Commercial Aircraft Disassembly Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

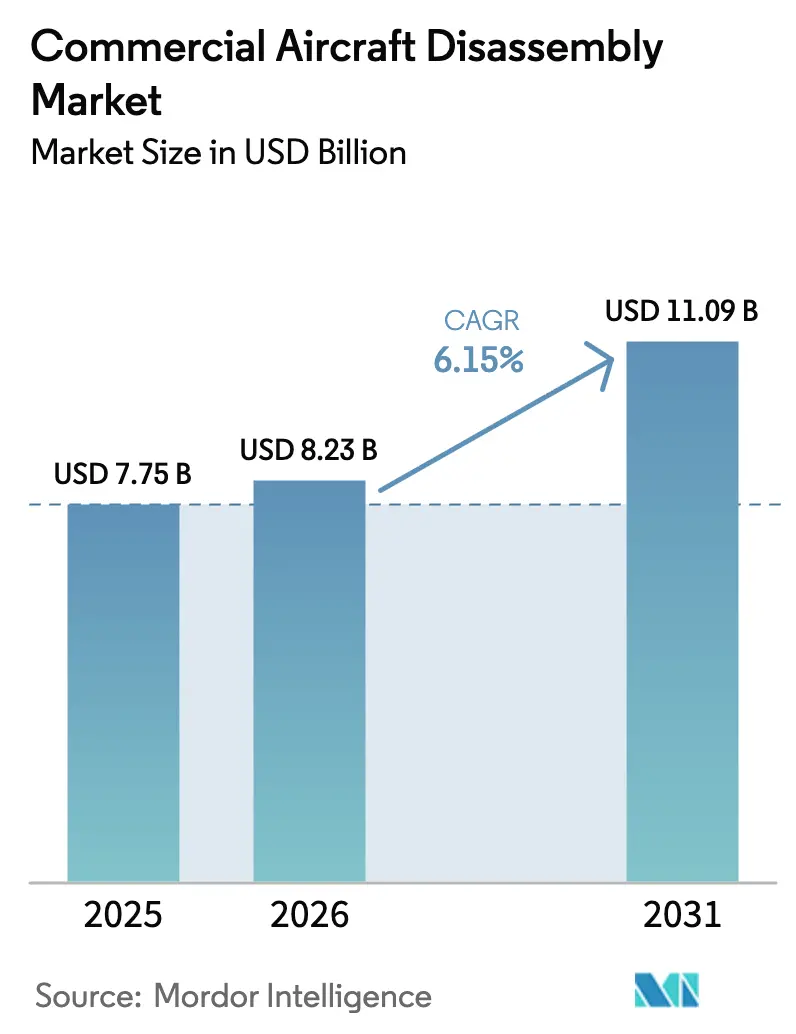

| Market Size (2026) | USD 8.23 Billion |

| Market Size (2031) | USD 11.09 Billion |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

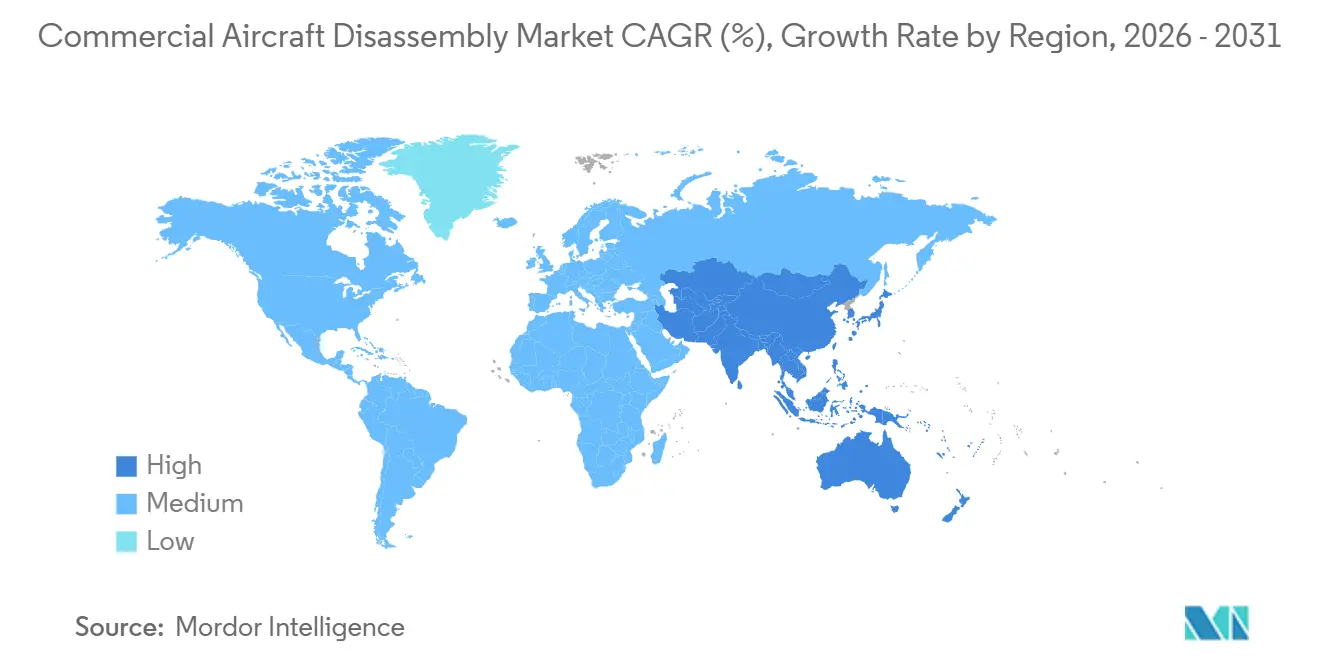

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Aircraft Disassembly Market Analysis by Mordor Intelligence

The commercial aircraft disassembly market size is expected to grow from USD 7.75 billion in 2025 to USD 8.23 billion in 2026 and is forecast to reach USD 11.09 billion by 2031 at a 6.15% CAGR over 2026-2031. Rising adoption of certified used serviceable material (USM), persistent engine shop-visit backlogs, and delivery delays are shifting value from scrap to component recovery as operators seek cost certainty and uptime. Lessors are formalizing end‑of‑life playbooks to monetize assets through teardown when lease economics weaken, while OEMs are integrating lifecycle programs to protect quality and improve supply resilience. Asia-Pacific is building capability and throughput to support a fast-growing installed base, while North America remains the largest teardown hub by volume and certifications. Circular design and improved composite recovery methods support higher reuse rates over time, though composite-heavy airframes still pose processing and certification hurdles for high-value reintegration.

Key Report Takeaways

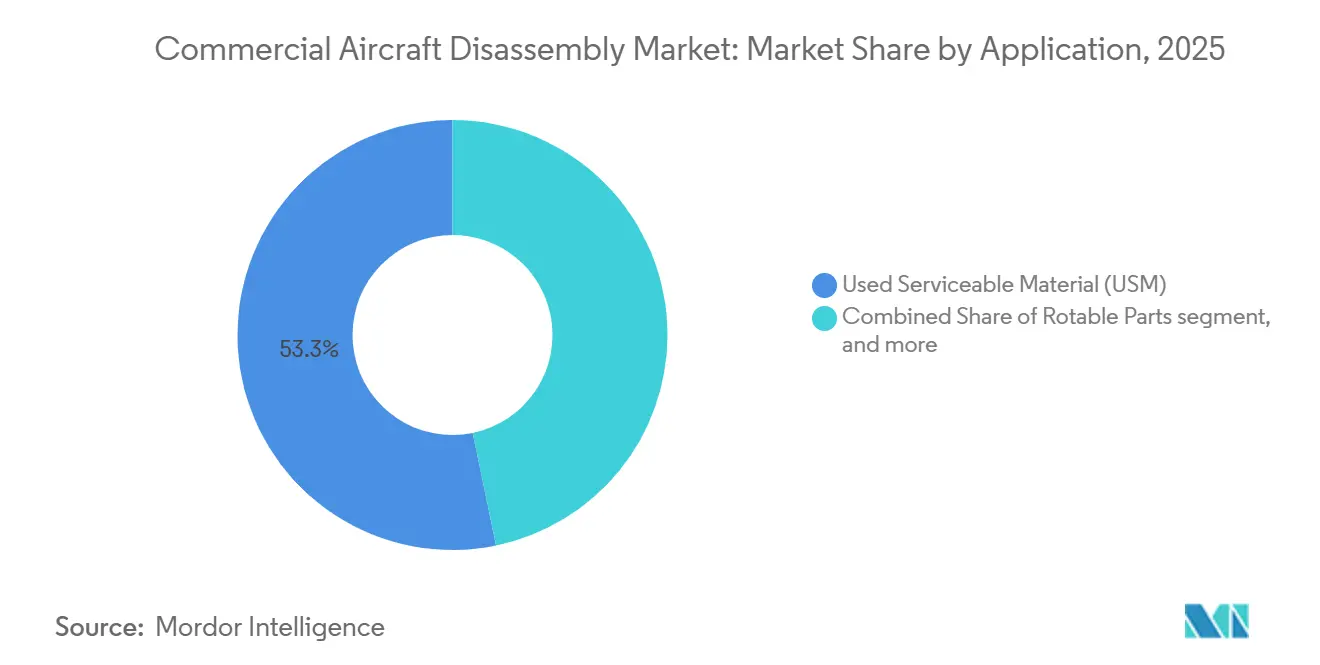

- By application, used serviceable material (USM) led with a 53.25% revenue share in 2025 and is forecasted to expand at an 8.24% CAGR through 2031.

- By aircraft type, narrowbody platforms accounted for 58.47% share of the commercial aircraft disassembly market in 2025, and the segment is projected to grow at 6.35% CAGR through 2031.

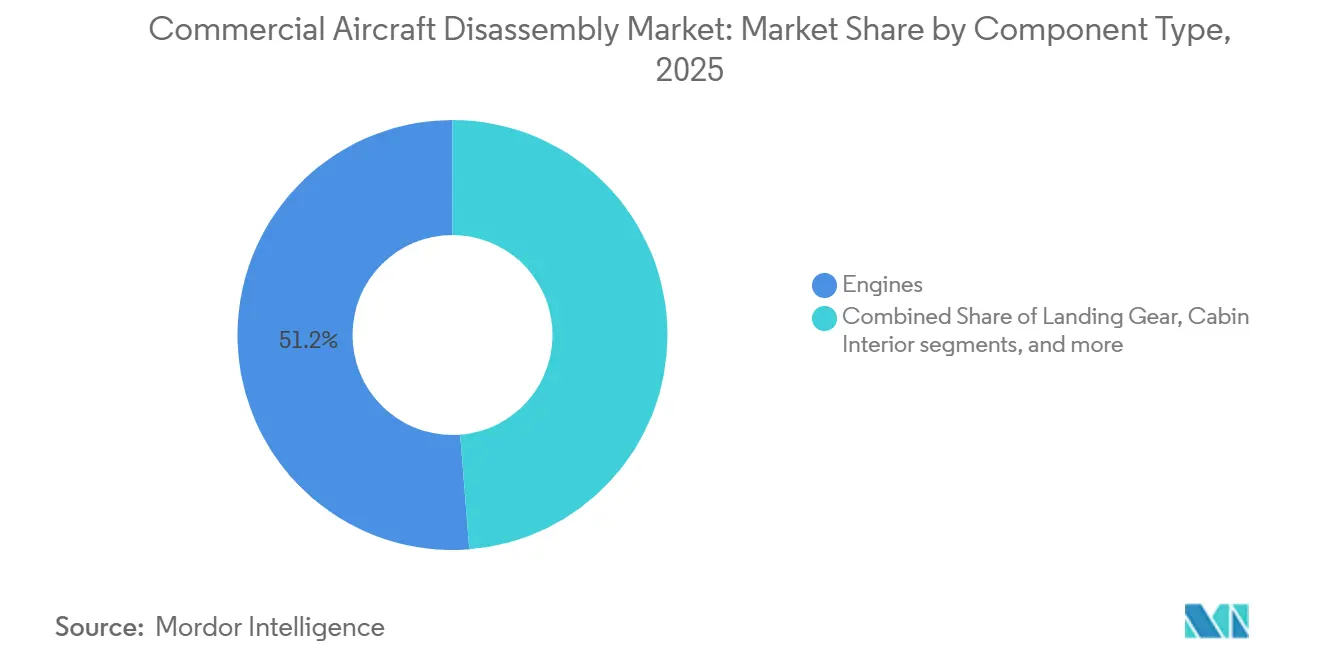

- By component type, engines captured a 51.24% share of the commercial aircraft disassembly market in 2025 and are projected to grow at a 7.68% CAGR through 2031.

- By end-user, leasing companies held a 42.57% share of the commercial aircraft disassembly market in 2025 and are projected to grow at a 6.58% CAGR through 2031.

- By geography, North America accounted for 41.65% in 2025, while the Asia-Pacific is the fastest-growing region over the forecast period, registering a CAGR of 7.57%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Commercial Aircraft Disassembly Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-2027 retirement wave and replacement cycle expand part-out volumes | +1.8% | Global, with concentrated impact in North America and Europe | Medium term (2-4 years) |

| Persistent parts shortages and inflation push wider USM adoption | +1.5% | Global, with highest intensity in the Asia-Pacific core, spill-over to the Middle East and Africa | Short term (≤ 2 years) |

| Engine shop-visit surge and reliability issues accelerate engine part-outs | +1.3% | North America, Europe, Middle East hotspots | Short term (≤ 2 years) |

| OEM/lessor lifecycle programs (recycling + USM) increase supply chain integration | +0.9% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Circular-economy mandates and recovery-tech breakthroughs lift recyclability | +0.5% | EU primary, North America and Asia-Pacific adopting | Long term (≥ 4 years) |

| Emerging Asia-Pacific teardown hubs as fleets mature | +0.6% | Asia-Pacific core, particularly China, India, Philippines, Singapore | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-2027 Retirement Wave And Replacement Cycle Expand Part-Out Volumes

A replacement cycle is building as large narrowbody cohorts from the 2010s approach economic transition points in the late 2020s, supporting elevated teardown volumes and a deeper pool of certified components. Boeing’s 2025 Commercial Market Outlook signals extensive fleet replacement over the next two decades, with North America positioned to deliver the highest replacement share among regions, creating a steady teardown pipeline as older aircraft exit service.[1]Boeing, “Boeing Expands Used Serviceable Material Capacity to Address Supply Chain Challenges,” Boeing Global Services, boeing.com Retirement timing was suppressed in 2024 by lease extensions and delivery backlogs, a trend that tightened component supply and reset valuations for high-demand parts.[2]SMBC Aviation Capital, “Plane Insights Q2 2025,” SMBC Aviation Capital, smbc.aero As operators normalize fleet plans and OEM supply recovers, a catch-up pulse of removals is expected to flow into certified teardown channels rather than general scrap, reinforcing the commercial aircraft disassembly market. Standardized decommissioning and AFRA(Aircraft Fleet Recycling Association) best practices now act as a threshold for access to many lessor programs, which aligns with Boeing’s policy to use AFRA-accredited partners in its expanded USM consignment model.[3]Aircraft Fleet Recycling Association, “Accreditation Info,” AFRA, afraassociation.org These structural shifts create more predictable part‑out volumes, improving planning and pricing outcomes for buyers and sellers in the commercial aircraft disassembly market.

Persistent Parts Shortages And Inflation Push Wider USM Adoption

Airline maintenance costs have been pressured by supply bottlenecks and longer repair cycles, which has raised the appeal of certified used components that can be delivered on short lead times. IATA estimates that supply chain constraints carried a multi-billion-dollar cost burden in 2025, reinforcing the case for reliable and traceable alternatives to sourcing new parts from backlogged channels.[4]International Air Transport Association, “Aerospace Supply Chain Bottlenecks Continue to Constrain Airlines,” IATA, iata.org USM programs offer operators faster AOG recovery windows through established logistics, quality assurance, and dual regulatory certifications, which can reduce service disruptions in high-utilization fleets. Vertically integrated teardown and repair models further support cost and time efficiency by consolidating inspection, repair, and certification within the same enterprise, which accelerates component release to service. Industry bodies and regulators have tightened documentation and distributor accreditation requirements, which has raised confidence in certified USM and helped the commercial aircraft disassembly market absorb more demand from operators who value rigorous compliance. As backlogs persist, robust traceability, strong quality assurance, and predictable logistics continue to drive the adoption of certified USM pathways across major fleets, sustaining momentum in the commercial aircraft disassembly market.

Engine Shop-Visit Surge And Reliability Issues Accelerate Engine Part-Outs

Higher shop-visit loads on new-technology narrowbody engines have increased demand for serviceable engine modules and life-limited parts that can be quickly certified back to service. Rolls‑Royce has implemented durability enhancements on the Trent XWB‑97 to improve time-on-wing in challenging environments, underscoring how reliability actions and inspection mandates can push components into maintenance queues in greater numbers. CFM International has issued certified durability kits and expanded MRO capacity for LEAP engines, addressing in‑service wear patterns and supporting more predictable off‑wing cycles during the next phase of growth. Additional shop capacity additions, such as new LEAP support in India and a Premier MRO designation in Dallas, illustrate the depth of investment required to stabilize turn times and support growing fleets. Lufthansa Technik has also scaled capabilities for LEAP support, integrating predictive tools with material flow to reduce disruption risk during peak shop-visit cycles. The outcome is a persistent demand for certified engine parts sourced from teardown to close near-term supply gaps in high-value assemblies, driving a greater share of value toward engines in the commercial aircraft disassembly market. These conditions reinforce supplier credibility and documentation standards as critical differentiators in sourcing strategies across operators and MRO partners.

OEM/Lessor Lifecycle Programs Increase Supply Chain Integration

Boeing has expanded a consignment-based USM and recycling model with AFRA-accredited partners to deliver traceable parts streams from retired aircraft into global maintenance channels, aligning teardown activities with OEM oversight and environmental protocols. This approach aligns incentives among OEMs, operators, and lessors to harvest more components per induction and to prioritize compliant processes that preserve asset value for resale. Lessor policies are also maturing, with portfolio strategies that weigh end‑of‑life options based on engine and component economics rather than age alone, and with greater attention to transparent recovery metrics to support reporting obligations. Industry frameworks are moving toward broader recognition of open maintenance ecosystems that protect warranties while allowing flexibility in parts and repair sourcing under defined quality regimes, as illustrated by IATA’s renewed pro‑competitive agreement with CFM. As lifecycle programs scale, they enable consistent access to documentation, calibrated testing, and accredited depollution practices, thereby reducing counterparty risk and supporting broader USM adoption in the commercial aircraft disassembly market. This integration also expands the pool of certified inventory available for quick-turn installation, reducing AOG risk while raising confidence in chain-of-custody records.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Near-term feedstock scarcity from low retirements and lease extensions | -1.2% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Composite-heavy airframes remain costly to process | -0.7% | Global, particularly affecting newer fleet teardowns (787, A350) | Long term (≥ 4 years) |

| OEM control and lessor preferences limit USM on specific platforms | -0.5% | Global, with stronger impact in North America | Medium term (2-4 years) |

| Counterfeit/traceability risks raise compliance costs and TATs | -0.4% | Global, particularly the Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Near-Term Feedstock Scarcity From Low Retirements And Lease Extensions

Retirements have been below historical norms as airlines extend leases and keep mid‑life aircraft in service to bridge new‑delivery shortfalls, which constrains the immediate flow of teardown candidates. This near‑term scarcity reduces the availability of high‑demand serviceable engines and high‑turn parts, which raises competition for certified inventory. Lower inductions also limit the variety of part numbers entering circulation at any given time, which can lengthen sourcing searches for specific configurations. IATA has highlighted how constrained supply and maintenance bottlenecks impede capacity recovery, which reinforces why feedstock scarcity is a binding factor for operators relying on USM to keep fleets flying. As deliveries normalize and deferred retirements resume, more material should re‑enter the commercial aircraft disassembly market, though near‑term pricing may remain firm for select components. Operators that pre‑position parts and work with accredited suppliers are better insulated from temporary shortages and delays.

Composite-Heavy Airframes Remain Costly To Process

Teardown of next‑generation composite structures requires specialized tooling, strict environmental controls, and bespoke processes that increase labor and capital costs compared with aluminum‑dominant aircraft. Peer‑reviewed studies show that while fiber recovery is technically feasible through pyrolysis and solvolysis, consistent aerospace‑grade reintegration remains difficult and costly at an industrial scale. Precision dismantling technologies such as robotic abrasive‑waterjet cutting improve safety and quality but raise investment thresholds, which can limit adoption among smaller facilities. Demonstrations of high‑quality composite repurposing, as shown by Airbus and partners, indicate a pathway to better outcomes but require further scale and certification to broadly impact economics. Regulatory and documentation requirements for handling coatings, adhesives, and hazardous substances add process time and compliance costs, which weigh on teardown profitability for composite airframes. Until large-scale recovery and certification pathways mature, composite-heavy airframes will continue to temper the realized value from part-outs in the commercial aircraft disassembly market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: USM Dominates Amid Supply Chain Stress, Rotable Pools Gain Traction

USM held 53.25% of 2025 revenue and is projected to grow at an 8.24% CAGR through 2031, reflecting the clear customer preference for certified, quick‑turn components during prolonged new‑part backlogs. The commercial aircraft disassembly market continues to absorb demand that was redirected from delayed OEM deliveries and long repair queues, with USM providing predictable availability through accredited networks. Airlines and MROs report greater reliance on USM for high‑turn items that drive AOG exposure, a pattern supported by formal distributor accreditation and dual FAA/EASA certifications that maintain traceability. Boeing’s consignment program increases supply chain visibility and accelerates recertification throughput, which lowers time to market for parts harvested from retirements and managed transitions. As USM becomes a standard cost lever for operators, the commercial aircraft disassembly market is positioned to support deeper rotables coverage for critical part families.

The rotable parts segment leverages predictive maintenance insights to position inventory near hubs ahead of scheduled interventions, improving dispatch reliability and reducing AOG risk. Integrated teardown and repair models unlock speed by aligning inspection, repair, and documentation, streamlining release‑to‑service, and reducing logistics friction for time‑sensitive components. AFRA best practices for depollution and documentation continue to standardize disassembly and reduce quality variance, which protects the value of the recovered pool. As a result, certified USM and rotable pools reinforce each other, with the former supplying depth and the latter optimizing availability. These effects help the commercial aircraft disassembly market reduce operating risk for airlines facing tight capacity, thereby increasing reliance on accredited USM suppliers. The commercial aircraft disassembly industry has therefore moved from episodic to programmatic adoption across leading carriers and MRO alliances, making quality systems and accreditation central to supplier selection.

By Aircraft Type: Narrowbody Retirements Drive Volume, While Widebody Part-Outs Skew Toward Engines

Narrowbody platforms accounted for 58.47% of the market in 2025, and the category is projected to expand at 6.35% through 2031 as fleets cycle into replacement and operators arbitrage engine economics in select cases. The commercial aircraft disassembly market benefits from the scale of the installed B737 and A320 families, where teardown inputs convert into large pools of serviceable engines, airframe components, and avionics suitable for cross‑fleet use. New‑technology engine reliability measures and shop capacity expansions by OEMs and licensed shops should gradually stabilize turn times. Still, airlines maintain a strong appetite for certified USM to mitigate disruptions. Asia-Pacific teardown projects have demonstrated compressed turnaround times for A320neo disassembly, suggesting a greater regional role in narrowbody part‑outs over the forecast period. These trends keep a high proportion of near‑term value concentrated in narrowbodies as they account for the bulk of removals and serviceable part demand in short‑haul networks.

Widebody inductions tend to be less frequent, but they often yield higher per‑aircraft value through engine and nacelle systems alongside specialized avionics. Durability initiatives on engines such as the Trent XWB‑97 illustrate how reliability improvements can shift the timing of parts needs, while not eliminating the strategic role of USM in managing costs and risk. The commercial aircraft disassembly market remains responsive to cargo fleet dynamics and long‑haul network plans, which influence lease decisions and phase‑outs that release larger engines and structures into certified channels. Accredited operators are meeting higher documentation thresholds for widebody components to ensure acceptability in cross‑border transfers and to support more complex integration tasks. Narrowbody and widebody dynamics together ensure a balanced induction flow, with narrowbodies delivering volume and widebodies anchoring premium engine material that supports global engine shops.

By Component Type: Engines Anchor Value, While Landing Gear And Avionics Provide Consistent Pull

Engines held a 51.24% share in 2025 and are projected to grow at 7.68% through 2031, reflecting their central role in residual value and time‑critical maintenance. Reliability enhancements, maturity kits, and shop‑capacity additions by engine OEMs support a more predictable off‑wing cycle over time. Still, fleets continue to source certified engine modules and life‑limited parts to mitigate near‑term constraints. Lufthansa Technik’s focus on LEAP support and integrated digital planning highlights how MROs are aligning predictive demand with teardown-sourced supply to smooth operations. Recognizing engine-centric value capture, accredited dismantlers prioritize engine harvesting and full documentation, ensuring rapid recertification and sale to maintenance networks that need immediate availability. These practices keep engines at the center of realized value for the commercial aircraft disassembly market.

Landing gear and avionics demonstrate consistent pull because of strict documentation requirements and refurbishment cycles that align with airworthiness programs. Buyers prioritize complete overhaul and traceability records for landing gear, which supports steady demand for serviceable assemblies from trusted providers. Avionics flows benefit from cross‑platform commonality and frequent refresh cycles that sustain a lively secondary market for certified units, especially when paired with MRO-managed rotable pools. Stronger documentation practices, including digital provenance and standardized testing, now underpin acceptance for both categories at transfer. Together, these segments provide durable revenue pools that complement engines and help balance the commercial aircraft disassembly market through cycles.

By End‑User: Lessors Monetize End‑Of‑Life, While MROs Integrate For Speed And Assurance

Lessors held a 42.57% share in 2025 and are projected to grow at 6.58% through 2031, as portfolio strategies increasingly weigh engine economics and component value recovery against lease renewals. Circularity commitments and AFRA accreditation have become common signals of quality, pushing lessors and their partners to prioritize higher recovery rates with full traceability for part‑outs. Consignment models and structured teardown programs supported by OEMs add further assurance and raise the yield of certified parts from each aircraft. Lessors also benefit from better reporting on material flows, which strengthens governance and supports financing discussions tied to lifecycle performance indicators.

MROs are building end‑to‑end material solutions by integrating teardown, repair, and distribution, thereby improving cycle time and quality control. Lufthansa Technik and other major providers embed predictive analytics and parts pooling to pre‑position components near hubs ahead of scheduled visits, which strengthens on‑time performance. Integrated models reduce touchpoints, compress certification timelines, and ensure robust documentation, helping operators minimize AOG exposure value. As these models scale, they draw more USM into curated channels with tighter QA systems, which supports the maturation of the commercial aircraft disassembly market. The commercial aircraft disassembly industry, therefore, balances lessor-led asset monetization and MRO‑driven integration, both of which rely on strong accreditation and stable supply partnerships.

Geography Analysis

North America held a 41.65% share in 2025, supported by a large installed base, established storage and dismantling sites in arid climates, and a deep ecosystem of AFRA-accredited and FAA-certified operators. The regional advantage includes faster logistics to major MRO hubs and a long record of compliance with hazardous‑materials handling and depollution standards, which builds buyer confidence in certified parts. Demand for high‑turn components remains strong as airlines balance capacity plans with maintenance constraints and delivery timing, which keeps sourcing strategies focused on trusted suppliers. North American shops continue to work through tight engine capacity conditions and related schedules, which sustains appetite for certified engine materials that can be released quickly under dual certification. This combination of scale, accreditation, and logistics keeps the commercial aircraft disassembly market anchored in North America for near‑term supply needs.

Europe benefits from stringent circular frameworks, standardized accreditation, and large-scale teardown and recycling programs operated under the oversight of leading OEMs and partners. EASA guidance on end‑of‑life practices and EU circular policies support higher recovery targets, which promote selective disassembly and material reuse under audited conditions. Airbus and partners have demonstrated practical composite repurposing at industrial quality, adding momentum to advanced recovery pathways that can scale as methods standardize. European buyers prioritize dual certification, full chain‑of‑custody, and AFRA membership, which influences sourcing decisions and concentrates demand among accredited suppliers. These attributes sustain competitive pricing for certified parts and support greater utilization of rotable pools, thereby reducing AOG risk across dense intra‑European networks.

Asia-Pacific is the fastest-advancing region, growing at a 7.57% CAGR in capability, as teardown and MRO capacity expand to serve a growing fleet footprint. Recent A320neo disassembly projects completed in the Philippines have indicated improved throughput and greater discipline on newer platforms, strengthening regional credibility for high‑value part recovery. Logistics providers are co‑locating services and building bonded facilities to shorten the time from induction to shipment, which reduces lead times for regional carriers. Engine MRO investments, including new LEAP shops in India and OEM-aligned expansions, support the maintenance ecosystem required to absorb more USM locally. As new projects come online, the commercial aircraft disassembly market gains a more balanced global footprint, reducing shipping distances and helping match parts supply with regional fleet needs. This geographic rebalancing enhances resilience for operators across Asia-Pacific and deepens liquidity in global parts exchanges that rely on certified, traceable components.

Competitive Landscape

The commercial aircraft disassembly market is moderately fragmented with signs of consolidation through vertical integration and OEM‑aligned programs. Leading specialists differentiate through AFRA accreditation, multi‑site capability, and integration with repair and distribution functions that reduce cycle time and improve documentation integrity. Companies that combine teardown, repair, and logistics deliver faster release‑to‑service and stronger quality assurance, which drives repeat sourcing from airlines and MROs under pressure to manage AOG exposure. OEM-led lifecycle models are growing, with Boeing’s consignment-based USM program creating a curated supply of parts from retired aircraft under controlled environmental and compliance protocols. These strategic moves reinforce quality expectations and support broader acceptance of certified USM across fleet segments.

Engine reliability actions and shop‑capacity expansions shape the competitive field by influencing the availability of serviceable modules and LLPs. CFM’s durability kits and MRO network expansion address known wear patterns and support better time‑on‑wing stability for LEAP engines, while keeping near‑term demand for certified USM high as fleets transition through upgrades. Lufthansa Technik’s LEAP focus underlines how MROs are integrating predictive analytics to anticipate shortages and align teardown‑sourced materials with scheduled maintenance. Suppliers with deeper digital traceability and QA systems gain an advantage in cross‑border trades that require a complete chain‑of‑custody. As standards converge, leaders who invest in integration and compliance widen their moat in the commercial aircraft disassembly market.

Regional execution is another differentiator. Asia-Pacific operators showcased a rapid A320neo teardown and coordinated logistics that released significant volumes of line‑replaceable units into the aftermarket, improving regional availability and lowering dependence on long pipelines from North America and Europe. In Europe, OEM‑partnered recycling pilots for thermoplastic components demonstrated credible pathways for composite reuse at industrial quality, foreshadowing future cost and sustainability advantages as methods scale. North American incumbents continue to benefit from scale and accreditation density. Across regions, the commercial aircraft disassembly market continues to reward suppliers that can guarantee documentation integrity, minimize turnaround time, and maintain accreditation across FAA, EASA, and AFRA frameworks.

Commercial Aircraft Disassembly Industry Leaders

ComAv Asset Management, LLC

Air Salvage International Limited

CAVU Aerospace, Inc

TARMAC AEROSAVE S.A.S

eCube Solutions Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: AerFin, a prominent aviation asset specialist, announced that it has set an industry milestone by completing the commercial disassembly of multiple aircraft at Hong Kong International Airport (HKIA). This achievement highlights the company’s innovative approach, operational excellence, and commitment to advancing sustainable aviation practices.

- August 2024: Skyservice Business Aviation, headquartered in Toronto, opened a new aircraft recycling division accredited by the Aircraft Fleet Recycling Association for adhering to best practices in disassembly and maintenance. The company, known for its aircraft maintenance and management services and its network of Fixed Base Operators (FBOs) across Canada and the US, aims to deliver sustainable aviation solutions through this initiative.

- July 2024: Vallair, a leading specialist in mature aircraft assets, is conducting a comprehensive teardown of an A330 airframe for CORAX, a Danish company specializing in spare components. The 23-year-old aircraft, previously operated by Hong Kong Airlines, is 80% dismantled. Upon completion, more than 1,500 parts will be extracted as Used Serviceable Material (USM). Vallair's logistics team systematically processes, catalogs, and packages all parts for assessment before repair and subsequent sale by CORAX.

Global Commercial Aircraft Disassembly Market Report Scope

Commercial aircraft disassembly encompasses the teardown, depollution, component harvesting, certification, logistics, storage, and recycling activities that return aircraft parts and materials to regulated reuse or responsible end-of-life outcomes. Core functions include environmental depollution, parts identification and testing, back-to-birth documentation and traceability, engine and landing gear module recovery, airframe dismantling, certified materials recycling, and rotable pooling and distribution.

The global commercial aircraft disassembly market is segmented by application, aircraft type, component type, end-user, and geography. By application, the market covers disassembly and dismantling, recycling and storage, used serviceable material (USM), and rotable parts. By aircraft type, it breaks down into narrowbody, widebody, and regional jets. By component type, it is classified into engines, landing gear, avionics and electronics, fuselage and structures, and cabin interiors. By end-user, the study considers MRO service providers, leasing companies, parts traders and brokers, and OEMs and Tier-1 suppliers. The report also covers the market sizes and forecasts for the commercial aircraft disassembly market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

Source: https://www.mordorintelligence.com/industry-reports/airport-lounges-market

| Disassembly and Dismantling |

| Recycling and Storage |

| Used Serviceable Material (USM) |

| Rotable Parts |

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

| Engines |

| Landing Gear |

| Avionics and Electronics |

| Fuselage and Structures |

| Cabin Interiors |

| MRO Service Providers |

| Leasing Companies |

| Parts Traders and Brokers |

| OEMs and Tier-1 Suppliers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Application | Disassembly and Dismantling | ||

| Recycling and Storage | |||

| Used Serviceable Material (USM) | |||

| Rotable Parts | |||

| By Aircraft Type | Narrowbody Aircraft | ||

| Widebody Aircraft | |||

| Regional Jets | |||

| By Component Type | Engines | ||

| Landing Gear | |||

| Avionics and Electronics | |||

| Fuselage and Structures | |||

| Cabin Interiors | |||

| By End-User | MRO Service Providers | ||

| Leasing Companies | |||

| Parts Traders and Brokers | |||

| OEMs and Tier-1 Suppliers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size and growth outlook for the commercial aircraft disassembly space in 2026–2031?

The commercial aircraft disassembly market size is USD 8.23 billion in 2026 and is forecast to reach USD 11.09 billion by 2031 at a 6.15% CAGR.

Which application leads demand in commercial aircraft disassembly today?

Used Serviceable Material (USM) leads with 53.25% revenue share in 2025 and is projected to grow at an 8.24% CAGR through 2031, supported by tighter supply chains and accredited sourcing.

Why are engines central to value recovery in commercial aircraft disassembly?

Engines combine high unit value with immediate maintenance needs, and they held 51.24% share in 2025 with a projected 7.68% growth path as fleets balance reliability upgrades with quick‑turn USM sourcing.

Which regions are most important for sourcing certified parts from end‑of‑life aircraft?

North America holds the largest 2025 share at 41.65% with dense accreditation and logistics, while Asia‑Pacific is the fastest-advancing on capability as new teardown and MRO projects scale.

How are OEMs and lessors shaping the future of commercial aircraft disassembly?

OEM consignment models and lessor portfolio strategies are integrating lifecycle management and AFRA standards to increase traceable parts recovery, reduce AOG risk, and support circular objectives.

What standards and tools improve trust in certified used parts for aviation?

AFRA accreditation, FAA and EASA quality frameworks, and digital traceability systems reinforce chain‑of‑custody and speed certification, strengthening adoption of USM for time‑critical maintenance.

Page last updated on: