United States Ambulatory Electronic Health Record (EHR) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

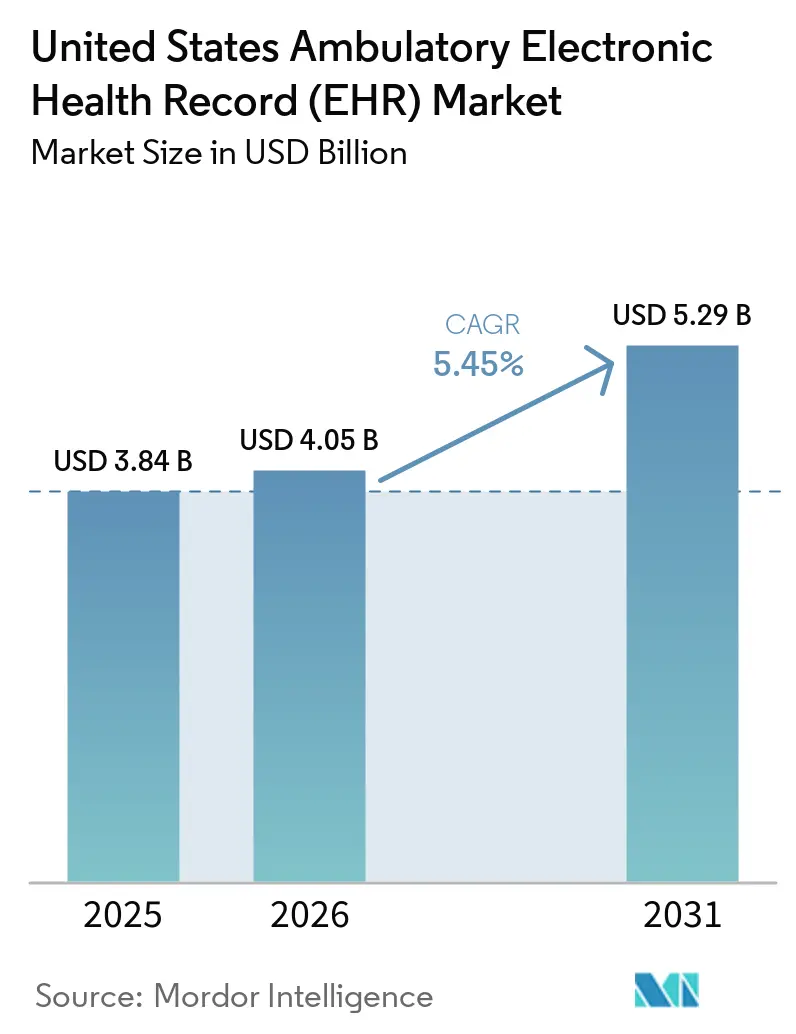

| Base Year Market Size (2025) | USD 3.84 Billion |

| Market Size (2026) | USD 4.05 Billion |

| Market Size (2031) | USD 5.29 Billion |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

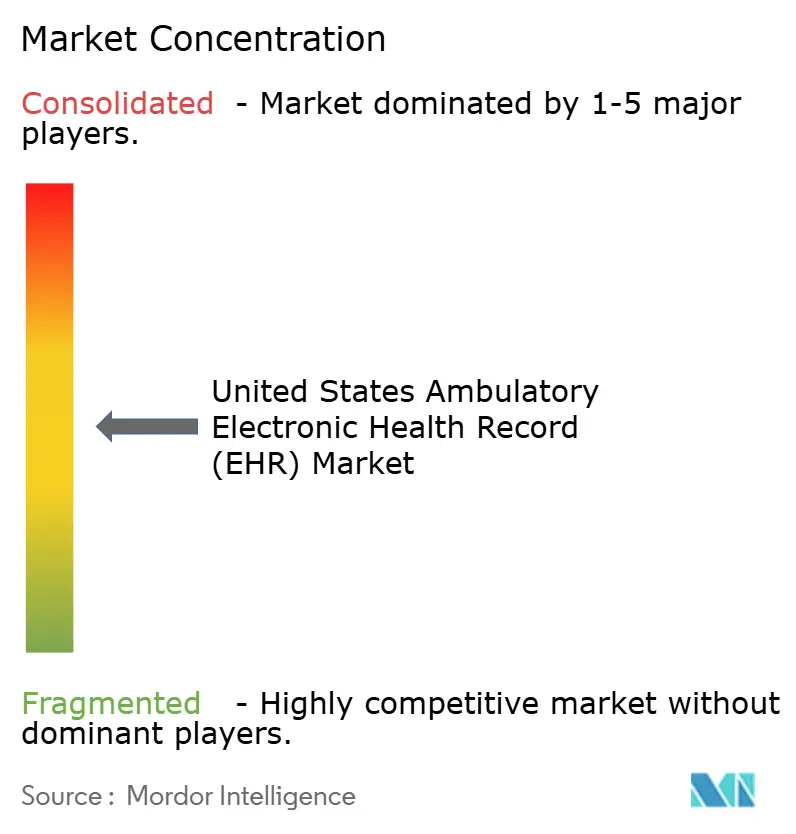

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Ambulatory Electronic Health Record (EHR) Market Analysis by Mordor Intelligence

The United States Ambulatory Electronic Health Record (EHR) Market size is expected to grow from USD 3.84 billion in 2025 to USD 4.05 billion in 2026 and is forecast to reach USD 5.29 billion by 2031 at 5.45% CAGR over 2026-2031.

The main force behind this expansion is the sustained move of procedures into outpatient settings, where Medicare-certified ambulatory surgery centers reached 6,436 facilities in 2024 and procedure volume per fee-for-service Medicare beneficiary rose 3.5% in the same year. CMS is also widening the outpatient procedure base, with 285 mostly musculoskeletal procedures removed from the inpatient-only list in 2026 and 271 procedures added to the ASC covered list, which supports steady platform demand in newly eligible care settings. The United States ambulatory EHR software market is also being shaped by a firm compliance timetable, since federal interoperability and prior authorization rules require vendors and providers to modernize data exchange, workflow, and reporting capabilities on a fixed schedule. Competition is moving toward embedded AI and FHIR-native interoperability, with Epic and Oracle Health both tying next-generation workflow tools to core platform upgrades in 2025 and 2026. At the same time, cyber risk remains a meaningful brake on adoption pace for smaller providers, because healthcare breach costs averaged USD 7.42 million in 2025 and ransomware appeared in 44% of reviewed incidents.

Key Report Takeaways

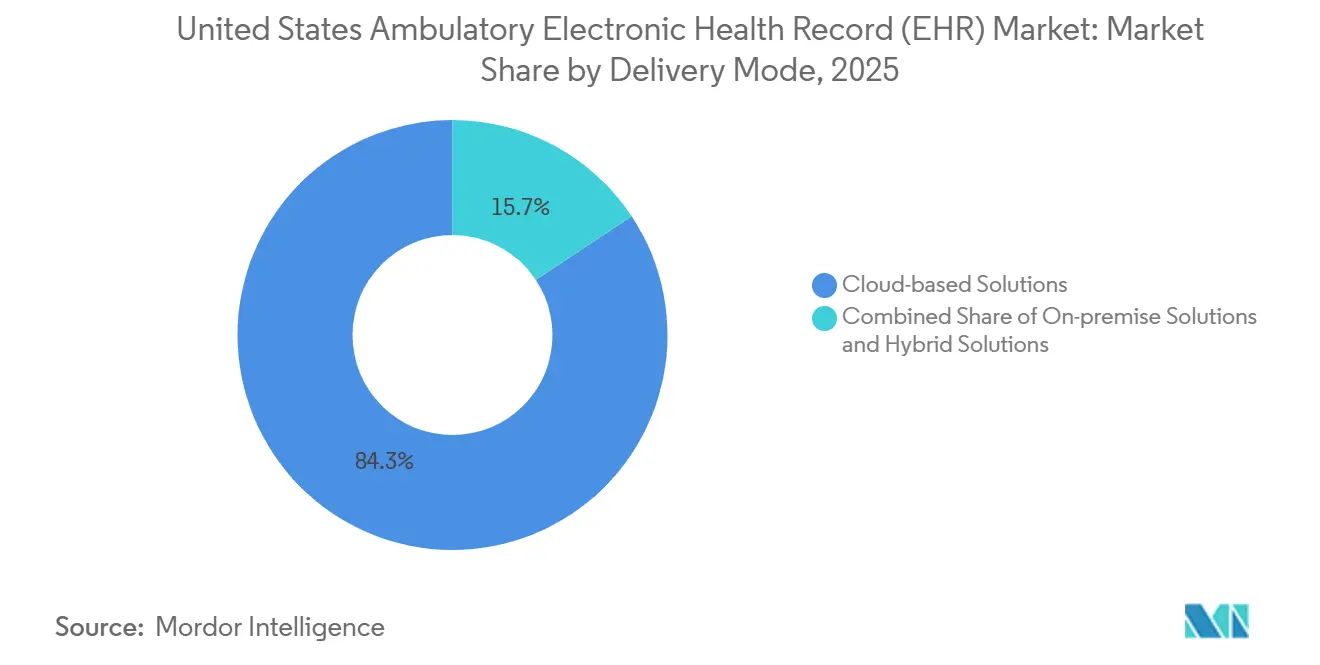

- By delivery mode, cloud-based solutions held 84.3% of the United States ambulatory EHR software market size in 2025 and also recorded the fastest growth at 6.4% through 2031.

- By functionality, practice management led with a 22.2% share in 2025, while patient management expanded at the highest projected CAGR of 6.5% through 2031.

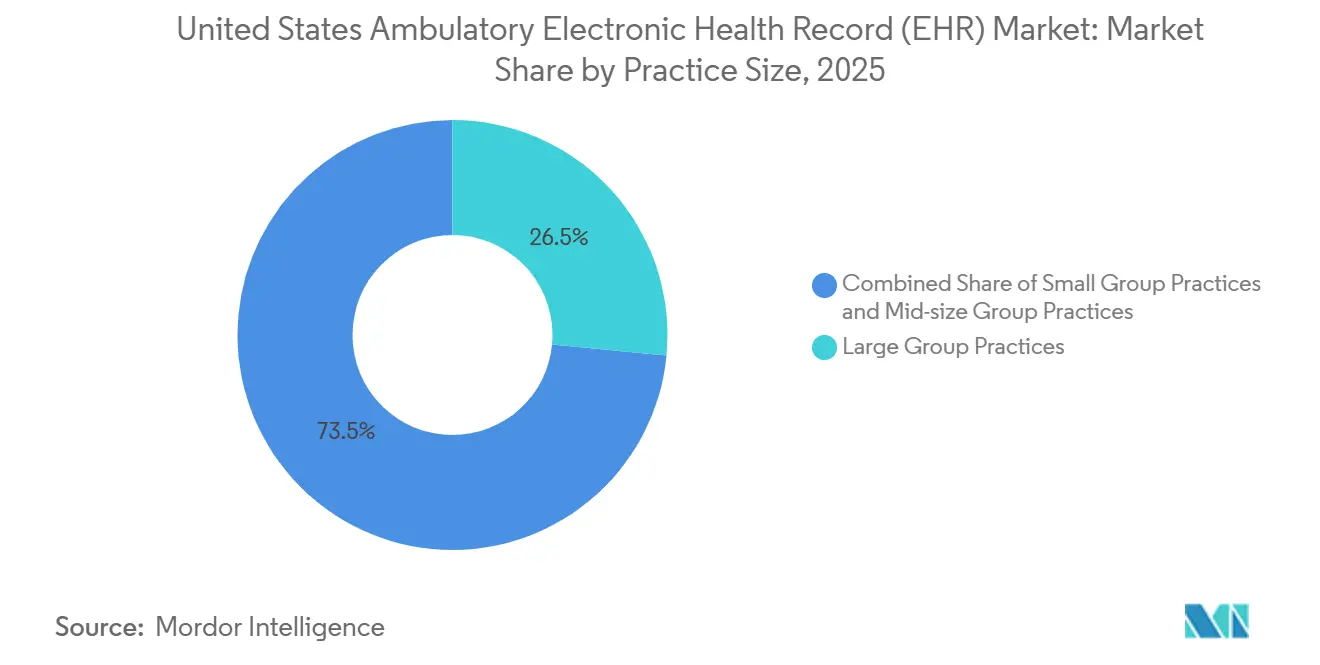

- By practice size, large group practices held 26.5% of United States ambulatory EHR software market share in 2025, while small group practices posted the fastest projected CAGR at 6.3% through 2031.

- By ownership, hospital-owned ambulatory centers accounted for 42.5% share in 2025, while independent ambulatory centers recorded the highest projected CAGR at 6.8% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Ambulatory Electronic Health Record (EHR) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outpatient care shift and ASC expansion | +1.5% | National, with concentrated gains in Sun Belt and suburban markets | Short term (≤ 2 years) |

| Cloud-native replacement cycle | +1.2% | National, with early adoption in large metro multi-specialty groups | Short term (≤ 2 years) and Medium term (2-4 years) |

| Value-based care reporting pressure | +0.9% | National, MSSP-heavy Northeast, Midwest, and California markets | Medium term (2-4 years) |

| Ambient AI and specialty workflow upgrades | +0.8% | National, metropolitan hospitals and large group practices lead adoption | Short term (≤ 2 years) and Medium term (2-4 years) |

| Prior-authorization API readiness | +0.5% | National | Medium term (2-4 years) |

| FHIR, USCDI, and TEFCA interoperability refresh | +0.4% | National | Medium term (2-4 years) and Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Outpatient Care Shift and ASC Expansion Drive Structural Demand

The United States ambulatory EHR software market is gaining durable support from the continued shift of surgery into outpatient settings. A 2026 Penn LDI research update, based on a study in Medical Care Research and Review, found that outpatient surgery grew 6% annually after the pandemic and that more than 65% of surgeries were already being performed outside inpatient settings. MedPAC reports in March 2026 that Medicare-certified ASCs increased 2.2% to 6,436 facilities in 2024 and that ASC procedures per fee-for-service Medicare beneficiary rose 3.5% in the same year. CMS is reinforcing that shift by removing 285 procedures from the inpatient-only list for 2026 and adding 271 procedures to the ASC covered list, which expands the outpatient case mix that ambulatory records systems must support[1]Centers for Medicare & Medicaid Services, “Medicare Program, Hospital Outpatient Prospective Payment and Ambulatory Surgical Center Payment Systems, Quality Reporting Programs,” Federal Register, govinfo.gov. MedPAC also shows faster procedure growth in orthopedics, cardiology, and multispecialty pain management, which raises the need for specialty-specific documentation, scheduling, and authorization workflows inside the United States ambulatory EHR software market.

Cloud-Native Replacement Cycle Reshapes Vendor Economics

The United States ambulatory EHR software market is also being reshaped by an active migration away from legacy on-premise systems. The ONC HTI-1 final rule requires certified health IT to support USCDI v3 through FHIR US Core profiles, which makes modern API support a basic product requirement rather than an optional enhancement. Cloud architectures are better aligned with recurring standards updates because they can push interoperability and compliance changes without the slower local upgrade cycle common in older deployments. Oracle Health reinforces that direction with its OCI-native ambulatory EHR and Clinical AI Agent, which connect new AI functionality directly to cloud infrastructure choices. As data portability becomes a compliance expectation, switching friction should keep easing and replacement activity should continue to move through the United States ambulatory EHR software market.

Value-Based Care Reporting Pressure Drives Certified EHR Upgrades

Value-based care reporting is creating a separate upgrade cycle inside the United States ambulatory EHR software market. CMS states in the 2026 Physician Fee Schedule final rule that all Medicare Shared Savings Program ACO participants must report MIPS Promoting Interoperability measures regardless of track, which removes flexibility for practices still operating on outdated certified systems[2]Centers for Medicare & Medicaid Services, “Medicare and Medicaid Programs, CY 2026 Payment Policies Under the Physician Fee Schedule,” Federal Register, federalregister.gov. This raises the cost of delaying upgrades because ambulatory providers must capture, structure, and exchange data in a more consistent way across quality and interoperability workflows. CMS also shows that Promoting Interoperability represented 25% of the MIPS final score for traditional participants in 2025, which means weak reporting can translate into future Medicare payment pressure. Vendors that can support quality reporting, standards-based exchange, and real-time workflow monitoring inside one platform should keep gaining ground in the United States ambulatory EHR software market.

Ambient AI Embeds Into EHR Workflows At A Sector-Defining Pace

Ambient AI is moving from pilot programs into mainstream workflow design across the United States ambulatory EHR software market. Research published in The American Journal of Managed Care found that 62.6% of Epic-using U.S. hospitals had adopted at least 1 ambient AI documentation tool by June 2025, which signals unusually fast diffusion for a new clinical software category. A multicenter study published in JAMA Network Open found that burnout fell from 51.9% to 38.8% and after-hours documentation time decreased by 0.9 hours per week after ambient AI scribe use across 6 U.S. health systems. Epic is embedding AI Charting inside its own platform in February 2026, while Oracle Health already launched an AI-driven ambulatory EHR in August 2025, which shows that core vendors now treat ambient assistance as a platform feature instead of a peripheral add-on. Practices that remain on older systems without native or certified AI integrations are likely to face growing pressure in clinician recruitment, retention, and workflow efficiency as the United States ambulatory EHR software market moves forward.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity and outage exposure | -0.8% | National, independent ambulatory centers and small practices are most exposed | Short term (≤ 2 years) |

| High implementation and migration costs | -0.7% | Rural markets and small group practices | Medium term (2-4 years) |

| Workflow disruption and staff training burden | -0.5% | Small and rural practices, resource-constrained independent providers | Short term (≤ 2 years) and Medium term (2-4 years) |

| API monetization and integration overages | -0.4% | National, independent and mid-size practices | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity And Outage Exposure Slow Cloud Adoption Among At-Risk Segments

Cybersecurity remains the clearest operating restraint in the United States ambulatory EHR software market. IBM reports that the average healthcare breach cost reached USD 7.42 million in 2025 and that the average breach lifecycle extended to 279 days, which kept healthcare as the costliest sector for the 14th consecutive year. A July 2025 study in JAMA Network Open found that 34% of Epic-using hospitals experienced detectable service disruption during the July 2024 CrowdStrike outage, including interruptions tied to scheduling, lab results, prescription refills, and secure messaging. These events show that risk does not stop with ransomware and also includes wider infrastructure and third-party failures that can interrupt basic ambulatory operations. Smaller and independent providers will therefore keep assessing vendors through a strong security lens, which can slow replacement timing inside the United States ambulatory EHR software market.

High Implementation And Migration Costs Persist As A Barrier

High implementation and migration costs still slow change in the United States ambulatory EHR software market. The AMA describes EHR transitions as remarkably expensive, laborious, personnel-devouring, and time-consuming, which captures the scale of operational disruption that many practices still expect during a switch[3]American Medical Association, “EHR Transitions, Best Practices for Implementing a New EHR System,” AMA STEPS Forward, ama-assn.org. The burden extends beyond software contracts because training, workflow redesign, interface validation, and short-term productivity loss all consume scarce staff capacity. Federal data portability rules should reduce lock-in over time, but they do not remove the local work required to clean data, map workflows, and retrain users for a new platform. This keeps many smaller organizations cautious even when the product and compliance case for modernization is strong in the United States ambulatory EHR software market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Delivery Mode: Cloud Consolidation Advances Across All Practice Tiers

Cloud-based solutions held 84.3% of the United States ambulatory EHR software market size in 2025 and are projected to grow at a 6.4% CAGR through 2031. That lead shows the replacement cycle is still active rather than complete. Cloud delivery is gaining support because it makes regulatory updates, interoperability changes, and recurring software releases easier to manage across distributed ambulatory sites. The ONC HTI-1 rule and the CMS prior authorization framework both favor platforms that can deliver FHIR-based exchange as a routine product function instead of a major local project. This gives cloud vendors a practical advantage when buyers weigh compliance risk against aging technology debt.

The United States ambulatory EHR software market still keeps a smaller on-premise base among academic groups, research-linked settings, and organizations with long legacy contract cycles. Some larger systems will continue using hybrid designs where core records remain tightly governed while analytics, interoperability layers, or AI tools shift into hosted environments. Even so, AI capability is moving closer to cloud infrastructure, and Oracle Health makes that link clear through its OCI-native ambulatory EHR roadmap. As a result, cloud growth should remain broad across practice tiers, while on-premise demand is more likely to come from delayed replacement than from fresh expansion. In the ambulatory EHR software industry, delivery choices now depend on compliance readiness and automation access as much as on hosting preference.

By Functionality: Practice Management Anchors Revenue, Patient Management Accelerates

Practice management held 22.2% share in 2025, which made it the largest functionality block in the United States ambulatory EHR software market. That position reflects the daily role of scheduling, billing, coding support, and claims follow-up in outpatient economics. Ambulatory providers still treat these tools as the first defense against revenue leakage because front-office errors and denial issues affect cash flow quickly. The segment also benefits from the rise of ASCs and multi-site outpatient groups, which need consistent administrative routines across locations. This keeps practice management central even as more advanced clinical and AI functions expand.

Patient management is projected to grow at a 6.5% CAGR through 2031, the fastest rate among functionality segments in the United States ambulatory EHR software market. Growth is tied to stronger quality reporting demands, population health tracking, and the need to close care gaps within value-based contracts. The 2026 Physician Fee Schedule rule and ongoing Promoting Interoperability requirements make more consistent data capture unavoidable for ACO-aligned ambulatory practices. Referral management and e-prescribing should remain important because compliance and care coordination both depend on clean data moving across the ambulatory workflow. The ambulatory EHR software industry is therefore shifting toward platforms that combine financial, clinical, and reporting functions within one connected record.

By Practice Size: Large Practices Lead By Share, Small Practices Drive Growth

Large group practices held 26.5% of the United States ambulatory EHR software market share in 2025 and remained the biggest practice-size segment. Their lead reflects stronger budgets, wider IT support, and a greater ability to spread implementation work across many clinicians and sites. These organizations fit enterprise purchasing models that prioritize standardization, centralized reporting, and tighter governance of clinical workflows. They are also better positioned to deploy ambient AI, interoperability tooling, and advanced reporting because change management can be handled more systematically. This keeps large practices important to incumbent vendors even when overall growth shifts elsewhere.

Small group practices are projected to expand at a 6.3% CAGR through 2031, making them the fastest-growing practice-size tier in the United States ambulatory EHR software market. Growth is tied to suburban and peri-urban outpatient expansion, where independent physicians and newer ambulatory centers continue to create demand for lighter and more affordable digital platforms. Cloud delivery lowers the technical barrier for these buyers, even if migration still feels costly and disruptive. Mid-size groups remain the most contested accounts because they need more depth than entry-level products but often resist the price and complexity of enterprise suites. CMS reweighting for small practices eases part of the reporting burden, but replacement timing will still depend on workflow fit, budget discipline, and vendor service quality .

By Ownership: Hospital Systems Anchor Market, Independent Centers Grow Fastest

Hospital-owned ambulatory centers held 42.5% share in 2025 and represented the largest ownership segment in the United States ambulatory EHR software market. Their scale gives them stronger capital capacity and easier access to enterprise vendor agreements. They also benefit from direct links into hospital clinical, financial, and reporting systems, which makes standardization a practical requirement rather than a discretionary upgrade. This keeps major incumbent vendors well positioned in health-system-linked outpatient networks. It also reinforces the market's bias toward integrated platforms in multi-site settings.

Independent ambulatory centers are projected to grow at a 6.8% CAGR through 2031, which makes them the fastest-growing ownership group in the United States ambulatory EHR software market. That gap points to continued consolidation across independent ASC and multispecialty physician networks, where operators need standardized software across distributed sites. The same group remains more exposed to implementation cost and cyber risk, so vendor selection often centers on ease of deployment and security reassurance. Health-system-affiliated physician groups also face stronger pressure to align reporting and data exchange as interoperability and Promoting Interoperability rules tighten. Ownership trends should therefore keep rewarding vendors that can serve both enterprise consolidation and independent outpatient expansion.

Geography Analysis

The South and wider Sun Belt continue to offer strong demand because population growth and site-of-care migration are adding outpatient capacity in suburban and metro areas. MedPAC shows that ASC density ranged from 2 per 100,000 Part B beneficiaries in Vermont to 36 in Maryland, which highlights how uneven outpatient infrastructure remains across the country. That spread creates equally uneven demand intensity for deployment, support, and replacement activity in the United States ambulatory EHR software market. States that repealed certificate-of-need laws, including South Carolina, Georgia, and North Carolina, are positioned for added new-site demand as ambulatory facilities keep opening.

The Northeast remains a mature part of the United States ambulatory EHR software market because hospital-employed physician groups and ACO participation are more concentrated there. That maturity supports replacement demand more than first-time adoption, with interoperability, reporting, and standardization driving budgets. The Midwest shows a slower AI profile, since predicted ambient AI adoption probability was 54.9% there compared with 69.5% in the South. This gap gives AI-forward vendors room to compete on clinician workflow relief rather than on core charting alone. The United States ambulatory EHR software market in these mature regions is therefore being shaped less by seat growth and more by replacement timing, integration depth, and compliance pressure.

Rural markets across Appalachia, the Great Plains, and the Mountain West continue to face weaker adoption conditions because broadband constraints, limited cybersecurity staffing, and tighter margins reduce implementation capacity. The rural gap is reinforced by the heavy urban concentration of ASCs, which leaves fewer procedure-driven anchors for large new deployments. Federal interoperability and security obligations still apply uniformly, so smaller markets face the same compliance deadlines with fewer internal resources. As a result, the United States ambulatory EHR software market should keep expanding nationally, but vendors with simpler cloud rollouts and stronger security support are likely to perform better outside the largest metro clusters.

Competitive Landscape

The United States ambulatory EHR software market remains moderately concentrated, with Epic Systems, athenahealth, eClinicalWorks, Oracle Health, and NextGen Healthcare holding the majority of enterprise and mid-market revenue. That top layer is balanced by a long tail of specialty vendors that compete on workflow fit rather than on scale alone. Epic raises the competitive bar in February 2026 with AI Charting inside its Art for Clinicians suite, which gives health systems a native documentation tool tied directly to the core record. Oracle Health also strengthens its position through an OCI-native ambulatory EHR with a Clinical AI Agent, which shows that cloud infrastructure and AI capability now sit at the center of platform differentiation. The United States ambulatory EHR software market is therefore moving through a replacement cycle where usability, interoperability, and embedded automation matter as much as the core chart itself.

Specialty-focused companies such as ModMed, Tebra Technologies, and Nextech Systems continue to capture demand in dermatology, ophthalmology, orthopedics, and behavioral health because those practices need deeper templates and more tailored workflows. That specialty pressure matters because larger platforms have historically been strongest in multispecialty and hospital-linked settings. The next layer of competition is increasingly defined by interoperability readiness, since federal rules require certified systems to support FHIR-based data exchange and prior authorization workflows on a fixed schedule. Vendors that deliver these updates natively should reduce buyer hesitation, while vendors that depend on heavy customization may struggle to keep pace. The United States ambulatory EHR software market also favors platforms that can package security controls, AI tools, and reporting capabilities within a single contract as provider groups try to limit vendor sprawl.

Recent strategic moves show that leading vendors are extending their reach beyond core recordkeeping. Epic and Labcorp expand their collaboration in May 2026 so Labcorp's full diagnostic menu can flow through Epic's Aura platform, which supports tighter ordering and results integration across ambulatory settings. Oracle Health reaches CMS Aligned Network status in April 2026 and integrates CLEAR identity tools into EHR check-in workflows, which underscores its effort to compete through interoperability and front-end workflow redesign. These moves support a competitive pattern in which large vendors defend installed bases through platform breadth, while niche vendors keep winning where specialty depth remains insufficient.

United States Ambulatory Electronic Health Record (EHR) Industry Leaders

Epic Systems Corporation

eClinicalWorks, LLC

athenahealth, Inc.

Oracle Health

NextGen Healthcare, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Epic and Labcorp expanded their collaboration to make Labcorp's full diagnostic test menu available through Epic's Aura platform, streamlining lab ordering and result integration across Epic's ambulatory installed base and reducing per-interface IT maintenance costs for health systems.

- April 2026: Oracle Health achieved CMS Aligned Network status and integrated CLEAR's secure identity platform into EHR check-in workflows to support CMS's "Kill the Clipboard" initiative, with AtlantiCare as an early ambulatory adopter, demonstrating Oracle Health's interoperability-first repositioning strategy.

United States Ambulatory Electronic Health Record (EHR) Market Report Scope

As per the scope of the report, an ambulatory electronic health record (EHR) is a digital version of a patient's medical chart that is used in outpatient settings such as clinics, physician offices, and outpatient care facilities. It contains comprehensive health information, including medical history, medications, allergies, lab results, imaging, and treatment plans, enabling healthcare providers to deliver coordinated and efficient care outside of hospital inpatient environments.

The United States ambulatory EHR market is segmented by delivery mode into cloud-based solutions, on-premise solutions, and hybrid solutions. By functionality, the market is categorized into practice management, patient management, e-prescribing, referral management, population health management, and others. Based on practice size, the segmentation includes small group practices, mid-size group practices, and large group practices. By ownership, the market is divided into hospital-owned ambulatory centers, health-system affiliated physician groups, and independent ambulatory centers. For each segment, the market size and forecast are provided in terms of value (USD).

| Cloud-based Solutions |

| On-premise Solutions |

| Hybrid Solutions |

| Practice Management |

| Patient Management |

| E-Prescribing |

| Referral Management |

| Population Health Management |

| Others |

| Small Group Practices |

| Mid-size Group Practices |

| Large Group Practices |

| Hospital-owned Ambulatory Centers |

| Health-system Affiliated Physician Groups |

| Independent Ambulatory Centers |

| By Delivery Mode | Cloud-based Solutions |

| On-premise Solutions | |

| Hybrid Solutions | |

| By Functionality | Practice Management |

| Patient Management | |

| E-Prescribing | |

| Referral Management | |

| Population Health Management | |

| Others | |

| By Practice Size | Small Group Practices |

| Mid-size Group Practices | |

| Large Group Practices | |

| By Ownership | Hospital-owned Ambulatory Centers |

| Health-system Affiliated Physician Groups | |

| Independent Ambulatory Centers |

Key Questions Answered in the Report

What is the projected value of the United States ambulatory EHR software market by 2031?

The United States ambulatory EHR software market is projected to reach USD 5.29 billion by 2031, up from USD 4.05 billion in 2026, with a forecast CAGR of 5.45%.

Why is outpatient care migration so important for ambulatory EHR demand?

More procedures are moving into ASCs and other outpatient settings, which creates direct demand for scheduling, documentation, interoperability, and billing workflows built for ambulatory care.

Which delivery model leads U.S. ambulatory EHR adoption?

Cloud-based solutions led with 84.3% share in 2025 and also posted the fastest projected growth at 6.4% through 2031, reflecting the ongoing shift away from legacy systems.

What is pushing providers to upgrade certified systems now?

Federal interoperability deadlines, prior authorization API readiness, and mandatory Promoting Interoperability reporting for MSSP ACO participants are creating a fixed modernization timetable.

How is ambient AI changing vendor competition in ambulatory care records software?

Ambient AI is becoming a core platform feature, with Epic and Oracle embedding documentation support into their platforms and research showing lower burnout and less after-hours charting time after adoption.

What are the main risks slowing software replacement for smaller practices?

Cybersecurity exposure, outage risk, training burden, and migration disruption remain the main barriers, especially for smaller independent providers that have limited internal IT and security resources.

Page last updated on: