CRISPR-based Gene Editing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.65 Billion |

| Market Size (2031) | USD 12.45 Billion |

| Growth Rate (2026 - 2031) | 13.35% CAGR |

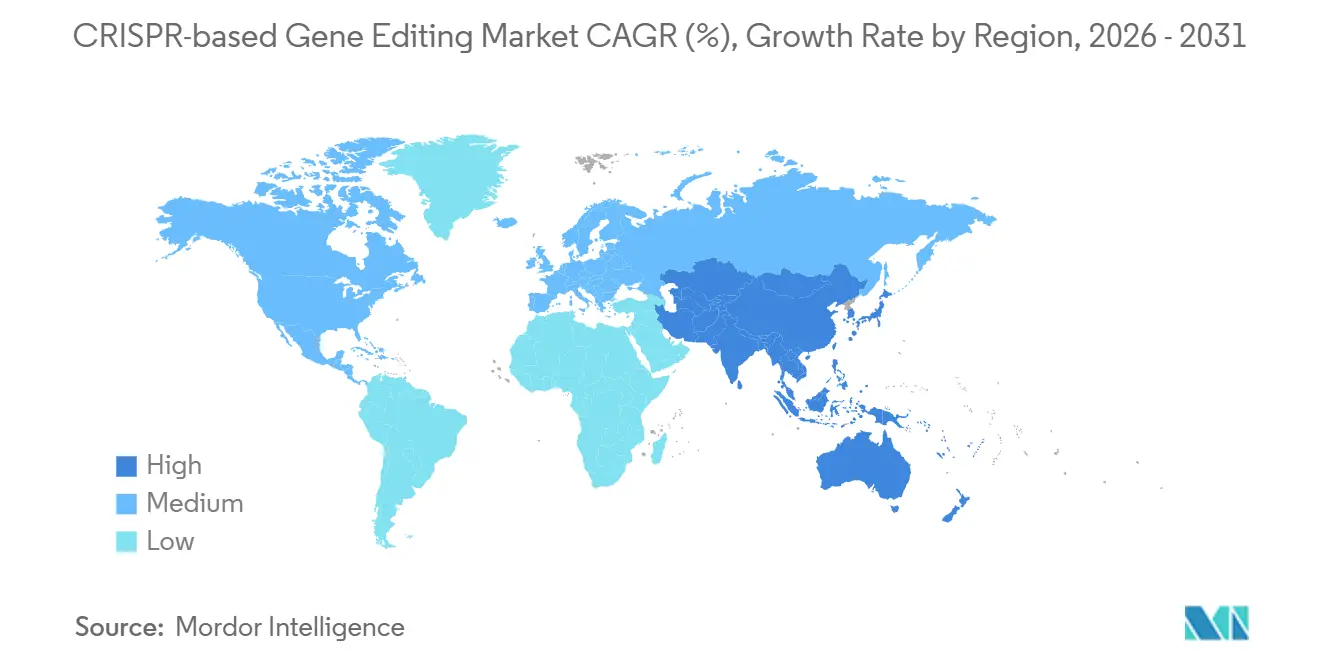

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CRISPR-based Gene Editing Market Analysis by Mordor Intelligence

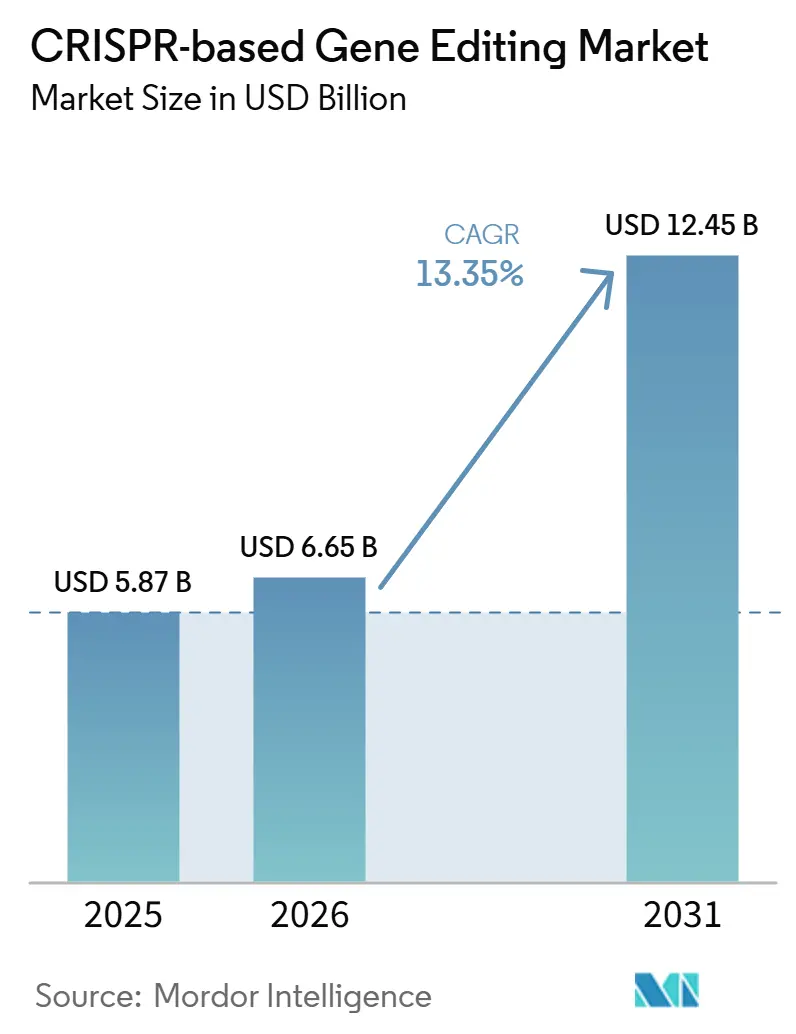

The CRISPR-based Gene Editing Market size is projected to expand from USD 5.87 billion in 2025 and USD 6.65 billion in 2026 to USD 12.45 billion by 2031, registering a CAGR of 13.35% between 2026 to 2031.

Growth in the CRISPR-based gene editing market reflects parallel progress in regulatory familiarity, GMP manufacturing scale-up, and wider institutional use across pharmaceutical R&D, academic research, and diagnostic workflows. Commercial traction has become more visible as CASGEVY exceeded USD 100 million in revenue during 2025 and posted a near threefold increase in patient initiations and cell collections compared with 2024, which showed that approved CRISPR therapies can move beyond clinical validation into revenue generation. The market is also benefiting from a financing effect, because every successful clinical and regulatory milestone lowers perceived execution risk for later programs and helps widen the capital pool available to the CRISPR-based gene editing market. Delivery limits outside the liver and persistent concern around off-target editing still restrain expansion, because both issues extend validation needs and keep development timelines demanding for sponsors entering later-stage studies. Even with those constraints, the combination of stronger commercial precedent, better GMP readiness, and growing software integration keeps the CRISPR-based gene editing market on a firm growth path through 2031.

Key Report Takeaways

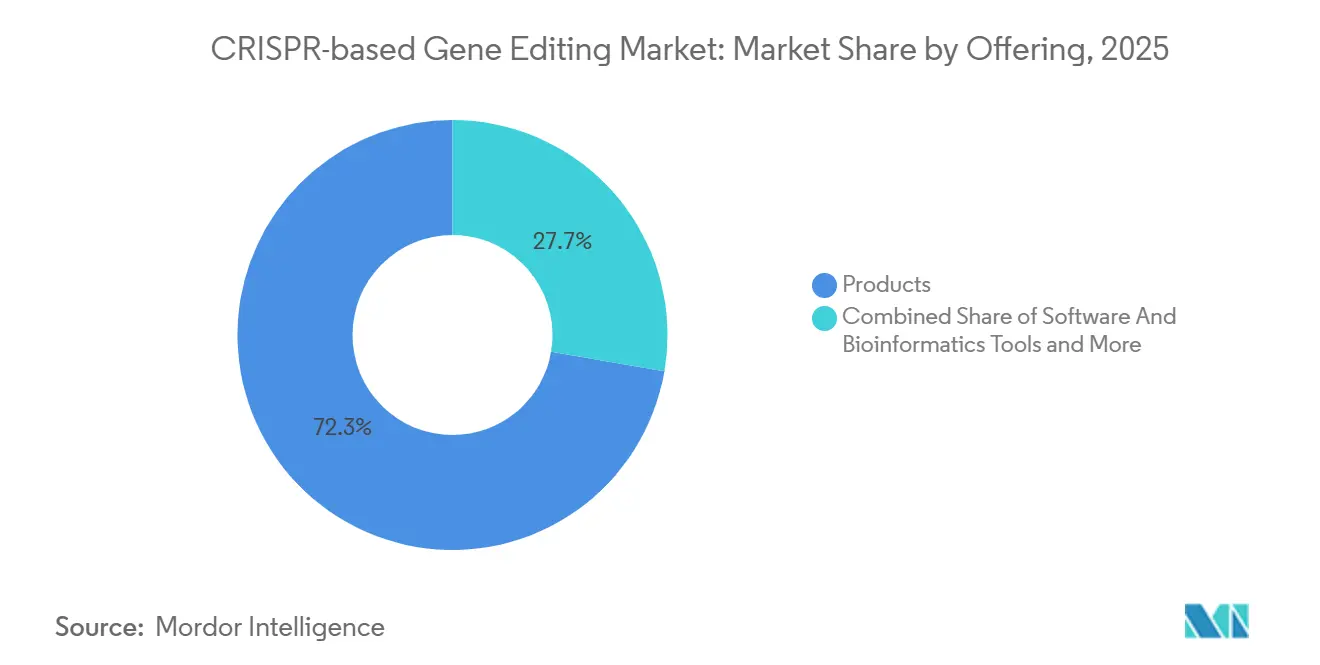

- By offering, products held 72.31% share in 2025, while software and bioinformatics tools are forecast to expand at 18.38% CAGR through 2031.

- By technology, CRISPR-Cas9 held 52.24% share in 2025, while CRISPR-Cas13 is projected to record the fastest growth at 19.52% CAGR through 2031.

- By gene editing modality, ex-vivo editing accounted for 54.26% share in 2025, while in-vivo editing is expected to advance at 14.55% CAGR through 2031.

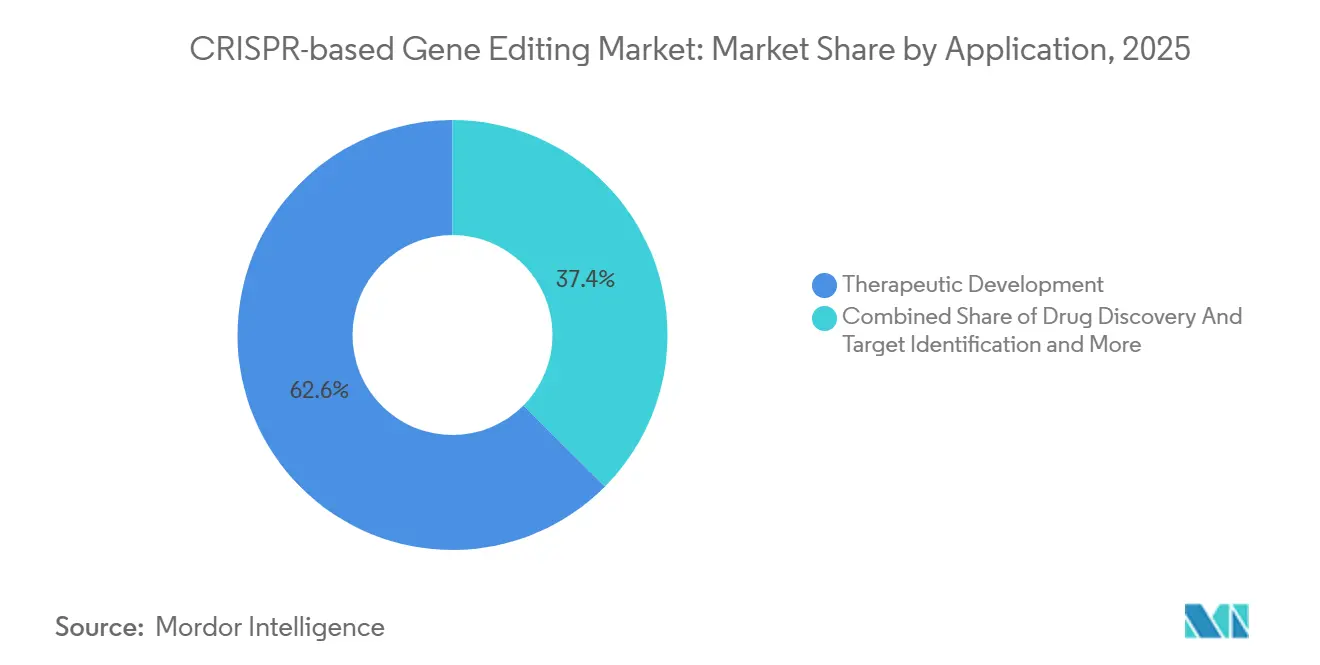

- By application, therapeutic development captured 62.56% share in 2025 and is expected to record the fastest expansion at 17.65% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies held 42.52% share in 2025, while contract research organizations and CDMOs are expected to grow at 18.25% CAGR through 2031.

- By geography, North America held 41.62% share in 2025, while the Asia-Pacific is projected to grow at 15.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global CRISPR-based Gene Editing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Therapeutic Development For Genetic Disorders | +3.5% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Clinical Validation Of CRISPR Based Cell And Gene Therapies | +2.8% | Global, with North America leading approvals | Medium term (2-4 years) |

| Expansion Of Translational Workflows In Pharma And Biotech R&D | +2.0% | Global | Medium term (2-4 years) |

| Widening Use In Multiplex Screening And Functional Genomics Platforms | +1.5% | North America, Europe, APAC (China, Japan) | Medium term (2-4 years) |

| GMP Grade Tooling And Workflow Standardization For Commercial Programs | +1.0% | North America, Europe, APAC | Short term (≤ 2 years) |

| IP And Reagent Ecosystems Supporting Next Generation Editing Modalities | +0.7% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Therapeutic Development For Genetic Disorders

The CRISPR-based gene editing market is moving beyond proof-of-concept and into a stage where clinical development is becoming more repeatable across multiple disease areas. CASGEVY’s 2025 commercial performance showed that approved CRISPR therapies can support real patient uptake and meaningful revenue generation, which matters because it narrows the gap between scientific validation and commercial execution. A May 2025 New England Journal of Medicine report described a patient-specific in vivo base-editing treatment for carbamoyl-phosphate synthetase 1 deficiency that was delivered within months of diagnosis, which showed how quickly development timelines can compress in high-need settings. That matters for the CRISPR-based gene editing market because faster movement from diagnosis to intervention can widen the future addressable population for severe inherited disorders. The same pattern also improves sponsor confidence that rare disease programs can progress with clearer development logic once a working regulatory and manufacturing path has been demonstrated. As a result, therapeutic development is no longer just a scientific frontier in the CRISPR-based gene editing market, because it now functions as the main engine behind future revenue expansion.

Clinical Validation Of CRISPR Based Cell And Gene Therapies

Clinical validation now spans ex-vivo cell therapy, in-vivo liver editing, and early RNA-targeting approaches, which gives the CRISPR-based gene editing market a broader evidence base than earlier gene therapy waves. Phase 1 data for CRISPR Therapeutics’ CTX310 showed a 73% mean ANGPTL3 reduction, a 55% triglyceride reduction, and a 49% LDL reduction after a single intravenous infusion, with few adverse events reported in the early dataset. Nexiguran ziclumeran also delivered rapid, deep, and durable serum TTR reductions in hereditary transthyretin amyloidosis with polyneuropathy, which added another human proof point for in-vivo editing in a clinically meaningful setting. In oncology, CRISPR-Cas9 knockout of CISH in tumor-infiltrating lymphocytes produced complete and ongoing responses in metastatic colorectal cancer in a Phase 1 study, which showed that durable anti-tumor activity is possible even in difficult solid tumors. Together, these results show that the CRISPR-based gene editing market is gaining validation across different editing settings rather than relying on one narrow clinical use case. They also show why commercial and regulatory expectations are shifting upward for later programs that now enter development behind a stronger body of human data.

Expansion Of Translational Workflows In Pharma And Biotech R&D

The CRISPR-based gene editing market is also being supported by deeper integration into translational research workflows across pharmaceutical and biotechnology organizations. Thermo Fisher Scientific’s 2025 collaboration with OpenAI reflects a push to embed AI-assisted life science tools into drug development, which strengthens the role of computational support inside CRISPR-enabled discovery pipelines. A genome-scale CRISPRi perturbation atlas of human induced pluripotent stem cells, published in July 2026, showed how gene function mapping is now operating at a scale that directly informs target prioritization and translational research design. GenScript Biotech’s full-year 2025 results also reflected growing customer reliance on integrated platforms that connect gene synthesis, protein production, and cell therapy support services inside a broader workflow structure[1]GenScript Biotech Corporation, “GenScript Biotech Corp Reports Strong FY2025 Results,” GenScript Press Release, genscript.com. This changes the position of CRISPR inside the CRISPR-based gene editing market, because it is no longer limited to a validation tool used late in the research cycle. It is increasingly being treated as a critical operational layer that supports target discovery, lead optimization, and biomarker development from earlier stages onward.

Widening Use In Multiplex Screening And Functional Genomics Platforms

Functional genomics has become one of the most active use cases supporting the CRISPR-based gene editing market, especially where target discovery and resistance mapping depend on large-scale perturbation studies. A 2025 review in Science China Life Sciences described how CRISPR screening is reshaping therapeutic target identification and drug discovery with greater precision and scalability than older approaches. Precision multiplexed base editing in human cells using Cas12a-derived editors enabled editing at up to 15 endogenous target sites simultaneously, which materially improves the speed of variant-to-function work in complex biological systems. Another July 2026 study in Nature Communications showed that AI-guided CRISPR screening could reveal therapeutic targets in psoriasis, which demonstrates how AI is improving the signal extracted from each screen. These developments matter for the CRISPR-based gene editing market because they shorten the time between genetic perturbation and actionable biological interpretation. They also improve the economics of early discovery by making large functional studies more informative and more operationally efficient.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Delivery Efficiency And Tissue Specific Uptake Limitations | -1.8% | Global | Long term (≥ 4 years) |

| Off Target Risk And Editing Fidelity Concerns | -1.5% | Global | Medium term (2-4 years) |

| Ethical And Germline Governance Constraints | -0.9% | Global (EU, US, Japan particularly) | Long term (≥ 4 years) |

| High Cost Of Translational Scale Up, QA, And Regulatory Evidence Generation | -0.8% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Delivery Efficiency And Tissue Specific Uptake Limitations

Delivery remains the most important technical limit on how far the CRISPR-based gene editing market can expand beyond current liver-focused use cases. Lipid nanoparticles have supported hepatic editing programs, but delivery to the brain, heart, skeletal muscle, and hematopoietic stem cells outside ex-vivo settings remains much less mature, which restricts the near-term indication map[2]European Medicines Agency and Intellia Therapeutics, “Challenges in Development of In Vivo Gene Editing Therapeutics,” European Medicines Agency, ema.europa.eu. A 2025 review in Precision Medicine and Engineering also found that organ-specific delivery strategies continue to face biodistribution and immune clearance challenges, which shows that vector precision is still inadequate for many targets. rAAV-CRISPR delivery adds another layer of difficulty because Cas9-directed immune clearance can weaken treatment effect and force the use of transient immunosuppression protocols. These issues keep the CRISPR-based gene editing market segmented into a liver-led early in-vivo wave and a later non-hepatic expansion path. Until that delivery barrier improves, many programs will continue to favor ex-vivo settings where editing and quality control are easier to manage before reinfusion.

Off Target Risk And Editing Fidelity Concerns

Off-target editing remains a regulatory and development burden for the CRISPR-based gene editing market, even as editing systems become more refined. A 2025 review in Molecular Therapy, Nucleic Acids noted that the lack of standardized off-target assessment guidelines still creates inconsistent analytical practice across clinical programs. Base editing and prime editing reduce some double-strand break risks, but they introduce distinct mutagenic profiles such as bystander edits and reverse transcriptase-related indels that still require long-term evaluation. That means development teams in the CRISPR-based gene editing market must spend more time and capital on profiling work before regulators are likely to accept broader clinical use. The burden is especially heavy for smaller biotechnology companies that do not have the balance sheet strength to absorb prolonged nonclinical and translational work. As more candidates move deeper into trials, editing fidelity will continue to shape cost, timing, and competitive viability across the CRISPR-based gene editing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Reagent Revenues Lead, But Software Defines the Next Growth Curve

Products held 72.31% of the offering segment in 2025, which made them the largest current revenue pool inside the CRISPR-based gene editing market. That position reflects recurring demand for guide RNA synthesis, Cas protein enzymes, and delivery vectors across both research settings and clinical development workflows. Reagent demand is also being lifted by tighter quality expectations as more programs move closer to regulated therapeutic use. Synthego’s cGMP-grade gRNA solutions, which are produced under ISO 13485 certification and FDA GMP-compliant conditions, show how the reagent bar is moving upward for clinical-stage work[3]Synthego Corporation, “cGMP CRISPR Clinical Solutions,” Synthego, synthego.com. Services form the third offering pillar in the CRISPR-based gene editing market, spanning editing design, cell therapy manufacturing, and outsourced functional genomics support for sponsors that want to limit fixed investment.

Software and bioinformatics tools remain the smallest current offering segment, but they are projected to expand at 18.38% CAGR through 2031, which makes them the fastest-growing component of the CRISPR-based gene editing market. CRISPR-GPT, reported in Nature Biomedical Engineering in 2025, showed how agentic software can automate experiment design and data analysis, which lowers the expertise barrier for laboratories that lack deep computational resources. The July 2026 CRISPRi atlas in human iPSCs further showed that bioinformatics is no longer a downstream reporting layer, because it now supports high-scale interpretation within both academic and industrial settings. This shift matters because procurement in the CRISPR-based gene editing market is moving toward platforms that combine wet-lab editing capability with stronger computational decision support. Over time, that should narrow the revenue gap between products and software even if reagents remain the larger absolute category.

By Technology: Cas9 Holds Structural Dominance While Next-Generation Editors Gain Clinical Footholds

CRISPR-Cas9 held 52.24% of the technology segment in 2025, which keeps it as the anchor platform across the CRISPR-based gene editing market. Its lead comes from deep integration into ex-vivo cell therapy workflows and from its growing use in liver-directed in-vivo editing programs. Sponsors also continue to favor Cas9 because it carries the strongest clinical familiarity and the clearest regulatory precedent among commercial-stage editing systems. Base editing is progressing as an important adjacent platform, and its clinical roadmap has already drawn attention to manufacturing control requirements and later-stage trial design standards. That dynamic keeps Cas9 structurally dominant in the CRISPR-based gene editing market, while newer editors build validation through more selective clinical entry points.

CRISPR-Cas13 is the fastest-growing technology segment at 19.52% CAGR through 2031, which highlights how RNA targeting is creating a distinct growth lane inside the CRISPR-based gene editing market. SHERLOCK and DETECTR platforms offer attomolar sensitivity with results in 30 to 60 minutes, which gives CRISPR diagnostics a meaningful point-of-care position relative to PCR in time-sensitive or resource-constrained settings. Prime editing also entered first-in-human trial stages in 2026, although efficiency and delivery remain important barriers to wide adoption. AI-designed Cas variants such as OpenCRISPR-1 indicate that the future technology map will extend beyond the currently familiar Cas families. As a result, the CRISPR-based gene editing market is likely to keep a dual structure in which Cas9 supports scale today while newer editors expand the future application perimeter.

By Gene Editing Modality: Commercial Maturity Anchors Ex-Vivo While In-Vivo Builds a Clinical Bridgehead

Ex-vivo editing held 54.26% of the modality segment in 2025, which made it the larger current modality in the CRISPR-based gene editing market. That lead reflects established manufacturing protocols for hematopoietic stem cell editing and CAR-T workflows, where product handling, quality control, and release testing are more manageable before reinfusion. CASGEVY’s commercial rollout has also given regulators and manufacturers a more familiar operational reference for ex-vivo CRISPR therapy execution. Caribou Biosciences is extending that platform through vispa-cel and CB-011, with dose expansion activity and pivotal planning that keep ex-vivo editing active in hematologic oncology. CRISPR Therapeutics’ zugo-cel work in autoimmune indications adds another example of how the ex-vivo platform is broadening beyond its earliest blood disorder focus.

In-vivo editing is projected to expand at 14.55% CAGR through 2031, which makes it the faster-growing modality in the CRISPR-based gene editing market as hepatic programs move through clinical development. CRISPR Therapeutics has already advanced CTX310 into Phase 1b work after encouraging early human data, which supports the view that systemic in-vivo editing is progressing from concept toward broader clinical relevance. Editas Medicine’s EDIT-401 showed more than 90% mean LDL-C reduction in non-human primates, along with meaningful Lp(a) and ApoB reductions, and the company targeted IND or CTA filing for mid-2026. Even so, today’s in-vivo opportunity in the CRISPR-based gene editing market is still concentrated in liver-accessible biology. Until extrahepatic delivery improves, modality growth will remain real but bounded by tissue access rather than by demand.

By Application: Therapeutic Development Commands Both Scale and Momentum

Therapeutic development accounted for 62.56% share of the CRISPR-based gene editing market size in 2025, and it is projected to grow at 17.65% CAGR through 2031, which makes it both the largest and fastest-moving application in the current revenue structure. This leadership reflects a shift away from dependence on research tools alone and toward revenue creation from clinical assets and approved therapies. CRISPR Therapeutics entered 2026 with 7 clinical-stage programs across hemoglobinopathies, cardiovascular disease, oncology, autoimmune disorders, and regenerative medicine, which shows how one validated platform can spread into several treatment areas. Drug discovery and target identification remain the second-largest application, supported by functional genomics and AI-assisted screening workflows that are becoming more embedded in translational R&D. This keeps therapeutic development at the center of the CRISPR-based gene editing market, while discovery applications continue to supply the target pipeline that feeds future clinical work.

Diagnostics is an emerging application pocket in the CRISPR-based gene editing market, supported by Cas12 and Cas13 systems that can deliver lab-quality sensitivity in formats closer to point-of-care use. That creates a practical advantage over PCR where speed, cost, or infrastructure constraints shape the testing model. Preclinical model development also keeps a stable role as academic labs and CROs generate edited cell lines and animal models before programs move into clinical translation. Because revenue concentration remains high in therapeutic development, major clinical readouts in the next few years will influence far more than the sponsoring pipeline alone. Positive outcomes from late-stage or near-late-stage programs are likely to reprice expectations across the full application mix within the CRISPR-based gene editing market.

By End User: CRO and CDMO Outsourcing Redefines the Manufacturing Value Chain

Pharmaceutical and biotechnology companies held 42.52% of the end-user segment in 2025, which kept them as the largest direct demand center in the CRISPR-based gene editing market. Their lead reflects the fact that they fund most therapeutic development, own key clinical pipelines, and control program advancement decisions across multiple disease areas. Academic and research institutes remain the second-largest end-user group and continue to supply many of the new editing tools, disease models, and biological findings that later enter commercial pipelines. Diagnostic laboratories form a smaller but structurally distinct end-user category as more clinically oriented detection platforms move closer to practical use. This mix shows that the CRISPR-based gene editing market still depends on commercial sponsors for revenue scale, even while innovation remains distributed across several institutional types.

Contract research organizations and CDMOs are projected to grow at 18.25% CAGR through 2031, which makes them the fastest-expanding end-user segment in the CRISPR-based gene editing market. Their momentum reflects rising sponsor interest in outsourcing GMP-grade payload manufacturing, editing workflow execution, and specialized process development rather than building every capability in house. Forge Biologics’ 200,000 sq ft Hearth facility in Columbus, Ohio, with 20,000L of bioreactor capacity, shows the scale of infrastructure now being built to support advanced therapy manufacturing programs. These service providers also matter because their validation work across multiple clients helps build a shared GMP operating knowledge base for the wider CRISPR-based gene editing market. Over time, that operating experience can lower execution friction and improve manufacturing consistency for sponsors that would otherwise face steep internal capability gaps.

Geography Analysis

North America held 41.62% of CRISPR-based gene editing market share in 2025, which kept it as the largest regional contributor in the current global structure. The region’s lead rests on deep biotechnology infrastructure, stronger financing access, established clinical trial networks, and a concentration of companies with late-stage or commercial CRISPR assets. CRISPR Therapeutics entered 2026 with approximately USD 2 billion in cash and multiple active clinical programs, which reinforces North America’s role as the deepest capital and pipeline base for the CRISPR-based gene editing market. Editas Medicine also planned first-in-human progress for EDIT-401 in 2026, which adds to the region’s in-vivo development momentum. The U.S. Patent and Trademark Office’s reaffirmation of the Broad Institute’s position in the CRISPR/Cas9 interference case also shows how intellectual property still shapes competitive positioning and licensing structures in the leading regional cluster.

Europe remains the second-largest regional block in the CRISPR-based gene editing market and continues to develop under the EMA’s Advanced Therapy Medicinal Products framework. The EMA granted CASGEVY PRIME designation and recommended 15-year long-term follow-up for genome-editing medicinal products, which has direct implications for development cost and timeline planning across the regional pipeline. The December 2025 agreement on major pharmaceutical legislation reform in the European Union signaled an intent to streamline advanced therapy governance and reduce uncertainty for developers entering the region. Germany and the United Kingdom remain the strongest national anchors, while France, Italy, Spain, and the rest of Europe are expanding as treatment center capacity and reimbursement pathways improve.

Asia-Pacific is projected to grow at 15.15% CAGR through 2031, which makes it the fastest-growing regional segment in the CRISPR-based gene editing market. China and Japan lead the region’s momentum through expanding clinical activity, domestic development capability, and policy structures that are becoming more relevant to advanced therapies. India, South Korea, and Australia also contribute growing academic activity and sponsored trial participation, which supports a broader regional base beyond the two leading national markets. The Middle East and Africa, led by GCC countries with high sickle cell disease and thalassemia burden, represent a demand-pull opportunity for approved CRISPR therapies as access pathways mature. South America, with Brazil and Argentina as the main anchors, remains in earlier adoption and is still shaped more by university research and sponsored clinical trial activity than by broad commercial penetration.

Competitive Landscape

The competitive landscape in the CRISPR-based gene editing market is moderately concentrated at the therapeutic level and fragmented across tools, reagents, software, and service offerings. CRISPR Therapeutics, Intellia Therapeutics, and Vertex Pharmaceuticals hold the most visible positions in clinical-stage assets and emerging commercial revenue, while Thermo Fisher Scientific, Danaher, QIAGEN, Merck KGaA, and Integrated DNA Technologies compete on tool breadth, workflow compatibility, and GMP readiness. One clear strategic pattern has been the move toward multi-program in-vivo platforms, which allows leading developers to spread a single editing and delivery backbone across several disease areas. Another has been precision-indication partnering, such as CRISPR Therapeutics’ collaboration with Lilly to evaluate zugocabtagene geleucel with pirtobrutinib in aggressive B-cell lymphomas. Danaher’s work with the Innovative Genomics Institute and the Chan Zuckerberg Initiative on a CRISPR Cookbook is a different type of strategic move, because it aims to standardize protocols and expand clinical-grade manufacturing know-how across the ecosystem rather than capture one narrow product niche.

White-space opportunity still clusters around extrahepatic in-vivo delivery, epigenetic editing, and CRISPR diagnostics in emerging markets, which means the CRISPR-based gene editing market still has visible room for new positioning. Editas Medicine is pursuing LDLR upregulation through in-vivo CRISPR for familial hypercholesterolemia with EDIT-401, which gives it a differentiated route that does not directly overlap with the hemoglobinopathy focus of CASGEVY. Epicrispr Biotechnologies’ cGMP manufacturing partnership with Forge Biologics shows how emerging players are using specialist partners to reach the clinic in indications that depend on durable gene silencing rather than sequence-level editing. In the tools segment, FDA 21 CFR Part 11 alignment and ISO 13485 certification are becoming meaningful differentiators for suppliers that want preferred-vendor status in late-stage programs. That matters because clinical sponsors in the CRISPR-based gene editing market increasingly need vendors that can support both scientific performance and regulated manufacturing expectations.

A less visible pressure point in the CRISPR-based gene editing market is the gap between scientific success and commercial execution capacity. CASGEVY’s precedent showed that approved CRISPR therapies still require manufacturing depth, patient operations capability, and commercialization infrastructure that many single-program biotechnology companies do not possess alone. That reality keeps partnership, licensing, and acquisition pressure high for smaller developers whose science may be strong but whose operating model remains narrow. It also means the CRISPR-based gene editing market is likely to remain strategically active, even if product approvals continue to emerge from a relatively small group of visible leaders.

CRISPR-based Gene Editing Industry Leaders

Thermo Fisher Scientific Inc.

Merck KGaA

Danaher Corporation

GenScript Biotech Corporation

New England Biolabs, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ChristianaCare’s Gene Editing Institute launched DECODR Inc., a for-profit company created to expand access to a leading software tool that evaluates CRISPR gene editing effectiveness.

- March 2026: Editas Medicine Inc. announced that the U.S. Patent and Trademark Office reaffirmed the Patent Trial and Appeal Board’s (PTAB) decision favoring the Broad Institute in a U.S. patent interference over CRISPR/Cas9 editing in human cells. The case involved the University of California, the University of Vienna, and Emmanuelle Charpentier (collectively, CVC), and the Broad Institute, Massachusetts Institute of Technology (MIT), and Harvard University (collectively, Broad).

Global CRISPR-based Gene Editing Market Report Scope

As per the scope of the report, CRISPR-based gene editing is a revolutionary biotechnology technique that allows scientists to precisely modify an organism's DNA. It utilizes the CRISPR-Cas system, which is derived from a natural immune defense mechanism in bacteria. The technique involves designing a guide RNA to target specific DNA sequences and using the Cas enzyme (such as Cas9) to cut the DNA at the desired location. This enables the addition, deletion, or alteration of genetic material, facilitating research, medical therapies, and crop improvement.

The CRISPR-based gene editing market is segmented by offering into products, software and bioinformatics tools, and services; by technology into CRISPR-Cas9, CRISPR-Cas12, CRISPR-Cas13, base editing, prime editing, epigenetic editing, and other technologies; by gene editing modality into ex vivo editing and in vivo editing; by application into therapeutic development, drug discovery and target identification, preclinical model development, diagnostics, and other applications; by end user into pharmaceutical and biotechnology companies, academic and research institutes, contract research organizations and CDMOs, diagnostic laboratories, and other end users; and by geography into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Products |

| Software And Bioinformatics Tools |

| Services |

| CRISPR-Cas9 |

| CRISPR-Cas12 |

| CRISPR-Cas13 |

| Base Editing |

| Prime Editing |

| Epigenetic Editing |

| Other Technologies |

| Ex-Vivo Editing |

| In-Vivo Editing |

| Therapeutic Development |

| Drug Discovery And Target Identification |

| Preclinical Model Development |

| Diagnostics |

| Other Applications |

| Pharmaceutical And Biotechnology Companies |

| Academic And Research Institutes |

| Contract Research Organizations And CDMOs |

| Diagnostic Laboratories |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Products | |

| Software And Bioinformatics Tools | ||

| Services | ||

| By Technology | CRISPR-Cas9 | |

| CRISPR-Cas12 | ||

| CRISPR-Cas13 | ||

| Base Editing | ||

| Prime Editing | ||

| Epigenetic Editing | ||

| Other Technologies | ||

| By Gene Editing Modality | Ex-Vivo Editing | |

| In-Vivo Editing | ||

| By Application | Therapeutic Development | |

| Drug Discovery And Target Identification | ||

| Preclinical Model Development | ||

| Diagnostics | ||

| Other Applications | ||

| By End User | Pharmaceutical And Biotechnology Companies | |

| Academic And Research Institutes | ||

| Contract Research Organizations And CDMOs | ||

| Diagnostic Laboratories | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 to 2031 growth outlook for CRISPR-based gene editing?

The CRISPR-based gene editing market is valued at USD 6.65 billion in 2026 and is forecast to reach USD 12.45 billion by 2031 at a CAGR of 13.35%, supported by therapeutic progress, manufacturing scale-up, and broader translational use.

Which application area currently leads revenue generation in CRISPR-based gene editing?

Therapeutic development leads with 62.56% share in 2025 and is also the fastest-growing application at 17.65% CAGR through 2031, which shows how strongly the sector is shifting toward clinical and commercial use.

Why does ex-vivo editing still hold a larger position than in-vivo editing?

Ex-vivo editing held 54.26% share in 2025 because manufacturing control, release testing, and regulatory familiarity are stronger when cells are edited outside the body before reinfusion.

Which end-user group is expanding the fastest in CRISPR workflows?

Contract research organizations and CDMOs are growing at 18.25% CAGR through 2031 as sponsors increasingly outsource GMP manufacturing, process development, and specialized editing support.

What is the main technical barrier limiting wider adoption beyond liver-focused programs?

Delivery remains the main barrier, because tissue-specific uptake outside the liver is still difficult in organs such as the brain, heart, and skeletal muscle, which limits the near-term indication map.

Which region is leading today, and which region is growing the fastest?

North America led with 41.62% share in 2025 due to its clinical and financing depth, while Asia-Pacific is the fastest-growing region at 15.15% CAGR through 2031.

Page last updated on: