Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2017 - 2023 |

| Market Size (2025) | USD 1.62 Billion |

| Market Size (2030) | USD 1.97 Billion |

| Growth Rate (2025 - 2030) | 4.03% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Commercial Aircraft Cabin Interior Market Analysis by Mordor Intelligence

The North America Commercial Aircraft Cabin Interior Market size is estimated at 1.62 billion USD in 2025, and is expected to reach 1.97 billion USD by 2030, growing at a CAGR of 4.03% during the forecast period (2025-2030).

The North American aircraft cabin interior market is experiencing significant transformation driven by airlines' focus on enhancing passenger experience while improving operational efficiency. Airlines are increasingly adopting lightweight materials and innovative designs across aircraft cabin components to reduce fuel consumption and operating costs. For instance, aircraft cabin lighting in new aircraft cabins is approximately 40% lighter than traditional incandescent bulbs, while offering enhanced durability with a mean time between failures of 10,000 hours compared to 1,000 hours for conventional lighting. This shift toward lightweight solutions extends beyond lighting to include seats, galleys, and other cabin components, reflecting the industry's commitment to sustainability and operational efficiency.

The market is witnessing substantial fleet modernization initiatives as airlines seek to enhance their service offerings and maintain competitive advantage. As of August 2023, North American carriers have placed significant orders, with a combined backlog of 1,474 Boeing and 986 Airbus aircraft. Major carriers are actively expanding their fleets, exemplified by United Airlines' order for 200 Boeing 737 MAX and 70 Airbus A321neo aircraft, while Delta Airlines has committed to 100 Boeing 737-10 aircraft. These fleet expansion programs are driving the integration of advanced aircraft cabin systems that prioritize both passenger comfort and operational efficiency.

Airlines are increasingly focusing on customizable cabin configurations and enhanced passenger amenities to meet evolving consumer preferences. The industry is witnessing a trend toward more sophisticated cabin designs incorporating advanced mood lighting systems, improved seating configurations, and enhanced in-flight entertainment options. North American carriers are investing in modernized cabins with LED ambient lighting technology and advanced in-flight entertainment systems, with major airlines like United Airlines, American Airlines, and Delta Airlines featuring seatback screens in their active fleets. This focus on passenger experience is reshaping cabin interior designs and driving innovation in the sector.

The market is characterized by expanding route networks and increasing connectivity, which is influencing cabin interior requirements. In 2022, airlines launched over 650 new routes involving North American airports, necessitating flexible and efficient cabin configurations that can accommodate varying route demands. Airlines are responding by adopting versatile aviation interior solutions that can be optimized for different route lengths and passenger segments. This trend is particularly evident in the narrowbody segment, where airlines are implementing premium cabin features traditionally found in widebody aircraft to enhance the passenger experience on longer routes while maintaining operational efficiency.

North America Commercial Aircraft Cabin Interior Market Trends and Insights

Rising economy, increase in tourism industry and ease of restrictions are the driving factors for a consistent air passenger traffic growth in North America

- North America's vast landmass and diverse destinations make it a popular choice for millions of passengers who choose to fly both domestically and internationally. Factors such as a growing economy, increased affordability of air travel, and a rising middle class have contributed to a significant uptick in air passenger traffic. Air passenger traffic in the United States reached 1.04 billion in 2022, up by 7% compared to 2021 and 12% compared to 2019. In 2022, from January through December, US airlines carried 853 million passengers, up from 658 million in 2021 and 388 million in 2020. The total number of passengers carried by airlines in Canada reached 107 million in 2022, surpassing the levels in 2021 by 6%. In 2022, Mexico had 100 million air passenger traffic, representing a 7% growth compared to its 2021 traffic levels. North America has benefitted from fewer and shorter-lasting travel restrictions than many other countries and regions. This has boosted domestic travel in the large home market, as well as international travel. Net profits in the region are expected to rise from USD 9.9 billion in 2022 to USD 11.4 billion in 2023.

- To cater to the demand driven by air passenger traffic, various airlines in the region are planning to procure new aircraft. For instance, around one-third of global aircraft deliveries in 2023 were anticipated to be received by various carriers in North America. Although the region’s aircraft deliveries were already above 2019 levels in 2022, they were expected to grow by an additional 72 units in 2023. Overall, with consistent air travel, the region's air passenger traffic is expected to increase by 1.7 billion in 2030 compared to 1.2 billion recorded in 2022.

Rising economic stability, particularly in the United States, is expected to support North America's GDP per capita growth

- The United States is a developed country and has the world's largest nominal GDP and net wealth. Real GDP increased by 2.1% in 2022, compared to 5.9% in 2021. The increase in real GDP in 2022 primarily reflected increases in consumer spending, exports, private inventory investment, and non-residential fixed investment that were partly offset by decreases in residential fixed investment and federal government spending. The rise in most sectors is expected to eventually boost the region's GDP per capita and, hence, support the air transport industry. North America has the highest continental GDP per capita by both GDP Nominal and PPP in the world. In 2022, the United States had the highest GDP per capita in the region at USD 76,350.

- In 2022, Canada's real gross domestic product (GDP) grew by 3.8%. Oil and gas extraction (except oil sands) decreased by 1.6% in December, primarily due to lower-than-seasonal growth in oil extraction in the month after strong offshore production. Winter storms had a significant impact on air and railway transportation in December. The month saw a 2.3% decrease in air transportation, the first such decrease since January 2022.

- Mexico has solid macroeconomic institutions, is open to trade, and has a diversified manufacturing base connected to global value chains. The Mexican economy grew by 3.1% in 2022, after a bounce-back of 4.7% in 2021 and an 8.0% fall in 2020 due to the COVID-19 pandemic. The economy has recovered its employment and Gross Domestic Product (GDP) pre-pandemic levels. Mexico's stable macroeconomic framework, the US dynamism, and solid manufacturing base will support economic growth.

,-By-Country,-USD,-North-America,-2017---2030.svg)

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Airlines are placing huge orders for new fuel-efficient aircraft, and the expansion of LCCs is contributing to the growth of the market

- The aircraft backlog in North America is primarily driven by the increasing demand for smaller and more efficient aircraft by various airlines

- The growing demand for air travel and the allocation of funds toward airport infrastructure are the key driving factors behind the growth of the region's aviation industry

- Commercial aircraft orders that are being placed with major OEMs are the primary drivers of revenue for the aircraft manufacturers in this market

- The aviation industry's growth is fueled by the recovery of air travel and the high volume of aircraft orders placed by various airlines

- Airlines are expected to reduce the overall aircraft weight by adopting fuel-efficient measures

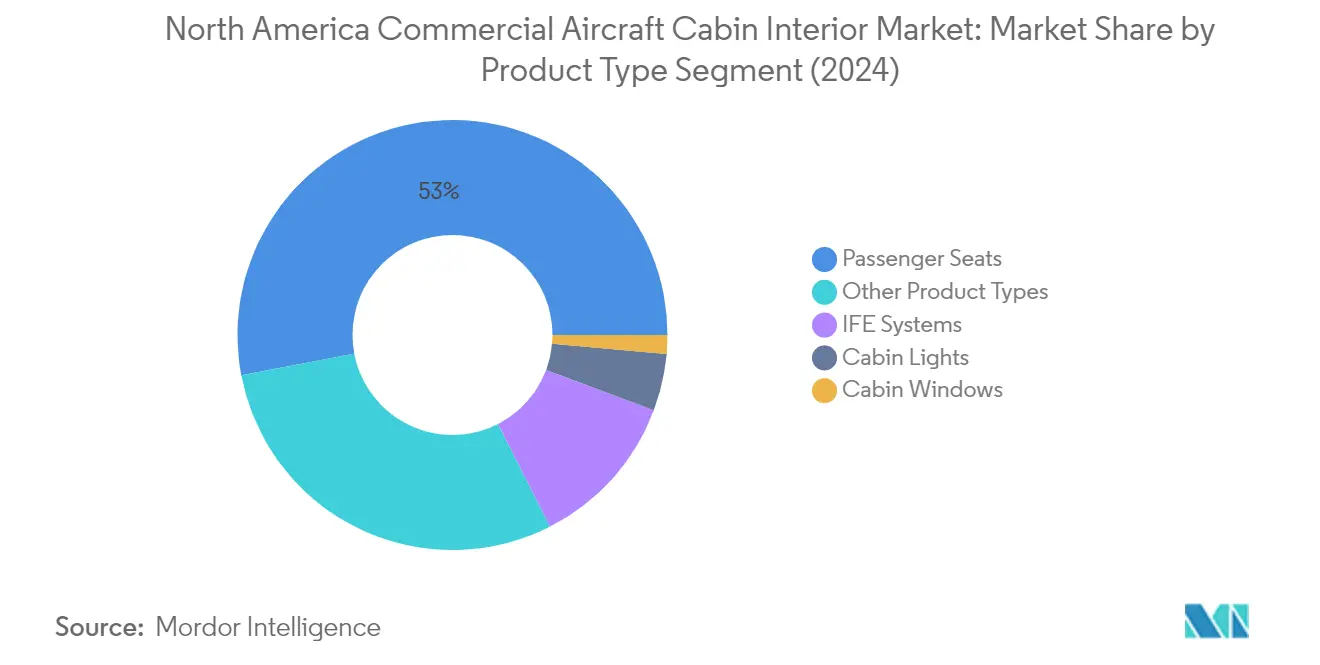

Segment Analysis: Product Type

Passenger Seats Segment in North America Commercial Aircraft Cabin Interior Market

The passenger seats segment dominates the North American commercial aircraft cabin interior market, accounting for approximately 53% of the total market value in 2024. Airlines in North America are adopting lighter aircraft seating to reduce overall aircraft weight and improve cabin space utilization. Modern-generation aircraft seats are manufactured using lightweight, non-metallic materials and innovative designs to reduce fuel expenses and increase aircraft sustainability. Major airlines like United Airlines, American Airlines, and Air Canada are investing significantly in new seating configurations that offer enhanced features and technological conveniences. The demand is particularly strong in the economy and premium economy classes, where airlines are focusing on improving passenger comfort while maintaining operational efficiency. The integration of advanced materials and smart design solutions has enabled seat manufacturers to develop products that balance passenger comfort with airline profitability requirements.

Passenger Seats Segment Growth in North America Commercial Aircraft Cabin Interior Market

The passenger seats segment is projected to experience the fastest growth in the North American commercial aircraft cabin interior market through 2024-2029. This growth is driven by several factors, including the increasing demand for seats with enhanced features and technological conveniences. Airlines are actively pursuing fleet expansion programs, with carriers like United Airlines integrating new Boeing 737 MAX and Airbus 321neo aircraft. The trend toward lightweight seating solutions continues to accelerate, with manufacturers developing innovative products that reduce fuel consumption while maintaining passenger comfort. Additionally, the rising importance of premium economy offerings and the integration of advanced materials in seat construction are contributing to the segment's growth. The market is also benefiting from the increasing focus on customizable seating options that cater to different passenger preferences and route requirements.

Remaining Segments in Product Type

The other segments in the North American commercial aircraft cabin interior market include in-flight entertainment systems, cabin lights, cabin windows, and other product types such as aircraft galleys, overhead bins, and aircraft lavatories modules. The IFE systems segment is experiencing significant innovation with the introduction of advanced 4K displays and integrated connectivity solutions. Aircraft cabin lighting has evolved with the adoption of LED technology and sophisticated mood lighting systems that enhance the passenger experience. Cabin windows are seeing technological advancements with the introduction of electrochromic dimming features and larger designs for improved natural lighting. The remaining product types, including galleys and lavatories, are also undergoing modernization with touch-free features and improved space utilization designs to meet evolving passenger needs and airline requirements.

Segment Analysis: Aircraft Type

Narrowbody Segment in North America Commercial Aircraft Cabin Interior Market

The narrowbody segment dominates the North American commercial aircraft cabin interior market, commanding approximately 77% of the total market share in 2024. This dominance is primarily driven by the increasing preference for fuel-efficient aircraft and the expansion of low-cost carriers in the region. The introduction of new fuel-efficient narrowbody aircraft models with increased range, particularly the A321XLR, which is expected to enter service by 2024, has further strengthened this segment's position. Major airlines like JetBlue, American Airlines, Air Canada, and United Airlines have placed significant orders for these aircraft, demonstrating strong market confidence. The segment is also witnessing innovations in passenger comfort, with airlines focusing on improving cabin interiors through enhanced seating configurations and premium offerings. For instance, JetBlue has introduced Thompson Aero's VantageSolo seat for its business class Mint Suite on its new A321XLRs, while American Airlines is planning to install Flagship Suite seats featuring privacy doors on its A321XLR fleet. The segment is projected to maintain its growth trajectory at around 5% through 2029, driven by airlines' shift towards point-to-point routes and the anticipated delivery of approximately 2,678 narrowbody aircraft during the forecast period.

Widebody Segment in North America Commercial Aircraft Cabin Interior Market

The widebody segment represents a crucial component of the North American commercial aircraft cabin interior market, with major carriers like United Airlines, American Airlines, Delta Airlines, and Air Canada driving demand. These airlines are implementing various seating configurations in their widebody aircraft, with seat widths ranging from 17 to 21 inches and seat pitches varying from 30 to 80 inches. Airlines are particularly focusing on enhancing the passenger experience through advanced in-flight entertainment systems, with carriers like Hawaiian Airlines and WestJet Airlines incorporating sophisticated IFE systems in their widebody fleets. The segment is witnessing significant technological advancements, with airlines opting for lighter IFE systems to reduce overall aircraft weight, cost, and maintenance requirements. Seatback IFE system sizes in these aircraft range from 10 inches to 18 inches, depending on the airline's specifications. The introduction of new aircraft models, such as the Boeing 777X with its two variants (777-8 and 777-9) scheduled for delivery from 2024, is expected to further drive innovation in cabin interiors for widebody aircraft.

Segment Analysis: Cabin Class

Business and First Class Segment in North America Commercial Aircraft Cabin Interior Market

The Business and First Class segment dominates the North American commercial aircraft cabin interior market, accounting for approximately 62% of the total market value in 2024. Airlines in the region are increasingly focusing on enhancing their premium cabin offerings to cater to high-yield passengers and maintain competitive advantage. Major carriers like United Airlines, American Airlines, and Delta Air Lines are investing significantly in upgrading their business class products with features such as lie-flat seats, enhanced privacy solutions, and improved in-flight entertainment systems. The segment is also experiencing the fastest growth trajectory, driven by airlines' strategy to maximize revenue through premium cabin configurations. Airlines are particularly emphasizing the development of business class products for narrowbody aircraft operating on transcontinental routes, with innovations such as Thompson Aero's VantageSolo seat being adopted for enhanced passenger comfort. The trend of converting first-class cabins into more efficient business-class configurations is gaining momentum, as evidenced by American Airlines' plan to eliminate first class completely by the end of 2024 and replace it with new business-class products.

Economy and Premium Economy Class Segment in North America Commercial Aircraft Cabin Interior Market

The Economy and Premium Economy Class segment represents a significant portion of the North American commercial aircraft cabin interior market, with airlines continuously working to optimize these cabins for improved passenger experience and operational efficiency. Airlines are gradually transforming their economy offerings by creating a distinctive premium economy segment that bridges the gap between standard economy and business class services. This strategic positioning typically commands 65-85% higher fares than standard economy while offering enhanced features such as extra legroom, improved reclining capabilities, and superior in-flight entertainment options. Major carriers are implementing innovative solutions in these cabins, as demonstrated by Zim Aircraft Seating's introduction of the Zim Privacy Seat, which sets new standards for comfort and privacy in the premium economy class through features like integrated privacy shields, individually adjustable armrests, and extra-large IFE screens. The segment is witnessing substantial developments in seat design and cabin configuration, particularly in narrowbody aircraft where airlines are optimizing space utilization while maintaining passenger comfort levels.

North America Commercial Aircraft Cabin Interior Market Geography Segment Analysis

North America Commercial Aircraft Cabin Interior Market in the United States

The United States dominates the North American commercial aircraft interior manufacturers market, accounting for approximately 89% of the total market value in 2024. As home to major aircraft manufacturers, airlines, and aircraft interiors companies, the country serves as a significant hub for innovation and development in this sector. The market is primarily driven by the procurement of newer aircraft by various US airlines, with several carriers focusing on enhancing passenger experience through advanced cabin interior features. Major US airlines are prioritizing improvements in lighting systems, in-flight entertainment (IFE) screens, seating configurations, and overall cabin aesthetics. The presence of key players like Collins Aerospace and their manufacturing facilities has strengthened the country's position in the market. The market is expected to grow at around 5% during 2024-2029, driven by the increasing focus on fuel efficiency and passenger comfort. Airlines are investing heavily in lightweight materials and innovative aircraft cabin solutions to reduce operational costs while maintaining high standards of passenger experience. The substantial backlog of aircraft orders from US-based carriers further indicates strong growth potential in the coming years.

North America Commercial Aircraft Cabin Interior Market in Canada

Canada represents a significant market in the North American commercial aircraft cabin interior sector, benefiting from several US-Canada agreements that facilitate aerospace operations. The country's aviation sector is characterized by its strong focus on technological advancement and passenger comfort enhancement. Canadian airlines are actively modernizing their fleets with advanced cabin interior features, particularly in terms of lighting, seatback IFE systems, and seating configurations. The country's position as one of the world's largest aerospace markets and its ranking as the fourth-largest in civil aircraft production has attracted significant investments in cabin interior innovations. Major Canadian carriers are implementing various cabin upgrade programs, focusing on premium economy and business class segments to meet evolving passenger preferences. The presence of repair stations and manufacturing facilities of leading aircraft interiors companies has strengthened the country's position in the market. Canadian airlines' emphasis on sustainable and lightweight cabin solutions aligns with global trends toward fuel efficiency and environmental consciousness.

North America Commercial Aircraft Cabin Interior Market in Other Countries

The commercial aircraft interior manufacturers market in other North American countries, including Mexico and various Central American nations, demonstrates unique characteristics and growth potential. These markets are witnessing increasing adoption of modern cabin interior solutions, driven by the expansion of their aviation sectors and growing passenger expectations. Airlines in these regions are focusing on differentiating their services through enhanced cabin experiences, particularly in the growing low-cost carrier segment. The modernization of aircraft fleets in these countries has created opportunities for cabin interior suppliers to introduce innovative products and solutions. Regional carriers are particularly interested in cost-effective yet comfortable cabin configurations that maximize space utilization while maintaining passenger comfort. The growing tourism sector in these countries has also influenced airlines' decisions regarding cabin interior upgrades, with a particular focus on creating distinctive brand identities through cabin design and amenities.

Competitive Landscape

Top Companies in North America Commercial Aircraft Cabin Interior Market

The commercial aircraft cabin interior market in North America is characterized by continuous product innovation and strategic partnerships among key players. Companies are focusing on developing lightweight, fuel-efficient cabin components while incorporating advanced technologies like LED lighting systems and enhanced in-flight entertainment (IFE) solutions. Operational agility is demonstrated through the establishment of regional manufacturing facilities and service centers to better serve airline customers. Strategic moves include long-term agreements with major airlines and aircraft manufacturers, particularly for new aircraft programs. Market leaders are expanding their product portfolios through both organic development and strategic acquisitions, with a particular emphasis on sustainable aircraft interior materials and customizable aircraft cabin solutions that improve passenger experience.

Consolidated Market Led By Global Players

The market structure is highly consolidated with major global aerospace conglomerates dominating the landscape. These established players leverage their extensive research and development capabilities, manufacturing expertise, and long-standing relationships with aircraft manufacturers and airlines. The presence of high entry barriers, including stringent certification requirements and substantial capital investments, has limited the entry of new players. Recent years have witnessed significant merger and acquisition activities, particularly among tier-one suppliers looking to expand their cabin interior capabilities.

The competitive dynamics are shaped by the presence of both diversified aerospace companies and specialized cabin interior manufacturers. While global conglomerates offer comprehensive solutions across multiple aircraft platforms, specialist players focus on specific product categories like seating or lighting systems. The market has seen vertical integration trends with larger players acquiring smaller, specialized manufacturers to enhance their product offerings and technological capabilities. This consolidation has resulted in improved economies of scale and stronger negotiating power with aircraft manufacturers. Additionally, the use of innovative aircraft interior materials is becoming a key differentiator in this competitive landscape.

Innovation and Customer Relations Drive Success

For incumbent players to maintain and increase their market share, a focus on technological innovation and strong customer relationships remains crucial. Companies are investing in research and development to create differentiated products that address airlines' needs for fuel efficiency and passenger comfort. Building long-term partnerships with aircraft manufacturers through supplier-furnished equipment (SFE) programs and maintaining strong aftermarket support networks are essential strategies. Additionally, developing customizable solutions that allow airlines to differentiate their cabin offerings while maintaining operational efficiency is becoming increasingly important.

New entrants and smaller players can gain ground by focusing on niche market segments and developing innovative solutions that address specific airline requirements. Success factors include establishing strategic partnerships with larger suppliers or aircraft manufacturers, investing in certification capabilities, and building regional support networks. The market's future will be influenced by airlines' focus on passenger experience enhancement, sustainability requirements, and potential regulatory changes regarding cabin safety and emissions. Companies that can adapt to these evolving requirements while maintaining cost competitiveness will be better positioned for growth. Furthermore, the increasing demand for aircraft retrofit services presents opportunities for both established and new aircraft interiors companies, as they seek to upgrade existing fleets with advanced aircraft interior systems.

North America Commercial Aircraft Cabin Interior Industry Leaders

Collins Aerospace

Jamco Corporation

Panasonic Avionics Corporation

Recaro Group

Safran

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2023: Jamco Corporation announced that through a collaboration with KLM Royal Dutch Airlines (KLM), its premium class seats, Venture reverse herringbone, were installed in the World Business Class (WBC) of KLM's B777 Fleet.

- June 2023: United will be the first US airline to offer Panasonic's Astrova system, giving customers exclusive features like 4K OLED screens, high fidelity audio, and programmable LED lighting, starting in 2025.

- June 2023: French designer and aircraft seat manufacturer Expliseat is expected to deliver more than 2,000 units of its latest TiSeat model named E2. This model will be installed on the aircraft of the expanding Kuwaiti airline Jazeera Airways, which uses the Airbus A320 and A321 models, providing additional comfort to its passengers.

North America Commercial Aircraft Cabin Interior Market Report Scope

Cabin Lights, Cabin Windows, In-Flight Entertainment System, Passenger Seats are covered as segments by Product Type. Narrowbody, Widebody are covered as segments by Aircraft Type. Business and First Class, Economy and Premium Economy Class are covered as segments by Cabin Class. Canada, United States are covered as segments by Country.Product Type

| Cabin Lights |

| Cabin Windows |

| In-Flight Entertainment System |

| Passenger Seats |

| Other Product Types |

Aircraft Type

| Narrowbody |

| Widebody |

Cabin Class

| Business and First Class |

| Economy and Premium Economy Class |

Country

| Canada |

| United States |

| Rest of North America |

| Product Type | Cabin Lights |

| Cabin Windows | |

| In-Flight Entertainment System | |

| Passenger Seats | |

| Other Product Types | |

| Aircraft Type | Narrowbody |

| Widebody | |

| Cabin Class | Business and First Class |

| Economy and Premium Economy Class | |

| Country | Canada |

| United States | |

| Rest of North America |

Market Definition

- Product Type - Commercial Aircraft cabin interior products such as passenger seats, cabin lighting, inflight entertainment system, cabin windows, lavatories, galley, and stowage bins have been included under the product type in this study.

- Aircraft Type - All the passenger aircraft such as narrowbody and widebody which are single-aisle and twin-aisle are included in this study.

- Cabin Class - Business and First Class, economy and premium economy are classes of air travel provided by the airlines that offer various services to the passengers.

| Keyword | Definition |

|---|---|

| Gross domestic product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| High Dynamic Range (HDR) | Dynamic range describes the ratio between the brightest and darkest parts of an image. HDR is used to capture a greater dynamic range than SDR. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| European Aviation Safety Agency (EASA) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| 4K Display | 4K resolution refers to a horizontal display resolution of approximately 4,000 pixels. |

| Organic Light Emitting Diode (OLED) | It is the light-emitting diode (LED) in which the emissive electroluminescent layer is a film of organic compound that emits light in response to an electric current. |

| Mean Time Between Failures (MTBF) | The mean time between failures is the predicted elapsed time between inherent failures of a mechanical or electronic system, during normal system operation. |

| (Low-Cost Carrier (LCCs) | It is an airline that is operated with an especially high emphasis on minimizing operating costs and without some of the traditional services and amenities provided in the fare |

| Electronically Dimmable Windows (EDW) | It is a type of window that blocks up to 99.96% of all visible light and provide full opacity, integrated into the window cassette of the sidewall panel. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step 1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step 2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step 3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms