AI In Biomanufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 25.13 Billion |

| Market Size (2031) | USD 44.68 Billion |

| Growth Rate (2026 - 2031) | 12.20% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Biomanufacturing Market Analysis by Mordor Intelligence

The AI In Biomanufacturing Market size was valued at USD 22.40 billion in 2025 and is estimated to grow from USD 25.13 billion in 2026 to reach USD 44.68 billion by 2031, at a CAGR of 12.20% during the forecast period (2026-2031).

The AI in biomanufacturing market is expanding because biologics production is becoming harder to manage with manual decision making alone, especially when manufacturers need tighter control over yield, quality, and scale-up. Cost pressure is also rising across originators, biosimilar developers, and contract manufacturers, which is pushing the AI in biomanufacturing market toward tools that reduce waste, shorten changeovers, and improve batch consistency. A larger stream of process data from sensors, digital twins, and connected production systems is making the AI in biomanufacturing market more practical for real manufacturing settings rather than limited pilot use cases.

Key Report Takeaways

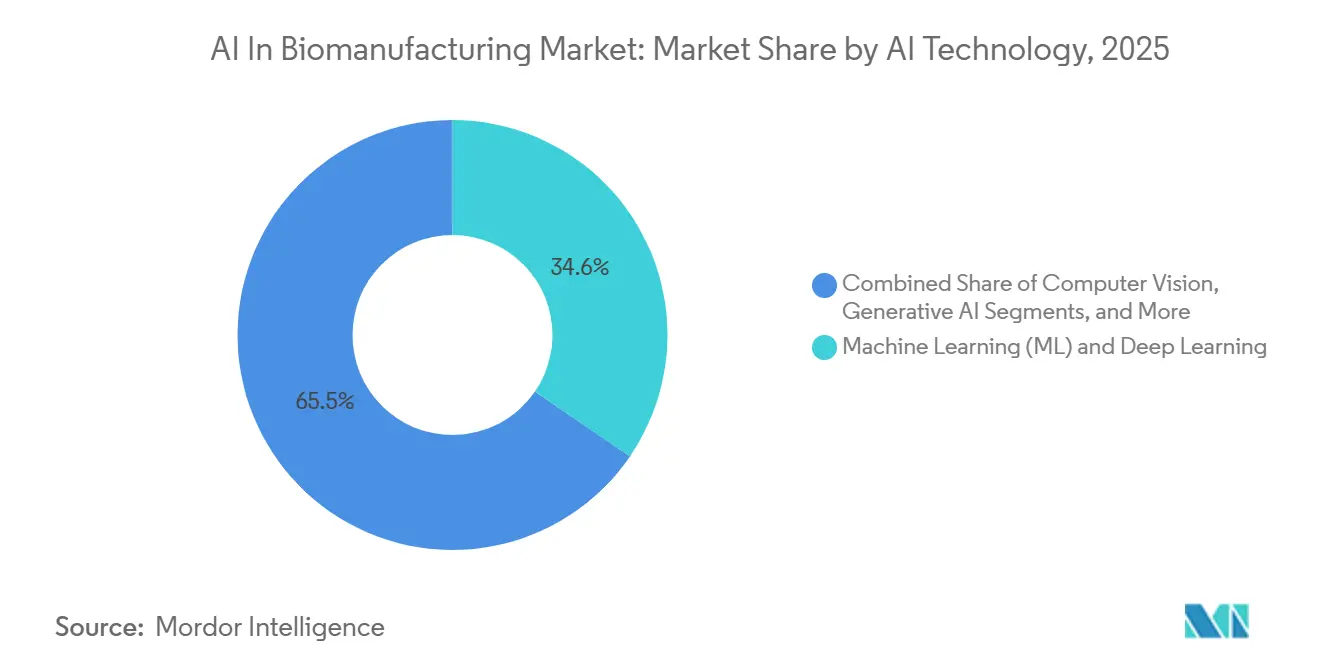

- By AI technology, machine learning and deep learning led with 34.55% share in 2025, while computer vision is projected to expand at a 13.23% CAGR through 2031.

- By offering, software held 62.45% revenue share in 2025, while services will grow the fastest at a 14.15% CAGR through 2031.

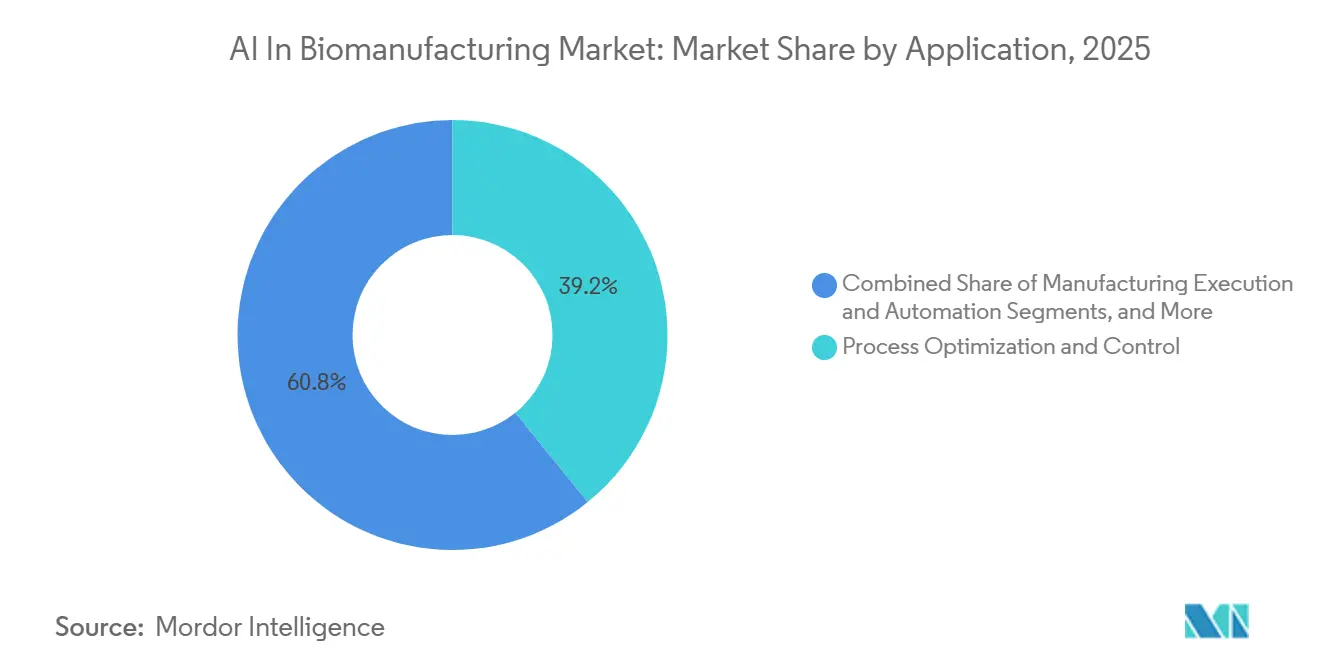

- By application, process optimization and control accounted for 39.17% of the AI in biomanufacturing market size in 2025, while manufacturing execution and automation will advance at the highest CAGR of 15.1% through 2031.

- By deployment mode, cloud-based solutions led with 60.43% share in 2025, while on-premise deployment will grow faster at a 12.96% CAGR through 2031.

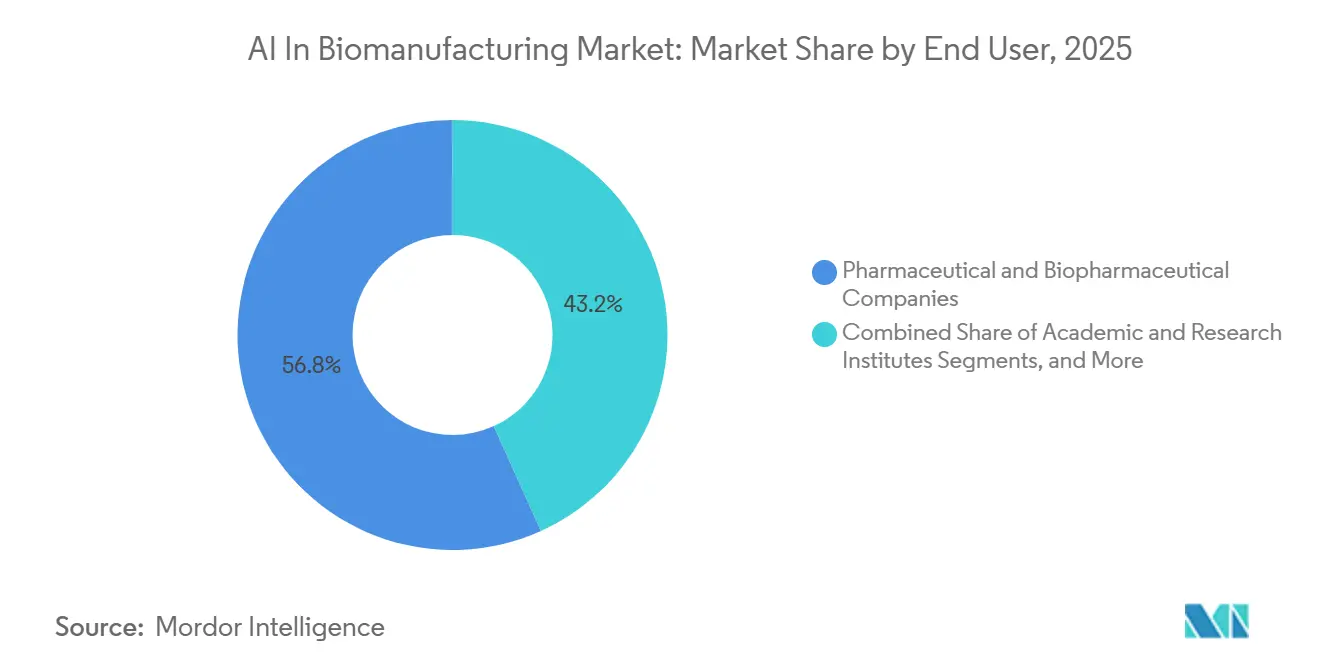

- By end user, pharmaceutical and biopharmaceutical companies held 56.76% share in 2025, while CDMOs and CMOs will post the highest CAGR of 12.75% through 2031.

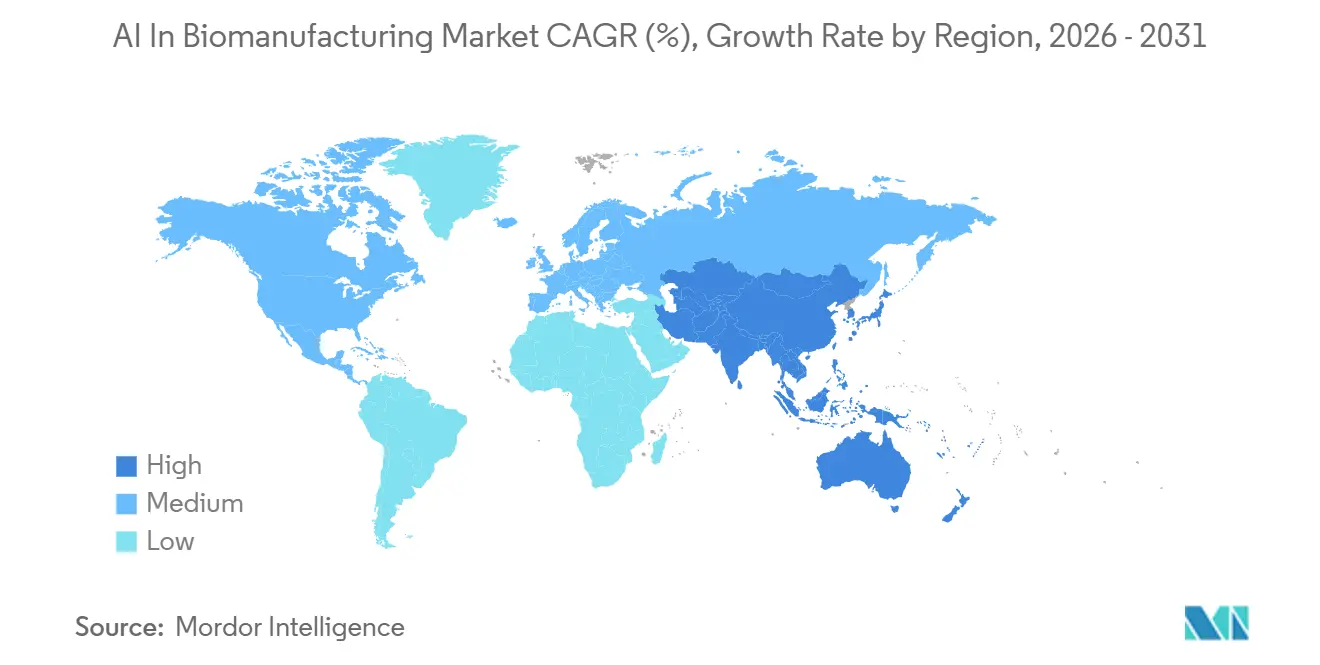

- By geography, North America held 39.67% of the AI in biomanufacturing market share in 2025, while Asia-Pacific will record the fastest regional expansion at a 15.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Biomanufacturing Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Biologics, biosimilars, and advanced therapies raise production complexity | +3.0% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Cost of goods pressure in biopharmaceutical manufacturing | +1.8% | Global, especially APAC low-cost production centers | Medium term (2-4 years) |

| Industry 4.0 and smart manufacturing adoption in biopharma | +2.0% | North America, Europe, South Korea, Japan | Medium term (2-4 years) |

| Bioprocess data growth supports AI model training | +1.5% | Global, with early gains in North America and APAC | Medium term (2-4 years) |

| Cell and gene therapy scale-up needs AI support | +1.8% | North America, Europe | Long term (≥ 4 years) |

| PAT and quality by design support data-driven control | +1.3% | Global, most acute in the US and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Biologics and Biosimilars Demand Reshaping AI Investment Priorities

The biomanufacturing industry is responding to the increasing demand for biologics, biosimilars, and advanced therapies. These products require higher process sensitivity, complex scale-up methods, and stricter quality standards, driving the need for continuous process intelligence. Manufacturers are addressing challenges such as batch variability, tighter release timelines, and process transfers across facilities while maintaining labor efficiency. Additionally, patent expirations for biologics are pressuring biosimilar producers to achieve cost efficiency and high yields from the start. This shift has led to AI applications focusing on cell culture control, fill-finish operations, and quality predictions, with service-based adoption rising as producers seek AI solutions without building extensive internal teams.

Bioprocess Data Surge Enabling Production-Grade AI

The availability of abundant, frequent, and connected process data is accelerating AI adoption in biomanufacturing. Advanced platforms now monitor numerous process attributes and generate significantly higher data density compared to traditional methods, enabling real-time quality assessments and reducing delays from offline testing. Early adopters gain a competitive edge by leveraging proprietary process histories for model training, which late entrants cannot easily replicate. Machine learning advancements are optimizing culture conditions, improving decision-making in complex manufacturing environments. The market is increasingly shaped by the ownership of high-quality, transferable datasets alongside algorithm sophistication.

Cell and Gene Therapy Pipeline Driving AI-Enabled Scale-Up

Cell and gene therapy production presents unique scale-up challenges, including patient-specific workflows, strict chain-of-identity requirements, and variable starting materials. These complexities demand systems capable of predicting failure risks, streamlining technology transfers, and enhancing throughput control without compromising quality. AI investments are shifting toward digital twins, adaptive scheduling, and model-assisted experimental designs to address these needs. CDMOs with advanced digital infrastructures are leveraging AI as a competitive differentiator, while smaller players face margin pressures as sponsors prioritize partners offering scale, compliance, and data intelligence.

Regulatory Emphasis on PAT and Quality by Design Accelerating AI Adoption

Regulatory guidance is driving AI adoption in biomanufacturing by clarifying its role in manufacturing processes. Recent guidelines emphasize risk-based credibility assessments for AI in regulatory decision-making, encouraging manufacturers to invest in AI programs. The PAT and Quality by Design framework supports data-driven control strategies, predictive monitoring, and structured model validation. Regulatory preferences for transparent and stable models over frequently changing systems are shaping the market. Vendors and manufacturers that combine performance improvements with traceability, validation rigor, and lifecycle management are well-positioned for success.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented and siloed bioprocess data infrastructure | -0.9% | Global, most acute in APAC and South America | Medium term (2-4 years) |

| High capital cost and integration burden in legacy GMP facilities | -0.8% | Global, most severe in aging European and North American facilities | Long term (≥ 4 years) |

| Regulatory and compliance uncertainty around AI use | -0.5% | EU, Global | Short term (≤ 2 years) |

| Shortage of bioprocess and AI talent | -0.8% | Global, most acute in North America, Western Europe, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Data Infrastructure as the Primary Adoption Ceiling

Biomanufacturing facilities face challenges due to data generated in incompatible formats across process development, manufacturing, and quality systems. Years of isolated equipment purchases have resulted in disconnected instruments, inconsistent metadata, and insufficient context for training cross-functional models. This slows deployment as teams spend more time aligning records than validating AI use cases. Additionally, models trained at one site often underperform at others due to differences in naming conventions, sensor data, and workflows. As a result, digitally advanced sites progress faster, while legacy sites remain in pilot stages, delaying enterprise scaling and extending ROI timelines.

Talent Shortage Constraining AI Governance Depth and Model Lifecycle Management

The AI in biomanufacturing market is constrained by a lack of professionals skilled in both regulated bioprocessing and AI model management in production environments. Developing a model is only part of the process; organizations also need experts to monitor drift, manage revalidation, document changes, and address audit requirements. This gap is more critical in advanced therapies, where deviations pose higher risks. Rapid tool evolution further shortens skill refresh cycles, increasing training demands even for experienced teams. Consequently, many companies struggle to transition from proof of concept to scalable deployment, despite the availability of technology. Growth in the market will remain uneven until organizations build robust, multidisciplinary teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By AI Technology: Machine Learning Dominates; Computer Vision Disrupts Process Visibility

In 2025, Machine Learning and Deep Learning held a 34.55% share of the AI in biomanufacturing market, establishing their role as core technologies for control, prediction, and optimization in bioprocessing. Their dominance stems from applications in process monitoring, predictive maintenance, and quality forecasting, particularly where structured data and defined variables like yield or impurity trends exist. Machine learning offers a practical entry point for measurable value without factory redesigns, with supervised and hybrid approaches attracting the largest budgets. Computer Vision is projected to grow at a 13.23% CAGR through 2031, driven by its ability to automate visual inspections, container integrity checks, and equipment monitoring. This technology converts visual data into actionable insights, improving compliance and efficiency in sterile environments.

By Offering: Software Scale-Up Leads; Services Emerges as the Strategic Growth Vector

In 2025, software accounted for 62.45% of the market, reflecting its role in integrating platforms, analytics, and applications with existing infrastructure. Manufacturers favored software for its ability to connect systems like LIMS and quality workflows while enabling incremental adoption. This flexibility allowed companies to test use cases without major hardware investments. Services are expected to grow at a 14.15% CAGR through 2031, as buyers increasingly seek outcomes over licenses. Services address critical needs like process mapping, model validation, and compliance, making them essential for operationalizing AI tools in regulated environments.

By Application: Process Optimization Anchors Revenue; Manufacturing Execution Signals Automation Maturity

In 2025, Process Optimization and Control captured 39.17% of the market, driven by its direct impact on yield, cycle time, and consistency. Manufacturers prioritize optimization tools for their measurable business value and ability to assist operators without requiring full autonomy. Manufacturing Execution and Automation is set to grow at a 15.1% CAGR through 2031, as companies transition from advisory AI to systems that refine production workflows. This shift reflects increasing confidence in autonomous production support as digital maturity and governance frameworks improve.

By Deployment Mode: Cloud Scales; On-Premise Grows on Data Sovereignty Logic

In 2025, Cloud-Based deployments held a 60.43% market share, driven by scalability, computational access, and ease of software updates. The cloud model supports flexible computing for model training and data aggregation, making it a preferred choice for early-stage AI adoption. On-Premise deployments are projected to grow at a 12.96% CAGR through 2031, as manufacturers prioritize compliance, data sovereignty, and internal security. Hybrid architectures are gaining traction, enabling companies to balance flexibility and compliance by separating regulated data from analytics workloads.

By End User: Pharma Leads; CDMOs Compete on Digital Intelligence

In 2025, Pharmaceutical and Biopharmaceutical Companies held a 56.76% market share, leveraging larger budgets, proprietary datasets, and integrated process control across the product lifecycle. Their scale allows for significant investments in platform integration and validation, giving them a structural advantage. CDMOs and CMOs are expected to grow at a 12.75% CAGR through 2031, as customers demand digital capabilities for faster technology transfer and improved process visibility. For contract manufacturers, AI has become a competitive differentiator, enabling smarter process control and reliable scale-up in biologics and advanced therapies.

Geography Analysis

In 2025, North America secured 39.67% of the AI in biomanufacturing market share, making it the leading regional contributor. The region benefits from a high concentration of pharmaceutical headquarters, specialist manufacturers, CDMOs, and digital infrastructure providers. Its early-mover advantage in biologics production ensures many sites already have the necessary data history and automation foundation for AI deployment. Regulatory clarity provided by the FDA further strengthens North America's position, aligning capital availability, regulatory engagement, and data maturity.

Europe plays a pivotal role in the AI in biomanufacturing market, combining established biologics capacity with a strong regulatory and industrial base. Countries like Germany, the United Kingdom, France, and Switzerland drive regional activity with extensive manufacturing networks and advanced quality systems.

Asia-Pacific will be the fastest-growing regional segment, with a projected 15.45% CAGR through 2031. The region's rapid growth is fueled by increasing capacity, supportive policies, and digital advancements. China's strategic focus on biomanufacturing and Japan's collaborative efforts in process design and advanced manufacturing further enhance the region's potential for AI-driven innovation and infrastructure development.

Competitive Landscape

In the AI in biomanufacturing market, a diverse array of participants creates a moderately fragmented landscape. Major players like Thermo Fisher Scientific, Danaher, Sartorius, and Siemens compete with AI-native software firms, cloud platforms, and advanced digital manufacturing service providers. This diversity sets the market apart from more consolidated equipment categories, as leadership isn't solely defined by a singular capability. Buyers assess not just the tools but their compatibility with existing data, validation, and plant systems.

In the AI in biomanufacturing arena, a discernible trend emerges: the pursuit of dominance over the data layer, eclipsing mere ownership of the application layer. Platforms like Benchling, TetraScience, and Aizon aim to position themselves above current execution and quality systems, aspiring to be the nexus for interconnected manufacturing data. Established life science vendors maintain a competitive edge due to their closer ties with instruments, process analytics, and existing manufacturing setups.

Product launches, investments in digital twins, and expansion of intellectual property are actively molding the AI in biomanufacturing market. WuXi Biologics introduced its PatroLab digital twin platform in January 2026, enhancing capabilities in predictive modeling and automated control. Sartorius expanded its patent portfolio from 7,260 to 7,806 patents between 2023 and 2024, focusing on bioprocess sensors, analytics, and AI-driven cell culture tools. The market is expected to remain fragmented as no single vendor bridges gaps across data, compliance, hardware, and specialized expertise.

AI In Biomanufacturing Industry Leaders

Ginkgo Bioworks Holdings Inc.

Benchling Inc.

Culture Biosciences Inc.

Dassault Systèmes SE (BIOVIA)

DataHow AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Form Bio launched FormManufacturing, an AI-driven platform for cell and gene therapy manufacturing, combining AI-based construct design optimization (FormSightAI) and genomic quality analytics (FormBatchQC) for AAV programs, the platform demonstrated 8x improvement in genome integrity and 2-3x yield increase across customer programs, directly addressing the fact that 74% of FDA rejections in CGT are manufacturing-quality-related.

- April 2026: WuXi Biologics' Chengdu Microbial Commercial Manufacturing Site achieved structural completion, targeting GMP release by end of 2026, the 95,000 sq meter facility features a 15,000-liter fermenter expandable to 60,000 liters for up to 110 drug substance batches annually, integrating automated digital systems for compliance and data integrity across 945 active client projects.

- April 2026: ArgusEye secured EUR 3.3 million (USD 3.6 million) from Voima Ventures, Eir Ventures, and Impilo Partners to scale its Auga real-time bioprocess monitoring platform globally, reflecting biopharma's accelerating shift toward continuous, data-driven manufacturing.

- February 2026: Shionogi Pharmaceutical and Hitachi launched a generative AI solution for regulatory document creation in Japan, demonstrating 50% reduction in clinical study report preparation time and 20% reduction in protocol creation time, representing a significant productivity gain for regulatory affairs teams.

Global AI In Biomanufacturing Market Report Scope

As per the scope of the report, AI in biomanufacturing refers to the integration of machine learning and predictive analytics to automate, monitor, and optimize the production of biological goods. It allows companies to fine-tune delicate biological processes, significantly improving product yield, reducing batch failures, and lowering overall manufacturing costs.

The AI in biomanufacturing market is segmented by AI technology, offering, application, deployment mode, end-user, and geography. By AI technology, the market includes machine learning (ML) and deep learning, natural language processing (NLP), computer vision, digital twin and simulation AI, reinforcement learning, generative AI, and other AI technologies (federated learning, physics-informed neural networks, hybrid AI). By offering, the market is segmented into software, hardware, and services. By application, the market is categorized into process optimization and control, quality control and assurance, predictive maintenance, drug discovery and development support, manufacturing execution and automation, supply chain optimization and demand forecasting, regulatory compliance and documentation, and other applications. By deployment mode, the market is segmented into cloud-based, on-premise, and hybrid. By end-user, the market is segmented into pharmaceutical and biopharmaceutical companies, contract development and manufacturing organizations (CDMOs/CMOs), biotechnology companies, academic and research institutes, food and beverage manufacturers (precision fermentation, alternative proteins), and other end-users (environmental biotechnology, industrial chemicals). By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Machine Learning (ML) and Deep Learning |

| Natural Language Processing (NLP) |

| Computer Vision |

| Digital Twin and Simulation AI |

| Reinforcement Learning |

| Generative AI |

| Other AI Technologies (Federated Learning, Physics-Informed Neural Networks, Hybrid AI) |

| Software |

| Hardware |

| Services |

| Process Optimization and Control |

| Quality Control and Assurance |

| Predictive Maintenance |

| Drug Discovery and Development Support |

| Manufacturing Execution and Automation |

| Supply Chain Optimization and Demand Forecasting |

| Regulatory Compliance and Documentation |

| Other Applications |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Pharmaceutical and Biopharmaceutical Companies |

| Contract Development and Manufacturing Organizations (CDMOs/CMOs) |

| Biotechnology Companies |

| Academic and Research Institutes |

| Food and Beverage Manufacturers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By AI Technology | Machine Learning (ML) and Deep Learning | |

| Natural Language Processing (NLP) | ||

| Computer Vision | ||

| Digital Twin and Simulation AI | ||

| Reinforcement Learning | ||

| Generative AI | ||

| Other AI Technologies (Federated Learning, Physics-Informed Neural Networks, Hybrid AI) | ||

| By Offering | Software | |

| Hardware | ||

| Services | ||

| By Application | Process Optimization and Control | |

| Quality Control and Assurance | ||

| Predictive Maintenance | ||

| Drug Discovery and Development Support | ||

| Manufacturing Execution and Automation | ||

| Supply Chain Optimization and Demand Forecasting | ||

| Regulatory Compliance and Documentation | ||

| Other Applications | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By End User | Pharmaceutical and Biopharmaceutical Companies | |

| Contract Development and Manufacturing Organizations (CDMOs/CMOs) | ||

| Biotechnology Companies | ||

| Academic and Research Institutes | ||

| Food and Beverage Manufacturers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Which application area leads revenue generation?

Process Optimization and Control led with 39.17% share in 2025 because it directly affects yield, quality consistency, and cycle time.

Which region is growing the fastest through 2031?

Asia-Pacific is the fastest-growing region with a 15.45% CAGR, supported by policy backing and expanding biomanufacturing capacity.

Why are on-premise deployments still gaining traction if cloud leads overall adoption?

On-premise solutions are growing faster at 12.96% CAGR because GMP documentation controls, data sovereignty, and internal security needs still matter in regulated environments.

Which end-user group is expected to grow the fastest?

CDMOs and CMOs are projected to grow the fastest at a 12.75% CAGR as sponsors increasingly demand AI-enabled technology transfer and digital process visibility.

What is the biggest barrier to wider adoption across production sites?

Fragmented data infrastructure remains the main barrier because disconnected instruments and inconsistent data formats make model training, transfer, and validation harder across sites.

Page last updated on: