Aircraft Seat Actuation Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 0.72 Billion |

| Market Size (2030) | USD 1.08 Billion |

| Growth Rate (2025 - 2030) | 8.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Seat Actuation Systems Market Analysis by Mordor Intelligence

Market Analysis

The aircraft seat actuation systems market size is estimated at USD 0.72 billion in 2025, and is expected to reach USD 1.08 billion by 2030, at a CAGR of 8.56% during the forecast period. Airlines accelerated premium-cabin retrofits, OEMs standardized electro-mechanical platforms, and suppliers introduced data-rich seat motion solutions, jointly lifting demand. North America led with a 43.77% share in 2024 thanks to its deep aerospace supply base, yet Asia-Pacific rose fastest as fleet modernization and long-haul network expansion gained pace. Rotary mechanisms dominated volume, but hybrid dual-motion units climbed swiftly, reflecting passenger appetite for lie-flat comfort. Sector consolidation sharpened competition; at the same time, strict DO-160 testing and supply bottlenecks raised the bar for new entrants.

Key Report Takeaways

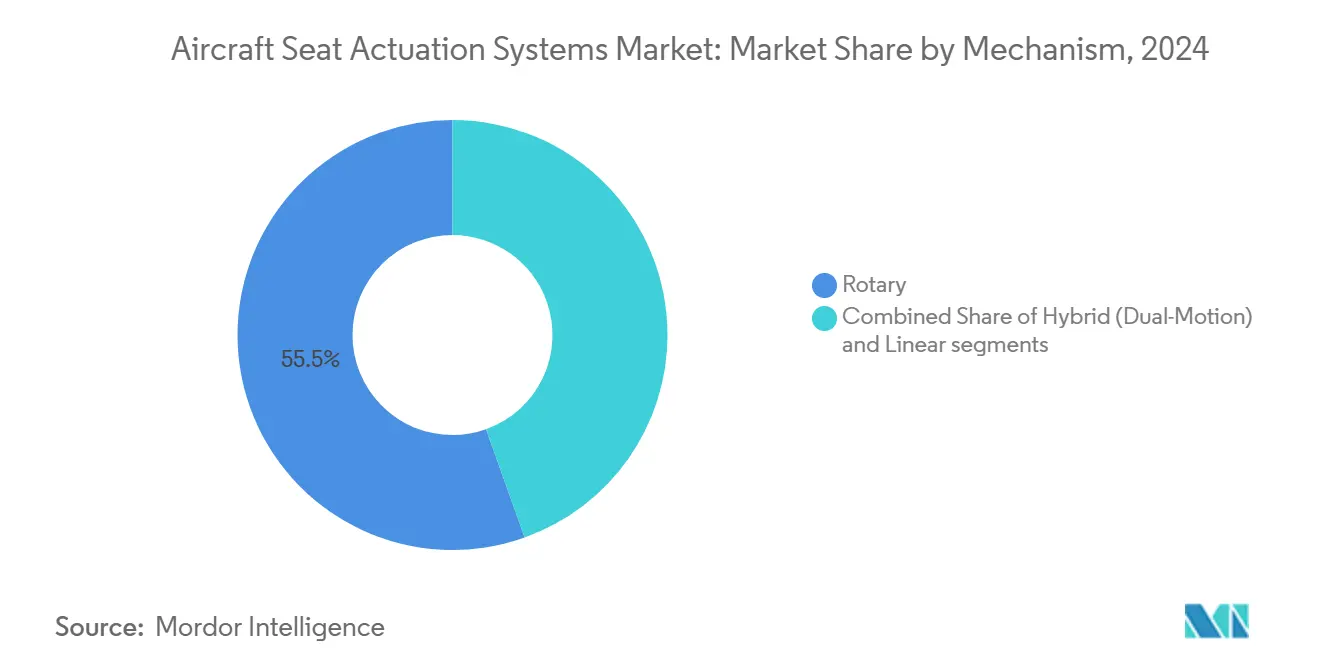

- By mechanism, rotary solutions held 55.45% of the aircraft seat actuation systems market share in 2024; hybrid dual-motion units are advancing at a 7.34% CAGR to 2030.

- By aircraft type, narrowbody platforms captured 47.39% revenue share in 2024, while helicopters are forecasted to grow at 9.23% CAGR through 2030.

- By seat class, economy commanded a 41.76% share of the aircraft seat actuation systems market in 2024; first-class is set to expand at an 8.78% CAGR between 2025 and 2030.

- By end user, linefit applications led the aircraft seat actuation systems market, accounting for 55.68% of the size in 2024; retrofit demand is projected to grow at a 9.12% CAGR to 2030.

- By component, actuator motors contributed 50.24% of the aircraft seat actuation systems market share in 2024; gearbox and screw assemblies are poised for 7.45% CAGR growth to 2030.

- By geography, North America maintained a 43.77% share in 2024 while Asia-Pacific is projected to witness the fastest growth at a 9.12% CAGR through 2030.

Global Aircraft Seat Actuation Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for premium-economy and business-class retrofits | +1.2% | Global, early gains in North America & Europe | Medium term (2-4 years) |

| Surge in electro-mechanical actuators replacing hydraulic units | +1.1% | Global | Long term (≥ 4 years) |

| OEM focus on “More-Electric Aircraft” platforms | +1.0% | North America & Europe, spill-over to APAC | Long term (≥ 4 years) |

| Smart-seat IoT sensors enabling predictive maintenance | +0.9% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Urban air mobility (UAM) and eVTOL interior requirements | +0.8% | North America & APAC | Short term (≤ 2 years) |

| Sustainability push for recyclable actuator materials | +0.7% | Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for premium-economy and business-class retrofits

Airlines defer new-build deliveries yet still seek revenue uplift, so retrofit programs flourish. LATAM Airlines’ 2024 decision to install RECARO R7 mini-suites on B787s typifies a shift toward lie-flat comfort that commands higher fares.[1]AviTrader, “LATAM Airlines to retrofit Boeing 787 fleet with RECARO’s premium R7 mini-suites,” avitrader.com Hybrid dual-motion systems simplify installation and enable full-flat transition, merging rotary and linear moves in one compact housing. Retrofit projects also benefit from lower downtime because electro-mechanical lines do not need hydraulic plumbing. Asia-Pacific carriers compete head-to-head with Gulf rivals, fueling brisk demand for advanced seat motion and pushing the aircraft seat actuation systems market toward intelligent, multi-axis products.

Surge in electro-mechanical actuators replacing hydraulic units

More-electric aircraft architecture is now standard on new-generation widebodies, with B787 and A350 demonstrating up to 15% empty-weight savings from all-electric seat systems.[2]Honeywell, “Electromechanical Actuation Advantages,” honeywell.com Eliminating fluid cuts fire risk and maintenance, while torque-dense brushless motors allow smooth, low-noise transitions. Digital control loops also integrate with cabin management networks, letting airlines preset preferred positions for loyalty customers. Suppliers able to qualify high-torque motors and resilient PCUs position themselves for durable share gains in the aircraft seat actuation systems market.

OEM focus on “More-Electric Aircraft” platforms

OEMs broaden the electric design philosophy beyond flight controls to encompass cabin motion. Central power distribution trims wiring duplication and eases certification since typical architecture applies across seat rows.[3]Honeywell, “Anthem Cockpit Solutions,” honeywell.com Airbus and Boeing partner with actuation specialists early in airframe design, locking in long-term supply agreements. As ICAO emissions thresholds tighten, airlines value every kilogram saved; electric seat motion contributes to weight reduction through lighter harnesses and removal of hydraulic reservoirs, further accelerating the aircraft seat actuation systems market.

Smart-seat IoT sensors enabling predictive maintenance

Embedded sensors in seat drives capture load, vibration, and thermal data, transmitting through secure gateways to airline cloud dashboards. Astronics’ Carat Seat Motion platform streams telemetry that flags wear trends before failure, cutting unscheduled maintenance events by up to 30%.[4]Honeywell, “Anthem Cockpit Solutions,” honeywell.com Predictive analytics aligns spare-part stocking with real-time usage, shrinking inventory carrying costs. Regulators mandate cybersecurity hardening under DO-160, and vendors that merge data science with avionics compliance hold an edge in the expanding aircraft seat actuation systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent certification and DO-160 qualification costs | -0.8% | Global | Medium term (2-4 years) |

| Supply-chain consolidation and long lead-times | -0.7% | Global, acute impact in APAC | Short term (≤ 2 years) |

| New fire-safety rules for seat-electronics enclosures | -0.6% | Global | Medium term (2-4 years) |

| ULCC shift to fixed-shell slim‐seats (non-reclining) | -0.5% | North America & Europe, spreading APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent certification and DO-160 qualification costs

Full DO-160 environmental qualification can exceed USD 2 million per product variant and add two years to launch schedules, stifling newcomers. Fire-safety amendments now oblige tougher flame and smoke tests for motor controllers, increasing the cost. Incumbents with in-house labs and test rigs amortize expenses across broad portfolios. In contrast, start-ups often seek joint ventures or exit, concentrating power among the top five aircraft seat actuation systems market suppliers.

Supply-chain consolidation and long lead-times

The pandemic aftershocks and geopolitical friction left only a small cadre of DO-178/DO-254-qualified motor makers and PCB fabricators. GAO logged seat-actuator lead-times stretching to 18 months in 2024, double pre-pandemic levels. Airlines hedge by signing multi-year service agreements, which lock up capacity and squeeze late entrants. Material shortages for rare-earth magnets threaten schedule adherence, forcing integrators to redesign around substitute alloys that still meet torque density targets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mechanism: Rotary systems drive current demand

Rotary drives supplied 55.45% revenue in 2024 as their straightforward gearing suits high-density economy rows. The aircraft seat actuation systems market size for rotary solutions is projected to reach USD 590.2 billion in 2030, advancing at a 7.10% CAGR. Hybrid dual-motion units, however, post the fastest trajectory because lie-flat programs demand seamless recline, leg-rest, and lumbar action from one envelope. Airlines value fewer parts and faster installation, which lowers downtime and keeps premium jets flying. Suppliers integrate smart encoders and low-noise screws, curbing cabin acoustic footprint and boosting brand reputation.

By Aircraft type: Narrowbody dominance with helicopter growth

Single-aisle jets accounted for 47.39% of 2024 revenue, powered by prolific B737 and A320 production. The aircraft seat actuation systems market share for narrowbodies benefits from densified layouts that multiply actuator units per fuselage. Helicopters yield modest units but a hot 9.23% CAGR, especially as offshore energy firms retrofit older rotorcraft with ergonomic seating to curb crew fatigue. Vibration-proof designs and compact footprints drive R&D in this niche, foreshadowing technology crossover into UAM cabs.

By Seat Class: Economy volume meets premium innovation

Economy rows retained a 41.76% share, yet ultra-low-cost models favor fixed-shell designs that sideline motorized recline. In contrast, first-class drives technical frontiers; its aircraft seat actuation systems market size is poised for an 8.78% CAGR lift as Gulf carriers roll out enclosed suites with individual privacy doors. These seats need high-torque motors, silent bearings, and fault-tolerant controllers that interface with passenger-service interfaces. OEMs channel lessons learned here to premium economy, uplifting traveler expectations across cabins.

By End User: Retrofit momentum accelerates

OEM deliveries still captured 55.68% of the 2024 value, yet retrofit projects outpace at 9.12% CAGR to 2030 as backlogs stall new airframes. Airlines convert older jets into high-yield premium cabins, often during heavy checks, shortening payback cycles. Providers that bundle seat design, STC engineering, and onsite installation capture a larger wallet share within the aircraft seat actuation systems market.

By Component: Motors remain core, gearbox assemblies climb

Motors had a 50.24% share in 2024 because every actuation chain begins with dense, efficient torque machines. Gearbox and screw systems rose fastest as multi-axis seats push for precise translation under heavy loads. Integrated packages join motor, gearbox, PCB, harness, and sensors in sealed units, trimming wiring and easing maintenance.

Geography Analysis

North America maintained a 43.77% share in 2024 thanks to a deep aerospace ecosystem clustered around Seattle, Wichita, Montréal, and Phoenix. FAA certification norms often set global precedent, helping regional suppliers export proven solutions.

Asia-Pacific will add the most net value, growing 9.12% CAGR through 2030 as China and India induct record aircraft and refurbish twin-aisles for premium service. Local regulators encourage indigenous sourcing, pressuring multinational firms to partner or localize.

Europe holds a stable share anchored by Airbus assembly lines; EU Green Deal regulations reward lighter electro-mechanical systems constructed from recyclable alloys. Middle East carriers deploy headline-grabbing first-class suites, crystallizing demand for cutting-edge motion tech, while Africa begins renewing fleets with modern cabins to tap tourism rebound.

Competitive Landscape

Innovation and Partnerships Drive Future Success

Success in the global aircraft actuation market size increasingly depends on manufacturers' ability to develop innovative solutions that address emerging industry trends, particularly in electrification and weight reduction. Incumbent players must strengthen their research and development capabilities while maintaining close relationships with aircraft manufacturers to anticipate and respond to changing requirements. The ability to offer integrated solutions that combine mechanical reliability with advanced electronic controls will become increasingly important, as will the capacity to provide comprehensive aftermarket support and maintenance services.

Specialization in specific aircraft categories or regional markets presents a viable strategy for contenders seeking to gain market share. Success factors include developing proprietary technologies that offer significant advantages in terms of weight, reliability, or maintenance costs. The relatively concentrated nature of the customer base, comprising major aircraft manufacturers and airlines, necessitates building strong relationships and establishing credibility through certifications and proven performance. While substitution risk remains low due to the specialized nature of aircraft seat actuation systems, manufacturers must stay ahead of regulatory changes, particularly those related to safety standards and environmental requirements.

Aircraft Seat Actuation Systems Industry Leaders

Safran SA

Collins Aerospace (RTX Corporation)

Astronics Corporation

Crane Aerospace & Electronics (Crane Company)

ITT Enidine Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Safran completed the acquisition of Collins Aerospace's flight control and actuation operations, which are critical systems for commercial and military aircraft and helicopters.

- April 2025: Collins Aerospace introduced innovative aftermarket seating solutions designed to enhance the airline experience using its Pinnacle main cabin seats.

- March 2025: At ProMat 2025, ITT Inc.’s Enidine and Compact brands showcased their reliable motion control solutions and upgraded product customization software.

- December 2024: Woodward signed a definitive agreement to acquire Safran Electronics & Defense's electro-mechanical actuation business, which has operations in the US, Mexico, and Canada.

Global Aircraft Seat Actuation Systems Market Report Scope

Seat actuation systems onboard aircraft will allow the passengers to adjust their seating positions as per their comfort level. Various mechanical and electro-mechanical actuators enable the seat to adapt between different seating positions based on the requirements of passengers. The aircraft seat actuation systems market is segmented based on mechanism into linear and rotary. The market is also segmented by aircraft type to fixed-wing aircraft and helicopters. The report also covers the market sizes and forecasts for the market in major countries across different regions. The market sizing and forecasts have been provided in value (USD million).

| Linear |

| Rotary |

| Hybrid (Dual-Motion) |

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Transport Aircraft |

| Helicopters |

| First |

| Business |

| Premium-Economy |

| Economy |

| OEM Line-fit |

| Retrofit/Aftermarket |

| Actuator Motor |

| Gearbox and Screw Assembly |

| Control Electronics (PCU) |

| Harness and Sensors |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| Mechanism | Linear | ||

| Rotary | |||

| Hybrid (Dual-Motion) | |||

| Aircraft Type | Narrowbody Aircraft | ||

| Widebody Aircraft | |||

| Regional Transport Aircraft | |||

| Helicopters | |||

| Seat Class | First | ||

| Business | |||

| Premium-Economy | |||

| Economy | |||

| End User | OEM Line-fit | ||

| Retrofit/Aftermarket | |||

| Component | Actuator Motor | ||

| Gearbox and Screw Assembly | |||

| Control Electronics (PCU) | |||

| Harness and Sensors | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the aircraft seat actuation systems market in 2025?

The aircraft seat actuation systems market size is estimated at USD 0.72 billion in 2025, and is expected to reach USD 1.08 billion by 2030, at a CAGR of 8.56%.

Which region leads demand for seat actuation technology?

North America held 43.77% market share in 2024 due to its dense aerospace manufacturing base and early tech adoption.

Why are airlines prioritizing retrofit programs now?

Retrofit projects deliver faster revenue gains than new aircraft purchases amid supply-chain delays and allow carriers to launch premium service quickly.

What drives the shift from hydraulic to electro-mechanical actuators?

Electro-mechanical units cut weight, remove fluid maintenance, and integrate easily with digital cabin systems, improving reliability and fuel efficiency.

How strict are certification hurdles for new seat actuation suppliers?

DO-160 qualification can cost over USD 2 million and take up to two years per variant, favoring incumbents with in-house test facilities.

Page last updated on: