Aircraft Fire Protection Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

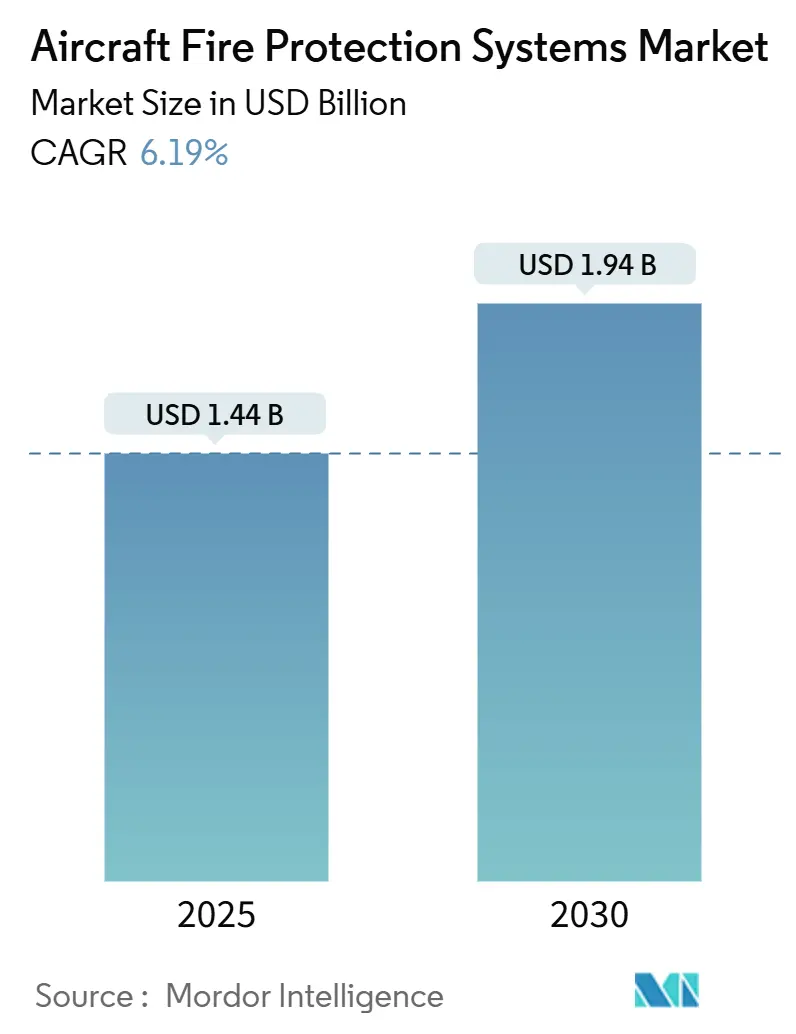

| Market Size (2025) | USD 1.44 Billion |

| Market Size (2030) | USD 1.94 Billion |

| Growth Rate (2025 - 2030) | 6.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

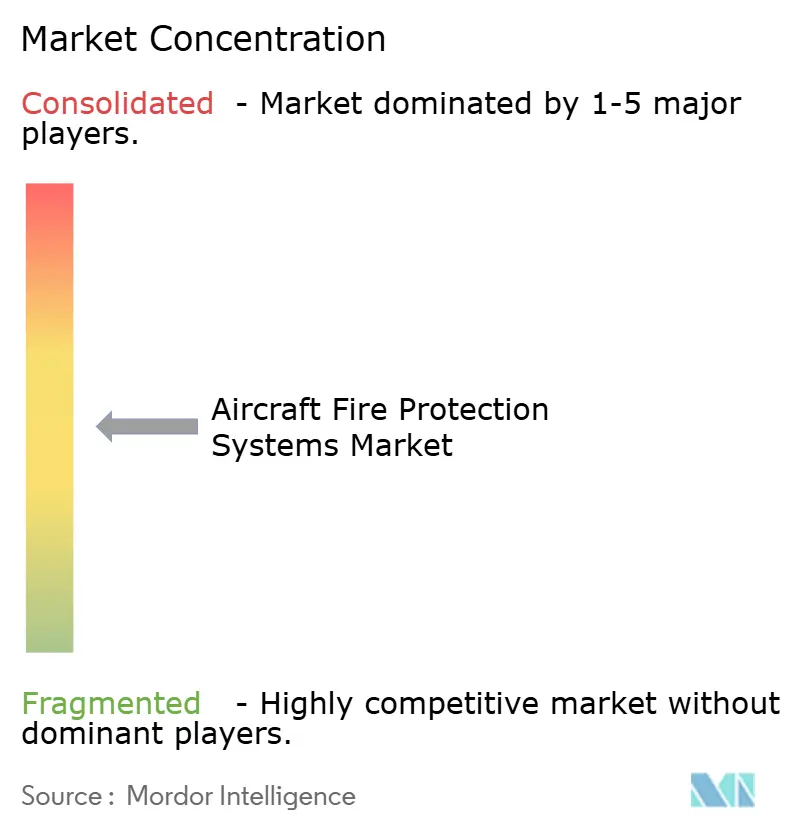

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Fire Protection Systems Market Analysis by Mordor Intelligence

The aircraft fire protection systems market size is estimated at USD 1.44 billion in 2025. It is expected to reach USD 1.94 billion by 2030, at a CAGR of 6.19% during the forecast period. The growth reflects stricter ICAO and FAA regulations, rising commercial aircraft production, and the industry-wide switch to halon-free suppression agents. Cargo operators are accelerating upgrades to mitigate lithium-battery thermal runaway, while OEMs integrate lightweight detection networks into next-generation composites. Suppliers that deliver predictive health-monitoring sensors, miniaturized cylinders, and eco-friendly agents are best positioned to capture this expanding opportunity. Competitive intensity centers on weight optimization, agent certification, and digital diagnostics as fleet operators demand higher safety with lower lifecycle costs.

Key Report Takeaways

- By product type, fire detection systems led with 41.35% of the aircraft fire protection systems market share in 2024. Fire suppression systems are forecast to expand by 8.35% CAGR through 2030.

- By aircraft type, commercial aircraft commanded a 68.56% share of the aircraft fire protection systems market size in 2024. Urban air mobility (UAM) platforms are advancing at a 7.23% CAGR by 2030.

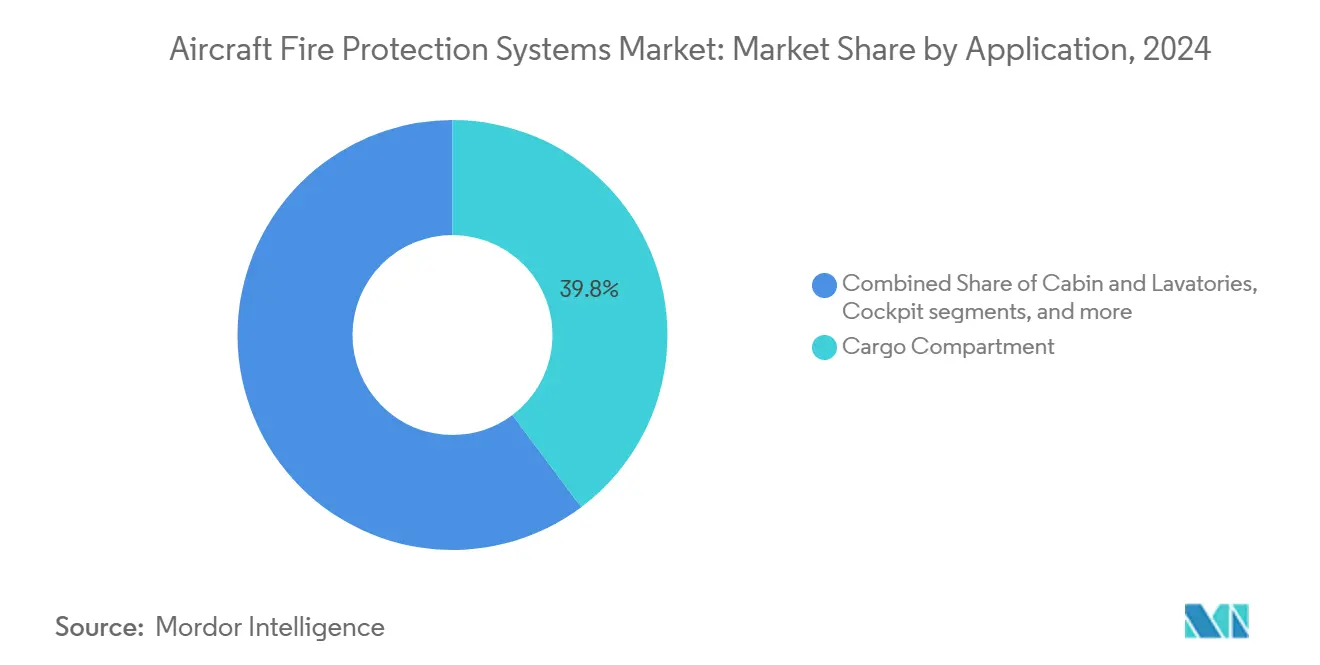

- By application, cargo compartments accounted for a 39.78% share of the aircraft fire protection systems market size in 2024. Wheel well and landing gear installations are set to grow at a 6.15% CAGR through 2030.

- By end user, OEM linefit held 61.45% of the aircraft fire protection systems market share in 2024. Aftermarket retrofit and MRO activities are registering a 7.56% CAGR to 2030.

- North America retained the largest regional share, at 39.57%, in 2024, whereas the Asia-Pacific is pacing ahead at an 8.12% CAGR.

Global Aircraft Fire Protection Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Necessity to comply with stringent ICAO and FAA fire-safety regulations | +1.2% | North America and Europe | Long term (≥ 4 years) |

| Rising production rates for next-gen fuel-efficient commercial aircraft | +1.8% | Global core regions | Medium term (2-4 years) |

| Higher incidence of lithium-battery thermal runaway events in cargo holds | +0.9% | Cargo-heavy routes | Short term (≤ 2 years) |

| Shift toward halon-free and eco-friendly suppression agents (e.g., HFO-1233zd) | +0.7% | EU-driven | Medium term (2-4 years) |

| Adoption of predictive health-monitoring sensors for early fire detection in composite fuselages | +0.6% | Advanced markets | Long term (≥ 4 years) |

| Growth of urban air mobility (UAM) platforms requiring lightweight fire protection | +0.3% | Urban hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Necessity to comply with stringent ICAO and FAA fire-safety regulations

Global regulators have tightened fire-safety mandates after several cargo events. ICAO Annex 6 now requires enhanced lithium battery detection, while FAA Advisory Circular 25.851-1 trims allowed suppression response time to 60 seconds.[1]International Civil Aviation Organization, “Standards and Recommended Practices – Annex 6,” icao.int Transport Canada mirrored these steps, extending rules to regional aircraft. Performance-based certification encourages suppliers to introduce multi-sensor arrays and predictive analytics that spot thermal anomalies early. Demand peaks among freighter operators that handle dense battery shipments and must meet the new standards without adding downtime.

Rising production rates for next-gen fuel-efficient commercial aircraft

Boeing’s B737 MAX production ramp-up and the Dreamliner’s composite fuselage have boosted orders for integrated fire protection solutions.[2]Boeing Company, “737 MAX Production and Delivery Updates,” boeing.com Airbus A350 and A320neo lines follow similar trajectories, and each airframe relies on HFO-1233zd suppression to replace halon bottles. Higher-temperature engines also push up requirements for engine-bay detection, promoting fiber-optic sensing and thermal-resistant wiring. OEMs seek mass-reduced cylinders and distributed sensor nodes that slot neatly into space-constrained architectures.

Higher incidence of lithium-battery thermal runaway events in cargo holds

FAA data show that lithium battery events have risen 340% since 2019, with temperatures topping 1,000 °C and toxic gases released.[3]Federal Aviation Administration, “Lithium Battery Incident Reports and Safety Recommendations,” faa.gov Operators specify multispectral infrared detectors that recognize runaway signatures before flames appear. Hybrid nitrogen-water and aerosol systems capable of extended cooling cycles are increasingly selected because halon alternatives lose effectiveness against lithium cells. As a result, most widebody freighters on trans-Pacific routes include double-redundant suppression for class C holds.

Shift toward halon-free and eco-friendly suppression agents

The EU F-gas regulation phases out high-GWP substances by 2030, propelling the adoption of HFO-1233zd and Novec 1230.[4]European Commission, “Regulation on Fluorinated Greenhouse Gases,” ec.europa.eu Although Novec carries a premium price, its rapid evaporation suits hot engine zones. Certification processes are lengthy, requiring proof that new agents equal halon performance across altitudes and cabin pressures. Firms are investing in pressure-regulated manifolds that dispense lower agent volumes yet sustain extinguishing concentration, trimming bottle mass by up to 30%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weight and space penalties restraining adoption in regional jets | −0.8% | Global, particularly affecting regional carriers in emerging markets | Medium term (2-4 years) |

| Volatility in raw-material prices for advanced sensors and cylinders | −0.5% | Global, with supply-chain concentration in Asia-Pacific | Short term (≤ 2 years) |

| Certification delays due to evolving environmental rules on fluorinated gases | −0.4% | Global, with strongest influence in Europe and North America | Medium term (2-4 years) |

| Limited retrofit demand amid airline cash-flow pressures post-pandemic | −0.3% | Global, most acute among cost-sensitive carriers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Weight and space penalties restraining adoption in regional jets

Advanced systems add 15-25 kg per installation, a notable burden for Embraer E-Jets and CRJ variants that operate tight payload envelopes. Cargo bays in regional types leave little room for suppression cylinders, and airlines favor revenue upgrades over safety kits if weight cuts seat or freight capacity. Composite fuselage variants introduce more monitoring points, further stressing cabin real estate.

Volatility in raw-material prices for advanced sensors and cylinders

Antimony trioxide costs climbed 180% in 2024, pushing up flame-retardant additives. Titanium and specialty steels for high-pressure bottles followed similar spikes. Semiconductor shortages lengthened lead times for infrared arrays, and fiber-optic cores drew premiums. Mid-tier suppliers struggle to absorb these swings, while airframers hesitate to lock in multi-year component contracts, delaying some retrofit projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Detection systems lead despite suppression growth

Fire detection systems held a 41.35% share in 2024, making them the largest slice of the aircraft fire protection systems market. Optical smoke detectors, infrared scanners, and multi-sensor nodes form the backbone of every commercial and military platform. Demand remains steady because regulators mandate redundancy across cabins, cargo holds, and engine bays. The aircraft fire protection systems market size attributed to suppression systems is rising as operators insist on active containment. Cylinders with HFO-1233zd agents, hybrid nitrogen-water sprayers, and micro-aerosol cartridges underpin the 8.35% CAGR forecast. Suppliers combine predictive algorithms and sensor fusion, resulting in integrated control units that self-diagnose faults and schedule maintenance. Advancements such as wireless cabin alert modules and voice warnings support crew situational awareness, reducing evacuation time.

The near-term innovation frontier involves embedding fiber Bragg gratings into composites, enabling simultaneous structural-health and fire detection. AI-driven algorithms label thermal patterns and trigger early alerts, thus preventing full ignition events. Integration with avionics allows direct relay of anomaly data to airline operations centers, improving decision-making on diversion versus continuation. IoT connectivity gives MRO teams access to live health dashboards, promoting planned replacement over reactive fixes and cutting unscheduled costs.

By Aircraft Type: Commercial dominance meets eVTOL innovation

Commercial airframes accounted for a 68.56% share in 2024, deriving strength from Airbus and Boeing backlogs. These fleets require scalable detection and suppression solutions that span narrowbody, widebody, and freighter variants. Although smaller in volume, military platforms demand ruggedized systems resistant to vibration, shock, and electronic warfare (EW). General aviation and rotorcraft operators look for mass-optimized kits that slot into limited bays without structural re-engineering.

UAM vehicles represent the fastest-growing slice at 7.23% CAGR. Certification bodies are drafting fresh guidelines to tackle high-energy battery packs and distributed electric propulsion, introducing multiple ignition sources. Suppliers develop canister-based suppression lines embedded within battery enclosures that discharge inert agents when cell temperatures climb. Miniaturized optical sensors mount directly above motor nacelles, spotting arcing or overheating. The aircraft fire protection systems market size for eVTOL remains modest today. Yet, volume ramps sharply as pilotless cargo drones and air taxis move into commercial service later in the decade.

By Application: Cargo concerns drive wheel well innovation

Cargo compartments represented 39.78% of revenue in 2024. The lithium-battery freight surge forces operators to install early-alert detectors using multispectral IR and gas-sampling technology. Hybrid suppression systems capable of long-duration cooling cycles prevail because lithium cells can reignite after initial knockdown. Engine and APU zones maintain stable demand, amplified by hotter core temperatures in high-bypass turbofans.

Once peripheral, wheel well and landing gear bays are now the fastest-expanding niche at 6.15% CAGR. Composite gear doors and hydraulic lines elevate fire risk, and operators fit thermochromic paint strips plus point temperature detectors that feed cockpit alerts. Visual indicators assist ground crews in spotting hot spots on turnarounds, cutting incident probability. Fuel tank and wing structures employ distributed fiber-optic loops, allowing real-time insights into heat signatures during lightning strikes and refuel cycles.

By End User: OEM integration leads aftermarket growth

OEM linefit captured 61.45% share in 2024 because integrated solutions ship with new B737 MAX, A320neo, and E-Jet airframes. Airframers prefer single-supplier packages covering detection, suppression, and alert functions, simplifying certification and logistics. Digital integration enhances data flow to onboard maintenance computers, enabling condition-based maintenance from entry into service.

Retrofit and MRO services grow at a 7.56% CAGR. Airlines are under regulatory pressure to upgrade older cargo facilities for lithium battery compliance. Modular line-replaceable units facilitate overnight hangar installations, mitigating downtime. FAA guidance on class E cargo holds has sparked retroactive orders for temperature-controlled containers and dual-agent suppression kits. In business aviation, owners invest in wireless detection nodes to align with steep insurance requirements and to protect valuable interiors.

Geography Analysis

North America retained a 39.57% share in 2024, benefiting from Boeing production and a strict FAA rule environment. Collins Aerospace and Safran maintain extensive US manufacturing and MRO centers, ensuring supply continuity. Canada’s Bombardier linefit orders and Mexico’s tier-2 parts ecosystem further support the regional base. Programs such as Lockheed Martin’s tanker upgrades also incorporate next-gen fire-protection retrofits.

Asia-Pacific advances at an 8.12% CAGR as COMAC C919 and ARJ21 output rises, creating domestic demand for localized systems. India’s Make-in-India aerospace push lures tier-1 suppliers to set up cylinder forging and sensor electronics lines. Japanese sensor specialists feed advanced infrared arrays into regional supply chains. Airlines across China and Southeast Asia expand cargo routes, heightening retrofit orders for lithium battery compliance.

Europe balances the field with stringent EASA oversight and environmental leadership. The F-gas phase-down accelerates HFO-1233zd adoption, and Airbus taps EU research funds to reduce suppression bottle mass. Safran’s acquisition of Preligens augments AI-based detection, positioning the firm firmly with European carriers.

The Middle East orders new widebodies for fleet renewal, typically linefitting comprehensive systems at OEMs. Africa and South America adopt upgrades more gradually, constrained by budget but prodded by cargo safety mandates.

Competitive Landscape

Competitive Landscape

Market concentration is moderate. Collins Aerospace, Meggitt, and Safran control over 45% of 2024 revenue. Collins delivers broad portfolios that bundle detectors, bottles, and cockpit annunciators, leveraging scale across civil and defense programs. Meggitt pioneers high-temp engine zones with ceramic-insulated loops that tolerate 1,200 °C. Safran invests in AI algorithms post-Preligens acquisition, enabling predictive analytics layered on sensor data.

Strategic moves include vertical integration. RTX brought bottle machining in-house to secure a titanium supply, while Meggitt established a fiber-optic core plant to curb semiconductor risk. Partnerships with eVTOL developers such as JetZero give incumbents an early foothold in emerging platforms. Patent filings emphasize distributed detection and agent dispersion optimization. Startups focus on battery-pack suppression micro-capsules, a gap for legacy suppliers.

Pricing pressure arises from raw-material volatility. Larger firms hedge metals exposure, whereas smaller players cede share on cost swings. Eco-friendly agent approval timelines create barriers; only suppliers with extensive certification labs can iterate rapidly. Service offerings grow as airlines demand predictive maintenance dashboards delivered via secure cloud links, driving software revenue alongside hardware.

Aircraft Fire Protection Systems Industry Leaders

Siemens AG

Collins Aerospace (RTX Corporation)

Safran SA

Diehl Stiftung & Co. KG

Meggitt Ltd. (Parker-Hannifin Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The US Secretary of Agriculture officially signed a new five-year contract with Perimeter Solutions to supply domestically produced fire retardants. This agreement supports the aerial wildland fire suppression initiatives of the US Forest Service and the Department of the Interior.

- March 2023: H3R Aviation announced the availability of fire extinguishers and mounting solutions designed for fixed-wing and rotary-wing aircraft of various types and sizes. Their recently launched Halotron BrX fire extinguishers utilize halon-alternative agents that comply with industry standards.

Global Aircraft Fire Protection Systems Market Report Scope

A fire protection system is installed onboard an aircraft to extinguish or control the spread of fire and minimize the extent of damage caused to critical systems, which may result in a catastrophic failure.

The aircraft fire protection system market is segmented based on type, aircraft type, application, and geography. By type, the market is segmented into fire detection systems, alarm and warning systems, and fire suppression systems. By aircraft type, the market is divided into commercial aircraft, military aircraft, and general aviation aircraft. By application, the market is classified into cabin and lavatories, cockpit, cargo compartment, and engine and APU. The report also covers the market sizes and forecasts for the aircraft fire protection systems market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Fire Detection Systems | Smoke Detectors |

| Optical/Infrared Detectors | |

| Thermal Detectors | |

| Multi-sensor Detectors | |

| Alarm and Warning Systems | Aural Warning Devices (Buzzers, Horns) |

| Visual Indicator Panels (LED/Lighted Annunciators) | |

| Master Caution/Warning Annunciator Panels | |

| Integrated Voice Alerting Systems (3D/Directional Audio) | |

| Centralized Warning Control Units (ECAM/EICAS) | |

| Wireless Cabin Alert Modules (eVTOL/UAM) | |

| Fire Suppression Systems | Gaseous Agent Systems |

| Liquid Agent Systems | |

| Dry-Chemical Systems | |

| Aerosol-based Systems | |

| Hybrid Nitrogen-Water Systems | |

| Portable/Handheld Extinguishers |

| Commercial Aircraft |

| Military Aircraft |

| General Aviation |

| Helicopters |

| Urban Air Mobility (UAM) |

| Cabin and Lavatories |

| Cockpit |

| Cargo Compartment |

| Engine and Auxiliary Power Unit (APU) |

| Wheel Well and Landing Gear |

| Fuel Tanks and Wings |

| OEM Linefit |

| Aftermarket Retrofit and MRO |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Product Type | Fire Detection Systems | Smoke Detectors | |

| Optical/Infrared Detectors | |||

| Thermal Detectors | |||

| Multi-sensor Detectors | |||

| Alarm and Warning Systems | Aural Warning Devices (Buzzers, Horns) | ||

| Visual Indicator Panels (LED/Lighted Annunciators) | |||

| Master Caution/Warning Annunciator Panels | |||

| Integrated Voice Alerting Systems (3D/Directional Audio) | |||

| Centralized Warning Control Units (ECAM/EICAS) | |||

| Wireless Cabin Alert Modules (eVTOL/UAM) | |||

| Fire Suppression Systems | Gaseous Agent Systems | ||

| Liquid Agent Systems | |||

| Dry-Chemical Systems | |||

| Aerosol-based Systems | |||

| Hybrid Nitrogen-Water Systems | |||

| Portable/Handheld Extinguishers | |||

| By Aircraft Type | Commercial Aircraft | ||

| Military Aircraft | |||

| General Aviation | |||

| Helicopters | |||

| Urban Air Mobility (UAM) | |||

| By Application | Cabin and Lavatories | ||

| Cockpit | |||

| Cargo Compartment | |||

| Engine and Auxiliary Power Unit (APU) | |||

| Wheel Well and Landing Gear | |||

| Fuel Tanks and Wings | |||

| By End User | OEM Linefit | ||

| Aftermarket Retrofit and MRO | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the forecast size of the aircraft fire protection systems market by 2030?

The aircraft fire protection systems market is projected to reach USD 1.94 billion, reflecting a 6.19% CAGR from 2025.

Which product category currently holds the largest share?

Fire detection systems led with 41.35% share in 2024.

Which aircraft segment is growing the fastest?

UAM platforms are advancing at a 7.23% CAGR through 2030.

Why are cargo compartment systems in high demand?

Lithium-battery thermal-runaway incidents have risen sharply, prompting operators to install advanced detection and hybrid suppression solutions.

What region is expected to record the highest growth rate?

Asia-Pacific is set to expand at an 8.12% CAGR, driven by rising fleet sizes and local manufacturing programs.

How are OEMs lowering system weight?

They deploy miniaturized sensors, pressure-regulated manifolds, and HFO-1233zd agent bottles that together reduce mass without sacrificing performance.

Page last updated on: