AI In Regulatory Affairs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.9 Billion |

| Market Size (2031) | USD 4.47 Billion |

| Growth Rate (2026 - 2031) | 18.65% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Regulatory Affairs Market Analysis by Mordor Intelligence

The AI In Regulatory Affairs Market size is projected to expand from USD 1.60 billion in 2025 and USD 1.9 billion in 2026 to USD 4.47 billion by 2031, registering a CAGR of 18.65% between 2026 to 2031.

Start-ups backed by venture capital and established life-sciences platforms are increasingly incorporating machine learning, knowledge graphs, and large language models into their regulatory information management suites. These suites handle various data types, including clinical study reports, manufacturing batch data, and safety signals. This trend is accelerating following the U.S. Food and Drug Administration's draft guidance on AI credibility issued in January 2025. Additionally, the European Medicines Agency's alignment with the FDA in 2026, adopting ten shared AI principles, provides the industry with a clear framework for development. Sponsors are opting for cloud infrastructure, preferring usage-based fees over the significant capital investment required for on-premise GPU stacks.[1]European Medicines Agency, “EMA and FDA set common principles for AI in medicine development,” ema.europa.eu Generative co-pilots are also transforming the drug application process, cutting authoring cycles from weeks to hours. Furthermore, there is increasing demand for proactive compliance analytics that predict labeling changes and anticipate health authority inquiries, helping to avoid approval delays.

Key Report Takeaways

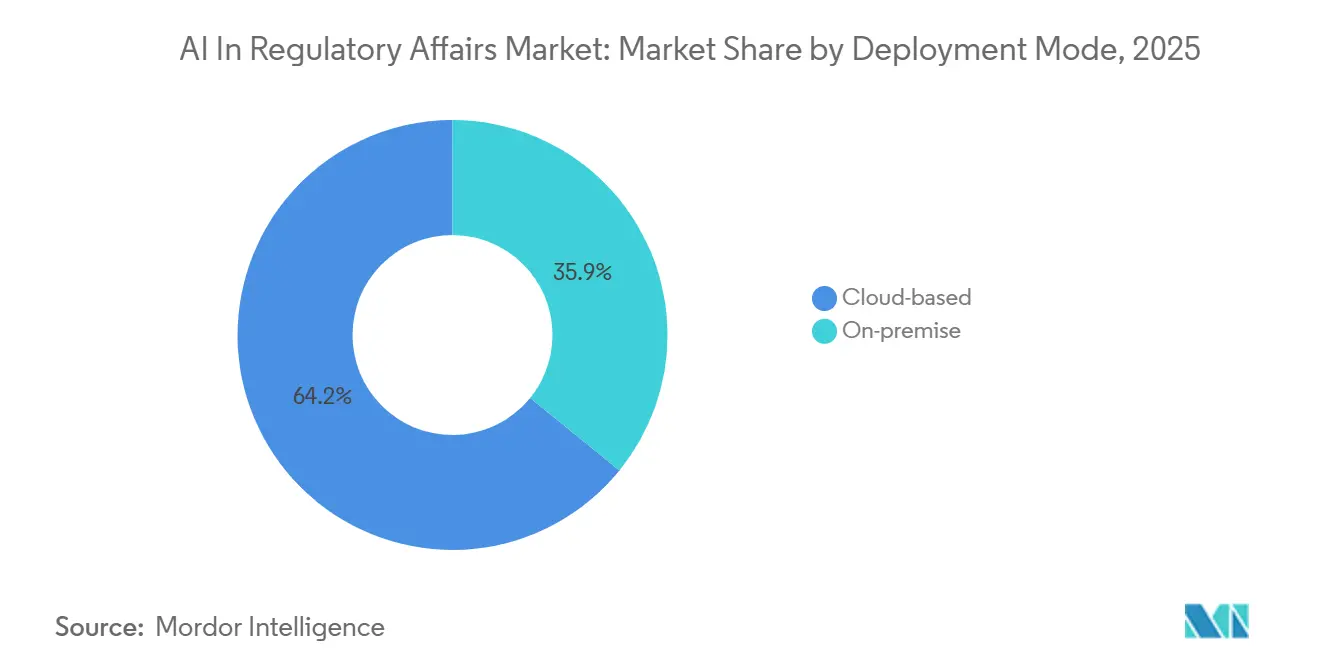

- By deployment mode, cloud solutions held 64.15% of the AI in regulatory affairs market share in 2025.

- By technology, knowledge graphs are projected to expand at a 21.00% CAGR between 2026-2031, the fastest among all technology categories in the AI in regulatory affairs market.

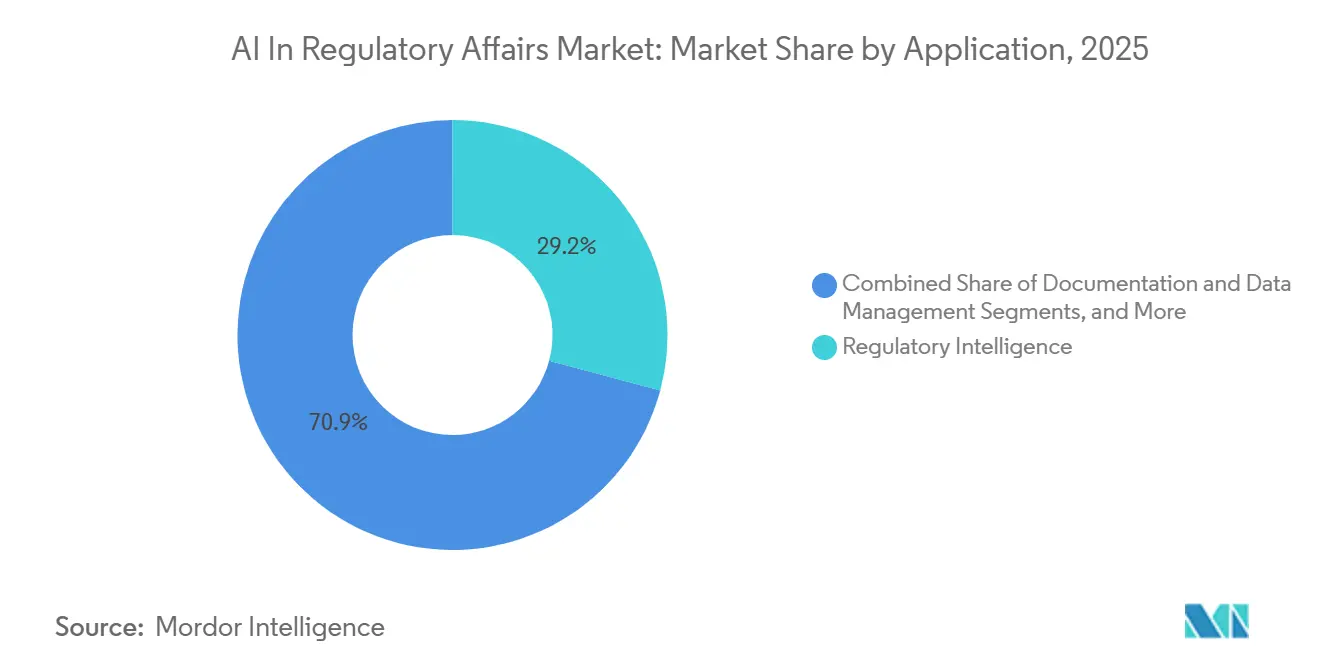

- By application, regulatory intelligence led with 29.15% revenue share in 2025, whereas post-market surveillance is forecasted to advance at a 20.75% CAGR to 2031.

- By end user, pharmaceutical companies accounted for 38.35% share of the AI in regulatory affairs market size in 2025, while regulatory consulting firms are expected to grow at a 19.96% CAGR through 2031.

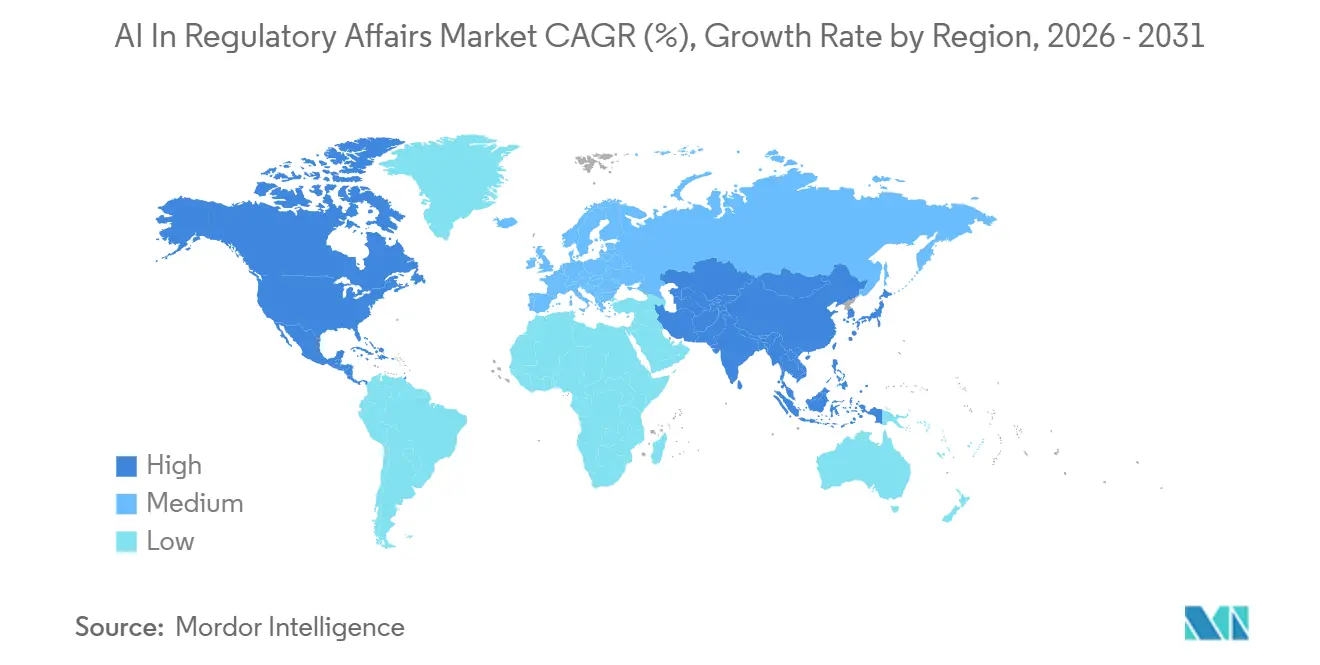

- By geography, North America secured 46.48% revenue share in 2025; Asia-Pacific is projected to register the highest regional CAGR of 22.45% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Regulatory Affairs Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerated regulatory-submission timelines | +4.5% | Global, strongest in United States, Europe, Japan | Short term (≤ 2 years) |

| Rising Regtech Adoption Mandates by the U.S. FDA & EMA | +2.8% | North America, Europe, India, Southeast Asia | Medium term (2–4 years) |

| Growing volume of labeling changes | +3.2% | Global, especially U.S., EU, Asia-Pacific | Medium term (2–4 years) |

| Cloud-native AI platforms | +2.8% | North America, Europe, India, Southeast Asia | Medium term (2–4 years) |

| Generative AI co-pilots | +5.1% | Global, early adoption in U.S. and EU | Short term (≤ 2 years) |

| Knowledge-graph compliance analytics | +2.9% | North America, Europe, expanding in Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Accelerated Regulatory-Submission Timelines in Pharmaceutical and Biotechnology Companies

Expedited approval pathways for oncology, rare-disease, and pandemic-response therapies create strong incentives to compress investigational new drug and new drug application timelines. Sponsors now deploy AI platforms that auto-extract clinical study data, validate references, and assemble electronic Common Technical Documents in hours rather than weeks. Weave Bio and Parexel demonstrated a 60% faster NDA preparation cycle in April 2026, illustrating measurable return on investment for early adopters. Similar productivity gains appear at Recursion Pharmaceuticals, where its Recursion OS accelerated first-in-human readiness for an LSD1 inhibitor in roughly 20 months versus the historical 45-month average, saving multiple years of carrying costs.

Growing Volume of Global Labeling Changes Driven by Multi-Market Launches

Divergent U.S. Structured Product Labeling, European Summary of Product Characteristics, and Japanese package-insert rules require sponsors to tailor each update by language, format, and referral channels. A single safety signal can mandate changes across 50 countries, and manual coordination often pushes launches back an entire quarter. In 2025 Consainsights fine-tuned large language models on historic labeling templates and pharmacovigilance taxonomies, achieving 70% cycle-time compression and 85% concordance between AI drafts and final authority-approved labels. Faster multi-lingual updates preserve synchronized global market availability and prevent revenue leakage.

Cloud-Native AI Platforms Lowering Total Cost of Ownership for Mid-Size Sponsors

Cloud deployment captured more than three-fifths of 2025 revenue and will outpace on-premise at a 20.55% CAGR because usage-based pricing aligns costs with small biotech cash flow. Vendors shoulder GPU refresh, cybersecurity, and validation burdens, letting a 50-person sponsor scale from one to hundreds of simultaneous submissions without purchasing servers. Veeva Systems announced in October 2025 that AI agents would be embedded across every Vault application by 2026 with pay-per-agent billing, underscoring the momentum behind cloud subscription economics.

Deployment of Generative AI Co-Pilots for Dossier Authoring and Quality Control

Generative co-pilots transform regulatory writers into reviewers who refine drafts rather than create them from scratch. AutoIND’s 2025 field study found that writing a non-clinical IND summary dropped from roughly 100 hours to four, with no critical compliance errors, despite requiring stylistic edits to lift readability scores above 75%. These gains release medical writers to craft higher-value benefit–risk narratives, and sponsors can redirect saved labor toward strategic interactions with agencies.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Data privacy & sovereignty concerns | -2.1% | Europe, China, Middle East | Short term (≤ 2 years) |

| Black-box AI explainability gaps | -1.8% | U.S., EU, Japan | Medium term (2–4 years) |

| Legacy on-premise validation hurdles | -1.5% | Global, strongest in regulated markets (U.S., EU) | Medium term (2–4 years) |

| Limited annotated regulatory data | -2.4% | Global, especially emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Sovereignty Concerns Limiting Cross-Border AI Training Datasets

Sovereign data laws in the European Union, China, UAE, and Saudi Arabia fracture training corpora, forcing life-sciences companies to either replicate models locally or adopt federated learning. The UAE, for example, restricts cross-border transfer of health data unless exception criteria are met, requiring in-country processing or irreversible anonymization. Fragmented data sets can lower model accuracy when global AI services attempt to interpret region-specific medical terminologies, complicating validation and maintenance costs.

“Black-Box” AI Explainability Gaps in Regulatory Submissions

The FDA’s 2025 draft guidance frames model credibility as a function of risk and transparency. Deep learning architectures with millions of parameters often rely on post-hoc explainers such as SHAP or LIME that offer only approximations. Regulators therefore encourage hybrid approaches combining symbolic knowledge graphs with machine learning to allow traceability back to source data. Sponsors incorporating explainability at design time will enjoy fewer information requests and shorter review cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Infrastructure Unlocks Scalability for Cross-Functional Teams

Cloud deployments accounted for 64.15% AI in the regulatory affairs market share in 2025 and are projected to maintain supremacy by expanding at 20.55% CAGR through 2031. The AI in Regulatory Affairs market size for cloud-based solutions is forecast to reach USD 2.93 billion by 2031. Multitenant architecture spreads validation and cybersecurity costs, delivers instant feature upgrades, and simplifies disaster recovery. On-premises deployments persist in Japan and Germany, where data localization laws remain strict, but their total cost of ownership climbs as GPU prices, electricity tariffs, and specialized DevOps salaries rise. Cloud vendors now pass independent validation audits 21 CFR Part 11, EU Annex 11, ISO 27001, providing documented assurance that satisfies most agency inspectors. Integration bridges to electronic trial master file and quality-management systems make the cloud the default for new market entrants.

By Technology: Machine Learning Dominates Today, Knowledge Graphs Gain Regulatory Mapping Strength

Machine learning accounted for 41.00% AI in the regulatory affairs market share in 2025, yet knowledge graphs should grow fastest at a 21.00% CAGR. Graph databases represent entity relationships, products, indications, jurisdictions, and guidance documents in a human-readable form that regulatory reviewers trust. Linking a safety signal to all affected labels across 70 countries becomes one query instead of thousands of manual cross-checks. Meanwhile, natural-language processing underpins generative co-pilots that translate tables and statistical outputs into submission narratives. Robotic process automation fills niche gaps such as extracting scanned signatures from legacy PDFs, but its rule-based logic limits scalability. Computer vision remains in an early stage, confined to identifying tables or signatures in non-searchable images.

By Application: Regulatory Intelligence Leads, Post-Market Surveillance Accelerates

Regulatory intelligence systems captured 29.15% revenue share in 2025 and remain the first AI investment because every sponsor must understand evolving rules before drafting any submission. Horizon-scanning algorithms parse daily FDA, EMA, and PMDA updates, then alert dossier owners within minutes. Impact-analysis engines bucket changes by priority, triggering automatic task creation in regulatory information management dashboards. Post-market surveillance grows at 20.75% CAGR as adaptive algorithms enter real-world settings where regulators require ongoing performance evidence.

By End User: Pharmaceutical Companies Lead Adoption, Regulatory Consultancies Grow Fastest

Pharmaceutical companies held 38.35% AI in regulatory affairs market share in 2025, justified by the direct revenue risk of submission delays one blockbuster can lose USD 1-3 million daily if approval slips. Large sponsors embed AI across CMC, clinical, and safety functions. Regulatory consultancies, however, will post the highest CAGR at 19.96%, driven by demand from virtual biotechs and digital-health start-ups that outsource technology configuration, validation, and maintenance. The AI in Regulatory Affairs market size for consulting services could nearly triple by 2031 as mid-size innovators prefer operational expenditure over hiring internal data-science teams.

Geography Analysis

North America contributed 46.48% revenue in 2025 on the back of FDA leadership. The agency released draft guidance on AI credibility in January 2025 and unveiled “Elsa,” an internal generative AI reviewer assistant, in June 2025. Such initiatives validate AI’s legitimacy and encourage private investment. U.S. firms accounted for more than half of 2025 patent filings related to AI-driven regulatory technologies. Canada also expanded its Regulatory Experimentation Hub in Health in 2026, opening sandboxes for AI explainability pilots.

Europe follows closely after the EMA and FDA agreed on ten principles governing AI in drug development in January 2026. The EU’s AI Act, entering force in 2026, classifies medical-product regulatory AI as “high-risk,” requiring quality-management systems and human-oversight provisions that many vendors already implement, easing transition costs. The United Kingdom Medicines and Healthcare products Regulatory Agency (MHRA) launched its own AI Signal Detection Pilot in October 2025 to refine post-marketing safety analytics.

Asia-Pacific posts the fastest growth, forecast at 22.45% CAGR through 2031. Japan’s AI Promotion Act, live since June 2025, funds translational AI projects and shortens review windows for digitally enabled submissions. South Korea’s AI Framework Act, effective January 2026, couples transparency mandates with incentives for certified AI providers, spurring domestic vendors. India’s New Drugs and Clinical Trials Rules, amended in February 2026, now recognize electronic source data and AI-assisted dossier preparation, boosting SaaS adoption among generics manufacturers seeking U.S. FDA parity.

Competitive Landscape

The AI in Regulatory Affairs market is moderately fragmented. Veeva Systems, ArisGlobal, MasterControl, and IQVIA bundle AI into end-to-end suites that serve pharmaceutical quality, clinical, safety, and regulatory teams. Veeva launched Veeva AI in April 2025, rolling out agents across CRM, PromoMats, safety, quality, clinical, and regulatory through 2026, while partnering with Accenture and EY for change-management services. ArisGlobal expanded its LifeSphere platform with generative co-pilots in January 2026, focusing on automated case narrative writing.

Specialist start-ups target single pain points. Weave Bio’s HAQ Manager automates answers to health authority questions, attracting early customers among oncology biotech firms with lean regulatory staff. IntuitionLabs commercialized AutoIND for small molecules, and Zifo Technologies launched a knowledge-graph library tailored to EU centralized procedures. Large system integrators such as Accenture, Deloitte, and Capgemini invest in alliances and minority stakes. Accenture’s April 2026 backing of Iridius secures compliant AI infrastructure components for regulated workloads.

Competition now hinges on integration depth, validation documentation, and explainability. Vendors that demonstrate live traceability from an AI-generated sentence to its clinical-study source table pass agency audits faster. Interoperability with existing EDC, eTMF, and quality-management systems removes data-silo barriers and builds switching costs. Pricing models trend toward consumption-based, aligning vendor revenue with sponsor submission volume. Market entrants that cannot produce part-11-ready audit trails or do not hold ISO 27001 certification struggle to win procurement tenders.

AI In Regulatory Affairs Industry Leaders

ArisGlobal

Veeva Systems

IQVIA

Accenture

Deloitte

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Accenture Ventures invested in Iridius to scale compliance-first AI infrastructure for life-sciences clients.

- April 2026: Weave Bio, in partnership with Parexel, unveiled an AI-native NDA Support platform that cut authoring time by 60% for early pilot customers.

- January 2026: The Global Agency for Responsible AI in Health signed an MoU with TOPRA to advance responsible AI practices across the regulatory-affairs community.

- November 2025: Brazil’s Anvisa announced the USD 4.9 million “AnvisAI” program to shorten review queues and hired 102 new specialists for 2026 deployment.

- October 2025: Veeva Systems confirmed usage-based pricing for Veeva AI Agents, starting roll-out across commercial in December 2025 and R&D in 2026.

Global AI In Regulatory Affairs Market Report Scope

As per the scope of the report, AI in Regulatory Affairs refers to the application of artificial intelligence technologies, specifically machine learning (ML), natural language processing (NLP), and generative AI to automate, accelerate, and enhance the processes required to ensure that pharmaceuticals, medical devices, and biologics comply with global health authority regulations.

The AI in Regulatory Affairs Market is segmented by deployment mode, technology, application, end-user, and geography. By deployment mode, the market includes on-premise and cloud-based solutions. By technology, the market is segmented into machine learning, natural language processing, robotic process automation, computer vision, and knowledge graphs. By application, the market is categorized into regulatory intelligence, document & data management, dossier preparation & submission, labeling & artwork management, post-market surveillance & compliance, and others. By end-user, the market is segmented into pharmaceutical companies, biotechnology firms, medical device manufacturers, contract research organizations, regulatory consulting firms, and others. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| On-premise |

| Cloud-based |

| Machine Learning |

| Natural Language Processing |

| Robotic Process Automation |

| Computer Vision |

| Knowledge Graphs |

| Regulatory Intelligence |

| Document & Data Management |

| Dossier Preparation & Submission |

| Labelling & Artwork Management |

| Post-Market Surveillance & Compliance |

| Others |

| Pharmaceutical Companies |

| Biotechnology Firms |

| Medical Device Manufacturers |

| Contract Research Organizations |

| Regulatory Consulting Firms |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Deployment Mode | On-premise | |

| Cloud-based | ||

| By Technology | Machine Learning | |

| Natural Language Processing | ||

| Robotic Process Automation | ||

| Computer Vision | ||

| Knowledge Graphs | ||

| By Application | Regulatory Intelligence | |

| Document & Data Management | ||

| Dossier Preparation & Submission | ||

| Labelling & Artwork Management | ||

| Post-Market Surveillance & Compliance | ||

| Others | ||

| By End-User | Pharmaceutical Companies | |

| Biotechnology Firms | ||

| Medical Device Manufacturers | ||

| Contract Research Organizations | ||

| Regulatory Consulting Firms | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast will spending on AI tools for regulatory affairs grow through 2031?

The AI in Regulatory Affairs market is projected to expand at an 18.65% CAGR between 2027-2031, rising from USD 1.90 billion in 2025 to USD 4.47 billion by 2031.

Which deployment model dominates spending today?

Cloud solutions held 64.15% of 2025 revenue because sponsors prefer usage-based subscriptions that avoid on-premise GPU investment.

What application area attracts the most investment?

Regulatory intelligence platforms led with 29.15% share in 2025, reflecting the need to monitor and interpret changing global rules.

Which region is forecast to grow the quickest?

Asia-Pacific is expected to register a 22.45% CAGR from 2026-2031, outpacing every other region thanks to supportive AI legislation in Japan, South Korea, India, and China.

Why are knowledge graphs important in this space?

Knowledge graphs map complex relationships among products, indications, and regional rules, supporting proactive compliance analytics and are forecast to post the fastest technology growth at a 21.00% CAGR.

Page last updated on: