AI In Remote Patient Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.44 Billion |

| Market Size (2031) | USD 5.20 Billion |

| Growth Rate (2026 - 2031) | 16.38% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

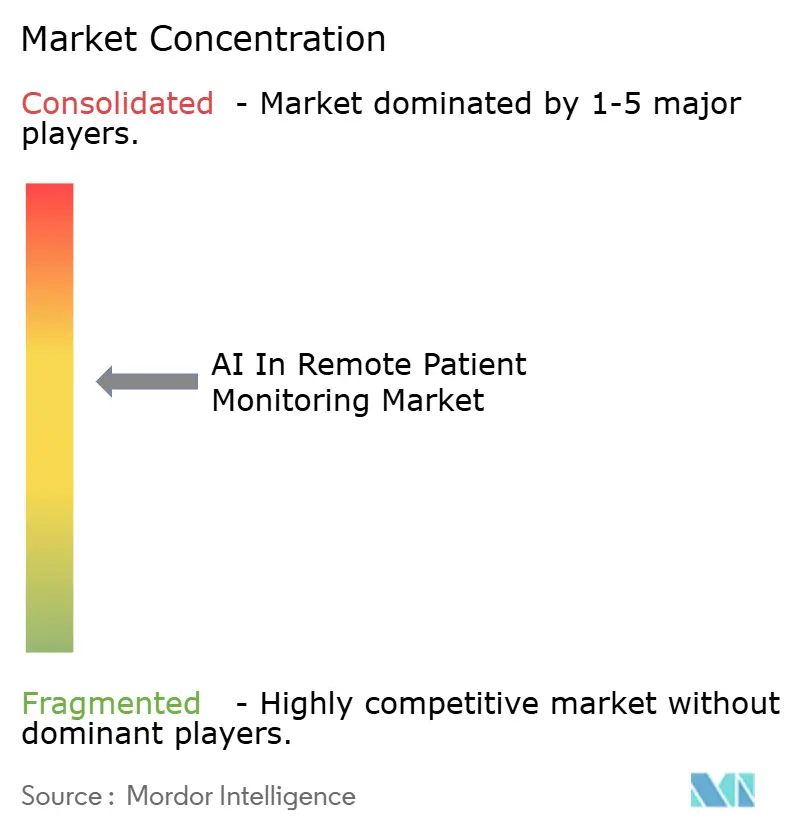

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Remote Patient Monitoring Market Analysis by Mordor Intelligence

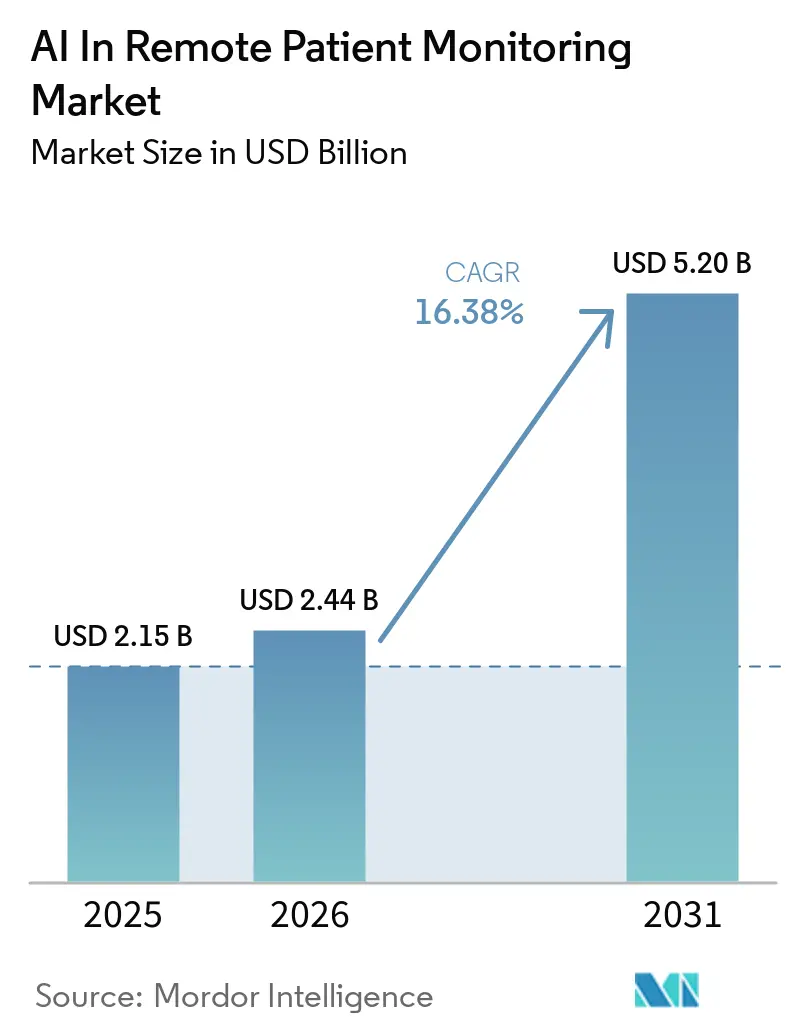

The AI in remote patient monitoring market is expected to grow from USD 2.15 billion in 2025 to USD 2.44 billion in 2026 and is forecasted to reach USD 5.20 billion by 2031 at 16384% CAGR over 2026-2031. The AI in remote patient monitoring market is expanding because chronic noncommunicable diseases still create a large pool of patients who need continuous follow-up, and these diseases account for 41 million deaths each year, or 74% of all deaths globally. The AI in remote patient monitoring market is also benefiting from a payment environment that increasingly rewards measurable outcomes, with Medicare payments for remote patient monitoring services in the United States rising above USD 536 million in 2024 and nearly 1 million enrollees receiving RPM services that year. What separates this cycle from earlier adoption is that AI now acts more as a clinical decision layer, which shortens the path between incoming data and intervention. Revenue concentration in software platforms and cloud delivery still defines the AI in remote patient monitoring market, but faster growth in managed services shows that buyers are paying for operating support and clinical workflow execution rather than only for software access. Vendors that can pair strong interoperability with auditable AI models are likely to stay better aligned with tightening provider procurement standards.

Key Report Takeaways

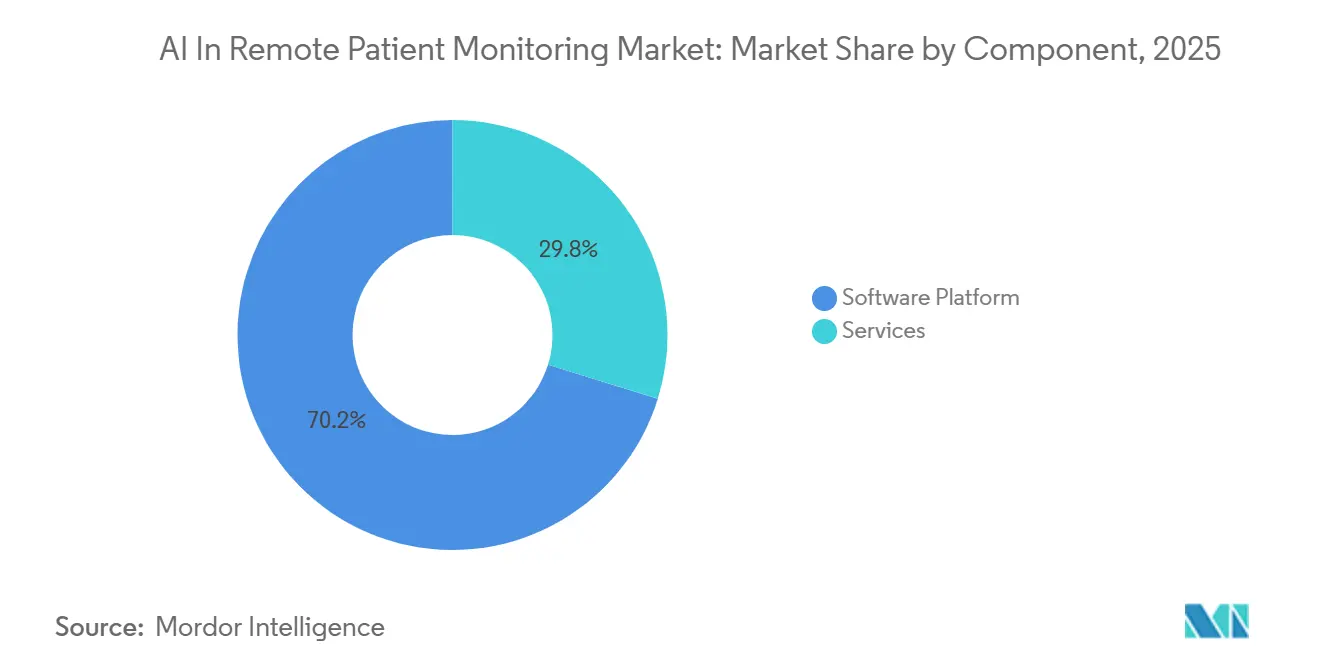

- By component, software platforms led with 70.24% revenue share in 2025, while services are projected to expand at a 17.47% CAGR through 2031.

- By deployment mode, cloud-based deployment held 55.76% share in 2025 and is also expected to grow at 18.37% CAGR through 2031.

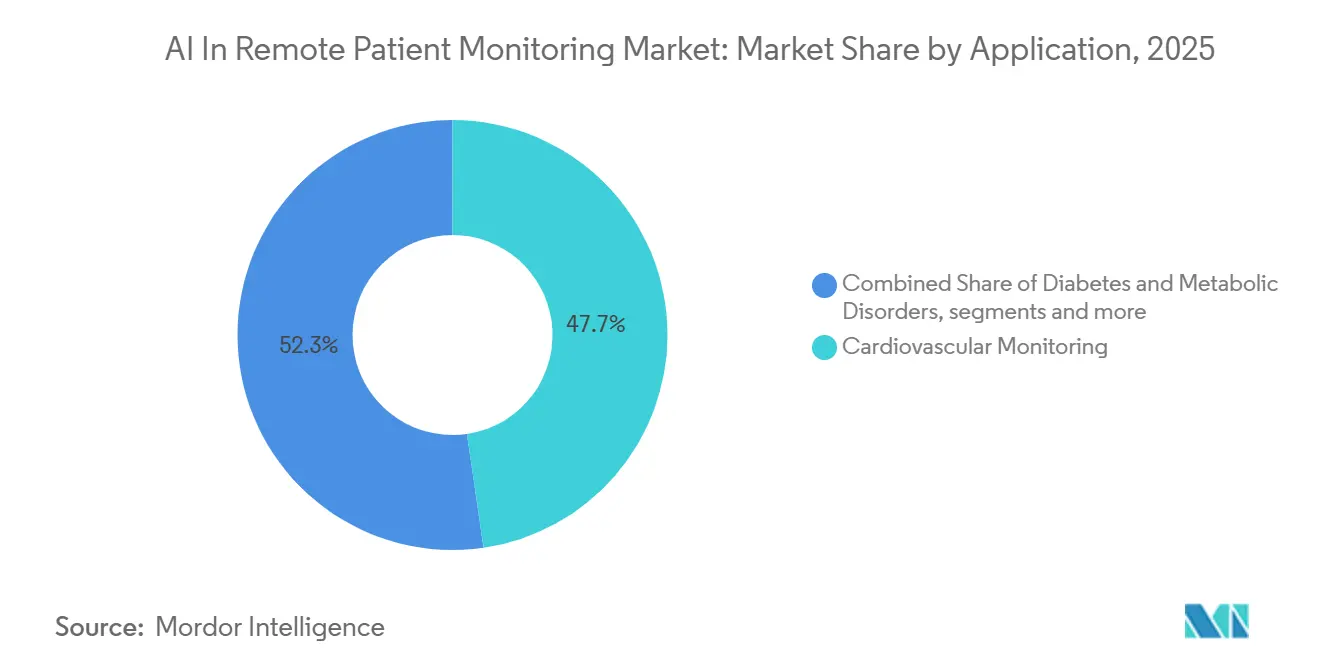

- By application, cardiovascular monitoring accounted for 47.74% share in 2025, while diabetes and metabolic disorders are projected to grow at a 17.86% CAGR through 2031.

- By end-user, hospitals and clinics captured 50.25% market share in 2025, while home-care settings are projected to advance at an 18.44% CAGR through 2031.

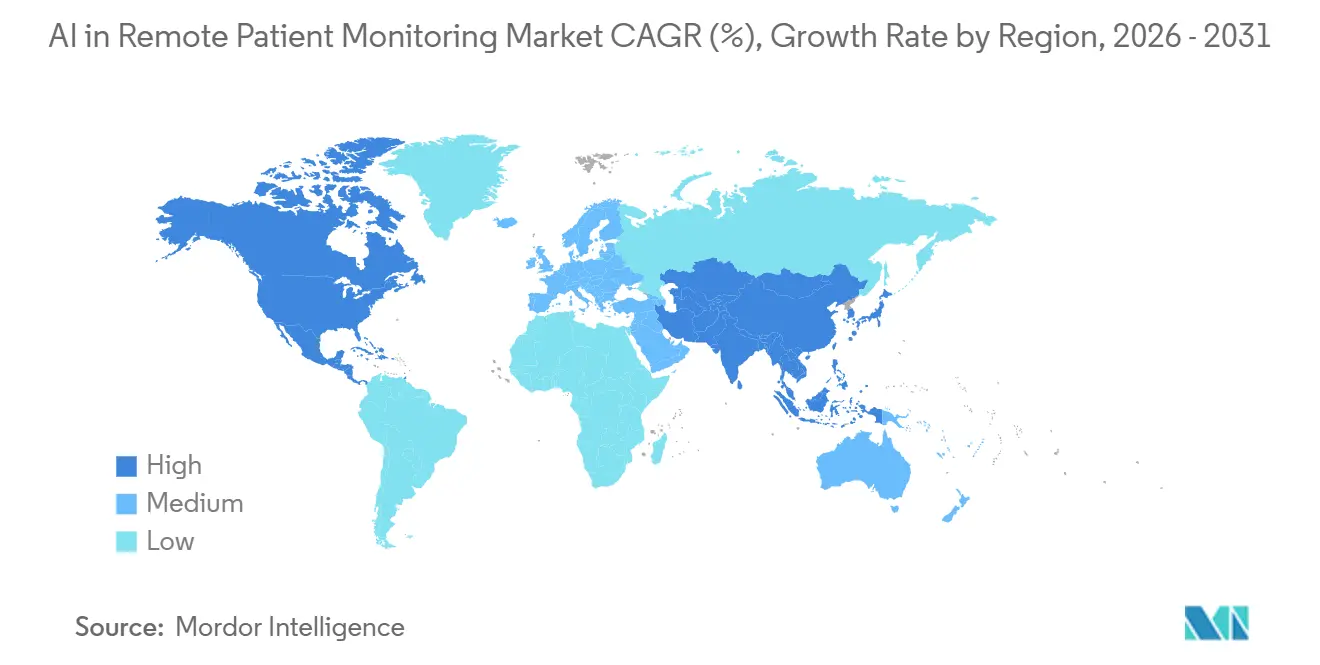

- By region, North America led with 54.37% revenue share in 2025, while the Asia-Pacific is projected to expand at a 19.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Remote Patient Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ubiquitous Chronic Disease Burden and Telehealth Reimbursement Mandates | +4.5% | Global | Medium term (2-4 years) |

| Advancements in AI Enabled Edge Processing and Wearable Efficiency | +3.2% | Global, North America and APAC core | Long term (≥ 4 years) |

| Real Time AI Edge Processing Chips Extending Wearable Battery Life | +1.8% | Global, APAC and North America core | Medium term (2-4 years) |

| Expansion of Hospital at Home and Decentralized Care Delivery Models | +2.8% | North America and EU | Short term (≤ 2 years) |

| Shift Toward Value Based Care and Population Health Management Programs | +2.4% | North America, with early gains in EU | Medium term (2-4 years) |

| Federated Learning Models Solving Cross Border Data Privacy Barriers | +1.2% | EU, with emerging adoption in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ubiquitous Chronic-Disease Burden and Telehealth Reimbursement Mandates

The AI in remote patient monitoring market is seeing durable demand because chronic disease management requires contact far more often than periodic office visits can provide. Noncommunicable diseases now account for 74% of global deaths, with cardiovascular disease, diabetes, and chronic respiratory illness carrying a major share of that burden. That clinical need is turning into spend because the CMS ACCESS model links recurring chronic care payments to health outcomes rather than to device activity alone. Medicare also continues to scale its use of remote monitoring, with payments above USD 536 million in 2024 and enrollment nearing 1 million beneficiaries.[1]U.S. Department of Health and Human Services Office of Inspector General, “Data Snapshot: Billing for Remote Patient Monitoring in Medicare,” HHS OIG, connectwithcare.org Published program evidence is helping health systems justify larger budgets, with a Mayo Clinic Proceedings study highlighted in late 2025 showing lower total cost of care and lower inpatient spending for patients in a structured RPM program. As that financial case becomes clearer, the AI in remote patient monitoring market is moving further into mainstream care pathways.

Advancements in AI-Enabled Edge Processing and Wearable Efficiency

The AI in remote patient monitoring market is gaining from better on-device inference, because more signal processing can now happen at the point of capture instead of being pushed to the cloud first. That shift helps lower bandwidth demand, improves device efficiency, and makes continuous monitoring more practical for longer wear periods. It also changes where differentiation sits, since better chip performance alone does not remove the value of proprietary algorithms and labeled training data. In the AI in remote patient monitoring market, vendors with strong biosignal libraries still have an advantage when they train deterioration detection, rhythm analysis, or predictive risk models. iRhythm has pointed to more than 3 billion hours of curated ECG data and continued algorithm development, which shows how data depth can remain a moat even as hardware improves.[2]: iRhythm Technologies, “Data Presented at ACC.26 and Launch of iRhythm Academy,” iRhythm Investor Relations, investors.irhythmtech.comThe result is that better wearables support growth, but the strongest pricing power is still likely to sit with platforms that combine efficient hardware with clinically validated AI.

Expansion of Hospital-at-Home and Decentralized Care Delivery Models

The AI in remote patient monitoring market is also moving forward because care delivery itself is shifting closer to the patient’s home. The extension of the Acute Hospital Care at Home waiver through 2030 gives U.S. health systems a longer planning horizon for inpatient-level care delivered outside traditional facilities.[3]American Medical Association, “Lawmakers Extend CMS Hospital-at-Home Waiver for Five Years,” AMA, ama-assn.orgThat matters because home-based acute care requires denser monitoring, more alerts, and faster escalation logic than basic wellness tracking. In the AI in remote patient monitoring market, this raises demand for platforms that can combine multiple vital signs into a single clinical view and identify deterioration in real time. It also helps explain why home-care settings are set to grow faster than hospitals even though hospitals still hold the larger current share. Vendors that can support hospital-level acuity in home settings are positioned to capture a larger part of new program spending.

Shift Toward Value-Based Care and Population Health Management Programs

The AI in remote patient monitoring market is increasingly being bought through an outcomes lens rather than through a feature checklist. Health systems and accountable care organizations are placing more weight on whether a platform can lower readmissions, manage risk earlier, and support broader population health goals. A nationwide hypertension program published in 2025 also showed strong engagement and statistically significant blood pressure reductions, including in rural and underserved communities. These results support the case that the AI in remote patient monitoring market can function as a population health tool rather than as a narrow specialist add-on. Platforms that are embedded in value-based contracts are likely to face less pricing pressure and hold contracts for longer periods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Algorithmic Bias and Clinical Validation Gaps Slowing FDA and EMA Approvals | -1.4% | North America and EU | Short term (≤ 2 years) |

| Cyber Security Liabilities for Multi Tenant Cloud RPM Platforms | -1.2% | Global | Medium term (2-4 years) |

| High Implementation and Integration Costs Limiting Adoption in Emerging Markets | -0.9% | MEA, South America, APAC emerging | Long term (≥ 4 years) |

| Lack of Device to EHR Interoperability Standards in Emerging Markets | -0.8% | APAC emerging, MEA, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Algorithmic Bias and Clinical-Validation Gaps Slowing FDA/EMA Approvals

The AI in remote patient monitoring market still faces a meaningful restraint from uneven validation quality across AI-enabled medical devices. A 2025 review discussed by the American Hospital Association found 60 AI-enabled devices linked to 182 recall events, with 43% of those recalls occurring within 1 year of initial clearance. That pattern matters because many AI devices still reach market with limited prospective real-world testing. A peer-reviewed 2025 study found that machine learning models could infer race or ethnicity from vital-sign values alone, which points to fairness risks that standard performance metrics may miss. Another 2025 study in npj Cardiovascular Health showed that deep learning models trained on ECG signals could surface different outcomes across racial groups even in the absence of genetic explanations. For the AI in remote patient monitoring market, this means validation now has to cover accuracy, safety, and demographic equity at the same time, which raises the cost and complexity of expansion across multiple conditions.

Cyber-Security Liabilities for Multi-Tenant Cloud RPM Platforms

The AI in remote patient monitoring market also carries a cyber risk profile that is wider than the hospital network alone. Patient devices operate in homes, connect through varied consumer networks, and feed data into shared cloud environments, which creates more points of exposure than site-based monitoring systems. Any compromise in that chain can affect alert quality, clinician trust, and procurement decisions. In the AI in remote patient monitoring market, this is especially important because altered wearable data can distort the clinical output of an AI model without causing an obvious platform outage. Buyers are therefore paying more attention to security controls, update policies, and vendor accountability during enterprise selection. Vendors that cannot show strong protections around device integrity, cloud architecture, and post-market monitoring are likely to see longer sales cycles and higher scrutiny.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Layer Captures Value as Software Commoditizes

Software platforms held 70.24% of the AI in remote patient monitoring market share in 2025, which shows how much value sits in analytics, alerting, and model orchestration rather than in sensor hardware alone. The AI in remote patient monitoring market has favored software because recurring licensing revenue is easier to scale when the core intelligence sits in the platform layer. That advantage is strongest among vendors that have built proprietary models on large labeled biosignal datasets. Their differentiation is harder to copy quickly because clinical training data take time, workflow access, and long validation cycles to assemble. Even so, the software lead does not mean the rest of the value chain is standing still.

Services are projected to grow at a 17.47% CAGR from 2026 to 2031, which places them slightly ahead of the overall AI in remote patient monitoring market. Health systems increasingly prefer managed RPM programs where the vendor supports workflow setup, patient engagement, reporting, and operating execution. That shift reduces the buyer’s internal burden and makes the purchase decision less about a software seat and more about ongoing performance delivery. The AI in remote patient monitoring industry is therefore moving toward a two-layer model where the platform remains important, but services increasingly determine retention and account growth.

By Deployment Mode: Cloud Dominates but On-Premise Holds Structural Niche

Cloud-based deployment accounted for 55.76% of the AI in remote patient monitoring market size in 2025, and it is also projected to grow at the fastest 18.37% CAGR through 2031. This is the only major segmentation line in the AI in remote patient monitoring market where the largest segment is also the fastest-growing one. The explanation is straightforward because AI retraining on streaming biosignal data requires elastic compute and storage that are hard to match economically with local installations. Cloud delivery also makes updates, analytics rollouts, and multi-site scaling easier for provider organizations. Even so, strong growth in cloud does not mean on-premise deployment loses all relevance.

On-premise deployment continues to hold a structural niche in the AI in remote patient monitoring market where data residency, sovereignty, and compliance requirements remain strict. A 2025 JMIR AI study also showed a federated deep learning setup that linked 12 hospitals across 8 nations and 4 continents without moving raw patient data across borders. That model shows how hybrid architectures can preserve local data control while still supporting broader algorithm development. Vendors that combine cloud-scale training with local inference are likely to be better positioned in regulated parts of the AI in remote patient monitoring market.

By Application: Cardiovascular Holds Share While Diabetes Metabolics Accelerates

Cardiovascular monitoring held 47.74% of the AI in remote patient monitoring market share in 2025, which keeps it as the largest application segment. The AI in remote patient monitoring market remains concentrated in cardiac use cases because arrhythmia, hypertension, and heart failure management already fit well with continuous measurement and alert-based care. This segment also benefits from a longer history of clinical evidence and reimbursement familiarity than many newer application areas.

Diabetes and metabolic disorders are projected to grow at a 17.86% CAGR from 2026 to 2031, making them the fastest-growing application in the AI in remote patient monitoring market. Continuous glucose monitoring with embedded AI support is pushing this segment forward because the clinical value now extends beyond a simple reading stream. Respiratory monitoring, oncology and specialty care, post-acute and chronic care management, and sleep and mental health monitoring also remain open growth areas in the AI in remote patient monitoring market. ResMed’s FDA-cleared Smart Comfort system adds another sign of movement, because it brings AI-based personalization into home CPAP management.

By End-User: Hospitals Lead Share but Home-Care Drives Growth Momentum

Hospitals and clinics held 50.25% share of the AI in remote patient monitoring market in 2025, which reflects their role as both major technology buyers and core clinical operators. In the AI in remote patient monitoring market, hospitals still anchor adoption because they manage step-down surveillance, post-procedure follow-up, and transition-of-care monitoring at scale. Their budgets also support the initial purchase of enterprise platforms, integrations, and analytics modules. That installed-base advantage helps hospitals maintain the largest share position in 2026. Still, the center of delivery is gradually moving outward.

Home-care settings are anticipated to expand at an 18.44% CAGR through 2031, which makes them the fastest-growing end-user segment in the AI in remote patient monitoring market. The extended hospital-at-home framework through 2030 gives providers a clearer reimbursement case for investing in home-based acute and post-acute monitoring. Ambulatory surgical centers remain smaller, but they are becoming more relevant as outpatient volumes rise and post-procedure monitoring windows gain attention. Wearables that can detect arrhythmias or oxygen desaturation in the first 24 to 72 hours after a procedure are increasingly useful in this setting. The AI in remote patient monitoring industry is therefore shifting toward a model where hospitals remain oversight hubs, while more day-to-day monitoring moves into the patient’s home.

Geography Analysis

North America accounted for 54.37% of the AI in remote patient monitoring market size in 2025, which keeps it as the largest regional contributor. The AI in remote patient monitoring market is strongest in North America because the United States already has a mature reimbursement path and a provider base that has expanded RPM programs over several years. Medicare payments for remote monitoring services exceeded USD 536 million in 2024, and nearly 1 million enrollees received RPM services during that year. The 2026 extension of Hospital-at-Home through 2030 adds further structural support for AI-enabled home monitoring in the region.

Asia-Pacific is projected to grow at a 19.62% CAGR from 2026 to 2031, making it the fastest-growing region in the AI in remote patient monitoring market. Growth in the AI in remote patient monitoring market across Asia-Pacific is being driven by demographic scale, rising chronic disease pressure, and improving digital health infrastructure. China remains important because its aging population and chronic care burden create strong demand for scalable monitoring, while tighter quality expectations are likely to favor clinically reliable devices over consumer-grade offerings. Japan, Australia, and South Korea are also supporting uptake through digital health programs, while India remains a longer-horizon opportunity as telehealth regulation and care infrastructure continue to mature.

Europe remains a large part of the AI in remote patient monitoring market, but it is structurally more complex because healthcare delivery and payment rules vary by country. Germany’s digitalization push, including mandatory electronic patient records and an official strategy to integrate digital innovation more deeply into care, is creating a clearer direction for RPM adoption. The United Kingdom, France, Italy, and Spain are building national digital health systems that create procurement openings but also raise interoperability expectations. In the AI in remote patient monitoring market, the Middle East and Africa are growing from a smaller base, led by GCC investment in digital health, while South America remains centered on private network adoption in Brazil and Argentina.

Competitive Landscape

The AI in remote patient monitoring market shows a two-tier competitive structure, with moderate concentration in the intelligent platform and managed-services layer and a more fragmented field across condition-specific devices and application-layer startups. Companies such as iRhythm Technologies, ResMed, Philips, Medtronic, and Masimo hold defensible positions because they combine brand reach with datasets, clinical evidence, and installed provider relationships. In the AI in remote patient monitoring market, iRhythm stands out for its data moat, with more than 3 billion hours of curated ECG data and continued algorithm development that supports iterative performance gains. Medtronic and Abbott also illustrate a practical partnership strategy, since the companies expanded access for systems that combine Medtronic insulin delivery with Abbott sensing technology.

White-space opportunity in the AI in remote patient monitoring market remains strongest in post-acute oncology monitoring, mental health biomarker tracking, and multi-condition monitoring for patients with 3 or more comorbidities. These areas remain less settled because no single vendor has built the same degree of dominance seen in cardiac and diabetes sub-segments. AI-native entrants are still capable of winning specific use cases when they bring deeply validated models to a high-acuity clinical problem.

In the AI in remote patient monitoring market, integration depth with EHR workflows is becoming as important as the model itself. Platforms that can place actionable output into existing clinical systems are more likely to reduce alert fatigue and gain sustained clinician use. Procurement teams are also paying closer attention to fairness, explainability, and update governance because algorithmic bias has become a visible operational risk. That favors larger incumbents with stronger regulatory and implementation teams, but it does not eliminate room for specialists in fragmented categories such as sleep monitoring and oncology specialty care. The AI in remote patient monitoring industry is therefore likely to keep rewarding companies that combine clinical evidence, interoperable design, and the ability to operate managed programs at scale.

AI In Remote Patient Monitoring Industry Leaders

Koninklijke Philips N.V.

Medtronic plc

Dexcom Inc.

Abbott Laboratories

ResMed Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Abbott secured CE Mark for Libre Duo and Libre Duo 10 Day, the world's first dual glucose-ketone sensing system that continuously measures both glucose and ketone levels every minute. The technology enables early detection of diabetic ketoacidosis risk without traditional blood or urine tests and is scheduled for European commercial launch in select markets later in 2026.

- May 2026: Bayesian Health received the first-ever FDA 510(k) clearance for a continuous AI sepsis monitoring device. The system monitors all patients continuously, surfaces deterioration risk in real time, and is positioned for New Technology Add-on Payment approval under CMS effective October 2026, a reimbursement pathway that strengthens the financial case for hospital deployment.

- March 2026: iRhythm Technologies presented new clinical data at ACC.26 across multiple patient populations and launched iRhythm Academy, a digital education platform for ambulatory cardiac monitoring. The company also announced its first active health system deployment of AI-based predictive arrhythmia identification integrated with its Zio monitoring service.

- March 2026: Anumana secured FDA 510(k) clearance for its ECG-AI algorithm for early detection of pulmonary hypertension, the first AI algorithm cleared for use with standard 12-lead ECG to detect PH. The algorithm had previously received FDA Breakthrough Device Designation and was validated across 21,066 patient records across 5 health systems.

Global AI In Remote Patient Monitoring Market Report Scope

According to the report’s scope, AI in remote patient monitoring market refers to the use of artificial intelligence technologies to analyze health data collected from connected devices, wearables, and remote monitoring systems. These solutions help healthcare providers track patient conditions in real time, detect potential health risks, generate predictive insights, and support timely interventions, improving patient outcomes and care efficiency outside traditional clinical settings.

The AI in remote patient monitoring market is segmented into component, deployment mode, application, end-user, and geography. By component, the market is segmented into software platform and services. By deployment mode, the market is segmented into cloud-based and on-premise. By application, the market is segmented into cardiovascular monitoring, diabetes and metabolic disorders, respiratory monitoring, oncology and specialty care, post-acute and chronic care management, sleep and mental health monitoring, and other applications. By end-user, the market is segmented into hospitals and clinics, home-care settings, and ambulatory surgical centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software Platform |

| Services |

| Cloud-Based |

| On-Premise |

| Cardiovascular Monitoring |

| Diabetes and Metabolic Disorders |

| Respiratory Monitoring |

| Oncology and Specialty Care |

| Post-Acute and Chronic Care Management |

| Sleep and Mental Health Monitoring |

| Other Applications |

| Hospitals and Clinics |

| Home-Care Settings |

| Ambulatory Surgical centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software Platform | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| By Application | Cardiovascular Monitoring | |

| Diabetes and Metabolic Disorders | ||

| Respiratory Monitoring | ||

| Oncology and Specialty Care | ||

| Post-Acute and Chronic Care Management | ||

| Sleep and Mental Health Monitoring | ||

| Other Applications | ||

| By End-User | Hospitals and Clinics | |

| Home-Care Settings | ||

| Ambulatory Surgical centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in AI in remote patient monitoring through 2031?

Growth is being supported by the rise in chronic disease, outcome-based reimbursement, and the shift of monitoring closer to the home. The sector is projected to rise from USD 2.44 billion in 2026 to USD 5.20 billion by 2031 at a 16.38% CAGR.

Which component generates the most revenue today?

Software platforms lead with 70.24% share in 2025 because clinical analytics, alerting, and AI model deployment capture more value than device hardware alone.

Why is cardiovascular monitoring still the leading application?

Cardiovascular monitoring held 47.74% share in 2025 because it has a large patient base, established reimbursement support, and strong clinical evidence for continuous monitoring.

Which region offers the strongest near-term expansion potential?

Asia-Pacific has the fastest projected regional growth at a 19.62% CAGR through 2031, supported by demographic scale and continued buildout of digital health systems.

Page last updated on: