Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 9.40 Billion |

| Market Size (2031) | USD 12.11 Billion |

| Growth Rate (2026 - 2031) | 5.20% CAGR |

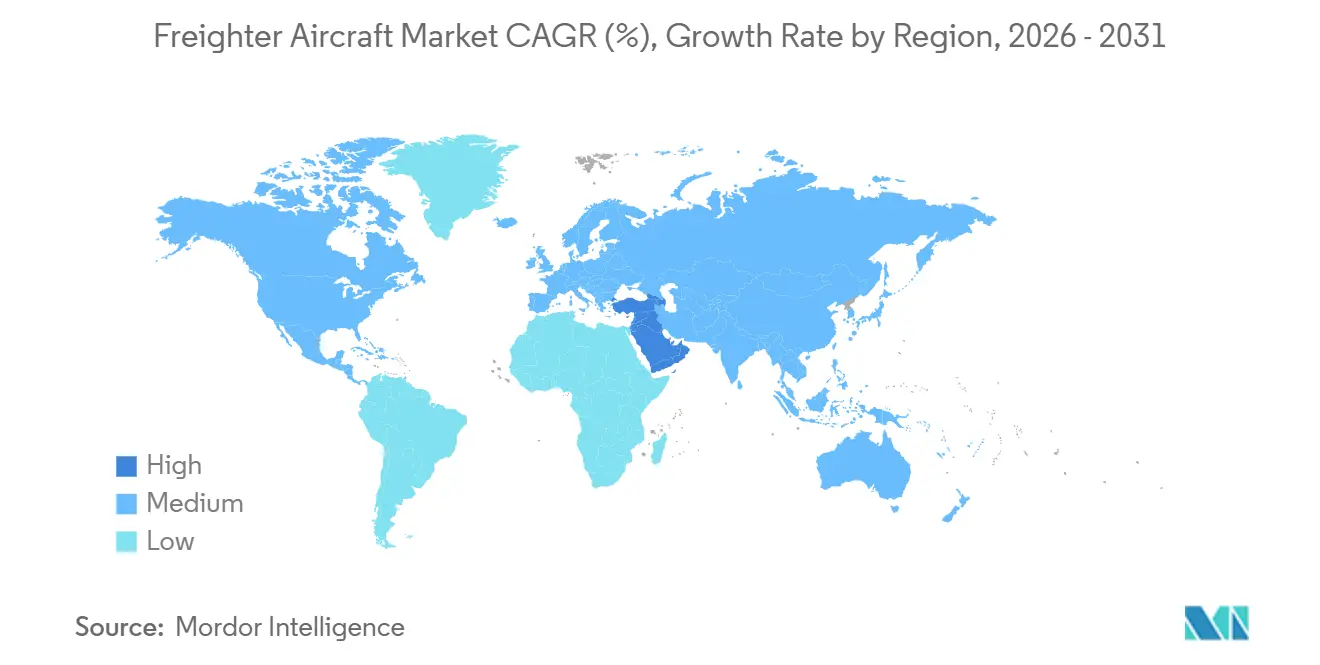

| Fastest Growing Market | Middle East |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Freighter Aircraft Market Analysis by Mordor Intelligence

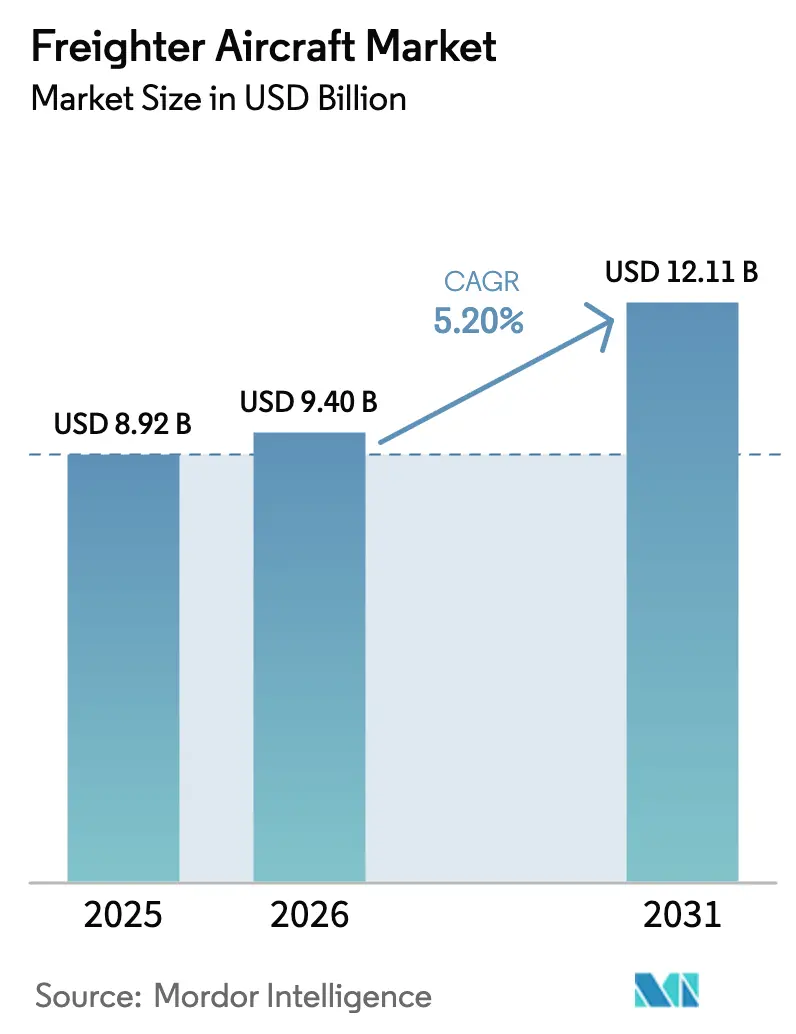

The freighter aircraft market size is expected to grow from USD 8.92 billion in 2025 to USD 9.40 billion in 2026 and is forecasted to reach USD 12.11 billion by 2031 at a 5.20% CAGR over 2026-2031. This trajectory is driven by sustained growth in cross-border e-commerce, the structural contraction of passenger belly-hold capacity, and regulatory pressure that is accelerating fleet renewal. Express parcel volumes now account for as much as one-third of international air-cargo tonnage, prompting integrators to secure dedicated main-deck lift well ahead of seasonal peaks. Operators are also influencing investment decisions due to the International Civil Aviation Organization’s CO₂ standard, effective 2027, and Chapter 14 noise limits, which are phasing out Stage 3 aircraft. At the same time, the European Union Emissions Trading System’s full aviation inclusion from 2026 embeds carbon costs into every trans-Atlantic sector, tilting fleet-planning economics further toward fuel-efficient types. These converging forces underpin the resilient double-digit growth outlook for the freighter aircraft market.

Key Report Takeaways

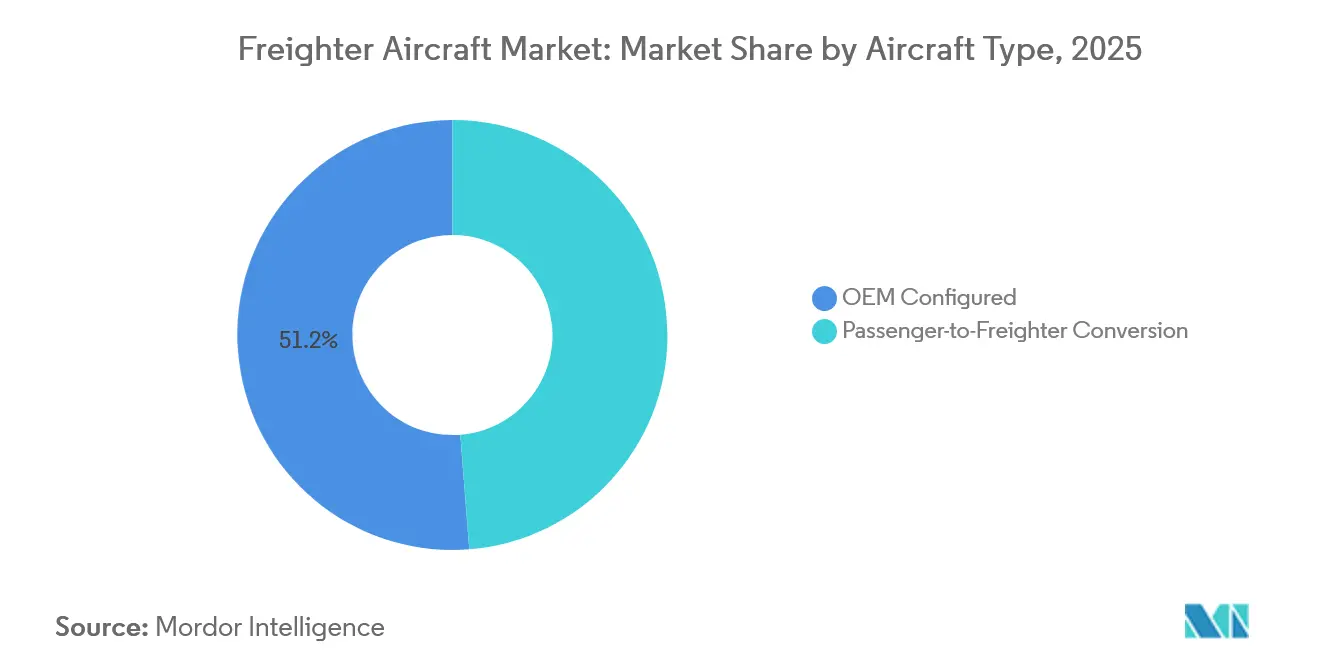

- By aircraft type, passenger-to-freighter conversions expanded at a 5.95% CAGR through 2031 while OEM-configured units held a 51.25% freighter aircraft market share in 2025.

- By payload capacity, medium widebodies captured 41.21% of the freighter aircraft market size in 2025, whereas standard-body aircraft under 45 tonnes are advancing at a 5.76% CAGR.

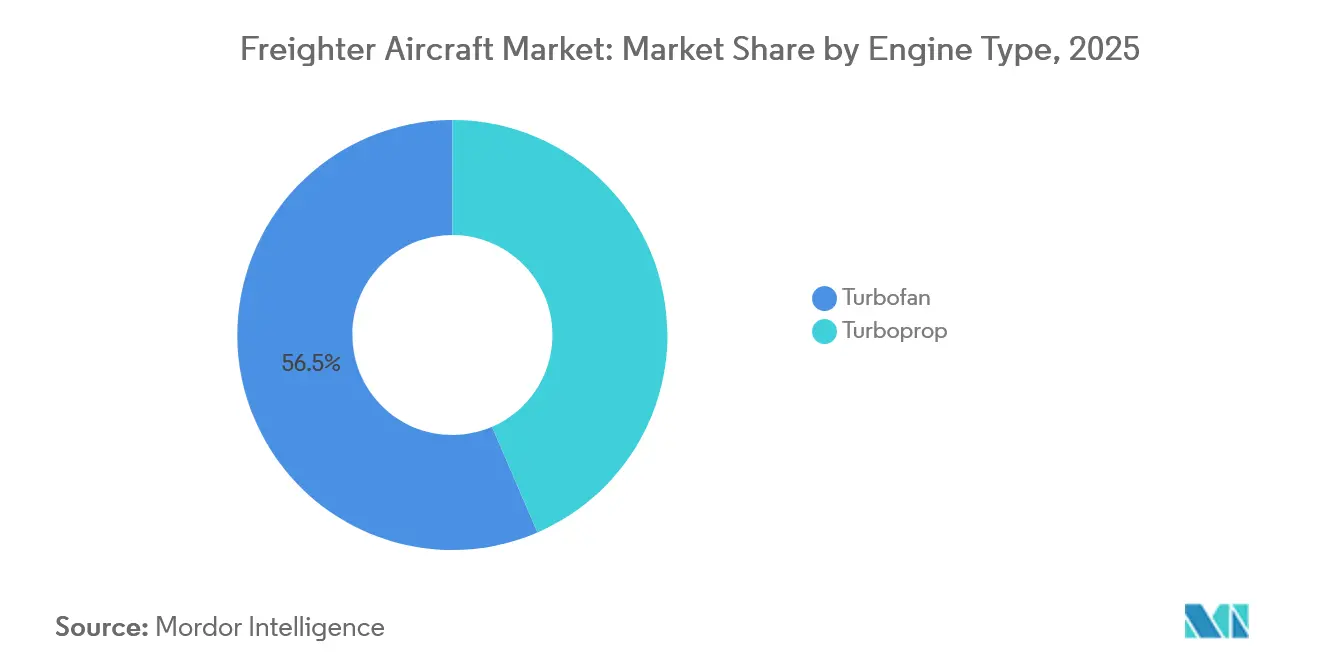

- By engine type, turbofan platforms commanded 56.47% freighter aircraft market share in 2025, with turboprops logging a 6.11% CAGR.

- By geography, North America retained a 46.81% freighter aircraft market share in 2025, while the Middle East is the fastest-growing region, with a 6.23% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Freighter Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce and express parcel boom | +3.20% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Fleet renewal to meet ICAO CO₂/noise rules | +2.80% | Global, with Europe and North America most exposed | Long term (≥4 years) |

| Shrinking belly-cargo capacity on airliners | +1.90% | Global, acute on trans-Atlantic and trans-Pacific lanes | Short term (≤2 years) |

| Expanding intra-Asia and trans-Pacific trade | +1.50% | Asia-Pacific core with spill-over to Middle East hubs | Medium term (2-4 years) |

| Special-cargo demand for temp-controlled lift | +0.70% | Global, led by North America and Europe | Long term (≥4 years) |

| Opening of polar ETOPS routes post-2027 | +0.40% | Asia-Europe corridors, secondary effect on Middle East | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

E-commerce and Express Parcel Boom

Cross-border parcel shipments are forecast to rise 12-15% annually to 2028, a pace that obliges integrators to reserve conversion slots three years in advance. Amazon Air’s fleet climbed to 110 aircraft in 2025, and the company secured 20 additional 767-300 conversions to sustain two-day delivery across secondary US cities.[1]Amazon, “Amazon Air Fleet Expansion,” amazon.com Cainiao Logistics ordered 10 converted 777Fs in 2024 to buffer Singles’ Day surges, which can triple daily tonnage, a profile that a belly-hold cannot absorb. Premiums for guaranteed next-day lift now run 15-20% above standard charters, supporting aggressive capital deployment into dedicated freighters even when lease rates tighten.

Fleet Renewal to Meet ICAO CO₂/Noise Rules

ICAO’s CO₂ design standard applies from 2027, while Chapter 14 noise limits that took full effect in 2024 have already excluded older 747-400 and MD-11 freighters from European and Japanese gateways.[2]European Union Aviation Safety Agency, “Environment and Noise,” easa.europa.eu FedEx retired its final MD-11F in early 2024 and firmed 24 777F deliveries through 2028, citing compliance certainty as the overriding rationale. With OEM order backlogs stretching to 36 months, operators unable to defer decisions beyond 2026 face a shrinking retrofit window that magnifies the tailwind behind the freighter aircraft market.

Shrinking Belly-Cargo Capacity on Passenger Fleets

Permanent 747-400 and A380 retirements eliminated roughly 15% of pre-2020 belly-hold capacity, a gap that narrowbody replacements cannot fill because 737 and A320 lower holds carry a fraction of widebody volume. Forwarders now pay 30-40% higher kilo-rates for what little belly space remains, erasing its historical cost edge over main-deck lift. Boeing’s 2024 Commercial Market Outlook projects that only 85% of lost belly tonnage will return by 2030, securing long-term demand for dedicated freighters.

Expanding Intra-Asia and Trans-Pacific Trade Lanes

Intra-Asia tonnage expanded 8% in 2025, outstripping the global average, as supply-chain diversification toward Vietnam, Thailand, and India required just-in-time component flows. SF Express grew its freighter fleet from 75 to 92 aircraft in one year, deploying 737-800BCFs on dense Shenzhen-Hanoi and Guangzhou-Bangkok corridors. Balanced east-bound and west-bound loads now keep Trans-Pacific utilization above 80%, reinforcing the economic case for medium-widebody freighters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fuel-price and carbon-price volatility | -1.8% | Global, most acute in Europe due to EU-ETS | Short term (≤2 years) |

| Tightening environmental compliance cost (EU-ETS) | -1.4% | Europe plus global CORSIA routes | Medium term (2-4 years) |

| Passenger-aircraft feedstock shortage for P2F slots | -0.9% | Global, narrowbody segment most exposed | Medium term (2-4 years) |

| Slot and runway congestion at cargo mega-hubs | -0.6% | Asia-Pacific (HKG, PVG), North America (MEM, ANC) | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Fuel-Price and Carbon-Price Volatility

Jet-fuel averaged between USD 2.50 and USD 3.50 per gallon in 2025; every USD 0.50 swing adds roughly USD 150,000 in annual fuel spend per 777F, compressing margins that average 8-12%.[3]U.S. Energy Information Administration, “Petroleum & Other Liquids,” eia.gov Carbon allowances under the EU-ETS traded at EUR 60-80 (USD 69.8-93.07) per tonne in 2025, translating to EUR 8,000-10,000 (USD 9,306.72-11,633.4) for a single trans-Atlantic 777F leg. Smaller cargo carriers lack the balance-sheet strength to hedge both fuel and carbon exposure, creating potential capacity shake-outs during price spikes.

Tightening Environmental Compliance Costs (EU-ETS, CORSIA)

The Carbon Offsetting and Reduction Scheme for International Aviation transitions from a pilot to a mandatory phase in 2027, obliging airlines to offset emissions growth above 2019 levels. Credit prices ranged from USD 15 to 25 per tonne in 2025 and are expected to escalate as aviation demand for high-quality offsets rises. Administrative overhead linked to monitoring, reporting, and verification further adds to carriers’ fixed cost base, accelerating consolidation toward well-capitalized incumbents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Conversions Counter High Capital Costs

Passenger-to-freighter conversions are forecast to expand at a 5.95% CAGR to 2031, eclipsing OEM builds even as factory freighters controlled 51.25% of the 2025 freighter aircraft market share. Operators drawn to conversions cite capital expenditures (capex) savings: a 15-year-old 767-300ER converted for USD 22 million, versus a USD 220 million list price for a 777F, enabling capacity additions without 20-year debt loads. Israel Aerospace Industries launched its 777-300ER Special Freighter in 2024 and had 23 commitments by mid-2025, targeting the 80-90 tonne slot not served by the 767F or factory-built 777F.[4]Israel Aerospace Industries, “Aviation Group,” iai.co.il ST Engineering’s A321P2F, certified in 2024, offers 28 tonnes of lift and a containerized main deck, bringing widebody-like loading efficiency into short-haul express networks.

OEM freighters nonetheless retain structural advantages. A new 777-8F will burn 15% less fuel per tonne-kilometer than a converted 777-300ER and is immediately compliant with 2027 ICAO standards. Airbus handed over eight A350Fs in 2025, with Lufthansa Cargo and Singapore Airlines among launch customers that prioritize residual value and unrestricted airport access. Lead-time risk, however, keeps conversions attractive for operators that must respond within 18-24 months to e-commerce surges, insulating the secondary market from OEM competition and cementing its role in the freighter aircraft market.

By Payload Capacity: Standard-Body Upswing in Last-Mile Networks

Standard-body aircraft under 45 tonnes are logging the fastest growth at 5.76% CAGR as Amazon Air, DHL, and regional integrators saturate next-day networks with 737-800BCFs and A321P2Fs. These types bridge airports that require 8-12 daily departures, instead of one high-capacity widebody, thereby boosting schedule granularity that e-commerce shippers prize. The freighter aircraft market size for standard-body units is expected to rise from USD 2.4 billion in 2026 to USD 4.1 billion by 2031. Medium-widebodies in the 40-80 tonne band held 41.21% of the freighter aircraft market share in 2025, with the 767-300F entrenched as the sector's workhorse. FedEx operates 120 units alone and plans service life extensions to 2035, despite a higher fuel burn compared to newer models.

Large widebodies above 80 tonnes, dominated by 777Fs and legacy 747-8Fs, face a transitional gap until Boeing’s 777-8F enters service in 2028. Charter rates for the segment rose 20% in 2025 as the 747-8F exited production and its operators deferred replacement decisions. Ethiopian Cargo added two ATR 72-600Fs in 2025 to serve Nairobi, Kigali, and Dar es Salaam, illustrating the type’s role on thin African lanes.

By Engine Type: Turbofan Dominance, Turboprop Niche Growth

Turbofan engines retained a commanding 56.47% slice of the 2025 freighter aircraft market share, a position sustained by fuel-efficient twin-engine widebodies such as the 777F and A350F that burn less than 0.50 lb of fuel per pound of thrust per hour and can fly 9,000-kilometre missions without payload penalties. Airlines that operate both passenger and cargo variants of these types consolidate spare parts pools and line maintenance crews, cutting unit maintenance costs by as much as 10%, an advantage turboprops cannot replicate.

Even so, turboprops are expected to expand at a 6.11% CAGR through 2031, as they excel in short-haul sectors or at airports with limited runway length or ground infrastructure. FedEx Feeder already deploys 240 ATR and Cessna turboprops to connect 120 US cities to its Memphis super-hub, offering frequency and slot flexibility that jets would oversupply. Annual production remains modest; ATR rolls out only 40-50 freighter units, but each airframe quickly finds a home in Southeast Asia, the Caribbean, or Central Africa, regions where Chapter 14-compliant noise footprints and short-field performance outweigh the speed premium of turbofans.

Geography Analysis

North America’s freighter aircraft market size was USD 4.4 billion in 2026, accounting for 46.81% of the global value, as e-commerce penetration is expected to reach 30% of US retail sales by 2031. FedEx’s Memphis super-hub processes 500,000 packages per hour at peak, while UPS’s Louisville complex tops 400,000; these volumes underpin sustained demand for widebody lift. Canada’s Cargojet added three 767-300Fs in 2025 and renewed a long-term capacity-purchase agreement with Amazon Canada, reflecting continued strength in domestic overnight parcels.

The Middle East is the fastest-growing region, with a 6.23% CAGR. Emirates SkyCargo is committed to delivering five additional 777Fs through 2027, which will raise its total fleet to 16 and reinforce Dubai’s role as a sixth-freedom bridge between Asia and Europe. Qatar Airways Cargo operates 28 freighters, including two 747-8Fs dedicated to handling outsized loads, such as oil-field equipment, which leverage Doha’s uncongested nighttime slots. Etihad Cargo remains a minor player but is retrofitting A350Fs with active cooling units to target pharmaceuticals, adding competitive depth to the regional landscape.

Asia-Pacific demand is accelerating, driven by supply-chain shifts and intra-regional e-commerce, which is pledging 48-hour delivery. SF Express plans to grow its fleet to 92 units by the end of 2025 and has reserved 15 additional 737-800BCF slots for 2026-2027. Singapore Airlines Cargo, an early A350F operator, is redeploying 777Fs to Australia and India, optimizing aircraft gauge to lane density. Airport constraints in Hong Kong and Shanghai are steering incremental frequencies toward secondary hubs, such as Shenzhen and Phnom Penh, thereby diversifying the capacity map.

Europe maintains a stable volume, anchored by Lufthansa Cargo’s Leipzig and Frankfurt operations, as well as DHL’s pan-European network. Slot scarcity at Frankfurt restricts further frequency growth, but fuel-efficient A350Fs allow Lufthansa to up-gauge without breaching local noise quotas. Latin America and Africa remain niche markets, yet LATAM Cargo and Ethiopian Cargo each added two wide-body aircraft in 2025, citing agricultural exports and mining parts as catalysts for dedicated main-deck services. Although their combined market share remains under 5%, these regions provide high-yield backhaul opportunities that improve global network balance.

Competitive Landscape

The production of freighter aircraft is concentrated within a two-manufacturer market. In 2025, Boeing is projected to account for 70% of factory deliveries, with 22 units of the 777F and six units of the 767F delivered. Meanwhile, Airbus is expected to produce eight A350Fs during the aircraft's first full year of production. The passenger-to-freighter conversion arena, however, is fragmented. Israel Aerospace Industries, ST Engineering, Precision Aircraft Solutions, and KF Aerospace collectively completed 105 conversions in 2025, competing fiercely for airframes and hangar labor. Lessors such as AerCap pre-purchase slots, then market converted 737-800BCFs and 777-300ERSFs on operating leases that shift residual-value and compliance risk away from airlines, a structure attractive to e-commerce logistics arms with thin balance sheets.

OEMs are relying on technology to maintain their market share. Boeing’s 777-8F will incorporate composite wing-covers and advanced flutter-suppression logic to cut fuel burn 20% versus the 747-8F, translating to roughly USD 2 million annual savings per aircraft even at USD 2.75 per-gallon jet fuel. Airbus positions the A350F as a compliance hedge: its inherent CO₂ performance beats ICAO’s 2027 line-fit target by a 10% margin, ensuring unrestricted airport access beyond 2045. Conversion specialists respond by reducing downtime; ST Engineering trimmed its A321P2F turnaround to 82 days through the use of modular kit design, resulting in a 15% lead-time gain over 2024.

Digital forwarders are another competitive vector. Freightos and Flexport aggregate capacity and publish all-in rates via APIs, eroding traditional forwarders’ informational advantage. Incumbent cargo airlines are therefore investing in real-time booking portals and predictive load planning to defend their share, amplifying the technology arms race within the freighter aircraft market.

Freighter Aircraft Industry Leaders

The Boeing Company

Airbus SE

Avions de Transport Régional (ATR)

Singapore Technologies Engineering Ltd

Aeronautical Engineers Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Hong Kong Air Cargo added an Airbus A330-200 P2F freighter to its fleet, increasing its total number of A330-200 freighters to six. All these aircraft are dry leased from its parent company, Hong Kong Airlines.

- November 2025: Air China Cargo entered into a purchase agreement with Airbus for six A350F freighters, making it the first mainland Chinese customer for the new A350F model.

- October 2025: Miami-based Aeronautical Engineers Inc. (AEI) initiated the development of a Boeing 737-900ER passenger-to-freighter (P2F) program. The program aims for certification by 2029, offering a payload capacity of approximately 26 tonnes and a cargo volume of 206 m³.

Global Freighter Aircraft Market Report Scope

This report examines the global freighter aircraft market, focusing on the development, production, conversion, and operation of fixed-wing aircraft designed or explicitly modified for cargo transportation. The market encompasses both OEM-configured freighters and passenger-to-freighter (P2F) conversions, utilized in express parcel, general cargo, and specialized cargo operations, including temperature-controlled, oversized, and high-value freight. The analysis examines market dynamics shaped by the growth of e-commerce, changes in belly cargo availability, evolving environmental regulations, and shifts in global trade routes.

The report provides segmentation by aircraft type (OEM-configured and P2F conversions), payload capacity (standard-body below 45 tonnes, medium-widebody 40–80 tonnes, and large-widebody above 80 tonnes), engine type (turbofan and turboprop), and geography. Geographic coverage encompasses North America, South America, Europe, the Asia-Pacific region, and the Middle East and Africa, with detailed country-level analysis for key cargo hubs.

By Aircraft Type

| OEM Configured |

| Passenger-to-Freighter Conversion |

By Payload Capacity

| Standard-Body (Less than 45 tonnes) |

| Medium Widebody (40–80 tonnes) |

| Large Widebody (Greater than 80 tonnes) |

By Engine Type

| Turbofan |

| Turboprop |

Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Aircraft Type | OEM Configured | ||

| Passenger-to-Freighter Conversion | |||

| By Payload Capacity | Standard-Body (Less than 45 tonnes) | ||

| Medium Widebody (40–80 tonnes) | |||

| Large Widebody (Greater than 80 tonnes) | |||

| By Engine Type | Turbofan | ||

| Turboprop | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the freighter aircraft market?

The freighter aircraft market size was USD 9.40 billion in 2026 and is projected to reach USD 12.11 billion by 2031, with a CAGR of 5.20%.

Which aircraft type is expanding the fastest?

Passenger-to-freighter conversions are growing at 5.95% CAGR, outpacing new-build deliveries.

Why is the Middle East showing the highest regional growth?

Carriers such as Emirates and Qatar are adding 777Fs to leverage sixth-freedom hubs that link Asia with Europe and Africa, resulting in a 6.23% CAGR for the region.

How will ICAO’s 2027 CO₂ standard affect fleet plans?

Operators must choose between ordering new 777-8Fs and A350Fs that meet the rule or converting mid-life passenger jets and accepting operational restrictions at noise-sensitive airports.

What are the main cost risks for cargo airlines?

Volatile jet-fuel prices and rising carbon-allowance costs under the EU-ETS can erode margins rapidly, especially for carriers without strong hedging capacity.

Are turboprop freighters still relevant?

Yes, turboprops such as the ATR 72-600F are expected to expand at a 6.11% CAGR through 2031 on short routes with runway or demand constraints that make jets uneconomical.

Page last updated on: