AI-Native HCM Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.68 Billion |

| Market Size (2031) | USD 39.15 Billion |

| Growth Rate (2026 - 2031) | 21.68% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Native HCM Platform Market Analysis by Mordor Intelligence

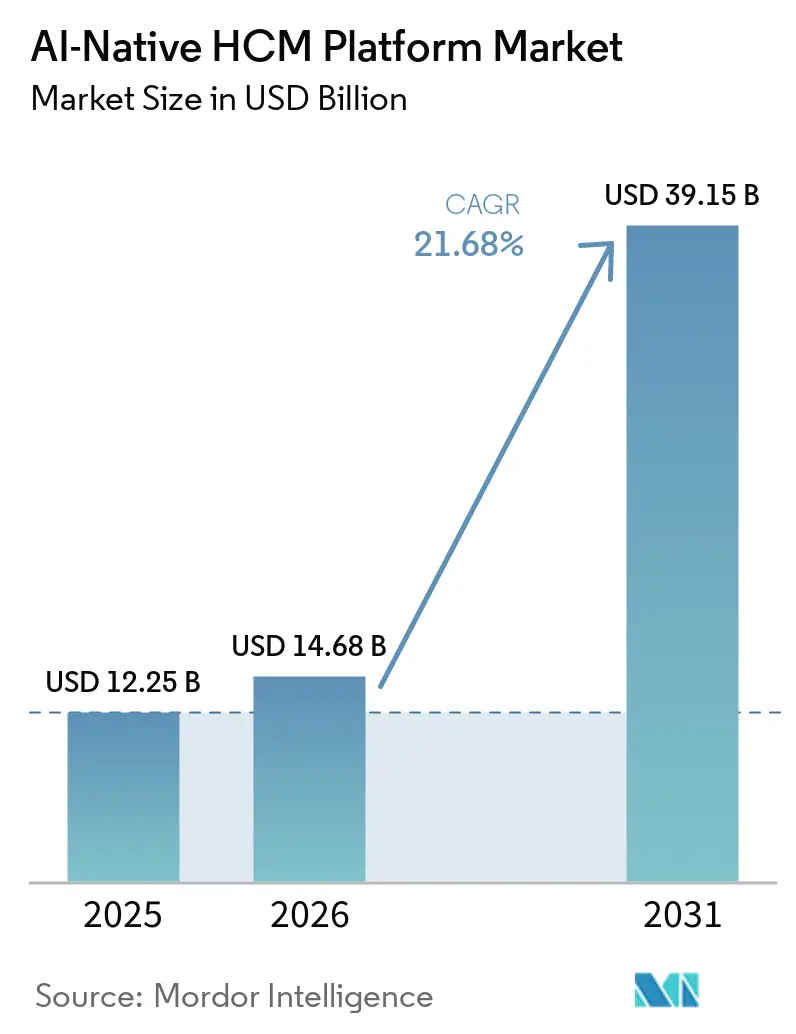

The AI-Native HCM Platform Market size is expected to grow from USD 12.25 billion in 2025 to USD 14.68 billion in 2026 and is forecast to reach USD 39.15 billion by 2031 at 21.68% CAGR over 2026-2031. The market moved beyond the earlier pilot phase as enterprises started treating AI in HR as core operating infrastructure rather than a narrow experimentation budget. Growth is being shaped by large language model-based HR assistants becoming part of real workflow execution, steady migration away from aging on-premises HCM environments, and demand for unified suites that connect people, payroll, and workforce intelligence data in one record system. Competitive behavior in 2026 reflects a clear push toward deeper data layers, auditable automation, and interfaces that sit inside the tools employees and managers already use every day. The strongest opportunities sit with platforms that can work with entrenched payroll and identity systems instead of forcing full rip-and-replace programs at the start. The market also benefits from buyer preference for software vendors that combine AI execution, governance controls, and service capacity in the same delivery model.

Key Report Takeaways

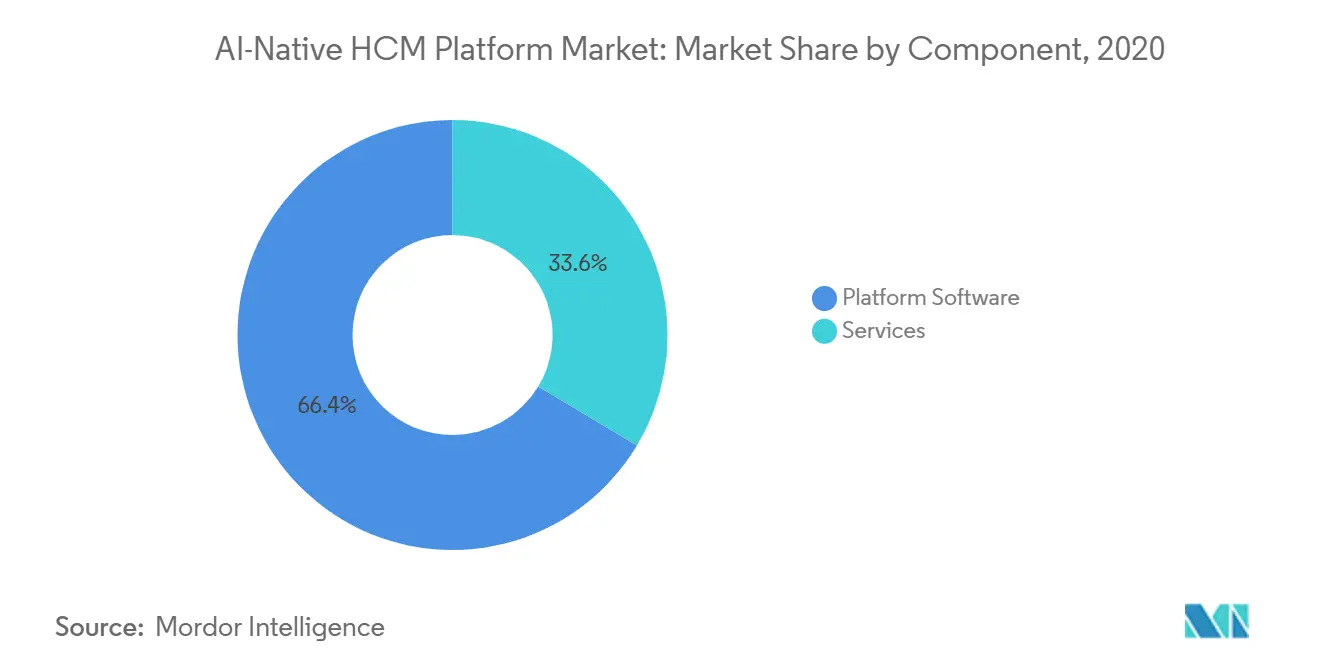

- By component, platform software held 66.41% of the AI-native HCM platform market revenue in 2025, while services are projected to expand at a 23.12% CAGR through 2031.

- By deployment model, cloud captured 72.41% of revenue in 2025, while hybrid deployment is projected to grow at a 22.68% CAGR through 2031.

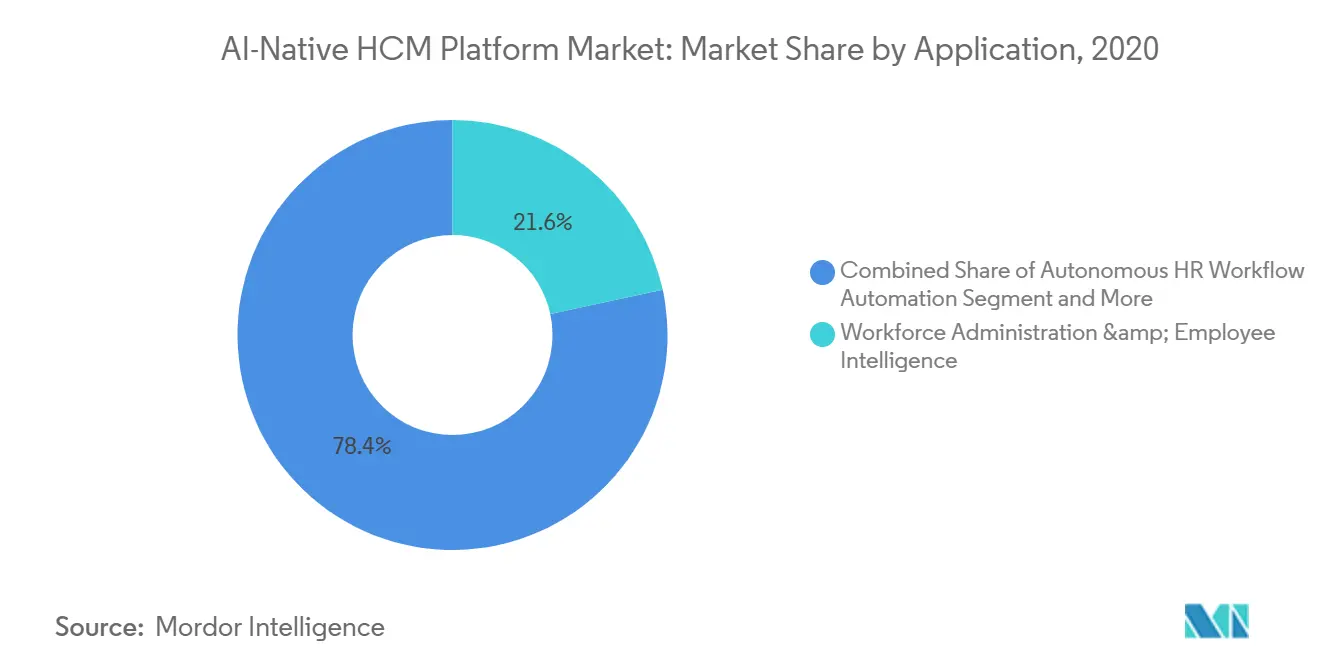

- By application, workforce administration and employee intelligence accounted for 21.63% of revenue in 2025, while autonomous HR workflow automation is projected to advance at a 24.18% CAGR through 2031.

- By end-user industry, information technology and telecom held 27.42% of revenue in 2025, while healthcare and life sciences are projected to expand at a 22.87% CAGR through 2031.

- By enterprise size, large enterprises held 61.39% of revenue in 2025, while small and medium enterprises are projected to grow at a 23.94% CAGR through 2031.

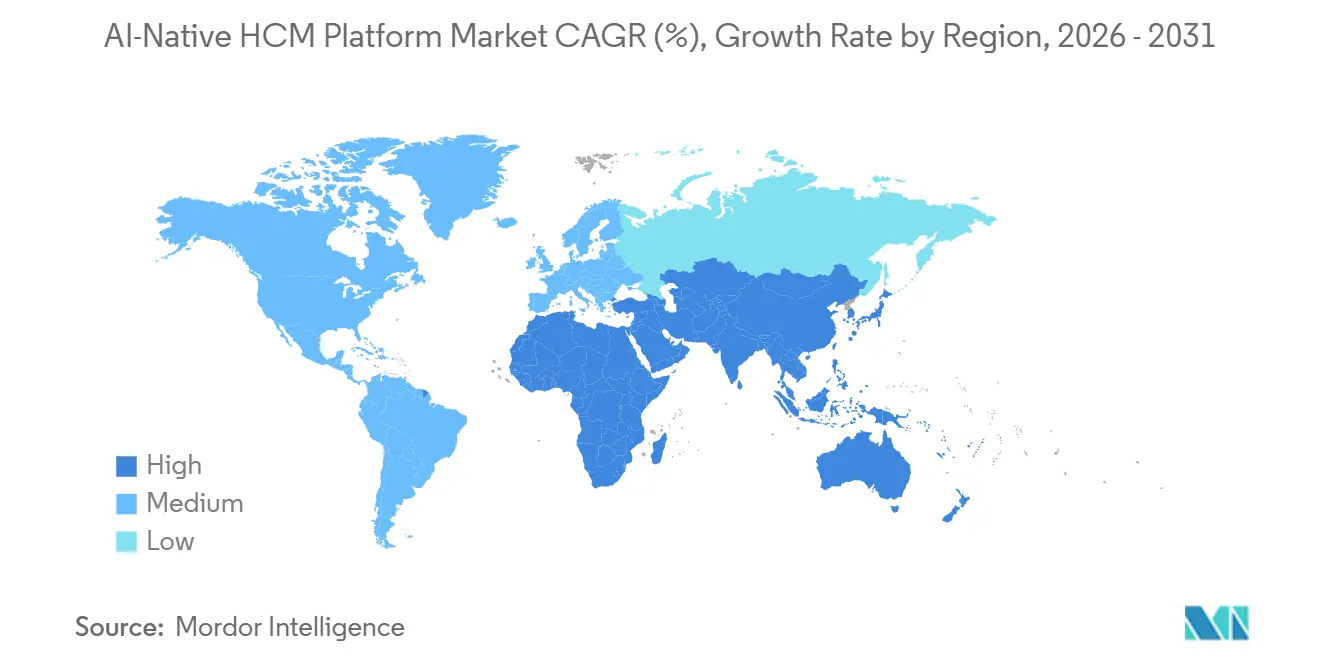

- By geography, North America held 40.12% of the AI-Native HCM Platform Market in 2025, while Asia-Pacific is projected to expand at a 24.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Native HCM Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Artificial Intelligence Copilots Moving from Pilot To System Of Record Workflows | 5.8% | Global, concentrated in North America and Western Europe | Short term (≤ 2 years) |

| Skills-Based Workforce Planning Becoming a Core HCM Buying Criterion | 4.5% | Global, with early gains in North America, UK, and Germany | Medium term (2-4 years) |

| Cloud HR Modernization and Suite Consolidation Favoring AI-Embedded Platforms | 3.9% | Global, concentrated in South America and APAC core, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| Demand for Continuous Employee Self-Service And Manager Assistants | 3.1% | Global | Medium term (2-4 years) |

| Need to Harmonize Fragmented Skills Taxonomies Across Enterprises | 2.3% | North America and EU, spill-over to APAC | Long term (≥ 4 years) |

| Real-Time Employment Data and Worker Record Modernization Improving AI Context | 1.7% | Global, with early gains in North America, India, and the UK | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Artificial Intelligence Copilots Moving From Pilot To System Of Record Workflows

The strongest growth force in the AI-Native HCM Platform Market is the shift of AI assistants from isolated use cases into production workflows that replace older menu-based HR interaction patterns. By 2026, buyers are no longer asking only whether copilots can answer questions; they are asking whether those tools can complete multistep tasks inside systems of record with clear permissions and audit trails. SHRM noted that 92% of CHROs expected further AI integration in 2026, up from 83% in 2025, and AI was already deployed in 39% of HR functions, led by recruiting at 27%, HR technology administration at 21%, and learning and development at 17%.[1]SHRM, “The State of AI in HR 2026,” Society for Human Resource Management, shrm.org That adoption pattern shows HR moving faster than many other back-office functions in turning AI into day-to-day operating infrastructure. Workday reinforced this direction in March 2026 with the global release of Sana, and then expanded the model in May 2026 by bringing Sana Self-Service Agent into Microsoft 365 Copilot, placing HR actions within an employee’s normal work environment rather than requiring a switch back to a separate application. The AI-Native HCM Platform Market is therefore moving toward platforms that can execute, not just suggest, and that shift is steadily raising the bar for renewal and expansion decisions.[2]Workday, “Introducing Sana From Workday: Superintelligence for Work That Finds Answers, Takes Action, and Automates Workflows,” Workday Newsroom, en-gb.newsroom.workday.com

Skills-Based Workforce Planning Becoming A Core HCM Buying Criterion

Skills-based workforce planning has moved closer to the center of buying decisions in the AI-Native HCM Platform Market because static job architectures no longer support the pace of role redesign taking place across enterprises. Buyers are placing more emphasis on platforms that can infer skills, maintain living taxonomies, and connect workforce planning to changing business demand. That change is making skills intelligence less of a side module and more of an architectural control point for hiring, internal mobility, redeployment, and learning. It also changes who influences purchases, because finance leaders and business unit heads now view workforce capability visibility as part of enterprise planning discipline rather than a narrow HR process issue. Vendors that can show verified skills supply and demand libraries, better redeployment logic, and tighter links between workforce data and planning workflows are gaining more attention in the AI-Native HCM Platform Market. This is also pushing product roadmaps toward embedded inference, taxonomy management, and manager-facing tools that translate skills data into staffing actions.

Cloud HR Modernization And Suite Consolidation Favoring AI-Embedded Platforms

Cloud modernization remains a major driver for the AI-Native HCM Platform Market, but the buying logic in 2026 goes beyond simple SaaS migration. Many enterprises are reaching decision points because older payroll and core HR environments are approaching support deadlines or have become too rigid to support new AI functions effectively. As a result, platform evaluations are increasingly shaped by AI readiness, workflow orchestration, and integration depth, not only by whether a vendor can mirror legacy features in a modern interface. Suite consolidation is also gaining support because buyers want a single record layer across people data, payroll data, skills data, and workforce intelligence rather than a stack of disconnected point tools. That preference favors AI-embedded platforms that can span administration, analytics, self-service, and policy execution with fewer handoffs. The AI-Native HCM Platform Market is therefore benefiting from a replacement cycle that ties cloud adoption directly to automation ambition and to confidence in a vendor’s long-term data model.

Demand For Continuous Employee Self-Service And Manager Assistants

The AI Native HCM Platform Market is also expanding because employees and managers increasingly expect always-on digital help for routine HR tasks, approvals, and information retrieval. What began as a cost-efficiency case for HR chatbots is turning into a retention and usability issue, especially in distributed and frontline-heavy workforces that need support outside standard HR service hours. SHRM found that employees were 5.7 times more likely to see job responsibilities shift because of AI than to lose their jobs, which helps explain why tools that support work redesign are gaining acceptance faster than tools framed mainly around labor replacement. This matters because employee and manager assistants are being judged not only on response quality but also on whether they reduce friction in everyday tasks such as approvals, scheduling, and navigating policies. The challenge is that more AI-generated signals can also overload managers if the platform does not guide decisions clearly or assign accountability for overrides. Vendors that structure self-service around controlled workflows, transparent policy logic, and easy escalation paths are likely to continue winning share in the AI-Native HCM Platform Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sensitive HR Data Governance and Explainability Requirements | -3.2% | Global, concentrated in EU, North America, and APAC-regulated markets | Medium term (2-4 years) |

| Legacy Payroll and Identity Stacks Slowing End-To-End Automation | -2.4% | Global, concentrated in North America and Western Europe | Short term (≤ 2 years) |

| EU AI Act and Works Council Obligations Extending Sales Cycles | -1.8% | EU member states and European Economic Area markets | Medium term (2-4 years) |

| Interoperability Gaps Across Skills Ontologies and Labor Data Standards | -1.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sensitive HR Data Governance And Explainability Requirements

Governance remains the clearest restraint on the AI Native HCM Platform Market because HR systems handle highly sensitive records tied to compensation, performance, leave, identity, and employee behavior. Procurement teams are now asking for explainability, documentation, auditability, and human oversight controls at the start of evaluation rather than treating them as legal details to resolve later. Reports show that 49% of organizations using or piloting AI had workforce AI policies, yet only 25% of that group described those policies as clear and future-proof, and 57% of HR professionals in the 19 most populous U.S. states with active AI employment laws were unaware that those laws existed. In Europe, the EU AI Act and the GDPR set a stricter regulatory framework for employment-related AI and require controls on high-risk uses, human oversight, and data impact considerations before those systems can be placed on the market. The AI Native HCM Platform Market also faces a significant financial risk threshold, as Article 99 allows penalties of up to EUR 35 million, which the 2025 IRS yearly average exchange rate reference places at approximately USD 37.9 million, or 7% of global annual turnover for non-compliance. This is slowing some purchase decisions, but it is also rewarding vendors that built explainability and outcome logging into their platforms earlier.[3]European Commission, “AI Act | Shaping Europe’s Digital Future,” European Commission, digital-strategy.ec.europa.eu

Legacy Payroll And Identity Stacks Slowing End-To-End Automation

Legacy payroll and identity infrastructure still slows the AI-Native HCM Platform Market by limiting how far automation can progress from recommendation to execution. Many enterprises can deploy copilots on top of legacy systems, but they cannot achieve full automation returns if the underlying payroll engine cannot accept reliable, real-time actions from AI layers. One case study showed that a company’s U.S. and Canada payroll system was more than 45 years old before the migration, and the move required extensive rewriting of multidecade customizations for a workforce of 19,000 people.[4]Strada Global, “ADM HR Transformation with SuccessFactors,” Strada Global, stradaglobal.com That profile is common in large global organizations where local compliance rules, union terms, benefits logic, and identity systems have been layered onto the core over many years. As a result, the deployment path for AI-native vendors often starts with orchestrating above the legacy stack rather than replacing the stack itself. The AI Native HCM Platform Market therefore grows fastest when vendors can integrate with legacy payroll and identity systems without breaking legal controls, historical records, or financial processes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Signals Beyond Software Complexity

Platform software remained the largest component in the AI-Native HCM Platform Market and held 66.41% of 2025 revenue, which means core suites still capture most spending when buyers consolidate HR records, workforce intelligence, and automation capabilities in one platform. That position reflects demand for AI core HCM platforms and decision engines that unify workflows previously spread across separate tools. In practical terms, software still anchors most enterprise purchasing because organizations first need the base system where people data, process rules, and AI actions can sit together. At the same time, buyers are placing greater weight on governance and security features within the software layer, as AI use in HR now touches sensitive employee records and business-critical workflows. In that sense, platform software continues to define the operating center of the AI-Native HCM Platform Market size in 2025.

Services, however, are projected to expand at a 23.12% CAGR through 2031, faster than platform software, which points to the real complexity of deployment at scale. Enterprises are spending more on implementation design, multi-country rollout support, compliance advisory, and model governance because AI-native platforms are being deployed across varied environments rather than in clean, greenfield settings. This pattern is especially visible in organizations that lack internal teams capable of configuring workforce intelligence models or managing cross-functional ownership between HR, IT, legal, and finance. The gap between software share and service growth suggests that the AI-Native HCM Platform Industry is still in a build-out phase, where operating change matters almost as much as product functionality. It also means that vendors with strong service ecosystems can protect account value even as software features converge. In the AI-Native HCM Platform Market, services are no longer a support layer around software; they are part of the adoption logic itself.

By Deployment Model: Hybrid Adoption Reshapes Cloud-First Assumptions

Cloud deployment accounted for 72.41% of 2025 revenue in the AI-Native HCM Platform Market, underscoring that SaaS-first buying behavior continues to define the mainstream direction of core HR modernization. Cloud remained the default because it offers buyers faster releases, broader integration options, and easier access to AI capabilities than older on-premises environments. It also aligns with the broader preference for unified suites that can support self-service, analytics, and workflow orchestration from a common record layer. The concentration of demand in cloud shows that the AI-Native HCM Platform Market size still rests on platforms designed for regular updates and continuous model improvement. Buyers continue to view the cloud as the most practical way to connect HR, payroll, and workforce intelligence without rebuilding those relationships locally in every environment.

Hybrid deployment is still the fastest-growing model and is projected to expand at a 22.68% CAGR through 2031, which means real buying behavior is more mixed than a simple cloud-first story would suggest. Regulated sectors and data-sovereign markets often cannot move every payroll, identity, or worker record into third-party infrastructure within the forecast window. Large enterprises also face the practical problem that payroll engines and adjacent systems may take years to replace, even when the front-end HCM layer moves earlier. This creates demand for platforms that can address local data constraints while still providing cloud-based AI inference, analytics, and user experience. On-premises deployment is losing share, but it remains important in accounts where worker data handling is governed by legal or institutional limits rather than by technology alone. The AI-Native HCM Platform Industry, therefore, continues to reward vendors that treat hybrid architecture as a deliberate product path rather than a temporary compromise.

By End User Enterprise Size: SME Adoption Narrows The Enterprise Gap

Large enterprises held 61.39% of 2025 revenue in the AI Native HCM Platform Market, reflecting their earlier access to enterprise suites, larger transformation budgets, and stronger in-house HR and IT teams. That lead also stemmed from the fact that large organizations had already spent years digitizing employee records, payroll, and workflows, making them the earliest buyers of AI co-pilots and automation layers. Extra-large organizations reached 60% AI-in-HR implementation, compared with 33% for small organizations and 35% for midsize organizations. Large enterprises, therefore, entered the current cycle with a maturity advantage, and that advantage continues to support their role as the largest revenue base in the AI Native HCM Platform Market. The share picture makes clear that enterprise demand still accounts for much of the current market volume, especially in global, compliance-heavy deployments.

Small and medium enterprises are nonetheless the fastest-growing size band and are projected to expand at a 23.94% CAGR through 2031. Cloud pricing, modular products, and vendors built for simpler deployment have made advanced capabilities available to buyers that previously lacked the budget or specialist teams to manage them. This matters because many SMEs are adopting AI-enabled HR systems before they accumulate the process debt that now slows large-enterprise transformation programs. Vendors such as BambooHR, HiBob, Rippling, and Darwinbox are benefiting from that gap by offering faster deployments, lighter configurations, and mobile-first user experiences aligned with the needs of smaller companies. Regional specialists also matter in this part of the AI Native HCM Platform Market because local compliance support often carries more weight than global breadth. Over time, SME growth will narrow the enterprise gap, even if large accounts continue to dominate absolute revenue.

By Application: Autonomous Workflow Automation Overtakes Legacy Decision Support

Workforce administration and employee intelligence held 21.63% of 2025 revenue, making it the largest application area in the AI Native HCM Platform Market. That position reflects the long history of enterprise spending on employee records, organizational structures, self-service, and core administrative workflows. It also shows why many AI functions in HR are first attached to the existing record and administration layer rather than launched as stand-alone tools. The installed importance of administration keeps this category at the center of the AI Native HCM Platform Market size, as every subsequent automation step still depends on accurate worker records and policy logic. Talent acquisition and candidate intelligence also remain important spending areas because many organizations began their AI deployment path in screening, matching, and interview support before expanding into other HR functions.

Autonomous HR workflow automation is projected to grow at a 24.18% CAGR through 2031 and is the fastest-growing application category. That shift marks a move away from systems that only recommend an action toward systems that can execute multistep processes, such as onboarding, exception routing, or compliance attestation with controlled human oversight. Payroll, compensation, and benefits intelligence are also gaining momentum as risk controls improve and enterprises become more comfortable automating portions of review and approval logic. New AI-driven features across platforms have included skills- and certification-based scheduling, agentic timesheet approvals, and AI-powered time-off features. Learning, skills intelligence, and internal mobility are also being reshaped by large language model-based authoring and inference, while AI governance and workforce risk management are emerging as a distinct buying category. The AI Native HCM Platform Market is therefore shifting from insight delivery toward action delivery across application layers.

By End-User Industry: Healthcare’s Structural Workforce Pressures Accelerate AI Adoption

Information technology and telecom firms captured 27.42% of 2025 revenue in the AI-Native HCM Platform Market, which reflects how engineering-led organizations adopted AI HR assistants earlier than most other verticals. These companies often had greater familiarity with internal AI, larger digital workforces, and less resistance to testing new workflow models across recruiting, learning, and employee support. That helped them establish internal benchmarks earlier, which, in turn, supported broader adoption of workforce intelligence capabilities. BFSI followed as another important spending vertical because the need for auditability, structured controls, and employee data governance aligns closely with the design priorities of AI-enabled HCM systems. The AI-Native HCM Platform Industry, therefore, shows a clear pattern where early-adopting verticals are those already comfortable managing both digital workflow complexity and regulatory scrutiny.

Healthcare and life sciences are projected to expand at a 22.87% CAGR through 2031, making them the fastest-growing end-user vertical in the AI-Native HCM Platform Market. Growth is being driven by difficult shift scheduling, credential verification requirements, and labor constraints that make workforce planning errors more costly than in many other sectors. Retail and e-commerce are also accelerating adoption because high-turnover frontline operations benefit from smarter scheduling and employee support tools. Industrial manufacturing is focusing more on workforce planning, aging labor transitions, and compliance-heavy safety training workflows that benefit from automation. Government and public sector demand is rising as workforce modernization programs move forward, but sovereign data requirements often push those deployments toward hybrid models. Other sectors, including education, energy, and professional services, continue to add residual demand, especially where skills intelligence supports resource planning and internal redeployment.

Geography Analysis

North America held 40.12% of 2025 revenue and remained the largest regional contributor to the AI Native HCM Platform Market. The region benefited from a dense base of large enterprises already active in AI programs and from a mature enterprise software-buying environment that enabled faster evaluation and purchasing cycles. In practical terms, North America accounted for 40.12% of the AI Native HCM Platform Market share in 2025 because buyers there were further along in cloud HCM adoption, AI experimentation, and multi-function platform consolidation. The region also showed a split competitive pattern in 2026, with incumbents retaining strength in large enterprise renewals while faster-moving challengers gained traction in mid-market and SME accounts through shorter deployment windows.

Asia Pacific is projected to expand at a 24.47% CAGR through 2031, making it the fastest-growing regional bloc in the AI Native HCM Platform Market. The region benefits from greenfield cloud HCM deployment paths that let many buyers bypass the legacy drag that slows automation in mature Western markets. CEO reassessment of operating models for speed and AI integration is reshaping CHRO priorities across Japan, South Korea, Australia, and Southeast Asia. India is especially important because vendors born in APAC are exporting AI native HCM capabilities rather than remaining purely domestic suppliers. China remains important as a large but distinct market where local data residency and government compliance requirements shape platform design, while Australia, South Korea, and Southeast Asian economies continue to support adoption through digital transformation programs and rising employer demand for modern workforce systems.

Europe accounted for meaningful 2025 revenue in the AI Native HCM Platform Market, led by Germany, the United Kingdom, and France. The region’s near-term buying behavior is being shaped less by feature comparison alone and more by how well vendors can handle pay transparency rules, AI risk classification, and data processing obligations under the EU framework. South America, the Middle East, and Africa are earlier-stage regions, but they remain important growth territories where mobile-first and AI-embedded platforms are gaining traction in markets that did not fully institutionalize older desktop HR stacks. Brazil and Saudi Arabia serve as anchor markets in their respective sub-regions, while Nigeria and South Africa stand out across Africa as multinational employers continue to support first-wave cloud HCM adoption through workforce modernization programs.

Competitive Landscape

The AI Native HCM Platform Market remains fragmented and highly competitive, with established vendors such as Workday, ADP, Dayforce, UKG, and Paychex facing pressure from AI native challengers including Rippling, Darwinbox, Deel, and HiBob. Incumbents still hold advantages in historical payroll depth, enterprise relationships, and integration reach, while challengers compete more aggressively on speed of deployment, cleaner architectures, and pricing that better fits mid-market buyers. This has created a split-strategy environment where larger vendors defend their installed bases through embedded AI extensions, while challengers pursue new account creation with faster time-to-value. In 2026, competitive differentiation in the AI Native HCM Platform Market is increasingly tied to data context, orchestration depth, and proof that automation can operate with human oversight and auditability in high-stakes HR processes. That is why the market is not won by who has the most features, but by who can link data depth, workflow execution, and governance in a way that buyers can trust.

Workday has been one of the clearest examples of this strategy shift. It made Sana generally available in March 2026 and then extended its reach in May 2026 by integrating Sana Self-Service Agent for HR and finance into Microsoft 365 Copilot, bringing HR actions closer to where employees already work. Paychex also expanded the competitive field in February 2026 by adding AI-driven scheduling, time-off, and timesheet approval capabilities across Paycor and Paychex Flex, reinforcing the importance of execution-oriented features in SME and mid-market accounts. Darwinbox strengthened its position through capital support and international expansion, and in August 2025, it also highlighted support for the Model Context Protocol and introduced its Darwinbox Super Agent across a footprint of 4 million employees in 130 countries.

The competitive field in the AI Native HCM Platform Market is also being shaped by white-space demand in AI governance tooling, multi-country payroll orchestration, and skills intelligence tied directly to internal mobility. Vendors that can bridge legacy payroll engines rather than forcing immediate replacement are likely to see better traction in large enterprise accounts where finance and legal teams still control the pace of back-end change. At the same time, mid-market customers continue to reward vendors that reduce implementation effort and present consumer-like interfaces without weakening control structures. This means the next stage of competition will likely favor platforms that combine flexible architecture with strong governance artifacts, because buyers increasingly want AI that can act inside HR processes without creating new compliance risk.

AI-Native HCM Platform Industry Leaders

Workday, Inc.

ADP, Inc.

Dayforce, Inc.

UKG Inc.

Paycom Software, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Workday integrated Sana Self-Service Agent into Microsoft 365 Copilot, enabling HR tasks like time-off requests and payslip reviews directly in Microsoft 365.

- May 2026: Workday launched Sana for IT Service Management and Travel Agent, extending AI into onboarding, access, travel, and expenses.

- March 2026: Workday made Sana generally available worldwide, including conversational AI, self-service, and enterprise orchestration.

- February 2026: Paychex added AI features to Paycor and Paychex Flex, including smart scheduling, agentic timesheet approvals, and AI-powered time-off.

Global AI-Native HCM Platform Market Report Scope

The AI-Native HCM Platform market refers to advanced human capital management solutions that embed artificial intelligence at the core of HR operations, combining workforce intelligence, skills analytics, conversational HR assistants, autonomous workflow automation, and AI-driven governance and compliance. Delivered through cloud, on-premises, and hybrid models, these platforms serve both large enterprises and SMEs across industries such as BFSI, healthcare, IT and telecom, retail, manufacturing, government, and others. The core purpose of this market is to transform HR management by leveraging AI for automation, predictive insights, compliance assurance, and enhanced employee engagement, thereby enabling organizations to optimize workforce productivity and strategic decision-making.

The AI-Native HCM Platform market report is segmented by Component (Platform Software, [AI Core HCM Platforms, AI Copilots and Conversational HR Assistants, Workforce Intelligence and Decision Engines, Skills Intelligence Platforms, Autonomous HR Workflow Automation Platforms, and AI Governance, Security and Compliance Platforms], and Services), Deployment Model (Cloud, On-Premises, and Hybrid Deployment), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Application (Talent Acquisition, Recruiting and Candidate Intelligence; Workforce Administration and Employee Intelligence; Payroll, Compensation and Benefits Intelligence; Workforce Planning, Analytics and Decision Intelligence; Learning, Skills Intelligence and Internal Mobility; Employee Experience, HR Service Delivery and AI Assistants; Autonomous HR Workflow Automation; and AI Governance, and Compliance amd Workforce Risk Management), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Platform Software | AI Core HCM Platforms |

| AI Copilots and Conversational HR Assistants | |

| Workforce Intelligence and Decision Engines | |

| Skills Intelligence Platforms | |

| Autonomous HR Workflow Automation Platforms | |

| AI Governance, Security and Compliance Platforms | |

| Services |

| Cloud |

| On-Premises |

| Hybrid Deployment |

| Large Enterprises |

| Small and Medium Enterprises |

| Talent Acquisition, Recruiting and Candidate Intelligence |

| Workforce Administration and Employee Intelligence |

| Payroll, Compensation and Benefits Intelligence |

| Workforce Planning, Analytics and Decision Intelligence |

| Learning, Skills Intelligence and Internal Mobility |

| Employee Experience, HR Service Delivery and AI Assistants |

| Autonomous HR Workflow Automation |

| AI Governance, Compliance and Workforce Risk Management |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Platform Software | AI Core HCM Platforms |

| AI Copilots and Conversational HR Assistants | ||

| Workforce Intelligence and Decision Engines | ||

| Skills Intelligence Platforms | ||

| Autonomous HR Workflow Automation Platforms | ||

| AI Governance, Security and Compliance Platforms | ||

| Services | ||

| By Deployment Model | Cloud | |

| On-Premises | ||

| Hybrid Deployment | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Application | Talent Acquisition, Recruiting and Candidate Intelligence | |

| Workforce Administration and Employee Intelligence | ||

| Payroll, Compensation and Benefits Intelligence | ||

| Workforce Planning, Analytics and Decision Intelligence | ||

| Learning, Skills Intelligence and Internal Mobility | ||

| Employee Experience, HR Service Delivery and AI Assistants | ||

| Autonomous HR Workflow Automation | ||

| AI Governance, Compliance and Workforce Risk Management | ||

| By End-user Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast size of the AI-Native HCM Platform Market?

The AI-Native HCM Platform Market stood at USD 14.68 billion in 2026 and is forecast to reach USD 39.15 billion by 2031, growing at a 21.68% CAGR over 2026-2031.

Which deployment model leads spending in AI-native HCM platforms?

Cloud led spending with 72.41% of 2025 revenue, but hybrid is growing faster because many regulated and large-enterprise environments still need a mix of cloud and on-premises infrastructure.

Which application area is growing the fastest in AI-native HCM platforms?

Autonomous HR workflow automation is the fastest-growing application, with a projected 24.18% CAGR through 2031, as buyers move from AI recommendations toward AI execution of multistep HR tasks.

Which customer size group is creating the fastest growth opportunity?

Small and medium enterprises are expanding the fastest at a 23.94% CAGR through 2031, helped by SaaS pricing, modular deployment, and easier access to AI tools once limited to large organizations.

Which region is expected to expand the fastest through 2031?

Asia-Pacific is projected to grow at a 24.47% CAGR through 2031, supported by greenfield cloud deployments and fewer legacy constraints than North America and Europe.

What is the biggest barrier to wider adoption of AI-native HCM platforms?

Sensitive HR data governance and explainability requirements remain the biggest barrier, especially where employment-related AI must meet strict oversight, documentation, and compliance standards.

Page last updated on: