Aircraft Cabin Trash Compactors Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

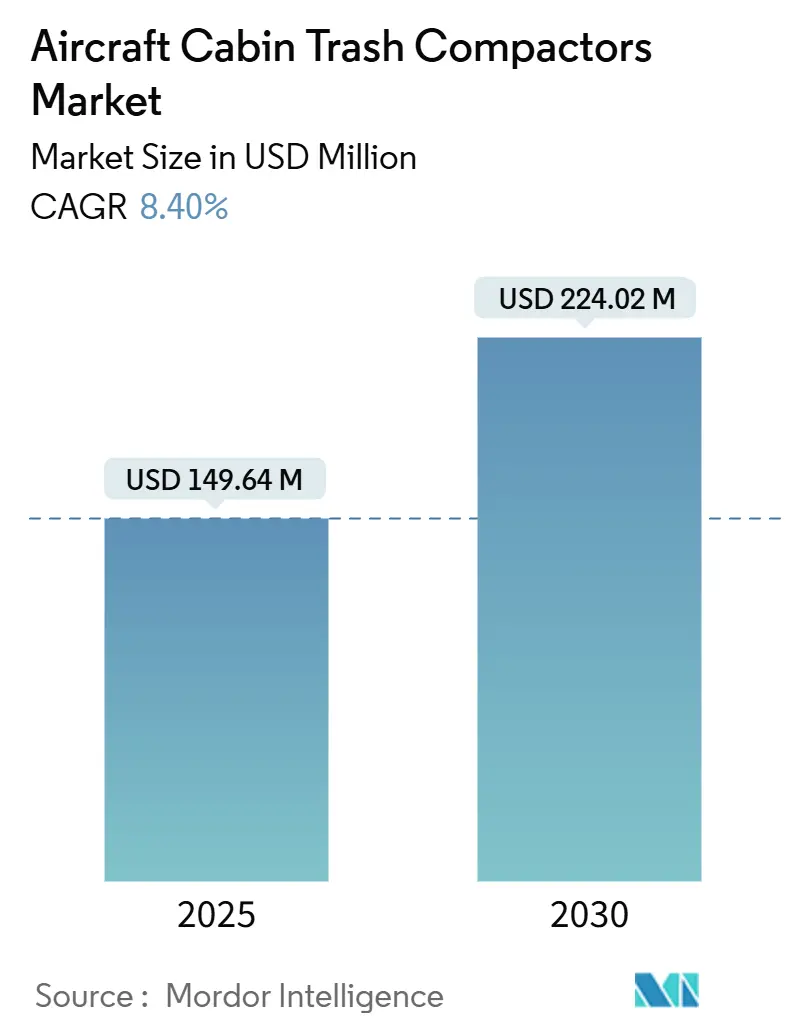

| Market Size (2025) | USD 149.64 Million |

| Market Size (2030) | USD 224.02 Million |

| Growth Rate (2025 - 2030) | 8.40% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Cabin Trash Compactors Market Analysis by Mordor Intelligence

The aircraft cabin trash compactors market size is USD 149.64 million in 2025 and is forecasted to reach USD 224.02 million by 2030, registering an 8.40% CAGR. Airlines continue to embed waste compaction into cabin upgrade programs because the systems save space, cut turnaround times, and support sustainability commitments. Retrofit activity is gaining momentum as carriers delay new-build deliveries, yet cabins still need to be aligned with stricter environmental regulations. Suppliers that demonstrate measurable fuel-burn reductions through lighter, energy-efficient designs gain preference, particularly on high-frequency narrowbody routes. Geopolitically driven fleet renewal in North America and rapid LCC expansion in Asia-Pacific keep order backlogs healthy, while tightening certification rules push manufacturers toward modular platforms that streamline multi-agency approvals. Competition, therefore, centers on integration capabilities rather than unit price, with smart sensors and predictive analytics turning trash management into another node in connected-cabin ecosystems.

Key Report Takeaways

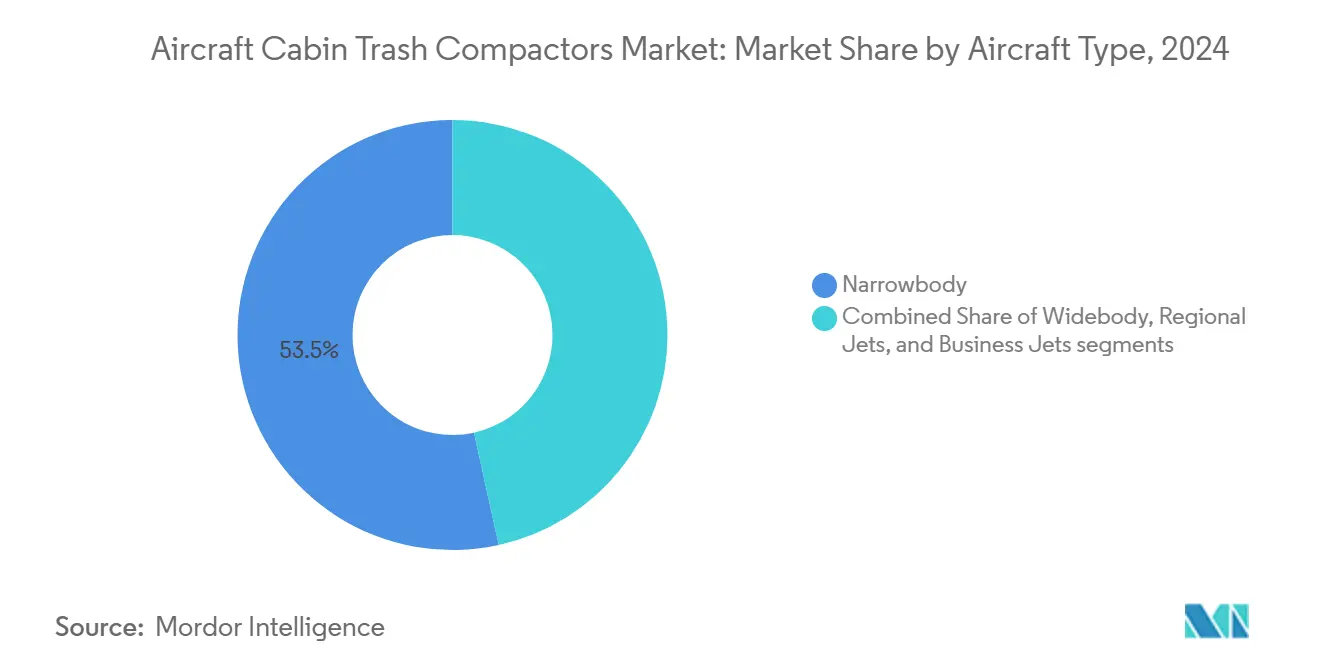

- By aircraft type, narrowbody aircraft led with 53.45% of the aircraft cabin trash compactors market share in 2024, while regional jets recorded the highest 9.53% CAGR through 2030.

- By installation location, galley systems commanded a 56.24% share of the aircraft cabin trash compactors market size in 2024 and are projected to expand at an 8.92% CAGR to 2030.

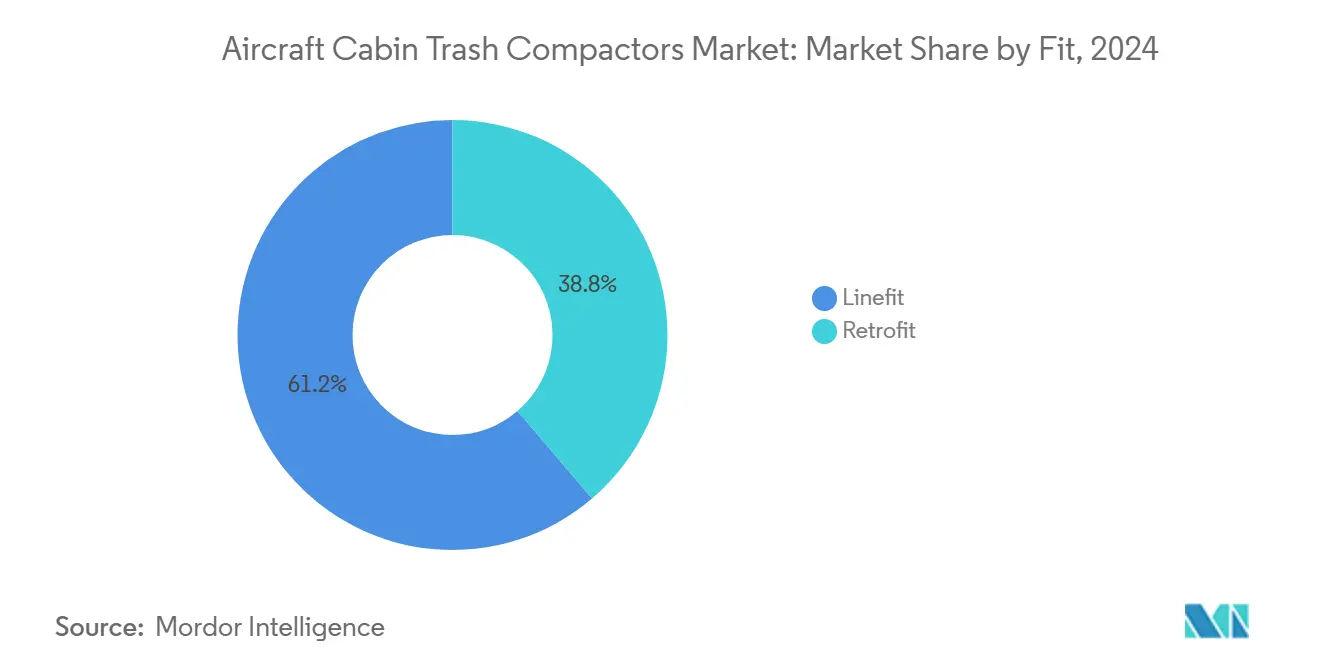

- By fit, linefit installations accounted for 61.24% of the aircraft cabin trash compactors market size in 2024, whereas retrofit applications posted the strongest 9.47% CAGR through 2030.

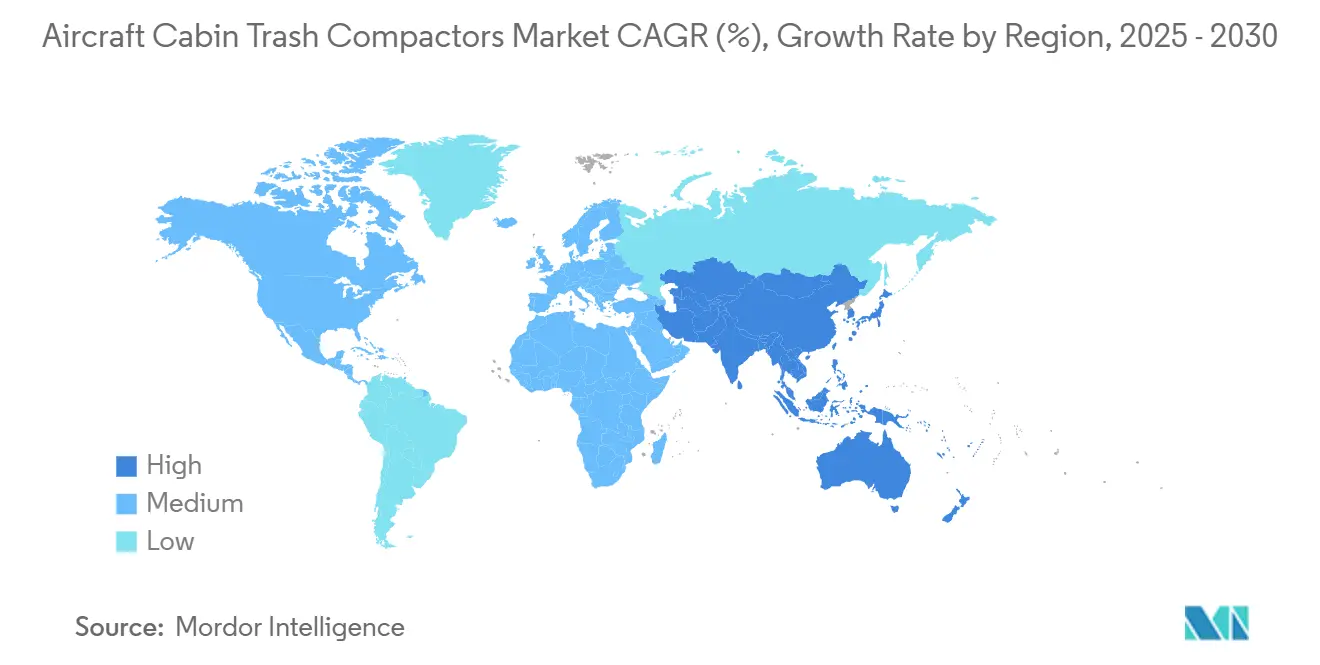

- By geography, North America held 32.67% of the aircraft cabin trash compactors market share in 2024, while Asia-Pacific is advancing at an 8.90% CAGR through 2030.

Global Aircraft Cabin Trash Compactors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating global air passenger growth and fleet expansion | +1.5% | Global; highest in Asia-Pacific and Middle East | Medium term (2 – 4 years) |

| Rising emphasis on in-flight sustainability and waste reduction | +1.3% | North America and EU leading; expanding to Asia-Pacific | Long term (≥ 4 years) |

| Strengthening international aviation regulations on cabin waste management | +1.2% | Global, with EASA and FAA precedents | Short term (≤ 2 years) |

| Increased retrofit demand for waste management in narrowbody fleets | +1.1% | North America and EU core; emerging markets next | Medium term (2 – 4 years) |

| Adoption of lightweight, energy-efficient compaction technologies | +0.9% | Global; early uptake by premium carriers | Medium term (2 – 4 years) |

| Integration of smart waste systems for enhanced operational efficiency | +0.8% | North America and EU first; Asia-Pacific following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Global Air Passenger Growth and Fleet Expansion

Airframe makers forecast more than 44,000 aircraft deliveries over the next two decades, keeping the aircraft cabin trash compactors market on a steady expansion path. Carriers that open secondary city-pairs rely on efficient cabin waste handling when ground support is limited, making compactors standard even on 100-seat regional jets. Higher passenger load factors on long-haul services intensify trash volumes, so airlines install multiple units to avoid mid-flight storage bottlenecks. Frequent short-haul operators view compaction as a route to faster turns because fewer waste bags need offloading, reducing the chance of departure delays. These operational gains reinforce procurement decisions despite persistent capital cost pressures.

Rising Emphasis on In-Flight Sustainability and Waste Reduction

Airlines generated 6.7 million tons of cabin waste in 2024, and boards now link waste minimization to corporate ESG targets. Galley compactors cut bag count and help carriers segregate food, plastics, and liquids for proper disposal under the EU Circular Economy Action Plan, strengthening compliance credibility with regulators. Lufthansa’s smart waste tracking program showed measurable volume cuts after introducing sensor-equipped units that guide crew on optimal compression timing.[1]Lufthansa Group, “Waste Management and Sustainability,” lufthansagroup.com Such results set competitive benchmarks, nudging peer airlines toward compaction upgrades. Passenger perception also matters; visible sustainability measures increasingly sway traveler loyalty on high-yield routes.

Strengthening International Aviation Regulations on Cabin Waste Management

ICAO’s Committee on Aviation Environmental Protection is drafting new cabin waste guidelines that explicitly reference onboard compaction as a best-practice method.[2] International Civil Aviation Organization, “Environmental Protection,” icao.int EASA has issued advice on in-cabin segregation, and FAA fire-safety updates favor self-contained units with integrated suppression. Compliance needs push airlines to specify certified equipment during cabin refits, shortening supplier shortlists to firms with robust regulatory portfolios. Smaller manufacturers seek partnerships with established integrators to share documentation costs, shaping a tiered supply structure within the aircraft cabin trash compactors market.

Increased Retrofit Demand for Waste Management in Narrowbody Fleets

Retrofit programs such as Air India’s USD 400 million cabin overhaul illustrate how carriers extend asset life while bringing interiors to modern sustainability standards.[3]Air India, “Fleet Modernization Program,” airindia.in Supplemental Type Certificate pathways are faster than line-fit approvals so that airlines can add compactors during scheduled C-checks without long ground time. Operators of mixed fleets value retrofit kits that standardize waste handling across aircraft types, improving crew familiarity and simplifying spare-part inventories. This retrofit boom lifts aftermarket revenues for suppliers and MROs, enlarging the aircraft cabin trash compactors market beyond OEM production cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High certification and compliance costs for cabin equipment suppliers | −0.7% | Global; highest impact in emerging markets | Short term (≤ 2 years) |

| Limited space availability in aircraft galley and lavatory zones | −0.6% | Global; acute on narrowbody aircraft | Medium term (2 – 4 years) |

| Capital expenditure prioritization toward revenue-generating cabin systems | −0.5% | Global; more pronounced among LCCs | Medium term (2 – 4 years) |

| Operational challenges in onboard waste sorting and segregation | −0.4% | Global; crew training varies by region | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Certification and Compliance Costs for Cabin Equipment Suppliers

An AS9100 approval dossier can exceed USD 2 million per aircraft type, and suppliers contend with parallel FAA and EASA test regimes that stretch program timelines. Rising European regulatory fees add to the burden, squeezing smaller innovators from bidding rounds. To stay viable, niche firms often align with major cabin integrators for joint certifications, trading some margin for market access. This cost reality concentrates share among incumbents and moderates the growth achievable by new entrants in the aircraft cabin trash compactors market.

Limited Space Availability in Aircraft Galley and Lavatory Zones

Galleys juggle ovens, chillers, and trolley stowage, leaving minimal real estate for additional hardware. Designers must weigh waste compaction against ancillary revenue fixtures such as premium-seat mini-bars on densified single-aisle layouts. Suppliers answer with modular footprints and under-counter units, but real estate tensions persist, especially on 30-inch pitch layouts standard with LCCs. This constraint tempers unit-per-aircraft penetration rates despite rising regulatory pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Regional Jets Drive Compactor Innovation

Regional jets contributed a 9.53% CAGR to the aircraft cabin trash compactors market between 2025 and 2030, even though narrowbody aircraft held a 53.45% share in 2024. Larger 100-to-150-seat regional platforms now operate trunk routes once dominated by mainline jets, so operators demand the same waste management sophistication found on narrowbodies. Narrowbody programs still underpin volume deliveries, and their high daily utilization amplifies the cost-saving benefits of onboard compaction.

Regional jet cabin layouts impose tighter volumetric constraints, spurring suppliers to develop lighter, vertically oriented compressors that tuck beside service trolleys without blocking workflow. Some operators install dual-chamber units to separate recyclable plastics from catering residues, supporting national recycling mandates in markets such as Japan and South Korea. Widebody installations remain concentrated in premium galley zones where frequent trolley exchanges justify larger-capacity compactors. Business jets represent a niche that values ultra-lightweight builds, and prototypes with carbon-fiber skins have shaved several kilograms relative to legacy aluminum housings, resonating with charter firms chasing range extensions.

By Installation Location: Galley Systems Dominate Growth

Galley-mounted units captured 56.24% of the aircraft cabin trash compactors market share in 2024 and are forecast to grow 8.92% annually through 2030. Their dominance stems from the galley’s role as the primary origin point for solid waste. High-capacity compressors integrated into service columns can handle mixed waste from both aisles, reducing crew trips and allowing more time for ancillary sales.

Trolley-based variants offer plug-and-play flexibility for carriers flying a mix of long- and short-sector rotations. Airlines redeploy them seasonally, rolling units onto longer flights where waste accumulation spikes. Lavatory-specific compactors handle paper towels and hygiene products; however, lower volumes prevent onboard odor issues that affect customer experience scores. Designers now integrate HEPA filters and odor-neutralization cartridges to meet upcoming health-safety guidelines, broadening the functional appeal of lavatory units within the aircraft cabin trash compactors market.

By Fit: Retrofit Segment Accelerates Market Expansion

Linefit options retained a 61.24% share of the aircraft cabin trash compactors market in 2024, reflecting OEM preference for fully integrated galleys during final assembly. However, retrofit demand is climbing at a 9.47% CAGR as airlines convert aging cabins to match new-build standards. The retrofit channel benefits independent MROs that bundle trash compactor upgrades with seat re-pitch, connectivity, or LED lighting programs, minimizing downtime during heavy checks.

Smart-ready retrofit kits include universal mounting rails, quick-disconnect wiring looms, and digital control panels compatible with multiple galley layouts. Such modularity lowers install hours, enabling overnight turnarounds on narrowbodies hosted at outstations. Linefit retains an integration advantage, allowing full harness routing behind sidewalls and direct tie-in to aircraft data buses for monitoring. OEMs therefore pitch compaction functionality during new program campaigns, ensuring baseline attachment rates remain robust through 2030.

Geography Analysis

North America led the aircraft cabin trash compactors market with a 32.67% revenue share in 2024, powered by fleet renewal and state-level waste mandates that penalize mixed trash landfilling. Major carriers like Delta retrofit entire B737-900ER fleets with integrated waste columns to meet corporate carbon targets. FAA guidance on fire suppression offers a mature approval pathway that shortens the time to service entry. A well-developed MRO ecosystem means airlines can schedule installations during ordinary maintenance, avoiding additional ground days.

Asia-Pacific posts the fastest 8.90% CAGR, propelled by LCC expansion and airport infrastructure gaps that make in-cabin waste reduction essential. China plans to double its fleet to 9,740 aircraft by 2043, and each new delivery provides an opportunity for factory-installed compactors. Government-backed sustainability rules in Japan and Australia further encourage adoption, while India’s retrofit boom underscores the value proposition where new equipment deliveries face leasing backlogs. Suppliers that localize production benefit from offset programs and reduced tariff exposure, sharpening their positioning in this aircraft cabin trash compactors market region.

Europe maintains steady momentum as legacy carriers modernize galleys under the EU Circular Economy Action Plan. EASA’s predictable certification structure incentivizes early engagement with authorities, and cross-border airline alliances drive harmonized equipment standards. Middle East operators increasingly specify lightweight compactors on long-haul widebodies to support nonstop rotations where ground waste removal is less frequent. Africa represents an emerging niche served primarily through donor aircraft retrofits.

Competitive Landscape

The aircraft cabin trash compactors market exhibits moderate concentration, with Safran, Collins Aerospace (RTX Corporation), and Iacobucci HF AEROSPACE S.p.A. collectively anchoring a substantial yet not dominant revenue portion. These incumbents capitalize on broad certification libraries and long-standing airline relationships, allowing them to bundle trash systems with larger galley packages. Technology differentiation rather than price competition defines tender outcomes; carriers rate sensors, connectivity, and weight savings ahead of upfront cost.

Collins Aerospace extends its Galley.ai suite to include waste-volume forecasting that syncs with catering systems, providing tangible time savings on turnarounds. Safran focuses on modular carbon-fiber constructions that drop unit weight into single-digit kilogram territory, while Iacobucci emphasizes low-noise gearboxes suitable for premium-cabin proximity.

New entrants typically address specialized needs such as lavatory-only units or trolley-mount quick-fits, carving space around legacy incumbents. Yet AS9100 and multi-agency certification hurdles raise the capital bar, which explains suppliers' steady but not explosive churn. Forward integration into data analytics platforms marks the next competitive frontier, transforming trash compactors from passive hardware to active data nodes within the digital cabin.

Aircraft Cabin Trash Compactors Industry Leaders

Safran

AVIC INTERNATIONAL HANGZHOU CO., LTD.

Collins Aerospace (RTX Corporation)

Iacobucci HF AEROSPACE S.p.A.

Hong Kong Aircraft Engineering Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Nikkiso Co., Ltd. began delivering trash compactor parts to Safran Cabin, a major manufacturer of aircraft interiors.

- April 2025: Airbus and Thai Airways International (THAI) signed a Letter of Intent (LoI) to retrofit the airline's A350 fleet. The upgrades include new lavatories, galleys, ovens, refrigerators, chillers, beverage makers, trash compactors, and electro-dimmable windows to improve passenger comfort and operational efficiency.

Global Aircraft Cabin Trash Compactors Market Report Scope

| Narrowbody |

| Widebody |

| Regional Jets |

| Business Jets |

| Galley |

| Trolley |

| Lavatory |

| Linefit |

| Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Aircraft Type | Narrowbody | ||

| Widebody | |||

| Regional Jets | |||

| Business Jets | |||

| By Installation Location | Galley | ||

| Trolley | |||

| Lavatory | |||

| By Fit | Linefit | ||

| Retrofit | |||

| By Region | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Aircraft cabin trash compactors market in 2025?

The market is valued at USD 149.64 million, with a forecasted CAGR of 8.40% to 2030.

Which aircraft segment offers the quickest growth for trash compactors?

Regional jets expand the fastest, growing at 9.53% CAGR through 2030 due to rapid fleet additions.

What region is expected to post the highest future growth?

Asia-Pacific leads with an 8.90% CAGR thanks to LCC expansion and large order backlogs.

Why are airlines investing in retrofit installations now?

Retrofits let carriers upgrade waste management without new-aircraft purchases, aligning fleets with stricter sustainability rules and avoiding long delivery queues.

What technology trends shape new compactor designs?

Lightweight composite housings, energy-efficient motors, and IoT sensors that enable predictive maintenance and waste analytics drive current innovation.

Page last updated on: