Clinical EHR Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.34 Billion |

| Market Size (2031) | USD 30.33 Billion |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

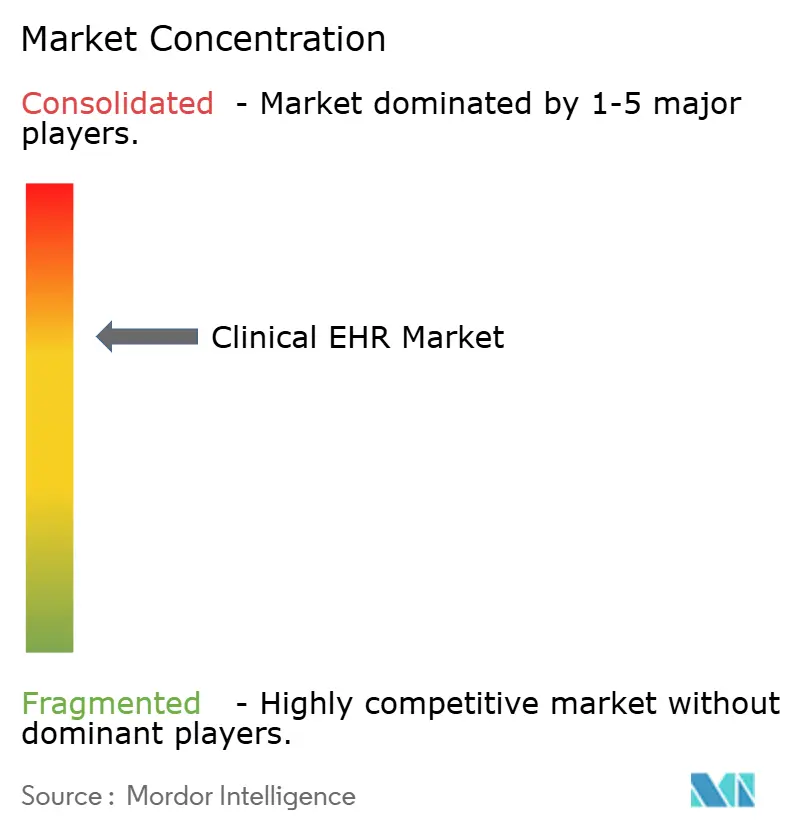

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical EHR Market Analysis by Mordor Intelligence

The clinical EHR market size is expected to grow from USD 22.15 billion in 2025 to USD 23.34 billion in 2026 and is forecast to reach USD 30.33 billion by 2031 at 5.38% CAGR over 2026-2031. Accelerated digitization of healthcare, stringent regulatory incentives, and the shift toward value-based reimbursement are the primary forces widening adoption. Hospitals and ambulatory networks are replacing siloed platforms with unified records to improve care coordination, while artificial intelligence tools embedded within modern solutions shorten clinical documentation time and reduce burnout. Cloud deployment now underpins most new projects because it lowers capital expenditure and provides instant scalability. Interoperability mandates such as TEFCA ensure that vendors align products with national exchange standards, prompting health systems to revisit procurement priorities toward platforms with proven data-sharing credentials.

Key Report Takeaways

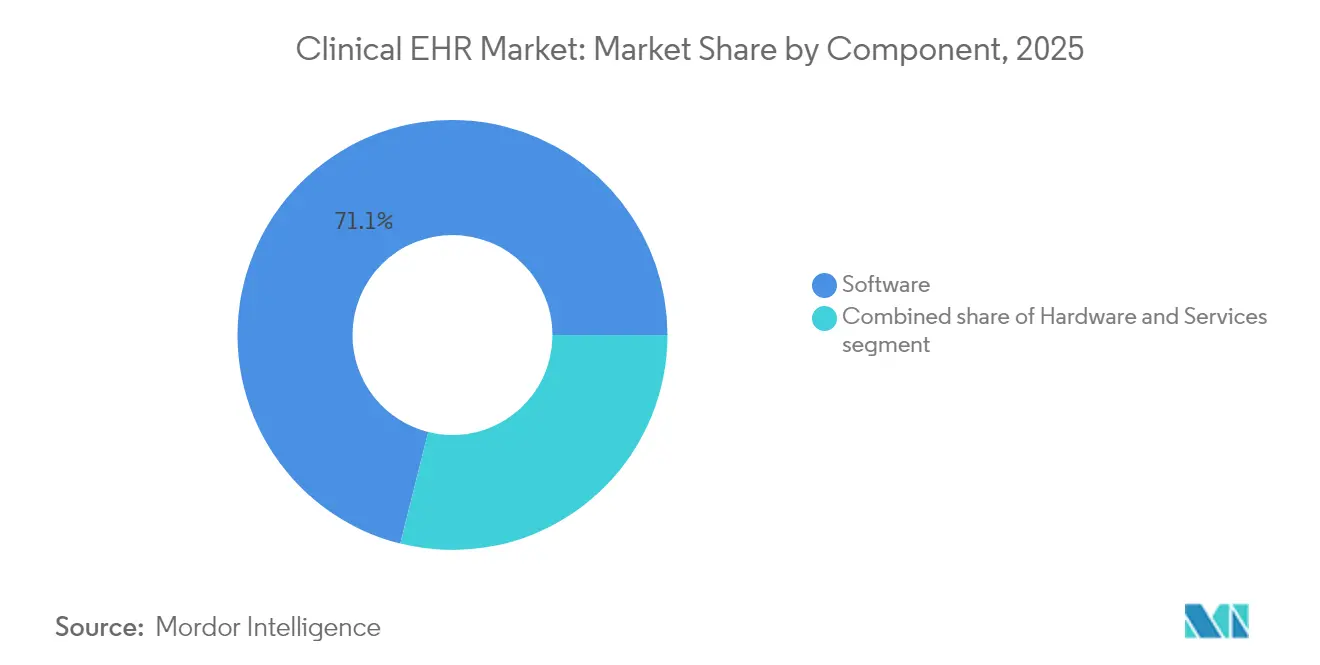

- By component, Software led with 71.10% of the clinical EHR market size in 2025, whereas Services is projected to post the fastest 6.02% CAGR through 2031.

- By delivery mode, Cloud-based solutions captured 70.05% of the clinical EHR market share in 2025 and are slated to expand at a 6.42% CAGR to 2031.

- By end-user, Hospitals accounted for 52.30% share of the clinical EHR market size in 2025, while Clinics and Ambulatory Centers are forecast to grow at 5.86% CAGR through 2031.

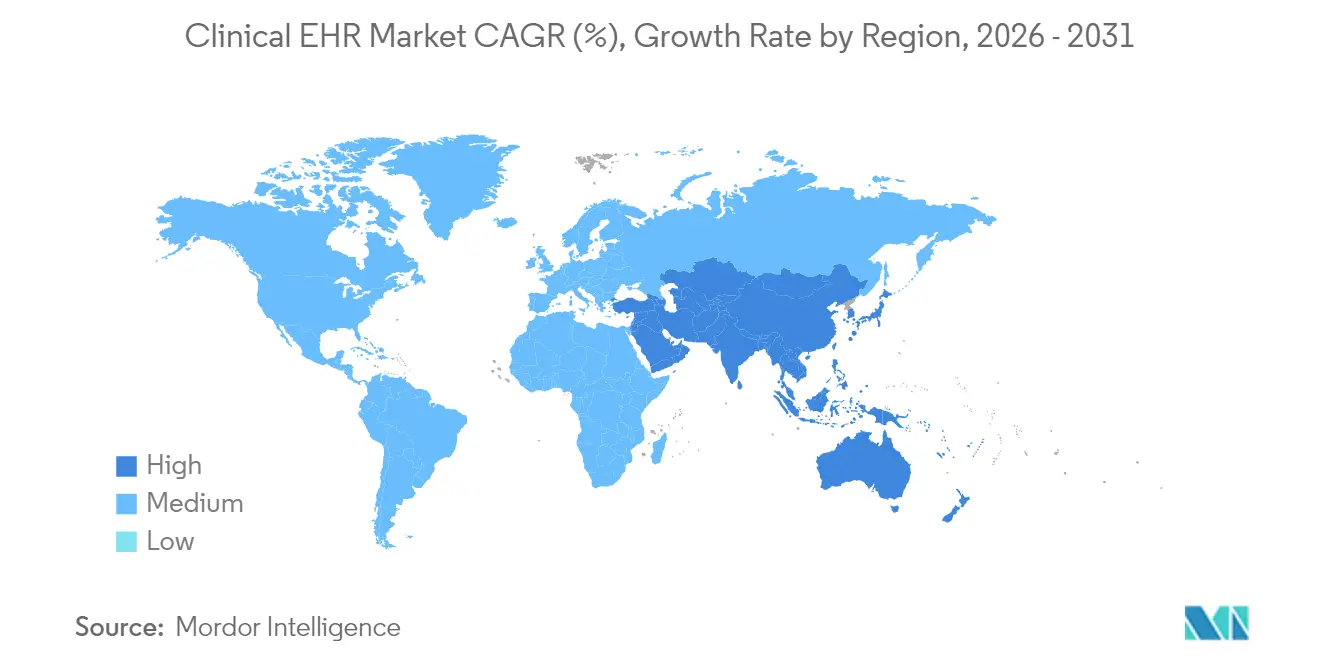

- By geography, North America commanded 39.10% share of the clinical EHR market size in 2025; Asia-Pacific is on track to be the fastest-growing region at a 6.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Clinical EHR Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Incentives for Nationwide EHR Adoption | +1.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Demand for Integrated Care Coordination Across Settings | +1.0% | Global, acute in fragmented systems | Long term (≥ 4 years) |

| Growing Tele-Health & Remote Monitoring Volume | +0.8% | Global, rapid in APAC and rural markets | Short term (≤ 2 years) |

| Shift to Value-Based Reimbursement | +0.6% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| Rise of AI-Assisted Voice Documentation | +0.4% | North America and Europe leading, expanding to APAC | Medium term (2-4 years) |

| Cyber-Security Insurance Rebates | +0.3% | North America and EU, emerging in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government incentives drive nationwide EHR adoption

Financial rewards[1]Centers for Medicare & Medicaid Services, “Calendar Year 2024 Program Requirements,” cms.gov embedded in updated Medicare Promoting Interoperability rules and Medicaid programs keep capital flowing toward certified records. Hospitals can receive as much as USD 63,750 per provider by exhibiting meaningful use, and penalties now target organizations that block information sharing. The 21st Century Cures Act further ties reimbursement to interoperability[2]Office of the Federal Register, “21st Century Cures Act—Establishment of Disincentives for Health Care Providers,” federalregister.gov , creating durable demand for platforms that satisfy data-exchange benchmarks.

Integrated care coordination demands drive system convergence

Fragmented records impede clinicians from accessing longitudinal patient histories. TEFCA, effective January 2025, compels vendors to support national exchange specifications[3]Office of the Federal Register, “Health Data, Technology, and Interoperability; Trusted Exchange Framework and Common Agreement,” federalregister.gov , steering procurement toward enterprise-wide solutions that eliminate data silos.

Telehealth integration accelerates remote care capabilities

Health systems embed virtual-care modules within core records so that vital signs captured at home feed directly into the chart, preserving workflow continuity and comprehensive documentation. Healthcare organizations report that integrated telehealth-EHR platforms improve provider productivity by maintaining familiar workflows while expanding service delivery capabilities beyond traditional facility boundaries.

AI-assisted voice documentation reduces clinical burden

Artificial intelligence (AI) integration within EHR systems addresses the persistent challenge of clinical documentation burden that contributes to physician burnout. Ambient scribes convert conversations into structured notes[4]Craig Lee, “Evaluating the Impact of Artificial Intelligence (AI) on Clinical Documentation Efficiency and Accuracy Across Clinical Settings: A Scoping Review,” Cureus, pmc.ncbi.nlm.nih.gov , cutting typing time by up to 90% and allowing physicians to focus on patient interaction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data privacy and interoperability concerns | -0.7% | Global, heightened in Europe and North America | Long term (≥ 4 years) |

| Shortage of trained health-IT workforce | -0.5% | Global, acute in emerging markets and rural areas | Medium term (2-4 years) |

| Rising cost of cloud egress fees | -0.4% | Global, highest in large health systems | Medium term (2-4 years) |

| Vendor lock-in slowing modular migration | -0.3% | Global, affects mid-size providers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data privacy and interoperability concerns constrain adoption

New HIPAA security revisions propose mandatory encryption and multi-factor authentication, escalating compliance complexity. The cumulative exposure from 136 million breached records in 2023 reinforces cautious budgeting for fresh deployments.

Health-IT workforce shortage limits implementation capacity

ONC training initiatives have enlarged the pool of certified specialists, yet unfilled roles remain across privacy, analytics, and integration. Smaller hospitals delay go-lives until they secure talent capable of sustaining system performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software leadership drives innovation

Software held 71.10% of the clinical EHR market share in 2025, reflecting provider preference for functionality over hardware. Services, though smaller, are advancing at 6.02% CAGR thanks to rising demand for implementation, optimization, and data migration engagements. The clinical EHR market benefits from AI-driven documentation, analytics, and predictive modules that layer onto core software. Vendors now embed natural-language interfaces so physicians speak, the system transcribes, and discrete fields update in real time.

Services expansion indicates recognition that change management often determines return on investment. Managed-service contracts cover interoperability upgrades, cybersecurity hardening, and regulatory reporting cycles. Hardware now accounts for a modest slice as cloud models offload server procurement.

By Delivery Mode: Cloud migration accelerates

Cloud deployments commanded 70.05% of the clinical EHR market size in 2025 and are projected to grow fastest at 6.42% annually. Providers cite elastic scaling, rapid feature releases, and embedded disaster-recovery safeguards. Some institutions retain on-premise environments for sensitive imaging archives, yet most new projects default to multi-tenant architecture.

Hybrid approaches serve multi-facility networks that must integrate legacy radiology or laboratory applications before full migration. Pay-as-you-go pricing redirects capital budgets to operating expenses, aligning with financial strategies focused on predictable cash-flow. Regulatory bodies now accept certified cloud hosting when encryption, audit trails, and regional data-residency rules are proven, further easing transition hurdles.

By End-User: Ambulatory care gains momentum

Hospitals represented 52.30% of the clinical EHR market share in 2025 because inpatient workflows remain complex and heavily regulated. However, Clinics and Ambulatory Centers are the fastest-growing user group at 5.86% CAGR, mirroring payer incentives that reward preventive and chronic-disease management outside the acute setting.

Ambulatory groups seek lightweight yet interoperable records that integrate scheduling, telehealth, and e-prescribing within one interface. Vendor roadmaps now prioritize outpatient templates and consumer portals to secure footholds before multi-practice networks standardize on enterprise platforms. Long-term care and specialty practices also accelerate adoption, encouraged by reimbursement models that punish information-blocking and reward coordinated transitions.

Geography Analysis

North America retained leadership with 39.10% share of the clinical EHR market size in 2025, underpinned by mature health IT policy, broad broadband coverage, and well-capitalized hospital chains. CMS incentive structures continue to fund upgrades, while private insurers increasingly require electronic records for network participation.

Europe experiences steady but slower migration as General Data Protection Regulation compliance introduces additional validation steps. National health services in the United Kingdom, Germany, and France invest in cloud migration programs that promise unified care records across regional trusts. Procurement cycles often synchronize with multi-year funding windows, creating periodic spikes in contract awards.

Asia-Pacific registers the fastest 6.31% CAGR through 2031. Large-scale public projects in India, China, and Southeast Asian nations combine infrastructure grants with mandatory reporting frameworks. Governments offer tax credits for cloud use and sponsor workforce-training programs to accelerate adoption. The Middle East and Africa follow similar trajectories; Gulf Cooperation Council members connect public hospitals via centralized exchanges, while African nations leverage donor financing for open-source rollouts.

Value Chain Analysis

The clinical EHR value chain begins with standards and compliance, supported by core technology inputs such as interoperability specifications (including TEFCA-aligned exchange requirements), clinical terminologies, cybersecurity controls, and cloud infrastructure from hyperscalers. EHR software vendors then build and certify core clinical workflows, including documentation, orders, results review, and revenue-cycle linkages, while increasingly embedding AI documentation and coding assistance through partnerships. Recent examples include athenahealth partnering with Abridge (February 2025) for ambient documentation in athenaOne and athenahealth collaborating with Microsoft to offer Dragon Copilot as an Ambient Notes option for ambulatory clinicians (announced December 2025 for release in 1H 2026), showing how model, voice, and cloud ecosystems now influence EHR feature roadmaps.

Implementation and optimization services, such as systems integration, data migration, training, and managed services, sit next in the chain. Health systems and consulting partners configure workflows, connect third-party modules, and manage ongoing regulatory reporting. Distribution and commercialization are handled through direct enterprise sales to hospitals and health systems, channel partners serving ambulatory practices, and marketplace-based integrations for third-party applications. Downstream, providers, payers, labs, imaging networks, and HIE/QHIN participants consume EHR data via APIs and exchange frameworks, with data harmonization and secure connectivity becoming central to adoption. InterSystems integrating HealthShare with Google Cloud Healthcare API (October 2025) highlights how these integration layers are being positioned to support AI-ready data pipelines and interoperability at scale.

Competitive Landscape

The clinical EHR market remains concentrated. Epic Systems expanded to cover a significant share of US hospitals by 2024, a testament to tight customer partnerships and broad application suites. Oracle Health, despite AI-centric enhancements, ceded sites due in part to implementation complexity. Regional leaders in Europe and APAC defend their share through localization and pre-built language packs.

Large platforms differentiate through full-stack interoperability, containing laboratory, imaging, and revenue-cycle functions. Smaller challengers focus on niche segments such as behavioral health or pediatrics, where tailored templates give workflow advantages. Artificial intelligence accelerators—ambient scribes, sepsis prediction, and automated coding—act as table stakes. Vendors unable to integrate these features risk exclusion from shortlists shaped by clinician satisfaction surveys and cyber-insurer checklists.

Strategic maneuvers include joint ventures with hyperscale cloud providers for embedded analytics and marketplaces that let third-party developers extend core functionality. Mergers seek scale economies in R&D and support, while private-equity investment supplies growth funds to mid-tier players aiming to enter new geographies.

Clinical EHR Industry Leaders

Epic Systems Corporation

Medical Information Technology, Inc. (Meditech)

Oracle Corporation

TruBridge, Inc.

Veradigm Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Interoperability compliance is creating near-term whitespace for EHR vendors and service partners that can operationalize standards-based exchange and API measurement, rather than focusing only on basic connectivity. CMS began requiring impacted payers to start annual reporting of Patient Access API usage metrics, with the first report covering calendar year 2025 due by March 31, 2026. This reporting timeline increases demand for EHR capabilities that generate clean, auditable API and data-access telemetry across patient portals, mobile apps, and connected third parties. At the same time, ONC SVAP continues to support a faster pathway for developers to adopt newer standards, with USCDI v5 included in the 2025 SVAP approved standards list. This supports services-led opportunities in upgrades, testing, and change management as organizations align interfaces, mapping, and governance.

TEFCA expansion and technical evolution also support opportunity in Facilitated FHIR enablement and enterprise integration. In February 2026, ASTP/ONC TEFCA updates cited the designation of three new QHINs in 2025, and the framework includes Participant/Subparticipant Terms of Participation alongside the Facilitated FHIR Implementation SOP. That structure pushes providers to prioritize EHR platforms and integration partners that can meet exchange specifications and production-grade onboarding requirements. ONC’s standards cadence adds a recurring roadmap anchor, including a targeted July 2026 release date for final USCDI v7, which can drive ongoing demand for interoperability releases, data-quality programs, and governance tooling to limit disruption during annual standard updates while supporting cross-setting care coordination and analytics.

Recent Industry Developments

- June 2026: Epic Systems detailed the first module within its EpicOps ERP suite, introducing Teamwork for staff scheduling. The expansion moves Epic beyond clinical documentation into operational workflows adjacent to the EHR, tightening platform stickiness and shifting competitive dynamics with standalone healthcare ERP and workforce management vendors.

- May 2026: MEDITECH announced a strategic collaboration with Rubrik to strengthen cyber resilience and data protection for MEDITECH Expanse. The partnership reflects buyer and insurer scrutiny of security posture and places security controls closer to the core EHR platform rather than treating them as a standalone add-on.

- October 2025: InterSystems integrated HealthShare with Google Cloud Healthcare API to support AI-ready data pipelines and interoperability at scale. This update highlights cloud-based data harmonization and upcoming AI-assisted workflows as more central elements of interoperability strategies, aligning with HIE and QHIN integration ambitions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues earned from clinical electronic health record (EHR) solutions used to capture, store, and share patient clinical information across care settings, including related software, services, and enabling hardware sold for clinical use.

Scope exclusions: It does not count non-clinical health apps for general wellness, or standalone billing and claims tools when they are sold without a clinical record system.

Segmentation Overview

- By Component

- Hardware

- Software

- Services

- By Delivery Mode

- Cloud-based Solutions

- On-premise Solutions

- Hybrid Solutions

- By End-User

- Hospitals

- Clinics & Ambulatory Centers

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public signals that indicate provider adoption and spend direction for clinical record systems, since those signals help keep assumptions tied to how budgets are actually moving. We reviewed sources such as the Office of the National Coordinator for Health IT (ONC) datasets, CMS program updates, OECD health statistics, and World Bank healthcare indicators, then cross-checked them with peer-reviewed health informatics journals.

To translate demand-side signals into a market model, we also used company annual reports, earnings call transcripts, product brochures, and credible press coverage to map typical pricing approaches and roll-out patterns. For validation support, we selectively used paid subscriptions focused on company financials and intelligence, news and financials, and patent databases to spot product cadence and investment timing. The sources listed here are illustrative and not exhaustive, and other public materials were also referenced to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary discussions were used to test what desk research could not fully answer, especially how buying decisions are made for EHR replacements, upgrades, and cloud migrations. We spoke with a mix of solution providers, implementation partners, and hospital and clinic stakeholders across APAC, EMEA, and the Americas, and then the feedback was used to confirm assumptions on deployment mix, typical contract scope, and service attach rates.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 22% | APAC: 45% |

| Mid tier: 48% | Functional/Unit leaders: 24% | EMEA: 35% |

| Smaller Players: 22% | Managers: 54% | Americas: 20% |

Market-Sizing & Forecasting

Sizing was built using both top-down and bottom-up logic, with the top-down side used first to reconstruct the demand pool by region through healthcare digitization indicators and enterprise software spending patterns in provider settings. Once the demand pool was set, it was split using inputs such as cloud adoption rates for clinical IT, hospital and clinic EHR penetration and replacement cycles, implementation intensity by facility size, and typical annual maintenance and support shares.

Then, to keep the totals believable, selective bottom-up checks were run using sampled price ranges and volume proxies from interviews, along with roll-ups for a limited set of visible supplier revenues where reporting allowed clean attribution to clinical EHR. When data was missing for smaller countries or fragmented care settings, gaps were handled by applying validated ratios from similar markets, and those ratios were re-tested with experts before locking the final numbers.

For forecasting, we relied mainly on scenario analysis, since policy timelines, interoperability mandates, and cloud migration pace can shift adoption curves faster than a single trendline would show. Scenarios were anchored to variables like provider IT budget growth, pace of legacy system replacement, share of cloud-based deployments, service intensity per installation, and average contract value progression in constant currency, and then adjusted based on what interviewees expected to change over the next few years.

Data Validation & Update Cycle

Outputs were checked through triangulation across demand indicators, supply-side revenue signals, and the primary feedback, and then unusual jumps were flagged for a second review. If a region total drifted too far from adoption metrics or procurement signals, the assumptions were reopened, and clarifying calls were triggered to resolve the variance.

Before sign-off, the model is reviewed in multiple steps, including unit checks, currency conversion timing checks, and consistency checks across historical and forecast years. Reports are refreshed annually, and interim updates are made when material events occur, such as major policy changes or meaningful shifts in deployment preferences. Right before delivery, we do a fresh pass so clients receive the most current view available.

Mordor Intelligence's Clinical Ehr Market Size Measured Against Other Published Estimates

Published market sizes for clinical EHR often do not match, even when the labels sound similar, because each study draws the line differently on what is included and how the year is measured. The gaps usually come from scope choices, service and hardware treatment, currency timing, and how aggressive the assumed replacement and cloud migration cycles are.

Some estimates bundle a broader healthcare IT stack around EHR, including adjacent administrative modules and wider digital health functions, which lifts the stated total. For Mordor Intelligence, the count stays with clinical EHR revenues across hardware, software, and services, and it excludes stand-alone practice management or billing systems when they are not sold as part of the clinical record workflow.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 22.15 B (2025) | |

| Global Consultancy A | USD 42.62 B (2025) | Uses a wider functional scope that blends clinical EHR with broader provider IT applications and associated modules, which increases the counted revenue pool beyond core clinical record management. |

| Industry Publisher B | USD 42.72 B (2025) | Counts a broader application set and may treat bundled practice and patient management plus billing-related functions as part of the core market, which can inflate totals when EHR is sold as a suite. |

The spread in the table is mainly explained by how far each source extends the product definition and how suites are counted. By keeping the counted revenues tied to clinical record capture, storage, exchange, and the directly attached services and hardware, the final number stays traceable to clear inputs and can be repeated when assumptions are updated.

Key Questions Answered in the Report

What factors are prompting providers to replace legacy EHR platforms?

Hospitals and ambulatory networks are prioritizing unified records that support real-time data exchange, telehealth integration, and streamlined regulatory reporting, making older siloed systems operationally untenable.

How is artificial intelligence reshaping clinician workflows within EHR systems?

Ambient voice tools now automate note-taking and coding, drastically reducing documentation time and allowing clinicians to devote more attention to direct patient care.

Why are cloud deployments increasingly favored over on-premise installations?

Cloud-hosted EHRs deliver automatic updates, elastic scaling, and lower maintenance burdens while satisfying modern disaster-recovery and security expectations.

What role do government regulations play in EHR purchasing decisions?

Compliance rules that tie reimbursement to interoperability and data-sharing incentives push providers toward vendors with proven exchange capabilities and certified security frameworks.

How are cybersecurity requirements influencing vendor selection?

Insurers now offer premium rebates for platforms that meet advanced security standards, so health systems weigh a vendor’s breach history and encryption protocols as heavily as clinical features.

Which user group is emerging as a key growth opportunity for EHR vendors?

Outpatient clinics and ambulatory centers are adopting agile, cloud-ready systems to meet value-based care objectives, making them a prime target for specialized product lines.

Page last updated on: