AI In Hospital Inventory Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

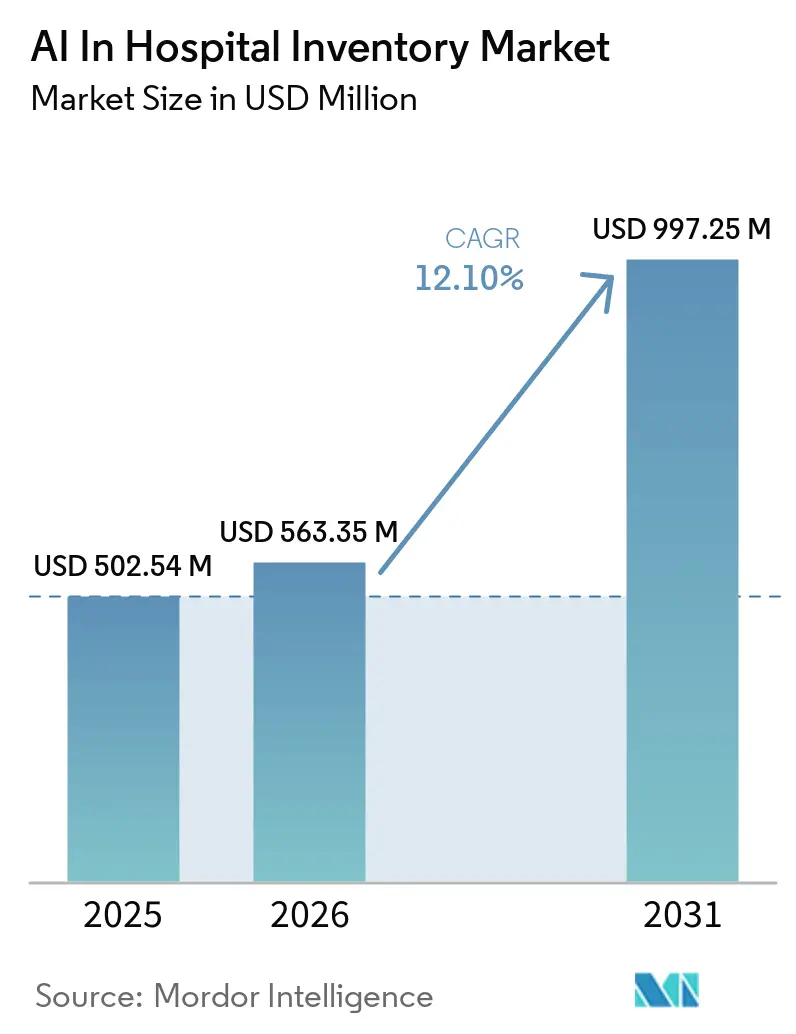

| Market Size (2026) | USD 563.35 Million |

| Market Size (2031) | USD 997.25 Million |

| Growth Rate (2026 - 2031) | 12.10% CAGR |

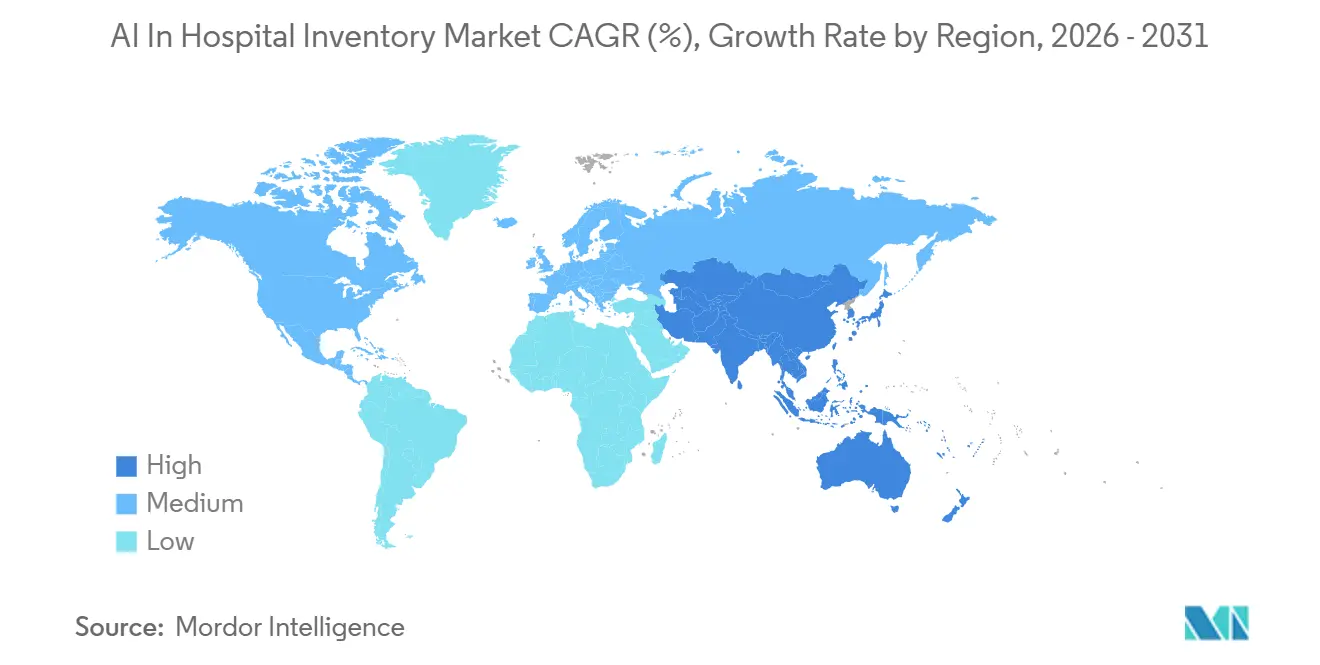

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

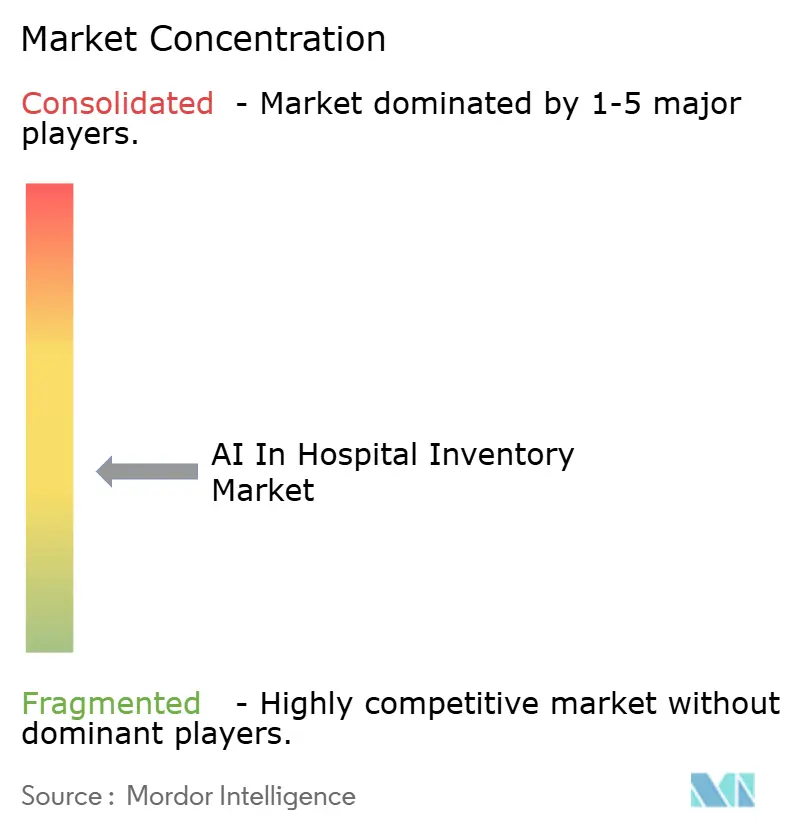

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Hospital Inventory Market Analysis by Mordor Intelligence

The AI In Hospital Inventory Market size is projected to be USD 502.54 million in 2025, USD 563.35 million in 2026, and reach USD 997.25 million by 2031, growing at a CAGR of 12.10% from 2026 to 2031.

Hospitals, under increasing compliance pressure from the Drug Supply Chain Security Act and the FDA's Unique Device Identification framework, are adopting traceable and digitally managed inventory workflows. This trend is fueling growth in the AI-driven hospital inventory management market. Furthermore, hospitals are leveraging AI to reduce stockouts, minimize waste, improve charge capture, and recover staff time previously lost to manual supply checks. The competitive landscape remains moderately fragmented, as hospitals continue to rely on disparate systems across pharmacies, operating rooms, and emergency care, limiting true end-to-end visibility. However, this fragmentation creates growth opportunities for platforms that integrate traceability, forecasting, replenishment, and workflow data into a unified operating model.

Key Report Takeaways

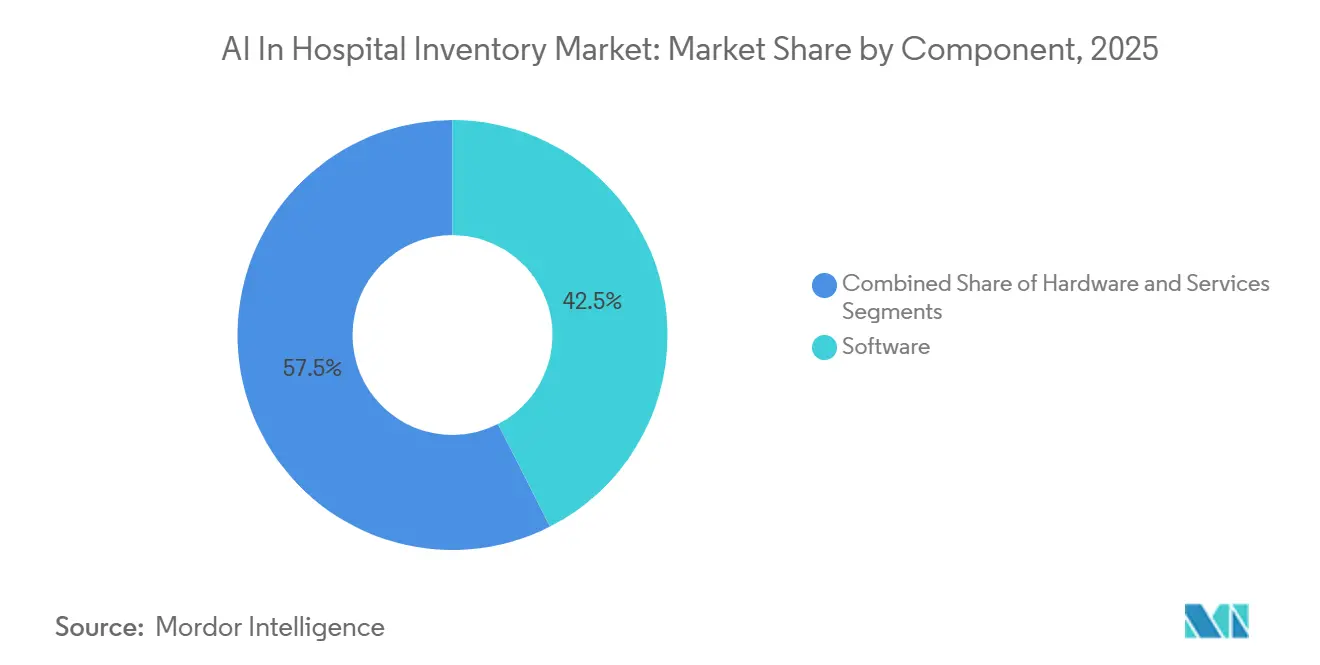

- By component, software led with 42.50% share in 2025, while hardware is projected to record the highest growth at 12.88% CAGR during 2026-2031.

- By deployment model, on-premises held 55.55% of the AI in hospital inventory management market share in 2025, while cloud-based solutions are projected to grow at 12.90% CAGR through 2031.

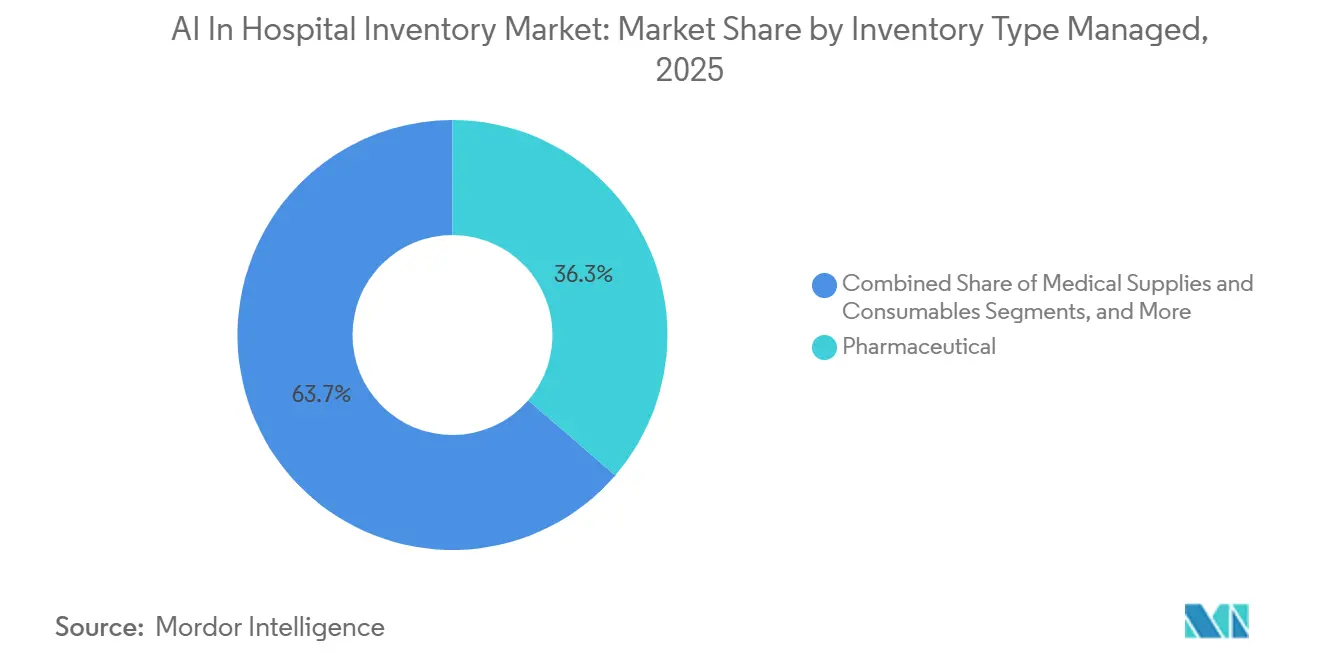

- By inventory type managed, pharmaceuticals accounted for 36.34% share in 2025, while medical supplies and consumables are projected to grow at 12.55% CAGR through 2031.

- By technology, RFID-enabled inventory systems held 32.43% share in 2025, while AI/ML predictive inventory systems are expected to expand at 13.15% CAGR during 2026-2031.

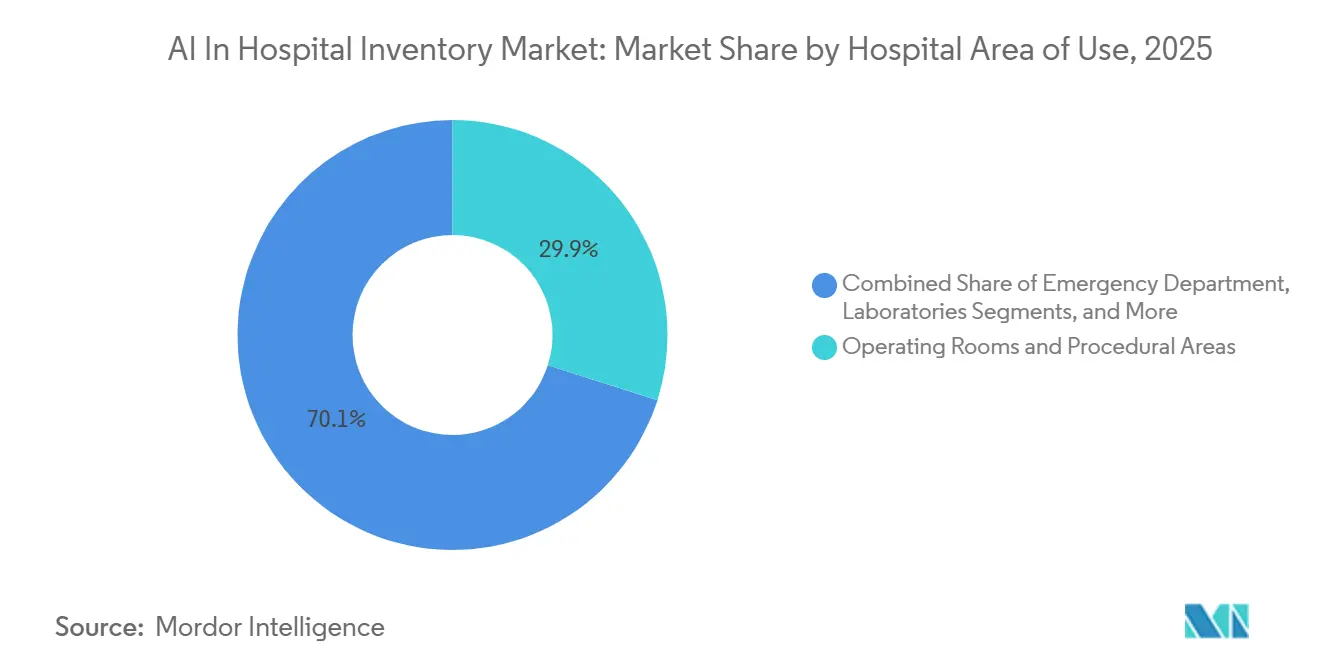

- By hospital area of use, operating rooms and procedural areas held 29.90% share in 2025, while the emergency department is projected to grow at 13.87% CAGR through 2031.

- By geography, North America led with 39.67% share in 2025, while Asia-Pacific is projected to grow at a CAGR of 14.15% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Hospital Inventory Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Traceability and recall compliance automation | +2.8% | Global, with primary compliance drivers in North America (DSCSA, UDI) and EU (MDR 2017/745) | Short term (≤ 2 years) |

| Waste and stockout reduction mandates | +2.3% | Global, most acute in North America and Western Europe where margin pressures are highest | Medium term (2-4 years) |

| Clinician time recovery from manual inventory work | +1.9% | Global, amplified in regions with nursing shortages, North America, the UK, Germany, and Japan | Medium term (2-4 years) |

| OR consignment and bill-only capture blind spots | +1.3% | North America and Europe | Short term (≤ 2 years) |

| Growing adoption of smart hospitals and digital healthcare | +2.0% | APAC core, especially China, Japan, and South Korea, with spillover to MEA | Long term (≥ 4 years) |

| Drug-shortage substitute orchestration | +1.4% | Global, especially North America, South Asia, and Sub-Saharan Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Traceability and Recall Compliance Automation

Traceability has transitioned from being a compliance-focused initiative to a critical operational requirement in the AI-driven hospital inventory management market. Regulatory frameworks, such as the FDA's UDI guidelines, have driven hospitals to enhance item-level visibility for devices across clinical settings.[1]U.S. Food and Drug Administration, “UDI Rule, Guidances, Training, and Other Resources,” U.S. Food and Drug Administration, fda.gov Additionally, broader UDI integration into interoperable data standards has strengthened the need to link scanned product data with clinical and inventory records. As a result, the AI in the hospital inventory management market is experiencing increased demand for systems that go beyond compliance tracking. Hospitals now seek AI solutions that integrate UDI capture with replenishment, recall management, billing accuracy, and real-time stock visibility.

Waste and Stockout Reduction Mandates

Efforts to reduce waste and prevent stockouts have become significant growth drivers for the AI in hospital inventory management market, as hospitals face mounting pressure to protect margins and maintain service continuity. Studies have demonstrated that AI-driven pharmaceutical demand forecasting can significantly reduce stockout incidents and lower holding costs within a short period. Public procurement trends also reflect this shift, with hospitals adopting AI inventory solutions that deliver high service rates and substantial logistics cost reductions.

Clinician Time Recovery from Manual Inventory Work

The AI in hospital inventory management market is expanding as hospitals aim to recover staff time lost to manual inventory tasks. Nurses, pharmacists, and support staff often spend considerable time checking shelves, locating missing items, and addressing discrepancies between recorded and actual stock levels. Transitioning to RFID and digitally tracked inventory systems has proven effective in reducing search times and unnecessary procurement. In some cases, hospital logistics teams are aligning demand planning with operating room schedules to ensure inventory availability matches expected clinical activities. This shift underscores that labor recovery is a measurable benefit of AI-driven inventory management, alongside reduced waste and improved stock accuracy.

Growing Adoption of Smart Hospitals and Digital Healthcare

The adoption of smart hospital infrastructure is providing the foundation for scaling the AI in hospital inventory management market. For example, UChicago Medicine’s enterprise agreement to deploy Artisight’s smart hospital platform across multiple devices is enabling real-time data capture for procedural and workflow optimization across various hospital units. Similarly, Beijing Anzhen Hospital in China, under the National Health Commission's "AI + Medical" initiative, has introduced a large-scale hospital operation management model, integrating HIS, SPD, and operational data systems to enhance efficiency.[2]MEDIXS, “在庫管理 - MEDIXS公式,” MEDIXS, medixs.jp Case studies have shown that intelligent logistics management supported by advanced demand prediction models can reduce energy consumption and handling mileage. As hospitals continue to build sensor-rich and software-connected environments, predictive inventory models are becoming increasingly valuable.[3]J. Akash et al., “AI-Based Pharmaceutical Demand Forecasting for Efficient Supply Chain Optimization,” International Journal of Engineering Development and Research, rjwave.org

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| ERP / EHR / MMIS integration burden | -2.5% | Global, most acute in North America and Europe where legacy system density is highest | Short term (≤ 2 years) |

| Cybersecurity and interoperability concerns | -1.8% | Global, highest regulatory risk in EU (AI Act, GDPR) and North America (HIPAA, HITECH) | Medium term (2-4 years) |

| Resistance to technology adoption among hospital staff | -1.3% | Global, amplified in South America, MEA, and rural or community hospitals globally | Medium term (2-4 years) |

| Poor item-master and UDI data quality | -1.0% | Global, particularly acute in APAC and MEA where data standardization is still developing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ERP / EHR / MMIS Integration Burden

Integration remains a key challenge in the AI-driven hospital inventory management market. Many hospitals still use outdated ERP, EHR, and materials management systems that lack compatibility with cloud-native data exchanges and real-time AI workflows. Infor highlights difficulties in unifying data across pharmacy, operating room, and nursing supply points due to inconsistent master data structures. Additionally, supporting UDI integration is often costly and time-intensive, even for well-resourced organizations. These factors lead to slower deployments, higher costs, and limited initial use cases.

Cybersecurity and Interoperability Concerns

Cybersecurity and interoperability concerns continue to impede adoption in the AI hospital inventory management market. Connected inventory tools increase the risk of sensitive data exposure, requiring robust governance and compliance measures. The EU AI Act and U.S. regulations like HIPAA and HITECH demand stringent controls for AI-enabled systems. Vendors such as Omnicell address these concerns through formal AI governance and certifications like HITRUST CSF i1. Until hospitals trust the security and auditability of predictive systems, these challenges will persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Anchors Platform Value; Hardware Investment Rising

In 2025, software led the AI in hospital inventory management market with a 42.50% share, driven by its ability to integrate with existing EHR, ERP, and pharmacy systems. Hospitals prioritize software-first deployments for enterprise visibility and forecasting before investing in hardware. Omnicell's OmniSphere exemplifies this trend by integrating robotics, smart devices, and workflows through a cloud-native platform. Services are gaining importance as hospitals rely on vendors for optimization and updates. Hardware, growing at 12.88% CAGR from 2026 to 2031, is critical for generating live data essential for predictive layers, complementing software's foundational role.

By Deployment Model: On-Premises Dominates; Cloud-Based Closing the Gap

On-premises deployment held a 55.55% share in 2025, reflecting hospitals' preference for direct control over data and system access. This model remains strong in academic and government systems due to data sensitivity and legacy infrastructure. Cloud-based solutions, growing at 12.90% CAGR from 2026 to 2031, are gaining traction as multi-hospital systems seek enterprise-wide visibility without duplicating infrastructure. Cloud architecture enables centralized updates and analytics, driving adoption. However, the pace of cloud adoption depends on resolving data governance and integration challenges.

By Inventory Type Managed: Pharma Leads on Value; Medical Supplies Fastest Growing

Pharmaceuticals accounted for 36.34% of the market in 2025, driven by regulatory requirements, audit pressures, and the critical need to prevent drug shortages in acute care settings. Hospitals invest in forecasting tools to ensure drug availability and patient safety. High-value items like implants and biologics, though smaller in volume, carry significant financial risks if tracking fails. These categories are increasingly targeted for AI adoption, while pharmaceuticals remain the largest inventory type.

By Technology: RFID Established as the Baseline; AI/ML Predictive is the Fastest Growing

RFID systems, with a 32.43% share in 2025, are the foundational technology in the AI in hospital inventory management market, offering fast and reliable visibility. Hospitals leverage RFID for automated tracking and data generation, which supports advanced forecasting. AI/ML predictive systems, growing at 13.15% CAGR from 2026 to 2031, are gaining traction as hospitals shift from visibility to demand modeling. RFID remains the operational baseline, while predictive AI drives differentiation.

By Hospital Area of Use: OR Leads on Spend; Emergency Department Fastest Growing

Operating rooms accounted for 29.90% of the market in 2025, driven by the high costs of implants, biologics, and surgical supplies. Hospitals benefit from improved charge capture and documentation in these areas. Emergency departments, growing at 13.87% CAGR from 2026 to 2031, are becoming a priority due to unpredictable demand and the need for rapid response. While operating rooms lead in spending, emergency departments represent the next major growth area.

Geography Analysis

In 2025, North America held a 39.67% share of the AI-driven hospital inventory management market, driven by stringent regulations, mature distributor networks, and significant hospital technology investments. Policies such as DSCSA enforcement, FDA's UDI mandates, and 340B audit requirements have pushed hospitals to adopt traceable and auditable inventory systems. This has positioned North America as a leader in deploying enterprise solutions across pharmacies, operating rooms, and supply chain workflows.

Europe remains a key player in the AI-driven hospital inventory management market, with regulations driving adoption while increasing implementation demands. The EU MDR 2017/745 enhances device traceability, while the EU AI Act and GDPR impose stricter governance and data requirements. Germany leads the region, with hospitals integrating AI-driven demand planning with operating room scheduling and logistics, creating consistent demand and higher expectations for vendor solutions.

Asia-Pacific is the fastest-growing region, with a 14.15% CAGR projected for 2026-2031, supported by rapid hospital digitalization in countries like China, Japan, South Korea, and India. China's National Health Commission is advancing the integration of HIS, SPD supply chain platforms, and operational data systems, while Japan promotes adoption through digitalization and AI subsidy programs. The market is transitioning from a North America-led base to a more balanced global structure, with Asia-Pacific driving growth.

Competitive Landscape

No single vendor dominates the AI in hospital inventory management market, which remains moderately fragmented. Established players like Omnicell, McKesson, and Cardinal Health, known for healthcare supply and automation, share the stage with AI-centric specialists such as IDENTI Medical, Countifi, DARVIS, and Mobile Aspects. While general ERP vendors have a presence, they primarily focus on the integration layer rather than delving deep into predictive inventory intelligence. This diverse landscape fuels competition, emphasizing software depth, workflow compatibility, and deployment speed.

In the AI in hospital inventory management arena, competitive strategies are diverging into two main paths. Larger, established players aim to weave inventory intelligence into expansive supply relationships and the hospital platforms they've already installed. In contrast, AI-centric vendors are honing in on areas like perioperative care, pharmacy, cath labs, and emergency departments, emphasizing visibility, forecasting precision, and swift deployment. A testament to this strategy is Omnicell's launch of OmniSphere, designed to integrate existing automation into a comprehensive cloud-based medication and inventory platform. Similarly, Oracle's bolstering of AI capabilities in its Fusion Cloud Applications underscores the trend of major platform vendors fortifying healthcare supply chain workflows.

Another wave of competition emerges from firms combining AI with real-time sensing and computer vision. IDENTI Medical leverages RFID and AI for charge capture, addressing challenges in high-value devices and surgical workflows. Artisight is enhancing smart hospital infrastructures to channel real-time operational data into cohesive care workflows. Smaller players are gaining traction with cost-effective IoT and camera-based models, making solutions accessible to community hospitals. Key opportunities lie in improving emergency department inventory visibility, tracking cath lab devices, and enabling cross-facility resource pooling. Vendors that excel in data reliability, compliance, and workflow integration are best positioned to scale in this evolving market.

AI In Hospital Inventory Industry Leaders

Autonomi

Becton, Dickinson and Company

Blue Yonder Group, Inc.

Countifi

Omnicell

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: UChicago Medicine partnered with Artisight to implement an AI-powered Smart Hospital Platform across over 1,800 devices in operating rooms, PACUs, patient rooms, and a new cancer facility opening in 2027. The platform integrates computer vision and voice recognition to track procedural milestones in real time and streamline EHR workflows, with nearly 500 hospitals in the U.S. under contract with Artisight.

- March 2026: Intelliguard completed the third phase of its RFID Mira Ecosystem rollout at Southlake Health by deploying the Mira Intelligence analytics and drug demand forecasting module. This upgrade enhances pharmacy operations with real-time inventory visibility, recall tracking, and predictive supply management.

- September 2025: Oracle introduced AI-driven features in its Fusion Cloud Applications to optimize healthcare supply chain operations. These tools simplify processes, automate workflows, reduce costs, and provide real-time visibility into medical supplies, improving efficiency and patient care.

Global AI In Hospital Inventory Market Report Scope

As per the scope of the report, AI in hospital inventory refers to the use of artificial intelligence, such as machine learning algorithms, IoT sensors, and computer vision, to autonomously track, manage, and forecast medical supplies in real time. It replaces manual counting with continuous, automated monitoring.

The AI in Hospital Inventory Market is segmented by component, deployment model, inventory type managed, technology, hospital area of use, and geography. By component, the market includes software, hardware, and services. By deployment model, the market is segmented into cloud-based, on-premises, and hybrid. By inventory type managed, the market is categorized into pharmaceuticals, medical supplies & consumables, implants & high-value devices, tissues & biologics, and laboratory supplies. By technology, the market is segmented into RFID-enabled inventory systems, barcode & mobile scanning, AI/ML predictive inventory systems, computer vision/image recognition, and IoT smart cabinets/smart shelves. By hospital area of use, the market is segmented into central pharmacy, operating rooms & procedural areas, nursing units/floor stock, cath lab/interventional radiology/electrophysiology labs, central supply/warehouse, laboratories, and emergency department. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Software |

| Hardware |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Pharmaceuticals |

| Medical Supplies & Consumables |

| Implants & High-Value Devices |

| Tissues & Biologics |

| Laboratory Supplies |

| RFID-Enabled Inventory Systems |

| Barcode & Mobile Scanning |

| AI/ML Predictive Inventory Systems |

| Computer Vision / Image Recognition |

| IoT Smart Cabinets / Smart Shelves |

| Central Pharmacy |

| Operating Rooms & Procedural Areas |

| Nursing Units / Floor Stock |

| Cath Lab / Interventional Radiology / Electrophysiology Labs |

| Central Supply / Warehouse |

| Laboratories |

| Emergency Department |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Hardware | ||

| Services | ||

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Inventory Type Managed | Pharmaceuticals | |

| Medical Supplies & Consumables | ||

| Implants & High-Value Devices | ||

| Tissues & Biologics | ||

| Laboratory Supplies | ||

| By Technology | RFID-Enabled Inventory Systems | |

| Barcode & Mobile Scanning | ||

| AI/ML Predictive Inventory Systems | ||

| Computer Vision / Image Recognition | ||

| IoT Smart Cabinets / Smart Shelves | ||

| By Hospital Area of Use | Central Pharmacy | |

| Operating Rooms & Procedural Areas | ||

| Nursing Units / Floor Stock | ||

| Cath Lab / Interventional Radiology / Electrophysiology Labs | ||

| Central Supply / Warehouse | ||

| Laboratories | ||

| Emergency Department | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of AI in hospital inventory management in 2026?

The AI in hospital inventory management market size is USD 563.35 million in 2026 and it is projected to reach USD 997.25 million by 2031 at a CAGR of 12.10%.

Which region leads adoption of AI in hospital inventory management?

North America led with 39.67% share in 2025 because regulatory pressure, hospital capital, and traceability requirements remain stronger there than in most other regions.

Which region is growing fastest through 2031?

Asia-Pacific is the fastest-growing region with a 14.15% CAGR during 2026-2031, supported by smart hospital programs and public digitalization efforts in countries such as China and Japan.

Which component category holds the largest share?

Software held the largest component share at 42.50% in 2025 because hospitals often adopt platform and integration layers before committing to larger hardware rollouts.

What technology is growing fastest in hospital inventory systems?

AI/ML predictive inventory systems are growing the fastest at 13.15% CAGR during 2026-2031 because hospitals want demand forecasting, not just item visibility.

Which hospital area creates the strongest demand for these tools?

Operating rooms and procedural areas held 29.90% share in 2025 due to the high cost of implants, biologics, and surgical supplies, while emergency departments are growing fastest at 13.87% CAGR.

Page last updated on: