Crashworthy Aircraft Seats Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

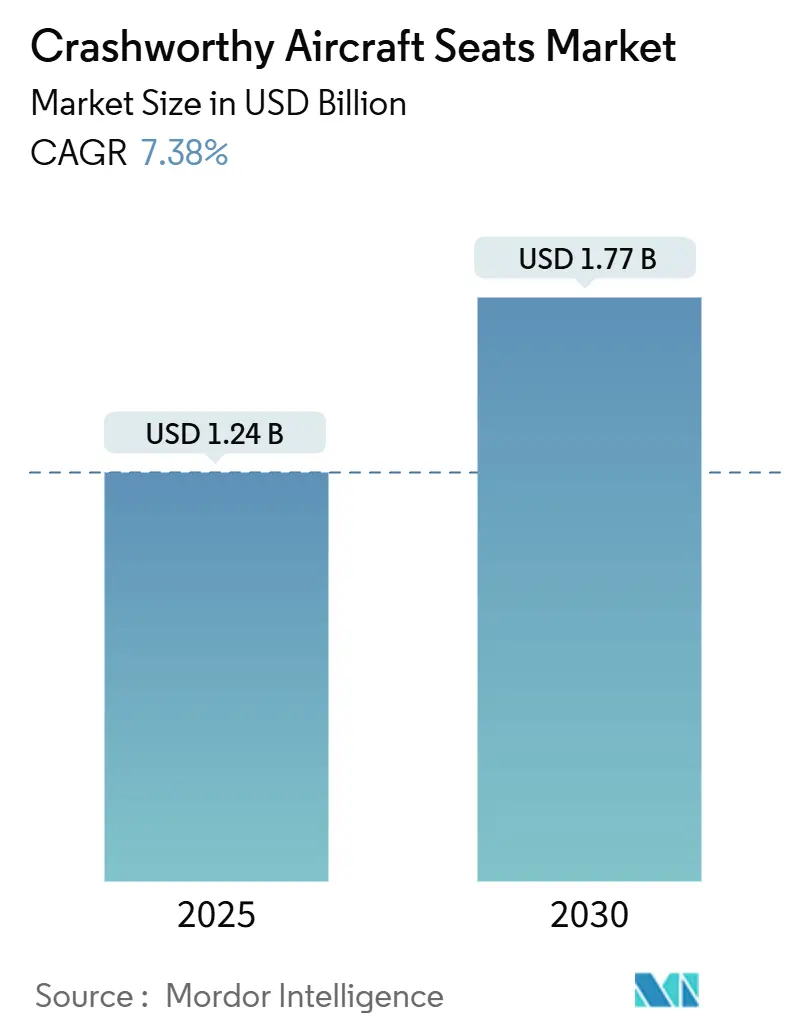

| Market Size (2025) | USD 1.24 Billion |

| Market Size (2030) | USD 1.77 Billion |

| Growth Rate (2025 - 2030) | 7.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Crashworthy Aircraft Seats Market Analysis by Mordor Intelligence

The crashworthy aircraft seats market size stood at USD 1.24 billion in 2025 and is projected to reach USD 1.77 billion by 2030, advancing at a 7.38% CAGR through the forecast period. The current valuation already reflects broad uptake of next-generation ejection seats for the F-35, T-7A Red Hawk, and other front-line combat aircraft whose procurement schedules were locked in earlier Defense Authorization Acts. Alongside these marquee programs, hundreds of legacy fighters and rotary platforms remain in service, and their operators view crashworthy seating as the most economical survivability upgrade that can be executed without grounding fleets. NATO’s enforcement of MIL-STD-3050 and analogous Department of Defense (DoD) mandates hard-code minimum attenuation levels, giving planners a clear technical baseline and streamlined budget justification.[1]Source: European Defence Agency, “European Defence Spending Surge 2022-2028,” eda.europa.eu Composite structures capable of shedding 20-30% mass improve aircraft range and payload while meeting energy-absorption thresholds, so prime contractors now routinely specify hybrid metal-composite frames. Finally, embedded sensors and autonomous sequencing reduce pilot workload, which is a priority as one-pilot cockpits become the norm.

Key Report Takeaways

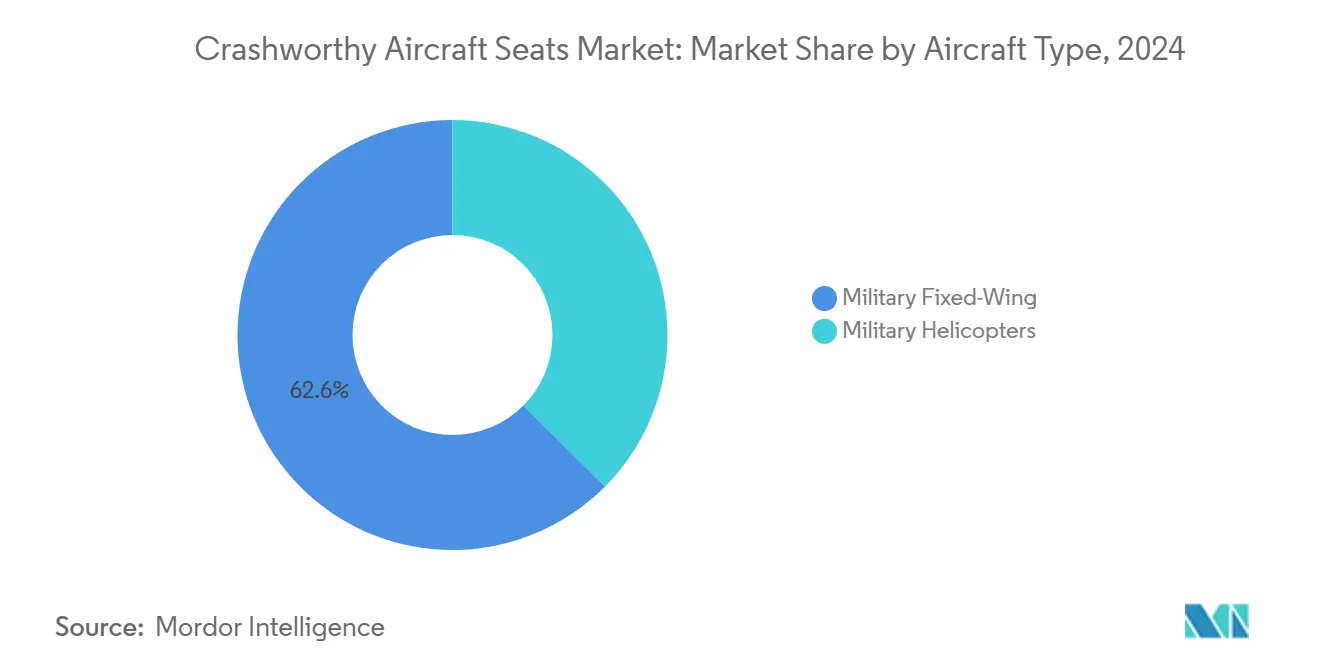

- By aircraft type, military fixed-wing platforms led with 62.56% of the crashworthy aircraft seats market share in 2024, whereas military helicopters posted the fastest growth at 8.36% CAGR to 2030.

- By seat type, ejection seats held a 46.72% share of the crashworthy aircraft seats market in 2024, and helicopter systems are expanding at an 8.20% CAGR through 2030.

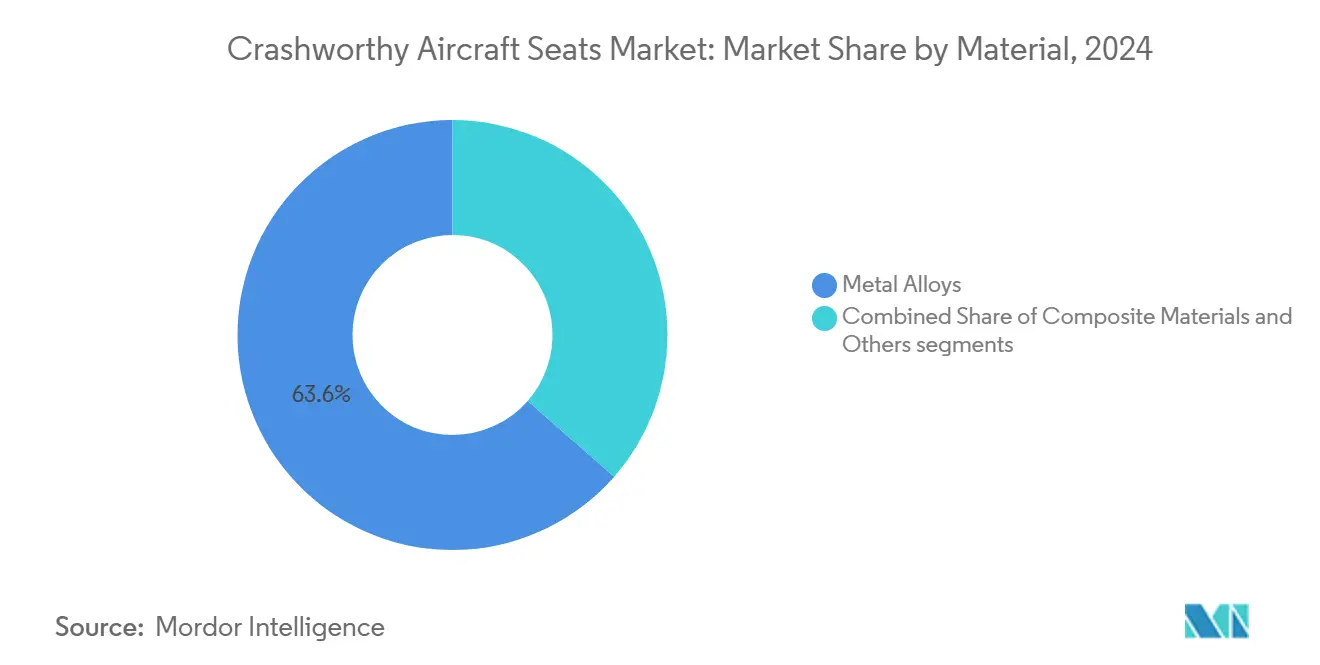

- By material, metal alloys accounted for a 63.55% share in 2024, while composites are forecasted to rise at a 10.65% CAGR to 2030.

- By end-user, OEM installations increased 61.75% in 2024, while the aftermarket advanced at a 9.70% CAGR over the same period.

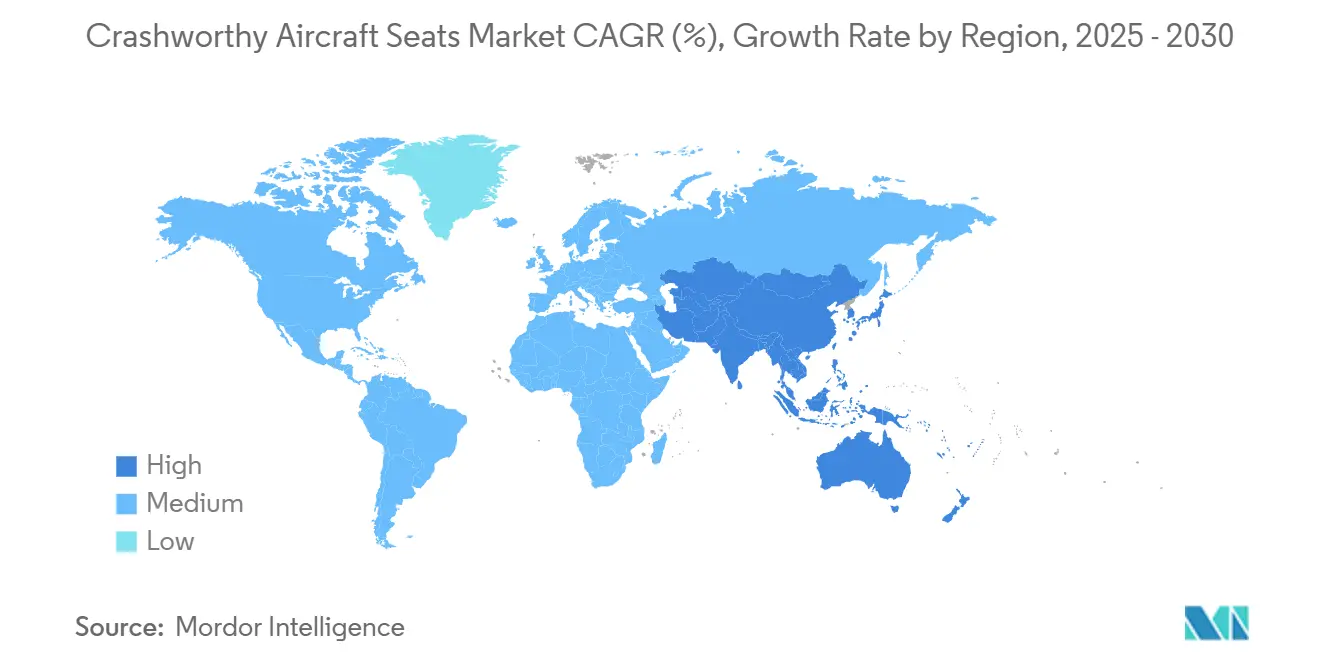

- North America dominated, with a 36.87% share in 2024, but Asia-Pacific is growing the quickest, at a 9.45% CAGR through 2030.

Global Crashworthy Aircraft Seats Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Modernization of ageing military helicopter fleets | +1.2% | North America and Europe primarily | Medium term (2-4 years) |

| Procurement of 5th and 6th-generation combat aircraft with zero-zero ejection seats | +1.8% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| NATO and DoD survivability mandates (e.g., MIL-STD-3050) | +1.1% | North America, Europe, allied nations | Medium term (2-4 years) |

| Autonomous seat-sequencing and crash-sensing technologies | +0.9% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Surge in side-by-side trainer aircraft creating dual-seat demand | +0.8% | North America and Asia-Pacific | Medium term (2-4 years) |

| AUKUS and Indo-Pacific alliance retrofit programs for legacy platforms | +0.7% | Asia-Pacific and allied nations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

NATO and DoD Survivability Mandates Drive Systematic Upgrades

NATO’s imposition of MIL-STD-3050 crashworthiness standards has converted what was once a voluntary adoption into a codified requirement for every member and partner air force.[2]Source: NATO Standardization Office, “MIL-STD-3050 Compliance,” nso.nato.intModernization departments now receive multi-year appropriations specifically earmarked for seat replacement, enabling phased retrofits that align with scheduled depot maintenance. Because the standard sets explicit vertical load and pulse attenuation thresholds, suppliers can engineer modular kits that drop into older cockpits without re-certifying the entire airframe, trimming downtime and engineering hours. Across Europe, the European Defence Agency (EDA) estimates that up to one-third of in-service fighters and nearly half of older helicopters will complete a seating upgrade before 2030, creating a recurring order book for prime contractors. Outside the Alliance, nations pursuing interoperability, such as Sweden and Finland, mirror the requirement to maintain joint mission readiness. As a result, the market experiences predictable demand spikes synchronized with five-year defense spending cycles, smoothing production volumes for tier-one seat manufacturers.

Procurement of 5th and 6th-Generation Combat Aircraft Accelerates Demand

Fifth-generation fighters mandate zero-zero seats that must initiate safely at the runway and during Mach-class escape envelopes, elevating the technical benchmark relative to fourth-generation predecessors.[3]Source: John A. Tirpak, “T-7A Red Hawk Trainer Faces Ejection Seat Challenges,” Air Force Magazine, airforcemag.com The ongoing F-35 program alone locks in thousands of Martin-Baker Mk16 units over its life-of-type, and follow-on iterations such as Japan’s F-X and the Franco-German-Spanish FCAS add a similar technology stack. Each next-gen cockpit integrates digital flight-control symbology with seat electronics, so suppliers ship integrated wiring, health-monitoring sensors, and software updates alongside mechanical assemblies. Collins Aerospace’s ACES 5, chosen for the T-7A, underscores how trainer aircraft are now developed in lockstep with frontline fighters, guaranteeing identical escape performance for student pilots. Government-to-government sales agreements often bundle sustainment contracts, granting the seat OEM long-term parts and service revenue. The procurement tempo, therefore, elevates the baseline production rate for crashworthy systems well beyond historic norms and provides a hedge against volatility in retrofit budgets.

Modernization of Aging Military Helicopter Fleets Creates Retrofit Opportunities

Rotorcraft fleets such as the UH-60 Black Hawk, NH90, and Tiger approach 30-40 years of service, and fatigue crack inspections routinely cite seats, harnesses, and rails among life-limited items requiring overhaul. Compared with full re-winging or drivetrain replacement, installing energy-absorbing seats offers a comparatively low-cost path to extend airframe life while meeting current survivability doctrine. Vertical impact tests must prove that crews remain within injury thresholds when aircraft settle from hover at velocities exceeding 30 ft/s, pushing designers toward stroking mechanisms, crushable tubes, and advanced foam geometries. Since helicopters often operate at low altitude in contested areas, crash-phase survivability is directly linked to mission continuation and personnel retention, strengthening the case for immediate upgrades. Operators also seize the opportunity to fit smart textiles that monitor occupant vitals, a capability that dovetails with broader soldier-system digitization trends. Consequently, the retrofit channel registers one of the steepest growth curves within the crashworthy aircraft seats market.

Autonomous Seat-Sequencing Technologies Enhance Safety Margins

The latest seat generations embed inertial measurement units, micro-electromechanical sensors, and high-speed processors that decide whether to fire the rocket catapult. Flight parameters such as bank angle, sink rate, and angle-of-attack are sampled in milliseconds. If thresholds are exceeded, the system triggers ejection, eliminating lag from pilot reaction or incapacitation. Autonomous sequencing also synchronizes dual or tandem seats, ensuring optimal spacing between firings to prevent collision within the escape trajectory. Beyond raw decision logic, predictive algorithms pre-arm canopies, adjust seat-back angle, and modulate rocket thrust to match instantaneous altitude and speed. These incremental improvements raise safe-egress probability without adding cognitive burden on crews already managing high-G events or degraded visibility. As air forces pivot toward augmented-reality helmets and network-centric flight displays, integrating seat health telemetry becomes straightforward, enabling condition-based maintenance that lowers life-cycle cost even as survivability metrics climb.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating R&D and qualification costs for dynamic-sled testing | -0.8% | Global, burdening smaller firms | Short term (≤ 2 years) |

| Defense budget realignments delaying seat-upgrade programs | -0.6% | Worldwide with regional variations | Medium term (2-4 years) |

| ITAR/EAR export restrictions curbing international sales | -0.5% | Affects non-allied nations globally | Long term (≥ 4 years) |

| Supply bottlenecks for rocket-motor and pyro-mechanism components | -0.4% | Concentrated in specialist supplier zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating R&D and Qualification Costs Challenge Market Entry

Dynamic-sled testing replicates vertical and longitudinal crash pulses, requiring bespoke track systems, high-speed cameras, and data acquisition suites that only a handful of laboratories possess. Booking a facility can involve waiting lists exceeding six months, and each campaign demands multiple dummy loads, cartridge firings, and post-test inspections, quickly inflating expenses past USD 2 million. When anomalies surface, additional test runs compound the outlay. Industry veterans can spread these costs across large order books, but startups struggle to finance such programs without diluting equity, thereby stifling disruptive innovation. Regulatory authorities tighten margins further by mandating digital traceability and cybersecurity reviews for instrumentation, adding non-recurring engineering hours. The cost-per-unit can become prohibitive if amortized over small volumes for niche seat variants such as those tailored to special-mission helicopters. As a result, the barrier to entry preserves incumbent market share but slows technology diffusion, mildly depressing overall growth.

Defense Budget Realignments Delay Upgrade Programs

Defense ministries periodically reallocate funds toward cyber-warfare, satellite assets, or unmanned platforms, often viewing seat retrofits as deferrable when immediate kinetic capability is not jeopardized. Political transitions or macroeconomic shocks can trigger mid-cycle rescissions that push planned seat acquisitions into later fiscal years. Indonesia’s experience in 2024 illustrated the ripple effect: a currency-driven budget squeeze forced the air force to shelve cockpit safety upgrades in favor of spare parts for transport aircraft, extending legacy seats beyond their certified service life. While operators eventually resume modernization, shifting timelines disrupt supply-chain forecasts, prompting manufacturers to idle capacity or carry higher inventory, which erodes margins. Multi-year procurement contracts mitigate some volatility, yet supplementary appropriations remain vulnerable to parliamentary debate. Consequently, the cyclical nature of public-sector finance introduces a drag on the otherwise robust growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Fixed-Wing Dominance Amid Helicopter Growth Acceleration

Military fixed-wing aircraft generated 62.56% of the crashworthy aircraft seats market share in 2024, owing mainly to ongoing F-35 low-rate initial production lots, F-15EX conversions, and Eurofighter modernization packages that specify premium seats priced between USD 400,000 and USD 600,000 each. These high ticket values quickly translate into significant revenue even on modest unit volumes. Fixed-wing programs also benefit from long design cycles; once a seat is qualified on a fighter, it stays linked for 30 years, locking manufacturers into sole-source positions.

Military helicopters, while currently the smaller revenue pool, post an 8.36% CAGR through 2030 as operators rush to extend service life without committing to new airframes. Crash-attenuating seats for Black Hawk or NH90 fleets cost less per unit but come in sets of four to 20 per helicopter, and replacement intervals shorten due to vibration loads and field operations. Therefore, aggregate demand rises quickly, and modeling firms expect the rotorcraft segment to narrow the revenue gap with fixed-wing by the decade's end. Helicopter retrofit programs are also favored because seat swaps can coincide with avionics or engine upgrades during regular depot visits, avoiding extra downtime. Complying with MIL-STD-58095 vertical crash criteria often requires only seat-rail reinforcement and updated floor brackets, streamlining certification.

Conversely, next-generation fixed-wing jets incorporate stealth shaping, meaning even minor cockpit changes might trigger costly radar-cross-section reassessments; hence, seats must be designed in from program inception. The contrasting retrofit economics explain why rotorcraft volume grows faster, even though fighters keep headline revenue dominance. The combination of high unit-price fighter seats and high unit-volume helicopter seats yields a balanced opportunity set for manufacturers, ensuring no single platform class monopolizes the market outlook.

By Seat Type: Ejection Seats Lead While Helicopter Systems Gain Momentum

Pilot and crew ejection seats controlled 46.72% of the crashworthy aircraft seats market size in 2024, reflecting both premium pricing and the technical sophistication required for zero-zero escape envelopes. These products integrate rocket motors, crash sensors, digital sequencers, and often personal survival packs, driving costs far above non-ejection systems. Because fighter cockpits are mission-critical, air forces rarely switch suppliers mid-life, creating sticky revenue streams for incumbents such as Martin-Baker and Collins Aerospace.

Crash-attenuating helicopter seats grow at 8.20% CAGR primarily because modern combat operations involve low-altitude profiles, making vertical shock the primary injury vector. Designs now use composite bucket shells and staged crush tubes that progressively absorb energy, keeping spinal loads within survivable thresholds. Though individually cheaper, helicopter seats multiply across troop, gunner, observer, and medevac roles, turning transport variants into high-volume customers on the aftermarket. Troop seats often employ foldable or palletized frames, allowing quick reconfiguration between transport and assault missions. Observer and gunner positions integrate arm-mount interfaces for stabilized weapon systems, adding complexity and value to what was once considered secondary seating. As multi-mission helicopters receive modular cabin designs, seat OEMs must offer plug-and-play kits compatible with cargo rails, oxygen lines, and crash-sensor buses. These dynamics deliver sustained growth even as ejection seats capture industry headlines. Meanwhile, developmental efforts in modular rocket packs and universal firing handles aim to reduce variant count across fighter fleets, opening the possibility for future single-family seat architectures that could lower life-cycle cost without sacrificing performance.

By Material: Metal Alloys Dominate as Composites Surge

Conventional aluminum-lithium (Al-Li) and titanium alloys maintained a 63.55% share in 2024. Their material properties are well recorded in certification databases, allowing engineers to confidently model deformation and fatigue. Established machine shops possess decades of tooling experience, and raw-material supply chains remain resilient, minimizing lead-time risk during production surges. Metal alloys also efficiently dissipate heat from rocket exhaust for ejection seats, protecting downstream components.

Composite materials, however, record a 10.65% CAGR, addressing two primary pain points: weight and corrosion. Carbon fiber laminates reduce mass by up to one-third, freeing margin for helmet-mounted displays, sensor pods, or extra fuel. Aramid honeycomb cores distribute load evenly, enabling smoother deceleration curves during crash events. Many new designs integrate woven sensor fibers that relay real-time strain and damage data to maintenance crews, aligning with condition-based support philosophies. These innovations converge on the same survivability targets while shrinking aircraft operating costs to lower structural weight. Adoption accelerates where composite manufacturing can piggyback on broader aerospace production lines, such as autoclaves used for airframe skins. Diehl Aviation’s recyclable fiber initiative exemplifies the push to blend performance with sustainability, appealing to defense ministries that now publish environmental impact reports. Certification hurdles remain, including fire-smoke-toxicity metrics and impact resistance demonstration, but successful pilot programs lower the barrier for follow-on projects. Over time, hybrid architectures combining metallic load paths with composite energy absorbers may become the norm, gradually eroding pure-metal dominance while maximizing each material’s strengths.

By End-User: OEM Dominance with Growing Aftermarket Opportunities

OEM installations supplied 61.75% of 2024 revenue, and this channel enjoys steady visibility because seats are frozen into digital baselines early in aircraft development. OEM contracts typically cover initial spares, support equipment, and sometimes local assembly facilities, embedding the seat maker for the platform’s 30-year lifespan. The T-7A program, for instance, mandates seat training aids, data loaders, and field service reps across all US Air Force bases.

The aftermarket, advancing at 9.70% CAGR, is fueled by service-life extensions where seat fatigue life or pyrotechnic shelf life has expired, even while airframes keep flying. Martin-Baker’s global repair centers overhaul more than 1,000 seats a year, swapping rocket motors, harnesses, and crash-sensor modules. Retrofit kits introducing composite backs or autonomous sequencing qualify as major modifications, commanding premium pricing. Consequently, profit margins on aftermarket parts frequently surpass OEM delivery margins, making this segment strategically important despite smaller immediate volumes. Secondary value streams include technical-publication updates, software patches for seat-sequencing firmware, and training-simulator inserts that mirror in-cockpit hardware for realistic ejection drills. As fleets diversify, mixing fourth-generation fighters with fifth-generation jets, air forces lean on seat OEMs to harmonize maintenance intervals, further anchoring long-term aftermarket demand. Looking ahead, predictive analytics fed by seat-embedded sensors will signal cartridge replacement or cushion wear before failure, shifting support models from hours-based to condition-based maintenance. Such digital services promise recurring revenue well after physical seat deliveries peak, ensuring a balanced portfolio for manufacturers.

Geography Analysis

North America contributed 36.8% of global revenue in 2024, underpinned by US defense budgets exceeding USD 800 billion and sustained procurement of F-35, F-15EX, and T-7A platforms. Domestic seat production benefits from streamlined certification via the Air Force Life Cycle Management Center, while foreign military sales channels extend North American designs to Israel, Finland, and other allies on favorable financing terms. Canada’s CF-18 life extension includes seat overhauls, and Mexico’s security cooperation programs create niche orders, collectively adding diversification within the region.

Asia-Pacific registers the fastest regional CAGR of 9.45%, driven by China’s expanding inventory, India’s Tejas and AMCA indigenous programs, and South Korea’s KF-21 development, each demanding advanced seats and support ecosystems. Australia’s 72-unit F-35A fleet, completed in 2024, locked in full spares packages and local depot rights for Mk16 seats, signaling long-run aftermarket revenue. Geopolitical flashpoints incentivize interim retrofits, accelerating order placement before new-build jets roll off production lines.

Europe retains a robust customer base via Tempest, Eurofighter, and Rafale projects, plus cross-service helicopter upgrades mandated by the European Defence Agency’s survivability agenda. Budget surges between 2022 and 2028 allocate resources for safety retrofits, with Germany prioritizing ejection-seat updates during its Eurofighter Quadriga package. Middle East and Africa remain smaller but attractive frontier regions; Saudi Arabia’s Typhoon fleet and the UAE’s Mirage upgrade include Western seats, while Israel integrates US seats into locally modified cockpits. Although export controls temper some opportunities, offset agreements and technology-transfer clauses keep European and US suppliers engaged.

Competitive Landscape

The crashworthy aircraft seats market exhibits moderate concentration, leaving room for specialized niche suppliers. Martin-Baker maintains leadership through a life-saving metric exceeding 7,500 personnel, cultivating customer trust and influencing procurement boards. Collins Aerospace leverages RTX’s scale to bundle avionics, oxygen systems, and seating into turnkey cockpit packages, lowering total acquisition cost for airframe OEMs. BAE Systems focuses on integration within European programs, exploiting its role in Eurofighter and Tempest to secure seat contracts.

Competition hinges on technological differentiation rather than price alone. Patents filed in 2024 cover new stroke-limiter mechanisms, articulated head-rests tailored for helmet-mounted displays, and low-toxicity propellant formulations, indicating a push toward incremental but meaningful performance gains. Boeing’s USD 8.3 billion acquisition of Spirit AeroSystems expands the aerospace giant’s internal capabilities, potentially allowing deeper integration of seat structures into forward fuselage assemblies.

While high barriers to entry persist, namely qualification costs and pyrotechnic expertise, regional players in Turkey, India, and South Korea are investing in indigenous seat projects to reduce import dependence. Incumbents respond with co-production and technology-transfer agreements, trading intellectual property for guaranteed volumes and market access. Supply chain resilience emerges as a competitive differentiator; firms with multiple rocket-motor sources and in-house energetics labs are better positioned to meet tight delivery schedules, particularly under surge demand scenarios.

Crashworthy Aircraft Seats Industry Leaders

RTX Corporation

BAE Systems plc

Israel Aerospace Industries Ltd.

AUTOFLUG GmbH

Martin-Baker Aircraft Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Martin-Baker, a leading ejection seat manufacturer, announced its plans to open a Bengaluru facility in 2025 to produce and maintain seats for the Indian Air Force and exports. The company is delivering IN16G seats for TEJAS MK-1A fighters and proposing MK18 seats for TEJAS MK-2, AMCA, and TEDBF programs.

- December 2024: The Spanish government signed a contract with NATO Eurofighter and Tornado Management Agency (NETMA) for 25 Eurofighter aircraft under the Halcon II programme, expanding its fleet to 115. Deliveries begin in 2030, enhancing Spain’s air power and NATO role and boosting demand for crashworthy seats.

Global Crashworthy Aircraft Seats Market Report Scope

| Military Fixed-Wing |

| Military Helicopters |

| Pilot/Crew Ejection Seats |

| Crash-Attenuating Helicopter Seats |

| Troop/Passenger Crashworthy Seats |

| Gunner and Observer Seats |

| Composite Materials |

| Metal Alloys |

| Others |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Aircraft Type | Military Fixed-Wing | ||

| Military Helicopters | |||

| By Seat Type | Pilot/Crew Ejection Seats | ||

| Crash-Attenuating Helicopter Seats | |||

| Troop/Passenger Crashworthy Seats | |||

| Gunner and Observer Seats | |||

| By Material | Composite Materials | ||

| Metal Alloys | |||

| Others | |||

| By End-User | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the crashworthy aircraft seats market?

The crashworthy aircraft seats market size stood at USD 1.24 billion in 2025 and is projected to reach USD 1.77 billion by 2030, advancing at a 7.38% CAGR through the forecast period.

How fast is demand for helicopter crash-attenuating seats growing?

Crash-attenuating helicopter seats are expanding at an 8.20% CAGR through 2030.

Which region is the fastest growing for crashworthy seating solutions?

Asia-Pacific posts the highest regional growth with a 9.45% CAGR driven by fleet modernization.

Why are composites gaining popularity in military seat construction?

Composite materials cut seat weight by up to 30% while improving energy absorption and are growing at a 10.65% CAGR.

Who are the leading suppliers of ejection seats?

Martin-Baker, Collins Aerospace, and BAE Systems top the supplier list due to proven zero-zero seat portfolios.

Page last updated on: