AI In CRO Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.55 Billion |

| Market Size (2031) | USD 18.45 Billion |

| Growth Rate (2026 - 2031) | 18.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In CRO Services Market Analysis by Mordor Intelligence

The AI In CRO Services Market size is projected to expand from USD 12.29 billion in 2025 and USD 14.55 billion in 2026 to USD 18.45 billion by 2031, registering a CAGR of 18.45% between 2026 to 2031.

Pharmaceutical and biotech companies are increasingly requiring their CRO partners to not only deliver trials but also provide data-driven decision support throughout the development stages. Between 2020 and 2024, study start-up timelines significantly lengthened, driving sponsors to adopt tools that address delays in planning, recruitment, execution, and documentation. Proven AI applications in trial execution have demonstrated reduced cycle times and improved operational control, strengthening the case for adoption. Additionally, the FDA's draft guidance in January 2025 has established a more structured compliance pathway for the AI in CRO market, even as final standards continue to evolve. As competition shifts from basic outsourcing capabilities, the AI in CRO market is increasingly shaped by platform sophistication, data quality, and the ability to seamlessly integrate AI into regulated workflows.

Key Report Takeaways

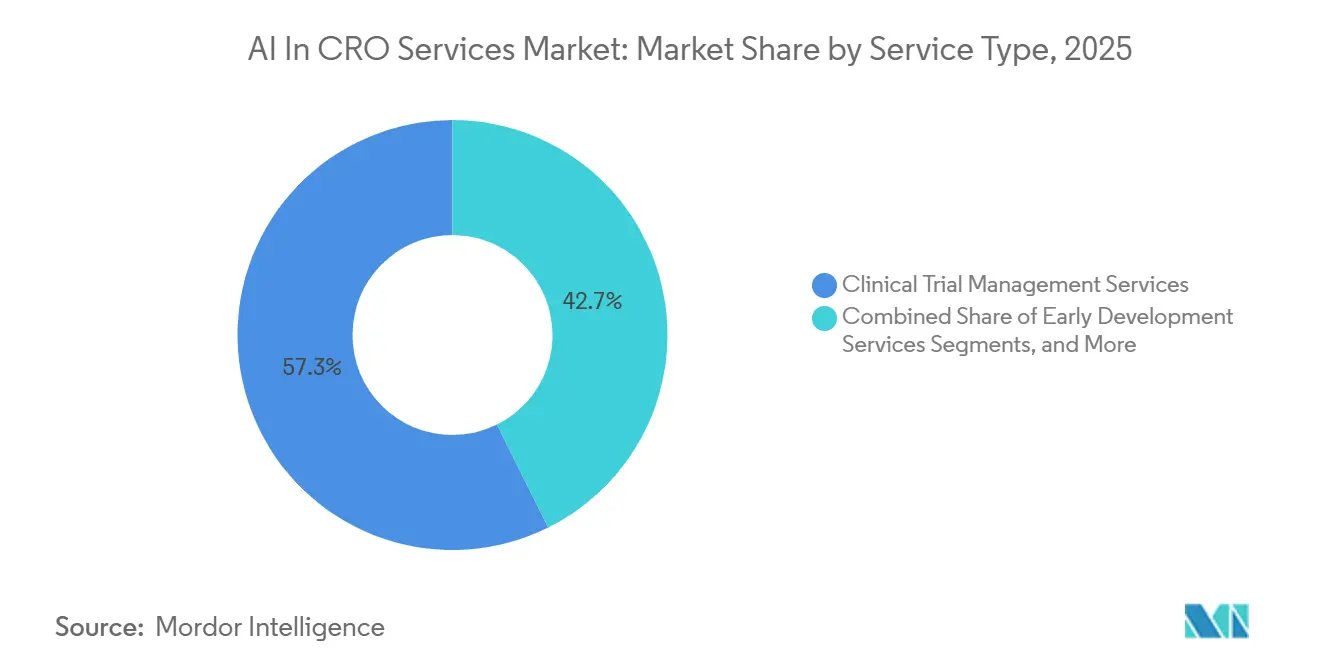

- By service type, clinical trial management services held 57.34% share in 2025, while early development & translational services are projected to grow at 19.20% CAGR through 2031.

- By AI technology, machine learning accounted for 42.45% share in 2025, while natural language processing is expected to expand at 20.35% CAGR through 2031.

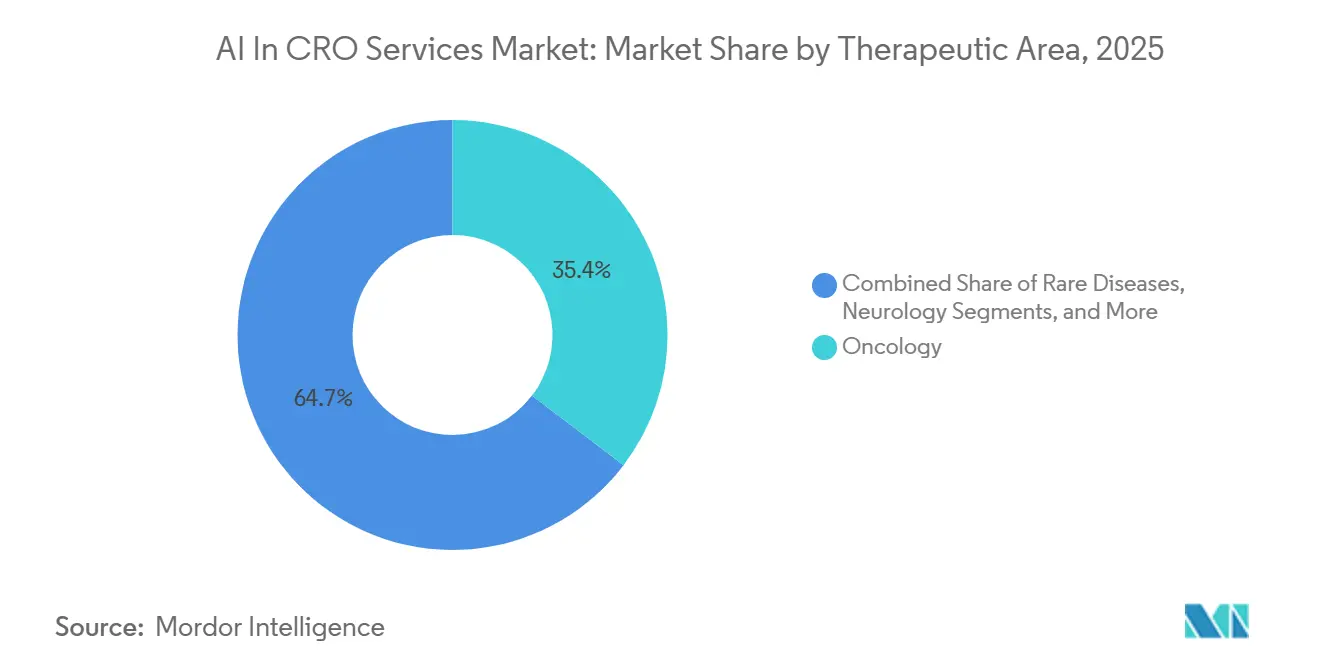

- By therapeutic area, oncology represented 35.35% share in 2025, while infectious diseases & vaccines are expected to record 19.6% CAGR through 2031.

- By trial phase, Phase III captured 45.60% share in 2025, while Phase I is projected to advance at 19.98% CAGR through 2031.

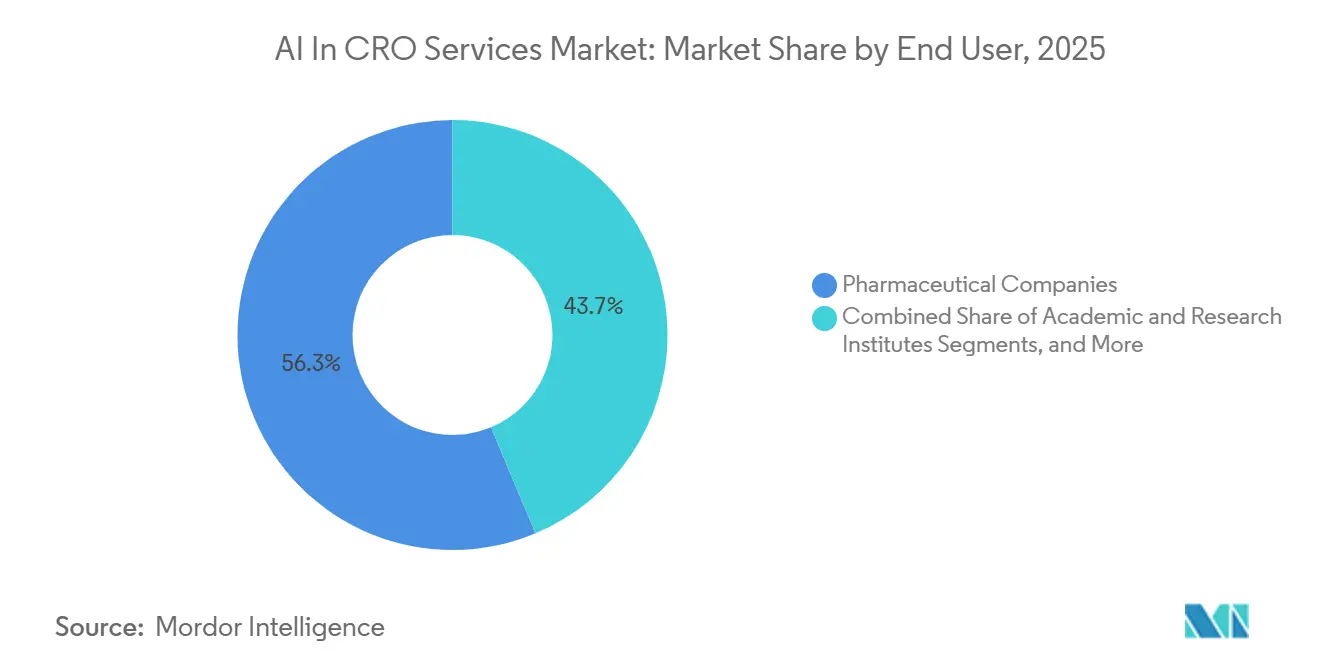

- By end user, pharmaceutical companies held 56.3% share in 2025, while academic & research institutes are expected to grow at 20.45% CAGR through 2031.

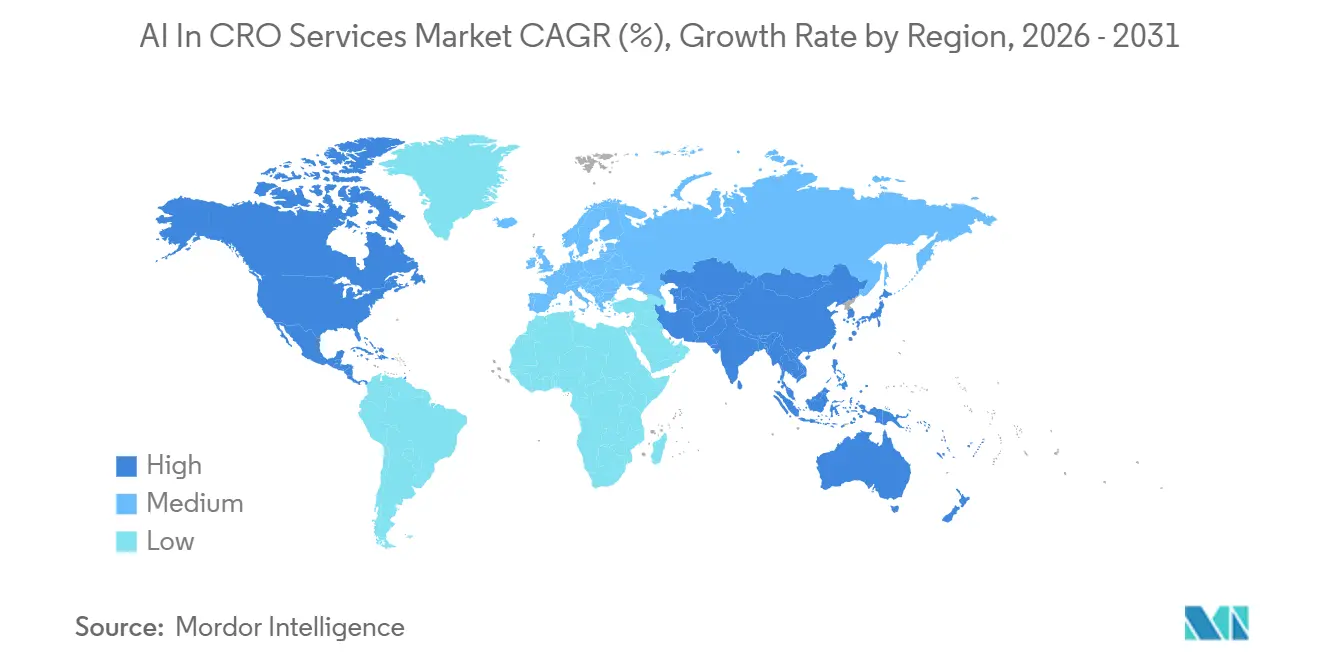

- By geography, North America accounted for 44.05% share in 2025, while Asia-Pacific is forecasted to grow at 23.00% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In CRO Services Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising late-stage trial complexity and data intensity | +3.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Biotech outsourcing demand for flexible clinical capacity | +3.0% | North America, Europe, and core Asia-Pacific markets | Medium term (2-4 years) |

| Decentralized and hybrid trial expansion | +2.7% | Global, with early gains in North America, Australia, and Western Europe | Short term (≤ 2 years) |

| Precision medicine and biomarker-driven recruitment | +2.9% | North America, Western Europe, South Korea, and Japan | Medium term (2-4 years) |

| Genai compression of study start-up and medical writing cycles | +3.4% | Global, with early-mover advantages in North America and the United Kingdom | Short term (≤ 2 years) |

| RWE-linked synthetic control and feasibility models | +2.4% | North America, Europe, and Japan, with spillover into Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Late-Stage Trial Complexity and Data Intensity

Traditional CRO operating models are increasingly inadequate in managing the growing data volumes from late-stage programs. This issue is particularly significant in Phase III studies within the AI in CRO services market, where adaptive endpoints, wearable signals, biomarker data, and real-world inputs are integrated into a single program. Centralized data flow approaches have demonstrated the ability to automate data ingestion, reduce programming cycle times, and enhance efficiency in data issue management. These advancements highlight why sponsors now consider AI capabilities a core criterion when awarding major programs. As a result, CTMS and data platforms in the AI in CRO services market have transitioned from supporting tools to essential commercial assets.

Biotech Outsourcing Demand for Flexible Clinical Capacity

Biotech companies, often operating with lean internal teams, increasingly rely on external partners for execution and planning support. In the AI in CRO services market, this reliance is shifting from basic outsourcing to engaging CROs capable of modeling trial scenarios, identifying potential bottlenecks, and accelerating feasibility decisions. This shift is redefining vendor competition, as staffing depth alone no longer meets sponsor needs when development plans change rapidly. Additionally, hybrid engagement models are gaining traction, allowing sponsors to access platforms and specialized support without committing to a single service structure. Consequently, AI readiness is becoming a critical factor in early-stage sponsor relationships.

Decentralized and Hybrid Trial Expansion

The adoption of decentralized and hybrid trials has expanded, driving the need for tools that monitor patients, sites, and protocol activities across diverse settings. The AI in CRO services market benefits from this trend, as AI supports patient matching, flags unusual remote data, and identifies protocol issues without relying solely on on-site monitoring. However, uneven site readiness can delay deployment, particularly when staff manage numerous disconnected systems.

Precision Medicine and Biomarker-Driven Recruitment

Precision medicine has transformed recruitment economics, with patient selection now based on detailed clinical and molecular criteria. This shift in the AI in CRO services market has increased demand for tools that efficiently and consistently match patients to trials, even with complex eligibility requirements. For example, tools have demonstrated the ability to significantly reduce matching times while maintaining high accuracy. These improvements are particularly critical in areas like oncology and early-stage development, where speed, biomarker alignment, and patient availability often determine trial success.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| AI validation and GxP compliance uncertainty | -1.8% | Global, with the greatest effect in the United States, Europe, and Japan | Short term (≤ 2 years) |

| Fragmented sponsor-CRO-site data interoperability | -1.4% | Global, with the strongest effect in multi-country programs | Medium term (2-4 years) |

| Liability ambiguity for AI-assisted regulated outputs | -1.0% | North America and Europe | Medium term (2-4 years) |

| Training-data bias in site and patient models | -0.8% | Global, with sharper effects in low-diversity trial geographies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI Validation and GxP Compliance Uncertainty

Validation remains a significant barrier to the broader adoption of AI in regulated clinical workflows. The FDA's draft guidance in January 2025 introduced a seven-step credibility framework for AI models in regulatory submissions.[1]Kim Jae, Christopher Mikson, Vernessa Pollard, Anisa Mohanty, Christopher Hooks, Danny Tobey, and Sean Fulton, “FDA and AI Alert Key Takeaways From FDA's Draft Guidance on Use of AI in Drug and Biological Life Cycle,” DLA Piper, dlapiper.com However, final guidance has yet to be issued. This situation places sponsors and CROs in an interim phase where expectations are somewhat clearer but not fully defined. In the AI in CRO services market, this challenge primarily impacts areas such as dose selection, safety monitoring, and submission-related applications, while lower-risk tasks like document or workflow management are less affected. As a result, the market continues to grow rapidly, but adoption rates vary across different service categories.

Fragmented Sponsor-CRO-Site Data Interoperability

AI tools deliver optimal performance only when data flows seamlessly among sponsors, CROs, and sites. However, in the AI in CRO services market, data fragmentation remains a critical challenge. EDC systems, site systems, document repositories, and sponsor data warehouses often fail to integrate effectively. Research has shown that while locally deployed large language models can achieve high accuracy in extracting structured data from EHR narratives, their success depends heavily on clean, institution-specific data infrastructure. This highlights that the issue extends beyond model quality to include the condition of the underlying data layer. Until interoperability across the operational stack improves, the AI in CRO services market will continue to face uneven adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Clinical Management Anchors Revenue; Early Development Accelerates

Clinical Trial Management Services, holding 57.34% of the market share in 2025, dominated the AI in CRO services market. This leadership reflects its critical role in global multi-site coordination, risk-based monitoring, site performance tracking, and regulatory document management. Efficiency gains from AI-driven orchestration functions have solidified their position as key revenue drivers. Additionally, steady investments in biometrics, data management, analytics, and regulatory support services further highlight their importance in trial execution.

Early Development & Translational Services is expected to grow at a 19.20% CAGR from 2026 to 2031, making it the fastest-growing segment. Sponsors are increasingly using AI for feasibility simulations and early decision-making to reduce delays in trial initiation. AI platforms have demonstrated the ability to identify trial sites efficiently, accelerating Phase III programs across multiple countries. Adjacent services, such as AI-enabled writing and pathology workflows, are also evolving, showcasing the industry's focus on early-stage AI capabilities.

By AI Technology: Machine Learning Leads; NLP Moves to the Core

Machine Learning, with a 42.45% share in 2025, led the AI in CRO services market as the primary technology layer. Its widespread application in site selection, risk prediction, data cleaning, anomaly detection, and workflow optimization underscores its commercial durability. The technology remains integral to improving recurring operational tasks, while emerging approaches like knowledge graphs are gaining traction in oncology and rare disease workflows.

Natural Language Processing (NLP) is projected to grow at a 20.35% CAGR through 2031, making it the fastest-growing AI technology segment. This growth is driven by the need to process large volumes of unstructured data, such as EHR notes and clinical narratives. AI systems have demonstrated strong performance in trial matching and structured data extraction, signaling a shift toward deeper applications of language models in recruitment, documentation, and data normalization.

By Therapeutic Area: Oncology Leads; Infectious Diseases Surpasses Expectations

Oncology, accounting for 35.35% of the market share in 2025, remained the largest therapeutic area in the AI in CRO services market. This dominance reflects the extensive oncology pipelines and the alignment of AI tools with oncology workflows, including biomarker matching and imaging reviews. AI-driven platforms are increasingly being deployed to enhance trial matching and expand access to cancer research, reinforcing oncology's position as a key revenue contributor.

Infectious Diseases & Vaccines is forecast to grow at a 19.6% CAGR from 2026 to 2031, making it the fastest-growing therapeutic area. The demand for flexible and rapid trial infrastructure post-pandemic has driven the adoption of AI tools. These tools enable remote recruitment, decentralized follow-ups, and adaptive protocols, aligning with the evolving needs of infectious disease programs and supporting their growth trajectory.

By Trial Phase: Phase III Maintains Anchor; Phase I Leads Growth

Phase III, with a 45.60% market share in 2025, was the largest trial phase by revenue. This reflects the high costs and complexity of late-stage studies, where AI-driven platforms have demonstrated the ability to significantly reduce trial timelines. The focus on improving efficiency in large-scale registration programs ensures Phase III remains the primary revenue anchor, even as earlier phases gain momentum.

Phase I is projected to grow at a 19.98% CAGR from 2026 to 2031, making it the fastest-growing phase segment. AI-guided dose-finding approaches and biomarker-led patient subtyping are driving this growth. Feasibility tools are also helping sponsors assess site readiness and patient pools, shifting AI value creation to the early stages of the development cycle and positioning Phase I as a critical growth area.

By End User: Pharma Dominates; Academic Institutions Emerge as Growth Catalysts

Pharmaceutical Companies, holding 56.3% of the market share in 2025, were the leading end-user group in the AI in CRO services market. Their scale and focus on reducing development timelines have driven the adoption of AI-enabled CRO services. The integration of AI into operational infrastructure highlights the industry's commitment to leveraging technology for efficiency and competitiveness.

Academic & Research Institutes are expected to grow at a 20.45% CAGR from 2026 to 2031, making them the fastest-growing end-user segment. This growth reflects the increasing adoption of commercial AI tools by public and academic research entities. The expansion of AI-driven trial matching platforms in academic settings broadens the market's buyer base and fosters innovative collaboration models, supporting trial quality and patient identification.

Geography Analysis

In 2025, North America accounted for 44.05% of the AI in CRO services market, maintaining its leadership position. This dominance stems from a strong biopharma sponsor base, a mature CRO ecosystem, and early regulatory advancements for AI in drug development. The region also benefits from being a hub for AI-specialist vendors and significant investments in full-service CRO platforms, strengthening its commercial foundation in the U.S. and Canada.

Europe is the second-largest regional market, driven by Germany, the U.K., and France. Its growth is supported by strong academic research networks, a large sponsor base, and investments in digital health and drug research. Europe also serves as a key base for multi-country studies, creating demand for vendors skilled in managing compliance and data workflows across jurisdictions.

Asia-Pacific is projected to grow at a 23.00% CAGR from 2026 to 2031, making it the fastest-growing region in the AI in CRO services market. The region's growth is fueled by large patient pools, cost-effective trials, and increasing digital health investments. China plays a significant role in this expansion, with AI integration deepening across the development process, positioning Asia-Pacific as a key area for market growth.

Competitive Landscape

The AI in CRO services market is moderately concentrated at the top, with significant fragmentation below. Key players like IQVIA, Labcorp Drug Development, ICON plc, Parexel, and Thermo Fisher Scientific's PPD dominate due to their global reach, extensive data assets, and ability to integrate AI across multiple service lines. Meanwhile, AI-native specialists are targeting specific workflows, creating a competitive environment where both scale and agility are critical.

Major vendors are responding by launching platforms, acquiring capabilities, and forming data partnerships. For example, IQVIA introduced a unified AI platform to expand its presence across workflows. Parexel enhanced its pharmacovigilance capabilities through acquisitions, while Thermo Fisher Scientific’s PPD strengthened trial feasibility and recruitment through strategic collaborations. These actions reflect a dual strategy of internal innovation and external capability building.

Data depth has become a key differentiator in the AI in CRO services market. Sponsors prioritize vendors that ensure reliable model performance across diverse datasets. Enterprise-scale data partnerships and proprietary workflow histories are gaining importance, while embedding AI into existing client systems reduces switching likelihood. This dynamic allows top players to maintain dominance while enabling niche specialists to capture market share by addressing specific challenges effectively.

AI In CRO Services Industry Leaders

Fortrea

charles river laboratories

Labcorp Drug Development

ICON plc

Parexel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Parexel acquired Vitrana, an AI pharmacovigilance technology developer, adding automated case intake, entity mapping, and narrative generation capabilities that reduce case processing time by 60%, positioning Parexel with a "fully automated end-to-end" pharmacovigilance solution ahead of competitors offering semi-automation.

- May 2026: Charles River Laboratories accelerated its AI digital pathology workflow, announcing AI-powered slide QC already in production and GLP-validated digital primary pathology reviews that reduce pathology read times by an average of 20% and improve pathologist efficiency by over 30%.

- April 2026: Thermo Fisher Scientific (PPD) partnered with HealthVerity, granting enterprise access to 270 million de-identified US patient lives across 70+ curated data sources, to strengthen AI-driven trial feasibility, recruitment, and RWE generation.

- April 2026: Fortrea launched Fortrea Intelligent Technology (FIT), an AI-enhanced suite built on the Xcellerate platform, encompassing Lifecycle, Foresight, and Companion pillars, automating workflows from pre-award to eTMF and offering SaaS deployment for sponsors and sites.

- April 2026: IQVIA launched IQVIA.ai, a unified agentic AI platform developed with NVIDIA, combining clinical and real-world data assets with NVIDIA's AI infrastructure for autonomous workflow orchestration, synthetic data generation, and cohort identification across clinical, commercial, and real-world operations.

Global AI In CRO Services Market Report Scope

As per the scope of the report, Artificial Intelligence (AI) in Contract Research Organization (CRO) services refers to the integration of machine learning, natural language processing (NLP), and predictive analytics into pharmaceutical and biotechnology R&D workflows. These AI-driven services automate manual, data-intensive tasks such as patient recruitment, protocol design, data monitoring, and regulatory submission to accelerate drug development timelines and reduce costs.

The AI in CRO Services Market is segmented by service type, AI technology, therapeutic area, trial phase, end-user, and geography. By service type, the market includes clinical trial management services, biometrics, data management & analytics services, laboratory, imaging & sample intelligence services, regulatory, safety & medical writing services, and early development & translational services. By AI technology, the market is segmented into machine learning, natural language processing, generative AI/large language models, computer vision, knowledge graphs & causal AI, and predictive analytics/digital twins. By therapeutic area, the market is categorized into oncology, rare diseases, infectious diseases & vaccines, neurology, cardiovascular & metabolic disorders, and immunology & inflammation. By trial phase, the market is segmented into Phase I, Phase II, Phase III, and Phase IV & real-world evidence. By end-user, the market is segmented into pharmaceutical companies, biotechnology companies, medical device companies, academic & research institutes, and government & nonprofit sponsors. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Clinical Trial Management Services |

| Biometrics, Data Management & Analytics Services |

| Laboratory, Imaging & Sample Intelligence Services |

| Regulatory, Safety & Medical Writing Services |

| Early Development & Translational Services |

| Machine Learning |

| Natural Language Processing |

| Generative AI / Large Language Models |

| Computer Vision |

| Knowledge Graphs & Causal AI |

| Predictive Analytics / Digital Twins |

| Oncology |

| Rare Diseases |

| Infectious Diseases & Vaccines |

| Neurology |

| Cardiovascular & Metabolic Disorders |

| Immunology & Inflammation |

| Phase I |

| Phase II |

| Phase III |

| Phase IV and Real-World Evidence |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Medical Device Companies |

| Academic & Research Institutes |

| Government and Nonprofit Sponsors |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Clinical Trial Management Services | |

| Biometrics, Data Management & Analytics Services | ||

| Laboratory, Imaging & Sample Intelligence Services | ||

| Regulatory, Safety & Medical Writing Services | ||

| Early Development & Translational Services | ||

| By AI Technology | Machine Learning | |

| Natural Language Processing | ||

| Generative AI / Large Language Models | ||

| Computer Vision | ||

| Knowledge Graphs & Causal AI | ||

| Predictive Analytics / Digital Twins | ||

| By Therapeutic Area | Oncology | |

| Rare Diseases | ||

| Infectious Diseases & Vaccines | ||

| Neurology | ||

| Cardiovascular & Metabolic Disorders | ||

| Immunology & Inflammation | ||

| By Trial Phase | Phase I | |

| Phase II | ||

| Phase III | ||

| Phase IV and Real-World Evidence | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| Medical Device Companies | ||

| Academic & Research Institutes | ||

| Government and Nonprofit Sponsors | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the AI in CRO space in 2026?

The AI in CRO services market is valued at USD 14.55 billion in 2026 and is projected to reach USD 28.65 billion by 2031 at an 18.45% CAGR.

Which service category brings in the most revenue?

Clinical Trial Management Services led in 2025 with a 57.34% share, showing that operational orchestration remains the main revenue base.

Which region is growing the fastest through 2031?

Asia-Pacific is the fastest-growing region, with a projected 23.00% CAGR from 2026 to 2031.

Why is oncology the largest therapeutic area for AI-enabled CRO work?

Oncology held 35.35% share in 2025 because trial pipelines are deep and AI tools fit well with biomarker matching, imaging review, and adaptive study design.

Which trial phase shows the strongest future expansion?

Phase I is projected to grow at 19.98% CAGR through 2031 as sponsors use AI more actively in dose-finding, feasibility, and early patient selection.

What are the main issues slowing broader adoption?

The main constraints are validation and GxP uncertainty, fragmented data interoperability, liability questions in regulated outputs, and bias risk in training data.

Page last updated on: