procurement is expanding the addressable platform base for the aircraft band clamp market beyond commercial aviation. The US Department of Defense (DoD) FY2026 budget allocated USD 68.30 billion for aircraft and related systems, including multiple F-35s, F-15EX Eagle IIs, and KC-46A tankers, while also funding the B-21 Raider and F-47 programs. These aircraft use band clamps across exhaust, hydraulic, and fuel-routing systems, and military qualification standards usually require tighter traceability and more precise tolerances than those in commercial aircraft programs. That raises the revenue value of each approved unit even when absolute production volumes remain below those of narrowbody airliners. Defense demand is also widening across Europe and parts of the Asia-Pacific region, which benefits suppliers that already operate under aerospace quality and approval frameworks. Once these programs enter service, they also create decades of aftermarket demand, which gives the aircraft band clamp market a long replacement tail beyond the initial production window.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Metal price volatility | -0.6% | Global, acute for North American and European manufacturers dependent on non-Chinese sponge | Medium term (2-4 years) |

| Lengthy airworthiness certification cycles | -0.5% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Band-less quick-release couplings adoption | -0.3% | North America and Europe, especially in MRO and narrowbody OEM applications | Medium term (2-4 years) |

| Specialty wire‐rod supply disruptions | -0.4% | Global, with acute exposure in APAC and suppliers tied to concentrated raw-material sources | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Metal Price Volatility Compressing Margin Predictability

Raw-material volatility remains a drag on the aircraft band clamp market because titanium and specialty alloys matter more as lightweight programs gain traction. Clamp suppliers often work under fixed-price or long-term agreements, so sudden changes in input costs are not always passed through to customers quickly. This pressure is most visible for manufacturers trying to scale titanium offerings while preserving margins under approved aerospace contracts. The issue is broader than pricing alone, as supply concentration and geopolitical disruption can also affect availability, lead times, and inventory strategy. Suppliers with stronger sourcing depth or better purchasing discipline are better placed to absorb these swings than smaller competitors. Even so, the aircraft band clamp market can see slower material substitution when buyers turn cautious during periods of unstable alloy economics.

Lengthy Airworthiness Certification Cycles Slowing New Product Introduction

Certification timelines are lengthening, and that slows commercial adoption of new designs in the aircraft band clamp market. The supplied draft states that FAA and EASA approval cycles for novel aerospace components now extend to 4-5 years, up from 12-24 months historically, following a period of closer quality scrutiny across the commercial supply chain. FAA and EASA amended their Technical Implementation Procedures in June 2025, which streamlined bilateral validation for some design changes but still left major departures subject to full approval requirements.[4]Federal Aviation Administration and European Union Aviation Safety Agency, “Technical Implementation Procedures For Airworthiness and Environmental Certification, Amendment 1 to Revision 7,” Federal Aviation Administration, faa.gov Additive-manufactured titanium clamps and sensor-enabled products, therefore, face a long runway before engineering work converts into booked revenue, creating a structural advantage for incumbents already listed on approved vendor rosters with OEMs and major MRO providers. It also increases the funding burden on new entrants, as they must cover compliance, testing, and documentation costs for years before reaching scale production.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Clamp Type: V-Band Clamps Hold The Lead While Integrated Variants Gain Speed

V-band clamps accounted for 35.21% of revenue in 2025, making them the leading product category in the aircraft band clamp market. Their lead comes from broad use in jet engine exhaust ducts, bleed-air systems, and APU connections where secure sealing and repeat serviceability are essential. These installations experience heavy thermal cycling, vibration, and frequent maintenance access, so operators favor a format that can maintain holding force during repeated service events. That requirement keeps V-band designs firmly embedded on many commercial narrowbody platforms and on military aircraft operating under demanding thermal conditions. T-bolt clamps followed with strong use in high-pressure fuel and hydraulic routing, while worm-drive variants remained important in lower-pressure ducting and air-distribution applications.

Cradle support latch clamps are forecast to grow at a 6.83% CAGR through 2031, and this segment of the aircraft band clamp market is supported by designs that combine structural support and sealing in a single unit. Aircraft builders are under pressure to reduce part count, shorten installation time, and simplify packaging around tighter assemblies, which favors these integrated products. Their appeal is strongest on next-generation narrowbody programs where production efficiency now carries more weight in design decisions. Airbus began serial integration of wire-directed energy-deposition titanium parts into the A350 cargo door surround in 2026, demonstrating how production design is moving toward consolidation and more geometry-efficient components. That same design direction supports clamp formats that do more than hold a joint, which is why growth is shifting toward multi-function variants across the aircraft band clamp market.

By Material: Stainless Steel Dominates While Titanium Gains Strategic Value

Stainless steel led material demand with 46.65% of revenue in 2025, reflecting its broad qualification base, balanced cost profile, and suitability for a wide range of aerospace uses. It remains the default choice for many non-extreme-temperature applications because it offers corrosion resistance, reliable durability, and predictable manufacturing economics. The high output of major narrowbody families also reinforces this position, since cost-controlled commercial production still depends heavily on proven stainless solutions. That is why stainless steel continues to anchor large-volume programs even as aircraft designers search for lighter options in selected assemblies. Aluminum alloys retain a meaningful role in lower-load airframe installations where weight sensitivity is high and thermal exposure is less severe.

Titanium is projected to grow at a 7.22% CAGR through 2031, and the market size for aircraft band clamps is gaining value as lightweighting pressure and advanced manufacturing capabilities converge. ICAO’s tighter environmental standards are increasing pressure to remove weight at the component level, which improves the case for titanium, where performance benefits justify a higher unit price. Airbus’s serial use of additively manufactured titanium structures in 2026 also signals that aerospace qualification pathways for complex titanium parts are becoming more practical at the production scale. Norsk Titanium stated that PA-DED titanium qualification for flight-critical structures delivered a 20% to 35% cost reduction compared to machined forgings, strengthening the economic case for geometry-rich titanium components. As a result, titanium is becoming the material that most clearly changes the value mix inside the aircraft band clamp industry.

By Aircraft Type: Fixed-Wing Aircraft Anchor Demand While UAVs Expand Fastest

Fixed-wing aircraft accounted for 68.71% of revenue in 2025, keeping this platform group at the center of the aircraft band clamp market. Commercial narrowbody production drives the largest yearly clamp volume because those aircraft are built in much larger numbers than most other aviation platforms. Military fixed-wing programs add a higher-value layer because exhaust, hydraulic, and fuel-routing assemblies often require tighter qualification and more durable materials. General aviation contributes a smaller but steady requirement base, especially in airframe and ducting applications that depend on long approved product cycles. This combination makes fixed-wing aircraft the volume anchor for suppliers planning capacity, qualification spending, and material inventory.

UAVs are forecast to grow at 8.42% CAGR through 2031, making them the fastest-rising platform in the aircraft band clamp market. Their clamps differ from those in crewed aircraft because compact packaging, persistent vibration, and shorter replacement cycles matter more in smaller airframes. That gives nimble suppliers room to tailor products for battery systems, compact propulsion layouts, and dense electronics routing without competing only in the most mature categories. Rotorcraft continues to provide a stable middle layer of demand, supported in part by Airbus Helicopters reporting an order book of 1,060 units in Q1 2026. As military and commercial drone fleets expand, UAV-focused designs may become one of the clearest differentiation paths within the aircraft band clamp industry.

By Application: Airframe Assemblies Lead While Electrical Systems Gain Momentum

Airframe assemblies accounted for 38.32% of revenue in 2025, which gave them the broadest installation base in the aircraft band clamp market. These clamps appear across structural routing, duct support, and general fastening points on nearly every aircraft platform, which explains the segment’s scale. Engine components are considered a high-value application because heat resistance, vibration damping, and qualification depth increase the value of each approved part. Hydraulic and fuel systems also remain important because failure tolerance is low and operators depend on corrosion-resistant, fatigue-tested designs over long service lives. This spread across multiple subsystems helps the aircraft band clamp market remain resilient when one program area slows.

Electrical systems are projected to grow at 7.51% CAGR through 2031, and this slice of the overall market is being lifted by rising wiring-harness density on newer aircraft platforms. Fly-by-wire controls, advanced avionics, in-flight entertainment, and electrified propulsion all add cable runs that require secure routing and thermal separation. These needs become more demanding on hybrid-electric and eVTOL platforms, where high-voltage pathways require qualified retention systems and tighter heat management. The FAA and NAA Network roadmap for advanced air mobility certification highlighted hydrogen and hybrid-electric airworthiness work across 2026 and 2027, which supports earlier qualification activity around cable-management hardware. That shift should move more clamp value toward electrical architectures, even if airframe assemblies remain the largest application group through the forecast period.

By End-User: OEMs Dominate Current Spending While Aftermarket Growth Outruns The Total

OEMs accounted for 69.91% of revenue in 2025, so first-build demand remains the largest channel in the aircraft band clamp market. This position reflects strict approved-parts rules at Boeing, Airbus, and defense primes, where supplier entry depends on qualification depth and delivery consistency. Large assembly lines also provide predictable demand, which helps established suppliers plan production and negotiate longer supply agreements. Those agreements often run for 3-5 years, stabilizing revenue for incumbents and raising switching barriers for new entrants. As long as major airframers continue to push output higher, OEM demand will remain the foundation of the aircraft band clamp market.

Aftermarket demand is forecast to grow at a 6.77% CAGR through 2031, making it the fastest-growing end-user segment. IATA said supply chain bottlenecks continued to constrain airline fleet renewal in 2025, which supports longer service lives for existing aircraft and more recurring maintenance activity. That extends the addressable installed base for certified replacement clamps across engine, hydraulic, and ducting systems. Engine-focused maintenance is especially relevant because V-band clamps are concentrated in engine compartments, aligning a large product category with a growing service channel and giving the aftermarket an increasingly important role in the aircraft band clamp industry, even though OEMs continue to dominate total spending.

Geography Analysis

Asia-Pacific accounted for 34.45% of revenue in 2025 and is forecast to grow at a 7.16% CAGR through 2031, making it the region with both the largest share and the fastest growth in the aircraft band clamp market. China, India, Japan, and South Korea each support demand through distinct mixes of fleet growth, indigenous aerospace programs, supplier development, and MRO expansion. Japan adds industrial depth through its role in the aerostructures of the B787 program, while South Korea adds military demand through locally produced aircraft platforms. India is becoming increasingly relevant as airline growth and a rising local maintenance base drive greater certified component sourcing into the region. With OEM sourcing gradually shifting eastward, Asia-Pacific is likely to widen its lead in the aircraft band clamp market over the forecast period.

North America ranked second in 2025, supported by Boeing production and the scale of the US defense aviation base. The US FY2026 defense budget included 47 F-35s, 21 F-15EX Eagle IIs, and 15 KC-46A tankers, which keeps a strong pipeline of military-grade clamp demand across propulsion and airframe systems. Domestic policy also supports local supply by encouraging steel tariffs and defense sourcing rules that favor manufacturing close to program demand, giving North American suppliers an advantage in approved defense work, even as the Asia-Pacific region grows faster in the broader aircraft band clamp market.

Europe ranked third by revenue, anchored by Airbus production in Toulouse, Hamburg, and Broughton, and by rising NATO defense spending. Airbus guided for around 870 commercial aircraft deliveries in 2026 and reported a helicopter order book of 1,060 units in Q1 2026, which sustains a broad regional demand base. South America remains smaller but benefits from Embraer-linked activity, while the Middle East and Africa are building local demand through MRO investment and broader aerospace ambitions. Turkey also adds an emerging opportunity set as domestic aircraft programs raise the need for locally qualified component supply.

Competitive Landscape

The aircraft band clamp market shows moderate concentration, with the top 5-6 players accounting for 45%-55% of global revenue, and no single company holding more than 20%. That structure keeps pricing disciplined while still leaving room for product differentiation, certification strength, and customer-specific engineering. The leading group combines diversified aerospace suppliers, such as Parker-Hannifin and Eaton, with more specialized clamp manufacturers, such as NORMA Group, Clampco Products, and Oetiker Group. Scale matters because approved-vendor status, testing capability, and material access create entry barriers that smaller entrants struggle to match quickly. At the same time, the long tail of regional suppliers keeps the aircraft band clamp market from becoming tightly consolidated.

Howmet Aerospace made the clearest consolidation move in 2026, completing the USD 1.8 billion acquisition of Consolidated Aerospace Manufacturing in April 2026 and adding Brunner Manufacturing in February 2026 for nearly USD 120 million. These transactions deepen Howmet’s position in fastening and adjacent fluid-fitting categories, potentially improving access to airframe assembly programs where clamp procurement is often linked to related hardware. NORMA Group also reshaped its portfolio in February 2026 by selling its Water Management business. Together, these actions show that strategic positioning in the aircraft band clamp market is increasingly driven by both acquisitions and portfolio refocus.

Competition below the top tier is centered on material innovation, application-specific geometry, and faster response to new platform requirements. UAV-related designs, electrical-routing clamps, and lightweight titanium variants represent the clearest opportunities for mid-tier suppliers seeking to avoid direct price competition in mature product lines. Eaton benefits from a broad aerospace presence in duct, anti-ice, and environmental control applications. At the same time, Parker-Hannifin can strengthen customer retention by supplying clamps as part of larger system packages, rendering the aircraft band clamp market active rather than fragmented, with incumbents holding meaningful advantages but not enough control to close off new niche competition.

Aircraft Band Clamp Industry Leaders

Parker-Hannifin Corporation

Eaton Corporation plc

Oetiker Group

Clampco Products, Inc.

NORMA Group SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Howmet Aerospace acquired Consolidated Aerospace Manufacturing, LLC (CAM) from Stanley Black & Decker for about USD 1.8 billion. This move integrated CAM's precision fasteners and fluid-fitting portfolio, which includes products adjacent to aerospace clamps, into Howmet's Fastening Systems segment.

- March 2026: The ICAO Council adopted a new CO2 emissions standard, tightening limits by 10% for new large aircraft designs. Set to take effect on August 3, 2026, this move underscores the growing emphasis on lightweight aerospace components, such as titanium-alloy band clamps.

- January 2026: Airbus SE began integrating wire-directed energy deposition (w-DED) titanium parts into the A350 Cargo Door Surround. This marked the inaugural industrial-scale application of additive-manufactured structural titanium in a commercially produced aircraft, signifying ramifications for titanium clamp procurement strategies.

Global Aircraft Band Clamp Market Report Scope

Aircraft band clamps are specialized metallic fastening devices. These clamps are adept at joining and securing cylindrical components, including pipes, tubes, exhaust systems, and ducts. Valued for their high structural strength and vibration resistance, these lightweight clamps also offer quick installation.

The aircraft band clamp market is segmented by clamp type, material, aircraft type, application, end-user, and geography. By clamp type, the market is segmented into V-band clamps, T-bolt band clamps, worm-drive band clamps, cradle support latch clamps, and other band clamps. By material, the market is segmented into stainless steel, titanium, aluminum alloys, nickel, and others. By aircraft type, the market is segmented into fixed-wing aircraft, rotorcraft, and unmanned aerial vehicles (UAVs). By application, the market is segmented into airframe assemblies, engine components, hydraulic systems, fuel systems, and electrical systems. By end-user, the market is segmented into original equipment manufacturer (OEM) and aftermarket. The report also covers the market sizes and forecasts in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| V-band Clamps |

| T-bolt Band Clamps |

| Worm-Drive Band Clamps |

| Cradle Support Latch Clamp |

| Other Band Clamps |

| Stainless Steel |

| Titanium |

| Aluminum Alloys |

| Nickel |

| Others |

| Fixed-Wing Aircraft | Commercial Aviation | Narrowbody |

| Widebody | ||

| Regional Jets | ||

| Military Aviation | Fighter Jets | |

| Transport Aircraft | ||

| Special Mission Aircraft | ||

| General Aviation | Business Jet | |

| Piston and Turbofan Aircraft | ||

| Rotorcraft | Civil Helicopters | |

| Military Helicopters | ||

| Unmanned Aerial Vehicles (UAVs) | ||

| Airframe Assemblies |

| Engine Components |

| Hydraulic Systems |

| Fuel Systems |

| Electrical Systems |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Clamp Type | V-band Clamps | ||

| T-bolt Band Clamps | |||

| Worm-Drive Band Clamps | |||

| Cradle Support Latch Clamp | |||

| Other Band Clamps | |||

| By Material | Stainless Steel | ||

| Titanium | |||

| Aluminum Alloys | |||

| Nickel | |||

| Others | |||

| By Aircraft Type | Fixed-Wing Aircraft | Commercial Aviation | Narrowbody |

| Widebody | |||

| Regional Jets | |||

| Military Aviation | Fighter Jets | ||

| Transport Aircraft | |||

| Special Mission Aircraft | |||

| General Aviation | Business Jet | ||

| Piston and Turbofan Aircraft | |||

| Rotorcraft | Civil Helicopters | ||

| Military Helicopters | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| By Application | Airframe Assemblies | ||

| Engine Components | |||

| Hydraulic Systems | |||

| Fuel Systems | |||

| Electrical Systems | |||

| By End-User | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the outlook for aircraft band clamps through 2031?

The aircraft band clamp market size is expected to grow from USD 253.23 million in 2025 to USD 267.44 million in 2026 and is forecast to reach USD 349.89 million by 2031 at 5.52% CAGR over 2026-2031.

Which clamp type is leading current demand?

V-band clamps led with 35.21% share in 2025 because they are widely used in engine exhaust ducts, bleed-air systems, and APU connections.

Why is titanium gaining more attention in aircraft hardware?

Titanium is forecast to grow at 7.22% CAGR because aircraft builders are under pressure to lower weight and improve fuel efficiency while maintaining strength and thermal performance.

Which region offers the strongest growth potential?

Asia-Pacific leads both on scale and growth, with 34.45% share in 2025 and a 7.16% CAGR through 2031, supported by fleet expansion and rising regional MRO capability.

How important is aftermarket demand for suppliers?

It is becoming more important because aftermarket demand is projected to grow at 6.77% CAGR, helped by an older global fleet and slower normalization in aircraft renewal.

How concentrated is competition among suppliers?

Competition is moderate, with the top 5 to 6 companies holding 45% to 55% of global revenue, which gives incumbents scale advantages but still leaves room for niche specialists.

Page last updated on: