Cardiac AI Monitoring And Diagnostic Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

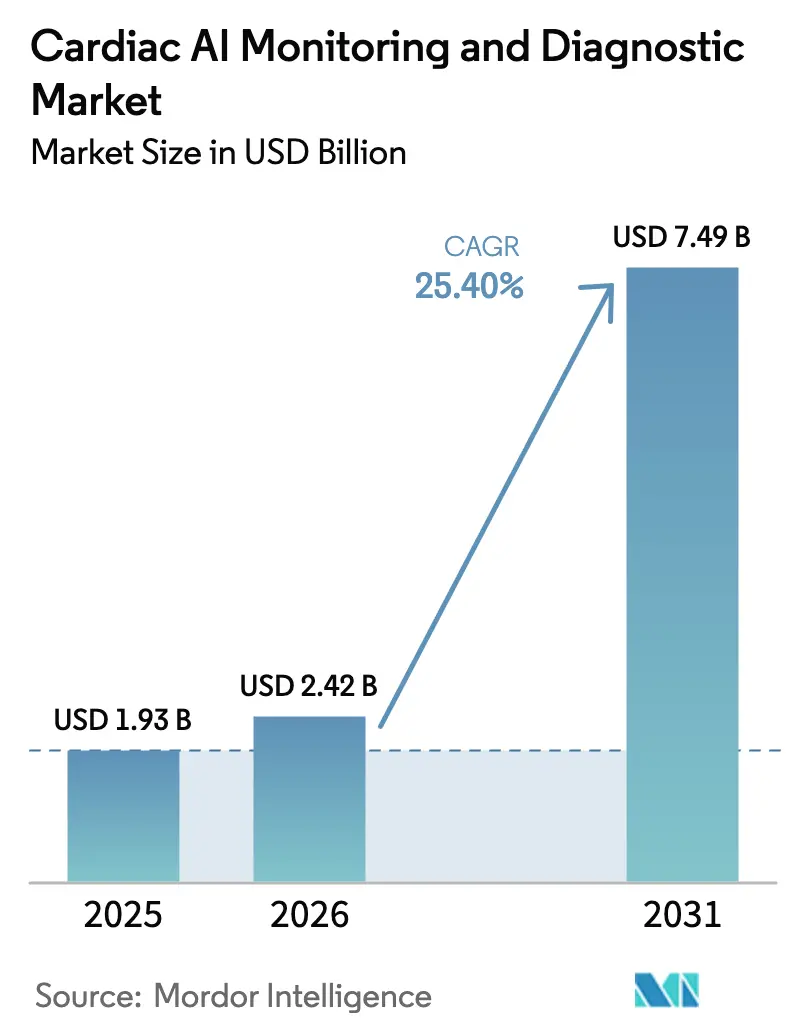

| Market Size (2026) | USD 2.42 Billion |

| Market Size (2031) | USD 7.49 Billion |

| Growth Rate (2026 - 2031) | 25.40% CAGR |

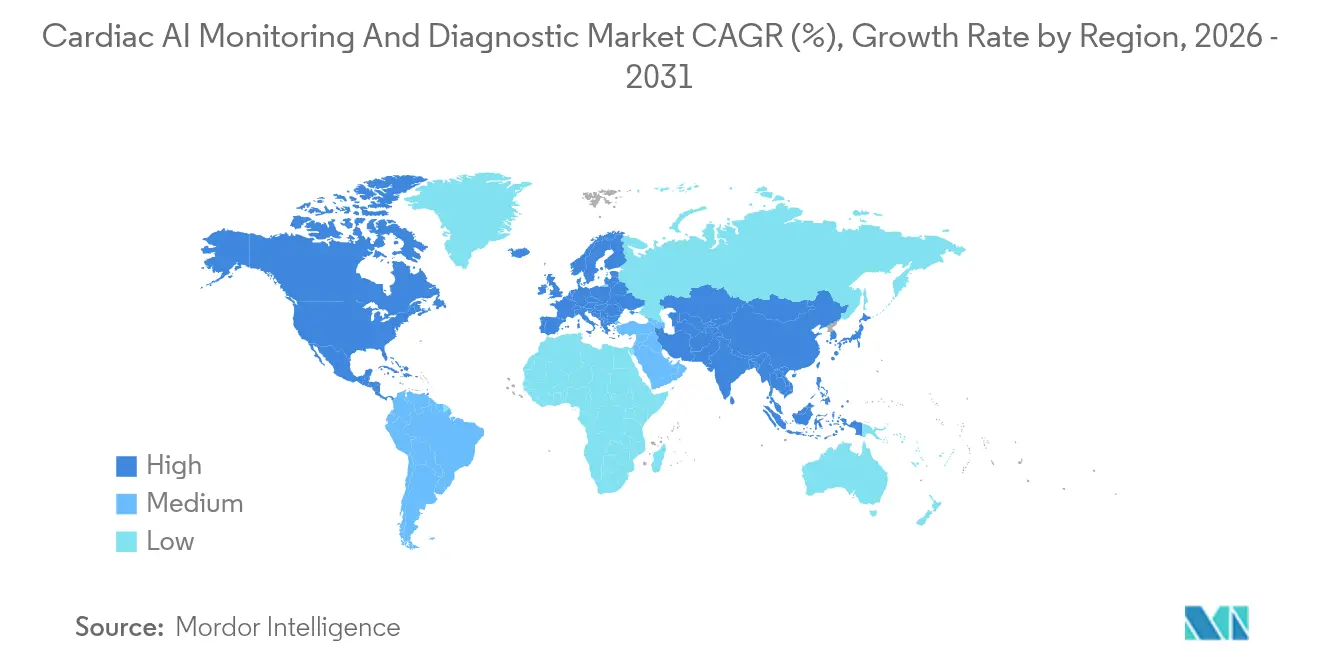

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiac AI Monitoring And Diagnostic Market Analysis by Mordor Intelligence

The cardiac AI monitoring and diagnostic market size is expected to grow from USD 1.93 billion in 2025 to USD 2.42 billion in 2026 and is forecast to reach USD 7.49 billion by 2031 at 25.4% CAGR over 2026-2031. The surge stems from growing cardiovascular disease prevalence, Medicare coverage decisions backing AI coronary plaque analysis, and the FDA’s steady stream of 160+ cardiology algorithm clearances. Cloud-native subscription models, edge-AI hardware, and wearable ECG ecosystems further elevate demand. Hospitals view technology as a path to earlier diagnosis, reduced readmissions, and streamlined workflows, while investors funnel fresh capital into developers who can navigate fast-track regulatory pathways.

Key Report Takeaways

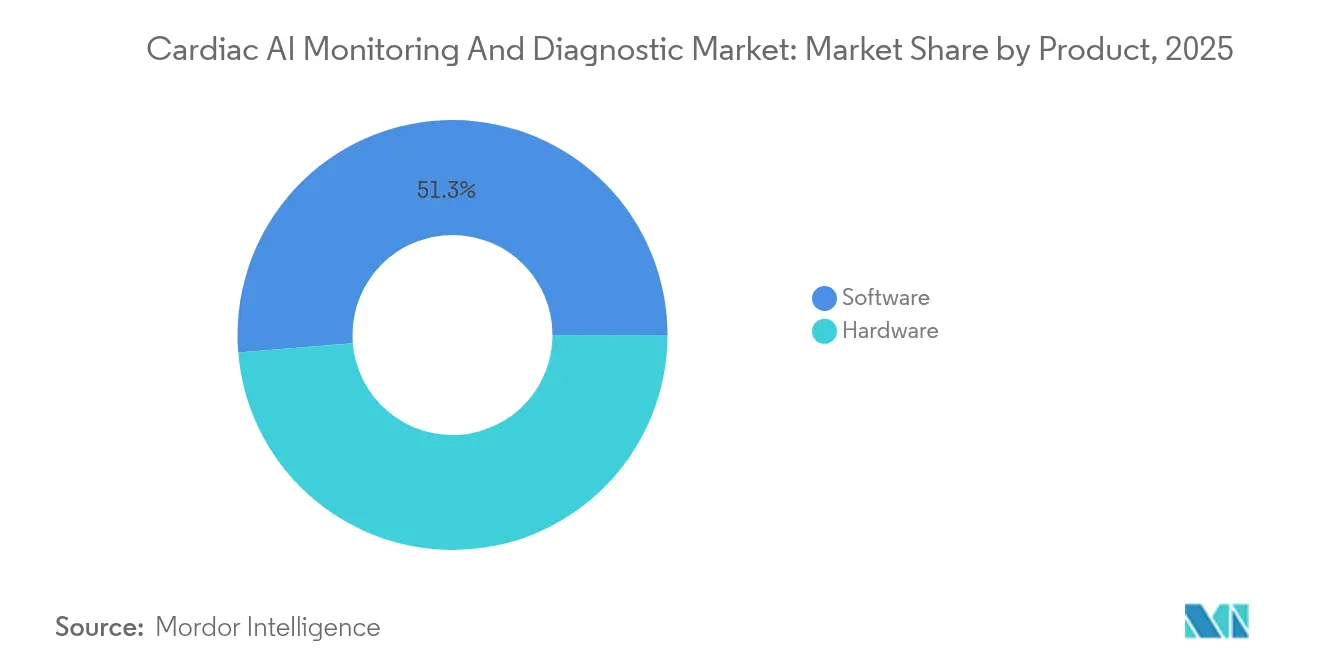

- By product type, software platforms dominated with 51.30% revenue share in 2025; SaaS plus edge-AI hardware is projected to expand at a 25.9% CAGR through 2031.

- By application, cardiac arrhythmia held 29.30% of the cardiac AI monitoring and diagnostic market share in 2025, whereas stroke detection algorithms are forecast to grow at 25.52% CAGR to 2031.

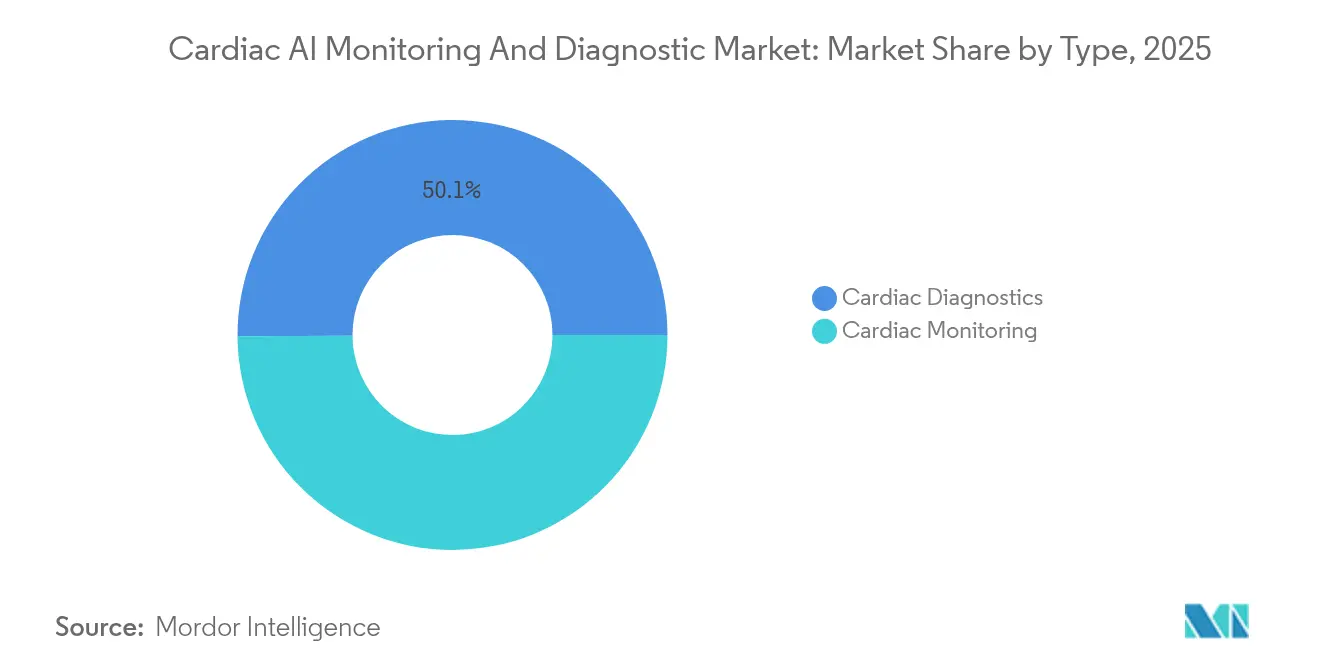

- By type, diagnostics accounted for 50.10% share of the cardiac AI monitoring and diagnostic market size in 2025; monitoring solutions are set to climb to 25.05% CAGR during 2026-2031.

- By end user, hospitals led with a 29.60% share in 2025, but diagnostic centers will register the fastest 26.4% CAGR to 2031.

- By geography, North America commanded a 28.70% share in 2025, while Asia Pacific is poised for the quickest 25.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardiac AI Monitoring And Diagnostic Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cardiovascular burden & tele-health expansion | +6.80% | Global; aging populations in North America, Europe, Japan | Medium term (2-4 years) |

| Government precision-medicine programs & reimbursements | +5.20% | North America, EU, selected APAC nations | Long term (≥4 years) |

| FDA fast-track clearances for cardiology algorithms | +4.90% | Global spillover from United States | Short term (≤2 years) |

| Shift to ambulatory & wearable ECG data streams | +4.10% | APAC focus, rising in North America | Medium term (2-4 years) |

| Multimodal imaging-AI to boost diagnostic yield | +3.70% | North America, EU | Long term (≥4 years) |

| Cloud-native subscription AI lowering capital cost | +2.40% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Cardiovascular Burden & Tele-Health Push

A record 121.5 million adults in the United States live with cardiovascular disease, prompting providers to adopt remote patient monitoring platforms that now embed AI in 35% of their solutions.[1]Ascension Saint Thomas, “Cardiovascular Disease Statistics 2025,” ascension.org Cardiovascular use already accounts for 21% of the USD 14-15 billion 2024 remote monitoring market, and AI-guided platforms such as Biofourmis demonstrate lower readmission rates through predictive analytics. Value-based payment models amplify urgency, positioning the cardiac AI monitoring and diagnostic market at the core of scalable chronic-care delivery.

Government Precision-Medicine AI Programs & Reimbursements

Federal funding initiatives, including ARPA-H’s PRECISE-AI and the NHLBI’s TOPMed program, channel resources toward trustworthy cardiac algorithms, while Medicare’s 2024 plaque-analysis coverage unlocks broad reimbursement.[2]ARPA-H, “PRECISE-AI Program Description,” arpa-h.gov The American Heart Association’s USD 12 million research commitment underscores a policy environment that rewards clinically validated AI and accelerates technology diffusion across health systems.

FDA Fast-Track Clearances for Cardiology Algorithms

Breakthrough designations for Cleerly’s CAD staging and Powerful Medical’s PMcardio STEMI tool illustrate truncated commercialization timelines. The agency’s predetermined change-control framework lets manufacturers refine algorithms post-approval, fostering rapid iteration while safeguarding patient safety.

Multimodal Imaging-AI Improves Diagnostic Yield

North American and European centers increasingly combine echocardiography, CT, and MRI feeds into unified AI pipelines that improve plaque characterization and shorten report turnaround times by up to 40%. Investments in high-performance inference chips aim to bring similar capabilities to select Asia Pacific tertiary hospitals during the forecast window.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability Gaps With Legacy Cardiology IT | -3.80% | Global, with acute impact in established healthcare systems with legacy infrastructure | Medium term (2-4 years) |

| Bias & Generalizability Issues Across Ethnic Groups | -2.10% | Global, with particular concern in diverse populations of North America and multicultural regions | Long term (≥ 4 years) |

| Data-Privacy Rules Limit Large-Scale Cardiac Data Sharing | -1.90% | North America & EU leading with GDPR and HIPAA compliance requirements, expanding globally | Short term (≤ 2 years) |

| Reimbursement Uncertainty For Stand-Alone AI Software | -1.40% | Global, with particular impact in emerging markets and healthcare systems with limited AI coverage policies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Interoperability Gaps With Legacy Cardiology IT

Parallel systems and incompatible data standards erode workflow efficiency despite validated AI gains. The American Heart Association highlights fragmented interfaces as a primary roadblock to scaling real-time decision support.[3]American Heart Association, “AI Research Grant Announcement,” heart.org Hospitals must invest in FHIR-compliant APIs and vendor-neutral archives before fully realizing AI benefits.

Bias & Generalizability Issues Across Ethnic Groups

Models trained on homogeneous datasets underperform among minority populations; for instance, deep-learning ECG tools show weaker predictive power in young Black women. Ongoing bias-mitigation efforts entail larger, balanced training cohorts and continuous algorithm auditing, adding cost and complexity but ensuring equitable care delivery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Software Dominance Drives Cloud Migration

Software accounted for 51.30% of 2025 revenue, establishing the cardiac AI monitoring and diagnostic market size leadership position. Hospitals gravitate to subscription deployments that bundle algorithm updates, cybersecurity, and analytics dashboards. Meanwhile, SaaS-plus-edge hardware is projected to register a 25.9% CAGR, fueled by on-device inference needs in wearable monitors and ambulatory clinics. Hardware traction intensifies as chipmakers unveil ultra-low-power neural processors consuming just 4.4 mW, sustaining continuous rhythm analysis with negligible battery impact.

Hybrid architectures that split processing between the device and the cloud keep patient data on-site while exploiting cloud elasticity for heavy training workloads. LSU Health Network’s HIPAA-compliant rollout illustrates how community hospitals outsource AI operations yet retain full data control, reinforcing software’s central role in the cardiac AI monitoring and diagnostic market.

By Application: Stroke Detection Accelerates Beyond Arrhythmias

Cardiac arrhythmias held 29.30% of the 2025 value, anchoring the cardiac AI monitoring and diagnostic market. FDA-cleared ECG analytics reduce manual review time, freeing cardiologists for complex cases. However, stroke detection solutions top the growth chart at a 25.52% CAGR as emergency departments adopt rapid CT-based AI triage capable of sizing lesions in 20 seconds.

Ensemble models combining coronary plaque, stenosis, and ventricular function further diversify application breadth. This pivot broadens revenue sources and curbs overreliance on arrhythmia workflows.

By Type: Monitoring Segment Outpaces Diagnostics

Diagnostics retained a 50.10% share of the cardiac AI monitoring and diagnostic market size in 2025, thanks to established imaging reimbursement codes. Yet monitoring platforms are predicted to climb 25.05% annually, mirroring health-system moves toward longitudinal disease management.

Implantable loop recorders and patch-based wearables feed continuous streams into cloud classifiers, issuing early alerts for decompensation. Providers that once adopted AI for spot diagnostics now seek unified dashboards aggregating diagnostics and monitoring to support preventive care strategies.

By End User: Diagnostic Centers Lead Growth

Hospitals captured 29.60% revenue in 2025, but diagnostic centers will exhibit the fastest 26.4% CAGR. Reimbursement clarity around AI-assisted plaque analysis empowers independent imaging chains to market premium, AI-enhanced studies.

Community clinics also embrace plug-and-play SaaS to offset specialist shortages, democratizing advanced cardiac insights. Research institutes, while smaller in revenue terms, drive algorithm benchmarking across diverse cohorts, directly improving fairness and generalizability within the cardiac AI monitoring and diagnostic market.

Geography Analysis

North America secured 28.70% of global revenue in 2025, bolstered by Medicare’s plaque-analysis coverage and a dense network of academic-industry alliances. Mayo Clinic’s ultrasound AI partnership with UltraSight typifies the region’s translational ecosystem, blending clinical data access with algorithm refinement. Venture investors poured USD 43 million into Octagos Health’s platform, reinforcing capital-market confidence.

Asia Pacific is on course for a 25.85% CAGR through 2031, propelled by large-scale deployments like Shanghai’s CardioMind system serving 820,000 annual outpatient visits. India’s National Health Authority is codifying AI standards alongside IIT Kanpur, aligning regulatory clarity with market depth. Japan, South Korea, and Australia leverage established imaging infrastructure and regulatory convergence with the FDA to expedite product approvals, further enlarging regional demand within the cardiac AI monitoring and diagnostic market.

Europe advances under the Medical Device Regulation and the forthcoming AI Act. High-risk medical software must clear CE marking, yet firms such as Caption Health have already obtained certification, illustrating viable compliance pathways. Post-Brexit, the United Kingdom deploys UKCA marking while funding digital health accelerators to remain competitive. Switzerland’s pragmatic recognition of FDA-approved devices mitigates disruption from shifting EU ties. These frameworks encourage steady adoption rates but necessitate robust post-market surveillance once AI tools enter routine cardiology practice.

Competitive Landscape

The cardiac AI monitoring and diagnostic industry remains moderately fragmented. HeartFlow leads in non-invasive physiological assessments, while Cleerly capitalizes on AI coronary staging. Viz.ai’s alliance with Cleerly integrates plaque analysis into a stroke-triage platform covering 1,600 hospitals, demonstrating a coopetition model centered on workflow integration over hardware lock-in. Funding cycles favor specialized innovators; Vektor’s USD 16 million round supports arrhythmia detection, and Acorai’s USD 4.5 million funds non-invasive hemodynamic monitoring.

Multimodal pipelines that fuse imaging, ECG, and wearable data are emerging white space. Bias-mitigation toolkits and edge-optimized inference also differentiate offerings. Vendors pursuing subscription revenues expand faster than perpetual-license incumbents, aided by recurring cash flows and seamless algorithm updates.

Ultimately, clinical validation, reimbursement access, and seamless interoperability will dictate competitive staying power within the cardiac AI monitoring and diagnostic market.

Cardiac AI Monitoring And Diagnostic Industry Leaders

Koninklijke Philips NV

GE HealthCare Technologies

Medtronic plc

Siemens Healthineers AG

iRhythm Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: VUNO’s cardiac arrest risk monitor obtained EU and UK certification, expanding market access.

- April 2025: HeartBeam and AccurKardia integrated advanced ECG analytics into their monitoring suite.

- March 2025: Powerful Medical secured breakthrough status for its PMcardio STEMI ECG algorithm.

- February 2025: HeartFlow’s AI plaque analysis received favorable Medicare coverage across five MACs.

Global Cardiac AI Monitoring And Diagnostic Market Report Scope

As per the scope of the report, cardiac AI monitoring and diagnostic solutions are integrated with artificial intelligence technologies, which are used to monitor and diagnose various cardiac diseases. The cardiac AI monitoring and diagnostic market is segmented into product, type, application, end user, and geography. By product, the market is segmented into software and hardware. By application, the market is segmented into cardiac arrhythmias, stroke, ischemic heart disease, stenosis, and other applications (pericardial disease and angina). By type, the market is segmented into cardiac diagnostics (imaging and ECG-based) and cardiac monitoring. By end user, the market is segmented into hospitals, specialty clinics, diagnostic centers, and research and academic institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for the above segments.

| Software |

| Hardware |

| Cardiac Arrhythmias |

| Stroke |

| Ischemic Heart Disease |

| Stenosis |

| Other Applications |

| Cardiac Diagnostics | Imaging |

| ECG-based | |

| Cardiac Monitoring |

| Hospitals |

| Specialty Clinics |

| Diagnostic Centers |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Software | |

| Hardware | ||

| By Application | Cardiac Arrhythmias | |

| Stroke | ||

| Ischemic Heart Disease | ||

| Stenosis | ||

| Other Applications | ||

| By Type | Cardiac Diagnostics | Imaging |

| ECG-based | ||

| Cardiac Monitoring | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Diagnostic Centers | ||

| Research & Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the cardiac AI monitoring and diagnostic market?

The market is valued at USD 2.42 billion in 2026 and is projected to reach USD 7.49 billion by 2031.

Which product category leads the cardiac AI monitoring and diagnostic market?

Software platforms command 51.30% revenue share, reflecting strong demand for scalable cloud and SaaS models.

Which application is growing fastest?

Stroke detection algorithms are forecast to grow at 25.52% CAGR, outpacing other applications.

Why are diagnostic centers adopting cardiac AI so rapidly?

Favorable reimbursement for AI plaque analysis and easy-to-deploy SaaS tools let diagnostic centers offer advanced studies without hiring additional specialists.

What restrains wider AI adoption in cardiology?

Interoperability gaps with legacy IT and algorithm bias across ethnic groups remain key hurdles requiring technical and regulatory attention.

Page last updated on: