AI In Genomics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.77 Billion |

| Market Size (2031) | USD 9.93 Billion |

| Growth Rate (2026 - 2031) | 41.25% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Genomics Market Analysis by Mordor Intelligence

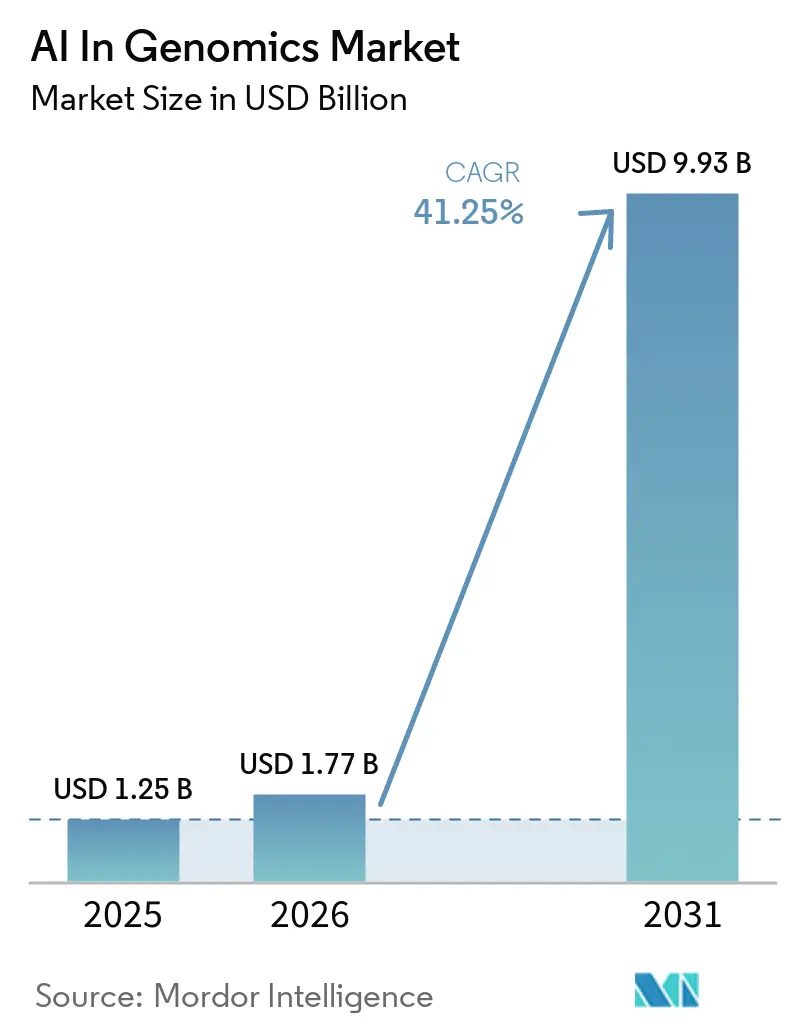

The AI In Genomics Market size was valued at USD 1.25 billion in 2025 and is estimated to grow from USD 1.77 billion in 2026 to reach USD 9.93 billion by 2031, at a CAGR of 41.25% during the forecast period (2026-2031).

The AI in genomics market is expanding on the back of a structural change in genomic workflows, because manual interpretation has become the main bottleneck in both clinical and research settings and AI now carries the scaling burden that sequencing hardware alone cannot solve. Genome Canada reported that annual genomic data generation has moved into tens of exabytes, and that scale is pushing research organizations to use AI as either a core objective or a direct analytical tool. The AI in genomics market is also benefiting from a shift in spending toward interpretation software, validation services, and platform partnerships, which is changing budgets in pharma, healthcare, and agriculture. At the same time, the AI in genomics market faces uneven regulation and uneven training data coverage, especially where European-ancestry datasets dominate model development and raise deployment limits in other populations. Even with those constraints, falling sequencing costs, genomic foundation models, and larger pharma platform deals keep the AI in genomics market on a strong growth path through 2031.

Key Report Takeaways

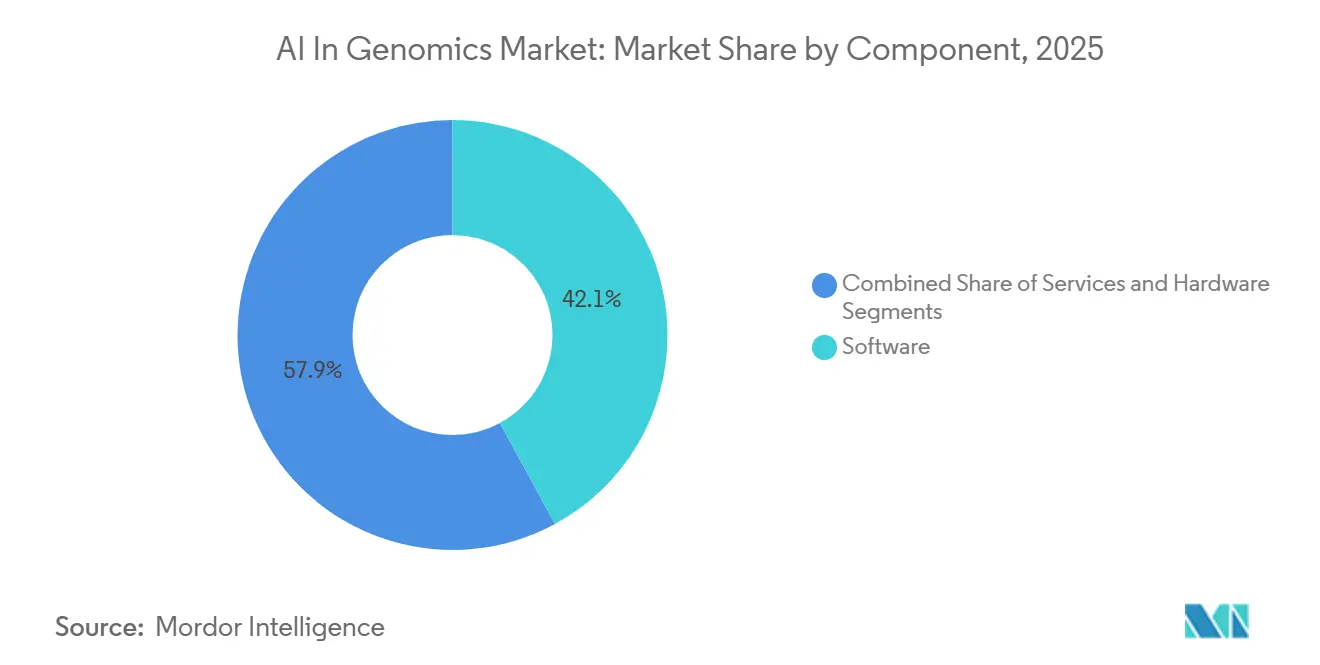

- By component, software held 42.10% of the AI in genomics market share in 2025, while services is projected to expand at a 42.87% CAGR through 2031.

- By technology, machine learning accounted for 63.18% share of the AI in genomics market size in 2025, while natural language processing is forecast to grow at a 43.18% CAGR through 2031.

- By functionality, genome sequencing led with 44.19% revenue share in 2025, while the source draft identifies gene editing as the second-largest functionality and clinical workflow tools as a rising area of adoption.

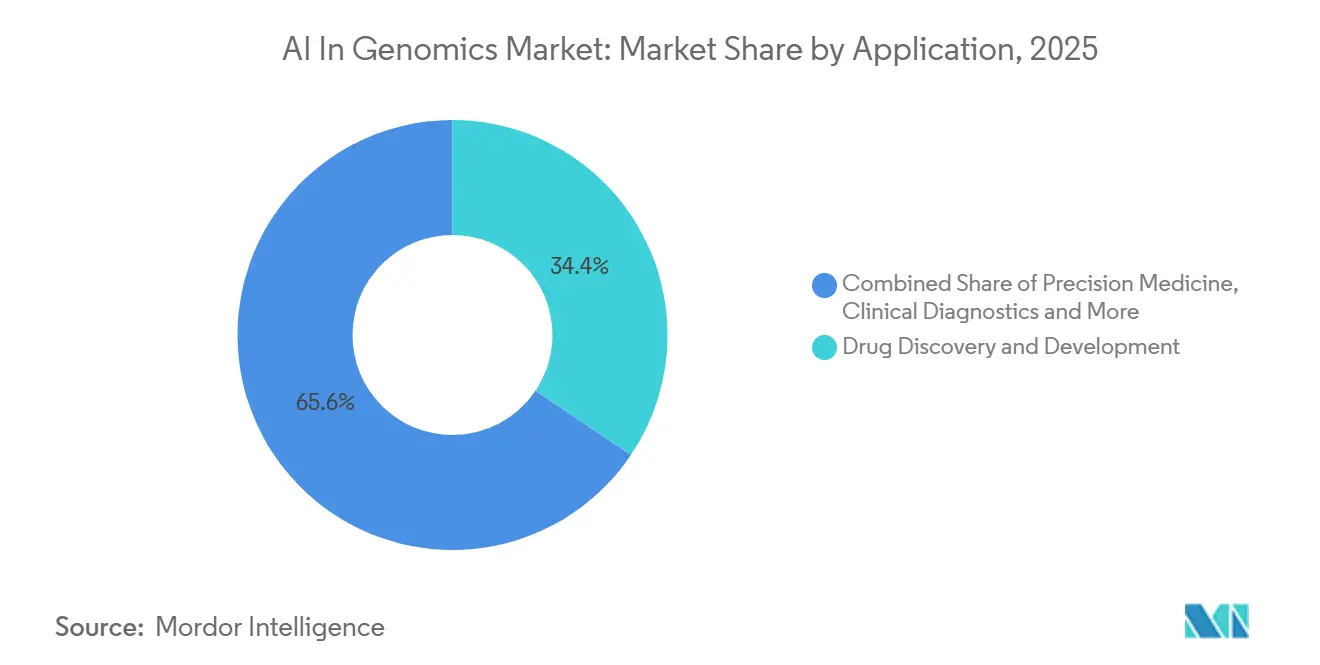

- By application, drug discovery and development captured 34.41% revenue share in 2025, while precision medicine is forecast to expand at a 43.69% CAGR through 2031.

- By deployment model, cloud-based deployment held 46.18% share in 2025, while hybrid deployment is projected to grow at a 44.11% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies accounted for 38.22% revenue share in 2025, while clinical laboratories and diagnostic centers are forecast to advance at a 42.41% CAGR through 2031.

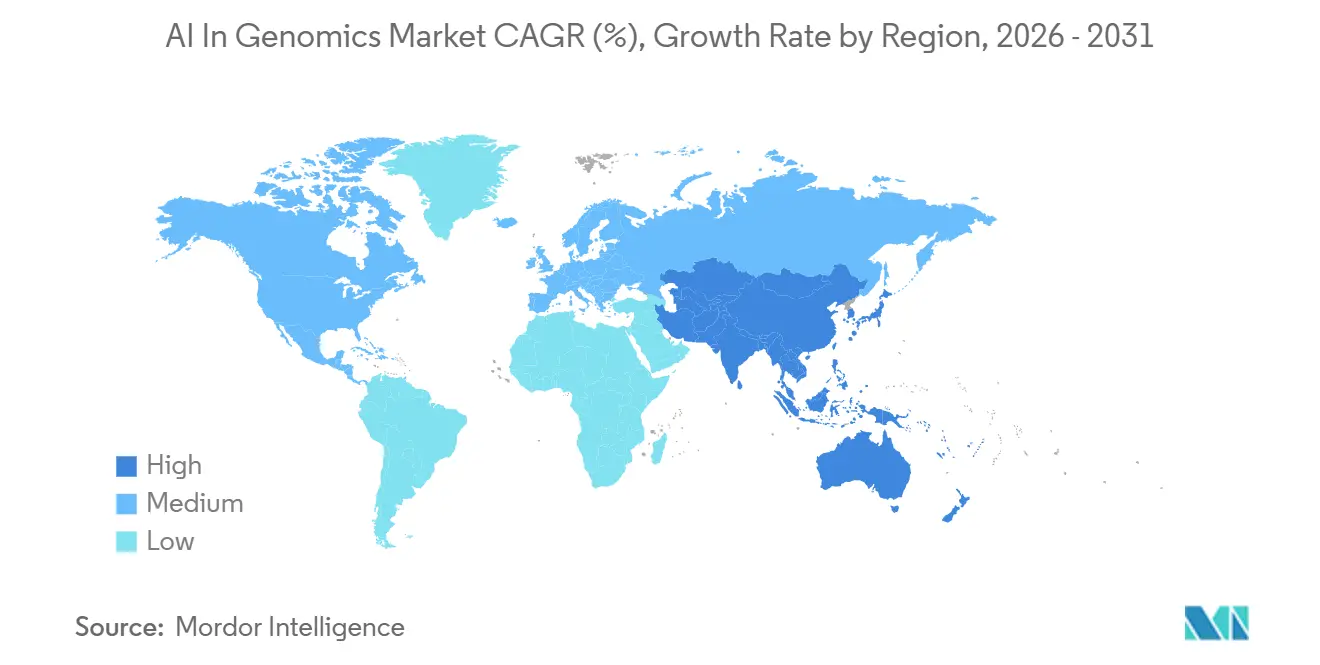

- By geography, North America held 38.52% of the AI in genomics market share in 2025, while Asia-Pacific is projected to expand at a 42.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Genomics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Genomic Data Explosion Outpacing Manual Interpretation | +8.5% | Global, with intensity in North America, EU, and APAC genomics hubs | Short term (≤ 2 years) |

| Precision Medicine Scaling Across Oncology and Rare Disease | +7.0% | North America and EU core, spill-over to APAC and MEA national programmes | Medium term (2-4 years) |

| AI-Led Drug Discovery Shortening Hypothesis Cycles | +7.5% | North America and EU, growing in Japan and China | Medium term (2-4 years) |

| Falling Sequencing Costs Widening Multi-Omic Adoption | +6.0% | Global, with fastest uptake in APAC and South America | Short term (≤ 2 years) |

| Noncoding Variant Interpretation Lifting Diagnostic Yield | +5.0% | EU, North America, emerging in Japan and Australia | Medium term (2-4 years) |

| Genomic Foundation Models Improving Multi-Task Inference | +5.5% | Global, with compute concentration in North America and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Genomic Data Explosion Outpacing Manual Interpretation

A single whole-genome sequence can generate 200 GB to 300 GB of raw data, and annual genomic data output now runs into tens of exabytes globally. That data load is growing faster than manual analyst teams can review it, so the AI in genomics market is increasingly tied to interpretation speed rather than to data generation alone. This shift also favors vendors that combine algorithms with large, labeled, clinically validated variant libraries, because curation quality matters as much as model design once throughput becomes the constraint. SeqOne’s acquisition of Congenica in September 2025 reflected that logic, as the combined platform brought AI sequencing analytics together with a clinical decision library derived from the Wellcome Sanger ecosystem. The combined operation processed more than 200,000 patient genomic analyses in 2025, which was a 3-fold increase over 2024 and shows how fast scaled interpretation platforms are moving into routine use. In practical terms, the AI in genomics market now rewards data curation depth, case volume, and workflow automation more than stand-alone model claims.

Precision Medicine Scaling Across Oncology and Rare Disease

The AI in genomics market is seeing stronger demand from precision medicine, especially where oncology and rare disease programs now rely on the same interpretation stack. A 2025 study in Clinical and Experimental Medicine found that an autonomous AI agent that combined histopathology and genomics reached 91% accuracy for microsatellite instability diagnosis, which is a key biomarker for immunotherapy selection. That result matters because it supports the use of unified models across tissue, molecular, and clinical data rather than isolated decision tools. In rare disease, GeneDx reported preliminary 2025 revenue of USD 427 million, up 41% year over year, while exome and genome revenue grew 54% as genomic newborn screening expanded through state-backed programs[1]GeneDx, “GeneDx Announces Preliminary 2025 Financial Results and Provides 2026 Guidance,” Business Wire, businesswire.com. Those two care pathways are no longer developing in isolation, and that is widening the addressable demand base for the AI in genomics market. The same operating model that supports therapy matching in oncology can also support fast diagnosis in pediatric and inherited disorders.

AI-Led Drug Discovery Shortening Hypothesis Cycles

Drug discovery remains one of the clearest spending channels for the AI in genomics market, because AI is reducing the time between target hypothesis and candidate design. Profluent’s AI foundation models were trained on large recombinase datasets and can design site-specific enzymes for exact genomic targets, which enabled Eli Lilly to enter a collaboration worth up to USD 2.25 billion in April 2026. Illumina’s Alliance for Genomic Discovery expanded to 312,000 paired whole genomes and clinical records in March 2026 after Regeneron Genetics Center joined as the tenth member, which shows the scale of data infrastructure feeding these discovery systems. Tempus AI also stated in early 2026 that it had active contracts with 19 of the top 20 pharmaceutical companies and more than USD 2 billion in signed data and applications contracts. These partnerships show that capital is moving beyond single assets and into repeatable data and model platforms. The AI in genomics market therefore gains not only from molecule design, but also from proprietary data flywheels that become harder for smaller competitors to match.

Falling Sequencing Costs Widening Multi-Omic Adoption

Lower sequencing costs are expanding the practical use cases for the AI in genomics market, because more routine testing means more phenotypic and longitudinal data for model training. Illumina stated in February 2026 that TruPath Genome reduced workflow complexity by removing traditional library preparation and supported output of 16 whole genomes per day. Once sequencing becomes easier to run in everyday clinical settings, data diversity improves, and that strengthens downstream AI performance across variant interpretation and patient stratification. The effect is not limited to volume, because lower-cost workflows also make multi-omic studies more feasible across research, translational medicine, and clinical diagnostics. This creates a reinforcing cycle where cheaper sequencing widens access, wider access improves training data, and better models then increase the value of additional testing. In that environment, the AI in genomics market benefits from both cost reduction upstream and higher interpretation value downstream.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy And Clinical AI Compliance Burden | -3.5% | EU, with AI Act mandatory from Aug 2027, APAC adopting analogous frameworks | Medium term (2-4 years) |

| Scarcity Of AI-Genomics Talent And Curated Labels | -2.5% | Global, most acute in South America and MEA | Long term (≥ 4 years) |

| Eurocentric Training Data Limiting Cross-Ancestry Accuracy | -1.5% | APAC, MEA, South America | Long term (≥ 4 years) |

| Data Sovereignty And Compute Cost Inflation Slowing Scale | -2.0% | Global, heightened in EU, India, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy And Clinical AI Compliance Burden

The AI in genomics market faces a real regulatory barrier in Europe, where the EU AI Act treats genomic IVD systems in higher classes as high-risk AI systems. That framework requires risk management, technical documentation, human oversight, and cybersecurity controls, and full provisions for high-risk systems take effect from August 2027. The burden is heavier for vendors that update models continuously, because documentation must track material model changes rather than cover the entire platform once. France’s national strategy for artificial intelligence and health data, published in 2025, also ties deployment more closely to secondary-use governance and interoperable health data rules. Those rules favor hybrid and locally controlled architectures, which adds cost and slows scale for smaller companies in the AI in genomics market. Compliance therefore acts as a market filter, not because the technology is weak, but because commercialization is becoming more documentation-heavy[2]Anja Segschneider, “AI-Act: Regulierung von KI im Gesundheitswesen,” BIOPRO Baden-Württemberg GmbH, bio-pro.de.

Scarcity of AI-Genomics Talent and Curated Labels

The AI in genomics market is also constrained by a shortage of teams that can combine clinical genomics, machine learning engineering, and production-grade data curation. Training data remains uneven, especially for splice events, structural variants, and deep intronic changes that are less represented in standard benchmark sets. A 2025 study in npj Genomic Medicine found substantial discordance between AlphaMissense outputs and clinical-grade curation in a rare-disease cohort, with precision of 32.9% for expert-curated pathogenic variants. That result shows why algorithm gains alone do not remove the need for curated clinical labels and domain-specific review. The AI in genomics market therefore gives a durable advantage to companies with proprietary case libraries, such as GeneDx and Tempus, because data quality and annotation depth still shape model performance at scale. This slows late entrants, especially where academic tools still need additional labeling work before they can operate reliably in clinical production.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Anchors Revenue While Services Accelerate

Software captured 42.1% of revenue in 2025, which made it the largest component in the AI in genomics market. The segment covers variant interpretation platforms, bioinformatics pipelines, clinical decision-support tools, and genomic foundation model APIs. Its lead position shows that the value stack is moving away from instruments and toward interpretation layers that can be sold on recurring terms. The AI in genomics market is therefore rewarding cloud-native software models that turn analytic logic into a repeatable revenue stream. QIAGEN’s May 2025 acquisition of Genoox, valued at USD 70 million to USD 80 million, confirmed this direction by adding the Franklin AI cloud platform to its Digital Insights portfolio. Franklin was active in more than 4,000 healthcare organizations across 50 countries and had supported more than 750,000 case interpretations at the time of the deal.

Services is the fastest-growing component, with a projected CAGR of 42.87% from 2026 to 2031. That pace reflects how much implementation, validation, and ongoing model maintenance matter once AI tools enter regulated environments. The AI in genomics market increasingly depends on professional services because laboratories and health systems often need support for integration, audit trails, and post-deployment tuning. Hardware remains the slowest-growing component, but it still matters in throughput-heavy workflows where compute performance shapes turnaround time. NVIDIA stated in March 2025 that Parabricks v4.5 reduced whole-genome germline analysis to under 8 minutes using 4 GPUs and added support for Blackwell architecture. That matters because software gains are strongest when labs can also process data at scale without long compute bottlenecks. Over time, the AI in genomics industry is likely to see more end-to-end contracts that bundle software, implementation services, and hardware acceleration into a single operating model. Those bundled deals raise switching costs and can stretch customer lifetime value well beyond an initial software subscription.

By Technology: Machine Learning Dominates While NLP Reshapes the Interface Layer

Machine learning held 63.18% of revenue in 2025, which kept it at the center of the AI in genomics market. Machine learning supports variant-effect prediction, polygenic risk scoring, biomarker classification, and other core tasks across research and clinical use. Classical methods such as gradient boosting and random forests still fit smaller and lower-dimensional clinical datasets well. Deep learning is more useful when the workflow involves large multi-omic inputs and higher-dimensional feature fusion. A systematic review in Clinical and Experimental Medicine reported that graph neural networks and attention-based models delivered strong performance in multi-omic oncology settings. That mix means the AI in genomics market is not moving toward a single model architecture, but toward a layered toolkit where older and newer methods coexist.

Natural language processing is the fastest-growing technology, with a projected CAGR of 43.18% through 2031. That growth comes from foundation model architectures that can read clinical notes, scientific literature, and variant databases in the same workflow. Tempus One added GenAI capabilities in January 2025 that supported patient timeline synthesis, prior authorization assistance, and querying across large volumes of unstructured documents. In the AI in genomics market, this moves NLP from a background enrichment role into the main clinical interface layer. Computer vision also retains a meaningful role in spatial multi-omic and digital pathology workflows, especially where image and molecular data need to be read together. Other methods, including reinforcement learning for design tasks and Bayesian methods for uncertainty handling, are still smaller parts of the mix but continue to widen the technical base of the AI in genomics market.

By Functionality: Sequencing Workflows Define Market Gravity

Genome sequencing accounted for 44.19% of revenue in 2025, making it the largest functional segment in the AI in genomics market. It is also expected to be the fastest-growing segment, registering a CAGR of 42.34% through 2031. That share reflects more than raw data generation, because AI now sits inside basecalling, alignment, variant calling, and quality scoring within the sequencing workflow itself. The AI in genomics market therefore draws a large part of its value from software layers that operate before formal interpretation even begins. Oxford Nanopore stated that its Dorado basecaller uses LSTM and transformer architectures for nanopore signal processing, runs on NVIDIA GPUs, processes hundreds of millions of signal samples per second, and achieves below 1% error from a single DNA strand. That kind of embedded AI raises the performance baseline for sequencing-led workflows. It also makes sequencing functionality harder to separate from software functionality in commercial terms.

Gene editing remained the second-largest functionality in the source draft, and its momentum is tied to AI-designed enzyme platforms. Profluent’s recombinase work, licensed by Eli Lilly in April 2026, shows how AI is extending editing beyond the insertion limits that constrain earlier approaches. Clinical workflow functionality is also moving higher in the revenue mix as automated prioritization tools reduce analyst hours in rare-disease review. A September 2025 clinical evaluation on medRxiv reported that SeqOne’s DiagAI identified causal variants in 94.9% of cases when HPO terms were integrated, and that 74% of top-listed variants were diagnostic. Predictive genetic testing is an emerging commercial frontier for the AI in genomics market, especially where preventive whole-genome sequencing is moving closer to health-plan settings. Illumina’s March 2026 consortium with Veritas Genetics supports that shift toward wider preventive use.

By Application: Drug Discovery Leads, Precision Medicine Sets the Pace

Drug discovery and development held 34.41% of revenue in 2025, which made it the largest application in the AI in genomics market. That lead reflects sustained pharma spending on AI-assisted target identification, lead optimization, and biomarker development. Tempus AI stated in early 2026 that 19 of the top 20 pharmaceutical companies had active data or application partnerships with the company. The same investor materials reported more than USD 2 billion in signed data and applications contracts, which shows how important platform access has become to pipeline strategy. The AI in genomics market is therefore being shaped by long-cycle platform relationships, not only by one-off software licenses. In that setting, companies that control curated data and real clinical workflows are gaining stronger bargaining power with pharma customers.

Precision medicine is the fastest-growing application, with a projected CAGR of 43.69% from 2026 to 2031. The demand driver is wider than oncology alone, because multi-disease molecular profiling is becoming a more practical preventive and diagnostic tool. A 2025 review in Clinical and Experimental Medicine cited federated learning frameworks that improved immunotherapy-response prediction by 30% across 17 institutions without pooling underlying data. That result matters because it shows the AI in genomics market can scale even in fragmented health systems where direct data pooling is difficult. Clinical diagnostics, agriculture, animal research, and other applications fill the remaining demand base. As those areas expand, the AI in genomics market gains a broader customer mix and becomes less dependent on a single vertical. The AI in genomics industry also benefits from this spread because demand is coming from both high-value clinical use and adjacent biological research workflows.

By Deployment Model: Cloud Leads While Hybrid Architecture Reshapes Delivery

Cloud-based deployment held 46.18% of revenue in 2025, which kept it as the largest delivery model in the AI in genomics market. Cloud platforms fit research and pharma users well because they simplify collaboration, scale compute resources, and support multi-site access. DNAnexus stated in September 2025 that its platform managed more than 125 petabytes of clinical, genomic, proteomic, and multiomic data across more than 60,000 registered users in 48 countries. The same announcement showed DNAnexus extending into point-of-care delivery through integration with Oracle Health EHR systems. That kind of expansion reinforces the role of cloud delivery in large research networks and commercial life sciences accounts. It also supports the AI in genomics market where shared data access matters more than local residency controls.

Hybrid deployment is the fastest-growing model, with a projected CAGR of 44.11% through 2031. The AI in genomics market is moving in that direction because regulated customers often need patient data to stay on-premise while still using cloud-based inference or orchestration tools. The EU AI Act and related European health data governance frameworks are pushing customers toward this design logic. France’s health data strategy, published in 2025, adds to this by emphasizing governance, interoperability, and secondary-use controls that hybrid systems can support more easily than pure cloud environments. On-premise deployment still matters in government genomics programs and in settings with more limited cloud infrastructure. Even so, the AI in genomics market is likely to see hybrid architectures absorb more of those workloads over time because they balance compliance and scale more effectively.

By End User: Pharma and Biotech Drive Volume While Clinical Labs Set Growth Pace

Pharmaceutical and biotechnology companies held 38.22% of revenue in 2025, which made them the largest end-user group in the AI in genomics market. Their lead position reflects large data partnerships, drug discovery platform subscriptions, and demand for AI-enabled trial design and biomarker workflows. Illumina’s Alliance for Genomic Discovery included AbbVie, Alnylam, Amgen, AstraZeneca, Bayer, Bristol Myers Squibb, GSK, Merck, and Novo Nordisk among its members in March 2026. That consortium shows how multi-omic data access is now treated as a core research input rather than a discretionary expense. Academic and research institutes remain important users because they generate training data and early workflow validation for the AI in genomics market. Their revenue contribution is still limited by grant cycles and procurement constraints. Even so, they continue to shape the long-term direction of model development and data diversity.

Clinical laboratories and diagnostic centers are the fastest-growing end-user group, with a projected CAGR of 42.41% from 2026 to 2031. This reflects rising demand for fast turnaround, automated prioritization, and integrated reporting in routine testing. GeneDx stated in January 2026 that its ultraRapid Genome Sequencing service could deliver actionable insights for NICU and PICU patients in as little as 48 hours. announced in February 2026 that 2 new U.S. integrated health system agreements were expected to add 60,000 analyses annually. Healthcare providers, including hospitals and health systems, are also becoming a stronger channel as reimbursement support for comprehensive profiling expands. Tempus reported in March 2026 that its advanced genomic profiling features identified actionable findings in 12% of patients that standard testing had missed. Those patterns show the AI in genomics market moving from research-led demand toward routine-testing demand. They also show why laboratory operations are becoming one of the most important adoption settings across the AI in genomics market.

Geography Analysis

North America held the largest regional position, with 38.52% share in 2025, and that reflects a mature base of sequencing capacity, commercial AI genomics platforms, and earlier reimbursement traction for advanced diagnostics. Tempus AI reported Q1 2026 revenue of USD 348.1 million, up 36.1% year over year, with hereditary testing volume growth of 54% and minimal residual disease test volume growth of more than 500%. Those operating figures show how the AI in genomics market is moving from specialist oncology settings toward broader clinical use in North America. The United States remains the regional center of commercial activity, while Canada signaled its intention in September 2025 to build sovereign genomic data and AI infrastructure through a national genomics strategy and precision health initiative.

Europe remains a major contributor to the AI in genomics market because it combines dense clinical genomics networks with a regulatory framework that increasingly shapes global product design. The EU AI Act is pushing vendors toward validated and auditable systems, and that favors platforms that can document model behavior and workflow controls in detail. The UK Cancer 2.0 program and wider clinical deployment activity across the region show that Europe is not only regulating AI genomics tools, but also expanding the use cases for them. reported in March 2026 that it ended 2025 with 528 core genomics customers across more than 90 countries, including new signings at the Royal Infirmary of Edinburgh, AZ Delta in Belgium, and Ruhr University Bochum in Germany[3]SOPHiA GENETICS, “SOPHiA GENETICS Reports Fourth Quarter and Full Year 2025 Results,” PR Newswire, prnewswire.com. France’s 2025 strategy for artificial intelligence and health data also shows a clear policy push toward interoperable genomic data systems at scale.

Asia-Pacific is the fastest-growing region in the AI in genomics market, with a projected CAGR of 42.81% through 2031. The regional outlook is supported by national genome programs, a broader build-out of AI-native diagnostic infrastructure, and a rising need for local data resources that improve cross-ancestry performance. The AI in genomics market in Asia-Pacific also benefits from the simple fact that new capacity is being added from a lower installed base, which supports faster expansion than in mature regions. Australia and South Korea continue to add weight through national genome initiatives and hospital-linked sequencing programs, while other markets in the region are building out clinical and translational capacity.

Middle East and Africa and South America remain smaller in current revenue terms, but both are moving further into the early commercial phase of adoption. stated in March 2026 that liquid biopsy adoption at King Abdullah International Medical Center in Saudi Arabia and platform use at Brazil’s Human Genome and Stem Cell Research Center show that deployment is broadening outside the main established regions.

Competitive Landscape

The AI in genomics market is moderately concentrated at the platform level and fragmented at the application level, with a small group of scaled data-and-AI platforms holding an advantage over a larger field of workflow-specific vendors. Tempus AI, SOPHiA GENETICS, and GeneDx stand out because proprietary datasets, clinical partnerships, and curated interpretation assets matter more as customers move toward production use. The AI in genomics market is also consolidating, as larger platforms are absorbing interpretation software and workflow assets that can strengthen their clinical positioning. QIAGEN’s acquisition of Genoox, GeneDx’s acquisition of Fabric Genomics, and SeqOne’s acquisition of Congenica all support that direction.

Smaller vendors are still finding room in the AI in genomics market through specialized foundation models, focused workflows, and compliance-ready product design. Google DeepMind’s AlphaGenome outperformed established models on 22 of 24 genomic benchmarks and predicts 5,930 tracks across 11 molecular modalities, which gives research users a strong example of how quickly model capability is advancing. The company’s non-commercial research API also helps seed adoption in academic and government labs before broader commercialization. In parallel, the AI in genomics market is being shaped by vendors that build auditability and laboratory compliance into product architecture from the start. That matters because clinical customers increasingly need traceability, validation support, and documentation that can survive regulatory review.

This competitive mix means the AI in genomics market is not controlled by a single dominant vendor, even though scaled platforms have clear operating advantages. The strongest strategic moves in the last year came from companies that expanded data depth or workflow reach rather than from companies that only launched isolated algorithms. Roche’s planned acquisition of PathAI in May 2026 is a clear example, because it brings digital pathology AI closer to Roche’s genomic diagnostics portfolio and supports a more integrated precision medicine workflow. Eli Lilly’s collaboration with Profluent is another example, because it places significant capital behind AI-designed recombinases at the platform layer rather than only backing a single product candidate. QIAGEN’s Genoox transaction added a scaled cloud interpretation engine to an established clinical genomics portfolio, which further shows where value is concentrating. The main open spaces remain in rare-variant discovery for non-European populations, federated multi-hospital training, and the integration of spatial multi-omic data with genomic interpretation. Those areas still look open because no single company has reached broad commercial scale across them yet, which leaves room for differentiated entrants in the AI in genomics market.

AI In Genomics Industry Leaders

NVIDIA

Google

Illumina, Inc.

BenevolentAI

SOPHiA GENETICS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Roche entered a definitive merger agreement to acquire PathAI for USD 750 million upfront and up to USD 300 million in additional milestone payments, combining digital pathology AI with Roche's genomic diagnostics portfolio to accelerate precision medicine companion diagnostic development.

- April 2026: Eli Lilly and Profluent Bio announced a strategic research collaboration worth up to USD 2.25 billion for AI-designed custom site-specific recombinases for genetic medicine, enabling kilobase-scale DNA editing across multiple genetic disease indications.

Global AI In Genomics Market Report Scope

As per the scope of the report, AI in Genomics refers to the application of artificial intelligence techniques and algorithms to analyze, interpret, and understand genomic data. It involves using machine learning, deep learning, and other AI methods to identify patterns, predict genetic traits or disease risks, discover new genes, and advance personalized medicine.

The segmentation for the AI in genomics market is categorized by component, technology, functionality, application, deployment model, end user, and geography. By component, the market is divided into software, services, and hardware. By technology, it includes machine learning, deep learning, natural language processing, computer vision, and other AI technologies. By functionality, the segmentation covers genome sequencing, gene editing, clinical workflow, predictive genetic testing, and other functionalities. By application, it encompasses drug discovery and development, precision medicine, clinical diagnostics, agriculture and animal research, and other applications. By deployment model, the market is segmented into cloud-based, on-premise, and hybrid. By end user, it includes pharmaceutical and biotechnology companies, healthcare providers, clinical laboratories and diagnostic centers, academic and research institutes, and other end users.

By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Software |

| Services |

| Hardware |

| Machine Learning |

| Deep Learning |

| Natural Language Processing |

| Computer Vision |

| Other AI Technologies |

| Genome Sequencing |

| Gene Editing |

| Clinical Workflow |

| Predictive Genetic Testing |

| Other Functionalities |

| Drug Discovery & Development |

| Precision Medicine |

| Clinical Diagnostics |

| Agriculture & Animal Research |

| Other Applications |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Pharmaceutical & Biotechnology Companies |

| Healthcare Providers |

| Clinical Laboratories & Diagnostic Centers |

| Academic & Research Institutes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| Hardware | ||

| By Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Other AI Technologies | ||

| By Functionality | Genome Sequencing | |

| Gene Editing | ||

| Clinical Workflow | ||

| Predictive Genetic Testing | ||

| Other Functionalities | ||

| By Application | Drug Discovery & Development | |

| Precision Medicine | ||

| Clinical Diagnostics | ||

| Agriculture & Animal Research | ||

| Other Applications | ||

| By Deployment Model | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Healthcare Providers | ||

| Clinical Laboratories & Diagnostic Centers | ||

| Academic & Research Institutes | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in AI in genomics through 2031?

Growth is being driven by manual interpretation bottlenecks, rising genomic data volumes, wider precision medicine use, and larger pharma platform partnerships. The market is projected to reach USD 9.93 billion by 2031 at a 41.25% CAGR.

Which segment leads revenue today?

Software led component revenue with 42.1% share in 2025, showing that interpretation platforms and decision-support tools now capture more value than instruments alone.

Which technology is growing the fastest in this space?

Natural language processing is the fastest-growing technology, with a projected 43.18% CAGR through 2031, because it helps turn clinical notes, literature, and variant databases into structured insights.

Why are clinical laboratories becoming more important buyers?

Clinical laboratories and diagnostic centers are projected to grow at a 42.41% CAGR through 2031 as turnaround time, workflow automation, and routine testing demand increase.

Which region is expanding the fastest?

Asia-Pacific is forecast to grow at a 42.81% CAGR through 2031, supported by national genome programs and continued build-out of AI-enabled diagnostic infrastructure.

What is the biggest restraint on commercial scaling?

Regulatory compliance is the biggest near-term constraint, especially in Europe, where high-risk AI requirements under the EU AI Act raise documentation, oversight, and deployment costs.

Page last updated on: