AI In Vaccinology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.32 Billion |

| Market Size (2031) | USD 32.67 Billion |

| Growth Rate (2026 - 2031) | 28.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Vaccinology Market Analysis by Mordor Intelligence

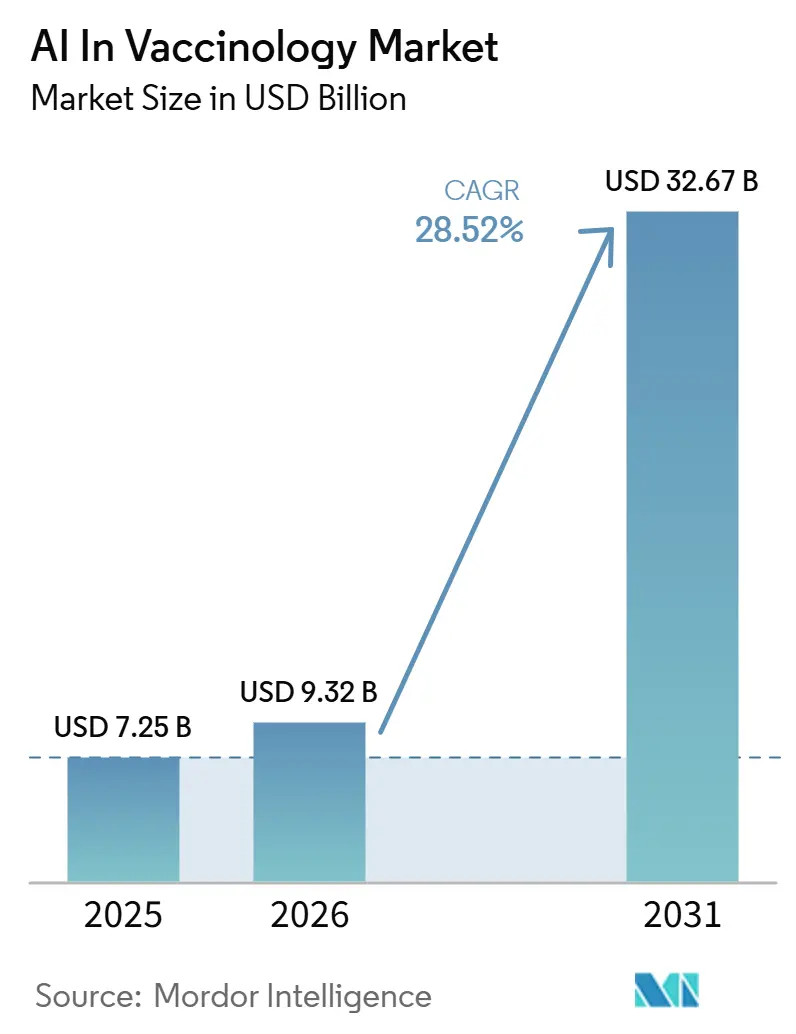

The AI In Vaccinology Market size is expected to grow from USD 7.25 billion in 2025 to USD 9.32 billion in 2026 and is forecast to reach USD 32.67 billion by 2031 at 28.52% CAGR over 2026-2031.

The AI in vaccinology market is moving into a more commercial phase because inverse vaccinology and generative models now let developers predict immune targets and design candidate antigens earlier in the research cycle than older discovery methods allowed. The AI in vaccinology market is also gaining credibility from real clinical progress, as the first human trial of an AI-designed pan-Sarbecovirus vaccine showed a practical link between computational design and early-stage safety validation. The AI in vaccinology market remains competitive because large vaccine developers, cloud platforms, and specialist AI firms are all trying to build stronger data assets, faster discovery tools, and more regulator-ready workflows. The AI in vaccinology market still faces a near-term commercialization limit because computational systems are producing more candidates than wet-lab and clinical pipelines can validate at the same pace. The AI in vaccinology market is also becoming more regionally uneven as explainability standards, data governance requirements, and health data controls shape where platforms can be deployed most efficiently.

Key Report Takeaways

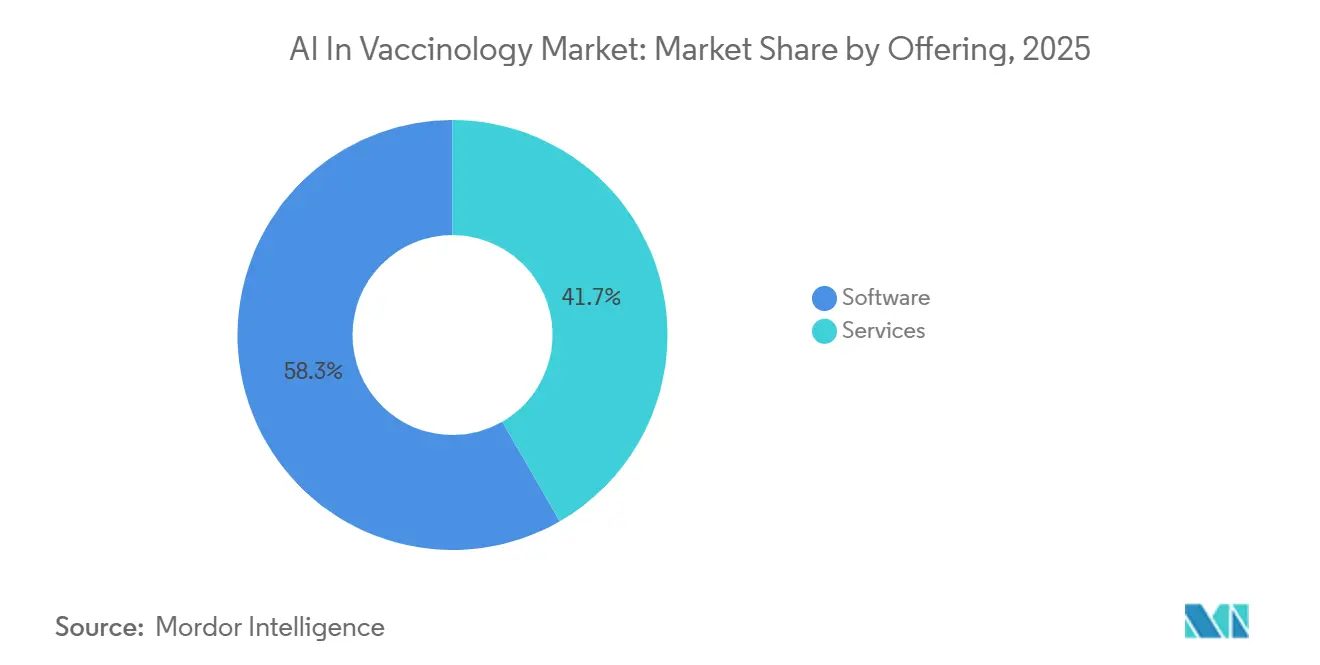

- By offering, software held 58.31% of revenue in 2025, while services are projected to expand at a 31.38% CAGR through 2031.

- By application, antigen discovery and design accounted for 32.24% of the AI in vaccinology market share in 2025, while clinical trial design and optimization is expected to record the highest CAGR at 32.52% through 2031.

- By end user, pharmaceutical and biotechnology companies captured 45.26% of revenue in 2025, while government and public health agencies are forecast to grow at a 30.55% CAGR through 2031.

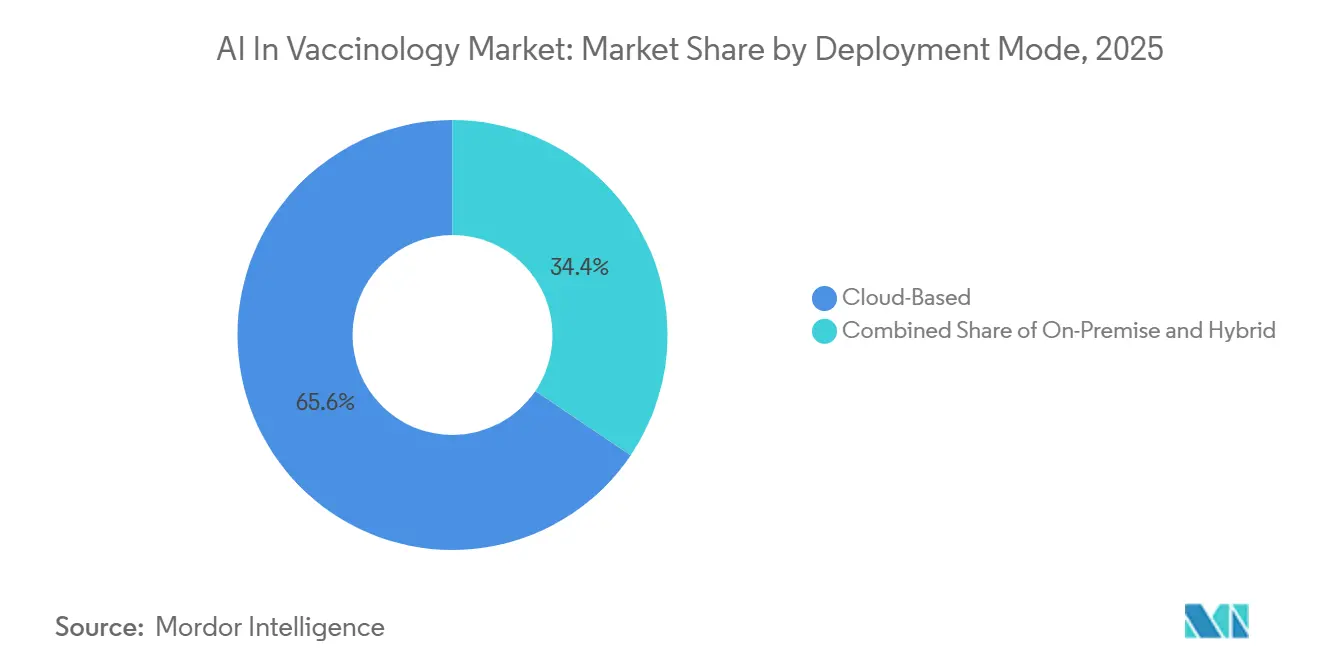

- By deployment mode, cloud-based solutions represented 65.56% of revenue in 2025, while hybrid deployment is expected to advance at a 32.65% CAGR through 2031.

- By stage of vaccinology workflow, discovery led with 35.52% of revenue in 2025, while clinical development is projected to grow at a 33.25% CAGR through 2031.

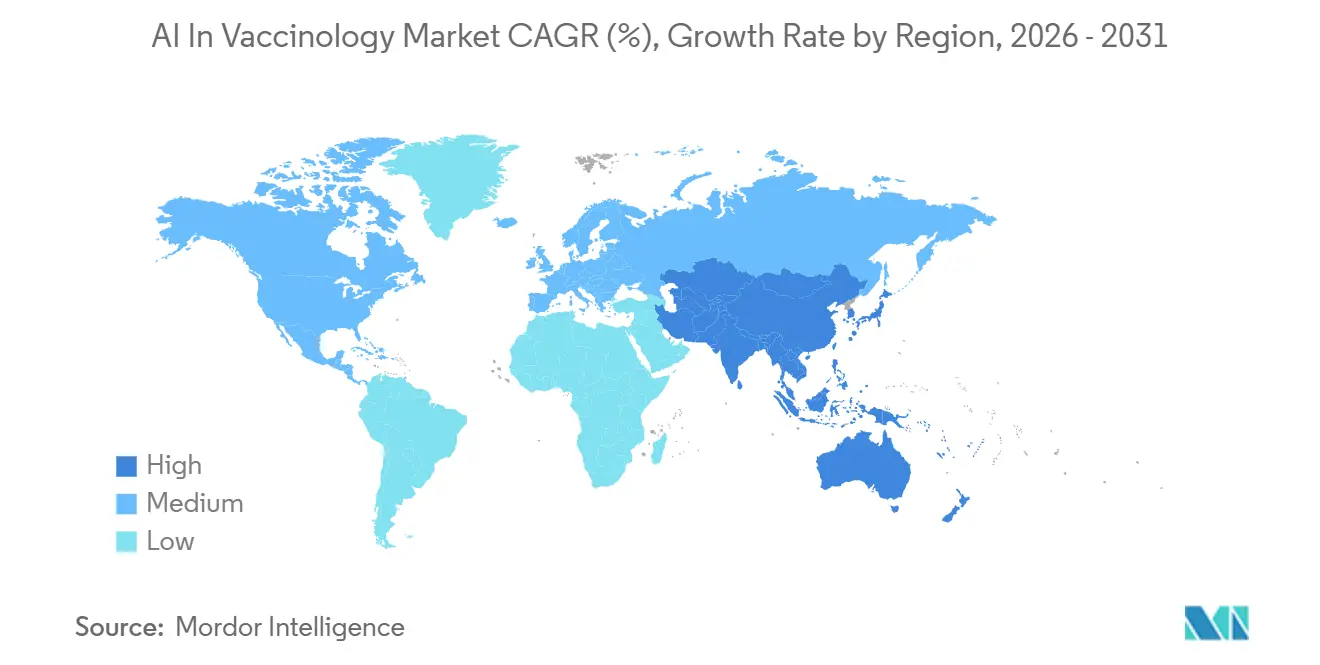

- By geography, North America held 38.62% of the AI in vaccinology market size in 2025, while Asia-Pacific is forecast to expand at a 31.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Vaccinology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Enabled Antigen Discovery Shortens Vaccine Design Cycles | +7.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Multi-Omics Data Integration Improves Candidate Selection Accuracy | +4.8% | North America & Europe core, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| AI-Optimized Clinical Trial Design Reduces Failure Risk | +4.1% | Global, led by US, EU, Japan | Medium term (2-4 years) |

| Government and CEPI-Led Pandemic Preparedness Funding | +3.6% | Global, targeted spend in Asia-Pacific, MEA, South America | Short term (≤ 2 years) |

| Explainable AI Becomes Essential for Regulatory Acceptance | +2.5% | North America & EU primarily | Medium term (2-4 years) |

| Model Training Demand Rises With Rare-Pathogen and Variant Surveillance | +2.0% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Enabled Antigen Discovery Shortens Vaccine Design Cycles

The AI in vaccinology market is getting immediate support from shorter antigen identification cycles, because developers can now screen and refine targets in weeks instead of waiting through long iterative lab programs. Google DeepMind’s AlphaFold work has strengthened this shift by helping researchers anticipate protein structure behavior and stability before wet-lab testing begins, which makes early design choices more informed and less repetitive[1]Google DeepMind, “AlphaFold,” DeepMind, deepmind.google. This time reduction matters because better structural prediction can remove weak candidates earlier and improve the quality of molecules that move into physical validation. The first Phase I human trial of pEVAC-PS in June 2026 showed that an AI-designed pan-Sarbecovirus antigen could reach human testing, which gave the AI in vaccinology market a visible proof point that computational design can advance into real development programs. A 2025 Nature Medicine study also showed that AI-based influenza strain selection can predict dominant circulating strains more accurately than conventional methods, which connects discovery tools directly with annual reformulation decisions in vaccine programs.

Multi-Omics Data Integration Improves Candidate Selection Accuracy

The AI in vaccinology market is also expanding because multi-omics integration gives developers a wider biological view than single-layer screening can provide. When transcriptomics, proteomics, metabolomics, epigenomics, interactomics, phosphoproteomics, glycomics, and lipidomics are analyzed together, AI systems can capture interactions that are hard to isolate through traditional workflows. A 2026 review in Frontiers in Systems Biology showed that AI applied to multi-omics data can build predictive immune response frameworks that reveal complex relationships across molecular layers. This matters for the AI in vaccinology market because candidate prioritization improves when developers can identify not only likely antigens but also the immune and formulation conditions that may shape response quality. Research from GSK and Lawrence Livermore National Laboratory in 2025 showed that machine learning for cross-reactive antigen design could outperform older combinatorial screening methods in meningococcal vaccine development. A 2026 Nature Communications study then linked multiomic analysis with glutaminolysis-dependent metabolic pathways that can support immune memory enhancement, which broadens the role of AI from target screening into response optimization.

AI-Optimized Clinical Trial Design Reduces Failure Risk

The AI in vaccinology market is moving further into downstream development because trial design, patient stratification, and dose planning are becoming more data-intensive and more suitable for AI support. Vaccine trials remain the costliest and most failure-prone part of the development cycle, so any tool that improves protocol quality or reduces uncertainty has a direct commercial effect. Developers are using AI not only to accelerate research but also to redesign operating workflows around faster evidence review and better dose selection. A July 2026 study from Weill Cornell Medicine showed that a multi-agent AI system could simulate, design, and improve clinical trials using real-world patient data, with the potential to lower costs and improve success rates[2]Weill Cornell Medicine, “AI Research Team Could Streamline Clinical Trial Design,” Weill Cornell Medicine Newsroom, news.weill.cornell.edu. For the AI in vaccinology market, that shift means value is moving from discovery support alone toward clinical execution support, where the financial payoff of better decisions is often larger and easier to measure.

Government and CEPI-Led Pandemic Preparedness Funding

The AI in vaccinology market is also being lifted by public and multilateral funding, because pandemic preparedness goals are turning AI-enabled vaccine capability into a strategic health security priority. CEPI’s Pandemic Preparedness Engine is designed as an end-to-end platform that combines genomic surveillance, epidemiological modeling, viral phylogenetics, vaccine design tools, and clinical pipeline support in one secure system. That approach matters because it supports the goal of moving from pathogen identification to candidate proposal within hours rather than through much slower fragmented workflows. CEPI also plans a network of AI factories that would widen access to computing infrastructure for vaccine manufacturers in lower-income settings, which helps prevent capability concentration in a small set of advanced markets. In the AI in vaccinology market, this type of funding changes near-term demand patterns because procurement can begin before fully mature commercial revenue models are established.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented and Biased Immunology Datasets Limit Model Generalization | -3.1% | Global, acute in MEA and South America | Long term (≥ 4 years) |

| Weak Wet-Lab Validation Pipelines Slow Commercial Translation | -2.2% | Global | Medium term (2-4 years) |

| Regulatory Uncertainty Around AI-Generated Biological Evidence | -1.9% | North America & EU primarily | Medium term (2-4 years) |

| Data Sovereignty and Cross-Border Health Data Restrictions | -1.5% | Asia-Pacific, MEA, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented And Biased Immunology Datasets Limit Model Generalization

The AI in vaccinology market still faces a deep structural constraint because model quality depends on immunology data that remains uneven in coverage, quality, and regional representation. A 2026 Frontiers in Systems Biology review identified underrepresentation of Global South populations in multi-omics datasets as a critical limitation, which means predictions can reflect a narrow genetic and environmental base rather than the wider populations vaccine programs are meant to serve. The same challenge becomes harder when batch effects, inconsistent collection protocols, and multicollinearity reduce the ability to reproduce findings across cohorts. Small sample sizes and high-dimensional datasets can produce overfit models that look persuasive in silico but fail when moved into experimental screening. In the AI in vaccinology market, this problem is most damaging for rare-pathogen programs because sparse data can bias entire candidate generations and flatten performance gains that stronger algorithms should otherwise deliver.

Weak Wet-Lab Validation Pipelines Slow Commercial Translation

The AI in vaccinology market is also constrained by the mismatch between digital candidate generation and physical validation capacity. Platforms can now produce more potential targets than many organizations can test through in vitro, animal, and human-stage workflows, which creates a throughput bottleneck rather than a pure discovery bottleneck. A 2025 umbrella review in Frontiers in Immunology noted that regulatory frameworks for AI-driven vaccine development remain nascent and that specific pathways for evaluating AI-generated biological evidence are still limited. That lack of clear validation standards creates uncertain review timelines and makes capital planning harder, especially for smaller AI-native firms that do not have the same regulatory experience as large vaccine incumbents. In the AI in vaccinology market, the commercial value of strong models will therefore remain partly capped until validation pipelines, experimental throughput, and review expectations become more aligned.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Platforms Lead, Service Ecosystems Accelerate

Software held 58.31% of revenue in 2025, which shows that the AI in vaccinology market still centers on core platforms used for epitope mapping, structural prediction, candidate ranking, and workflow integration. This lead reflects how platform vendors have moved beyond older bioinformatics tools and are now supplying systems built around proprietary training datasets, reusable model layers, and vaccine-specific development workflows. In the AI in vaccinology market, software advantage strengthens over time because every additional pathogen record, immune response datapoint, and validation outcome can improve future predictions and deepen switching costs. The segment also benefits from rising demand for tools that connect design, screening, and documentation rather than solving only one technical task. That dynamic keeps software central to the operating model of the AI in vaccinology market even as other service-based business lines expand more quickly.

Services are projected to grow at a 31.38% CAGR through 2031, which makes them the fastest-scaling offering type in the AI in vaccinology market. Growth is being supported by biotech firms, research groups, and public health agencies that need model training, annotation support, and deployment management without building full internal AI teams. The service opportunity is not limited to compute outsourcing, because applied research support and custom model development carry higher value when customers want program-specific outputs rather than generic platform access. This is especially relevant in the AI in vaccinology industry where customers often work with distinct pathogen sets, regulatory conditions, and data structures that require tailored execution. Over time, the AI in vaccinology market should keep favoring service providers that combine technical AI expertise with domain understanding in immunology, vaccine development, and quality-controlled deployment.

By Application: Antigen Design Matures, Clinical AI Gains Speed

Antigen discovery and design accounted for 32.24% of 2025 revenue, which kept it as the largest application area in the AI in vaccinology market. Its lead reflects the maturity of reverse vaccinology pipelines and the wider use of protein language models and structural learning systems in early candidate generation. A 2025 Nature Communications study on integrating protein language and geometric deep learning models showed how AI can improve protective antigen prediction beyond conventional immunoinformatic approaches. In the AI in vaccinology market, this application remains the entry point for many customers because faster and better antigen prioritization has a clear effect on both cost and development timing. The segment also remains well funded because discovery-stage tools create downstream value for screening, preclinical work, and reformulation planning.

Clinical trial design and optimization is projected to expand at a 32.52% CAGR through 2031, which makes it the fastest-growing application in the AI in vaccinology market. The shift shows that AI value is moving from lab support into statistical design, patient segmentation, protocol refinement, and dose-related decision support. The middle sections of the pipeline, including candidate screening and safety, efficacy, and adverse event prediction, are also strengthening as more labeled outcomes become available from AI-informed programs. The AI in vaccinology market size for this application is rising because organizations now see that better trial design can reduce both failure risk and operational waste in a way that is easier to measure than some early discovery outputs. A July 2026 report from Weill Cornell Medicine reinforced this direction by showing that an AI research team system could simulate and improve clinical trials using real-world patient data.

By End User: Pharma And Biotech Lead, Public Buyers Expand

Pharmaceutical and biotechnology companies represented 45.26% of revenue in 2025, which placed them at the center of the AI in vaccinology market. These companies hold the largest internal R&D budgets, maintain the deepest proprietary datasets, and face the strongest commercial pressure to shorten vaccine development timelines. Their lead also reflects their ability to absorb new software platforms, integrate them into regulated workflows, and support the wet-lab follow-through required to convert digital predictions into product candidates. In the AI in vaccinology market, large developers also benefit from existing regulatory relationships and quality systems that help them adopt AI without rebuilding governance from the ground up. That gives major vaccine makers a practical advantage over smaller entrants even when the underlying models are not radically different.

Government and public health agencies are forecast to grow at a 30.55% CAGR through 2031, which makes them the fastest-expanding end-user group in the AI in vaccinology market. This shift is being driven by pandemic preparedness mandates, sovereign health security planning, and multilateral funding programs that support AI-native vaccine capabilities. Academic and research institutes also remain essential because they produce foundational datasets, publish model methods, and shape early technical standards that later move into commercial environments. Contract research organizations are strengthening their role by adding AI capability to traditional outsourced development services, which moves differentiation away from low-cost execution toward data and modeling quality. In the AI in vaccinology industry, end-user growth is therefore widening from commercial R&D buyers toward public institutions that want faster response capacity, stronger surveillance support, and more resilient development infrastructure.

By Deployment Mode: Cloud Leads, Hybrid Adoption Accelerates

Cloud-based deployment held 65.56% of revenue in 2025, which made it the dominant architecture in the AI in vaccinology market. Its lead comes from elastic compute access, pay-per-use economics, and the way large cloud ecosystems reduce implementation barriers for biopharma users that need scalable model training and storage. Cloud architecture also helps the AI in vaccinology market because it supports distributed collaboration and can improve access to anonymized multi-site data in structured environments. For many users, it remains the most practical way to run computationally intensive discovery workloads without making heavy upfront infrastructure investments. That keeps cloud at the center of the AI in vaccinology market even in settings where regulatory requirements are becoming stricter.

Hybrid deployment is projected to grow at a 32.65% CAGR through 2031, which signals that governance concerns are becoming more important in architecture decisions. Hybrid models allow organizations to retain sensitive data and some regulated processes in controlled environments while still using cloud resources for scalable analytics and model execution. The AI in vaccinology market size tied to hybrid systems is gaining support from regional compliance rules that make pure public cloud deployment less attractive for some vaccine developers. The European Commission’s AI framework and the EMA’s guidance both strengthen the case for architectures that can combine flexibility with traceability, control, and audit readiness. Over the forecast period, the AI in vaccinology market should keep moving toward hybrid structures in regulated environments where local governance requirements outweigh the simplicity of an all-cloud model.

By Stage of Vaccinology Workflow: Discovery Leads, Clinical Development Advances

Discovery captured 35.52% of revenue in 2025, which made it the largest workflow stage in the AI in vaccinology market. This concentration reflects the fact that early-stage design has been the easiest point for AI adoption, since reverse vaccinology, pangenome-guided immunoinformatics, and generative design all fit naturally into data-rich computational workflows. A July 2026 Scientific Reports study on a multi-epitope vaccine candidate against Acinetobacter baumannii showed how discovery-stage tools are already being applied to broader pathogen targets than in earlier periods. In the AI in vaccinology market, this keeps discovery at the front of spending because it is the stage where computational advantage is most visible and easiest to scale. Preclinical development follows from this momentum, although it remains more constrained by fragmented immunogenicity data and the translation gap between digital and biological signals.

Clinical development is projected to grow at a 33.25% CAGR through 2031, which makes it the fastest-advancing workflow stage in the AI in vaccinology market. Growth reflects wider use of AI for trial design, protocol adaptation, and evidence review once early-stage tools have proven useful in target selection and candidate prioritization. Manufacturing and scale-up remain smaller, but they carry high leverage because digital twin models can compress process development and improve production planning. MIT researchers reported in 2025 that end-to-end digital twin software for continuous mRNA manufacturing could reduce process development cycles from months to days, which shows why manufacturing AI can create disproportionate value even from a smaller base. Post-market safety surveillance is still the smallest stage, yet the AI in vaccinology market is likely to give it more attention as AI-designed vaccines require faster monitoring across growing real-world data streams.

Geography Analysis

North America held 38.62% of revenue in 2025, which kept it as the largest regional block in the AI in vaccinology market. The region benefits from a dense mix of vaccine developers, AI talent, advanced research institutions, and public funding channels tied to health security and biodefense priorities. The AI in vaccinology market in North America also gains from organizations that can combine computational design with established translational and regulatory capabilities. Canada adds depth through institutions such as VIDO at the University of Saskatchewan, which received up to CAD 24 million (USD 17.6 million) at 2025 average rates, from CEPI to support global disease prevention capabilities[3]CEPI, “New CEPI Funding to Spearhead Pandemic Preparedness Research,” CEPI, cepi.net. Mexico is still at an earlier stage, with stronger near-term relevance in logistics and immunization planning than in advanced AI-led vaccine design.

Europe remains structurally important in the AI in vaccinology market because regulatory expectations there are shaping how platforms are built, documented, and deployed. The EMA’s 2024 reflection paper requires a stronger focus on transparency and explainability across medicinal product workflows, which gives Europe a significant role in setting regulator-ready design standards. In February 2026, the European Commission committed EUR 225 million (USD 243 million) at 2026 average rates, to support next-generation influenza vaccine development through HERA under the EU4Health program. Germany and the United Kingdom remain the most active European markets because they combine AI research depth, vaccine development capability, and commercial platform presence. The AI in vaccinology market share of Europe is therefore supported less by scale alone and more by its role in setting compliance and platform design norms.

Asia-Pacific is projected to grow at a 31.15% CAGR through 2031, which makes it the fastest-growing region in the AI in vaccinology market. China and South Korea are driving much of this momentum, although they are doing so through different policy, manufacturing, and public-sector channels. In February 2026, the Chinese Academy of Sciences published details on an LLM-assisted knowledge graph system for TB vaccine antigen selection that was trained on more than 77,000 PubMed records, which highlights the region’s growing depth in applied AI for vaccinology. The region also benefits from stronger public-sector interest in domestic vaccine capability and local platform development. Middle East and Africa and South America remain earlier-stage opportunities where multilateral support and infrastructure capacity will matter more than platform availability through most of the forecast period.

Competitive Landscape

The AI in vaccinology market shows moderate concentration at the top, with major vaccine developers such as Moderna, BioNTech, Pfizer, GSK, Sanofi, and AstraZeneca holding the strongest positions through data ownership, capital scale, and regulatory experience. These companies are competing less on isolated algorithms and more on the depth of proprietary datasets, the quality of translational workflows, and the ability to link AI tools with validated development programs. The AI in vaccinology market also depends heavily on infrastructure providers such as NVIDIA, Microsoft, and IBM, because compute access, model environments, and cloud tooling shape how quickly platforms can be trained and deployed. In practical terms, this creates a layered competitive map where vaccine manufacturers, AI platform specialists, and infrastructure firms all influence adoption. The result is a market where no single business model controls the full value chain, even though the largest incumbents still have the clearest scale advantages.

A second tier of specialized AI companies is competing through focused architectures rather than broad end-to-end reach, and this keeps the AI in vaccinology market open to targeted disruption. These players are more likely to win through milestone-based partnerships, co-development work, or workflow-specific deployments than through stand-alone platform licensing at global scale. One important strategic move has been Google DeepMind’s continued expansion of AlphaFold as a core tool for protein structure work, which supports antigen design use cases and strengthens the computational foundation available to vaccine developers. Another visible move came from DIOSynVax and the University of Cambridge, whose AI-designed pEVAC-PS candidate reached Phase I testing in 2026 and gave the market a concrete clinical proof point for computational antigen design. These moves matter because they show that competitive position is increasingly linked to usable biological outputs rather than to AI branding alone.

The AI in vaccinology market still has meaningful white space in post-market safety surveillance, where no single AI-native vendor has yet built dominant credibility, scale, and data access. Competitive advantage is also likely to shift toward platforms that can combine generative design with explainability, because regulators are asking for both stronger performance and clearer reasoning. The EMA’s reflection paper has already raised the value of explainable model layers and better lifecycle governance, which means compliance readiness can become a commercial differentiator rather than only a legal requirement. Companies that invest early in interpretable architectures, secure data environments, and integrated validation support should be better placed for future procurement cycles in the AI in vaccinology market. That is why the next phase of competition is likely to favor firms that can connect discovery speed, regulatory discipline, and deployment reliability in one operating model.

AI In Vaccinology Industry Leaders

IBM

Microsoft

NVIDIA Corporation

Google DeepMind

Moderna, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: SK bioscience launched the Research Optimization and Trial Outcome Recommender (ROTOR) platform with funding from the Gates Foundation. Developed in collaboration with PATH and Slalom, the AI platform helps support clinical development decisions, reduce uncertainty around Phase III advancement, and expand access for vaccine developers in low- and middle-income countries.

- June 2026: China began construction of its first domestic AI and mRNA tumor vaccine production line. With a total investment of approximately CNY 110 million (approximately USD 15.3 million), the facility combines AI-driven personalized antigen targeting with mRNA vaccine manufacturing and represents the country’s first commercial-scale AI-integrated vaccine manufacturing facility.

Global AI In Vaccinology Market Report Scope

As per the scope of the report, AI in Vaccinology refers to the application of artificial intelligence technologies and methods to the study, development, and optimization of vaccines. This includes using AI for predicting antigenic targets, accelerating vaccine design, analyzing clinical trial data, improving manufacturing processes, and enhancing vaccine safety and efficacy assessments. AI-driven approaches help streamline research, reduce development time, and enable personalized vaccination strategies.

The AI in vaccinology market is segmented by offering into software and services; by application into antigen discovery and design, vaccine candidate screening, clinical trial design and optimization, safety, efficacy, and adverse event prediction, vaccine manufacturing optimization, and supply chain and demand forecasting; by end user into pharmaceutical and biotechnology companies, academic and research institutes, contract research organizations, and government and public health agencies; by deployment mode into cloud-based, on-premise, and hybrid; by stage of vaccinology workflow into discovery, preclinical development, clinical development, manufacturing and scale-up, and post-market safety surveillance; and by geography into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Software |

| Services |

| Antigen Discovery and Design |

| Vaccine Candidate Screening |

| Clinical Trial Design and Optimization |

| Safety, Efficacy, and Adverse Event Prediction |

| Vaccine Manufacturing Optimization |

| Supply Chain and Demand Forecasting |

| Pharmaceutical and Biotechnology Companies |

| Academic and Research Institutes |

| Contract Research Organizations |

| Government and Public Health Agencies |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Discovery |

| Preclinical Development |

| Clinical Development |

| Manufacturing and Scale-Up |

| Post-Market Safety Surveillance |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Software | |

| Services | ||

| By Application | Antigen Discovery and Design | |

| Vaccine Candidate Screening | ||

| Clinical Trial Design and Optimization | ||

| Safety, Efficacy, and Adverse Event Prediction | ||

| Vaccine Manufacturing Optimization | ||

| Supply Chain and Demand Forecasting | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| Academic and Research Institutes | ||

| Contract Research Organizations | ||

| Government and Public Health Agencies | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Stage of Vaccinology Workflow | Discovery | |

| Preclinical Development | ||

| Clinical Development | ||

| Manufacturing and Scale-Up | ||

| Post-Market Safety Surveillance | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in AI in vaccinology through 2031?

Growth is being driven by faster antigen discovery, wider multi-omics integration, stronger public preparedness funding, and rising use of AI in clinical trial design.

How large will AI in vaccinology become by 2031?

The AI in vaccinology market is forecast to reach USD 32.67 billion by 2031 from USD 9.32 billion in 2026, growing at a 28.52% CAGR over 2026-2031.

Which application area leads revenue today?

Antigen discovery and design led with 32.24% of revenue in 2025 because it is the most established use case for AI across vaccine target identification and optimization.

Which end users are expanding fastest?

Government and public health agencies are the fastest-growing end users, with a projected 30.55% CAGR through 2031, supported by pandemic preparedness spending and public health mandates.

Why is hybrid deployment gaining traction in vaccine AI platforms?

Hybrid deployment is projected to grow at a 32.65% CAGR through 2031 because developers need both scalable analytics and stronger control over regulated data, traceability, and local governance.

Which region offers the fastest growth opportunity?

Asia-Pacific is projected to grow at a 31.15% CAGR through 2031, supported by stronger domestic platform development, public-sector demand, and applied AI research activity.

Page last updated on: