AI-Based EHR Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.15 Billion |

| Market Size (2031) | USD 31.87 Billion |

| Growth Rate (2026 - 2031) | 25.71% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Based EHR Systems Market Analysis by Mordor Intelligence

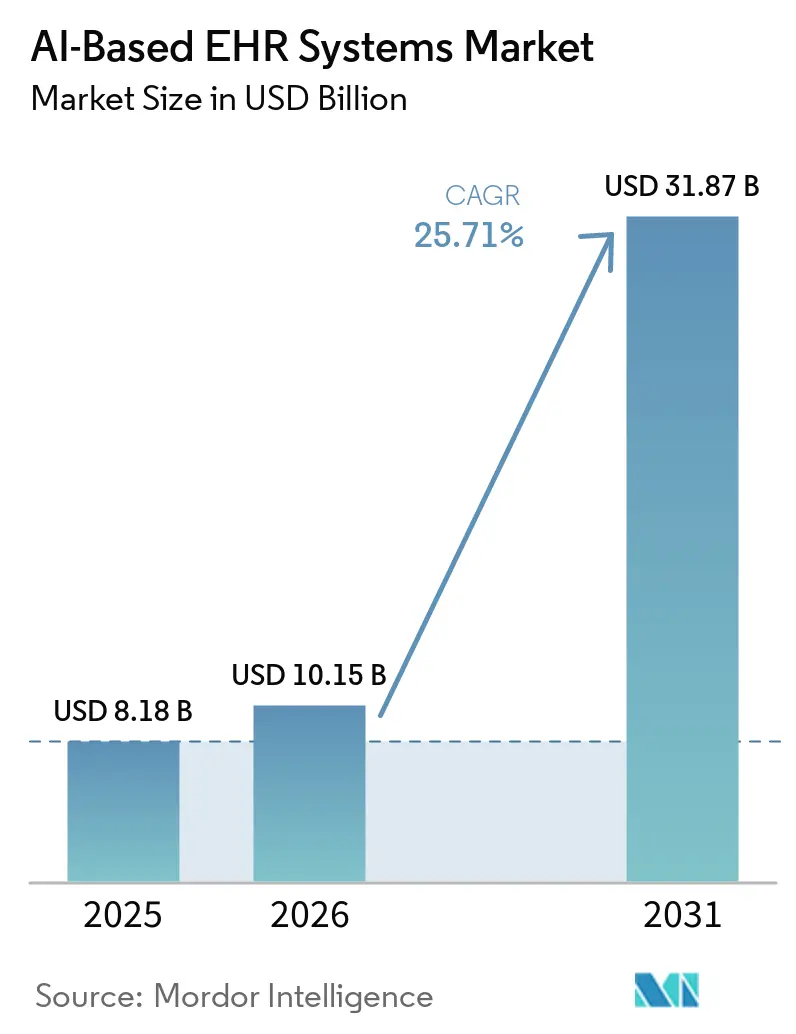

The AI-based EHR systems market is expected to grow from USD 8.18 billion in 2025 to USD 10.15 billion in 2026 and is forecasted to reach USD 31.87 billion by 2031 at 25.71% CAGR over 2026-2031. This pace reflects a broad shift in buyer expectations, because providers now want EHR platforms to interpret clinical data during care, not only store it after the encounter. Growth is being supported by ambient documentation, embedded AI inside core workflows, stronger interoperability standards, and rising pressure to link better records with coding accuracy, cleaner reimbursement, and more consistent care decisions. The AI-based EHR systems market is also being reshaped by a clear competitive split, with incumbent EHR vendors embedding AI natively while specialist AI vendors expand from documentation into revenue cycle management and clinical decision support. Procurement remains active, but health systems are applying stricter governance review because breach exposure, shadow AI usage, and clinician review requirements can slow approvals and widen perceived implementation risk. At the same time, standardized API requirements and FHIR-based modernization are widening the opportunity set for the AI-based EHR systems market because they make enterprise data access more usable for new AI workflows across large provider networks.

Key Report Takeaways

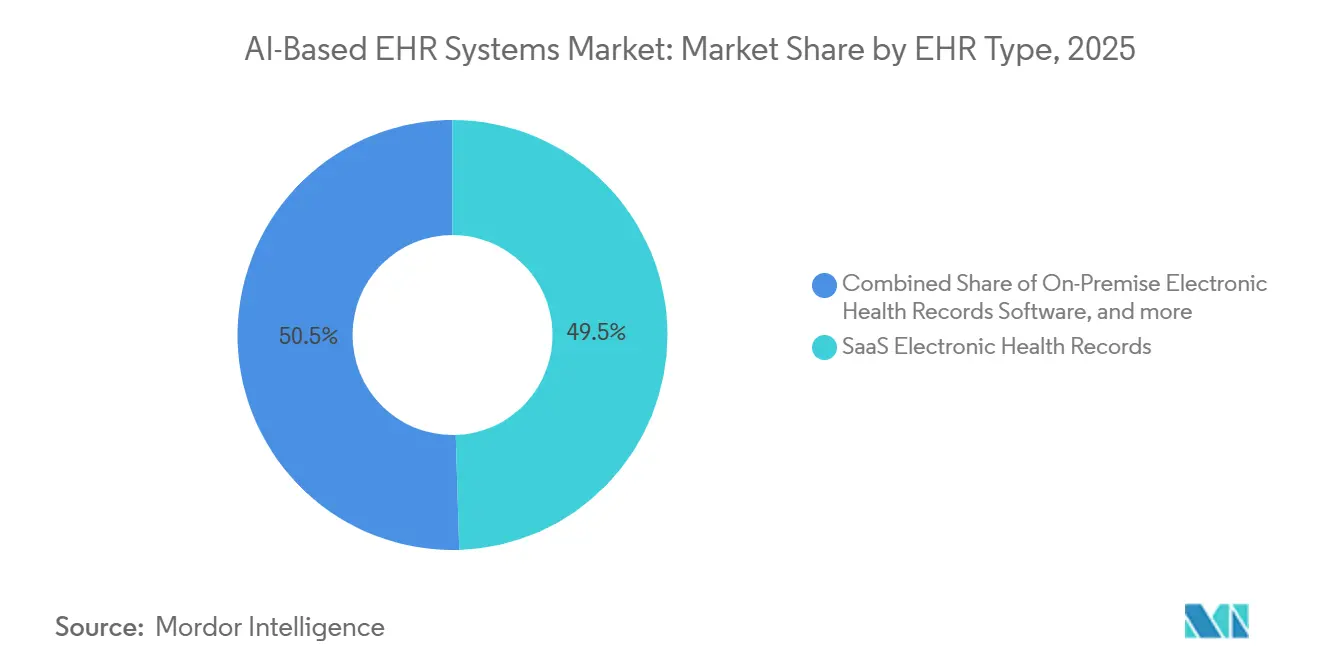

- By EHR type, SaaS electronic health records held 49.52% of the AI-based EHR systems market share in 2025, while custom-built electronic health records are projected to grow at 26.33% CAGR through 2031.

- By technology, machine learning accounted for 57.41% share of the AI-based EHR systems market size in 2025, while natural language processing is forecasted to expand at 25.87% CAGR through 2031.

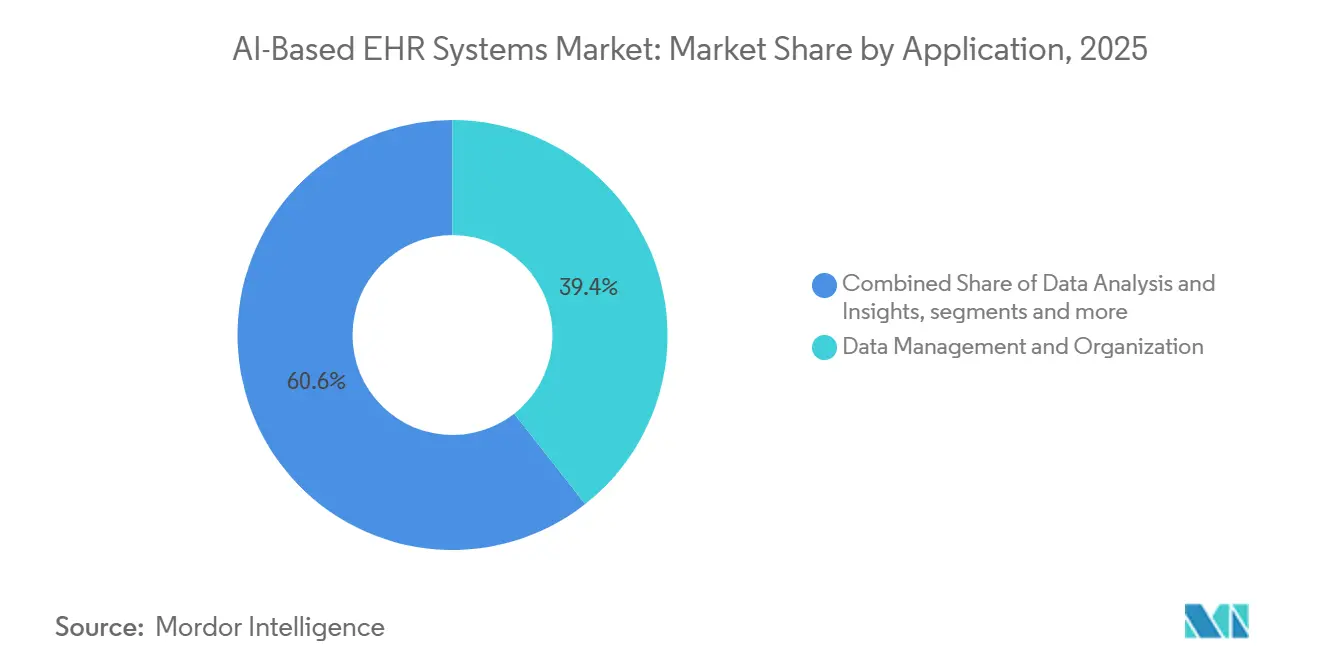

- By application, data management and organization represented 39.37% share of the AI-based EHR systems market size in 2025, while clinical decision support is projected to grow at 26.80% CAGR through 2031.

- By end-user, hospitals held 44.11% share in 2025, while clinics are forecasted to advance at 26.17% CAGR through 2031.

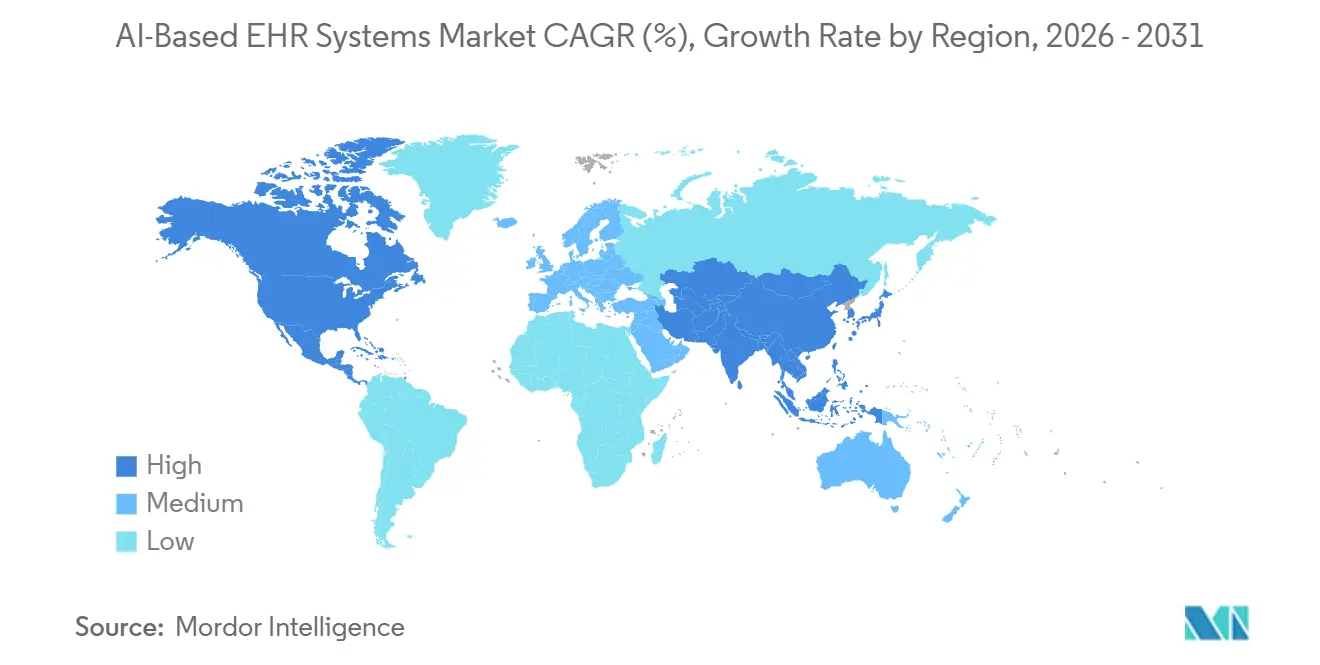

- By geography, North America held 46.48% share in 2025, while the Asia-Pacific is forecasted to grow at 27.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Based EHR Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Ambient Clinical Scribing | +5.2% | Global, with highest intensity in North America and Western Europe | Short term (≤ 2 years) |

| EHR-Native AI Integration in Core Workflows | +4.8% | Global, North America leads, APAC accelerating | Medium term (2-4 years) |

| Interoperability Mandates and FHIR Adoption | +3.6% | North America primary, EU and APAC spill-over | Medium term (2-4 years) |

| Value-Based Care and Revenue Integrity Pressure | +4.1% | North America and EU, emerging in APAC core markets | Medium term (2-4 years) |

| Multilingual Specialty Models for Under-Documented Settings | +2.9% | APAC, MEA, South America with spill-over to EU | Long term (≥ 4 years) |

| GPU-Efficient Enterprise AI Deployment Models | +3.2% | Global, with largest gains in cost-sensitive APAC and emerging markets | Short term (≤ 2 years), Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Ambient Clinical Scribing

Ambient clinical scribing has become the clearest short-cycle adoption path in the AI-based EHR systems market because it addresses a daily documentation burden that clinicians feel in nearly every patient encounter. Health systems have moved faster here because documentation pressure affects visit flow, physician capacity, staff burnout, and after-hours charting in ways that are immediate and measurable. At Intermountain Health, clinicians using Dragon Copilot saw a 27% reduction in time spent in notes per appointment across tracking from April 2024 through December 2025, and across five academic medical centers, AI scribe access cut total EHR time by 13.4 minutes per visit.[1]American Hospital Association, “6 Health Systems Enhancing Care Delivery with Ambient AI Scribes,” American Hospital Association, aha.org That matters because the AI-based EHR systems market is increasingly being judged on recovered clinician time and documentation quality, not only on software feature breadth. At the same time, payer interest in downcoding responses to richer AI-generated notes means some systems may see documentation quality improve faster than reimbursement yield, which changes the economic case for deployment at scale.[2]npj Digital Medicine, “Policy Brief, Ambient AI Scribes and the Coding Arms Race,” npj Digital Medicine, nature.com This keeps demand strong, but it also pushes buyers to justify ambient tools through productivity, compliance quality, and clinician experience rather than through revenue uplift alone.

EHR-Native AI Integration in Core Workflows

EHR vendors embedding AI directly inside their own platforms mark a deeper structural shift in the AI-based EHR systems market because workflow control is moving back toward the system of record. Epic put native AI Charting into live use in February 2026, and its Curiosity foundation models and Agent Factory platform show a clear effort to keep AI orchestration at the platform layer rather than leave it to external tools. Oracle has taken a similar direction by positioning AI-driven electronic health records as native workflow tools, not as add-on modules that sit outside the main record environment. As that pattern spreads, the AI-based EHR systems market gives third-party vendors less room to win on simple integration alone, because large platforms can bundle documentation, summarization, and workflow assistance into core contracts. This is pushing specialist AI firms toward areas such as revenue cycle intelligence, prior authorization, population health, and specialty-specific automation where EHR incumbency is weaker. The effect is not the disappearance of external AI vendors, but a shift in where margins can still be defended.

Interoperability Mandates and FHIR Adoption

Interoperability mandates are becoming a practical growth driver for the AI-based EHR systems market because AI workflows depend on consistent access to structured, query-ready patient data. ONC's HTI-5 Proposed Rule, published in December 2025, advances FHIR-based API requirements and strengthens the certification path around AI-enabled interoperability, which pushes both incumbent EHR vendors and newer entrants toward the same technical baseline.[3]Office of the National Coordinator for Health Information Technology, “HTI-5 Proposed Rule,” Office of the National Coordinator for Health Information Technology, healthit.gov Mandatory alignment with HL7 FHIR US Core Implementation Guide STU 6.1.0 by December 2025 and the release of USCDI v6 in July 2025 have forced developers to rebuild or re-expose data layers through standardized APIs. That work does more than improve data exchange, because it also makes the AI-based EHR systems market more usable for inference pipelines that need access to longitudinal clinical records at scale. A less visible effect is that standardization reduces the protective value of proprietary data architectures that long slowed third-party development. As a result, compliance investment is also intensifying competition because it narrows the integration moat that legacy platforms once relied on.

Value-Based Care and Revenue Integrity Pressure

Revenue integrity has become a central buying argument for the AI-based EHR systems market because documentation gaps directly affect risk capture, denials, and reimbursement under value-based contracts. Health systems operating under value-based arrangements increasingly want AI to identify missing documentation in real time and align records more closely with compliant coding logic. Platforms that support documentation aligned with CMS-HCC Version 28 are gaining attention because the financial impact of incomplete records is now easier for providers to quantify. Waystar stated in March 2026 that its AltitudeAI platform prevented more than USD 15 billion in denied claims in less than a year and reduced time spent on denial appeal and recovery by 90%. That kind of outcome matters for the AI-based EHR systems market because it connects clinical documentation directly with reimbursement performance and operating cash flow. It also supports the rise of a broader product category in which documentation tools, coding support, denial prevention, and workflow intelligence increasingly operate as one commercial package.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patient Consent Limits for Ambient Audio Capture | -1.4% | North America and EU, regulatory fragmentation across U.S. states and GDPR jurisdictions | Short term (≤ 2 years), Medium term (2-4 years) |

| Clinical Liability and Human Review Requirements | -1.8% | Global, most acute in North America, Australia, and EU where AI device rules apply | Medium term (2-4 years) |

| Cybersecurity and Centralized Data Exposure | -2.1% | Global, disproportionate risk in cloud-consolidating markets such as North America and core APAC | Short term (≤ 2 years) |

| Token, Inference, and Latency Economics at Scale | -1.6% | Global, highest constraint in cost-sensitive mid-market and emerging geographies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patient Consent Limits for Ambient Audio Capture

Consent limits remain a structural brake on the AI-based EHR systems market because ambient capture involves live audio from clinical encounters, not simply retrospective text processing. Several U.S. states apply two-party consent rules under wiretapping laws, which creates uneven deployment conditions for health systems operating across multiple jurisdictions. The issue is harder in practice than in policy documents because workflows must explain consent clearly, capture it consistently, and ensure that the record shows how audio-derived text entered the chart. An NHS England pilot conducted from May through September 2025 found that when an ambient scribe was not integrated directly into the EHR, clinicians resorted to copying and pasting AI-generated notes, which introduced both safety concerns and traceability gaps. That finding matters for the AI-based EHR systems market because it shows that disconnected workarounds do not remove the consent problem, they simply move it into less visible parts of the workflow. Vendors that cannot offer native, auditable integration will therefore face slower adoption in organizations with stricter legal review.

Clinical Liability and Human Review Requirements

Clinical liability rules are slowing full automation in the AI-based EHR systems market because regulators still require meaningful clinician oversight for outputs that affect diagnosis or treatment. The FDA's January 2026 Clinical Decision Support Software guidance keeps a clear line between reviewable, transparent support tools and device-class functions that generate specific diagnostic outputs without adequate clinician review. That distinction matters commercially because auto-signing AI-generated notes remains outside what most providers and regulators will currently accept. If vendors push automation too far, they risk moving into a device pathway that requires a fuller FDA marketing submission process, which adds time, cost, and uncertainty. As a result, the AI-based EHR systems market still depends on reviewable draft workflows rather than fully authoritative AI records. This design reality caps the throughput gains vendors can credibly promise and shifts product investment toward review interfaces, workflow controls, and explainability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By EHR Type: Cloud Flexibility Dominates but Custom Workflows Accelerate

SaaS electronic health records held 49.52% of the AI-based EHR systems market share in 2025, reflecting the continuation of multi-year migration away from on-premise infrastructure. In the AI-based EHR systems market, SaaS stands out because continuous model updates, fast rollout of ambient scribing improvements, and vendor-managed cloud inference reduce local hardware dependence. SaaS also gives provider networks a more practical path to deploy improvements across hospitals, outpatient sites, and multi-specialty clinics without separate hardware cycles for each location. These advantages have made cloud delivery the default choice for buyers that value scale, update speed, and centralized governance.

Custom-built electronic health records are projected to grow at 26.33% CAGR through 2031, showing that some health systems still prefer to build tailored AI layers on top of FHIR-ready data environments. That pattern suggests the AI-based EHR industry is not moving toward a single packaged architecture, because large enterprises with internal engineering resources want tighter control over workflow logic, specialty requirements, and internal orchestration. In effect, the line between packaged SaaS and custom development is becoming less rigid as platforms expose more controlled customization layers. On-premise deployments still persist in large academic medical centers and federal environments with sovereign data requirements, but their AI capabilities remain more constrained by inference latency, self-hosting burdens, and slower model update cycles.

By Technology: ML Infrastructure Anchors the Market While NLP Reshapes the Frontline

Machine learning retained 57.41% share in 2025, which shows how deeply predictive models are already embedded across deterioration alerts, risk stratification, revenue cycle automation, and patient flow management. Much of this installed base predates the current generative AI cycle, which is why the AI-based EHR systems market still leans heavily on established machine learning infrastructure even as newer tools receive more attention. Providers continue to rely on these models because they support operational decisions that are measurable, recurrent, and closely tied to quality and financial performance. The installed machine learning layer also gives vendors a base from which newer AI tools can be attached more easily inside existing EHR workflows. This helps explain why mature predictive capabilities still anchor the technology mix even while other modalities expand more quickly.

Natural language processing is forecasted to grow at 25.87% CAGR through 2031, making it the fastest-moving technology layer in the AI-based EHR systems market. Its growth is tied less to general chatbot adoption and more to ambient documentation, ICD coding automation, and clinical documentation integrity workflows that sit close to daily clinical operations. Deep learning is also gaining traction where models need to process narrative notes, lab values, and imaging-related information together, although deployment moves more slowly when regulatory requirements become more demanding.

By Application: Data Foundations Hold the Largest Base but Decision Support Scales Faster

Data management and organization represented 39.37% share of the AI-based EHR systems market size in 2025, which reflects the fact that most enterprise AI value still begins with data cleanup, harmonization, and structuring. The AI-based EHR systems market still depends on turning years of unstructured notes, lab histories, and imaging reports into FHIR-compliant and query-ready records before higher-value inference can be trusted. This foundational work remains essential because weak data architecture quickly limits model usefulness, governance quality, and clinician confidence. The result is that data management stays large not because it is the most visible use case, but because it underpins almost every other AI workflow inside the record.

Clinical decision support is projected to grow at 26.80% CAGR through 2031, making it the fastest-growing application area in the AI-based EHR systems market. That growth is being supported by real-time access to patient records, better model reasoning over longitudinal data, and payer pressure for more evidence-based care pathways. Predictive analytics sits in the middle of this transition because health systems are using deterioration models and readmission predictors not only for care management, but also for contract performance under value-based care. Data analysis and insights also remain important because executives still need platforms that convert patient-level information into usable financial and quality signals. Over time, this means the application mix is moving from passive organization toward active clinical and operational decision support without losing the foundational importance of data readiness.

By End-User: Hospital Scale Supports Revenue While Clinics Set the Pace

Hospitals held 44.11% of end-user share in 2025, reflecting both their budget capacity for enterprise contracts and the scale efficiency of deploying AI across inpatient and outpatient settings at the same time. In the AI-based EHR systems market, hospitals also gain from having broader informatics teams, stronger governance structures, and more direct links between documentation quality and revenue performance. Hospitals are therefore likely to remain the largest revenue pool even as other care settings adopt faster in percentage terms. This scale advantage helps sustain vendor focus on complex enterprise features, large workflow footprints, and platform-level contracts.

Clinics are projected to expand at 26.17% CAGR through 2031, which makes them the fastest-growing end-user group in the AI-based EHR systems market. The reason is operational rather than symbolic, because ambulatory practices face heavy documentation burden with fewer administrative staff to absorb it. Ambulatory surgical centers and diagnostic centers are also increasing adoption through targeted modules such as procedure note automation and structured radiology report generation, which are easier to implement than full enterprise rollouts. Other end-users, including long-term care and behavioral health facilities, remain important because vendors such as Netsmart Technologies and PointClickCare are developing care-setting-specific documentation workflows for historically under-digitized parts of the care continuum.

Geography Analysis

North America held 46.48% share of the AI-based EHR systems market size in 2025, supported by the region's dense Epic and Oracle Health installed base and by reimbursement structures that reward detailed documentation. In the AI-based EHR systems market, that reimbursement logic makes documentation integrity a financial priority for leadership teams, not only an IT issue. The United States remains the core demand center because value-based contracts make better risk capture and cleaner records commercially meaningful across provider organizations. ONC's HTI-5 proposal and the compliance buildout around prior authorization APIs are also accelerating FHIR readiness across the broader North American provider and payer ecosystem.

Asia-Pacific is forecasted to grow at 27.66% CAGR through 2031, which makes it the fastest-rising regional pool in the AI-based EHR systems market. Growth is being driven by government-led digital health programs in India and by the acceleration of AI integration mandates across Japan, South Korea, and Australia. The region also has large patient volumes and many under-documented care settings, which increases the value of multilingual documentation tools and specialty models. Cost discipline matters more here than in North America, so deployment models that reduce compute intensity and shorten implementation cycles are likely to gain faster traction. This means Asia-Pacific is not only a demand story for new software, but also a proving ground for scalable and lower-cost enterprise AI operations.

Europe held a meaningful share in 2025, and the AI-based EHR systems market there is supported by NHS digital transformation programs and Germany's hospital digitization fund even though GDPR complexity and fragmented national standards slow implementation. The EU AI Act, combined with MDR and IVDR obligations, adds a longer compliance path for new entrants and gives established vendors with regulatory processes more protection. In the Middle East and Africa and in South America, sovereign healthcare investment and ongoing digitization create longer-cycle opportunities for vendors that can support Arabic- and Portuguese-language clinical workflows. These regions remain smaller today, but they are strategically important because future growth will depend on how well vendors adapt models, interfaces, and governance to under-resourced settings.

Competitive Landscape

The AI-based EHR systems market is moderately concentrated at the platform layer, but it remains fragmented at the AI capability layer because more than 200 ambient AI vendors have entered since 2023. Epic Systems, Oracle Health, MEDITECH, and athenahealth are trying to keep workflow control inside their own environments, while Abridge AI, Suki AI, and Microsoft Dragon Copilot are expanding outward from documentation into adjacent clinical and financial workflows. This split defines the main competitive pattern in the AI-based EHR systems market because control over workflow is becoming as important as control over the record itself. Buyers are therefore comparing not only note quality and model performance, but also integration depth, governance controls, and the ability to support revenue cycle and decision support use cases. The result is a market where platform access, orchestration rights, and implementation speed increasingly shape vendor leverage.

Oracle had already signaled a similar strategy with AI-driven electronic health record capabilities designed to bring generative functions directly into core clinical workflows. Microsoft is pursuing scale through Dragon Copilot and through partnerships that extend into ambulatory care, which gives it a route into both large systems and distributed practice settings. In the AI-based EHR systems market, these moves show that major vendors are not treating AI as a stand-alone feature, but as a way to defend platform ownership and data gravity. They also raise the competitive bar for smaller AI companies that depend on open integration points to sustain premium pricing.

Pure-play vendors are responding by moving toward specialty-specific models, multilingual capabilities, and revenue cycle intelligence, where incumbents are less entrenched. Abridge's move into clinical decision support content and structured nursing flowsheets shows how ambient vendors are trying to expand into broader workflow ownership. AWS and Google Cloud are also deepening the infrastructure layer through HealthLake, Healthcare API connectivity, and revenue cycle partnerships, which means hyperscaler influence will continue to grow beneath the AI-based EHR systems market. White space remains strongest in post-acute care, long-term care, small practice automation, and multilingual deployments across South Asia and Sub-Saharan Africa, where product fit is still uneven.

AI-Based EHR Systems Industry Leaders

Epic Systems Corporation

Oracle

MEDITECH

athenahealth, Inc.

eClinicalWorks

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Abridge was ranked No. 30 on CNBC's Disruptor 50 list with a USD 5.3 billion valuation and USD 830 million in total funding, having expanded to 250 enterprise health systems including Johns Hopkins and Kaiser Permanente. The company is integrating clinical decision support via NEJM and JAMA content deals, moving firmly beyond ambient scribing into medical AI search and coding automation, signaling a platform consolidation play.

- May 2026: AWS HealthLake launched native support for the CMS Interoperability and Prior Authorization Final Rule (CMS-0057-F), providing FHIR-based API infrastructure for Medicare Advantage and Medicaid plans ahead of the January 1, 2027 compliance deadline. This positions AWS as a foundational compliance layer for AI EHR data infrastructure across the U.S. payer-provider ecosystem AWS.

- February 2026: Mount Sinai Health System selected Microsoft Dragon Copilot over Abridge and Suki AI following comparative pilots, citing EHR integration depth and enterprise compatibility as the key differentiators. This selection by a major academic medical center reinforces enterprise-grade integration as the decisive procurement criterion in the ambient AI space.

- February 2026: Epic launched AI Charting natively within its Art AI scribe, with Art's Insights patient chart summary feature recording a 3x usage increase from November 2025. Epic also confirmed Penny (revenue cycle AI) and Emmie (patient AI) as the full suite of EHR-native AI assistants, cementing its strategy of vertically integrating ambient documentation, revenue cycle, and patient engagement.

Global AI-Based EHR Systems Market Report Scope

According to the report’s scope, the AI‑based EHR systems market refers to electronic health record platforms enhanced with AI‑driven automation, predictive analytics, and intelligent clinical workflows to improve documentation accuracy, decision support, interoperability, and operational efficiency, reducing clinician burden and enabling more proactive, data‑driven care delivery.

The AI‑based EHR systems market is segmented into EHR type, technology, application, end-user, and geography. By EHR type, the market is segmented into on-premise electronic health records software, SaaS electronic health records, and custom-built electronic health records. By technology, the market is segmented into machine learning, deep learning, and natural language processing. By application, the market is segmented into data management and organization, data analysis and insights, predictive analytics, virtual medical assistance, clinical decision support, and clinical documentation integrity and coding support. By end-user, the market is segmented into hospitals, clinics, ambulatory surgical centers, diagnostic centers, and other end-users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| On-Premise Electronic Health Records Software |

| SaaS Electronic Health Records |

| Custom-Built Electronic Health Records |

| Machine Learning |

| Deep Learning |

| Natural Language Processing |

| Data Management and Organization |

| Data Analysis and Insights |

| Predictive Analytics |

| Virtual Medical Assistance |

| Clinical Decision Support |

| Clinical Documentation Integrity and Coding Support |

| Hospitals |

| Clinics |

| Ambulatory Surgical Centers |

| Diagnostic Centers |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By EHR Type | On-Premise Electronic Health Records Software | |

| SaaS Electronic Health Records | ||

| Custom-Built Electronic Health Records | ||

| By Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| By Application | Data Management and Organization | |

| Data Analysis and Insights | ||

| Predictive Analytics | ||

| Virtual Medical Assistance | ||

| Clinical Decision Support | ||

| Clinical Documentation Integrity and Coding Support | ||

| By End-User | Hospitals | |

| Clinics | ||

| Ambulatory Surgical Centers | ||

| Diagnostic Centers | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the AI-based EHR systems space in 2026 and where is it headed by 2031?

The AI-based EHR systems market stood at USD 8.18 billion in 2025 and reached USD 10.15 billion in 2026, it is forecasted to reach USD 31.87 billion by 2031, growing at a 25.71% CAGR over 2026-2031.

Which EHR type is leading adoption today?

SaaS electronic health records lead with 49.52% share in 2025 because they support centralized updates, vendor-managed inference, and faster rollout of new AI functionality.

Which technology area is growing fastest inside AI-enabled records platforms?

Natural language processing is expected to be the fastest-growing technology area at 25.87% CAGR through 2031, supported by ambient scribing, coding automation, and documentation integrity workflows.

Which region offers the strongest near-term revenue base and which region offers the fastest expansion?

North America remains the largest regional base with 46.48% share in 2025, while Asia-Pacific is projected to be the fastest-growing region with a 27.66% CAGR through 2031.

Page last updated on: