HBM For AI Training Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.89 Billion |

| Market Size (2031) | USD 8.52 Billion |

| Growth Rate (2026 - 2031) | 24.14% CAGR |

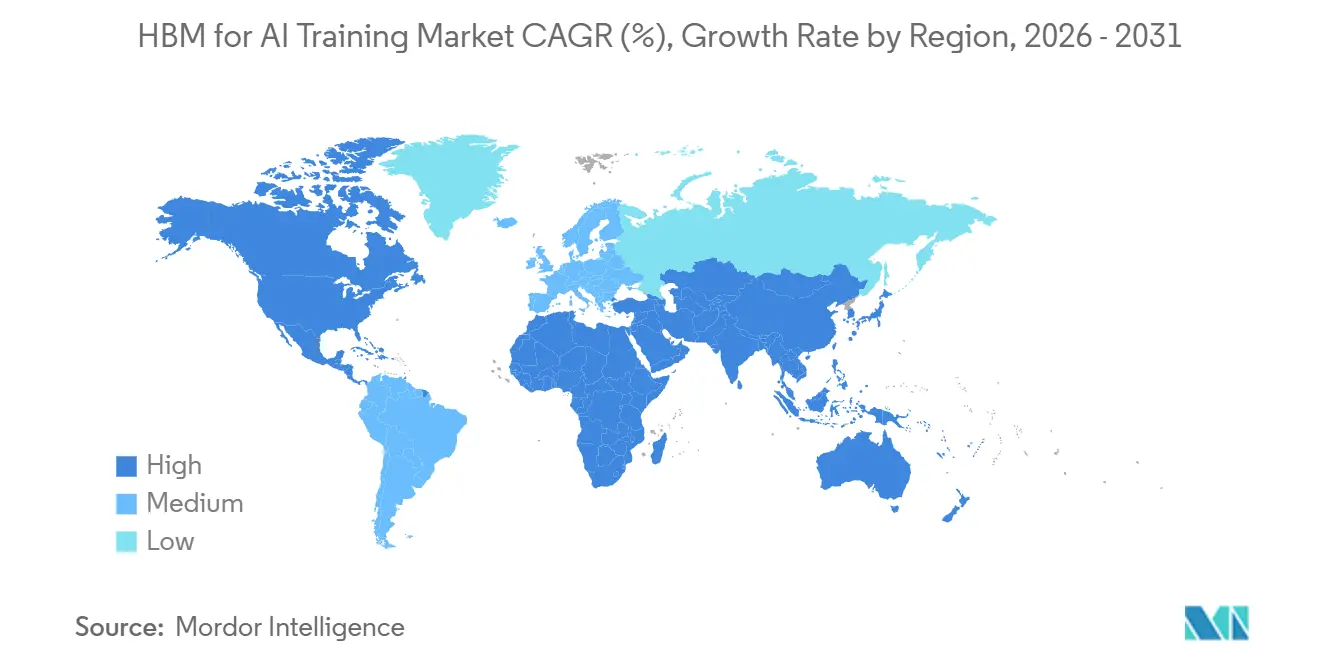

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HBM For AI Training Market Analysis by Mordor Intelligence

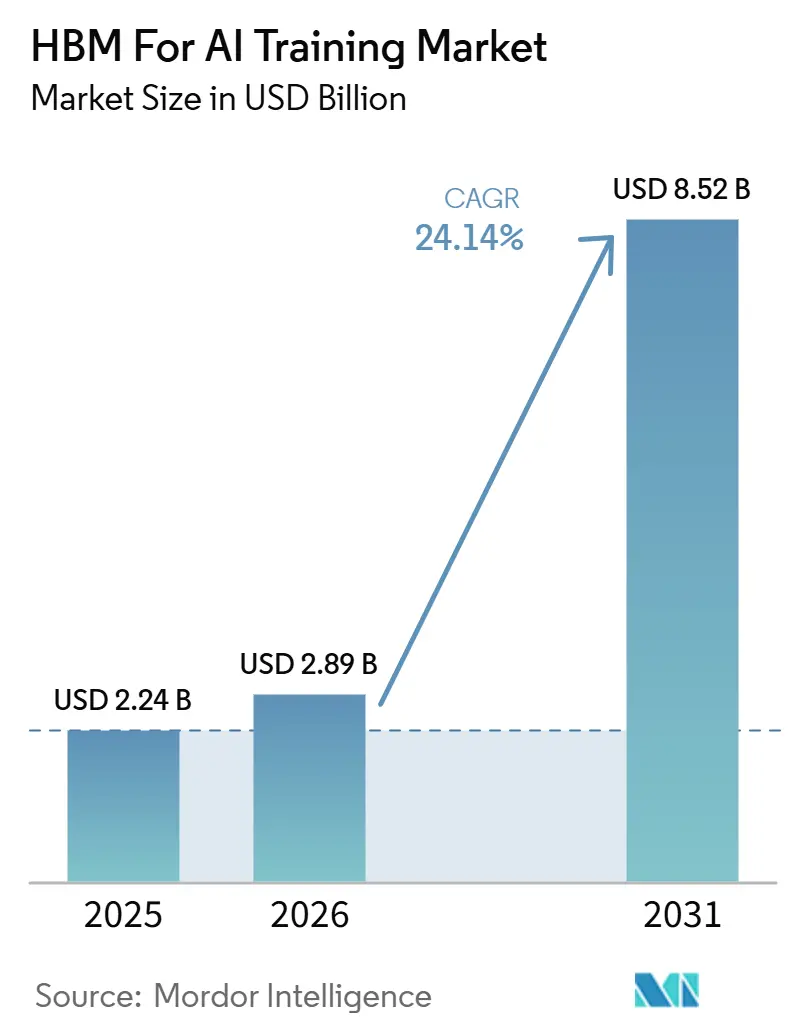

The HBM for AI training market size is expected to increase from USD 2.24 billion in 2025 to USD 2.89 billion in 2026 and reach USD 8.52 billion by 2031, growing at a CAGR of 24.14% over 2026-2031. The HBM for AI training market is expanding because each new AI accelerator cycle delivers more memory per processor, which increases HBM demand even as platform volumes rise at a steady pace. The HBM4 transition is strengthening this pattern in 2026 because leading GPU and custom silicon programs are moving to higher-capacity stacks with materially higher bandwidth requirements. Demand also remains concentrated in large training clusters, where hyperscalers and frontier AI labs continue to scale capital programs, while sovereign AI infrastructure programs are adding a second layer of multi-year procurement visibility. A narrow supplier base also shapes the HBM for AI training market, so qualification timing, packaging access, and co-development agreements influence revenue capture as much as manufacturing scale. Near-term expansion remains exposed to TSV yield pressure, advanced packaging constraints, and thermal management demands, but these same constraints reinforce the value of qualified supply and support continued investment across the HBM for AI training market.

Key Report Takeaways

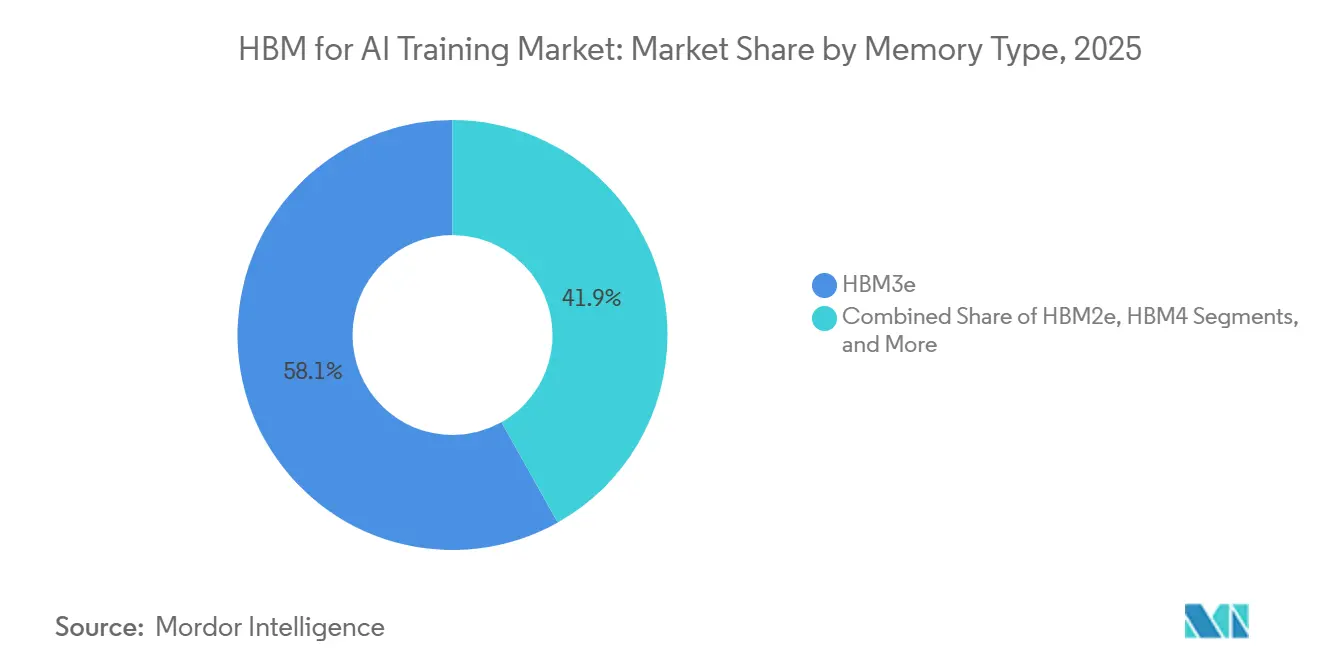

- By memory type, HBM3e led 58.14% of the HBM for AI training market in 2025, while HBM4 is projected to expand at a 24.96% CAGR through 2031.

- By deployment environment, hyperscale and cloud accounted for 87.33% of the HBM for AI training market in 2025, and it is projected to expand at a 24.73% CAGR through 2031.

- By interconnect and scaling, cluster-scale multi-node accounted for 61.74% of the HBM for AI training market in 2025, and it is projected to expand at a 24.68% CAGR through 2031.

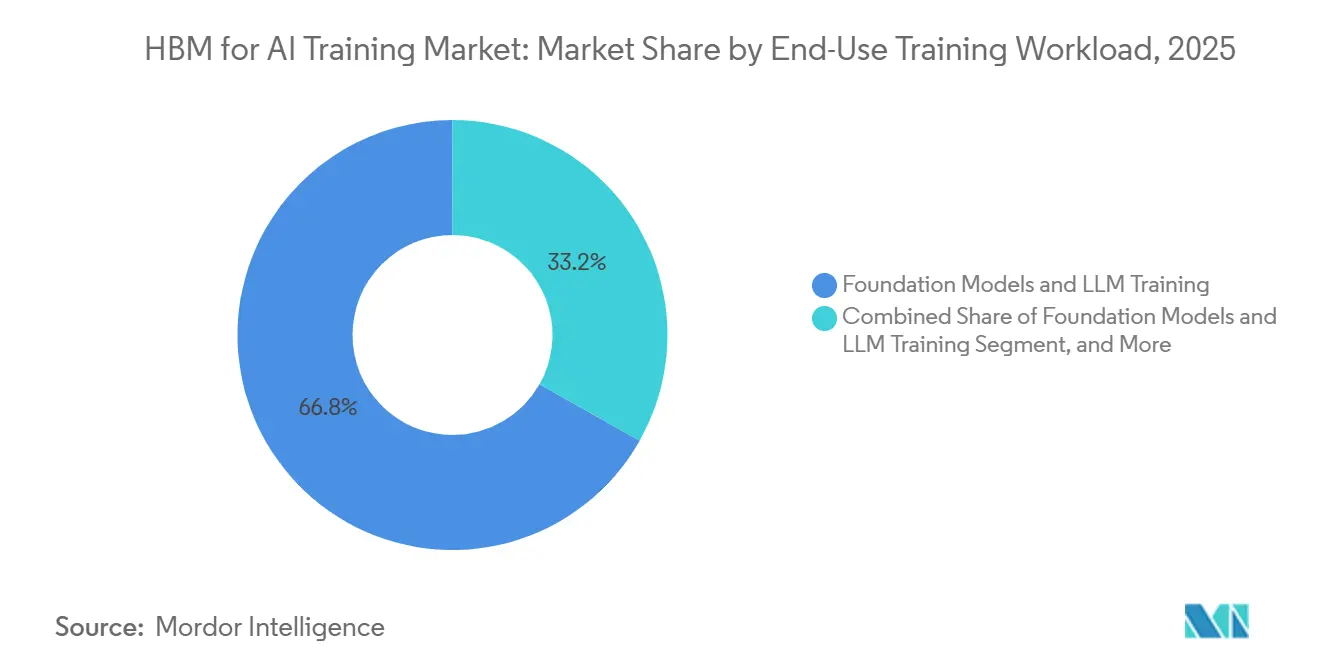

- By end-use training workload, foundation models and LLM training represented 66.82% of the HBM for AI training market in 2025, and it is projected to expand at a 24.94% CAGR through 2031.

- By processor type, GPUs held 91.18% of the HBM for AI training market in 2025, while AI ASICs are projected to expand at a 24.62% CAGR through 2031.

- By geography, North America held 51.68% of the HBM for AI training market in 2025, while Asia-Pacific is projected to grow at a 25.89% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HBM For AI Training Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Scaling of Frontier Model Training Clusters | +5.8% | Global | Short term (≤ 2 years) |

| HBM4 Readiness Across AI Accelerator Roadmaps | +4.9% | Global, APAC core | Short term (≤ 2 years) |

| Shift Toward Multi-TB Training Memory Footprints | +3.6% | North America and APAC | Medium term (2-4 years) |

| Rising Memory Share of Training GPU Bill Of Materials | +2.9% | Global | Short term (≤ 2 years) |

| Hyperscaler Reservation of Advanced Packaging Capacity | +2.2% | North America, APAC core, spill-over to EU | Short term (≤ 2 years) |

| Sovereign AI Buildouts Requiring Localized Accelerator Supply | +1.8% | Middle East, South Asia, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Scaling of Frontier Model Training Clusters

The HBM for AI training market is being pushed higher by the scale of frontier training systems that now require memory bandwidth at the rack and cluster level, not only at the single-chip level. NVIDIA’s GB200 NVL72 integrates 72 Blackwell GPUs into a single NVLink domain and supports up to 13.4 terabytes of HBM3e across the rack, demonstrating how one deployment unit now absorbs a very large memory footprint. The same architecture also delivers 1.8 terabytes per second of interconnect bandwidth per GPU, keeping large pools of HBM active during sustained training workloads rather than intermittent bursts. AWS Project Rainier went live in late 2025 with a cluster of approximately 500,000 Trainium2 chips for Anthropic, and that scale shows how a single customer program can drive very large HBM demand over a single training cycle.[1]Amazon, “AWS Project Rainier, The World’s Most Powerful Computer for Training AI,” Amazon, aboutamazon.com As more frontier model programs move from pilot phases into production, the HBM for the AI training market benefits from both higher unit deployments and higher memory content per system. That combination makes the HBM for AI training market less dependent on simple GPU shipment growth and more dependent on cluster design choices.

HBM4 Readiness Across AI Accelerator Roadmaps

HBM4 readiness is becoming a direct growth lever for the HBM for AI training market because the next platform wave is centered on larger stacks, higher bandwidth, and tighter memory integration. NVIDIA’s Vera Rubin architecture is in full production in 2026, with 288 gigabytes of HBM4 across 8 stacks and 13 terabytes per second of bandwidth, confirming a step change in memory capacity on flagship AI platforms. AMD's Instinct MI400 also targets 432 gigabytes of HBM4 and up to 19.6 terabytes per second, broadening HBM4 demand beyond a single vendor ecosystem. Samsung began mass production of commercial HBM4 in February 2026, indicating that supplier ramps are aligning with accelerator launch schedules rather than trailing them by a significant gap. Google 8th-generation TPU 8i features 288 gigabytes of HBM and doubles interconnect bandwidth over the prior generation, reinforcing that the HBM4 transition is now reaching custom silicon programs across hyperscale buyers. As qualification spreads across GPU, TPU, and ASIC roadmaps, the HBM for AI training market gains a broader demand base and stronger platform continuity through the forecast period.

Shift Toward Multi-TB Training Memory Footprints

The HBM for AI training market is also being lifted by a clear move toward multi-terabyte memory pools for training systems, and petabyte-scale shared memory at the supercomputer level. Google’s published TPU analysis showed that directly addressable shared HBM expanded 400 times from TPU v2 to Ironwood, rising from 4 terabytes to 1.77 petabytes. AWS Trainium3 delivers 144 gigabytes of HBM3e per chip with 4.9 terabytes per second of bandwidth, and one Trainium3 UltraServer scales to 20.7 terabytes of aggregate HBM3e. These memory pools support longer context windows, larger batch sizes, and more complex multimodal training runs that cannot be served efficiently by slower memory tiers. The shift also means that each new system generation consumes more HBM even before cluster counts are considered, which supports a structurally larger HBM for the AI training market. It also raises the cost of any supply disruption because a shortfall now affects larger memory footprints per deployment unit.

Rising Memory Share of Training GPU Bill of Materials

The HBM for AI training market is supported by the growing economic importance of memory in advanced accelerator systems. Each new flagship platform offers more HBM capacity and bandwidth, meaning memory now shapes procurement decisions more directly than in earlier AI hardware cycles. NVIDIA’s Vera Rubin platform and AMD’s MI400 both feature HBM configurations that are materially larger than those of prior generations, reflecting this shift in system design priorities. SK hynix and NVIDIA announced a multi-year technology partnership in June 2026, and that move shows that memory planning is now tied to accelerator roadmaps well before full production schedules are fixed. As memory becomes the key constraint in performance, availability, and system cost, buyers treat HBM procurement as a strategic decision rather than a component purchase. That change improves the visibility of the HBM for the AI training market because supply agreements are being secured earlier in the platform cycle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| TSV Yield Loss and Advanced Packaging Complexity | -2.4% | Global | Short term (≤ 2 years) |

| Foundry and OSAT Capacity Bottlenecks | -2.0% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Thermal Density and Power Envelope Constraints | -1.6% | Global | Medium term (2-4 years) |

| Supplier Concentration and Qualification Lead Times | -1.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

TSV Yield Loss and Advanced Packaging Complexity

TSV yield loss remains a major restraint on the HBM in the AI training market, as stack complexity increases with each generation. HBM4 imposes more advanced bonding requirements and tighter interfaces, resetting process learning during the shift from HBM3e to HBM4. Imec presented thermal and integration analyses at IEEE IEDM in December 2025, showing that 3D HBM-on-GPU integration raised operating temperature to 140.7°C under AI training workloads, highlighting how packaging, thermal design, and yield now move together. As stack heights increase, a defect in any layer can impair the usable stack, so output growth does not rise in a straight line with wafer input. That makes supply expansion slower than demand expansion, which can delay shipments across the HBM for the AI training market. It also raises the value of suppliers that have already qualified high-stack products on a scale.

Foundry and OSAT Capacity Bottlenecks

Foundry and OSAT bottlenecks limit the HBM for the AI training market because advanced packaging capacity must expand alongside memory supply and accelerator wafer starts. Even when HBM dies are available, AI systems cannot ship in volume without enough CoWoS and related integration capacity to connect memory and compute at scale. This keeps packaging access at the center of commercial execution for memory suppliers, GPU designers, and hyperscale buyers. The bottleneck also shifts competition away from pure memory output and toward ecosystem control, because companies with stronger packaging access can translate supply into revenue faster. In practice, the restraint is most visible in APAC production nodes, but its effects spread to North American system deployment schedules because many leading clusters depend on the same packaging chain. Until packaging capacity broadens meaningfully, the HBM for the AI training market will continue to face periods where demand is visible but not fully convertible into shipped systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Type: HBM4 Transition Resets the Supplier Qualification Order

HBM4 is the fastest-growing memory type in the HBM for AI training market, with the HBM4 market size projected to expand at a 24.96% CAGR through 2031. HBM3e led 58.14% of the HBM for AI training market in 2025 because it remained the incumbent generation in high-volume AI deployments and continued to serve the most active training rollouts. The HBM for AI training market also retained smaller positions for HBM2e and HBM3, mainly in lower-cost enterprise and research configurations where system replacement cycles move more slowly. SK hynix began volume production of HBM4 in early 2026 and shipped 12-Hi 48-gigabyte stacks with bandwidth above 2 terabytes per second, using MR-MUF packaging and a logic base die fabricated by TSMC.[2]SK hynix Newsroom, “2026 Market Outlook, SK hynix’s HBM to Fuel AI Memory Boom,” SK hynix, news.skhynix.com Samsung also began commercial HBM4 shipments in February 2026, with a transfer speed of 11.7 gigabits per second per pin, meeting the qualification requirements of leading AI platform buyers.

A more structural change in the HBM for AI training market is the move toward custom base die architectures within the HBM4 stack. This means memory suppliers are no longer selling only standardized stacks, because GPU and AI chip designers now want proprietary logic integrated inside the package itself. That design pattern creates a two-tier revenue structure, with standard configurations competing more directly on availability and custom configurations earning value from long-term co-development. Samsung stated in 2026 that more than half of its HBM output would shift toward HBM4, which shows how quickly supplier capacity is being redirected toward the new generation. As a result, the HBM for AI training market is moving through a reset point where qualification order, not only manufacturing scale, will shape supplier positioning during the next platform cycle.

By Deployment Environment: Hyperscale Dominance Conceals Enterprise Market Emergence

Hyperscale and cloud accounted for 87.33% of the HBM in the AI training market in 2025, underscoring the continued concentration of demand in very large training environments. The HBM for AI training market developed this way because multi-thousand-GPU or custom ASIC clusters require capital commitments, power access, and operational depth that only hyperscalers and a small group of AI labs can support. Project Rainier illustrates this concentration because one cloud-linked deployment scaled to approximately 500,000 Trainium2 chips for Anthropic’s training and inference workloads. The dominance of hyperscale buyers also means that the procurement timing of a few companies can influence near-term demand visibility across the HBM for the AI training market. At the same time, the concentration gives suppliers clearer customer signals because hyperscale roadmaps are tied to major platform transitions and longer reservation cycles.

Enterprise deployment remained much smaller in 2025, but its role is widening as HBM-dense systems become more available through infrastructure vendors and managed deployment models. Regulated sectors such as financial services, pharmaceuticals, and defense are gradually building on-premise training capacity because they cannot place all sensitive model development inside shared cloud environments. Government and research institutions form a separate path of demand, because procurement is tied more directly to sovereign AI programs and public compute initiatives than to commercial cloud cycles. That makes enterprise and government demand more episodic, but each purchase tends to be large because buyers often acquire full clusters rather than incremental capacity. As HBM4-based systems become more standardized through the later forecast period, the HBM for AI training market should gain a broader deployment mix even if hyperscale remains the anchor.

By Interconnect and Scaling: Cluster-Scale Multi-Node Defines the Frontier Training Architecture

Cluster-scale multi-node held 61.74% of the HBM for AI training market in 2025, which reflects the dominant architecture for very large model training. The HBM for AI training market has shifted toward this configuration because trillion-parameter and other frontier training workloads cannot remain inside the memory and bandwidth envelope of a single node. NVIDIA’s sixth-generation NVLink delivers 1.8 terabytes per second per GPU within the NVL72 rack-scale domain, and the Vera Rubin NVL72 is designed for 260 terabytes per second of aggregate GPU bandwidth. This architecture keeps larger memory pools active with lower communication friction, making HBM utilization more effective in rack-scale systems than in loosely connected, smaller clusters. It also increases the memory intensity per deployment because more HBM is tied to systems designed for synchronized training across large domains.

Single-GPU and multi-GPU intra-node systems remained relevant for inference, fine-tuning, and smaller, specialized training runs, but they accounted for a lower share of HBM demand in 2025. Their role in the HBM for AI training market is limited because the training scale has grown faster than single-node memory expansion alone can address. Published TPU and GPU system roadmaps also show that system designers are prioritizing interconnect and memory coherence together, not as separate upgrade paths. As model sizes and multimodal workloads continue to rise, cluster-scale deployments should remain the structural core of the HBM for AI training market. That keeps interconnect design tightly linked to HBM demand because the most valuable training systems are the ones that can keep very large memory pools addressable at scale.

By End-Use Training Workload: Foundation Model Economics Drive Memory Intensity

Foundation models and LLM training represented 66.82% of the HBM for AI training market in 2025, which made them the largest workload category by a wide margin. The HBM for AI training market reflects this concentration because transformer-based training at frontier scale requires sustained high-bandwidth memory access across very large parameter sets and long context windows. Amazon’s Project Rainier showed how a single foundation model deployment can translate into one of the world’s largest AI compute clusters, underscoring the HBM pull created by a single model roadmap. Google’s TPU 8i also expanded HBM capacity and interconnect bandwidth because pre-training and post-training for frontier models increasingly depend on keeping large memory pools directly addressable. This makes foundation model training the primary volume driver inside the HBM for the AI training market, especially when buyers are optimizing time to train rather than only chip count.

Computer vision, speech, and NLP, and recommendation and graph model training made up the remaining third of demand and still formed a meaningful part of the HBM for AI training market. Recommendation and graph workloads exhibit different memory access patterns, but their HBM requirements are increasing as graph sizes, feature depth, and personalization loops become more complex. Speech and broader NLP training are also gaining weight as multimodal models combine audio, text, and image processing inside one training stack. These categories do not yet match foundation model scale, but they widen the demand base because they bring more use cases into high-bandwidth training infrastructure. Over time, that mix strengthens the HBM for AI training market by reducing reliance on a single application path even while foundation models remain dominant.

By Processor Type: Custom ASICs Gain Ground in Hyperscale Training Deployments

GPUs held 91.18% of the HBM market share for AI training in 2025, reflecting the strength of the CUDA ecosystem and the lower execution risk of GPU-based clusters. The HBM for AI training market remains centered on GPUs, as most buyers prefer mature software tools, broad developer support, and proven deployment models for large-scale training. At the same time, AI ASICs are the fastest-growing processor segment, with the HBM for AI training market size for AI ASICs projected to grow at a 24.62% CAGR through 2031. AWS Trainium3 shows why, because it delivers 144 gigabytes of HBM3e per chip with 4.9 terabytes per second of memory bandwidth, while Trn3 UltraServer systems scale to 20.7 terabytes of aggregate HBM3e. SK hynix’s 2026 market outlook also stated that HBM demand from custom ASIC-based AI chips was expected to grow 82% in 2026 and account for one-third of total HBM demand, which supports the stronger growth profile of ASIC deployments.

FPGA accelerators remained a niche in the HBM for AI training market, mainly for research settings and early architecture testing before higher-volume GPU or ASIC choices are made. The more important change is that hyperscalers are increasingly willing to build custom silicon when workload shape, model architecture, and fleet economics are predictable. That can raise HBM intensity per chip because custom processors are designed around specific training and inference tradeoffs rather than broad workload compatibility. It also means that the processor mix in the HBM for AI training market is slowly widening even if GPUs remain the principal revenue base today. Over the forecast period, ASIC growth should make demand less dependent on one processor architecture and more closely tied to the memory needs of diversified AI compute fleets.

Geography Analysis

North America held 51.68% of the AI training market share in 2025, maintaining its position as the largest regional demand center. The HBM for AI training market remained anchored in North America because U.S.-based hyperscalers and frontier AI labs operated the largest installed pools of memory-dense training hardware. The regional demand base also benefited from a concentration of model developers such as Anthropic, OpenAI, and Meta AI, which kept the most advanced training programs close to North American cloud and colocation infrastructure. Micron’s development of a dedicated HBM facility in Idaho also linked memory supply planning more directly to U.S. industrial policy and domestic resilience goals. That combination of demand concentration and supply-chain repositioning kept North America at the center of the HBM for the AI training market in 2025.

Europe remained a secondary region in 2025, but its role in the HBM for AI training market was supported by sovereign compute initiatives and public cloud expansion. France announced EUR 109 billion (USD 119 billion) in AI investment in February 2025, signaling a multi-year path for hardware procurement and cluster buildout. Germany’s national AI compute efforts also added momentum by directing public investment toward training infrastructure that depends on high-bandwidth memory. These programs do not yet match North American scale, but they matter because they broaden the buyer base beyond commercial hyperscalers. In the HBM for AI training market, Europe’s importance is less about immediate volume leadership and more about creating sustained public-sector demand for large training systems.

Asia-Pacific is the fastest-growing regional segment of the HBM for AI training market, with a projected CAGR of 25.89% through 2031. The region combines the world’s highest concentration of HBM manufacturing capacity with critical advanced packaging infrastructure, which gives it a dual role as both supply base and demand center. South Korea remains central because SK hynix and Samsung are expanding HBM and packaging investment in line with AI training demand. Taiwan remains indispensable because advanced packaging for AI accelerators is concentrated there, which ties regional manufacturing directly to global deployment schedules.[3]Samsung Global Newsroom, “Samsung Ships Industry-First Commercial HBM4 With Ultimate Performance for AI Computing,” Samsung, news.samsung.com Japan and India are also expanding national AI compute programs, while South America and the Middle East and Africa remain earlier-stage demand centers with the Gulf states showing the strongest near-term cluster buildout potential. The HBM for AI training market therefore depends on Asia-Pacific not only for growth, but also for execution across the full supply chain.

Competitive Landscape

The HBM for AI training market operates with a highly concentrated supply structure led by SK hynix, Samsung Electronics, and Micron Technology. This triopoly persists because HBM development requires significant capital investment, deep process expertise, and lengthy qualification cycles that are difficult for new entrants to replicate. In the HBM for AI training market, supplier position is shaped not only by wafer output but also by successful qualification on new AI accelerator platforms. That makes customer alignment and time-to-qualification as important as absolute manufacturing scale. It also means revenue share can shift quickly during major platform transitions, even when the supplier list remains stable.

SK hynix strengthened its position in the HBM for AI training market through a multi-year technology partnership with NVIDIA, announced in June 2026. The agreement showed that memory roadmaps are now being planned in closer coordination with accelerator platform design, which raises barriers for suppliers that are not embedded early. Samsung pursued a different route by combining HBM memory, logic capability, and packaging ambition into a more integrated offer, and it began commercial HBM4 shipments in February 2026. Samsung also moved early on HBM4E sampling in 2026, which signaled its intent to compete on speed of commercial execution rather than only on scale. These moves show that the HBM for AI training market is competitive even within a small supplier set, because each company is trying to shape the next design cycle before demand peaks.

On the demand side, hyperscalers and AI chip designers are also reshaping the HBM for AI training market by building custom silicon and larger internal infrastructure fleets. Google’s TPU 8i and AWS Trainium3 show that memory-rich custom accelerators are becoming a durable part of the training hardware mix rather than a side path to GPUs.[4]Google Cloud, “AI Infrastructure at Next ’26,” Google Cloud Blog, cloud.google.com That widens the qualified customer base for HBM suppliers while also increasing pressure to support different stack designs, bandwidth targets, and packaging needs. The result is a market where concentration remains high, but competition inside the qualified supplier circle is intensifying as more buyers demand tailored memory solutions.

HBM For AI Training Industry Leaders

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

NVIDIA Corporation

Advanced Micro Devices, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: SK hynix and NVIDIA announced a multi-year technology partnership covering the co-development of next-generation memory aligned to NVIDIA's AI factory infrastructure roadmap and supply agreements for advanced memory across future accelerator platforms.

- June 2026: SK hynix began shipping 12-layer HBM4E samples to major customers, offering 48 gigabytes of capacity at 16 gigabits per second per pin with more than 20% better power efficiency than HBM4, initiating the qualification cycle for AI accelerators expected from 2027 onward.

- February 2026: Samsung Electronics began mass production of HBM4 and shipped the first commercial products to customers including NVIDIA, becoming the first supplier to deliver commercial HBM4 to market. The company's Pyeongtaek P5 facility came online in the same quarter dedicated to HBM stacking and packaging, with full ramp targeted for the second half of 2026.

- April 2026: SK hynix disclosed an additional investment of KRW 21.6 trillion (USD 13.9 billion) in Yongin semiconductor cluster Phase 2 through 6 cleanroom construction, dedicated to expanding HBM production capacity and advanced packaging capability in line with AI training demand growth through the forecast period.

Global HBM For AI Training Market Report Scope

The HBM for AI training market covers the development, production, and adoption of high-bandwidth memory solutions used to accelerate artificial intelligence training workloads in data centers, high-performance computing environments, and AI infrastructure. The market scope includes HBM technologies integrated with GPUs, AI accelerators, and other advanced processors that support large-scale model training by delivering high memory bandwidth, improved power efficiency, and faster data processing capabilities.

The HBM for AI Training Market Report is Segmented by Memory Type (HBM2e, HBM3, Hbm3e, and HBM4), Deployment Environment (Hyperscale and Cloud, Enterprise, and Government and Research), Interconnect and Scaling (Single GPU, Multi-GPU Intra-Node, and Cluster-Scale Multi-Node), End-Use Training Workload (Foundation Models and LLM Training, Computer Vision Training, Speech and NLP Model Training, and Recommendation and Graph Model Training), Processor Type (GPUs, AI ASICs, and FPGA Accelerators), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| HBM2e |

| HBM3 |

| HBM3e |

| HBM4 |

| Hyperscale and Cloud |

| Enterprise |

| Government and Research |

| Single GPU |

| Multi-GPU Intra-Node |

| Cluster-Scale Multi-Node |

| Foundation Models and LLM Training |

| Computer Vision Training |

| Speech and NLP Model Training |

| Recommendation and Graph Model Training |

| GPUs |

| AI ASICs |

| FPGA Accelerators |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Memory Type | HBM2e | |

| HBM3 | ||

| HBM3e | ||

| HBM4 | ||

| By Deployment Environment | Hyperscale and Cloud | |

| Enterprise | ||

| Government and Research | ||

| By Interconnect and Scaling | Single GPU | |

| Multi-GPU Intra-Node | ||

| Cluster-Scale Multi-Node | ||

| By End-Use Training Workload | Foundation Models and LLM Training | |

| Computer Vision Training | ||

| Speech and NLP Model Training | ||

| Recommendation and Graph Model Training | ||

| By Processor Type | GPUs | |

| AI ASICs | ||

| FPGA Accelerators | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 size of the HBM for AI training market?

The HBM for AI training market size is USD 2.89 billion in 2026 and is forecast to reach USD 8.52 billion by 2031 at a 24.14% CAGR over 2026-2031.

Why is demand for HBM in AI training rising so quickly?

Demand is rising because every new accelerator generation carries more HBM capacity and higher bandwidth, while frontier training clusters also keep expanding in scale.

Which region leads HBM demand for AI training systems?

North America led in 2025 with 51.68% share because major hyperscalers and frontier AI labs are concentrated in the United States.

Which region is growing fastest for HBM in AI training?

Asia-Pacific is the fastest-growing region with a projected CAGR of 25.89% through 2031, supported by HBM manufacturing concentration and expanding AI compute programs.

Which processor category is growing fastest in AI training hardware?

GPUs still dominated with 91.18% share in 2025, but AI ASICs are projected to grow fastest at a 24.62% CAGR through 2031.

What is the biggest deployment environment for HBM-based AI training systems?

Hyperscale and cloud remained the largest deployment environment with 87.33% share in 2025 because large training clusters require very high capital, power, and operating scale.

Page last updated on: