AI In Operating Room Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.45 Billion |

| Market Size (2031) | USD 8.89 Billion |

| Growth Rate (2026 - 2031) | 29.34% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

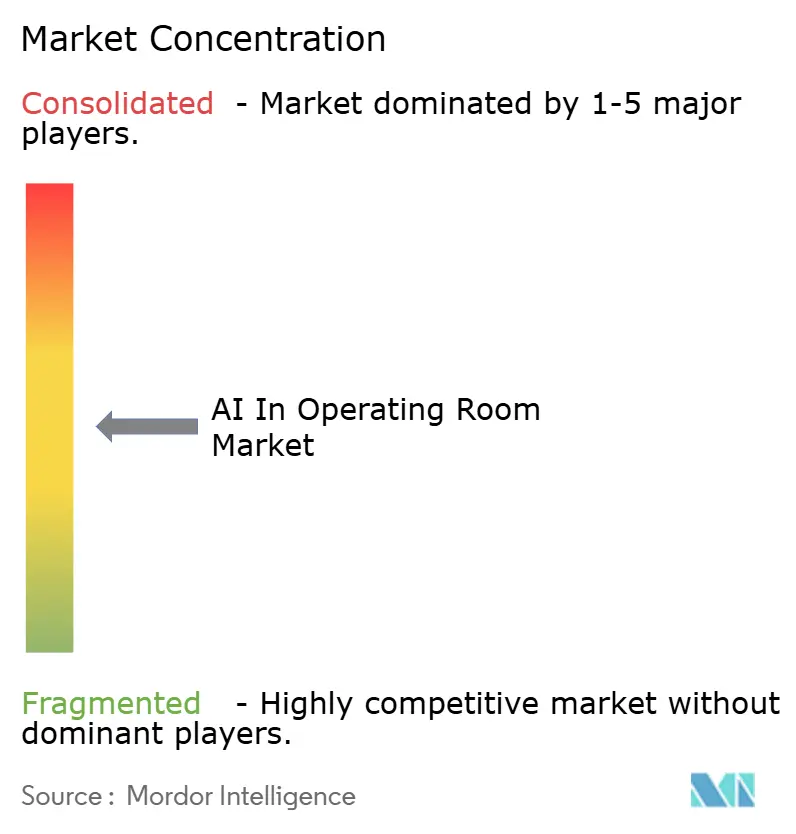

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Operating Room Market Analysis by Mordor Intelligence

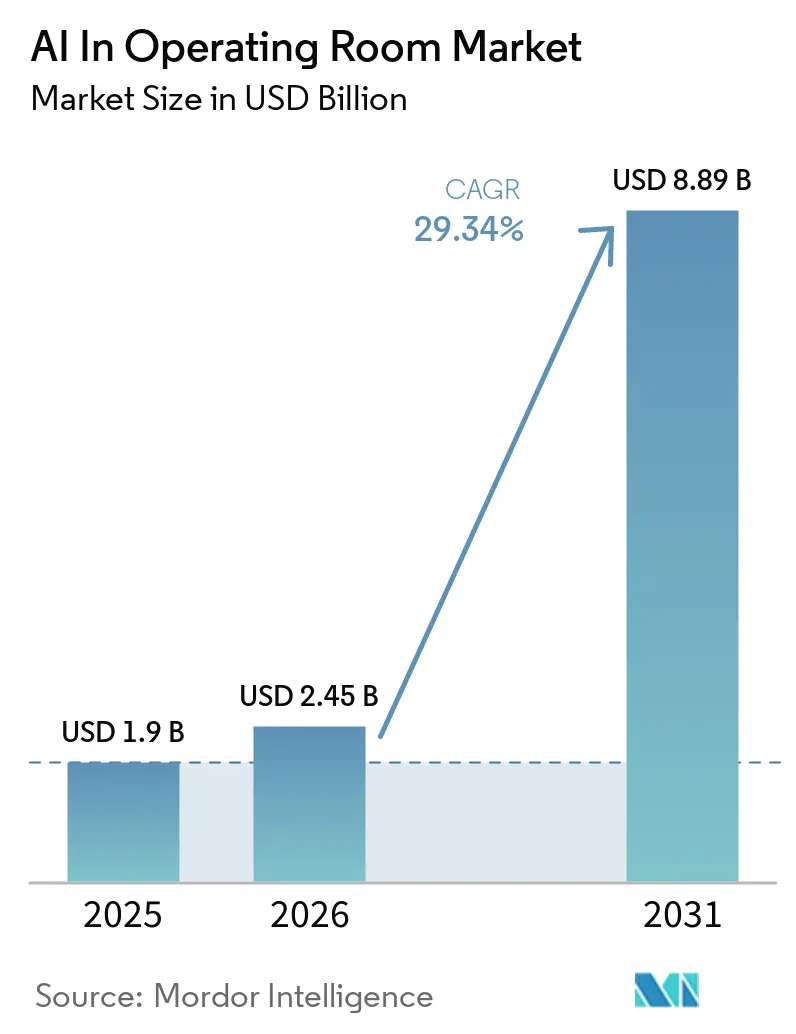

The AI In Operating Room Market size is expected to increase from USD 1.9 billion in 2025 to USD 2.45 billion in 2026 and reach USD 8.89 billion by 2031, growing at a CAGR of 29.34% over 2026-2031.

Surgical teams are increasingly adopting AI tools for planning, intraoperative execution, and post-procedure review, driving faster growth in the AI in operating room market compared to overall hospital IT spending. The UK recorded 36,209 robotic surgical cases in 2024, with the NHS targeting 90% of minimally invasive surgeries to be robotic within the next decade. The market is further supported by an active product clearance environment in North America and the use of multimodal surgical data to improve operating room models in scene perception and workflow understanding. These advancements are enhancing the efficiency and effectiveness of surgical procedures.

Key Report Takeaways

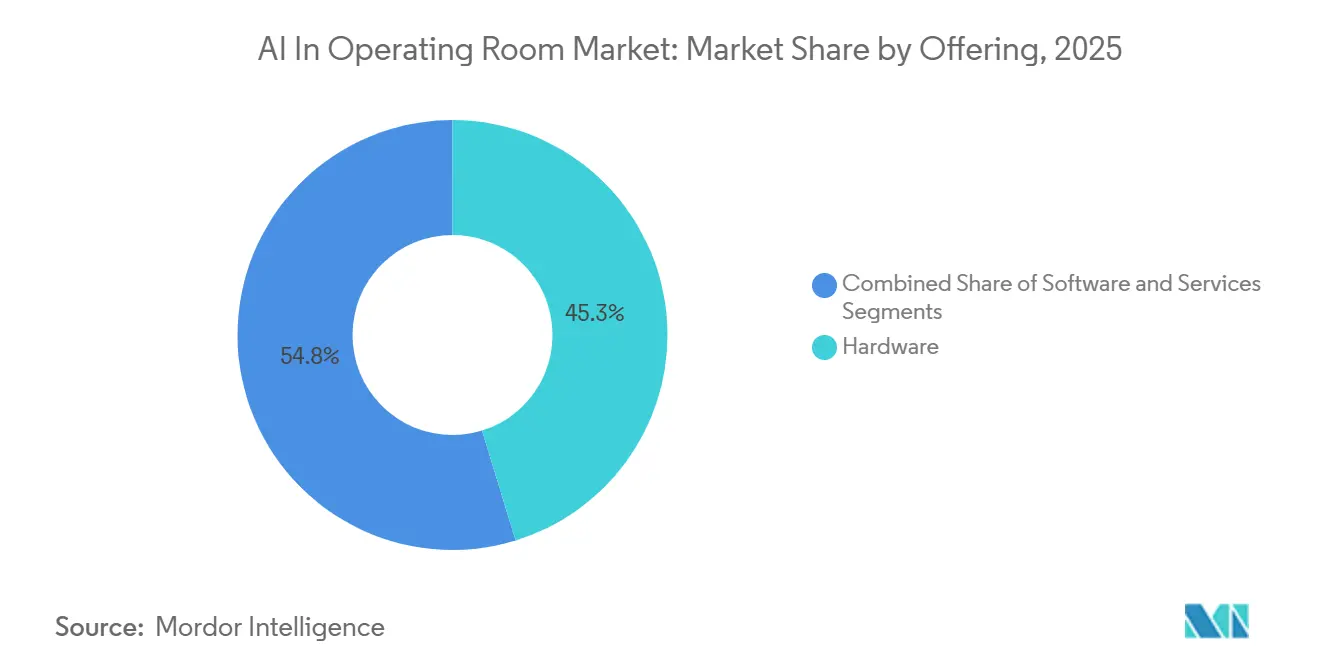

- By offering, hardware held 45.25% of revenue in 2025, while software is projected to expand at a 32.45% CAGR through 2031.

- By technology, machine learning and deep learning accounted for 48.56% of revenue in 2025, while augmented reality and virtual reality are projected to grow at a 33.24% CAGR through 2031.

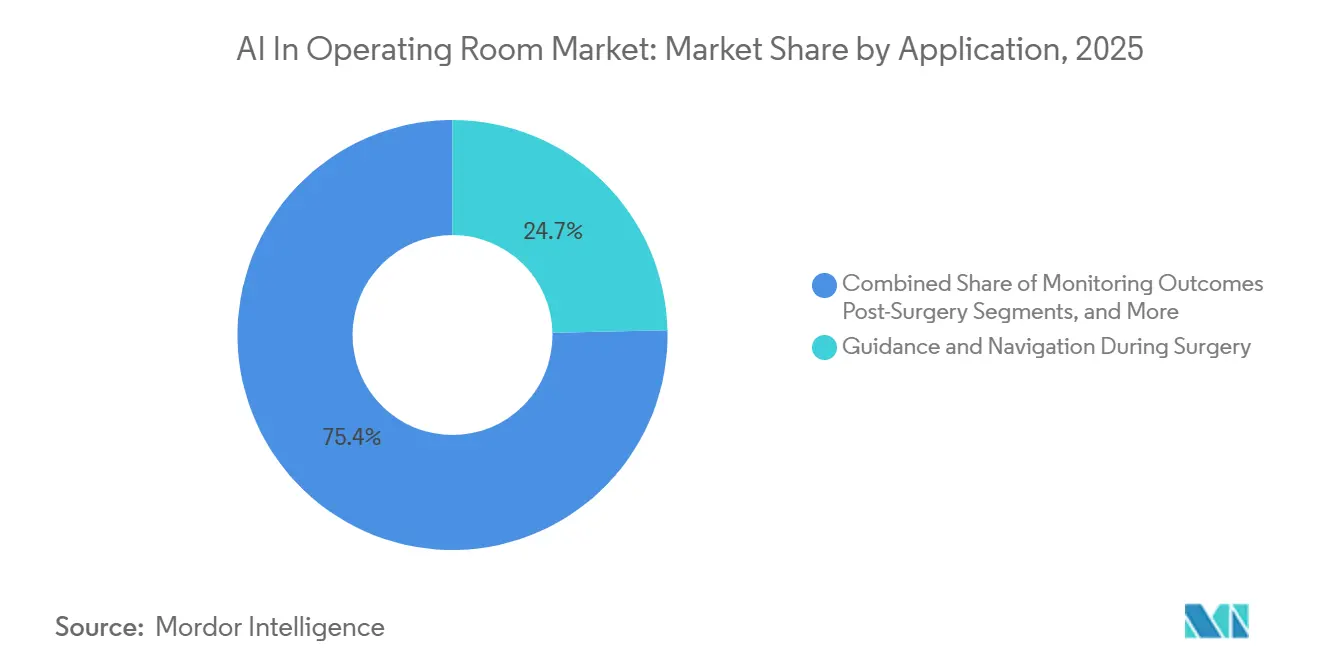

- By application, guidance and navigation during surgery represented 24.65% of the AI in operating room market size in 2025, while enhancing surgical workflow and efficiency is projected to advance at a 34.35% CAGR through 2031.

- By surgical specialty, general surgical practices held 44.35% of demand in 2025, while neurosurgical interventions are expected to grow at a 29.95% CAGR through 2031.

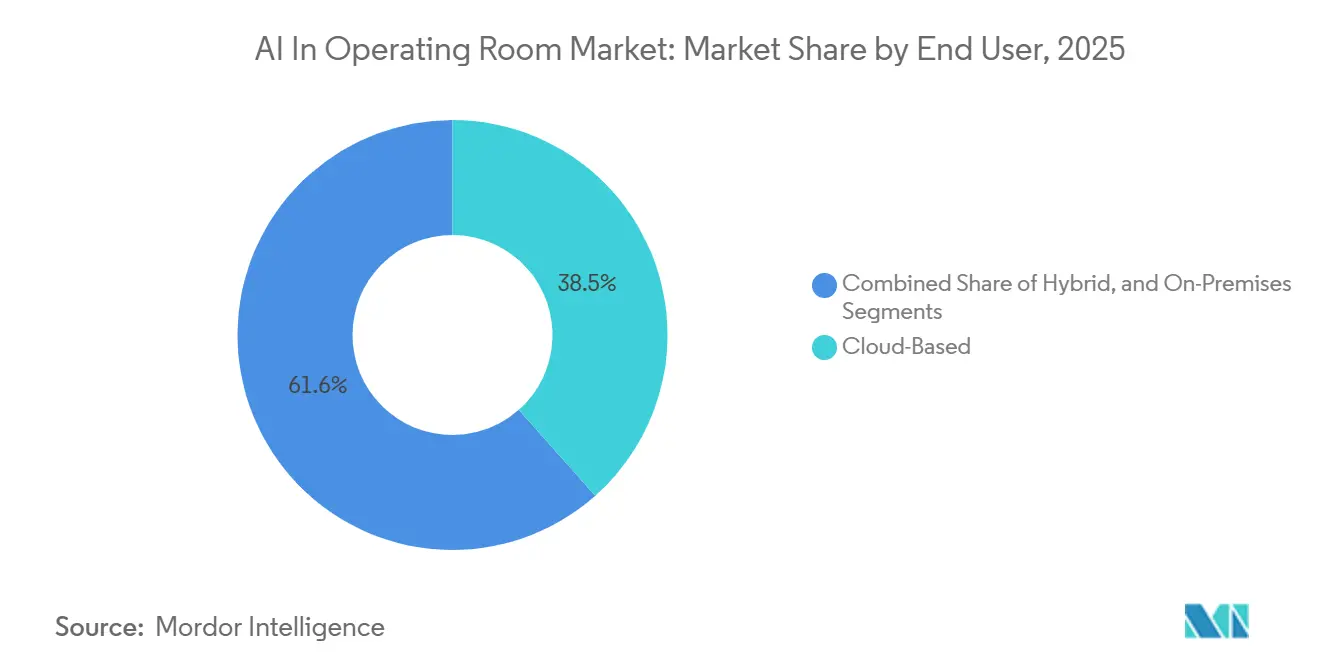

- By deployment mode, cloud-based solutions captured 38.45% of revenue in 2025, while on-premises deployments are projected to expand at a 32.65% CAGR through 2031.

- By end user, hospitals and surgical facilities held 58.72% of demand in 2025, while centers for ambulatory surgery are projected to grow at a 32.94% CAGR through 2031.

- By geography, North America accounted for 42.17% of the AI in operating room market share in 2025, while Asia-Pacific is projected to record the highest CAGR at 34.50% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Operating Room Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for minimally invasive and robotic-assisted surgeries | +6.0% | Global, strongest in North America, Europe, and East Asia | Medium term (2-4 years) |

| AI-driven intraoperative decision support and real-time imaging advancements | +5.5% | Global, with high concentration in North America and Western Europe | Short term (≤ 2 years) |

| Global surge in surgical volume amidst specialist surgeon shortages | +4.8% | Global, acute in Asia-Pacific, Middle East and Africa, and South America | Long term (≥ 4 years) |

| Imperatives for optimizing or workflow and enhancing operational efficiency | +4.5% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Broadened reimbursement policies for AI-enhanced medical procedures | +3.2% | North America and select European countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally Invasive and Robotic-Assisted Surgeries

The growing demand for minimally invasive surgeries is driving the AI in operating room market, as these procedures rely on imaging, precision, and workflow consistency. A 2025 study revealed that AI-robotic systems reduced operative times by 25%, intraoperative complications by 30%, and improved procedural precision by 40% compared to traditional methods.[1]Jack Ng Kok Wah, “The Rise of Robotics and AI-Assisted Surgery in Modern Healthcare,” Journal of Robotic Surgery, doi.org In 2024, the UK performed 36,209 robotic surgeries, indicating a shift from pilot programs to widespread adoption.[2]Donald Neil, Joseph Sebastian, and Giuseppe Preziosi, “National Adoption of Robotic-Assisted Surgery in the United Kingdom: A Decade of Growth, Distribution and Speciality Trends (2014-2024),” Surgical Endoscopy, doi.org As more procedures are conducted, annotated surgical data enhances AI models, creating a feedback loop that simplifies robotic system use and expands adoption.

AI-Driven Intraoperative Decision Support and Real-Time Imaging Advancements

Real-time AI decision support is emerging as a key growth driver for the AI in operating room market. A validated AI system for laparoscopic liver surgery processed video at 19.2 frames per second with 89% phase recognition accuracy and 91% phase classification. Another study demonstrated AI's ability to predict perfusion during colorectal surgery with 0.98 recall within 13 seconds.[3]Zi-Yang Peng, et al., “Development of an AI-Driven Digital Assistance System for Real-Time Safety Evaluation and Quality Control in Laparoscopic Liver Surgery,” Frontiers in Oncology, frontiersin.org In head and neck tumor surgeries, hyperspectral imaging with deep learning achieved 0.98 classification accuracy in under 10 minutes. These advancements enable standardized image interpretation and faster decision-making, reducing reliance on slower methods in critical cases.

Global Surge in Surgical Volume Amidst Specialist Surgeon Shortages

The AI in operating room market is supported by the growing gap between surgical demand and specialist availability. A 2025 analysis projected a shortage of 23,300 neurosurgeons globally, with over half of countries falling below target density by 2030. In 2022, the COSECSA region of Africa reported a surgeon density of 0.59 per 100,000 population, despite workforce growth since 2015. AI tools address this gap by automating anatomy recognition, phase tracking, and documentation, enabling specialists to manage more cases. Hospitals increasingly view surgical AI as a capacity solution rather than just a technological upgrade.

Imperatives for Optimizing OR Workflow and Enhancing Operational Efficiency

Hospitals are adopting AI to enhance operating room efficiency without increasing staff. AdventHealth Celebration improved on-time first case starts from 61.9% to 78% and reduced turnover times in select service lines using AI computer vision. Operating room delays impact case capacity, labor costs, and surgeon schedules, making AI tools essential for identifying bottlenecks, tracking workflow deviations, and optimizing resource use. The AI in operating room market benefits from these operational improvements, particularly in large hospitals where small changes can significantly increase annual procedure capacity.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Elevated capital expenditures and overall system ownership costs | -2.5% | Global, acute in emerging Asia-Pacific, Middle East and Africa, and South America | Long term (≥ 4 years) |

| Challenges in data privacy, cybersecurity, and system interoperability | -1.8% | Global, heightened in the European Union and in markets with fragmented EMR ecosystems | Short term (≤ 2 years) |

| Navigating regulatory complexities and validating AI devices | -1.5% | Europe and North America, with wider spillover into other regulated markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Elevated Capital Expenditures and Overall System Ownership Costs

Acquisition costs remain a significant barrier to AI adoption in operating rooms, particularly in smaller facilities. Robotic surgery platforms are 1.5 to 2 times more expensive per procedure than laparoscopic alternatives, with da Vinci system hardware costing between USD 0.5 million and USD 2.5 million per installation. Return on investment can take 3 to 5 years for high-volume centers and over 7 years for smaller hospitals. These costs, including software licensing, integration, validation, and training, slow adoption in community hospitals. Larger health systems with higher case volumes and multi-department usage are better positioned to absorb these expenses, driving faster market growth.

Challenges in Data Privacy, Cybersecurity, and System Interoperability

Data governance challenges hinder the AI in operating room market as surgical AI systems integrate video, imaging, vitals, and telemetry into a single workflow. Ambient AI tools without direct EHR integration risk patient data breaches, while multimodal data integration is complicated by diverse vendor equipment and non-harmonized infrastructure. These interoperability issues delay deployment, requiring vendors to invest in custom integrations. Additionally, regulatory requirements for documenting data governance, bias control, human oversight, and model risk increase costs, favoring larger operators with the resources to manage compliance and cybersecurity effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Hardware Anchors Revenue, Software Defines the Long-Term Value Stack

In 2025, hardware contributed 45.25% of segment revenue, maintaining its position as the leading offering in the AI-driven operating room market. This was driven by investments in robotic surgical consoles, imaging systems, and edge computing units essential for intraoperative AI functions. Hospitals prioritize these purchases as foundational for digital surgery programs, with many software tools relying on installed hardware. While software adoption is growing, hardware remains critical due to its role in enabling integrated workflow solutions.

Software is projected to grow at a 32.45% CAGR through 2031, signaling a shift in value creation. Vendor-neutral software layers are gaining traction, enabling integration across diverse equipment fleets and reducing upfront costs. Software also allows vendors to update models, add workflow modules, and enhance performance through continuous learning. As hospitals demand implementation support, services like integration and training are expanding, driving a transition toward recurring software and service contracts.

By Technology: Machine Learning Leads, Foundation Models Redefine the Competitive Horizon

Machine learning and deep learning held 48.56% of the technology segment in 2025, leading the AI-driven operating room market. Their dominance reflects advancements in surgical phase recognition, anatomy segmentation, and intraoperative risk prediction. These technologies are well-suited for operating room tasks and have demonstrated measurable clinical and operational benefits, supporting their adoption in hospital procurement.

Foundation models are redefining capabilities in this segment, with purpose-built surgical data enhancing performance. Augmented reality and virtual reality are forecast to grow at a 33.24% CAGR through 2031, driven by navigation overlays and simulation tools. The market is evolving, with machine learning driving current revenues while foundation models and AR/VR tools shape future differentiation, expanding competition beyond hardware.

By Application: Navigation Holds the Largest Share, Workflow Enhancement Accelerates Fastest

Guidance and navigation accounted for 24.65% of application revenue in 2025, making it the largest use case in the AI-driven operating room market. Navigation tools offer immediate clinical value by aiding anatomy localization, trajectory planning, and reducing repeat imaging. Their adoption is strong in spine, cranial, and minimally invasive procedures due to their impact on precision and workflow consistency.

Workflow enhancement is expected to grow at a 34.35% CAGR through 2031, driven by operational gains in scheduling, turnover, and documentation. Hospitals are adopting AI tools for perioperative planning and risk assessment, improving predictions for complications. Training and simulation are also expanding as health systems prepare staff for AI-supported environments, broadening the market's scope.

By Surgical Specialty: General Surgery’s Volume Base Meets Neurosurgery’s Precision Premium

General surgery captured 44.35% of specialty demand in 2025, leading the AI-driven operating room market. High procedure volumes in general surgery generate reusable data for model training, accelerating product development and clinical adoption. This makes general surgery a key entry point for AI platforms before expanding into specialized fields.

Neurosurgery is forecast to grow at a 29.95% CAGR through 2031, driven by the need for precision and the complexity of neural anatomy. AI-augmented workflows are improving outcomes, such as reducing unnecessary re-biopsies, addressing the global shortage of neurosurgeons, and enhancing procedural accuracy.

By Deployment Mode: Cloud-Based Leads Today, On-Premises Grows Fastest Tomorrow

Cloud-based deployments accounted for 38.45% of revenue in 2025, leading the AI-driven operating room market. Cloud environments support centralized analytics, multi-site access, and frequent software updates, simplifying coordination for multi-location health systems. These benefits drive strong adoption despite concerns about security and latency.

On-premises deployments are projected to grow at a 32.65% CAGR through 2031, reflecting the need for real-time decision support and data security. Hospitals are increasingly adopting on-premises setups for intraoperative tasks that cannot tolerate network delays, driving demand for hybrid solutions.

By End User: Hospitals Anchor Demand, Ambulatory Centers Accelerate

Hospitals and surgical facilities held 58.72% of demand in 2025, dominating the AI-driven operating room market. Their leadership is attributed to better capital access, clinical specialization, and infrastructure for imaging integration and staff training. Academic and tertiary centers play a significant role in shaping product design and early adoption.

Ambulatory surgery centers are expected to grow at a 32.94% CAGR through 2031, driven by the need for better utilization and scheduling as procedures shift to outpatient settings. AI tools are being adopted for anesthesia risk prediction, prior authorization, and perioperative coordination, supporting their rapid growth.

Geography Analysis

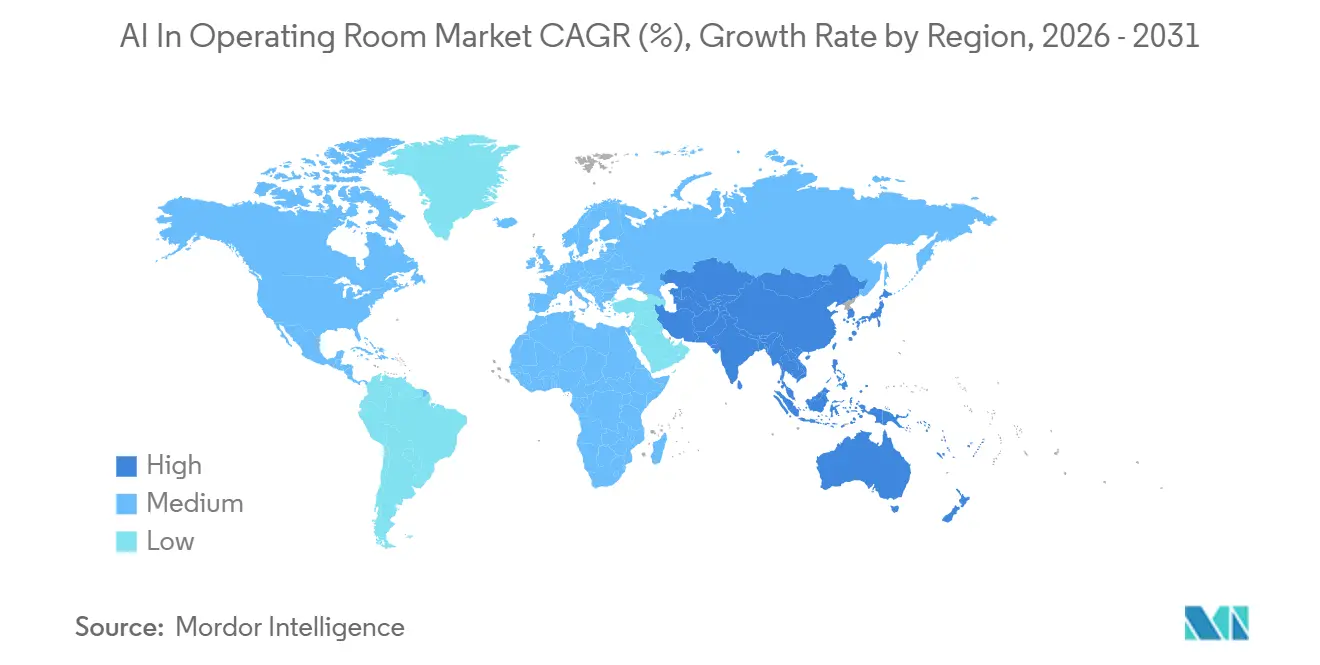

In 2025, North America commanded a dominant 42.17% share of the AI in operating room market, solidifying its position as the leading regional segment. This leadership stems from a large installed base of robotic systems, strong hospital technology budgets, and consistent regulatory approvals enabling commercial rollouts. The U.S. drives growth with expanding robotic procedure adoption across specialties and hospitals' ability to integrate connected surgical platforms. Canada and Mexico, though smaller markets, benefit from modernization efforts and growing cross-border clinical collaborations.

Asia-Pacific is set to outpace all regions, boasting a projected CAGR of 34.50% through 2031. Growth is driven by hospital modernization, a widening specialist shortage, and pressure to enhance surgical productivity. China leverages high procedural volumes and supportive policies for local platform development. India sees rapid adoption of surgical robotics and AI tools in urban hospitals, while Japan and South Korea contribute with advanced digitalization and investments in precision technologies.

Europe holds strategic importance in the AI in operating room market, but adoption faces challenges from stringent regulatory requirements. The EU AI Act and medical device rules increase documentation standards, affecting time to market. Despite this, Germany, France, the U.K., Italy, and Spain lead regional demand through surgical digitization and strong clinical interest. The Middle East, Africa, and South America, though in early stages, offer growth potential as health systems aim to improve access, training, and operating room efficiency.

Competitive Landscape

In the AI in operating room market, core surgical platforms are moderately consolidated, while software, analytics, and workflow applications remain fragmented. Leading medtech companies such as Intuitive Surgical, Medtronic, Stryker, and Johnson & Johnson dominate installed systems, procedure-linked ecosystems, and hospital relationships. Their established hardware presence supports navigation, imaging, robotics, and data capture, enabling hospitals to integrate AI capabilities through existing vendors. The absence of a single company controlling all application layers creates opportunities for specialized software providers.

Moves in 2025 and 2026 highlight the evolving competition in the AI in operating room market. Medtronic expanded its Stealth AXiS platform to include spine, cranial, and ENT workflows, strengthening its integrated planning, navigation, and robotics capabilities. Proprio advanced its position with multiple FDA clearances for its Paradigm AI platform, enhancing its role in spine and neuro workflows and enabling richer multimodal data generation. Johnson & Johnson’s investment in Distalmotion reflects its focus on modular robotic systems adaptable to both ambulatory and hospital settings. These developments demonstrate that competition extends beyond hardware to software innovation, workflow integration, and surgical data optimization.

AI-native firms are carving out significant niches, targeting areas where traditional device manufacturers have invested less. Companies like Caresyntax, DeepOR, and Theator focus on video intelligence, edge-to-cloud analytics, and workflow optimization across diverse device platforms. The competitive landscape is also shaped by multimodal foundation models and pre-training frameworks, which highlight the value of specialized surgical data as a competitive advantage. Future leadership in the AI in operating room market will depend on data quality, update speed, interoperability, and regulatory readiness across a broader software ecosystem.

AI In Operating Room Industry Leaders

Intuitive Surgical, Inc.

Medtronic plc

Brainlab AG

Johnson & Johnson (Ethicon)

Activ Surgical, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ZETA Surgical's AI-powered Zeta Navigation System received FDA 510(k) clearance for neurosurgical procedures, including brain tumor biopsies and hydrocephalus treatment. A 15-patient trial demonstrated ideal placements with a median setup time under 3 minutes, and a large-scale commercial pilot is planned for 2026 to expand its use to community hospitals.

- March 2026: Medtronic received FDA clearance for the Stealth AXiS surgical system, extending its spine-cleared platform to cranial and ENT procedures. The system integrates AI-based brain mapping and intraoperative ultrasound, enhancing its AiBLE ecosystem for soft-tissue and cranial surgeries.

- February 2026: Medtronic's Stealth AXiS platform, the first to unify AI-based planning, navigation, and robotics for spine surgeries, secured FDA clearance. Its LiveAlign feature eliminates repeated imaging steps and supports use in both hospitals and ambulatory surgery centers.

- February 2026: Proprio achieved its fourth consecutive FDA clearance for the Picasso radiation-free registration feature within its Paradigm AI platform. The system is being adopted by Duke Health and UW Medicine to build a multimodal surgical dataset for AI model training.

- January 2026: Johnson & Johnson made a strategic investment in Distalmotion following its USD 150 million Series G raise in November 2025. The Dexter robotic platform is positioned for ambulatory surgery center deployments, diversifying J&J's robotics portfolio beyond the OTTAVA platform.

Global AI In Operating Room Market Report Scope

As per the scope of the report, AI in the Operating Room (OR) refers to the integration of smart algorithms, machine learning, and robotics into surgical workflows. It is designed to assist medical teams before, during, and after procedures by analyzing massive amounts of clinical data to improve surgical precision, patient safety, and overall OR efficiency.

The AI in Operating Room Market is segmented by offering, technology, application, surgical specialty, deployment mode, end-user, and geography. By offering, the market includes software, hardware, and services. By technology, the market is segmented into machine learning and deep learning, generative AI and foundation models, natural language processing and knowledge graphs, computer vision and image recognition, augmented reality (AR) and virtual reality (VR), surgery's edge AI and IoT integration, and robotic process automation (RPA) in medical settings. By application, the market is categorized into guidance and navigation during surgery, planning and risk assessment before surgery, monitoring outcomes post-surgery, enhancing surgical workflow and efficiency, and training and simulation for surgeons. By surgical specialty, the market is segmented into general surgical practices, orthopedic and spine procedures, urological surgeries, cardiac and cardiothoracic operations, neurosurgical interventions, gastrointestinal and colorectal procedures, gynecological surgeries, ENT and eye operations, and others. By deployment mode, the market is segmented into cloud-based, hybrid, and on-premises. By end-user, the market is segmented into hospitals and surgical facilities, centers for ambulatory surgery (ASCs), specialized medical clinics, academic institutions and research bodies, and facilities for surgical training and AI health technology centers. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Software |

| Hardware |

| Services |

| Machine Learning and Deep Learning |

| Generative AI and Foundation Models |

| Natural Language Processing and Knowledge Graphs |

| Computer Vision and Image Recognition |

| Utilization of Augmented Reality (AR) / Virtual Reality (VR) |

| Surgery's Edge AI & IoT Integration |

| Robotic Process Automation (RPA) in Medical Settings |

| Guidance & Navigation During Surgery |

| Planning & Risk Assessment Before Surgery |

| Monitoring Outcomes Post-Surgery |

| Enhancing Surgical Workflow & Efficiency |

| Training & Simulation for Surgeons |

| General Surgical Practices |

| Orthopedic & Spine Procedures |

| Urological Surgeries |

| Cardiac & Cardiothoracic Operations |

| Neurosurgical Interventions |

| Gastrointestinal & Colorectal Procedures |

| Gynecological Surgeries |

| ENT & Eye Operations |

| Others |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Hospitals & Surgical Facilities |

| Centers for Ambulatory Surgery (ASCs) |

| Specialized Medical Clinics |

| Academic Institutions & Research Bodies |

| Facilities for Surgical Training & AI Health Technology Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Software | |

| Hardware | ||

| Services | ||

| By Technology | Machine Learning and Deep Learning | |

| Generative AI and Foundation Models | ||

| Natural Language Processing and Knowledge Graphs | ||

| Computer Vision and Image Recognition | ||

| Utilization of Augmented Reality (AR) / Virtual Reality (VR) | ||

| Surgery's Edge AI & IoT Integration | ||

| Robotic Process Automation (RPA) in Medical Settings | ||

| By Application | Guidance & Navigation During Surgery | |

| Planning & Risk Assessment Before Surgery | ||

| Monitoring Outcomes Post-Surgery | ||

| Enhancing Surgical Workflow & Efficiency | ||

| Training & Simulation for Surgeons | ||

| By Surgical Speciality | General Surgical Practices | |

| Orthopedic & Spine Procedures | ||

| Urological Surgeries | ||

| Cardiac & Cardiothoracic Operations | ||

| Neurosurgical Interventions | ||

| Gastrointestinal & Colorectal Procedures | ||

| Gynecological Surgeries | ||

| ENT & Eye Operations | ||

| Others | ||

| By Deployment Mode | Cloud-Based | |

| Hybrid | ||

| On-Premises | ||

| By End User | Hospitals & Surgical Facilities | |

| Centers for Ambulatory Surgery (ASCs) | ||

| Specialized Medical Clinics | ||

| Academic Institutions & Research Bodies | ||

| Facilities for Surgical Training & AI Health Technology Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of AI in operating room activity worldwide?

The AI in operating room market size stands at USD 1.9 billion in 2026 and is forecast to reach USD 8.89 billion by 2031, reflecting a 29.34% CAGR over 2026-2031.

Which region leads adoption of AI tools in surgical settings?

North America led in 2025 with 42.2% share, supported by high hospital IT spending, strong robotic surgery penetration, and frequent regulatory clearances.

Which technology category is most widely used in surgical AI systems?

Machine learning and deep learning led with 48.17% share in 2025 because they already support core functions such as phase recognition, anatomy segmentation, and intraoperative prediction.

What is driving faster growth in surgical AI software than hardware?

Software is forecast to grow at 32.45% CAGR through 2031 because subscription delivery lowers upfront cost and lets hospitals add AI capability without making a full capital purchase first.

Why is neurosurgery becoming a major growth area for AI-assisted operating rooms?

Neurosurgical interventions are projected to expand at a 29.95% CAGR through 2031 because these procedures require high precision and face a well-documented global specialist shortage.

What is the biggest barrier to wider use of AI in the operating room?

High ownership cost remains the main barrier, since robotic platforms can cost 1.5 to 2 times more per procedure than laparoscopic alternatives and large installations can take years to pay back.

Page last updated on: