AI In Cell and Gene Therapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

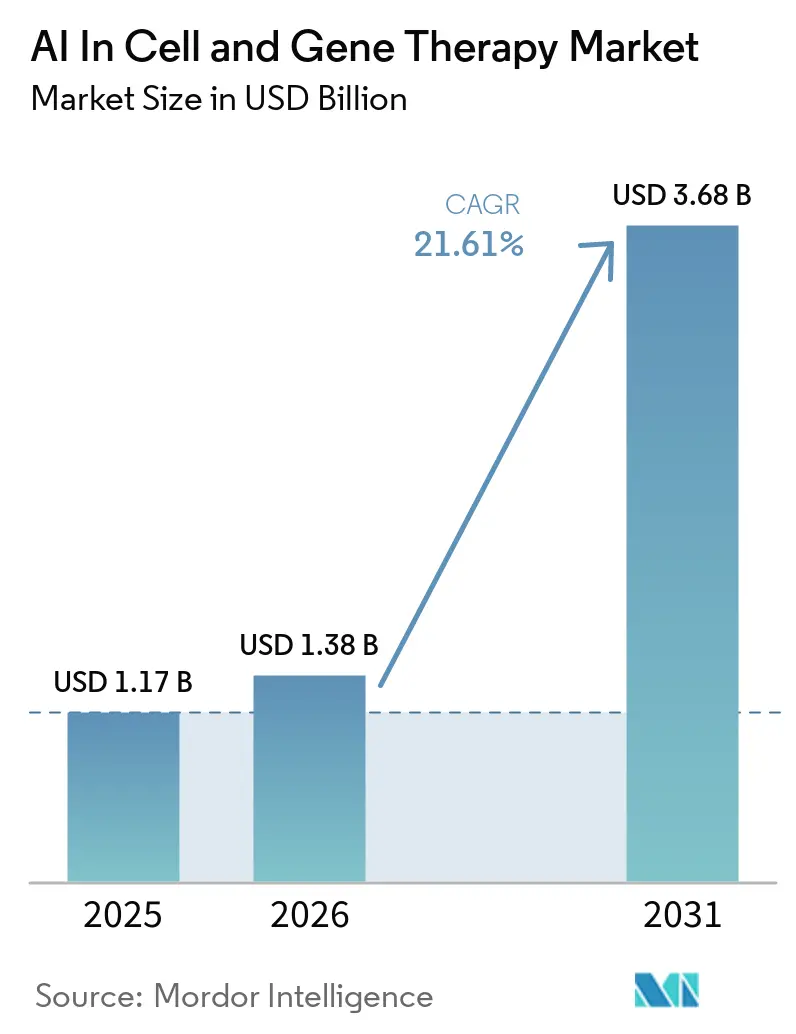

| Market Size (2026) | USD 1.38 Billion |

| Market Size (2031) | USD 3.68 Billion |

| Growth Rate (2026 - 2031) | 21.61% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Cell and Gene Therapy Market Analysis by Mordor Intelligence

The AI in cell and gene therapy market is expected to grow from USD 1.17 billion in 2025 to USD 1.38 billion in 2026 and is forecasted to reach USD 3.68 billion by 2031 at 21.61% CAGR over 2026-2031. The AI in cell and gene therapy market is expanding because single-cell and multi-omic datasets are rising faster than manual analysis can handle, which makes neural models more useful in discovery and process design. More than 3,200 active clinical trials for gene, cell, or RNA therapies were in progress globally by late 2025, which continues to deepen the data pool available for training and validating commercial models. Large pharmaceutical companies are also moving AI from pilot work into core development infrastructure, as shown by NVIDIA and Eli Lilly’s multi-year co-innovation lab and Roche’s global AI factory buildout. Wider access to GPU compute is letting more developers use the AI in cell and gene therapy market across discovery, manufacturing, and workflow orchestration instead of restricting advanced use to the largest organizations. Even so, the AI in cell and gene therapy market still faces practical limits from fragmented data environments and from the lack of clear audit standards for AI-guided manufacturing decisions in continuously learning systems.

Key Report Takeaways

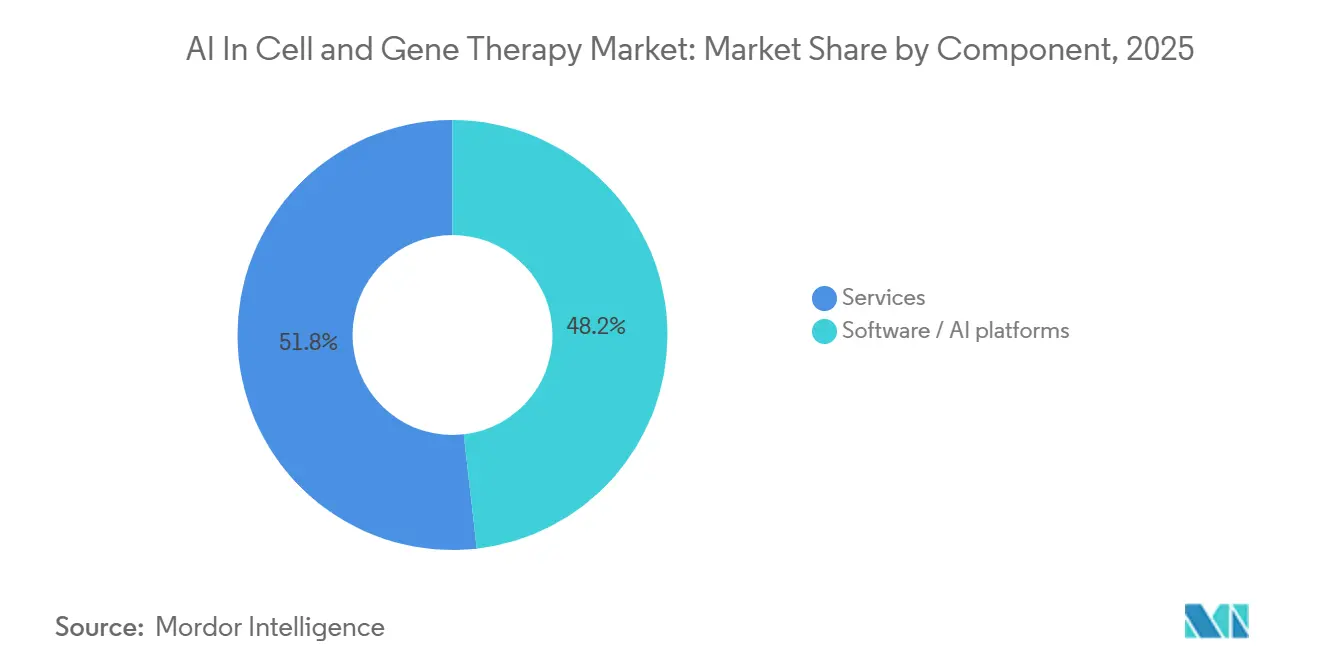

- By component, software/ AI platforms held 48.24% of revenue in 2025, and the same segment is projected to expand at 22.17% CAGR through 2031.

- By deployment, cloud-based deployment held 53.26% share in 2025, and is projected to grow at 22.38% CAGR through 2031, while on-premises and edge configurations remain important in GMP settings.

- By therapy type, cell therapy held 54.44% share in 2025, while gene therapy is projected to grow at 23.51% CAGR through 2031.

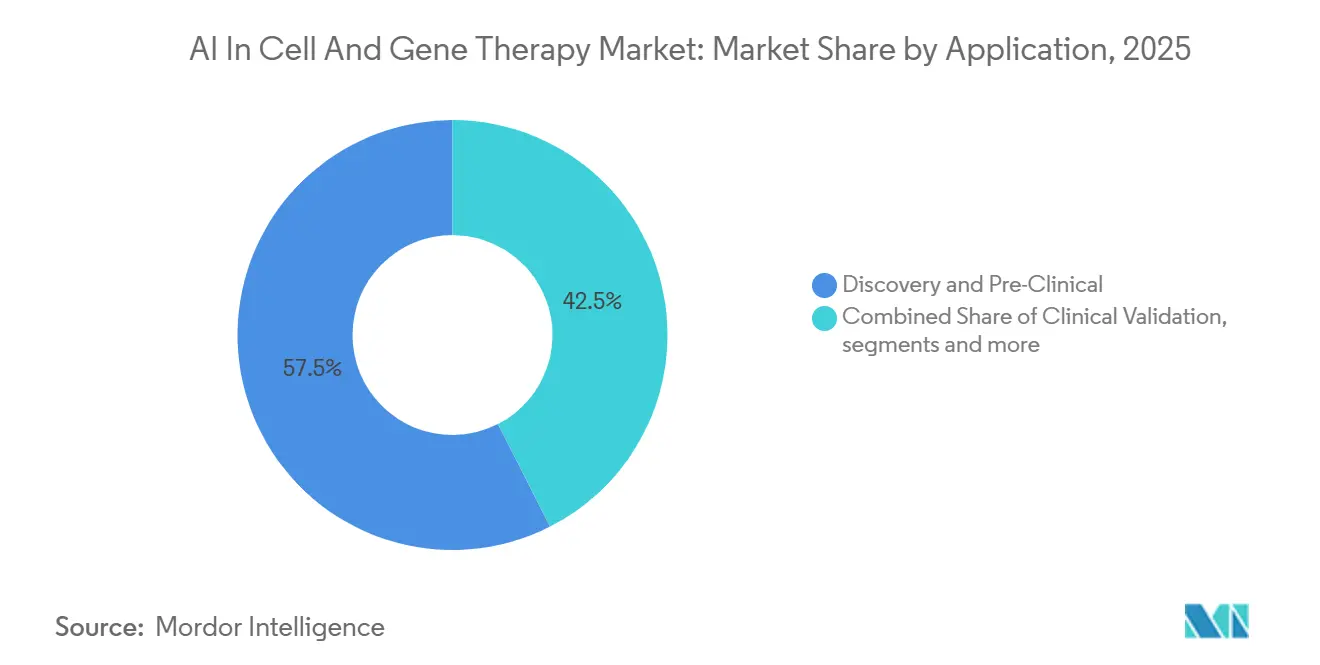

- By application, discovery and pre-clinical applications held 57.46% share in 2025, while commercial manufacturing is projected to grow at 22.52% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies held 58.25% share in 2025, while contract research organizations (CROs) are projected to grow at 22.41% CAGR through 2031.

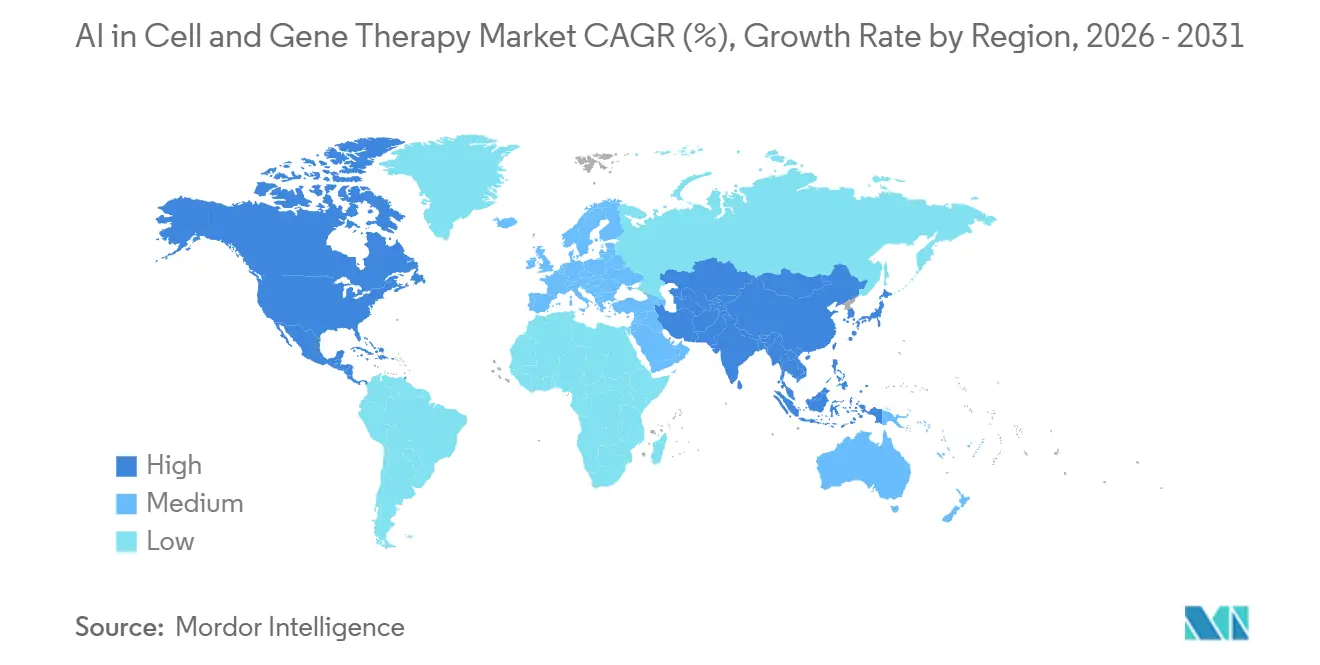

- By geography, North America held 51.62% share in 2025, while Asia-Pacific is projected to grow at 23.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Cell and Gene Therapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exponential Growth in High-Throughput Gene-Editing Datasets | +4.2% | Global, with concentration in North America and APAC | Medium term (2-4 years) |

| Increasing Big-Pharma Alliances with AI Start-Ups | +3.8% | Global, with early gains in US, UK, and Germany | Short term (≤ 2 years) |

| Falling Cost of Cloud GPUs | +2.3% | Global, with high impact in emerging APAC markets | Short term (≤ 2 years) |

| Convergence of Single-Cell Multi-Omics with Generative AI | +3.3% | North America and Europe core, with spillover to APAC | Medium term (2-4 years) |

| AI-Enabled Digital Twins Optimizing Bioreactor Parameters | +2.1% | Global, with concentration in US, Germany, and Singapore | Medium term (2-4 years) |

| Enterprise AI Platforms and GPU Access Enable Bundled Deployments | +2.0% | North America and Europe, with early APAC adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exponential Growth in High-Throughput Gene-Editing Datasets Demands AI-Driven Analytics

The AI in cell and gene therapy market is benefiting from a data expansion wave that is now as much an infrastructure issue as a scientific one. Illumina introduced the Billion Cell Atlas in January 2026 as the first release in a planned 5-billion-cell program built to support AI-driven drug discovery workflows.[1]Illumina Introduces Billion Cell Atlas to Accelerate AI and Drug Discovery,” Illumina Investor Relations, investor.illumina.comAs sequencing throughput rises, the operational bottleneck is moving away from data generation and toward annotation quality, because models still need clinically meaningful labels to separate real therapeutic signals from background biological noise. Recursion stated in 2026 that its biology maps, developed with Roche and Genentech, are built from more than 1 trillion iPSC-derived neuronal cells, which shows how curated multi-modal data can become a durable commercial asset rather than a disposable research input. This is why the AI in cell and gene therapy market is increasingly rewarding companies that control proprietary cellular datasets, not only those that publish stronger model architectures. Over time, the data owners with the broadest and cleanest libraries are likely to hold the strongest pricing power inside the AI in cell and gene therapy market.

Increasing Big-Pharma Alliances with AI Start-Ups to Shorten CGT Development Cycles

The AI in cell and gene therapy market is also gaining from a funding environment where large pharmaceutical companies treat AI as core development infrastructure. NVIDIA and Eli Lilly announced a co-innovation AI lab in January 2026, with a commitment of up to USD 1 billion over 5 years for protein diffusion models, genomics foundation models, and manufacturing digital twins.[2]NVIDIA and Lilly Announce Co-Innovation AI Lab to Reinvent Drug Discovery in the Age of AI,” NVIDIA Investor Relations, investor.nvidia.com Roche then expanded its AI factory strategy in March 2026 with more than 3,500 Blackwell GPUs across U.S. and European sites, which signals that large drug makers are building private compute capacity for time-sensitive regulated workflows instead of relying only on public cloud access. These alliances are shortening development cycles, but they are also changing competitive behavior because AI start-ups that become embedded inside sponsor workflows are harder to replace later. In practice, the AI in cell and gene therapy market is starting to resemble enterprise software, where switching costs rise after models, data pipelines, and scientific decisions are tied to one platform. That makes commercial relationships in the AI in cell and gene therapy market more durable than standard project-based outsourcing.

Convergence of Single-Cell Multi-Omics with Generative AI for Potency Prediction

The AI in cell and gene therapy market is moving toward models that do more than classify biology, because they can now predict functional behavior across new cellular states. In 2024, scGPT was reported as being trained on more than 33 million cells and achieved strong results in cell-type annotation, multi-omic integration, and perturbation prediction, which supports the use of pre-trained generative models for downstream therapeutic tasks.[3]Toward Building a Foundation Model for Single-Cell Multi-omics Using Generative AI,” Nature Methods, nature.comThat matters for potency prediction because developers can begin with a broad biological representation rather than rebuilding a model from each new experimental dataset. The practical advantage is zero-shot or low-shot transfer into new cell product settings, which can compress pre-IND work when fresh wet-lab data is still limited. The AI in cell and gene therapy market therefore gains from a feedback loop where larger atlases make models more useful, and more useful models increase the value of new atlas generation. This is one reason the AI in cell and gene therapy market is attracting continued investment in single-cell reference data, foundation models, and generative design tools that can support potency, reprogramming, and product consistency assessments.

AI-Enabled Digital Twins Optimizing Bioreactor Parameters for Cell-Therapy Yields

The AI in cell and gene therapy market is extending into manufacturing because digital twins can improve process control before a batch is finished. A 2026 study in PMC reported that a digital shadow model for CAR-T expansion in a perfusion bioreactor could predict cell concentrations up to 2.5 days ahead, with a mean relative error of 13%, which supports earlier and more data-driven harvest decisions. The limit is that autologous programs often remain donor specific, so each patient batch can require model retraining and reduce the reuse value of earlier results. This makes allogeneic programs more attractive for scaled digital-twin deployment because their production conditions are more repeatable. FRONTEO and Cellaxia announced a January 2026 proof of concept to use the Drug Discovery AI Factory for allogeneic DC-based cell therapy manufacturing efficiency and quality improvement, which shows that companies are already testing that model in commercial settings. Hitachi also announced in May 2025 that its Design Cell Development Platform could lift cell design throughput from tens of constructs per year to nearly 100,000, which changes the cost logic for AI adoption in the AI in cell and gene therapy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented, Proprietary Clinical Datasets | -3.1% | Global | Medium term (2-4 years) |

| Data-Privacy And Governance Concerns in Patient-Level Genomic Information | -2.4% | EU under GDPR, North America under HIPAA, and China under PIPL | Medium term (2-4 years) |

| Regulatory Ambiguity in SaMD AI Validation for CGT Workflows | -1.8% | Global, with the sharpest effect in US and EU | Long term (≥ 4 years) |

| Supply-Chain Bottlenecks for GMP-Grade GPU Clusters | -1.5% | Emerging markets, with APAC as a core exposure area | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented, Proprietary Clinical Datasets Limit Model Generalizability

The AI in cell and gene therapy market still faces a hard limit from siloed datasets that do not transfer cleanly across donors, disease settings, or manufacturing sites. A March 2026 review in Pharmaceutics described how AI models in cell and gene therapy often struggle to generalize when they are trained within narrow sponsor-specific data environments. This means architectural progress alone will not solve the performance gap if the training data remain fragmented and proprietary. It also creates a strong first-mover advantage for any organization that can aggregate diverse multi-site and multi-sponsor manufacturing and clinical datasets into one usable framework. Federated learning can reduce some of the sharing barriers, but it also slows execution because sites often work under different governance, privacy, and operational standards. Until the AI in cell and gene therapy market has stronger interoperability rules, model performance in the lab will continue to outpace what can be deployed consistently in commercial programs.

Data-Privacy and Governance Concerns in Patient-Level Genomic Information

The AI in cell and gene therapy market also has to work within some of the strictest privacy regimes applied to health data. Patient-level genomic information is governed by GDPR in Europe, HIPAA in the United States, and PIPL in China, which makes cross-border model training much harder to organize than typical enterprise AI work. That pushes developers toward federated or localized learning architectures, not because of design preference, but because the legal risk of centralized patient-level genomic storage is high. The challenge is especially important for gene therapy models, since clinical accuracy depends on exposure to diverse population-level genetic variation that cannot always be assembled inside one country or one sponsor dataset. As a result, the AI in cell and gene therapy market needs privacy-by-design engineering at the data layer, or commercialization timelines will slip even when the science is ready. The same constraint is likely to keep data governance strategy near the center of investment decisions across the AI in cell and gene therapy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software/AI Platforms Capture the Majority of CGT AI Value

Software/AI platforms accounted for 48.24% of the AI in cell and gene therapy market share in 2025, which made them the largest component category. That position reflects where buyers now see the most value, since model development, workflow orchestration, and predictive analytics are treated as the main deliverables, while underlying data storage and generic compute are becoming more standardized. The AI in cell and gene therapy market is therefore assigning more value to the control layer that links experiments, data, and decision support than to basic implementation work alone. Benchling’s May 2026 work with Baseten to bring GPU-scale inference into biotech R&D workflows shows how software vendors are absorbing capabilities that were previously handled by separate infrastructure providers. The same software segment is projected to expand at 22.17% CAGR through 2031, which means the largest component in the AI in cell and gene therapy market is also one of the fastest-moving.

Services still account for a meaningful share of revenue, but their role is shifting toward implementation support, validation, and regulatory advisory work tied to more complex deployments. Standard pre-clinical tasks are becoming more automated, which reduces labor intensity and slows the relative growth of services compared with software-led platforms. The AI in cell and gene therapy industry is also seeing buyers prefer repeatable platform subscriptions over one-time service engagements when they expect frequent model updates and ongoing workflow integration. Post-market surveillance and GMP quality functions still represent a smaller part of software spending than discovery does, yet that balance is likely to change as lifecycle expectations become stricter. Across the AI in cell and gene therapy market, the component mix suggests that durable value is building around integrated platforms that can hold experimental context, model outputs, and decision history in one operating environment.

By Deployment: Cloud Infrastructure Extends AI Reach While Edge Anchors GMP Workflows

Cloud-based deployment held 53.26% share in 2025, and is projected to grow at 22.38% CAGR through 2031, which makes it the fastest-growing deployment format in the AI in cell and gene therapy market. This pattern reflects the practical needs of discovery and pre-clinical teams, where access to distributed GPU infrastructure can be expanded faster than local hardware can be installed and validated. Cloud deployment also suits workloads that rise and fall across screening cycles, because organizations can scale compute without carrying all of the capital burden on site. In that sense, the AI in cell and gene therapy market is using cloud more as an operating model than only as a hosting decision. It is widening access for smaller developers that would otherwise struggle to fund advanced training and inference capacity.

Adoption remains uneven, though, because regulated manufacturing environments still require tighter control over data location, audit trails, latency, and system validation. Roche’s March 2026 AI factory expansion, with large GPU clusters across U.S. and European sites, is a clear signal that major manufacturers still view private infrastructure as a strategic requirement for certain regulated workflows. On-premises and edge or hybrid models therefore remain important in the AI in cell and gene therapy market even while cloud grows faster overall. Edge and hybrid architectures are currently smaller in revenue terms, but they are well placed for future growth in commercial manufacturing because they combine local governance with selected access to external compute. Over time, the AI in cell and gene therapy market is likely to separate by function, with cloud leading early-stage experimentation and hybrid deployment gaining ground where GMP oversight is strictest.

By Therapy Type: Gene Therapy Accelerates as AI Reshapes Vector Design Economics

Cell therapy held 54.44% share of revenue in 2025, which made it the larger therapy segment in the AI in cell and gene therapy market. That position reflects the installed base of autologous CAR-T programs and the clinical infrastructure that has been built around them over the last decade. Existing manufacturing complexity also creates many data-rich points where AI can support scheduling, yield prediction, and quality review. Even so, the AI in the cell and gene therapy market is projected to experience its fastest therapy expansion in gene therapy, which is projected to grow at 23.51% CAGR through 2031. The main reason is that vector and capsid design present a high-dimensional search problem where AI can evaluate candidate space much faster than conventional wet-lab iteration.

Dyno Therapeutics signed a second commercial capsid licensing deal in 2026, with a USD 15 million license involving Astellas for an AI-designed AAV capsid targeting skeletal muscle, which shows that AI-designed vectors are moving into commercial intellectual property rather than staying at proof-of-concept stage. That deal matters because it confirms that buyers are willing to pay for AI-designed vector performance before full downstream commercialization has matured. Within cell therapy, the move toward allogeneic programs remains important for the AI in cell and gene therapy market because it creates better conditions for reusable donor-independent manufacturing models. This could narrow the cost gap between autologous and off-the-shelf products over time if process data become more standardized. The therapy mix therefore shows that the AI in cell and gene therapy market is expanding from current cell therapy scale, while future acceleration is increasingly tied to gene therapy design economics.

By Application: Discovery Commands Revenue Share, but Manufacturing Closes the Gap

Discovery and pre-clinical applications held 57.46% of the AI in cell and gene therapy market size in 2025, which made them the largest application area. That lead is tied to AI’s strongest current advantage, since in silico screening and generative design can shorten repeated experimental cycles more clearly than many downstream uses can. The AI in cell and gene therapy market has therefore built its earliest commercial scale around identifying candidates faster and filtering out weak directions before costly bench work expands. Insitro reported validation of its POSH platform in Nature Communications in December 2025, highlighting how AI-enabled phenotypic discovery can support high-throughput human-cell screening at a scale that conventional hypothesis-led approaches struggle to match. The discovery side of the AI in cell and gene therapy market is therefore likely to remain the largest revenue pool across the near term.

Commercial manufacturing is projected to be the fastest-growing application segment, with 22.52% CAGR through 2031, because the economic cost of failed or inconsistent batches is high enough to justify more process intelligence. Yield optimization, adaptive process control, and quality-by-design tools are gaining attention as developers look for ways to reduce batch loss and improve reproducibility. The FDA’s recent stance on lifecycle management and regulated AI validation has also kept attention on how AI outputs are documented and controlled when used near manufacturing decisions. Clinical validation and post-market surveillance remain smaller today, but they are becoming more relevant as long-term CGT safety monitoring gains weight in regulation and follow-up obligations. This means the AI in cell and gene therapy market is still led by discovery, while manufacturing is closing the gap as regulatory acceptance and process economics become more favorable.

By End User: Pharma Controls Spending, CROs Emerge as AI Capacity Builders

Pharmaceutical and biotechnology companies accounted for 58.25% of spending in 2025, which made them the largest end-user group in the AI in cell and gene therapy market. Their lead comes from larger R&D budgets, deeper data ownership, and the need to apply AI across discovery, development, manufacturing, and commercial functions. These buyers are not only purchasing AI outputs, but are also funding the platforms, partnerships, and internal infrastructure that shape how the market develops. Bristol Myers Squibb’s 2026 agreement with Anthropic shows how large companies are moving from isolated tools toward shared AI environments that support scientific and operational workflows across the enterprise. That dynamic helps explain why the AI in cell and gene therapy market often becomes embedded in sponsor pipelines rather than sold as a simple interchangeable service.

CROs are projected to grow at 22.41% CAGR through 2031, which makes them the fastest-growing end-user segment. This reflects a clear operating preference among large sponsors, since many want to out-task AI-augmented experimental design and throughput expansion to specialist providers instead of replicating the same capability internally. At the same time, CDMOs such as Lonza and Thermo Fisher Scientific are building AI-enabled bioprocess and manufacturing tools that let them compete on both service quality and technical capability. The line between CRO and CDMO is therefore becoming less distinct inside the AI in cell and gene therapy market. A new competitive group is forming around full-service partners that combine in silico design, data interpretation, and GMP execution in one digital workflow.

Geography Analysis

North America accounted for 51.62% of the AI in cell and gene therapy market share in 2025, which kept it as the leading regional cluster. The region benefits from strong sponsor concentration, deep venture support, and the FDA’s active work on lifecycle management and risk-based validation for AI-related regulated software environments The U.S. remains the central driver because large pharmaceutical headquarters, academic cell therapy hubs, and advanced compute infrastructure are located close to one another. NVIDIA stated in 2026 that LillyPod became the world’s first NVIDIA DGX SuperPOD with DGX B300 systems, giving North American developers a major compute advantage for scaled model development and deployment.

Europe remains an established part of the AI in cell and gene therapy market, supported by strong bioprocess engineering capabilities and tighter attention to data compliance. Germany stands out because equipment, process engineering, and manufacturing know-how are closely tied to therapeutic development. Sartorius announced in 2025 that it was working with NVIDIA to advance AI in drug discovery and manufacturing, which fits Europe’s strength in linking instrumentation, data capture, and process insight. The United Kingdom, France, Italy, Spain, and the rest of Europe continue to add value through academic-originated AI biotech companies, specialized clinical programs, and EU-level support frameworks.

Asia-Pacific is projected to expand at 23.62% CAGR through 2031, which makes it the fastest-growing regional segment in the AI in cell and gene therapy market. China, Japan, and South Korea are the main growth centers, with stronger policy support, rising trial activity, and expanding local development ecosystems. Japan is contributing through company and academic work on manufacturing optimization and cell reprogramming, including Hitachi’s platform development for high-throughput cell design. South Korea and Australia are adding regional volume through CRO growth and clinical trial activity, which broadens the operating base for the AI in cell and gene therapy market beyond the largest national players. Middle East and Africa, especially the GCC and South Africa, and South America, including Brazil and Argentina, remain smaller markets, but they are starting to build relevance through selective government-backed genomic medicine and advanced therapy programs.

Competitive Landscape

The AI in cell and gene therapy market is moderately fragmented because competition happens across infrastructure, AI platforms, and life science manufacturing services rather than within one simple peer group. NVIDIA holds a central infrastructure position, since BioNeMo and related accelerated computing tools support programs across Roche, Lilly, QIAGEN, and Thermo Fisher Scientific, which creates a strong dependency layer for scaled biological AI work. That role does not make NVIDIA a direct substitute for every other supplier, but it does make its compute stack difficult to avoid when model size, throughput, and regulated deployment needs start to rise. In the AI in cell and gene therapy market, that gives infrastructure providers a different kind of power than platform-native biotech companies or contract manufacturers hold.

Platform-native companies are differentiating less through generic model claims and more through exclusive data depth, workflow fit, and scientific context. Recursion’s 2026 disclosure around its large-scale biology maps supports that point, since proprietary cellular data can be more durable than reusable algorithm choices alone. Owkin’s May 2026 licensing agreement with AstraZeneca also shows how competition is shifting toward agentic systems that become part of daily research decision support rather than stand-alone analytics tools. Benchling is following a related path by tying automation, lab context, and AI inference more closely together inside one R&D environment. This means the AI in cell and gene therapy market is rewarding companies that can sit inside the operating workflow, because embedded tools are harder to replace than point solutions.

Life science equipment and manufacturing companies are responding with more vertical integration. Sartorius is combining its proprietary live-cell and manufacturing data streams with NVIDIA collaboration to improve discovery and production workflows. Thermo Fisher Scientific is embedding AI guidance into scalable cell therapy manufacturing platforms, which shows that established suppliers are trying to protect service relationships by adding intelligence directly into production tools. White space still exists in regulated post-market surveillance, AI-powered patient stratification for CGT trials, and fully automated GMP digital twins, where no vendor has yet established clear commercial control. Across the AI in cell and gene therapy market, evolving compliance expectations such as FDA lifecycle management and software quality standards are likely to favor companies that can show validated outputs, traceability, and operational evidence at scale.

AI In Cell and Gene Therapy Industry Leaders

NVIDIA

Microsoft

Google DeepMind

Thermo Fisher Scientific, Inc.

Cytiva (Danaher)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Owkin signed a 3-year K Pro AI Scientist licensing agreement with AstraZeneca, under which Owkin will develop bespoke biopharma AI agents integrated into AstraZeneca's research and decision-support workflows, one of the first agentic AI licensing deals in the CGT-adjacent drug development space.

- May 2026: Ginkgo Bioworks launched ADME-One, a fully integrated AI-powered ADME (absorption, distribution, metabolism, excretion) platform for drug discovery, co-developed with Tangible Scientific and Inductive Bio, extending its Datapoints AI-driven lab-in-the-loop workflows into pharmacokinetic modeling relevant to CGT small molecule and genetic payloads.

- April 2026: Profluent and Eli Lilly announced a multi-program strategic collaboration to develop AI-designed site-specific recombinases for genetic medicine, the second major Lilly-AI partnership in the CGT space within four months, targeting precision gene insertion across multiple disease indications.

Global AI In Cell and Gene Therapy Market Report Scope

According to the report’s scope, the AI in cell and gene therapy market refers to the use of artificial intelligence technologies, including machine learning, predictive analytics, and automation tools, to enhance the discovery, development, manufacturing, and commercialization of cell and gene therapies. AI helps improve target identification, optimize clinical trials, streamline bioprocessing, and accelerate personalized treatment development across regenerative medicine and advanced therapeutics.

The AI in cell and gene therapy market is segmented into component, deployment, therapy type, application, end user, and geography. By component, the market is segmented into software / AI platforms and services. By deployment, the market is segmented into cloud-based, on-premises, and edge/hybrid. By therapy type, the market is segmented into cell therapy and gene therapy. By application, the market is segmented into discovery and pre-clinical, clinical validation, commercial manufacturing, and post-market surveillance. By end user, the market is segmented into pharmaceutical and biotechnology companies, contract research organizations (CROs), contract development and manufacturing organizations (CDMOs), and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software / AI platforms |

| Services |

| Cloud-Based |

| On-Premises |

| Edge / Hybrid |

| Cell Therapy |

| Gene Therapy |

| Discovery and Pre-Clinical |

| Clinical Validation |

| Commercial Manufacturing |

| Post-market Surveillance |

| Pharmaceutical and Biotechnology Companies |

| Contract Research Organizations (CROs) |

| Contract Development and Manufacturing Organizations (CDMOs) |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software / AI platforms | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Edge / Hybrid | ||

| By Therapy Type | Cell Therapy | |

| Gene Therapy | ||

| By Application | Discovery and Pre-Clinical | |

| Clinical Validation | ||

| Commercial Manufacturing | ||

| Post-market Surveillance | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| Contract Research Organizations (CROs) | ||

| Contract Development and Manufacturing Organizations (CDMOs) | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Which region leads revenue today?

North America leads, with 51.62% share in 2025. Its strength comes from dense sponsor presence, strong compute infrastructure, and an active FDA framework for regulated AI-related software.

Which region is expanding the fastest?

Asia-Pacific is the fastest-growing region, with a projected 23.62% CAGR through 2031. China, Japan, and South Korea are the key growth centers.

Why do software/AI platforms account for the largest share?

Software/AI platforms held 48.24% of revenue in 2025 because buyers value model orchestration, predictive analytics, and workflow integration more than stand-alone implementation support.

What is driving growth in AI for cell and gene therapy through 2031?

Growth is being driven by larger single-cell and multi-omic datasets, rising pharma investment in AI platforms, and wider access to GPU compute. The sector is projected to grow from USD 1.38 billion in 2026 to USD 3.68 billion by 2031 at 21.61% CAGR.

Page last updated on: