AI in Post-Market Surveillance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

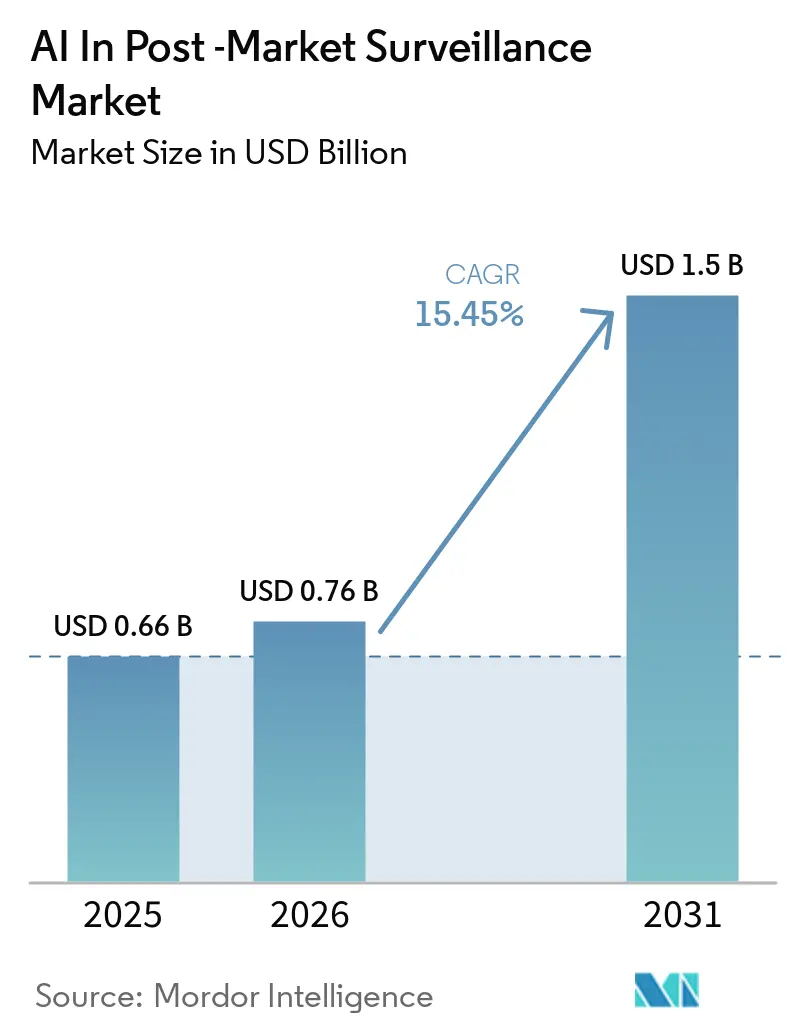

| Market Size (2026) | USD 0.76 Billion |

| Market Size (2031) | USD 1.5 Billion |

| Growth Rate (2026 - 2031) | 15.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI in Post-Market Surveillance Market Analysis by Mordor Intelligence

The AI in Post-Market Surveillance Market size was valued at USD 0.66 billion in 2025 and is estimated to grow from USD 0.76 billion in 2026 to reach USD 1.5 billion by 2031, at a CAGR of 15.45% during the forecast period (2026-2031).

Accelerating digital-first mandates from regulators, broader acceptance of real-world evidence, and the global transition to ICH E2B(R3) are together lifting platform demand as pharmacovigilance teams face swelling data volumes and tighter reporting clocks. Pharmaceutical license holders are streamlining adverse-event case intake with generative AI, while device manufacturers capitalize on EUDAMED’s vigilance module to build device-level safety analytics. Vendors are differentiating through explainability features that satisfy GxP validation and by offering hybrid deployments that reconcile data-residency rules in China and the European Union. Partnerships between software providers and contract research organizations have emerged as a dominant commercialization route, allowing mid-sized biotechnology firms to access enterprise-grade safety functionality without large fixed-cost burdens.

Key Report Takeaways

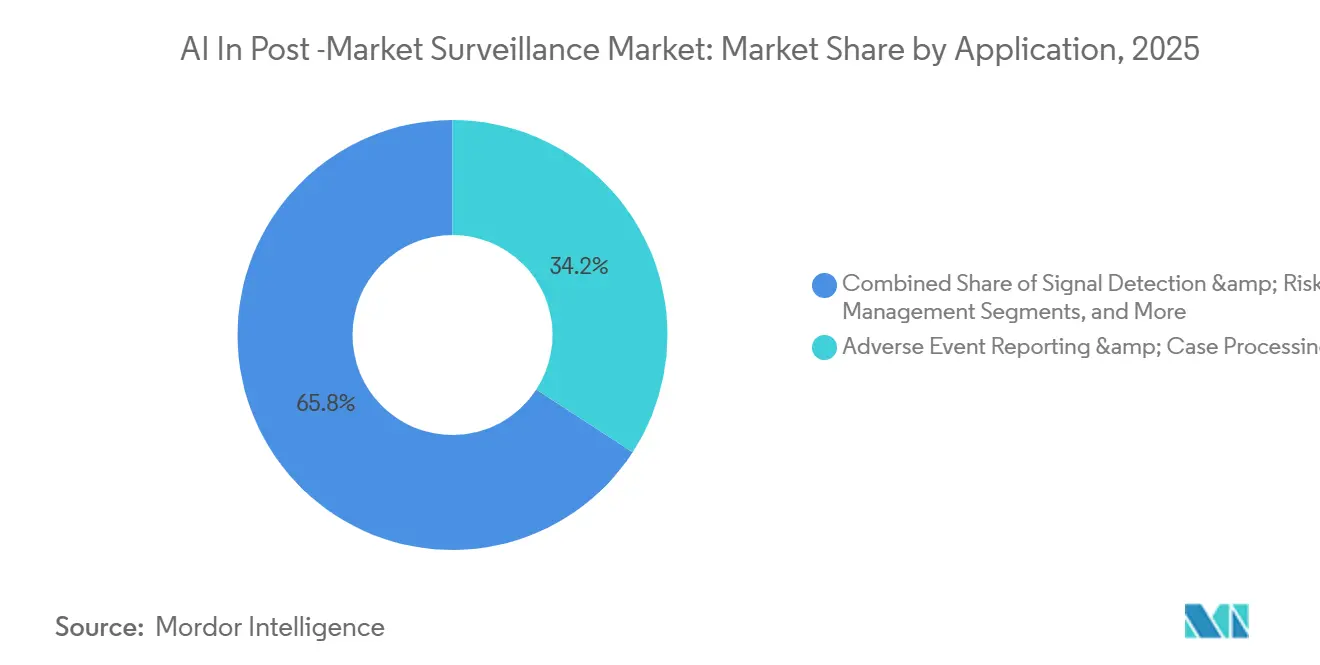

- By application, adverse event reporting & case processing commanded 34.18% of 2025 revenue, while signal detection & risk management are projected to grow at a 17.88% CAGR through 2031

- By end user, pharmaceutical companies held 41.67% of the 2025 share; biotechnology firms are projected to grow at a 18.15% CAGR to 2031 as lean teams embrace SaaS platforms.

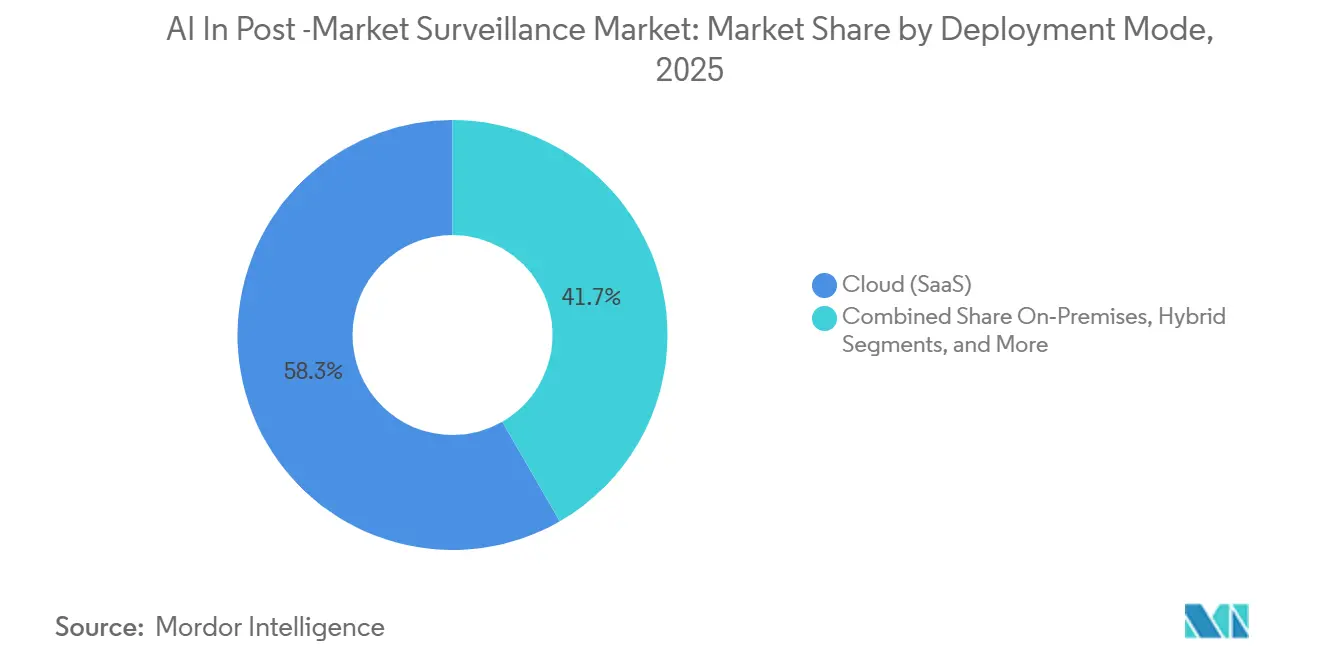

- By deployment mode, cloud captured 58.31% of 2025 installations, yet on-premises systems are projected to grow at 17.36% CAGR through 2031 because of regional data-sovereignty laws.

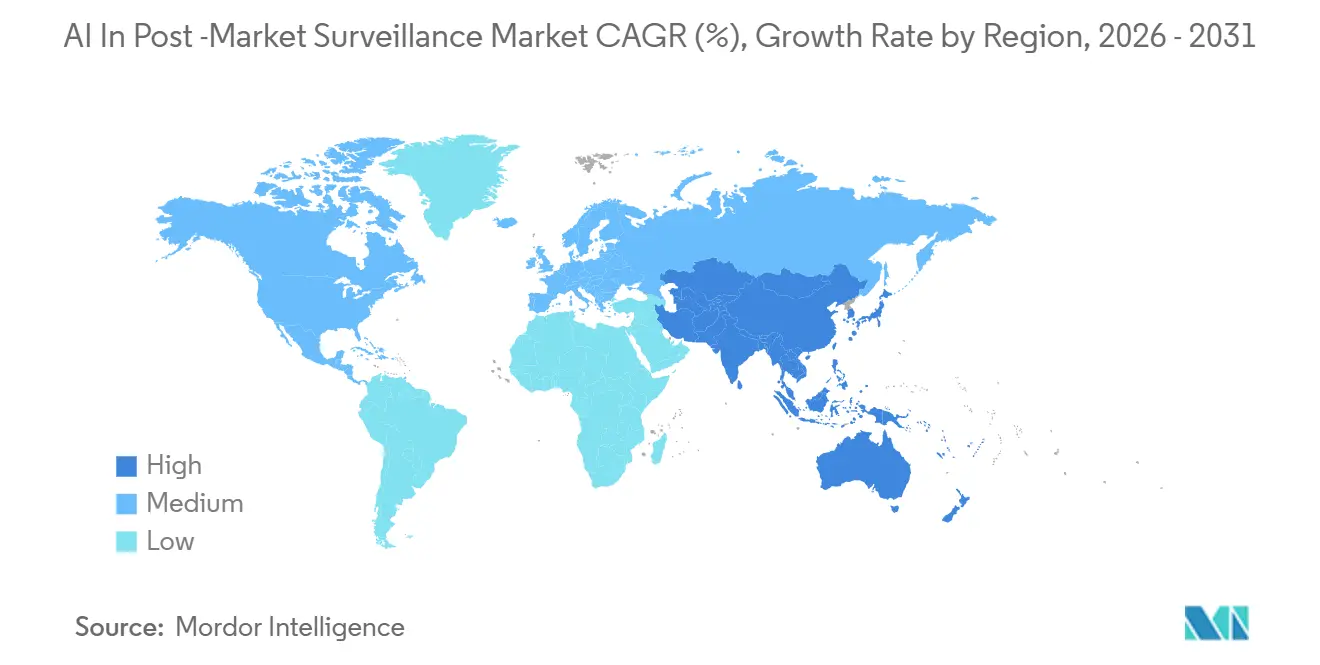

- By geography, North America led with 43.18% of 2025 revenue, while Asia-Pacific is on track for an 18.54% CAGR to 2031 on the back of China’s revised Pharmacovigilance Inspection Guidelines.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI in Post-Market Surveillance Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Regulatory mandates intensify PMS/PV digitization | 3.2% | Global, with North America & EU leading enforcement | Medium term (2-4 years) |

| Regulatory acceptance of RWE elevates analytics demand | 2.8% | North America, EU, APAC core markets | Long term (≥ 4 years) |

| Migration to ICH E2B(R3) standardizes structured safety data | 2.5% | Global, with staggered adoption across jurisdictions | Short term (≤ 2 years) |

| Cloud-first PV/PMS architectures reduce TCO and speed rollouts | 2.1% | North America, EU, APAC emerging markets | Medium term (2-4 years) |

| EUDAMED + UDI enable device-level field safety analytics | 1.9% | EU primary, spillover to APAC and MEA | Long term (≥ 4 years) |

| Validation frameworks for AI (ISPE GAMP AI) de-risk adoption | 1.6% | Global, with early uptake in North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Mandates Intensify PMS/PV Digitization

Health authorities are strengthening surveillance regulations as accelerated approvals shift evidence generation downstream. The FDA’s October 2026 ICH E2B(R3) deadline eliminates free-text narratives, a change that previously accounted for 60% of case-processing time at several firms.[1]U.S. Food and Drug Administration, “ICH E2B(R3) Implementation,” FDA.gov EMA’s electronic Periodic Safety Update Report requirement and the UK regulator’s 2024 medical-device guidance further highlight the non-compliance of manual workflows.[2]European Medicines Agency, “Real-World Evidence Guidance,” EMA.europa.eu China’s revised Pharmacovigilance Inspection Guidelines have assigned Marketing Authorization Holder responsibilities, driving a 40% increase in cloud safety-platform purchases in 2025.[3]National Medical Products Administration, “Pharmacovigilance Inspection Guidelines,” NMPA.gov.cn Collectively, these mandates establish a digital baseline that only AI-enabled systems can meet within statutory timelines.

Regulatory Acceptance of RWE Elevates Analytics Demand

Real-world evidence now directly influences label updates and benefit-risk assessments, encouraging companies to integrate AI into their analytics frameworks. The FDA Sentinel System utilized natural-language processing in 2025 to extract adverse events from 700 million patient records, reducing false-negative signal rates by 30%. EMA’s 2024 guidance permits sponsors to apply machine-learning models for confounding adjustments, provided they disclose validation methods.[4]International Council for Harmonisation, “ICH E2D(R1): Post-Approval Safety Data Management,” ICH.org Sanofi’s Project ARTEMIS, which processes 700,000 cases annually, achieved 15% cost savings in 2025 and aims for 50% by 2027 by combining AI-driven case intake with real-world evidence analytics.

Migration to ICH E2B(R3) Standardizes Structured Safety Data

The E2B(R3) schema introduces 1,200 data fields and nested structures, enabling individual case safety reports to be fully machine-readable. The FDA’s October 2026 implementation follows EMA’s 2022 mandate, requiring sponsors to manage dual-format pipelines during a four-year transition period. Oracle’s Argus Safety 2026.1.01 release includes Smart Duplicate Search, which identifies cross-format duplicates with 94% precision, eliminating a manual bottleneck that previously affected up to 20% of incoming reports. The updated ICH E2D(R1) guideline has expanded the definition of reportable sources to include digital-health applications, increasing data inflows that AI systems must process.[5]International Society for Pharmaceutical Engineering, “ISPE GAMP AI Guide for Life Sciences,” ISPE.org

Cloud-First PV/PMS Architectures Reduce TCO and Speed Rollouts

SaaS delivery is replacing on-premises systems as safety teams prioritize faster refresh cycles and reduced total cost of ownership. Veeva Vault Safety 26R1 introduced Case Intake Agent, reducing average processing time from 45 minutes to 8 minutes. EVERSANA’s ORCHESTRATE PV lowers lifecycle costs by 40% by eliminating server provisioning and patch management tasks, which traditionally consume one-third of pharmacovigilance IT budgets. Multinational companies, such as MSD, decommissioned 10 legacy databases after transitioning to Veeva’s unified global instance, reducing reconciliation efforts for 15% of cases.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| GxP validation and explainability burden for AI models | -2.3% | Global, with strictest enforcement in North America & EU | Medium term (2-4 years) |

| Interoperability gaps and staggered E2B(R3) readiness | -1.8% | Global, with acute friction at North America-EU interface | Short term (≤ 2 years) |

| LLM False positives/generalization risks require human review | -1.5% | Global, with heightened scrutiny in regulated submissions | Long term (≥ 4 years) |

| Fragmented device PMS registries slow harmonized analytics | -1.2% | EU primary, spillover to APAC and MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI Models Face GxP Validation and Explainability Challenges

The ISPE GAMP AI guide, a comprehensive 290-page document, expands traditional computer-system validation to include model training, drift monitoring, and interpretability. This development increases entry barriers for smaller biotech firms. The FDA's "Good AI Practice" framework, set to be implemented in January 2026, requires sensitivity analyses and external validation for high-stakes predictions, potentially delaying deployment timelines by several months. Additionally, CIOMS guidance mandates human review of every AI-generated safety signal before submission, limiting automation to approximately 70% of the workflow for end-to-end straight-through processing.

Interoperability Challenges and E2B(R3) Readiness Delays

A four-year gap between EMA and FDA mandates requires sponsors to manage dual pipelines, significantly increasing IT complexity. Despite the availability of translation tools, a 2025 survey indicated that 40% of firms faced quality issues when converting legacy cases, particularly with nested device-problem hierarchies. Moreover, Japan’s J-DREAMS database does not support direct E2B(R3) uploads, necessitating manual reconciliation and adding up to five business days per case.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Case Processing Still Leads While Signal Detection Accelerates

In 2025, Adverse Event Reporting & Case Processing accounted for 34.18% of the AI-driven post-market surveillance revenue, representing the largest market share. This segment grew as companies efficiently converted unstructured data such as emails, call-center transcripts, and physician letters into structured E2B(R3) messages, meeting regulatory requirements. Meanwhile, Signal Detection & Risk Management is projected to grow at a strong 17.88% CAGR through 2031, reflecting a shift toward proactive risk management as routine case intake processes become automated. The market for signal analytics is expanding as organizations integrate natural-language models to analyze spontaneous reports, EHR extracts, and literature for early safety signals. For example, advancements in duplicate-case identification have significantly reduced per-case costs, enhancing operational efficiency.

By End User: Pharmaceutical Majors Dominate While Biotech Surges

In 2025, pharmaceutical companies represented 41.67% of the market, driven by large-scale consolidations that streamlined operations and reduced manual reconciliation efforts. At the same time, biotechnology firms are expected to grow at an 18.15% CAGR through 2031, the highest among end users. This growth is attributed to smaller biotech teams adopting enterprise-grade safety solutions without requiring extensive IT infrastructure. This trend is expanding the market's reach, particularly among emerging biopharma companies.

Medical device manufacturers face distinct regulatory requirements under the EU Medical Device and In-Vitro Diagnostic Regulations, including post-market clinical follow-up studies that feed data directly into EUDAMED. However, fragmented national registries complicate cross-border analytics, resulting in slower spending growth compared to pharmaceutical companies.

By Deployment Mode: Cloud Remains Predominant, Yet On-Premises Rebounds

In 2025, cloud installations accounted for 58.31% of deployments, driven by SaaS solutions that reduced upfront costs and accelerated multi-region launches. While cloud-based systems are expected to maintain a significant market share, on-premises solutions are projected to grow at a 17.36% CAGR through 2031. Regulatory requirements for localized storage of sensitive patient data are influencing architecture choices, leading to the adoption of hybrid models that combine secure data storage with efficient analytics. For instance, AI-driven innovations in cloud-native systems have significantly reduced processing times, while cloud solutions have eliminated resource-intensive tasks associated with on-premises systems, optimizing operational budgets.

Geography Analysis

In 2025, North America accounted for 43.18% of the revenue, driven by the FDA's ICH E2B(R3) deadline in October 2026 and the expansion of the Sentinel System to include 700 million patient records. The region benefits from the Emerging Drug Safety Technology Program, which allows sponsors to pre-clear innovative AI models. This approach reduces the challenges of retrospective validation and accelerates platform adoption. U.S. sponsors are increasingly implementing real-world evidence pipelines that integrate EHR data, claims, and patient-generated health data. This integration increases both the volume and complexity of safety signals, requiring AI-driven triage.

Asia-Pacific is projected to achieve the fastest global CAGR of 18.54% through 2031. China's updated Pharmacovigilance Inspection Guidelines and mandatory data sovereignty regulations resulted in a 40% increase in on-premises platform agreements in 2025. Japan's expansion of the MID-NET database to cover 23 million patients enables device manufacturers to conduct post-market follow-ups without the need for new patient recruitment. This development reduces evidence-generation timelines from 18 months to just 6 months. Similarly, Australia and South Korea are establishing interconnected claims-EHR networks, creating significant opportunities for vendors to incorporate country-specific localization features.

Europe secured approximately one-third of the 2025 revenue, driven by the 2022 E2B(R3) mandate that prompted rapid modernizations. Under the Medical Device Regulation, device manufacturers face stringent post-market clinical follow-up requirements, which in turn expand the market size for AI in post-market surveillance across Europe. However, fragmented national device registries and varying health-data governance standards continue to hinder data consolidation, fostering the adoption of federated-analytics solutions. While the Middle East & Africa and South America collectively represent less than 10% of the revenue, they are expected to grow as cloud-native platforms overcome local IT infrastructure limitations.

Competitive Landscape

The market remains moderately fragmented, with the top four vendors, Veeva Systems, Oracle, IQVIA, and ArisGlobal, holding just under 50% of global revenue. Veeva's 26R1 release, featuring the integrated Case Intake Agent and Case Narrative Agent, has reduced case processing time to eight minutes, capturing market share from competitors lacking built-in large-language-model orchestration. Oracle strengthened its position with the introduction of Smart Duplicate Search in Argus Safety 2026.1.01, improving duplicate-detection precision to 94%. Meanwhile, IQVIA differentiates itself with Vigilance Detect’s cross-sponsor signal-detection network, leveraging its extensive longitudinal real-world data assets.

ArisGlobal reports an 80% efficiency improvement in MedDRA coding through AI-assisted term mapping, while EVERSANA targets mid-tier biotech with a comprehensive cloud solution that reduces total lifecycle costs by up to 40%. Emerging opportunities include providing explainability-as-a-service modules for smaller sponsors, implementing federated analytics that comply with data residency requirements, and developing hybrid deployments tailored to China's sovereignty regulations. Vendors that integrate safety, quality, and regulatory functions are gaining an advantage, as buyers increasingly prefer unified records and streamlined integrations.

AI in Post-Market Surveillance Industry Leaders

Oracle

Veeva Systems Inc.

IQVIA

Accenture

Cognizant

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Veeva Systems released Vault Safety 26R1, adding agentic AI for case intake and narrative generation, reducing per-case processing time from 45 minutes to 8 minutes.

- January 2026: The FDA issued Guiding Principles of Good AI Practice, establishing a risk-based credibility framework that includes external validation and counterfactual explanations for high-stakes predictions.

- October 2025: Oracle launched Argus Safety 2026.1.01, introducing Smart Duplicate Search with 94% precision and automated email intake.

- September 2025: ICH finalized E2D(R1), expanding post-approval safety data definitions to include digital platforms and mobile-health apps.

Global AI in Post-Market Surveillance Market Report Scope

As per the scope of the report, AI in Post-market Surveillance (PMS) is the use of artificial intelligence, machine learning, and natural language processing to proactively monitor the safety and performance of medical devices/drugs after they enter the market. It automates the analysis of large datasets (adverse events, patient data) to identify risks earlier, improve regulatory compliance, and shift from reactive to predictive safety management.

The AI in post-market surveillance market is segmented by application, end-user, and deployment mode. By application, the market includes adverse event reporting & case processing, signal detection & risk management, literature & social media monitoring, regulatory reporting & case submission (ICSR E2B(R3)), real-world evidence & safety analytics, and others. By end-user, the market is segmented into pharmaceutical companies, biotechnology companies, medical device manufacturers, CROs/BPOs & PV service providers, and regulatory authorities & notified bodies. By deployment mode, the market is categorized into cloud (SaaS), on-premises, and hybrid. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Adverse Event Reporting & Case Processing |

| Signal Detection & Risk Management |

| Literature & Social Media Monitoring |

| Regulatory Reporting & Case Submission (ICSR E2B(R3)) |

| Real-World Evidence & Safety Analytics |

| Others |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Medical Device Manufacturers |

| CROs/BPOs & PV Service Providers |

| Regulatory Authorities & Notified Bodies |

| Cloud (SaaS) |

| On-Premises |

| Hybrid |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Adverse Event Reporting & Case Processing | |

| Signal Detection & Risk Management | ||

| Literature & Social Media Monitoring | ||

| Regulatory Reporting & Case Submission (ICSR E2B(R3)) | ||

| Real-World Evidence & Safety Analytics | ||

| Others | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| Medical Device Manufacturers | ||

| CROs/BPOs & PV Service Providers | ||

| Regulatory Authorities & Notified Bodies | ||

| By Deployment Mode | Cloud (SaaS) | |

| On-Premises | ||

| Hybrid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the AI in post-market surveillance market by 2031?

The market is forecast to reach USD 1.5 billion by 2031, expanding at a 15.45% CAGR from 2026 to 2031.

Which application segment is growing fastest?

Signal Detection & Risk Management is poised for a 17.88% CAGR through 2031 as firms shift from reactive compliance to proactive risk mitigation.

Why are biotechnology companies increasing their adoption of AI safety platforms?

Lean biotech teams leverage SaaS solutions to meet Marketing Authorization Holder duties without the fixed costs of building in-house safety databases, propelling an 18.15% CAGR through 2031.

How do data-sovereignty laws influence deployment choices?

China’s Data Security Law and the EU’s Digital Operational Resilience Act compel on-premises or hybrid architectures that localize patient-level reports while routing computation to compliant clouds.

Which geography is expected to grow fastest, and why?

Asia-Pacific is set for an 18.54% CAGR to 2031, driven by China’s 2024 Pharmacovigilance Inspection Guidelines and Japan’s expansion of the MID-NET and J-DREAMS databases.

Page last updated on: