AI In Antibody Discovery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.62 Billion |

| Market Size (2031) | USD 1.88 Billion |

| Growth Rate (2026 - 2031) | 24.61% CAGR |

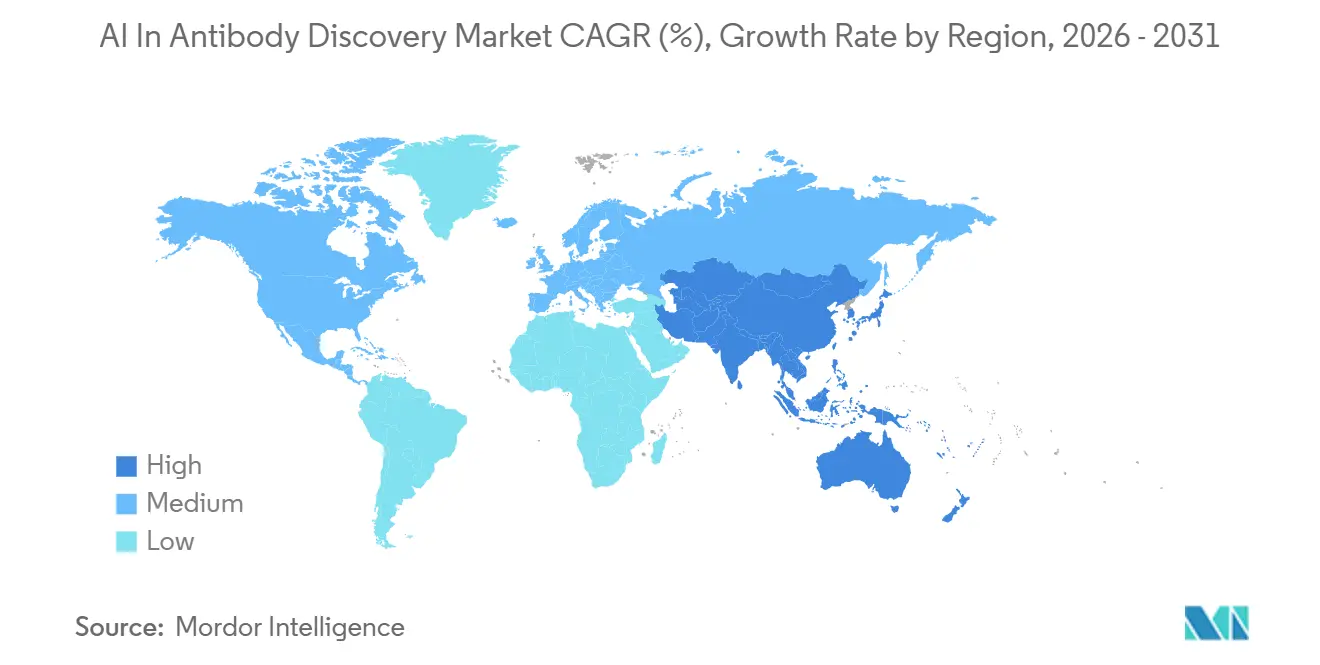

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

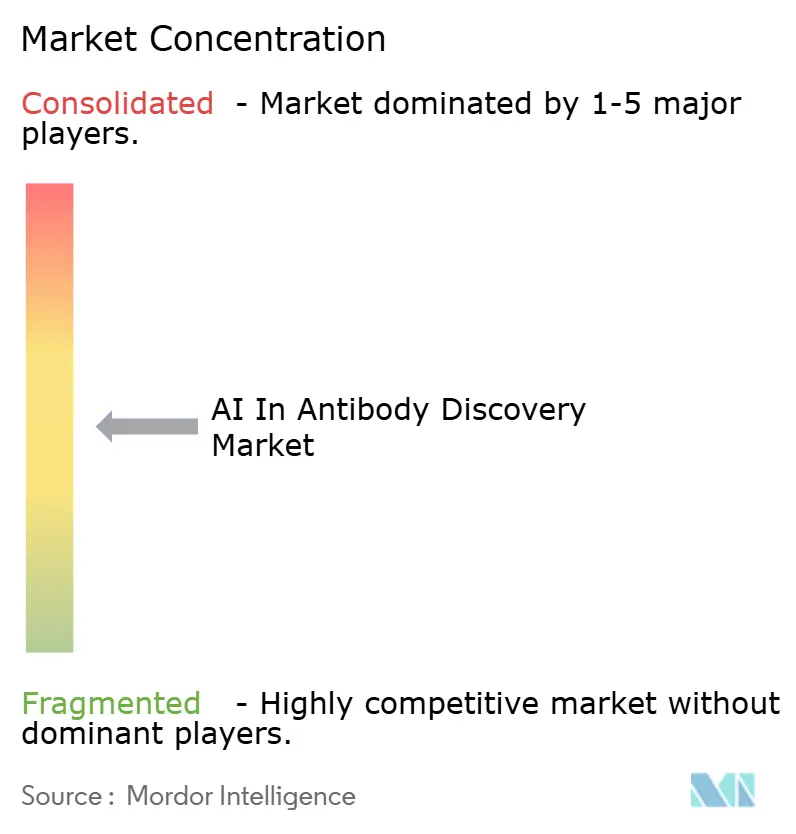

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Antibody Discovery Market Analysis by Mordor Intelligence

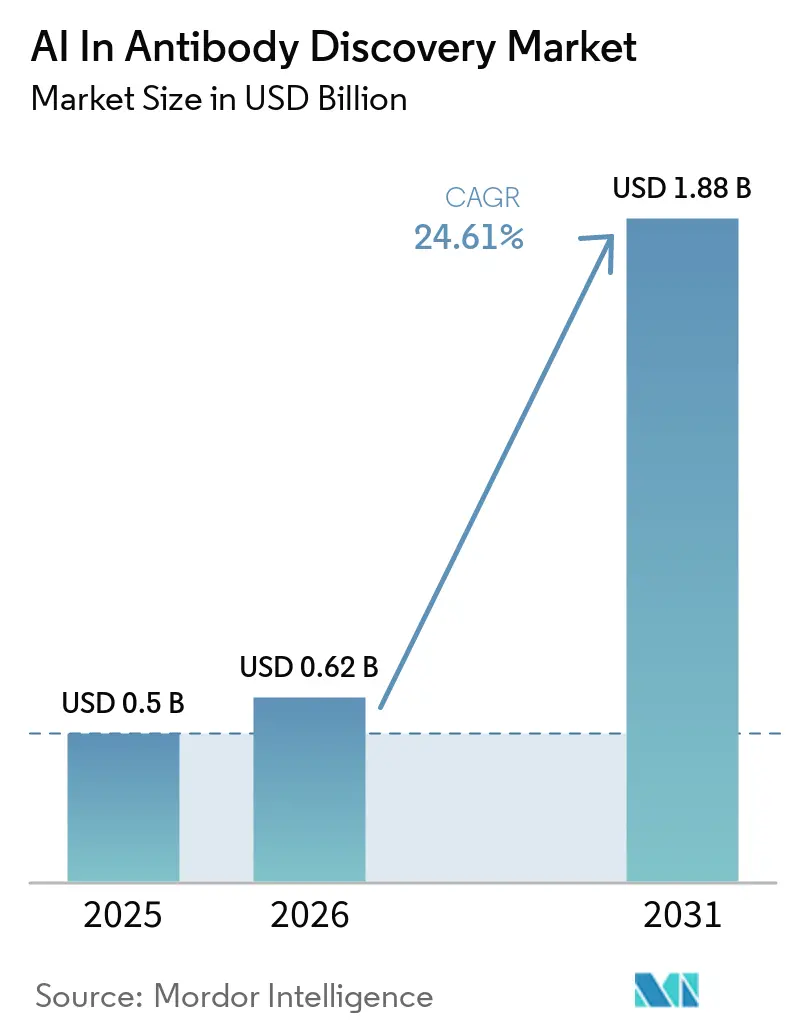

The AI In Antibody Discovery Market size is expected to grow from USD 0.5 billion in 2025 to USD 0.62 billion in 2026 and is forecast to reach USD 1.88 billion by 2031 at 24.61% CAGR over 2026-2031.

Traditional discovery economics have remained difficult for developers because per-program spending has historically exceeded USD 50 million over 4-6 years and preclinical attrition has stayed above 90%, which has pushed buyers to seek more measurable alternatives. Absci stated in its 2026 Form 10-K that AI-guided programs can complete similar scope in roughly 2 years at close to USD 15 million per program, which has sharpened the commercial case for platform adoption. The market is no longer moving as a simple digital upgrade to established screening workflows, because value is shifting toward AI-led biological hypothesis generation and toward the platforms that control those design loops. Competition is rising across a fragmented field of 15-20 AI-native companies, and differentiation is increasingly tied to benchmark performance, patent depth, and modality breadth rather than to software access alone. The main limiting factor remains structural, because the lack of harmonized validation frameworks under ISO/IEC for AI-generated biologics can slow downstream enablement, especially for programs that sit outside established regulatory markets.

Key Report Takeaways

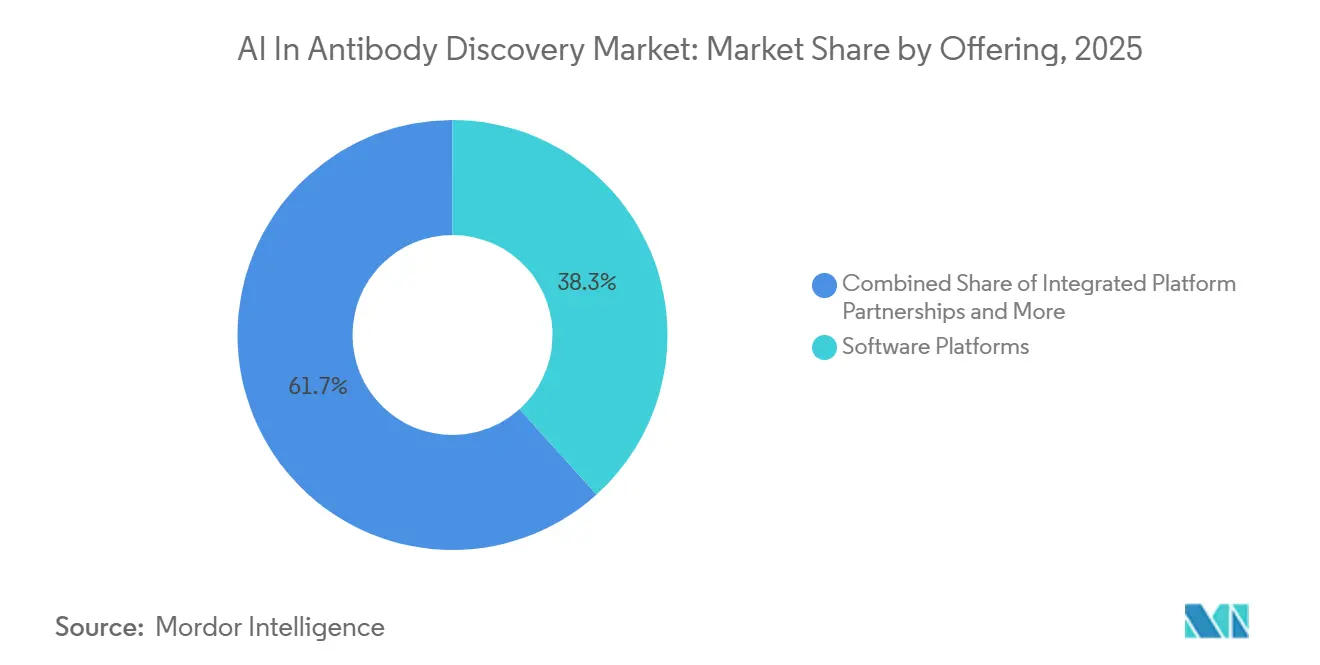

- By offering, Software Platforms held 38.31% of 2025 revenue, while Discovery Services is forecast to grow at a 26.38% CAGR through 2031.

- By technology, Structure Prediction accounted for 33.24% of 2025 revenue, while Generative AI and Protein Language Models is projected to expand at a 28.52% CAGR through 2031.

- By application, Target Identification and Validation held 28.52% of 2025 revenue, while De Novo Antibody Design is expected to advance at a 27.25% CAGR through 2031.

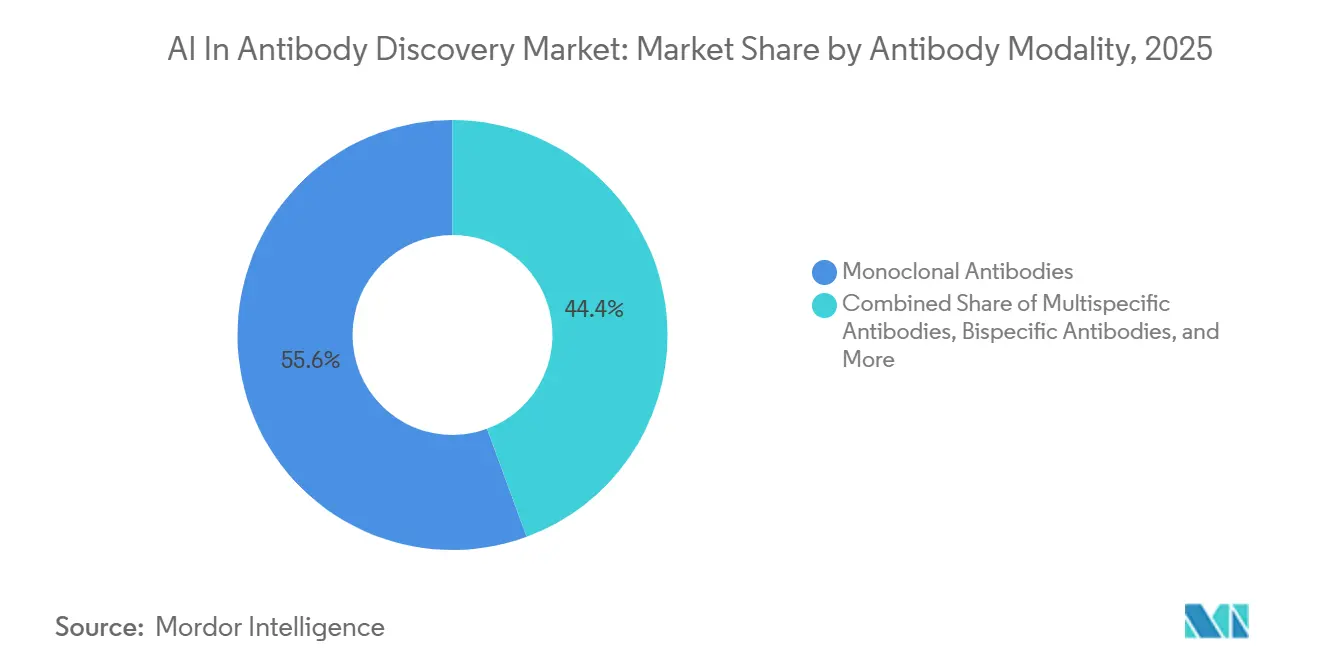

- By antibody modality, Monoclonal Antibodies commanded 55.62% of 2025 revenue, while Multispecific Antibodies is set to grow at a 27.55% CAGR through 2031.

- By therapeutic area, Oncology accounted for 38.84% of 2025 revenue, while Autoimmune and Inflammatory Diseases is forecast to expand at a 25.61% CAGR through 2031.

- By end user, Pharmaceutical Companies held 36.24% of 2025 revenue, while CROs and CDMOs is projected to grow at a 25.92% CAGR through 2031.

- By geography, North America held 43.44% of 2025 revenue, while Asia-Pacific is expected to grow at a 26.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Antibody Discovery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Conventional Discovery Cost and Attrition Pressure | +5.8% | Global | Medium term (2-4 years) |

| Rising Demand for Next-Generation Biologics | +4.5% | Global, led by North America, EU, and APAC | Long term (≥ 4 years) |

| Precision Medicine Demand in Oncology and Immunology | +3.5% | North America & EU, growing APAC | Long term (≥ 4 years) |

| Expanding Pharma-AI Collaboration Budgets | +2.8% | Global, concentrated in North America and EU | Short term (≤ 2 years) |

| AI Opening GPCR and Ion-Channel Antibody Programs | +3.2% | North America, APAC spill-over | Medium term (2-4 years) |

| Antibody-Specific Foundation Models Improving Hit Quality | +3.1% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Conventional Discovery Economics Force a Platform Pivot

The AI in antibody discovery market is gaining force because the cost burden of conventional antibody discovery has become difficult to justify in a tighter capital environment. Absci reported that AI-guided programs can lower per-program investment from more than USD 50 million to nearly USD 15 million and reduce development time from 4-6 years to roughly 2 years[1]Absci Corporation, “Annual Report (Form 10-K), Fiscal Year 2025,” Absci Investor Relations, investors.absci.com. Preclinical attrition has historically exceeded 90%, which means most early discovery spending has not translated into clinical return. The pressure is even stronger in early target classes such as GPCRs, ion channels, and multi-pass membrane proteins, where cryo-EM throughput still limits the structural information available for conventional studies. In the AI in antibody discovery market, that creates a practical first-mover window for platforms that can close difficult programs before traditional competitors fully characterize the antigen. It also explains why buyers are moving from narrow software use toward broader platform relationships that can carry more discovery risk and more program ownership.

Rising Demand for Next-Generation Biologics and Precision Medicine Expands AI's Design Surface

The market is also being lifted by a clear pipeline shift toward more complex biologics and toward precision medicine use cases in oncology and immunology. By early 2025, more than 12 bispecific antibodies had received regulatory approval worldwide, and more than 200 bispecifics were in active clinical trials across oncology and immunology. That pipeline mix expands the design problem beyond what traditional screening can manage efficiently, because multiple binding arms must be optimized at the same time for affinity, pharmacokinetics, and manufacturability. In the AI in antibody discovery market, precision medicine demand is reinforcing that shift because newer programs are targeting more selective cytokine receptors, co-stimulatory pathways, and immunology adjacencies that older methods handled poorly. Platforms that lack native multispecific design capability are therefore at risk of being excluded from the fastest-growing parts of future deal flow.

AI Opens GPCR and Ion-Channel Antibody Programs

The AI in antibody discovery market is widening because AI tools are starting to make GPCR and ion-channel antibody programs more workable. These target classes account for more than 35% of approved small-molecule drug targets, yet they have remained difficult for antibody therapeutics because membrane protein conformations are unstable and hard to prepare for immunization or structural analysis. Chai Discovery said its Chai-2 model produced the first fully AI-generated GPCR agonist antibody targeting CCR8 in January 2026 and reported an EC50 of 292 nM. AbCellera also reported that ABCL635, derived from its AI-supported discovery platform, reached Phase 2 in 2025 and was described as the first GPCR-derived antibody from an AI platform to reach that point[2]Business Wire, “AbCellera Reports Full-Year 2025 Financial Results and Business Updates,” Business Wire, businesswire.com. In the AI in antibody discovery market, those programs signal a category expansion rather than a line extension, because they open discovery revenue pools that were previously limited by antigen instability and poor structural coverage. The effect is especially relevant for CROs and CDMOs, since the ability to manage conformationally dynamic antigens can become a durable moat instead of a simple service feature.

Antibody-Specific Foundation Models Improve Hit Quality and Pull More Collaboration Spend

The market is moving faster as antibody-specific foundation models begin to change hit rates and wet-lab economics in measurable ways. Chai-2 reported a 20% experimental hit rate in May 2026, versus a traditional baseline near 0.1%, while Absci's Origin-1 delivered binders for 4 out of 10 difficult targets with fewer than 100 designs per target and DockQ scores of 0.73-0.83. When hit rates rise this sharply, validation cycles fall, and the cost per useful candidate drops enough to expand the buyer base beyond large pharma. That shift matters because collaboration budgets tend to follow reproducible performance rather than software promises, especially when benchmark data begins to appear in peer-reviewed or conference settings. In the AI in antibody discovery market, it also points to a split between firms that provide foundation-level infrastructure and firms that focus on therapeutic workflow integration. As more programs show external benchmark quality, spending is likely to keep moving toward platforms that can prove both model strength and downstream lab execution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Labeled Antibody Data | -3.4% | Global | Long term (≥ 4 years) |

| High Compute and Interdisciplinary Talent Cost | -1.8% | Global, most acute in emerging APAC markets | Medium term (2-4 years) |

| Wet-Lab Triage Bottleneck for AI-Generated Libraries | -2.8% | Global | Medium term (2-4 years) |

| Patentability and Enablement Pressure on AI-Generated Antibodies | -1.5% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Scarcity Structurally Limits Model Generalization

The market still faces a basic data problem, because public structural coverage remains too thin for broad generalization across target classes. Frontiers in Immunology noted that the Protein Data Bank contained fewer than 10,000 publicly available antibody structures and close to 2,000 VHH complexes across nearly 800 unique antigens as of May 2025. That scarcity is uneven, because common oncology targets have richer annotations while GPCR, ion-channel, and rare-disease antigens remain underrepresented. A November 2025 benchmark from the University of Tokyo showed that AlphaFold3 achieved only an 11% success rate at DockQ ≥ 0.80 for antibody-antigen complexes, which underlines how difficult heterodimer geometry still is for public models. In the AI in antibody discovery market, this makes proprietary dataset generation through wet-lab campaigns more valuable than simple model scaling. It also raises the cost of compute, increases the premium for cross-disciplinary talent, and makes patent enablement harder when physical validation trails digital design.

Wet-Lab Triage Bottleneck Constrains Throughput Gains

The AI in antibody discovery market is also limited by a widening gap between digital design speed and physical validation capacity. Standard mammalian expression systems validate only 200-400 candidates per month, while newer generative systems can output thousands of viable designs each week. Sino Biological said its XPressMAX platform validated more than 2,000 scFv and VHH candidates within 3-4 weeks per batch in May 2026, which is one of the highest public throughput figures disclosed so far. Even with that output, a single high-performing model can still overwhelm downstream screening queues and force serial batching. In the AI in antibody discovery market, that bottleneck matters beyond simple logistics because wet-lab reduction to practice also anchors patent filing and freedom-to-operate timing in the United States and Europe. Until expression, purification, and binding workflows scale more evenly with model output, commercial timelines will continue to depend on laboratory throughput as much as on algorithm performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Platforms Anchor Revenue as Services Gain Share

Software Platforms accounted for 38.31% of the AI in antibody discovery market share in 2025, while Discovery Services is projected to expand at a 26.38% CAGR through 2031. That mix shows how the market first commercialized through tools and interfaces, then began moving toward contracts that tie payment more closely to program delivery. Discovery Services is benefiting from buyers who prefer to shift discovery risk onto platform partners rather than build large internal stacks. The AI in antibody discovery market is therefore moving away from simple tool access and toward fuller outsourcing models that include target work, sequence generation, and validation support. Bayer said Cradle was being deployed across 6 of the top 25 global pharma companies and more than 50 active R&D programs as of January 2026, which supports the view that deeper service relationships are becoming more durable than license-only arrangements.

Integrated Platform Partnerships and Data and Model Licensing remain smaller today, but both carry strategic weight because they change how value is captured. The first model spreads upside through milestone-linked co-development structures, which can align platform incentives more closely with partner outcomes. The second model monetizes curated datasets and model weights as standalone intellectual property, which gives the AI in antibody discovery market a revenue layer that traditional CRO models did not offer. As foundation model leadership becomes harder to displace, data and model licensing may emerge as the highest-margin part of the commercial stack.

By Technology: Structure Prediction Leads but Generative AI Resets the Performance Ceiling

Structure Prediction held 33.24% of the AI in antibody discovery market size in 2025, while Generative AI and Protein Language Models is set to grow at a 28.52% CAGR through 2031. That revenue split reflects the fact that structure prediction remains the base layer for nearly every downstream design and optimization task. It is still the most established technical entry point, especially for teams that are adding AI into existing discovery workflows rather than rebuilding those workflows from the start. The AI in antibody discovery market is now shifting beyond prediction, though, because the main question is no longer just what structure exists but what sequence should be created. Chai-2's disclosed 20% hit rate versus a conventional baseline near 0.1% shows why generative approaches are resetting performance expectations.

Machine Learning and Deep Learning still hold meaningful commercial value in lead optimization, developability scoring, and ranking tasks where buyers want measured gains without changing the full process. Natural Language Processing and Knowledge Graphs are also building a narrower but useful role in target relationship mapping and literature synthesis. Closed-loop AI with Lab Automation remains the most disruptive long-run technology layer because it couples design and assay cycles into one system rather than treating them as separate steps. In the AI in antibody discovery market, that changes the cost structure by shifting the bottleneck from human analysis toward reagent flow, robotic throughput, and lab orchestration.

By Application: Target Identification Anchors Revenue While De Novo Design Accelerates

Target Identification and Validation accounted for 28.52% of the AI in antibody discovery market size in 2025, while De Novo Antibody Design is forecast to grow at a 27.25% CAGR through 2031. That balance shows that the highest current revenue still sits in the earlier and lower-risk end of discovery, where AI helps sort and prioritize target space at scale. De novo design, however, is growing faster because the commercial value of generating new binders from scratch is materially higher than the value of screening known templates more efficiently. The AI in antibody discovery market is therefore shifting from AI-assisted optimization toward AI-first origination, which changes how ownership, patent strategy, and partner contracts are framed. Absci's Origin-1 results, which showed binders for 4 out of 10 difficult targets in fewer than 100 design iterations per target, support that movement toward direct sequence generation.

Epitope Mapping and Binder Screening, together with Lead Optimization and Engineering, still form the most installed parts of the workflow because these steps benefit from larger existing labeled datasets. Developability and Manufacturability Prediction is gaining importance as teams try to identify aggregation risk and glycosylation issues before they become late-stage CMC problems. The AI in antibody discovery market is likely to keep seeing strong demand in these support applications because they reduce reformulation pressure and improve candidate quality earlier in the path. Even so, the highest strategic value is moving toward platforms that can originate novel molecules instead of only improving molecules that already exist.

By Antibody Modality: mAb Dominance Intact but Multispecifics Reshape Pipeline Mix

Monoclonal Antibodies commanded 55.62% of modality revenue in 2025, while Multispecific Antibodies is expected to grow at a 27.55% CAGR through 2031. The dominance of monoclonals still reflects their established manufacturing base, familiar clinical path, and the deeper structural data available for model training. That installed base keeps monoclonals central to the AI in antibody discovery market even as pipeline priorities start to change. Multispecifics are growing faster because they allow simultaneous engagement across multiple epitopes, which is proving more relevant in hard oncology and autoimmune settings. The design challenge is also well suited to AI, since co-optimizing affinity, selectivity, and stability across several binding arms is too complex for many empirical workflows.

The same pattern is extending into nanobodies and related single-domain formats. Latent Labs reported that its Latent-Y model generated single-digit nanomolar VHH binders with a 67% success rate and a 56-fold computational speed improvement over predecessor methods in March 2026. Bispecific Antibodies and Antibody-Drug Conjugates are also building momentum in large pharma pipelines, and that will keep pulling design demand toward platforms that support harder modalities. In the AI in antibody discovery market, modality breadth is becoming a stronger competitive filter because buyers increasingly want partners that can work across the full therapeutic design surface rather than across only standard monoclonal programs.

By Therapeutic Area: Oncology Drives Volume as Autoimmune Adjacencies Expand

Oncology held 38.84% of 2025 revenue, while Autoimmune and Inflammatory Diseases is projected to grow at a 25.61% CAGR through 2031. Oncology continues to anchor the AI in antibody discovery market because it has the largest active pipeline, the broadest biomarker base, and a steady need for checkpoint and tumor-antigen programs. That commercial depth keeps oncology at the center of current volume even when newer therapeutic opportunities are opening elsewhere. Autoimmune and inflammatory programs are growing faster because precision immunology is revealing new cytokine receptors and co-stimulatory pathways that older screening systems handled poorly. The AI in antibody discovery market is benefiting here from better discrimination across closely related immune cell surface targets, which helps platform teams address selectivity problems more efficiently.

Infectious diseases still matter strategically because they provide a strong use case for rapid antigen response and pandemic preparedness. A 2025 study cited for the MAGE framework showed hit rates of 28-45% against SARS-CoV-2, RSV, and H5N1 antigens, which supports the case for fast-cycle AI-led antibody generation. Neurology, Metabolic Diseases, and Rare Diseases remain smaller today, yet their long-term relevance is rising as foundation models widen coverage across harder and less common targets. In the AI in antibody discovery market, those areas offer room for above-average growth because they sit where biological complexity is high and historical training data has been thin.

By End User: Pharma Anchors Spend as CROs Build AI Infrastructure

Pharmaceutical Companies accounted for 36.24% of the AI in antibody discovery market size in 2025, while CROs and CDMOs are expected to grow at a 25.92% CAGR through 2031. Large drug developers remain the main spend center because they are still the biggest buyers of AI-generated leads and the core counterparties in milestone-based collaboration models. Their position gives the AI in antibody discovery market a relatively clear near-term demand base even while platform business models keep evolving. The faster growth of CROs and CDMOs shows that outsourcing is widening beyond routine lab work and into the design layer itself. That shift also reflects the preference among large pharma groups to keep discovery more asset-light rather than build every internal model, dataset, and validation stack on their own.

Biotechnology and platform companies remain the most innovation-dense part of the customer pool, even though their aggregate revenue is smaller because many are still early in commercialization. Academic and research institutes also retain an important role because they continue to supply new model ideas, training data, and spinout activity. The AI in antibody discovery market is likely to see more contract demand move toward service providers that can offer fixed-fee discovery packages with clearer timelines and stronger benchmarking. That makes infrastructure depth, wet-lab integration, and data ownership increasingly important selling points across the end-user base.

Geography Analysis

North America held 43.44% of the AI in antibody discovery market share in 2025, which kept it in the lead across regional demand. The region benefits from a dense group of AI-native biotechs, experienced capital allocators, and public science funding that supports protein engineering and machine learning work. That combination gives the AI in antibody discovery market a strong commercial center in North America because buyers, funders, and technical partners are already concentrated in the same ecosystem. It also supports multi-round partnership behavior, where pharma companies commit to longer co-development structures instead of testing AI through small pilot contracts only. North America therefore remains the main proving ground for benchmark differentiation, patent strategy, and milestone-based revenue models.

Asia-Pacific is projected to grow at a 26.22% CAGR through 2031, making it the fastest-growing regional cluster. China and Japan are driving that rise through different models, with China leaning on policy-backed AI biopharmaceutics investment and larger domestic compute build-out, while Japan is leaning more on corporate-academic collaboration. The AI in antibody discovery market is expanding in Asia-Pacific because local players are building stronger antibody datasets, stronger compute access, and more region-specific development infrastructure. Data sovereignty is also becoming a practical advantage, since regulated pharmaceutical collaborations are more likely to move forward when proprietary sequence data can remain under controlled domestic environments. The region's research ecosystems are now moving beyond follower status, and their benchmark progress suggests that competition with U.S. platforms will become more direct over the forecast period.

Europe remains a meaningful mid-tier region, supported mainly by Germany and the United Kingdom, where large pharma groups are putting AI discovery into core R&D instead of isolating it as an experimental add-on. Bayer's multi-year partnership with Cradle in January 2026 showed that established pharma companies in Europe are committing operating budgets to AI-assisted protein and antibody engineering rather than limiting spend to small exploratory pilots. The AI in antibody discovery market also benefits in Europe from early work in cell-free systems and closed-loop wet-lab integration, which fits the region's strength in process discipline and translational science. South America and the Middle East and Africa remain early-stage areas, with activity centered more on academic institutes and contract manufacturing expansion than on independent platform creation. Even so, the presence of global CROs offering AI discovery services is starting to build local demand that can turn into measurable regional share after 2027.

Competitive Landscape

The AI in antibody discovery market remains moderately fragmented, with 15-20 specialist platform companies competing beside a newer layer of technology infrastructure providers. Even within that fragmented structure, commercial activity is starting to concentrate around firms that can show benchmark quality, patent depth, and modality breadth. The AI in antibody discovery market is therefore becoming less about broad participation and more about technical proof that outside partners can inspect and compare. Absci said in its 2026 Form 10-K that it held 69 issued patents and 53 pending patents, which shows how intellectual property has become part of the commercial screening process for pharma partners. That strategy matters because buyers are no longer assessing only discovery speed, they are also judging whether a platform can support enablement and withstand later disputes around AI-generated antibody claims.

Preferred-vendor positioning is also becoming a stronger source of advantage. BigHat Biosciences deepened its relationship with Eli Lilly through the Catalyze360 initiative in April 2025 and then through TuneLab integration in January 2026, which illustrates how repeated entry into a single large pharma account can create multi-year revenue visibility. The AI in antibody discovery market is rewarding that type of account expansion because it converts technical credibility into longer commercial duration. White space remains clearest in GPCR and membrane-protein antibodies, in multispecific programs for rare diseases, and in fully integrated CRO-style discovery models that can run from target selection to IND-ready output.

A second layer of competition is coming from firms that can post unusually strong benchmarks or raise enough capital to build a broader stack. Latent Labs reported 67% success rates and 56-fold speed gains for its Latent-Y nanobody design system, which signals how fast specialist performance thresholds are moving[3]Latent Labs, “Latent-Y: An Autonomous Agent for Nanobody Design with 67% Success Rate,” Latent Labs, latentlabs.bio. Insilico Medicine also raised USD 110 million in Series E financing in March 2025, a move that supports its ability to integrate target identification, design, and optimization into a larger vertical model. In the AI in antibody discovery market, benchmark transparency is becoming the fastest-shifting differentiator because platform selection is moving toward externally visible hit rates and structural metrics rather than closed internal demonstrations. That favors companies that publish, disclose, or otherwise validate their results in settings that partners can compare with confidence.

AI In Antibody Discovery Industry Leaders

Generate:Biomedicines

Absci

AbCellera

Chai Discovery

LabGenius Therapeutics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Sino Biological launched XPressMAX, a high-throughput expression platform validating over 2,000 scFv and VHH candidates within 3-4 weeks per batch, directly addressing the wet-lab triage bottleneck constraining downstream throughput from AI-generated candidate libraries.

- April 2026: MOLCURE disclosed a confidential AI antibody design platform co-developed with Hitachi, employing trusted execution environments to protect proprietary sequence data during collaborative AI training sessions, and 28 ongoing projects across 19 industry partnerships were confirmed at the same disclosure event.

- April 2026: RevolKa launched RevoAb, an AI-optimized antibody engineering platform generating a 7x improvement in expression yield versus prior methods, reporting 92% satisfaction among initial users and targeting CRO and biotech customers seeking integrated expression optimization.

Global AI In Antibody Discovery Market Report Scope

As per the scope of the report, AI in antibody discovery refers to the application of artificial intelligence technologies, such as machine learning, deep learning, and data analytics, to identify, design, and optimize antibodies for therapeutic and diagnostic purposes.

The segmentation for the AI in antibody discovery market is categorized by offering, technology, application, antibody modality, therapeutic area, end user, and geography. By offering, the market includes software platforms, discovery services, integrated platform partnerships, and data and model licensing. By technology, it covers structure prediction, generative AI and protein language models, machine learning and deep learning, natural language processing and knowledge graphs, and closed-loop AI with lab automation. By application, the segmentation includes target identification and validation, epitope mapping and binder screening, de novo antibody design, lead optimization and engineering, and developability and manufacturability prediction.

By antibody modality, the market is divided into monoclonal antibodies, bispecific antibodies, multispecific antibodies, antibody-drug conjugates, and nanobodies and single-domain antibodies. By therapeutic area, it encompasses oncology, autoimmune and inflammatory diseases, infectious diseases, neurology, metabolic diseases, and rare diseases. By end user, the segmentation includes pharmaceutical companies, biotechnology and platform companies, CROs and CDMOs, and academic and research institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Software Platforms |

| Discovery Services |

| Integrated Platform Partnerships |

| Data and Model Licensing |

| Structure Prediction |

| Generative AI and Protein Language Models |

| Machine Learning and Deep Learning |

| Natural Language Processing and Knowledge Graphs |

| Closed-loop AI with Lab Automation |

| Target Identification and Validation |

| Epitope Mapping and Binder Screening |

| De novo Antibody Design |

| Lead Optimization and Engineering |

| Developability and Manufacturability Prediction |

| Monoclonal Antibodies |

| Bispecific Antibodies |

| Multispecific Antibodies |

| Antibody-Drug Conjugates |

| Nanobodies and Single-domain Antibodies |

| Oncology |

| Autoimmune and Inflammatory Diseases |

| Infectious Diseases |

| Neurology |

| Metabolic Diseases |

| Rare Diseases |

| Pharmaceutical Companies |

| Biotechnology and Platform Companies |

| CROs and CDMOs |

| Academic and Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Software Platforms | |

| Discovery Services | ||

| Integrated Platform Partnerships | ||

| Data and Model Licensing | ||

| By Technology | Structure Prediction | |

| Generative AI and Protein Language Models | ||

| Machine Learning and Deep Learning | ||

| Natural Language Processing and Knowledge Graphs | ||

| Closed-loop AI with Lab Automation | ||

| By Application | Target Identification and Validation | |

| Epitope Mapping and Binder Screening | ||

| De novo Antibody Design | ||

| Lead Optimization and Engineering | ||

| Developability and Manufacturability Prediction | ||

| By Antibody Modality | Monoclonal Antibodies | |

| Bispecific Antibodies | ||

| Multispecific Antibodies | ||

| Antibody-Drug Conjugates | ||

| Nanobodies and Single-domain Antibodies | ||

| By Therapeutic Area | Oncology | |

| Autoimmune and Inflammatory Diseases | ||

| Infectious Diseases | ||

| Neurology | ||

| Metabolic Diseases | ||

| Rare Diseases | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology and Platform Companies | ||

| CROs and CDMOs | ||

| Academic and Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of AI in antibody discovery in 2026?

The market stands at USD 0.62 billion in 2026 and is projected to reach USD 1.88 billion by 2031 at a 24.61% CAGR.

Why are drug developers turning to AI for antibody programs?

Traditional programs have often cost more than USD 50 million over 4-6 years with preclinical attrition above 90%, while AI-guided programs have shown the ability to cut cost and time materially.

Which region leads spending today and which one is growing fastest?

North America led with 43.44% share in 2025, while Asia-Pacific is the fastest-growing region with a 26.22% CAGR through 2031.

Which part of the workflow brings in the most revenue right now?

Target Identification and Validation held the largest application share at 28.52% in 2025, showing that buyers still spend most at the earlier and lower-risk end of discovery.

Which antibody format is seeing the strongest future momentum?

Multispecific Antibodies is the fastest-growing modality at a 27.55% CAGR through 2031, even though Monoclonal Antibodies still held 55.62% of revenue in 2025.

What is the main bottleneck limiting wider adoption?

Wet-lab triage remains a major constraint because model output is rising faster than expression, purification, and binding validation capacity, which slows both program throughput and patent timing.

Page last updated on: