CLV And Churn Prediction AI Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

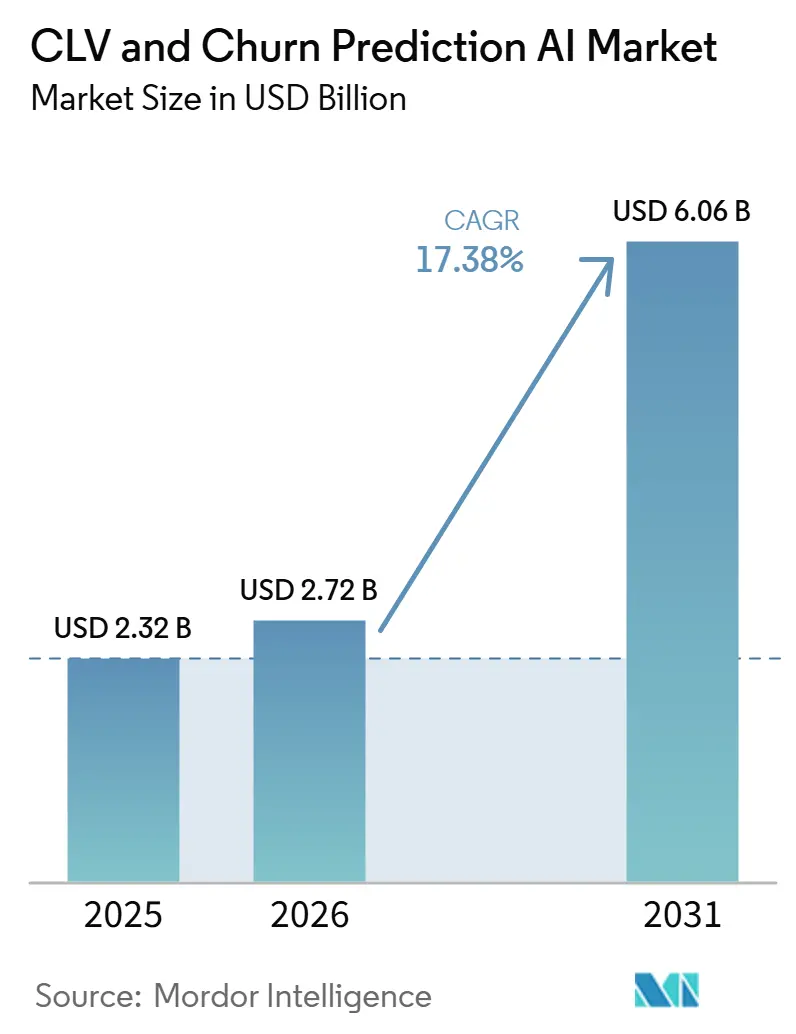

| Market Size (2026) | USD 2.72 Billion |

| Market Size (2031) | USD 6.06 Billion |

| Growth Rate (2026 - 2031) | 17.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CLV And Churn Prediction AI Market Analysis by Mordor Intelligence

The CLV and Churn Prediction AI market size is projected to be USD 2.32 billion in 2025, USD 2.72 billion in 2026, and reach USD 6.06 billion by 2031, growing at a CAGR of 17.38% from 2026 to 2031. Robust demand for predictive retention tooling is coming from retailers that now face data-rich but low-conversion traffic streams, telecommunications operators that must shield margins in saturated voice and data businesses, and banks turning to privacy-preserving AI to defend cross-sell revenue. Vendor focus is shifting from retrospective dashboards to self-improving agents that diagnose risk, decide on the next best action, and execute outreach without human intervention. Regulatory pressure is simultaneously elevating explainability, bias controls, and technical documentation as new buying criteria, favoring platforms with governance embedded in their architectures. Mergers and partnerships are accelerating as companies race to integrate customer data unification, real-time decisioning, and autonomous workflow execution into a single offering.

Key Report Takeaways

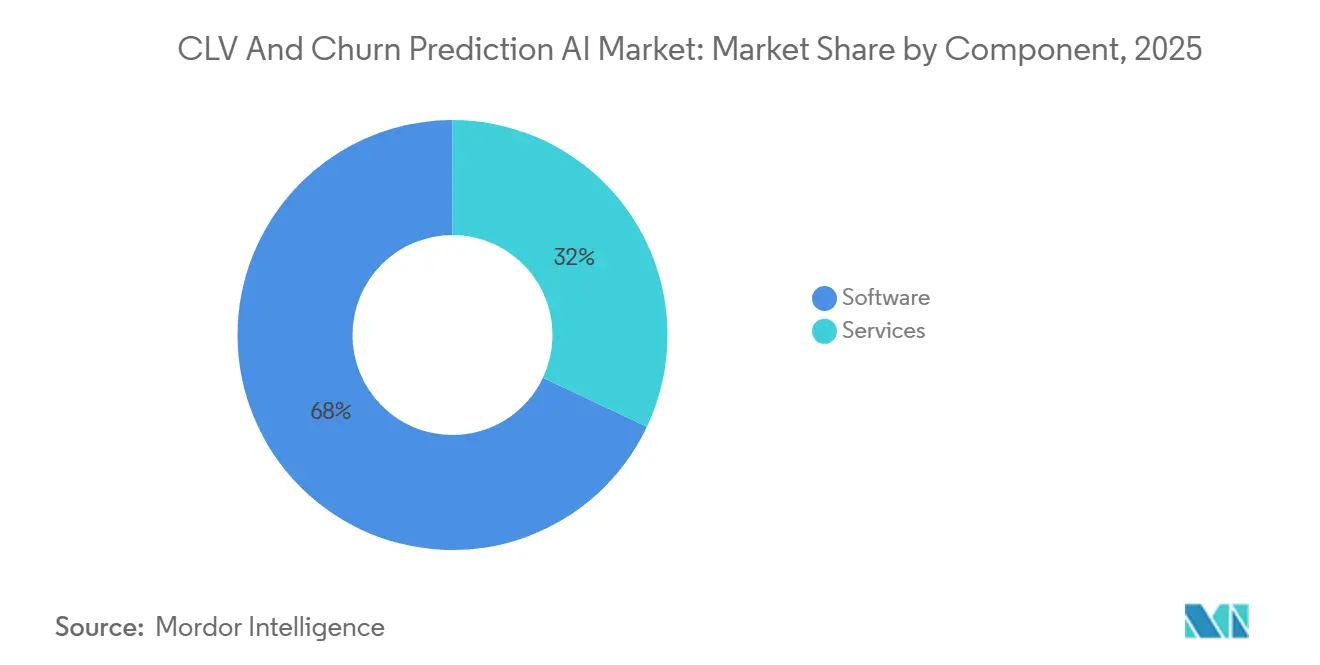

- By component, Software accounted for 67.98% of the CLV and Churn Prediction AI market share in 2025, while Services are projected to expand at an 18.91% CAGR through 2031.

- By deployment mode, Cloud held 71.78% of the CLV and Churn Prediction AI market share in 2025, and Hybrid architectures are forecast to grow at a 22.54% CAGR during 2026-2031.

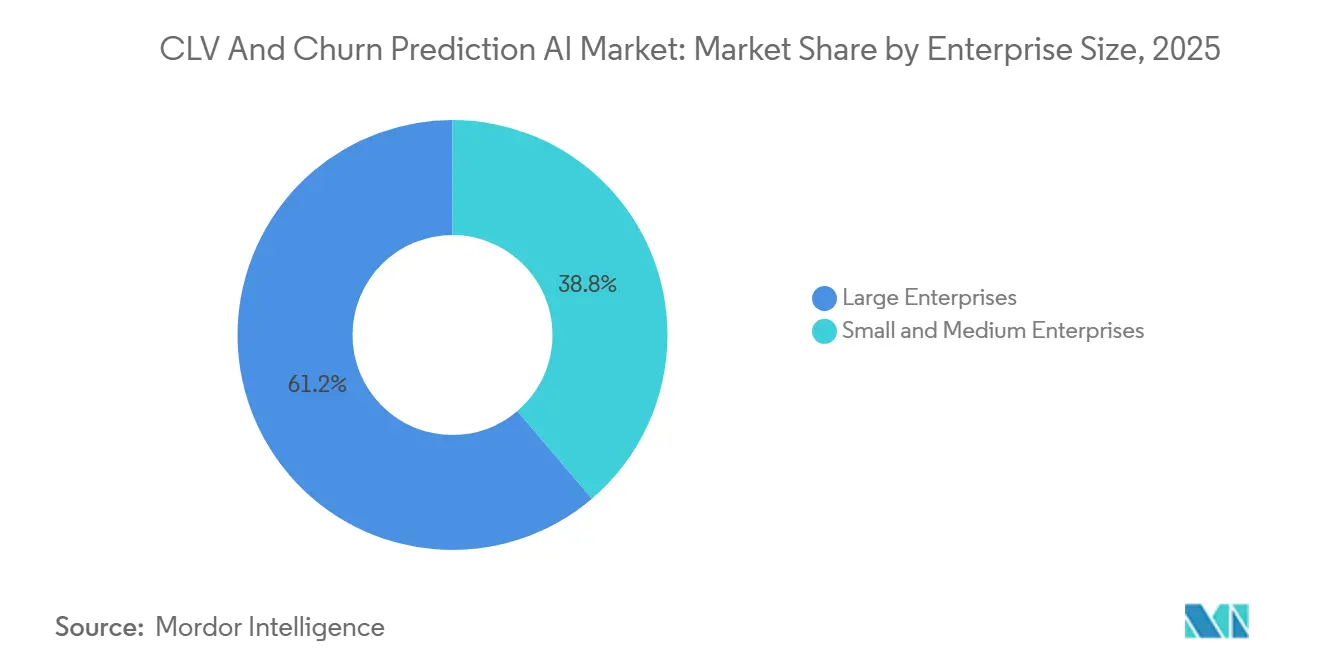

- By enterprise size, Large Enterprises commanded 61.23% revenue share in 2025, whereas Small and Medium Enterprises are poised to grow at a 21.58% CAGR to 2031.

- By end-user industry, Retail and E-commerce captured 29.48% of 2025 revenue, while Telecommunications is advancing at an 18.33% CAGR over the forecast horizon.

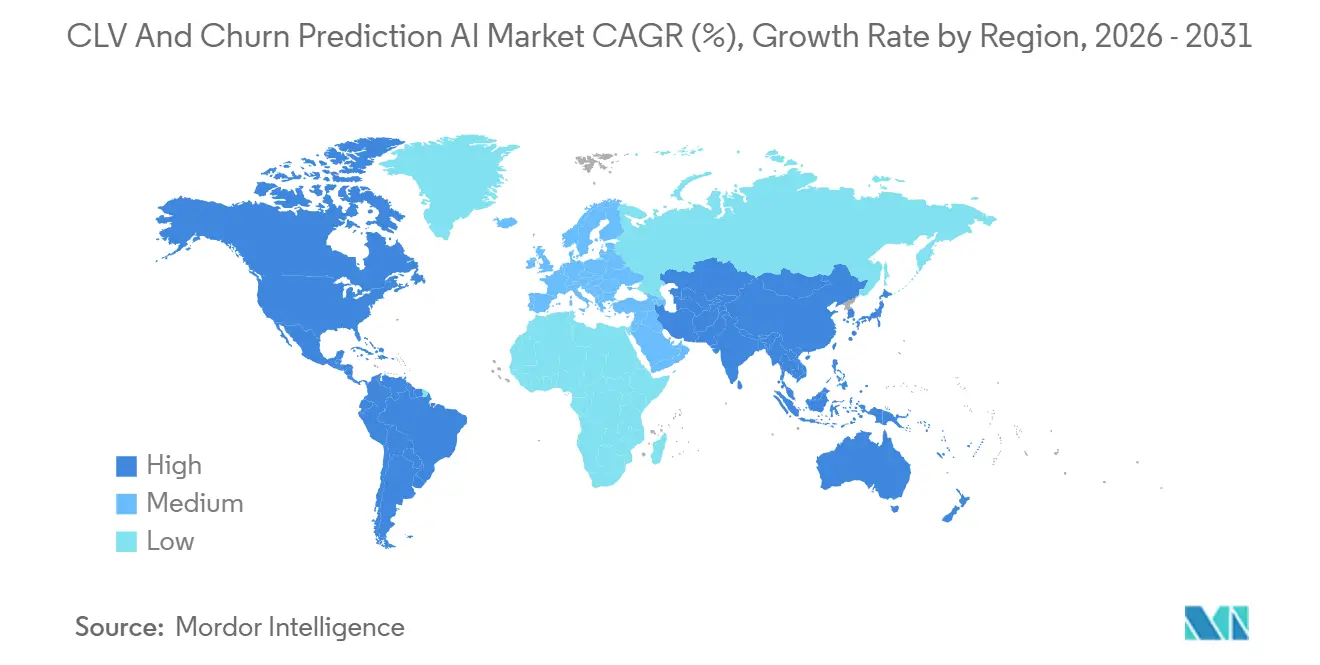

- By geography, North America accounted for 38.71% of the market share in 2025, and Asia-Pacific is expected to grow at a CAGR of 22.42% over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global CLV And Churn Prediction AI Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Predictive Analytics Tools Across Retail and BFSI | +3.8% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Rising Need to Reduce Customer Acquisition Costs Through Retention Strategies | +3.2% | Global | Short term (≤ 2 years) |

| Proliferation of Cloud-Native Customer Data Platforms Enabling Real-Time Churn Scoring | +2.9% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Increasing Integration of AI in Customer Success Workflows Among SaaS Enterprises | +2.6% | North America, Europe | Short term (≤ 2 years) |

| Emergence of Federated Learning Frameworks Addressing Data-Privacy Barriers in Cross-Industry CLV Modeling | +1.8% | Europe, North America financial hubs | Long term (≥ 4 years) |

| Demand for Explainable AI to Meet Upcoming EU AI Act Requirements Driving Platform Upgrades | +2.1% | Europe, with spillover to North America and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Predictive Analytics Tools Across Retail and BFSI

Retailers and banks are embedding real-time propensity scoring into revenue operations because generative AI has flooded digital storefronts with high-engagement shoppers who postpone purchases. During the 2024 holiday season, generative-AI referrals to United States retailers surged 1,300%, yet conversion rates trailed traditional channels by 9%.[1]Adobe, “How Generative AI Is Changing Consumer Behavior,” adobe.com Financial institutions mirror this urgency; a wealth-management firm with USD 18 billion in assets cut churn by 15% and saved USD 7.5 million annually after deploying an AI-driven retention model. Platforms processing billions of daily interactions, such as Klaviyo, now enable midsize brands to lift gross merchandise value 62% within a year by pushing predictive insights back into storefront workflows. Asia-Pacific’s private consumption is on track to reach USD 36 trillion by 2035, with 39% of consumers already using generative AI for shopping, expanding the addressable base for predictive tools.

Rising Need to Reduce Customer Acquisition Costs Through Retention Strategies

Digital advertising saturation and shifting search behaviors have inflated customer acquisition costs, making retention the fastest route to profitable growth. Sales, marketing, and service use cases account for nearly 40% of the USD 4.4 trillion long-term AI opportunity, yet fewer than half of executives report a revenue lift of more than 1% from generative AI so far. No-code agents such as Pecan’s Predictive AI Agent let planners build production-grade churn models in minutes, reducing manual forecasting time by 60%.[2]Pecan AI, “Introducing Pecan’s Predictive AI Agent,” pecan.ai Telecom research shows that explainable ensembles can slash churn by up to 25% and reduce retention marketing costs by 45% by prioritizing high-risk, short-tenure customers. Retailers balancing personalization with supply resilience also saw a 37% increase in customer lifetime value, though stockouts rose 29%, reinforcing the need for predictive models to align with operational constraints.

Proliferation of Cloud-Native Customer Data Platforms Enabling Real-Time Churn Scoring

Cloud-native customer data platforms collapse latency between behavioral signals and retention actions. Klaviyo synchronizes Shopify events in under 200 milliseconds, offering 160 templates, 80 flows, and 350 integrations that put AI-powered scoring in marketers' hands. Microsoft’s Dynamics 365 Customer Insights provides Copilot-enabled churn propensity models priced at USD 1,700 per tenant per month, making advanced analytics accessible without large capital outlays. Warehouse-native vendors such as Hightouch operationalize model outputs directly from data lakes, eliminating the need to replicate data across multiple stacks, while Visa’s analysis of billions of Asia-Pacific card transactions shows that real-time signals can isolate high-value, affluent cohorts responsible for 75% of new spending in 2025.

Increasing Integration of AI in Customer Success Workflows Among SaaS Enterprises

SaaS vendors embed AI within customer-success platforms to surface risk and automate remediation. Gainsight’s AI Agent for Slack brings real-time health scores and automated draft emails directly into collaboration channels, easing the burden on success managers. ChurnZero’s AI teammates run continuously to enrich data, create engagements, and generate alerts, with 80% of engineering capacity now dedicated to AI. Zendesk’s pending Forethought purchase sets a new baseline by resolving 80% of interactions end-to-end through autonomous agents, shrinking time-to-resolution and boosting satisfaction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Silos and Poor Data Quality Limiting Model Accuracy | -2.4% | Global | Short term (≤ 2 years) |

| Shortage of Skilled Data Scientists Constraining Implementation in SMEs | -1.9% | Global, acute in emerging markets | Medium term (2-4 years) |

| Rising API Access Fees Inflating Total Cost of Ownership | -1.3% | North America, Europe | Short term (≤ 2 years) |

| Model Performance Degradation from Rapidly Shifting Customer Behavior | -1.6% | Global, concentrated in digitally mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Silos and Poor Data Quality Limiting Model Accuracy

Nearly one-third of enterprises cite data quality as a top AI challenge, with only 43% reporting a consistent data structure across their systems. This inconsistency in data structure poses significant hurdles for organizations aiming to implement AI effectively. The healthcare sector serves as a prime example of this challenge. Companies like ClosedLoop must process a wide range of data types, including electronic health records, unstructured clinical notes, insurance claims, lab results, and social determinants of health, before they can generate explainable, actionable predictions. To address these data-related challenges, 60% of firms are planning to hire new providers specializing in data organization and multidisciplinary talent. This strategic move is expected to increase the average spending on outsourced services by 7%, reflecting the growing importance of data management in AI adoption.

Shortage of Skilled Data Scientists Constraining Implementation in SMEs

An OECD survey of 5,232 small and medium-sized enterprises (SMEs) finds that 50% of non-adopters cite a lack of skills as the primary barrier to adopting artificial intelligence (AI) technologies. On the other hand, SMEs that have adopted AI often leverage the technology itself to address skill gaps within their organizations. The emergence of no-code AI tools, such as Pecan, has significantly reduced onboarding challenges, making it easier for businesses to integrate AI solutions. For instance, Japanese SMEs report that 63.3% of users constrained by skill shortages find that AI effectively compensates for these deficiencies. Despite these advancements, essential skills such as programming, data analysis, and communication remain critical for maximizing the benefits of AI. Consequently, vendors are increasingly bundling training programs and advisory services with their AI platforms to help SMEs overcome these challenges and ensure successful adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Software as Compliance and Complexity Rise

Services captured a smaller base than Software in 2025, yet they are forecast to expand at an 18.91% CAGR between 2026 and 2031 as buyers outsource data harmonization, model validation, and EU AI Act conformity checks. Enterprises expect to increase spending on outsourced data services by 7%, and 60% will engage new partners for data organization and access to multidisciplinary talent. Totango’s Unison offering bundles professional services with custom models that analyze calls, emails, and tickets months before renewal, illustrating how specialized expertise underpins adoption. The shift extends across financial services and healthcare, where explainability and bias audits demand that domain regulators recognize.

Software is projected to maintain a 67.98% share of the Customer Lifetime Value (CLV) and Churn Prediction AI market in 2025, driven by the ability of agentic platforms to lower technical barriers for users. For instance, Pecan’s Predictive AI Agent significantly reduces the time required for model deployment, compressing it to just minutes. Similarly, ChurnZero’s credit-based AI marketplace enables businesses to scale operations without adding headcount. However, as governance costs continue to rise, hybrid engagement models are gaining traction. These models involve vendors offering a combination of software licenses and managed services, which is gradually narrowing the gap between revenue generated from pure software sales and fee-based implementation services.

By Deployment Mode: Hybrid Architectures Balance Sovereignty and Scale

Cloud held 71.78% of the CLV and Churn Prediction AI market share in 2025, driven by the adoption of warehouse-native data platforms and the scalability of elastic GPU capacity. However, hybrid deployments are projected to grow at a robust CAGR of 22.54%, as enterprises in Europe and the Middle East navigate the dual challenges of meeting transparency mandates while adhering to data-residency regulations. A recent Lenovo survey of 800 decision-makers found that 58% prefer hybrid AI solutions. The primary reasons cited for this preference were enhanced privacy controls and the ability to customize solutions to meet specific organizational needs. Teradata AI Factory brings NVIDIA’s AI stack on-premises for banks and hospitals that need deterministic costs and GDPR compliance.[3]Teradata, “Teradata Delivers Private AI Innovation in New Offering,” teradata.com

Public cloud continues to play a critical role in supporting burst training and enabling ecosystem integrations, such as Klaviyo’s real-time synchronization with Shopify. However, rising egress costs and concerns about inference latency are driving organizations to move recurrent scoring workloads closer to customer data. While on-premises solutions maintain a niche presence in defense and public-sector applications, they are increasingly integrating with managed update streams. This trend is gradually blurring the traditional lines between deployment models and expanding the CLV and Churn Prediction AI market size across diverse infrastructure frameworks.

By Enterprise Size: No-Code Agents Expand Accessibility for SMEs

Large Enterprises generated 61.23% of revenue in 2025 due to complex global account structures and multichannel data streams. These organizations often handle vast amounts of customer data, requiring robust, scalable solutions to manage their operations effectively. They consolidate spending on multi-product suites from vendors such as Klaviyo, which now processes 3.4 billion daily interactions across 8 billion profiles. Such platforms enable these enterprises to streamline operations, enhance customer engagement, and improve decision-making. These firms prioritize single-tenant security models, dedicated success teams, and deep customization to meet their specific business needs and ensure data security.

Small and Medium Enterprises (SMEs) are forecast to grow at a 21.58% CAGR, driven by no-code agents that dismantle skill barriers, making advanced technologies more accessible to smaller businesses. According to OECD data, generative AI adoption increases with firm size, yet even micro-enterprises are increasingly leveraging AI to address talent shortages and improve operational efficiency. Funding rounds, such as ZyG’s USD 58 million seed raise, highlight the growing venture capital interest in agentic operating systems.[4]Tech Funding News, “ZyG Raises USD 58 Million,” techfundingnews.com These systems integrate creative generation, SMS, and predictive lifetime-value forecasting into a pay-as-you-grow bundle, providing SMEs with cost-effective and scalable solutions. This trend is driving more SMEs to adopt AI-driven tools, further expanding their presence in the CLV and Churn Prediction AI market.

By End-User Industry: Telecommunications Emerges as Fastest-Growth Vertical

Retail and E-commerce led 2025 demand with a 29.48% share, as brands recalibrated their models to capture research-heavy, low-conversion traffic from generative AI. This shift highlights the growing importance of leveraging AI to optimize customer engagement and conversion strategies in a competitive market. However, Telecommunications is projected to register an 18.33% CAGR through 2031, driven by the increasing adoption of advanced AI models to enhance customer retention and operational efficiency. Peer-reviewed studies demonstrate that explainable ensemble models achieve 0.93 AUC and reduce churn by up to 25%, saving operators 35% to 45% on retention marketing costs, showcasing the tangible benefits of AI implementation in this sector.

BFSI accelerates with privacy-preserving federated learning that lets banks share insights without exposing raw data, ensuring compliance with stringent data privacy regulations while fostering collaboration. Healthcare use cases around member churn also grow as insurers tackle the 25% of United States residents who change coverage each year, raising acquisition costs and clinical risks. This trend underscores the critical role of AI in addressing churn-related challenges and improving operational outcomes. Manufacturing, logistics, and professional services lag due to fragmented data but represent upside as predictive maintenance and contract renewals become digitized, paving the way for future growth opportunities in these industries.

Geography Analysis

North America remained the largest contributor to the CLV and Churn Prediction AI market in 2025, as SaaS ecosystems mainstreamed AI across sales, service, and marketing. Examples include Gainsight embedding insights inside Slack and Zendesk, adding autonomous agents through the Forethought deal. The region benefits from deep venture funding, a robust SaaS ecosystem, and an abundance of technical talent, which collectively cement its leadership position. However, rising API costs have sparked debates over ownership and control of customer data, posing a challenge to the market's growth trajectory.

Europe and the Middle East are advancing rapidly, driven by a preference for hybrid deployment models and the need to meet compliance deadlines. A regional survey revealed that 46% of AI pilots successfully transitioned to production, with companies reporting an anticipated return of USD 2.78 for every USD 1 invested in AI initiatives. Despite this progress, only 27% of organizations in the region have implemented comprehensive governance frameworks. As a result, partners that specialize in data integration, bias audits, and documentation capture are gaining significant mindshare and competitive advantage in the market.

Asia-Pacific is forecast to record a 22.42% CAGR, outpacing every other region. The region's private consumption is expected to grow significantly, with affluent consumers generating three times the spending growth in 2025 and accounting for 75% of new spending. Cross-border e-commerce and tourism are growing at a faster pace than domestic markets, adding complexities such as travel frequency and foreign-exchange variables to lifetime-value models. Local brands in key markets like China, India, Indonesia, and Thailand are leveraging AI to iterate and innovate faster than multinational competitors. This dynamic reflects an innovation loop that is accelerating demand for churn prediction tools and driving the overall growth of the market in the region.

Competitive Landscape

The CLV and Churn Prediction AI market remains moderately fragmented. Established platforms are actively integrating agentic capabilities into customer-success, marketing, and service suites, while privacy-tech startups are focusing on federated learning. For instance, Zendesk’s initiative to resolve more than 80% of tickets autonomously through its partnership with Forethought sets a high benchmark that competitors are striving to achieve. Klaviyo’s collaboration with Google enhances its offerings by injecting search intent into billions of daily events, effectively pairing visibility during the discovery phase with targeted messaging at checkout.

Totango’s Unison platform provides enterprise-exclusive models that analyze unstructured interactions to identify risks months before renewal deadlines. Similarly, IBM Research’s PV4AML and Duality Tech are pioneering cryptography-based collaboration solutions that enable banks and payment networks to co-train models without sharing raw data, signaling the potential rise of industry consortia in highly regulated sectors. Venture capital investors are also driving democratization efforts through platforms like Pecan and ZyG, which aim to deliver production-ready models for businesses that lack in-house data science expertise.

Regulatory compliance is increasingly becoming a key differentiator in the market. The EU AI Act, for example, imposes penalties of up to 7% of global turnover for non-compliance, a challenge that smaller vendors may find difficult to manage. Providers that integrate quality management, bias testing, and human oversight into their solutions from the outset can position compliance as a competitive advantage. This approach allows them to market trust and reliability, shifting procurement decisions away from simple feature checklists toward considerations of audit readiness and total cost of ownership.

CLV And Churn Prediction AI Industry Leaders

Gainsight Inc.

Qualtrics International Inc.

Zendesk Inc.

Optimove Ltd.

Totango Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Zendesk agreed to acquire Forethought, aiming to mainstream self-improving agents that resolve more than 80% of service interactions end-to-end.

- February 2026: Klaviyo and Google formed a partnership that embeds real-time search intent into 3.4 billion daily interactions and enables conversational commerce via RCS for Business.

- February 2026: Turnstile secured USD 29 million Series A financing to launch an AI-first quote-to-cash platform with go-live times measured in minutes.

- February 2026: Sapiom raised USD 15.75 million in seed capital to build a financial access layer that enables AI agents to execute controlled payments for data and compute.

Global CLV And Churn Prediction AI Market Report Scope

The Customer Lifetime Value (CLV) and Churn Prediction AI Market refers to the global market for artificial intelligence-driven solutions that analyze customer data to estimate customer lifetime value and predict customer attrition. These solutions leverage technologies such as machine learning, predictive analytics, and big data analytics to help organizations identify high-value customers, detect churn risks, optimize retention strategies, and enhance customer engagement and profitability.

The CLV and Churn Prediction AI Market Report is Segmented by Component (Software and Services), Deployment Mode (Cloud, On-Premise, and Hybrid), Enterprise Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (Retail and E-commerce, BFSI, Telecommunications, Healthcare, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Retail and E-commerce |

| BFSI |

| Telecommunications |

| Healthcare |

| Other End-User Indutries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | Cloud | ||

| On-Premise | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-User Industry | Retail and E-commerce | ||

| BFSI | |||

| Telecommunications | |||

| Healthcare | |||

| Other End-User Indutries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What revenue will predictive retention technology generate by 2031?

The CLV and Churn Prediction AI market is projected to reach USD 6.06 billion by 2031.

Which deployment model is growing the fastest?

Hybrid architectures are forecast to expand at a 22.54% CAGR because they balance data-sovereignty and scalability needs.

Why are services revenue rising faster than software?

Enterprises outsource data harmonization and EU AI Act conformity work, driving an 18.91% CAGR for services between 2026 and 2031.

Which industry vertical shows the highest forecast growth?

Telecommunications leads with an expected 18.33% CAGR as explainable models cut churn and retention costs.

How are SMEs overcoming the data-science talent gap?

No-code agents such as Pecan’s Predictive AI Agent let business users build production-grade churn models, fueling a 21.58% CAGR among SMEs.

Page last updated on: