AI In Healthcare Data Orchestration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.61 Billion |

| Market Size (2031) | USD 5.01 Billion |

| Growth Rate (2026 - 2031) | 25.44% CAGR |

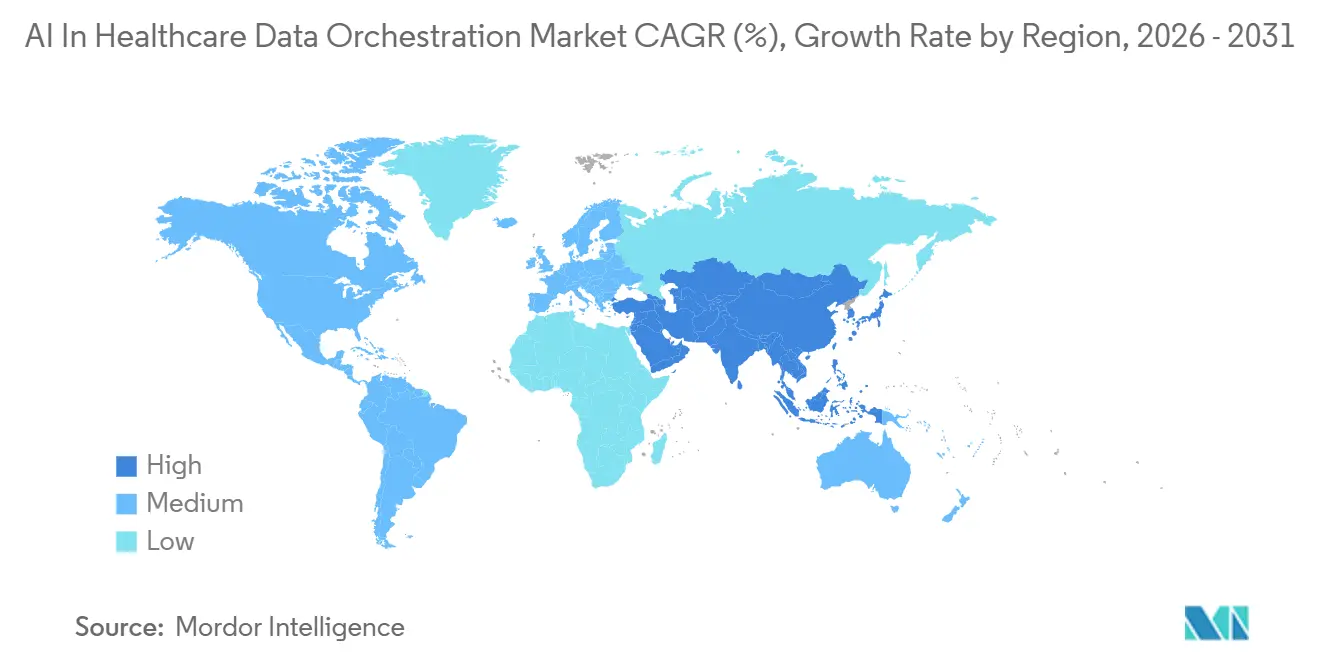

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

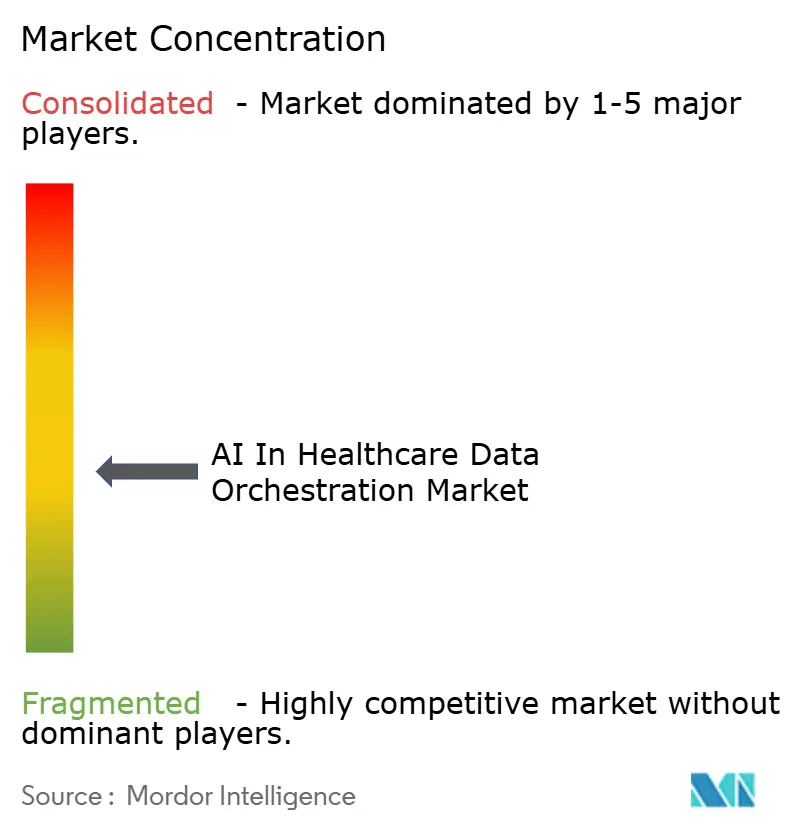

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Healthcare Data Orchestration Market Analysis by Mordor Intelligence

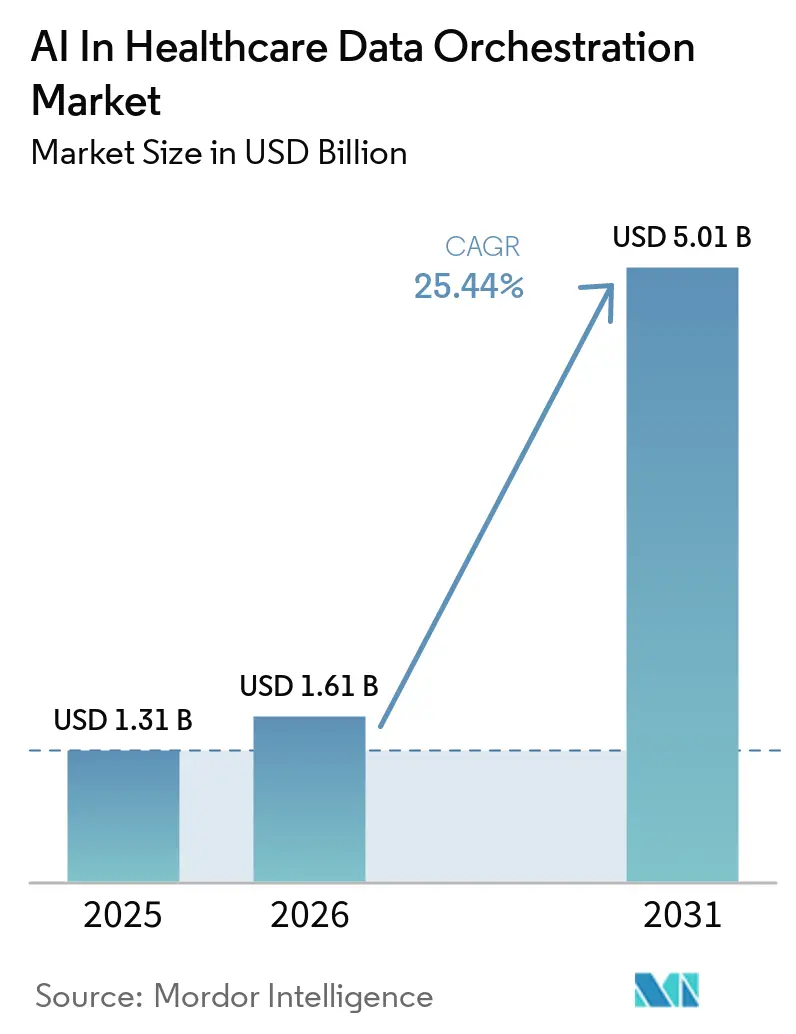

The AI In Healthcare Data Orchestration Market size is expected to increase from USD 1.31 billion in 2025 to USD 1.61 billion in 2026 and reach USD 5.01 billion by 2031, growing at a CAGR of 25.44% over 2026-2031.

Growth is being shaped by a tighter compliance cycle, especially in the United States, where payer organizations now face faster prior authorization response windows and a fixed path to FHIR-based API readiness under CMS-0057-F. That pressure is pushing healthcare organizations to invest beyond basic connectivity and into orchestration layers that can route workflows, standardize data elements, and support explainable operational decisions across payer, provider, and life sciences settings. The policy burden is also widening because TEFCA Common Agreement requirements and purpose-based exchange rules make production routing more complex once data begins moving across national-scale exchange networks. Europe is moving in the same direction through EHDS and national FHIR transition programs, which extend the addressable need for governed orchestration over a multi-year build cycle. Competition is therefore shifting toward vendors that can combine cloud scale, healthcare-specific integration logic, and policy-aware data handling in one operating layer.

Key Report Takeaways

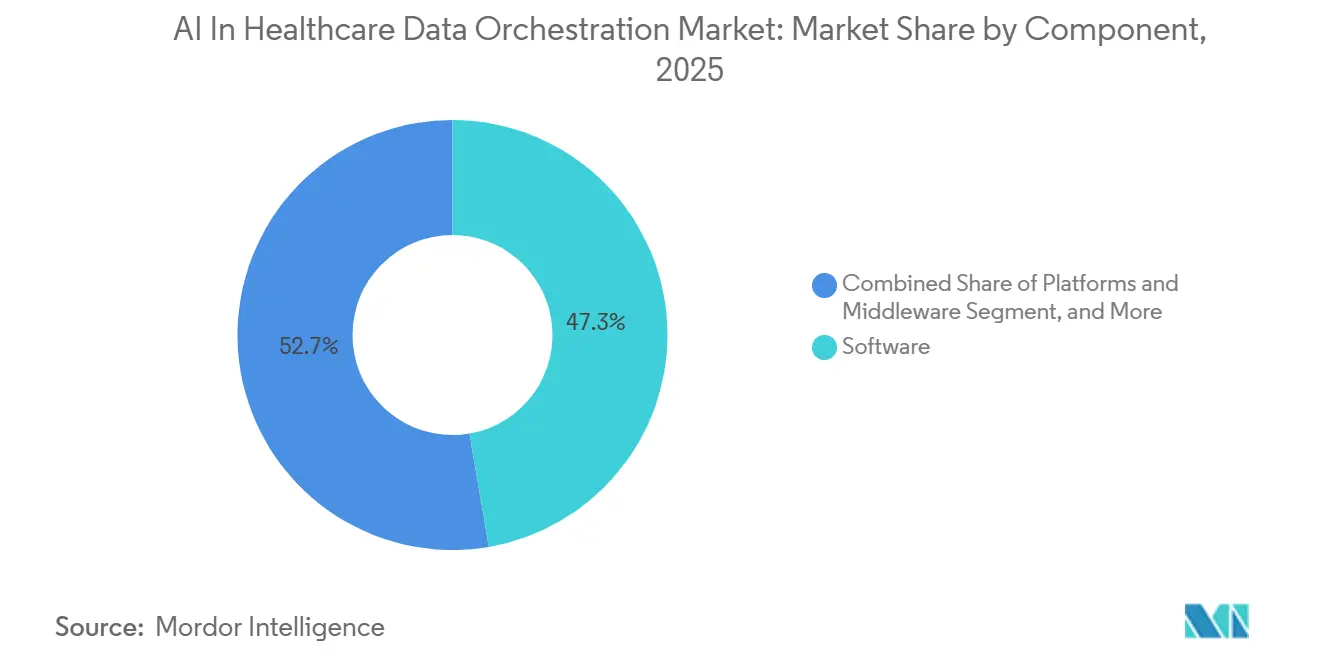

- By component, software held 47.32% of AI in healthcare data orchestration market share in 2025, while platforms and middleware are projected to expand at 26.24% CAGR through 2031.

- By application, data ingestion and normalization accounted for 45.73% of the market in 2025, while clinical document understanding is forecast to grow at 25.94% CAGR through 2031.

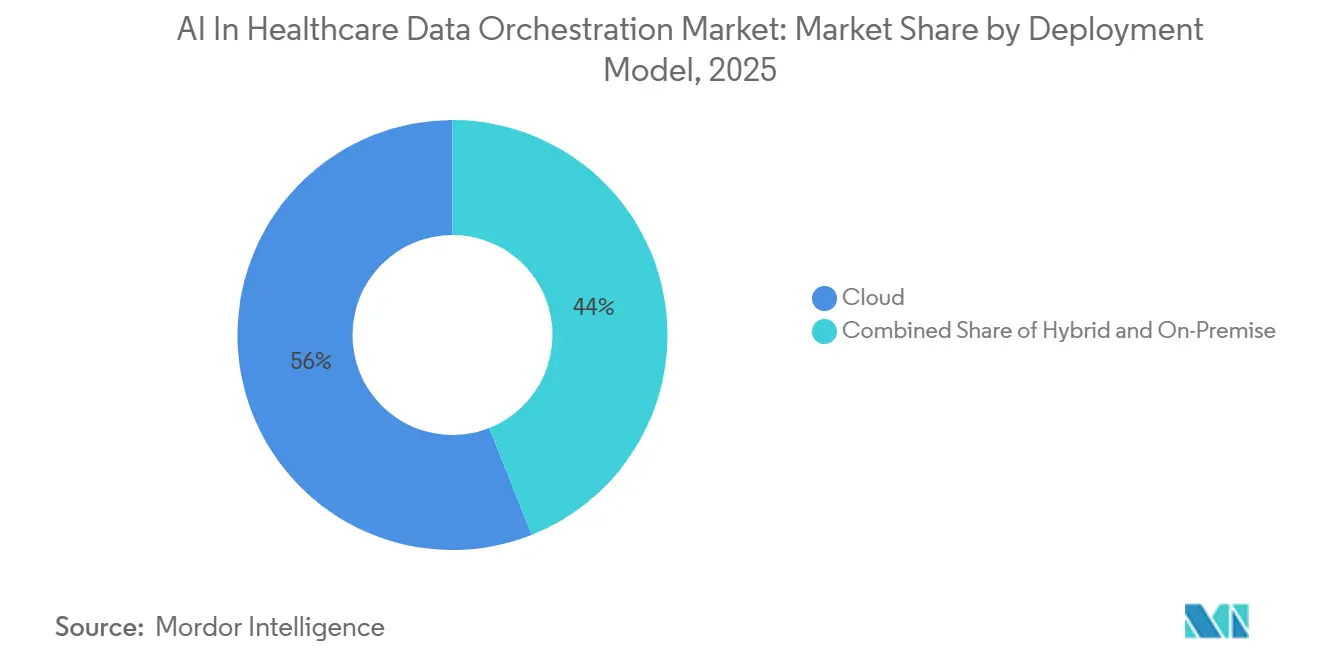

- By deployment model, cloud represented 56.01% of AI in healthcare data orchestration market size in 2025 and is also the fastest-growing model at 27.62% CAGR through 2031.

- By end user, healthcare providers led with 41.38% share in 2025, while healthcare payers are set to advance at 30.74% CAGR through 2031.

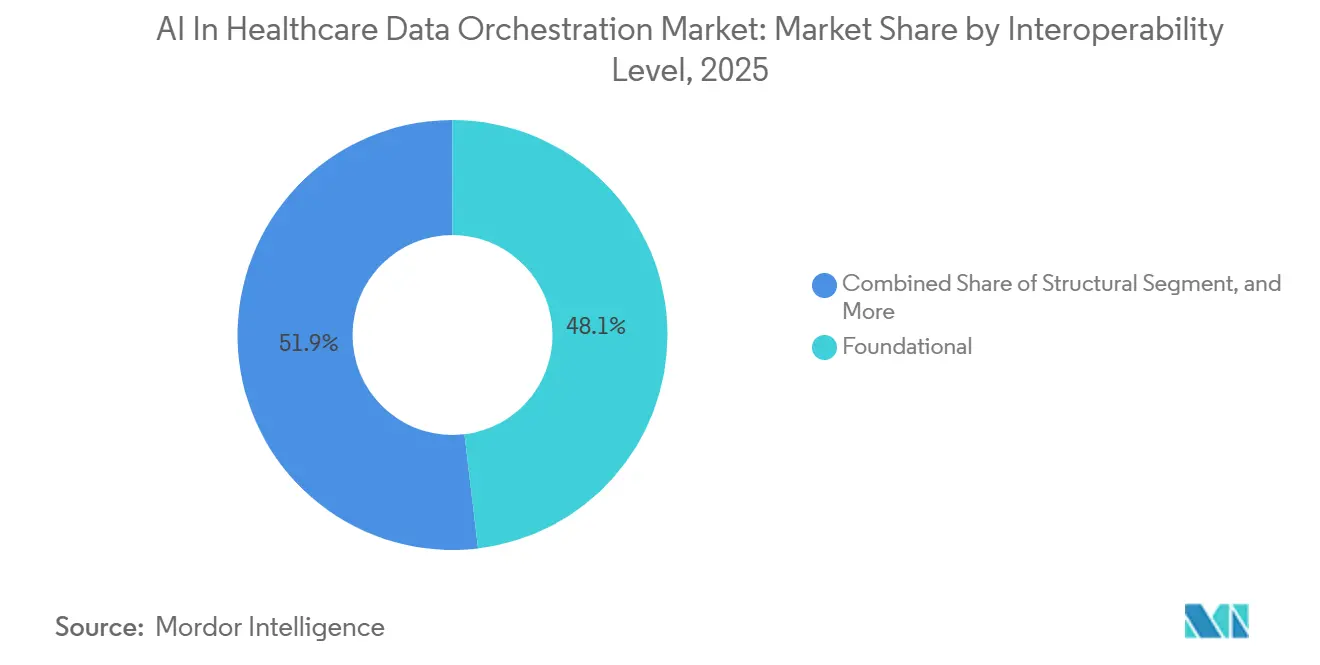

- By interoperability level, foundational interoperability held 48.13% share in 2025, while structural interoperability is projected to rise at 27.05% CAGR through 2031.

- By geography, North America captured 47.33% share in 2025, while Asia-Pacific is expected to register the fastest regional CAGR at 28.15% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Healthcare Data Orchestration Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FHIR API And Prior Authorization Mandates | +5.5% | North America, with spillover to Canada and Europe | Short term (≤ 2 years) |

| QHIN And HIE Expansion | +3.8% | North America, with early parallels in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Multimodal Data Growth And Longitudinal Unification | +3.5% | Global, with strong demand in Asia-Pacific and European research settings | Medium term (2-4 years) |

| Cloud-Native Health Data Platforms | +4.2% | Global, with North America and Asia-Pacific leading adoption | Short term (≤ 2 years) to Medium term (2-4 years) |

| USCDI And FHIR Version Migration Pressure | +2.6% | North America first, then Europe through alignment needs | Medium term (2-4 years) |

| AI Governance And Lineage Requirements | +2.8% | Global, with higher urgency in Europe and North America | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FHIR API and Prior-Authorization Mandates Accelerate Orchestration

The AI in healthcare data orchestration market is being pushed forward first by regulation rather than discretionary technology spending. CMS-0057-F required impacted payers to move faster on prior authorization decisions beginning January 1, 2026, and it set January 1, 2027, as the compliance point for Prior Authorization, Provider Access, and Payer-to-Payer FHIR APIs.[1]Centers for Medicare & Medicaid Services, “CMS Interoperability and Prior Authorization Final Rule CMS-0057-F,” CMS, cms.gov That requirement raises the value of orchestration because organizations must handle intake, routing, normalization, and response generation in one connected flow rather than through separate manual teams. The 2026 proposed rule for prior authorization standards for drugs expands that compliance surface and keeps the implementation agenda active beyond the first wave of payer changes. In the AI in healthcare data orchestration market, this turns middleware and workflow logic into a core operating requirement rather than a supporting integration feature. It also favors vendors that can bridge administrative data, clinical records, and standards-based exchange without forcing payers to rebuild older systems from scratch.

QHIN and HIE Expansion Increases Policy-Aware Routing Demand

The AI in healthcare data orchestration market is also benefiting from wider trusted exchange infrastructure in the United States. TEFCA Common Agreement v2.1 formalized permitted exchange purposes and made routing logic more policy sensitive because organizations must distinguish why data is being exchanged, not only where it should go.[2]Health and Human Services Department, “Notice of Publication of Common Agreement for Nationwide Health Information Interoperability (Common Agreement) Version 2.1,” Federal Register, federalregister.gov As national exchange becomes more operational, health systems still need internal orchestration to normalize patient identity, manage workflow triggers, and connect downstream analytics or AI tools to incoming records. Oracle Health’s push into aligned network status reflects how enterprise vendors now treat interoperability network participation as a strategic product layer rather than a separate service add-on. In the AI in healthcare data orchestration market, that creates sustained demand for policy-aware routing that sits between exchange endpoints and internal care, payment, and risk workflows. It also increases the importance of auditability because every exchange pathway must be understandable to compliance teams and operating teams at the same time.

Multimodal Data Growth Requires Longitudinal Data Unification

The AI in healthcare data orchestration market is expanding because healthcare data now arrives in many forms that do not move or align in the same way. Clinical notes, claims, genomic information, imaging files, and personal health records each carry different timing, structure, and governance needs, which makes a unified patient view difficult without a formal orchestration layer. The Fujitsu Japan and JMDC collaboration shows how organizations are now trying to connect anonymized DPC data, insurer data covering 20 million lives, and Pep Up PHR data from more than 7.7 million users into one longitudinal operating frame. That kind of integration supports care pathways that span prevention, diagnosis, treatment, and follow-up instead of staying inside a single care episode. In the AI in healthcare data orchestration market, the direct opportunity lies in systems that can keep these sources linked, governed, and usable for AI applications without constant remapping. The same trend also raises demand for lineage controls because organizations need to understand how each data element moved before they can trust automated decisions built on top of it.

Cloud-Native Health Data Platforms Embed AI-Ready Normalization

The AI in healthcare data orchestration market is also gaining from the way cloud-based health data platforms now bundle interoperability, governance, and AI services more tightly. Oracle’s recent product launches show how vendors are combining longitudinal health records, generative AI, and operational data handling inside one platform environment for healthcare and life sciences users.[3]Oracle, “Oracle Health Demonstrates Interoperability Leadership, Achieves CMS Aligned Network Status,” Oracle, oracle.com Epic reported more than 10 billion monthly FHIR API calls in March 2025, which points to a much larger flow of standards-based transactions feeding these orchestration layers. As transaction volume rises, buyers increasingly want normalization, access control, and orchestration tools that live close to the data platform rather than in separate point products. In the AI in healthcare data orchestration market, this supports cloud-native deployment because platforms can deliver updates, scaling, and integration logic faster than many on-site alternatives. It also changes competition because platform providers can move upward into workflow automation while pure integration vendors move downward into managed infrastructure services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PHI Privacy, Cybersecurity, And Cross-Border Controls | -3.2% | Global, with higher intensity in Europe and North America | Medium term (2-4 years) |

| Legacy Heterogeneity And Integration Complexity | -2.6% | Global, especially in provider environments with older infrastructure | Long term (≥ 4 years) |

| Consent Fragmentation In Purpose-Based Routing | -1.8% | North America, Europe, and selected Asia-Pacific markets | Medium term (2-4 years) |

| QHIN Onboarding, Patient Matching, And Directory Sync Overhead | -1.4% | North America first, with spillover to similar exchange models elsewhere | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PHI Privacy, Cybersecurity, and Cross-Border Controls

The AI in healthcare data orchestration market faces a clear restraint from privacy and governance obligations that become harder once data starts moving across organizational and national boundaries. TEFCA Common Agreement rules define multiple permitted exchange purposes, which means routing logic must reflect policy intent as well as technical connectivity. In Europe, EHDS adds another layer because cross-border exchange of priority health data categories will roll in under a structured regulatory timetable that places strict expectations on data handling and secondary use. France’s 2026 digital health doctrine also reinforces that national interoperability architecture is moving toward controlled FHIR-based exchange rather than open-ended data movement. In the AI in healthcare data orchestration market, this slows deployment when buyers need country-specific controls, purpose-based permissions, and traceable governance before scaling any AI workflow. It also raises the cost of expansion for vendors that built generic healthcare connectors but did not build healthcare-grade policy enforcement into the core platform.

Legacy Heterogeneity and Integration Complexity

The AI in healthcare data orchestration market is also constrained by the installed base of older healthcare interfaces and uneven standards adoption. Many operational environments still rely on mixed formats across HL7 v2, X12, documents, and newer FHIR APIs, which creates constant translation work before AI systems can use the data effectively. Rhapsody’s Axon launch, which spans FHIR, HL7 v2, X12, and API-based integrations, reflects how buyers still need tools that support several standards at once rather than a clean migration to one format. InterSystems made a similar point with its Epic Showroom payer connector, which packages governed logic around ADT notifications, claims data, and clinical summaries because those workflows remain heterogeneous in real deployments. In the AI in healthcare data orchestration market, legacy variation slows project timelines, widens implementation scope, and makes performance harder to standardize across customer environments. The result is that many buyers still spend heavily on integration readiness before they can capture the value promised by AI-enabled orchestration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Middleware Infrastructure Gains Strategic Weight

Software held 47.32% of the market in 2025, which kept it as the largest component in the AI in healthcare data orchestration market. That position reflects years of spending on analytics tools, activation layers, and application software that sat close to the EHR or payer core. The faster change is in platforms and middleware, which is projected to grow at 26.24% CAGR through 2031 as buyers move from isolated use cases to governed cross-system execution. This shift is happening because organizations now need one layer that can manage routing, schema enforcement, consent handling, and downstream AI actions together. In practical terms, the AI in healthcare data orchestration market is rewarding component vendors that can support policy-aware interoperability instead of simple message transfer.

That change is visible in product strategy across the vendor base. Redox positioned its interoperability layer as a long-term partner model in January 2026 and highlighted automation for configuration and complex transaction troubleshooting across a broad connected network. Rhapsody and InterSystems also moved deeper into operational orchestration rather than staying at the interface level, which shows that the AI in healthcare data orchestration market is pulling middleware closer to day-to-day workflow execution. Services still matter because many deployments require advisory, implementation, and managed support. Even so, services are increasingly tied to platform rollouts instead of stand-alone integration projects. This is why the AI in healthcare data orchestration industry is moving toward recurring infrastructure relationships rather than one-time project billing.

By Application: Clinical Intelligence Extends Beyond Data Movement

Data ingestion and normalization accounted for 45.73% of the market in 2025, making it the largest application area in the AI in healthcare data orchestration market. That lead makes sense because most organizations still need structured pipelines before they can do anything more advanced. Clinical document understanding is growing fastest at 25.94% CAGR through 2031, which shows where value is moving once foundational pipelines are in place. Healthcare organizations are learning that the most useful operational detail often sits inside notes, referrals, summaries, and other narrative records. As a result, the AI in healthcare data orchestration market is shifting from pure transport toward systems that can interpret and act on mixed clinical content.

The change is also visible in adjacent workflow integration. GRAIL’s Epic integration brings multi-cancer early detection data into a mainstream EHR workflow, and Labcorp expanded diagnostic integration through Epic Aura across hundreds of health systems, which shows that orchestration demand now includes more specialized data categories that must fit normal care processes. Patient record unification and workflow automation remain important because prior authorization and care coordination cannot scale well without a consolidated context. Research and real-world evidence activation are also becoming more material as organizations try to connect clinical operations with evidence generation. Within the AI in healthcare data orchestration industry, this broadens the application map from back-end data preparation to front-line clinical and administrative execution. It also explains why application growth is strongest where interpretation, timing, and action need to happen together.

By Deployment Model: Cloud Leads on Both Scale and Growth

Cloud held 56.01% of AI in healthcare data orchestration market size in 2025, and it is projected to grow at 27.62% CAGR through 2031. It is unusual for one deployment model to lead on both current scale and forecast growth, but that pattern fits this market because orchestration increasingly depends on elastic compute, managed interoperability services, and faster update cycles. The cloud model is no longer only a hosting decision in the AI in healthcare data orchestration market. It has become the preferred operating base for FHIR transactions, workflow logic, monitoring, and AI inference. That makes cloud especially attractive for organizations that want faster rollout without building every orchestration capability internally.

Official product activity supports that direction. Oracle launched a new AI-driven EHR on Oracle Cloud Infrastructure in 2025 and followed it with a life sciences data platform expansion in 2026, which reinforced cloud as a live execution environment rather than a passive storage layer. At the same time, hybrid and on-premise demand stays relevant in the AI in healthcare data orchestration market, where data residency, institutional policy, or operational sensitivity limits full migration. EHDS and national implementation rules in Europe support that continued role for controlled deployment models. Many buyers, therefore, adopt cloud first for scale while keeping selective workloads in local environments. The result is not a simple replacement of older models, but a clearer hierarchy in which the cloud becomes the center and hybrid models absorb the exceptions.

By End User: Payers Move From Optional Modernization to Required Execution

Healthcare providers held 41.38% share in 2025, which made them the largest end-user group in the AI in healthcare data orchestration market. Providers moved first because EHR-centered data flows created an early need for integration, analytics, and care coordination. Healthcare payers are forecast to grow fastest at 30.74% CAGR through 2031 because the compliance cycle around prior authorization and data access is now much harder to delay. CMS rules make payer investment a baseline operating requirement, especially where decisions must move faster and be more transparent. In the AI in healthcare data orchestration market, this change in demand is from selective digital improvement to regulated process execution.

Vendor activity also shows that this end-user mix is widening. InterSystems introduced a payer connector tied directly to Epic workflows, and Oracle Health strengthened its position around aligned network status and patient identity integration, both of which support payer-provider data exchange at operating scale. Government and public health agencies continue to matter because national exchange and program management require reliable orchestration. Life sciences organizations are also becoming more visible users as they try to connect research, clinical, and post-market evidence flows within one environment. The AI in healthcare data orchestration industry, therefore, serves a wider set of buyers than traditional interoperability markets did. That breadth supports growth, but it also forces vendors to package the same core orchestration engine for very different regulatory and operational settings.

By Interoperability Level: Structural Readiness Becomes the Main Upgrade Path

Foundational interoperability held 48.13% share in 2025, which shows that the largest installed base in the AI in healthcare data orchestration market still operates at basic connectivity. Structural interoperability is forecast to rise fastest at 27.05% CAGR through 2031 because compliance and AI execution both depend on cleaner data models. Once organizations move from transport to orchestration, they need resource profiles, schema consistency, and enforceable mappings across systems. That is why the AI in healthcare data orchestration market is now pushing buyers toward structural readiness as the main upgrade path. It is also why terminology and profile validation tools are becoming more important than simple interface counts.

Policy direction reinforces that shift. ONC’s HTI-2 proposed rule included HL7 FHIR Bulk Data Access v2.0.0 and FHIR Subscriptions, which support more real-time and standards-based orchestration patterns. NCQA’s USCDI guidance also shows how the data model continues to widen with newer social, behavioral, and demographic elements that require stronger semantic control. Organizational interoperability remains important because trust, governance, and purpose-based exchange still determine whether data can move. Even so, the most immediate spend in the AI in healthcare data orchestration market is moving into the structural layer, where transport becomes usable at scale. This is the part of the market that most clearly links regulatory compliance, application growth, and vendor differentiation.

Geography Analysis

North America accounted for 47.33% of AI in healthcare data orchestration market share in 2025, making it the leading regional cluster. The United States drives this position because regulatory mandates, payer modernization, and mature EHR usage all support earlier spending on orchestration. CMS-0057-F keeps the region in front by linking faster prior authorization handling with a defined FHIR API timeline. TEFCA Common Agreement rules add another layer of demand because national exchange requires more explicit routing, governance, and purpose handling in production systems. In the AI in healthcare data orchestration market, that combination makes North America the most regulation-driven revenue center.

Europe is not the largest region, but it has a long build cycle that supports steady demand in the AI in healthcare data orchestration market. EHDS entered into force on March 26, 2025, and it creates a staged path toward cross-border exchange of priority health data categories starting in 2029. France reinforced that direction in 2026 by requiring CI-SIS components to move to FHIR-based architecture under its updated digital health doctrine. Europe, therefore, combines strong interoperability pressure with tighter governance expectations, which keep hybrid deployment and traceability more relevant than in some other regions.

Asia-Pacific is the fastest-growing region at 28.15% CAGR through 2031, which gives it the strongest expansion profile in the AI in healthcare data orchestration market. Japan stands out because healthcare organizations are already linking insurer, provider, and personal health record data, as shown by the Fujitsu Japan and JMDC collaboration launched in early 2026. Official activity in Japan also shows growing interest in AI-enabled clinical workflow support, including medical interview and nursing voice input systems at the Osaka International Cancer Center. The Middle East and Africa remain smaller, but the GCC is generating visible demand, with Saudi Arabia’s private hospital sector adopting unified clinical and business platforms such as Oracle Health Foundation EHR. South America is still earlier in the adoption curve, yet national digital health efforts and private hospital investment are beginning to support broader FHIR-based connectivity. This leaves the AI in healthcare data orchestration market with a clear pattern where North America leads on current scale, Europe builds through regulation, and Asia-Pacific accelerates fastest through infrastructure expansion.

Competitive Landscape

The AI in healthcare data orchestration market remains fragmented, with competition spread across cloud platforms, interoperability specialists, EHR ecosystem players, and health data activation vendors. No single vendor controls the market across all components, applications, deployment, and interoperability layers. Instead, buyers select platforms based on how well vendors combine compliance readiness, data movement, workflow logic, and AI execution in one operating model. In the AI in healthcare data orchestration market, this creates a tiered structure where hyperscalers provide scale, middleware vendors provide healthcare-specific control, and EHR-adjacent platforms provide workflow access. That structure also keeps competitive pressure high because most large contracts now require more than one capability set.

Strategic moves in 2025 and 2026 show how vendors are trying to widen their role. Oracle pushed deeper into the AI in healthcare data orchestration market by achieving CMS Aligned Network status, extending identity-enabled interoperability workflows, and expanding its life sciences AI data platform. InterSystems launched Payer Connector on the Epic Showroom, which tied governed payer-provider data exchange more closely to the Epic procurement path. Rhapsody launched Axon and expanded its AWS Marketplace presence, which shows a deliberate move toward AI-enabled operational interoperability and broader cloud distribution. Epic’s expanding FHIR transaction volume and broad app ecosystem also reinforce how important EHR-linked distribution remains in this market.

The white space in the AI in healthcare data orchestration market sits between foundational connectivity and fully governed structural interoperability. Vendors that can simplify USCDI migration, profile enforcement, purpose-based routing, and workflow observability are likely to capture this next layer of spending. In the AI in healthcare data orchestration market, pure point solutions face a harder path because buyers now want measurable execution across several use cases instead of separate tools for each step. Partnerships also matter more because no vendor can easily cover every data source, clinical workflow, and governance requirement alone. That is why competition is becoming less about raw interface volume and more about who can make healthcare data usable, compliant, and operational at scale.

AI In Healthcare Data Orchestration Industry Leaders

InterSystems Corporation

Microsoft Corporation

Oracle Corporation

Veradigm LLC

Rhapsody Health Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Oracle Health demonstrated interoperability leadership by becoming a CMS Aligned Network and integrating CLEAR's secure identity platform to eliminate check-in paperwork through QR-code-based health record sharing. Oracle Health Information Network had achieved QHIN status in November 2025, giving Oracle one of the most comprehensive interoperability infrastructure positions in the market.

- April 2026: GRAIL announced integration of its Galleri multi-cancer early detection test into Epic via Aura, targeting approximately 450 health systems with broad availability expected by end of 2026. This integration enables clinicians to order the test and manage patient follow-up within existing Epic workflows, demonstrating how genomic data orchestration is entering mainstream EHR pipelines.

- March 2026: Rhapsody announced general availability of Rhapsody Axon, an AI agent embedded in the Rhapsody and Corepoint platforms to automate interoperability workflows across FHIR, HL7 v2, X12, and API-based integrations. Axon was validated with 50+ early adopters and targets the estimated 20+ hours per week that healthcare IT teams spend troubleshooting integration issues.

- February 2026: InterSystems introduced its Payer Connector, a governed integration engine with prebuilt Epic-aware schemas, to the Epic Showroom in February 2026, enabling health plans to route ADT notifications, retrieve CCD and analytics summaries, and push claims data into Epic Payer Platform across care management, utilization management, and quality programs.

Global AI In Healthcare Data Orchestration Market Report Scope

The AI in healthcare data orchestration market refers to the ecosystem of software, platforms, and services that coordinate diverse medical data sources (like EHRs and wearables) and integrate them seamlessly with multiple AI models and automated workflows. It transforms fragmented health data into actionable, automated, and continuous patient care.

The AI in Healthcare Data Orchestration Market Report is Segmented by Component (Software, Platforms and Middleware, Services), Application (Data Ingestion and Normalization, Clinical Document Understanding, Patient Record Unification, Workflow Automation and Prior Authorization, Population Health and Care Management, Research and Real-World Evidence Activation), Deployment Model (Cloud, Hybrid, On-Premise), End User (Healthcare Providers, Healthcare Payers, Government and Public Health Agencies, Life Sciences Organizations, Health Information Exchanges and Digital Health Networks), Interoperability Level (Foundational, Structural, Semantic, Organizational), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Platforms and Middleware |

| Services |

| Data Ingestion and Normalization |

| Clinical Document Understanding |

| Patient Record Unification |

| Workflow Automation and Prior Authorization |

| Population Health and Care Management |

| Research and Real-World Evidence Activation |

| Cloud |

| Hybrid |

| On-Premise |

| Healthcare Providers |

| Healthcare Payers |

| Government and Public Health Agencies |

| Life Sciences Organizations |

| Health Information Exchanges and Digital Health Networks |

| Foundational |

| Structural |

| Semantic |

| Organizational |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Platforms and Middleware | ||

| Services | ||

| By Application | Data Ingestion and Normalization | |

| Clinical Document Understanding | ||

| Patient Record Unification | ||

| Workflow Automation and Prior Authorization | ||

| Population Health and Care Management | ||

| Research and Real-World Evidence Activation | ||

| By Deployment Model | Cloud | |

| Hybrid | ||

| On-Premise | ||

| By End User | Healthcare Providers | |

| Healthcare Payers | ||

| Government and Public Health Agencies | ||

| Life Sciences Organizations | ||

| Health Information Exchanges and Digital Health Networks | ||

| By Interoperability Level | Foundational | |

| Structural | ||

| Semantic | ||

| Organizational | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in AI in healthcare data orchestration?

Growth is being driven by regulatory deadlines, especially CMS prior authorization and FHIR API requirements, along with the need to unify clinical, administrative, and longitudinal data across complex healthcare systems.

How large is the AI in healthcare data orchestration space expected to become by 2031?

The AI in healthcare data orchestration market is forecast to reach USD 5.01 billion by 2031, rising from USD 1.61 billion in 2026 at a 25.4% CAGR over 2026-2031.

Which region leads current demand for AI in healthcare data orchestration solutions?

North America led in 2025 with 47.33% share because of strong regulatory pressure, mature EHR infrastructure, and broader adoption of standards-based exchange.

Which region is expanding fastest through the forecast period?

Asia-Pacific is the fastest-growing region, with a projected 28.15% CAGR through 2031, supported by national digital health programs and growing demand for AI-ready data unification.

Page last updated on: