AI In Biotechnology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

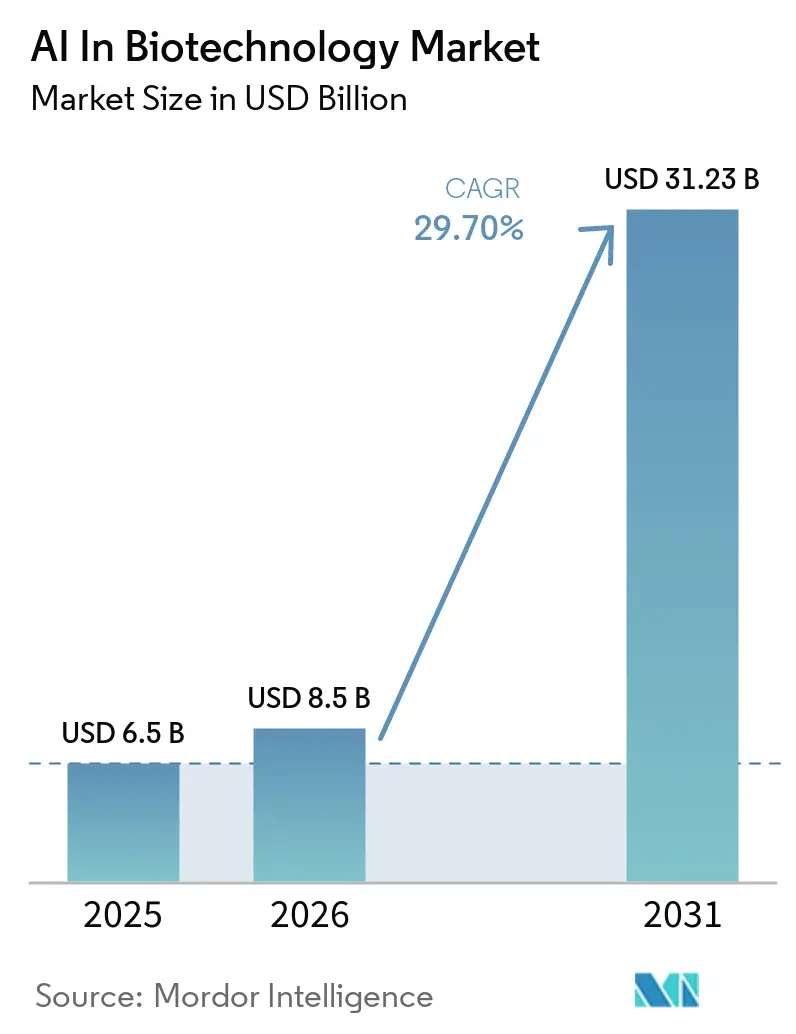

| Market Size (2026) | USD 8.5 Billion |

| Market Size (2031) | USD 31.23 Billion |

| Growth Rate (2026 - 2031) | 29.70% CAGR |

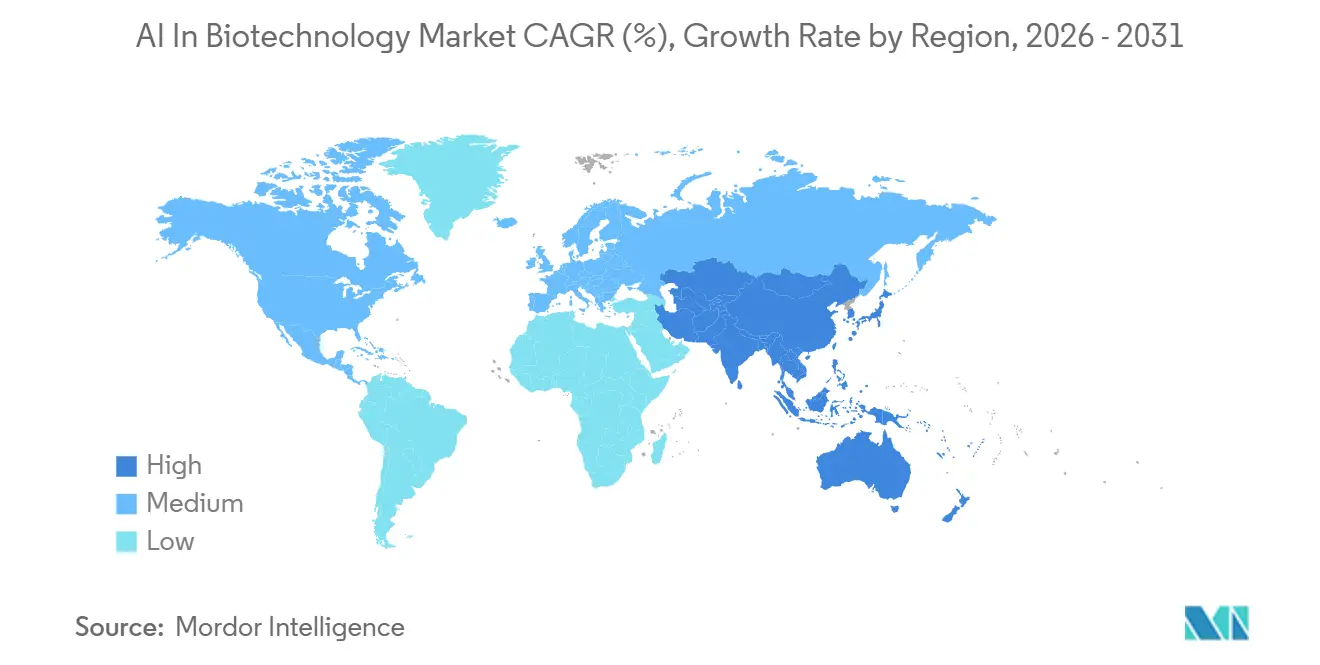

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

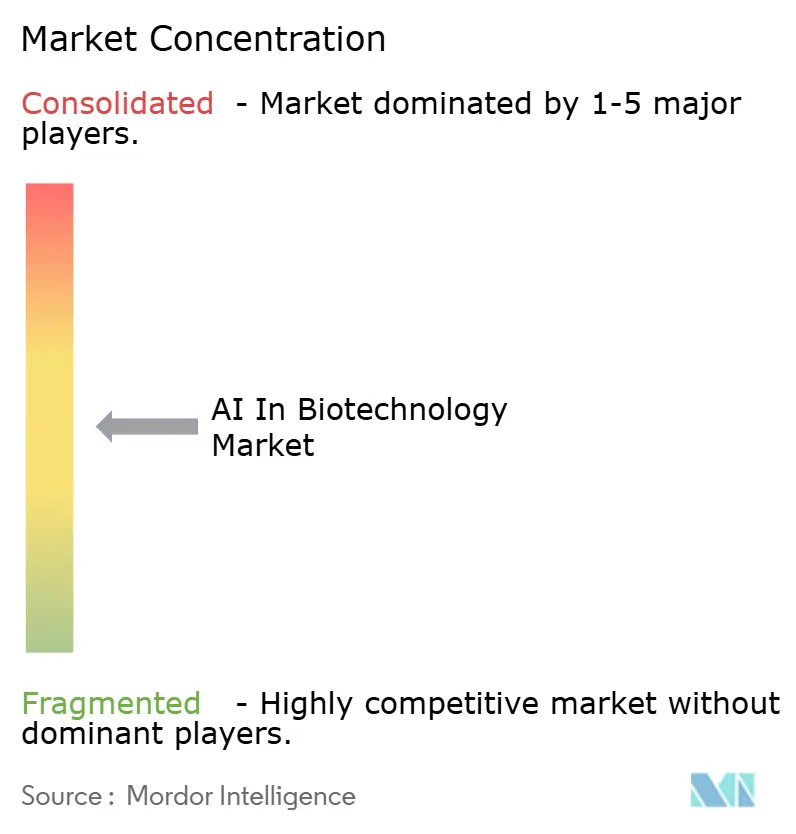

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Biotechnology Market Analysis by Mordor Intelligence

The AI In Biotechnology Market size was valued at USD 6.5 billion in 2025 and is estimated to grow from USD 8.5 billion in 2026 to reach USD 31.23 billion by 2031, at a CAGR of 29.70% during the forecast period (2026-2031).

High drug development costs, growing volumes of biological data, and the adoption of foundation models by life science companies are driving the expansion of the AI in biotechnology market. AI systems are accelerating early discovery cycles, reducing the need to screen numerous compounds, and enabling major drug manufacturers to manage broader pipelines without proportional cost increases. The market is witnessing a shift, with significant partnerships and funding rounds focusing on shared labs, integrated platforms, and long-term infrastructure commitments. This marks a departure from the earlier trend of small pilot contracts, reflecting a more strategic approach to AI adoption in biotechnology.

Key Report Takeaways

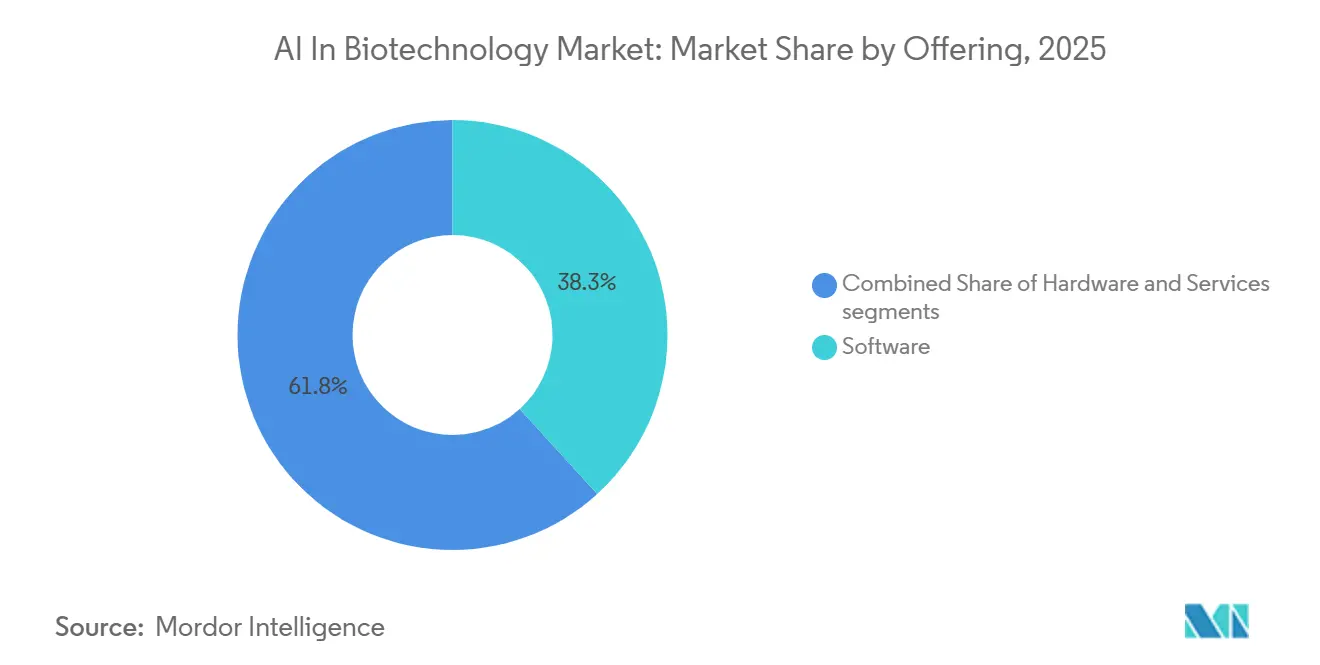

- By offering, software held 38.25% of the market in 2025, while services are projected to grow at a 31.45% CAGR through 2031.

- By application, drug discovery and development accounted for 45.3% in 2025, while clinical development is forecast to expand at a 33.24% CAGR through 2031.

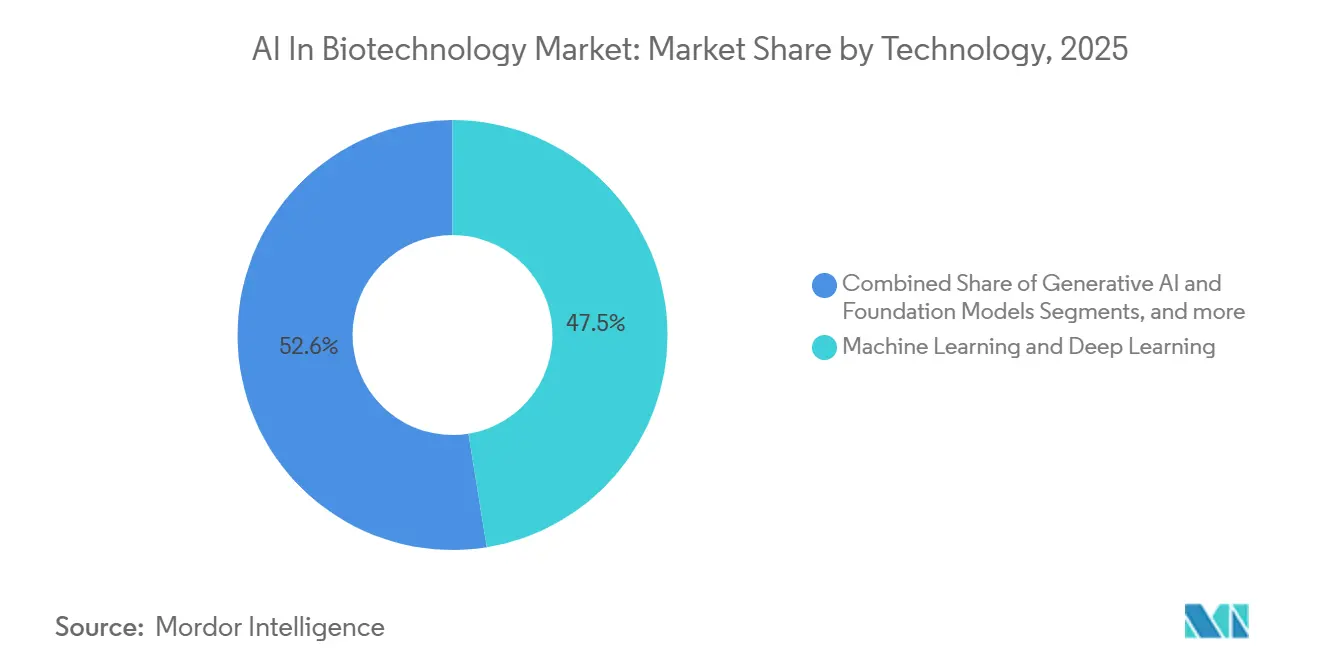

- By technology, machine learning and deep learning represented 47.45% in 2025, while natural language processing and knowledge graphs are expected to grow at a 34.35% CAGR through 2031.

- By deployment mode, cloud-based deployment captured 44.35% in 2025, while on-premises deployment is expected to advance at a 28.95% CAGR through 2031.

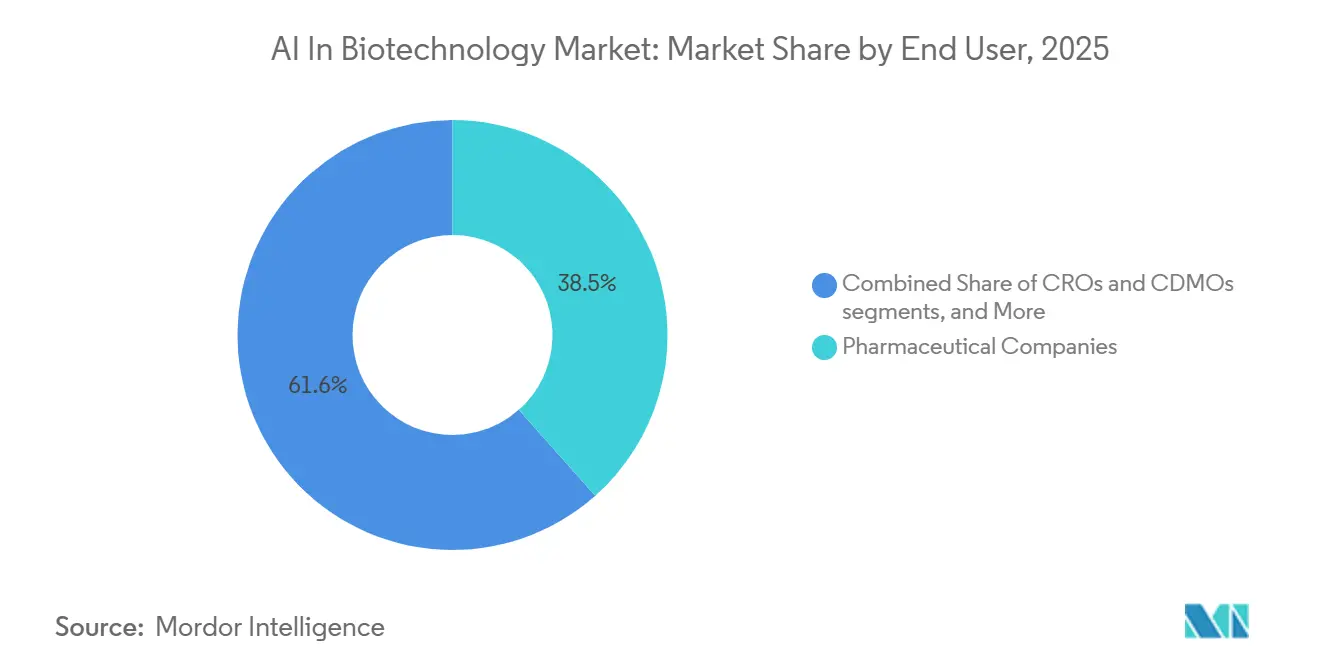

- By end user, pharmaceutical companies held 38.45% in 2025, while CROs and CDMOs are projected to rise at a 32.65% CAGR through 2031.

- By geography, North America led with 41.7% in 2025, while Asia-Pacific is forecast to record a 35.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Biotechnology Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| AI-led drug discovery acceleration | +6.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Precision medicine and biomarker-guided therapeutics | +5.8% | North America, Europe, with early gains in APAC | Long term (≥ 4 years) |

| Scaling genomic and multi-omics datasets | +4.5% | Global, high-growth vectors in China, India, South Korea | Medium term (2-4 years) |

| Biopharma-tech partnerships and funding momentum | +5.5% | Global, led by North America and UK | Short term (≤ 2 years) |

| Self-driving labs and closed-loop wet-lab automation | +3.8% | North America, Europe, spillover to APAC core | Medium term (2-4 years) |

| Federated multi-institution model training | +2.5% | Global, early deployment in EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Led Drug Discovery Accelerates

AI is driving significant advancements in early drug discovery, focusing on speed and compound efficiency alongside model performance. In 2025, Rentosertib became the first fully AI-designed and AI-discovered drug to complete Phase IIa trials, showing a mean forced vital capacity improvement of +98.4 mL compared to -20.3 mL for placebo in idiopathic pulmonary fibrosis patients.[1]Insilico Medicine, “Insilico Medicine Case Study, Insilico's Transformation,” Insilico Medicine, insilico.com Recursion demonstrated its platform's efficiency by synthesizing nearly 330 compounds per program in 17 months, compared to the industry average of 2,500 compounds in 42 months, with its REC-4881 program achieving a 43% median reduction in total polyp burden at 12 weeks in Phase 2 patients.[2]Recursion Reports Fourth Quarter and Full Year 2025 Financial Results and Provides Business Update,” GlobeNewswire, globenewswire.comThese developments highlight how AI is reshaping drug discovery economics, enabling pharmaceutical companies to diversify targets and indications, reducing reliance on conservative approaches.

Precision Medicine and Biomarkers Take Center Stage

The AI in biotechnology market is advancing with biomarker-guided research, where model quality depends on integrating molecular, clinical, and patient-level data. Sanofi's AI Research Factory improved active ingredient identification in immunology, oncology, and neurology by 20-30% over traditional methods, doubling the number of biologics and vaccines developed with AI since 2019. Precision medicine programs require robust patient stratification, biomarker selection, and early response variability insights. AI platforms capable of analyzing genomic and transcriptomic layers are enabling sponsors to identify enriched populations early, making smaller, complex patient groups commercially viable, especially in rare diseases and specialty areas.

Harnessing the Power of Vast Genomic and Multi-Omics Datasets

Dataset scale is becoming a critical advantage in the AI biotechnology market, as model performance improves with diverse biological data. Recursion has built a dataset exceeding 50 petabytes, supported by millions of weekly experiments across phenomics, transcriptomics, and proteomics. In China, large foundation models like CellFM and multimodal biomedical models trained on proprietary datasets spanning molecules, cells, tissues, and clinical layers are advancing research. A 2025 review highlighted AI-driven active compound discovery improving prediction accuracy for drug-like interactions by over 50%, while antibody design models achieved 16-20% hit rates by testing only 20 candidates.[3]Rory Kelleher, “Drug Discovery, STAT! NVIDIA, Recursion Speed Pharma R&D With AI Supercomputer,” NVIDIA Blog, blogs.nvidia.com Federated model development is also gaining traction, allowing broader dataset training while maintaining data privacy.

Biopharma-Tech Collaborations Gain Momentum

The AI in biotechnology market is progressing with larger deals, deeper partnerships, and increased patient capital. In 2026, Earendil Labs raised USD 787 million from investors, including Sanofi and Pfizer, and reported over 40 development programs generated by its platform. NVIDIA and Eli Lilly launched a co-innovation AI lab with up to USD 1 billion funding over five years, reflecting a shift toward collaborative scientific environments. These funding patterns accelerate the transition from model development to adoption in regulated research, supporting self-driving labs and automated wet-lab experimentation. This operational model is driving the market from pilot projects to scalable platform deployments across discovery, validation, and biologics development.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High implementation and validation cost | -3.2% | Global, most acute in emerging markets and smaller biotechs | Short term (≤ 2 years) |

| Data privacy and regulatory compliance burden | -2.8% | EU, North America | Medium term (2-4 years) |

| GPU and advanced compute bottlenecks | -1.5% | Global, concentrated in non-US markets | Short term (≤ 2 years) |

| IP and GxP auditability uncertainty | -1.1% | Global, most acute in regulated markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation and Validation Costs

The AI biotechnology market faces high entry barriers due to production-grade deployment costs exceeding pilot budgets. Challenges extend beyond model building to include data cleaning, workflow integration, validation records, and internal team support for regulated use. Smaller biotechnology firms and academic spinouts often lag large pharmaceutical companies by 12-24 months in commercial deployment due to the absence of established legal and computational frameworks. Limited access to GPUs and specialized infrastructure outside major U.S. hubs further favors well-funded platforms and large enterprise buyers, slowing smaller firms' transition from experimental AI drug discovery to operational use.

Data Privacy and Regulatory Compliance Challenges

Privacy regulations, regulatory reviews, and the need to document model behavior in regulated environments create friction in the AI biotechnology market. Cross-border model training remains complex, requiring formal agreements, local data controls, and continuous oversight, even with federated approaches. In healthcare and life sciences, developers must ensure transparency, traceability, and human oversight before AI supports critical decisions. Additionally, issues like IP ownership, audit trails, and GxP-ready documentation slow cross-institution collaborations and rollout in regulated markets, making compliance a core operational requirement for the sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Anchors Revenue, Services Scale Fastest

In 2025, software accounted for 38.25% of the AI in biotechnology market, maintaining its leading position among offerings. This dominance stems from platform-driven business models by companies like Insilico Medicine and Recursion Pharmaceuticals, leveraging recurring revenues through licenses and API access. The reuse of trained models across multiple programs without proportional cost increases further strengthens software's role. Eli Lilly's TuneLab platform, launched in September 2025, exemplifies scalable software delivery by providing external partners access to drug discovery models while safeguarding proprietary data. Software remains the revenue anchor, aligning with pharmaceutical companies' needs for accessible models and workflows.

Services are the fastest-growing segment in the AI in biotechnology market, with a projected CAGR of 31.45% through 2031. Many drug manufacturers prefer outsourcing tasks like model development and data curation instead of building in-house capabilities. This trend persists as successful deployment requires domain expertise, model tuning, and regulatory support, beyond just tool access.

By Application: Drug Discovery Dominates, Clinical Development Accelerates

Drug discovery and development held 45.3% of the AI in biotechnology market share in 2025, making it the largest application area. AI-first platforms significantly reduce synthesized molecules per program by over 90% while maintaining or improving hit rates. Recursion's platform generates over 100 million molecules annually, reducing wet-lab work by 40% and addressing cost and timing challenges in pharmaceutical R&D. AI drug discovery drives adoption by narrowing candidate pools, improving prioritization, and minimizing lab work before advancing programs.

Clinical development is the fastest-growing application in the AI in biotechnology market, with a projected CAGR of 33.24% through 2031. AI enhances trial operations by improving speed, enrollment planning, and execution. For example, AI platforms have reduced patient registration times and Phase III costs significantly. These operational gains justify broader AI deployment in clinical development, making it the fastest-growing area while drug discovery remains the largest application.

By Technology: Machine Learning Leads the Foundation, NLP and Knowledge Graphs Gain Momentum

Machine learning and deep learning accounted for 47.45% of the AI in biotechnology market in 2025, maintaining their central role in the technology stack. These technologies support critical tasks like target identification, biomarker work, and manufacturing quality control. NVIDIA's advancements in tools for model training and deployment further enhance machine learning's foundational role in the market. Machine learning remains the core analytical layer, even as specialized approaches gain traction.

Natural language processing (NLP) and knowledge graphs are the fastest-growing technology segment in the AI in biotechnology market, with a projected CAGR of 34.35% through 2031. These tools uncover non-obvious connections in biomedical research, significantly reducing time for tasks like target molecule searches. NLP and knowledge graphs complement machine learning, expanding hypothesis generation and driving adoption in literature-heavy research tasks.

By Deployment Mode: Cloud Scales Discovery, On-Premises Reclaims Ground

Cloud-based deployment held 44.35% of the AI in biotechnology market in 2025, leading among deployment modes. The cloud's flexibility supports early-stage discovery workloads with scalable compute and quick access to pre-trained models. It aligns with vendor strategies focused on platform subscriptions and ecosystem access, making it the preferred infrastructure for many users. Cloud deployment remains dominant for discovery teams needing scalable solutions without local infrastructure delays.

On-premises deployment is the fastest-growing mode in the AI in biotechnology market, with a projected CAGR of 28.95% through 2031. Companies increasingly favor local infrastructure for tighter data control and compliance with regulatory environments. Hybrid models combining on-premises and cloud architectures are gaining traction, especially for sensitive workloads. This shift reflects the growing importance of balancing cloud flexibility with local control for critical data and workflows.

By End User: Pharmaceutical Companies Lead Investment, CROs and CDMOs Define Growth Velocity

Pharmaceutical companies held 38.45% of the AI in biotechnology market in 2025, making them the largest end-user group. Their leadership is driven by substantial R&D investments and the financial benefits of improved productivity. Major players are also investing in infrastructure, building long-term capabilities beyond pilot projects. Biotechnology companies, the second-largest group, play a key role in advancing AI-native pipelines and validating broader platforms.

CROs and CDMOs are the fastest-growing end-user segment in the AI in biotechnology market, with a projected CAGR of 32.65% through 2031. These organizations are critical in accelerating AI adoption in outsourced research, development, and manufacturing. Their ability to deliver faster, cost-efficient solutions is driving growth as biopharma clients increasingly demand AI-enabled services. This trend positions CROs and CDMOs as key growth drivers in the market.

Geography Analysis

In 2025, North America commanded a dominant 41.7% share of the AI in biotechnology market, solidifying its top regional position. The region benefits from a strong venture capital base, extensive AI research talent, and a high concentration of pharmaceutical R&D headquarters. Significant infrastructure investments connect computing, biology, and drug development, with major collaborations reflecting the scale of investment in shared discovery environments. This combination of resources positions North America as a leader in platform development and enterprise adoption.

Europe holds a significant position in the AI in biotechnology market, combining a strong pharmaceutical foundation with a coordinated AI policy framework. Key hubs like Germany, the UK, France, Italy, and Spain drive commercial activity, while Austria and Nordic countries contribute research depth. The region's interconnected academic, biotech, and pharmaceutical networks support adoption across discovery and translational research. Stricter governance adds compliance challenges but establishes a formal framework for healthcare AI.

Asia-Pacific is the fastest-growing region in the AI in biotechnology market, with a forecast CAGR of 35.5% through 2031. Growth is driven by policy support, expanding research capacity, and local platform development in China, Japan, South Korea, and India. Milestones include China's launch of an AI-driven drug virtual screening platform and the introduction of AI Kongming for intelligent drug design. These developments highlight the region's focus on building domestic models and scalable research systems. The Middle East and Africa remain in early stages, with GCC precision medicine programs and South Africa's genomics base laying the groundwork for future adoption. South America, led by Brazil's clinical research ecosystem, is also in the early stages of development. While smaller today, these regions are building the foundation for broader AI adoption in biotechnology workflows. North America leads, Europe remains pivotal, and Asia-Pacific drives the fastest growth.

Competitive Landscape

The AI in biotechnology market features a competitive landscape divided between a select few vertically integrated AI-native platforms and a broader array of point-solution providers. Companies like Recursion Pharmaceuticals, Insilico Medicine, Schrödinger, Valo Health, and XtalPi compete with comprehensive discovery capabilities. In contrast, other firms focus on specialized areas such as AI pathology, genomic data management, federated oncology models, and NLP-driven target discovery.

Competitive pressures intensify as capital and strategic alliances concentrate on the platform layer. NVIDIA and Eli Lilly have committed up to USD 1 billion over five years to a co-innovation AI lab, highlighting the growing focus on compute, data science, and lab workflows. Isomorphic Labs secured USD 2.1 billion in Series B funding in May 2026 to scale its AI drug design engine, reflecting the capital influx toward integrated platforms with strong strategic backing. Similarly, Earendil Labs raised USD 787 million in March 2026 to expand its AI-driven biologics discovery platform and future IND activities, compressing timelines for mid-tier vendors lacking comparable scale or funding.

At the same time, the AI in biotechnology market still accommodates distinct specialists. Owkin stands out with federated learning for privacy-preserving multi-institution collaborations, while CytoReason and Iktos address specific workflow needs within larger pharmaceutical partnerships. White-space opportunities are strongest in AI bioprocessing and GxP-ready manufacturing, where operational improvements are significant, but competition remains limited. While consolidation is evident in discovery platforms, the broader market remains active, with buyers seeking specialized tools and partners for specific challenges.

AI In Biotechnology Industry Leaders

Insilico Medicine

Recursion Pharmaceuticals, Inc.

Insitro, Inc.

BenevolentAI SA

Owkin, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Isomorphic Labs secured USD 2.1 billion in Series B funding to expand its AI drug design engine (IsoDDE) across therapeutic areas and accelerate its pipeline toward clinical development. Strategic partnerships with Novartis, Lilly, and Johnson & Johnson highlight the platform's commercial traction.

- April 2026: FRONTEO and Astellas Pharma signed a target molecule discovery agreement using FRONTEO's Drug Discovery AI Factory (DDAIF) powered by KIBIT NLP AI. This collaboration reduces the traditional 2-year process to 2 days, enhancing FRONTEO's co-creation ecosystem.

- April 2026: FRONTEO and Tokyo University of Science opened a joint AI drug discovery research center at Yokohama Campus. The center integrates KIBIT-based target identification with advanced cell-state analysis and focuses on oncology with plans to out-license discoveries.

- March 2026: Earendil Labs raised USD 787 million to scale its AI-driven biologics discovery platform, which has over 40 development programs. The company plans multiple IND submissions in 2026-2027, including a Sanofi license for bispecific antibodies in autoimmune and inflammatory diseases.

- March 2026: Arctoris launched a Biophysics Centre of Excellence, expanding its AI-ready biophysical instrumentation tenfold. The SPRneo system enables autonomous protocol design, real-time optimization, and live analysis, supporting a closed-loop discovery model.

Global AI In Biotechnology Market Report Scope

As per the scope of the report, AI in biotechnology refers to the integration of machine learning, deep learning, and computational models with biological sciences to analyze complex biological data. It accelerates research by automating tasks, predicting biological outcomes, and shifting scientists from trial-and-error methods to data-driven discovery.

The AI in biotechnology market is segmented by offering, application, technology, deployment mode, end-user, and geography. By offering, the market includes software, hardware, and services. By application, the market is segmented into drug discovery and development, genomics and multi-omics analysis, clinical development, diagnostics and decision support, precision medicine, and bioprocessing and manufacturing. By technology, the market is categorized into machine learning and deep learning, generative AI and foundation models, natural language processing and knowledge graphs, computer vision, and graph, causal, and systems biology models. By deployment mode, the market is segmented into cloud-based, hybrid, and on-premises. By end-user, the market is segmented into pharmaceutical companies, biotechnology companies, CROs and CDMOs, academic and research institutes, and healthcare providers and diagnostic laboratories. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Software |

| Hardware |

| Services |

| Drug Discovery and Development |

| Genomics and Multi-Omics Analysis |

| Clinical Development |

| Diagnostics and Decision Support |

| Precision Medicine |

| Bioprocessing and Manufacturing |

| Machine Learning and Deep Learning |

| Generative AI and Foundation Models |

| Natural Language Processing and Knowledge Graphs |

| Computer Vision |

| Graph, Causal, and Systems Biology Models |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Pharmaceutical Companies |

| Biotechnology Companies |

| CROs and CDMOs |

| Academic and Research Institutes |

| Healthcare Providers and Diagnostic Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Software | |

| Hardware | ||

| Services | ||

| By Application | Drug Discovery and Development | |

| Genomics and Multi-Omics Analysis | ||

| Clinical Development | ||

| Diagnostics and Decision Support | ||

| Precision Medicine | ||

| Bioprocessing and Manufacturing | ||

| By Technology | Machine Learning and Deep Learning | |

| Generative AI and Foundation Models | ||

| Natural Language Processing and Knowledge Graphs | ||

| Computer Vision | ||

| Graph, Causal, and Systems Biology Models | ||

| By Deployment Mode | Cloud-Based | |

| Hybrid | ||

| On-Premises | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| CROs and CDMOs | ||

| Academic and Research Institutes | ||

| Healthcare Providers and Diagnostic Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of AI in biotechnology by 2031?

The AI in biotechnology market is forecast to reach USD 31.23 billion by 2031 from USD 8.50 billion in 2026, growing at a 29.70% CAGR.

Which application area leads adoption in AI-enabled biotechnology?

Drug discovery and development leads with a 45.3% share in 2025 because it offers the clearest gains in candidate screening, prioritization, and timeline compression.

Which region is growing the fastest in this space?

Asia-Pacific is the fastest-growing region with a 35.5% CAGR through 2031, supported by coordinated policy backing and expanding domestic platform development.

Why are pharmaceutical companies the largest end users?

Pharmaceutical companies held 38.45% in 2025 because their large R&D budgets make gains in speed, hit rates, and program efficiency financially meaningful.

What is driving growth in services for AI in biotechnology?

Services are projected to grow at a 31.45% CAGR because many companies still prefer outsourced model development, data curation, and validation support instead of building everything in-house.

How is competition evolving among AI biotechnology vendors?

Competition is tightening at the platform layer as larger players secure major funding rounds and strategic labs, while specialist vendors continue to compete in narrower workflow niches.

Page last updated on: