Aircraft Interiors Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 31.45 Billion |

| Market Size (2030) | USD 41.24 Billion |

| Growth Rate (2025 - 2030) | 5.57% CAGR |

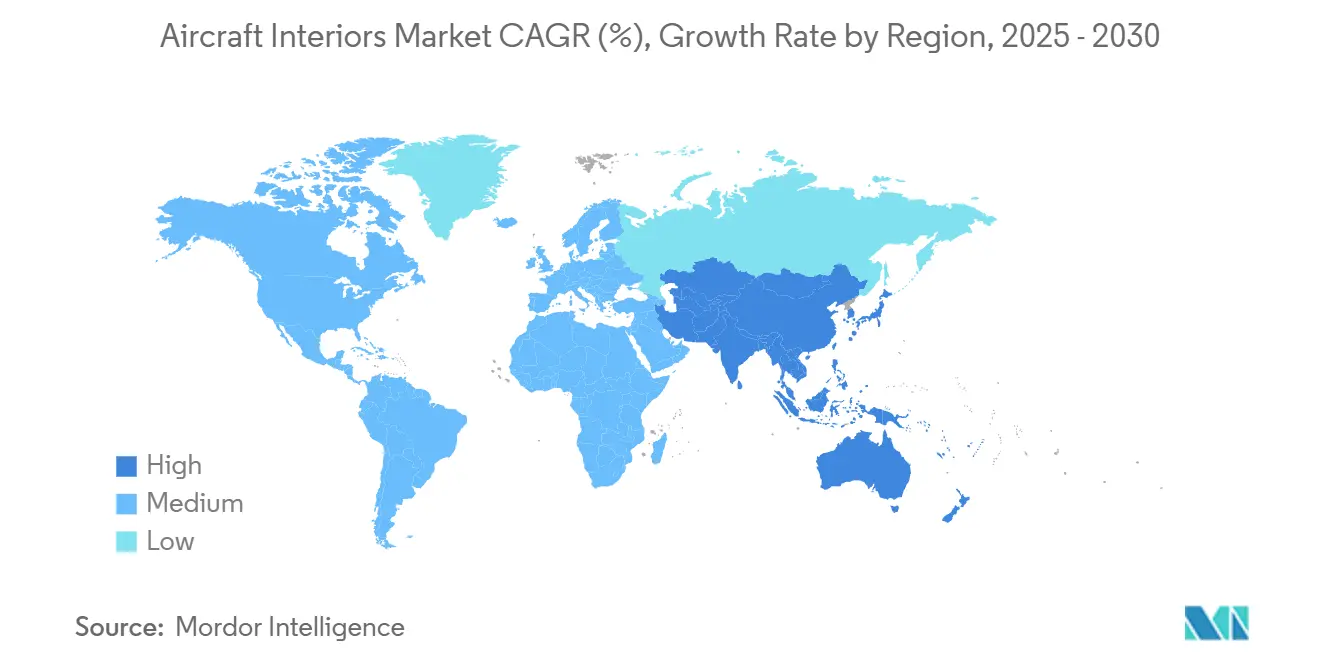

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

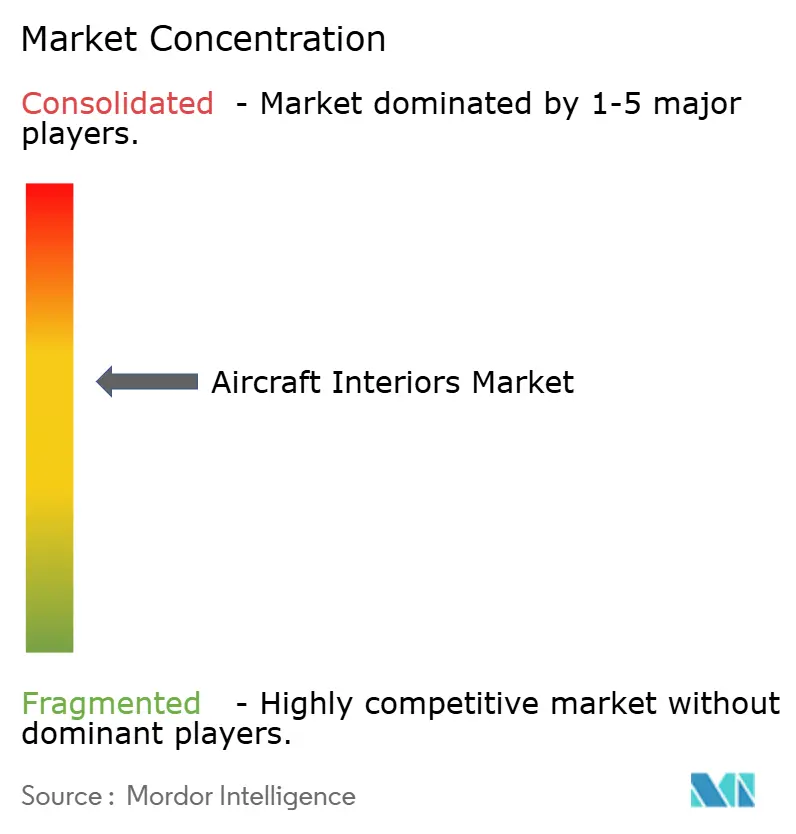

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Interiors Market Analysis by Mordor Intelligence

The aircraft interiors market size reached USD 31.45 billion in 2025 and is forecasted to expand at a 5.57% CAGR to USD 41.24 billion by 2030. Cabin densification programs, rapid fleet growth in emerging regions, lightweight composite adoption, and sustained retrofit activity are reinforcing the resilience of the aircraft interiors market. Airlines continue standardizing 31-inch economy-class pitch while carving out additional premium-economy rows, which lifts ancillary yields without significant floor-plan changes. Simultaneously, carbon-fiber seat structures such as AEGO X’s composite legs cut unit weight and fuel burn, encouraging carriers to favor suppliers that can provide lifecycle savings. The decade-long bloom in low-cost carrier (LCC) fleets drives high-density interior demand, especially in the Asia-Pacific region. At the same time, supply chain bottlenecks steer airlines toward retrofit solutions and mixed delivery-completion models. Competition sharpens as incumbents integrate digital-service layers with physical products, creating bundled propositions that promise predictive maintenance, passenger personalization, and circular-economy credentials.

Key Report Takeaways

- By component, seating led with a 32.56% revenue share in 2024, whereas IFEC recorded the fastest 7.23% CAGR through 2030.

- By aircraft type, narrowbodies commanded 46.24% of the aircraft interiors market share in 2024, while business jets are projected to grow at a 6.24% CAGR to 2030.

- By end user, OEM installations accounted for 62.22% of the aircraft interiors market size in 2024, but the aftermarket segment is advancing at a 6.57% CAGR.

- By geography, North America held 31.45% of 2024 revenues, yet Asia-Pacific is set to expand at a 7.23% CAGR on record fleet commitments.

Global Aircraft Interiors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing cabin densification strategies to maximize airline profitability | +1.2% | Global, with early gains in North America, Europe | Medium term (2-4 years) |

| Rising adoption of lightweight composites to reduce fuel consumption | +1.5% | Global, spill-over to emerging markets | Long term (≥ 4 years) |

| Growing retrofit demand from active and aging fleets | +1.1% | Asia-Pacific core, North America and EU | Short term (≤ 2 years) |

| Expansion of low-cost carrier fleets across emerging markets | +0.9% | Asia-Pacific, South America, Middle East | Medium term (2-4 years) |

| Proliferation of premium economy seating to meet passenger demand | +0.8% | Global, with concentration in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Technology transfer from eVTOL and UAM interiors into commercial aviation | +0.6% | North America and EU, early adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Cabin Densification Strategies to Maximize Airline Profitability

Airlines are refining seat-count economics to lift per-flight returns. Delta will debut tiered main-cabin fares in 2025, widening upsell opportunities while keeping seat pitch unchanged.[1]Travel Market Report, “Delta Air Lines to Launch New Main Cabin Fare in 2025,” travelmarketreport.com British Airways CityFlyer reconfigured E190LRs to 106 seats, using thinner backs and adjustable headrests to preserve ergonomics. Frontier and other ULCCs have introduced limited “first-class” rows, proving densification can still capture premium yields. Premium-economy cabins have matured into a high-margin middle ground that justifies investment in upgraded cushions, privacy wings, and power outlets. Suppliers able to balance slimline density with lumbar comfort are becoming preferred partners, underpinning growth for the aircraft interiors market.

Rising Adoption of Lightweight Composites to Reduce Fuel Consumption

Thermoplastic CFRP structures are prevalent in seat legs, monuments, and sidewalls. AEGO X reports double-digit weight savings per triple-seat assembly, translating into measurable fuel savings on short-haul cycles. Airbus successfully flight-tested bio-based CFRP nose panels that match mechanical strength while lowering lifecycle CO2 emissions.[2]CompositesWorld, “Airbus Flies Bio-Based Carbon Fiber Helicopter Nose Panel,” compositesworld.com Collins Aerospace will supply fiber-reinforced passenger-service units on A320 Airspace cabins, illustrating line-fit scale for advanced materials. FITS Thermoplastic sandwich panels cut 10% weight versus Nomex honeycomb and are fully recyclable, supporting airline sustainability metrics. Weight-focused innovations continue to add momentum to the aircraft interiors market.

Growing Retrofit Demand from Active and Aging Fleets

With global flight hours at 106% of pre-pandemic levels, carriers refurbish cabins to align with evolving brand standards. Airbus forecasts Asia-Pacific services spending will more than double to USD 129 billion by 2043, with enhancements and modernization outpacing other activities. Recent A350 deliveries to Iberia and Lufthansa lacked complete premium suites, forcing post-delivery retrofit programs that tax MRO slots. Retirement rates remain under 2%, so interiors designed for 12-year cycles stay in service longer. Consequently, soft-goods refreshes, monument retrofits, and IFEC swaps are intensifying, boosting aftermarket revenues across the aircraft interiors market.

Expansion of Low-Cost Carrier Fleets Across Emerging Markets

IndiGo aims to double international destinations by March 2025, and its first A321XLR deliveries will require new stretch-seat layouts and galley-lavatory relocations. Cebu Pacific placed a USD 24 billion order for 152 A321neo/A320neo aircraft, each capable of 240 seats in an optimized single-class arrangement. Akasa Air’s 226-aircraft commitment similarly underpins high-density layout demand across Southeast Asia. LCC operating models favor durable, quick-turn interiors, pushing vendors to deliver low-cost, low-weight seat and monument packages that withstand 30-minute turnarounds. These dynamics reinforce rapid growth prospects for the aircraft interiors market in emerging regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ongoing supply chain disruptions in aerospace-grade materials | -0.8% | Global, with acute impacts in North America and Europe | Short term (≤ 2 years) |

| High costs of certification and regulatory compliance requirements | -0.6% | Global, with varying regional standards | Long term (≥ 4 years) |

| Cabin weight and safety trade-off challenges in interior design | -0.7% | Global, with stricter requirements in North America and EU | Medium term (2-4 years) |

| Inflation-driven deferrals of airline capital expenditure plans | -0.5% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ongoing Supply Chain Disruptions in Aerospace-Grade Materials

Ninety-four percent of aerospace executives reported moderate-to-severe parts shortages in 2024, with titanium and specialty steels topping the list. Sanctions on a key Russian supplier removed roughly one-quarter of global titanium mill output, forcing OEMs to dual-source at higher cost. Boeing’s counterfeit-titanium incident exposed multi-tier traceability gaps, triggering decade-long document audits and slowing line-fit interiors due to suspended seat-track deliveries. Specialty steel mills faced outages and raw-material tightness, prompting airlines to stockpile spare floor beams, which added logistics costs and tied up working capital. IATA confirmed these pressures will persist through 2025, complicating cabin-retrofit timelines

High Costs of Certification and Regulatory Compliance Requirements

FAA ventilation regulations require 0.55 lb of fresh air per minute per occupant, and ongoing bleed-air contamination work could trigger additional sensor mandates.[3]Federal Aviation Administration, “Cabin Air Quality,” faa.gov SAE emergency-lighting standard Revision H raises photoluminescent performance thresholds, pushing vendors to redesign exit-path markings. SWISS needed 1.5 tons of ballast to offset its enclosed first-class suites, highlighting the cascading certification impacts of weight redistribution. Industry task-force reviews show FAA resource constraints stretching approval timelines, especially for additive-manufactured parts, thereby delaying innovative interior programs. Elevated certification budgets place particular strain on smaller entrants, tempering near-term adoption of novel interior solutions and marginally tempering aircraft interiors market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: IFEC Systems Drive Digital Transformation

The seating category accounted for 32.56% of 2024 revenues. Yet, IFEC is poised to outpace all other components at a 7.23% CAGR through 2030, signaling a pivot to digitally enabled cabins that monetize passenger engagement. Content-licensing fees surpassed USD 300 million in 2024, underscoring the growing value airlines attach to exclusive movies and games. The aircraft interiors market size attributable to IFEC upgrades alone is projected to reach USD 8.2 billion by 2030, buoyed by next-generation Ka-band connectivity packages that blend streaming, real-time e-commerce, and predictive maintenance data feeds.

IdeaNova and Safran debuted IPTV and user-generated-content mirroring tools in 2025 that treat seatback screens as network nodes rather than isolated displays. Simultaneously, programmable LED lighting mimics circadian rhythms to reduce jet lag, and composite galleys deliver 10% weight savings. Suppliers are marrying sustainable materials modularly so monuments can be swapped or refurbished multiple times during an airframe’s life. Regulatory oversight from the FAA and EASA continues to shape material selection and flammability standards, ensuring safety while encouraging innovations that help scale the aircraft interiors market.

By Aircraft Type: Business Jets Propel Premium Customization

Narrowbodies held a 46.24% slice of the aircraft interiors market share in 2024, reflecting robust single-aisle production rates. In contrast, business jets are advancing at a 6.24% CAGR on the back of an expected 8,500-unit delivery wave this decade.[4]Honeywell Aerospace, “New Business Aviation Outlook Forecasts High-Flying Demand,” aerospace.honeywell.com In value terms, the aircraft interiors market size for premium and bespoke business-jet cabins is forecast to reach USD 4.9 billion by 2030.

Airbus Corporate Jets notes more than 80% of customers now demand fully customized layouts, including spa zones and wellness lighting. Lufthansa’s Allegris widebody program, which will install over 31,000 new seats, illustrates parallel investment in twin-aisle fleets. At the same time, RECARO’s 75,000-seat deal on Eve eVTOLs hints at future cross-pollination of lightweight designs. Customization is now extending into noise-dampening sidewalls and smart-glass windows, indicating that differentiation is no longer limited to soft goods. These trends collectively reinforce premium demand pockets, sustaining the upward trajectory of the aircraft interiors market.

By End User: Aftermarket Momentum Accelerates

OEM installations still capture 62.22% of 2024 spend, yet aftermarket revenues are climbing at a 6.57% CAGR as airlines keep older jets flying amid delivery delays. Accenture observes that 42% of aerospace executives expect near-term MRO budget increases, with interiors a priority category. Retrofit-centric growth lifted the aircraft interiors market size for aftermarket services to USD 11.3 billion in 2025, and value is projected to top USD 15.5 billion by 2030.

Collins Aerospace now offers three modular upgrade paths for Pinnacle economy seats that reuse existing structures, lowering waste and certification effort. Seat shortages have delayed many OEM line-fits, forcing operators to accept “green” deliveries and schedule completion slots at independent MRO facilities. EASA Part 145 repair stations with seat-integration capabilities are, therefore, commanding premium labor rates. The trend signals a durable revenue pillar for suppliers that pivot toward quick-turn refurb solutions, further energizing the aircraft interiors market.

Geography Analysis

North America generated 31.45% of 2024 revenue, backed by premium-cabin investment programs, mature MRO networks, and sustained replacement cycles among legacy carriers. Major US airlines are trialing larger premium-economy cabins, while Canadian operators refresh narrowbody interiors to support ultra-long-haul transpacific missions. Seat and IFEC vendors benefit from consolidated airline purchasing and clear FAA certification pathways, positioning the region as a technology test bed that later influences global uptake.

Asia-Pacific is the standout growth engine with a 7.23% CAGR forecast through 2030, propelled by fleet commitments exceeding 4,000 single-aisle jets and a swelling middle-class traveler base. Airbus expects regional maintenance outlays to rise from USD 43 billion in 2024 to USD 109 billion by 2043, creating structural demand for retrofit galleys, lavatories, and connectivity packages. LCCs in India, Indonesia, and the Philippines favor high-density layouts, stimulating volume orders for slimline seating and lightweight monuments that lower turnaround times.

Europe faces capacity headwinds tied to supply-chain lags, yet premium cabin programs like Lufthansa’s Allegris drive high-margin orders for first-class suites and privacy doors. Regulatory synchronization between EASA and FAA lowers certification duplication, making the region a crucial second-wave adopter of new materials. The Middle East leverages mega-hub models to secure bespoke widebody interiors, while Africa and South America show incremental progress amid infrastructure gaps. Collectively, these regional dynamics keep the aircraft interiors market on a steady upward course.

Competitive Landscape

Market concentration is moderate. The top tier, Safran SA, Collins Aerospace, Panasonic Avionics Corporation, Jamco Corporation, and Honeywell International Inc., leverage integrated portfolios and long-term supplier-furnished-equipment (SFE) contracts. Insperial’s MGR Foamtex and Airline Graphics acquisitions expand its materials footprint and position it as a multi-continent fabric supplier. Yingling Aviation’s purchase of GETI exemplifies MRO consolidation that aims to capture more retrofit revenue.

Technology integration is a primary differentiator. Collins and Panasonic’s MAYA suite merges a 45-inch OLED display with AI-driven personalization, raising the bar for business-class experiences. Airbus’ Digital Alliance now includes Collins, creating a cross-OEM predictive-maintenance platform that links cabin-system health with airframe data. Start-ups are exploiting additive manufacturing to produce low-run, form-fit parts that bypass traditional tooling costs, though certification pathways remain lengthy. Sustainability is opening whitespace for bio-derived laminates and closed-loop textiles, with F/List unveiling heat-release-compliant wood veneers that do not add weight. Competitive intensity will remain high as suppliers race to secure scarce raw materials and navigate evolving regulatory hurdles within the aircraft interiors market.

Aircraft Interiors Industry Leaders

Safran SA

Honeywell International Inc.

JAMCO Corporation

Collins Aerospace (RTX Corporation)

Panasonic Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: AXISCADES Technologies secured two pilot projects for aircraft cabin interior design and retrofits, marking its entry into the cabin interiors market. The comprehensive project scope encompasses aircraft cabin design, seating systems engineering, electrical wiring design and integration, and retrofit and modernization solutions.

- May 2024: Panasonic Avionics Corporation of North America and EVA Air signed an agreement to install in-flight entertainment (IFE), connectivity systems, and digital services on 54 of EVA Air's widebody and narrowbody aircraft.

- June 2023: United Airlines and Panasonic Avionics established an agreement to implement Panasonic's Astrova in-flight entertainment (IFE) system. The airline plans to equip selected new B787 and A321XLR aircraft with the system.

Global Aircraft Interiors Market Report Scope

| Seating |

| Cabin Lighting |

| In-flight Entertainment and Connectivity (IFEC) |

| Galleys and Lavatories |

| Window and Windshields |

| Floor Panels and Sidewalls |

| Narrowbody |

| Widebody |

| Regional Jets |

| Business Jets |

| Military Aircraft |

| OEM |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Seating | ||

| Cabin Lighting | |||

| In-flight Entertainment and Connectivity (IFEC) | |||

| Galleys and Lavatories | |||

| Window and Windshields | |||

| Floor Panels and Sidewalls | |||

| By Aircraft Type | Narrowbody | ||

| Widebody | |||

| Regional Jets | |||

| Business Jets | |||

| Military Aircraft | |||

| By End User | OEM | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the aircraft interiors market be by 2030?

The aircraft interiors market is projected to reach USD 41.24 billion by 2030, reflecting a 5.57% CAGR from 2025.

Which component category is growing fastest in cabin retrofits?

In-flight entertainment and connectivity (IFEC) systems are expanding at a 7.23% CAGR as airlines integrate streaming, e-commerce, and real-time data services.

Why is Asia-Pacific the most promising region for cabin suppliers?

Fleet expansion plans exceeding 4,000 single-aisle deliveries and aggressive LCC growth drive a 7.23% regional CAGR through 2030.

How are supply-chain issues affecting interior programs?

Titanium and specialty-steel shortages have stretched lead times, prompting airlines to accept green aircraft and schedule post-delivery completions.

Are aftermarket opportunities surpassing OEM installations?

OEM work still leads, but retrofit demand is growing faster at 6.57% CAGR as airlines refresh cabins while waiting for delayed deliveries.

Page last updated on: