Ambulatory EHR Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.14 Billion |

| Market Size (2031) | USD 9.45 Billion |

| Growth Rate (2026 - 2031) | 5.76% CAGR |

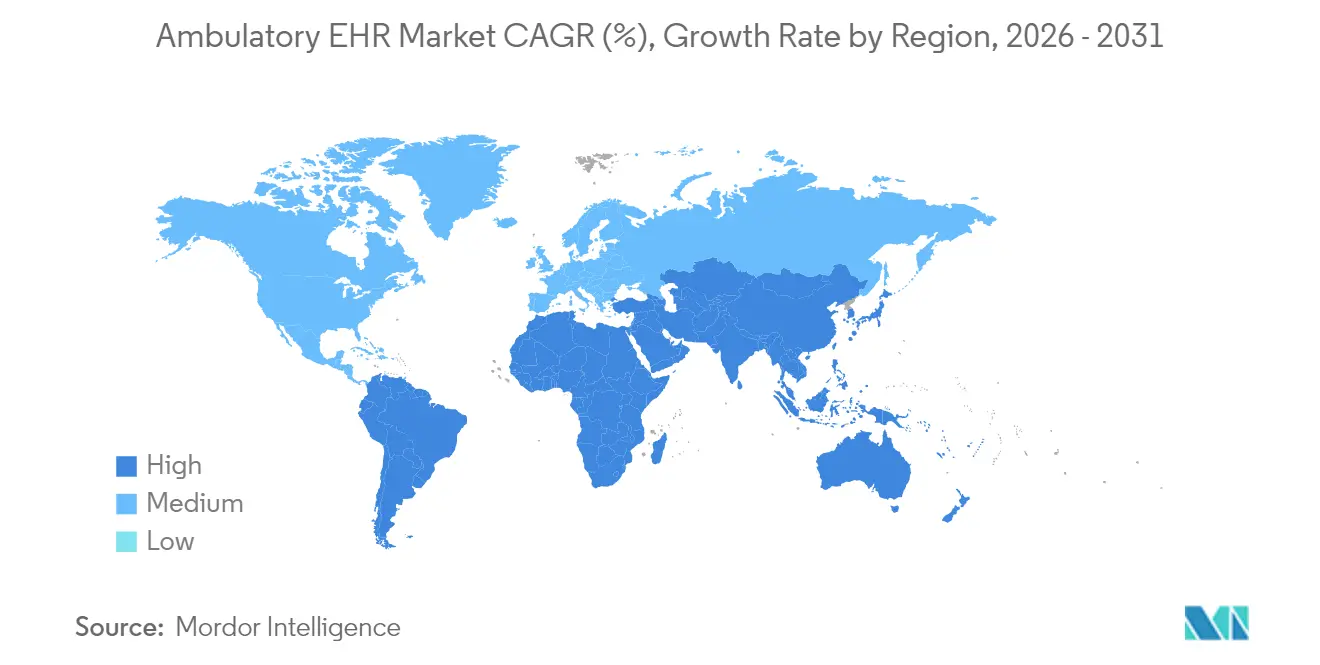

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

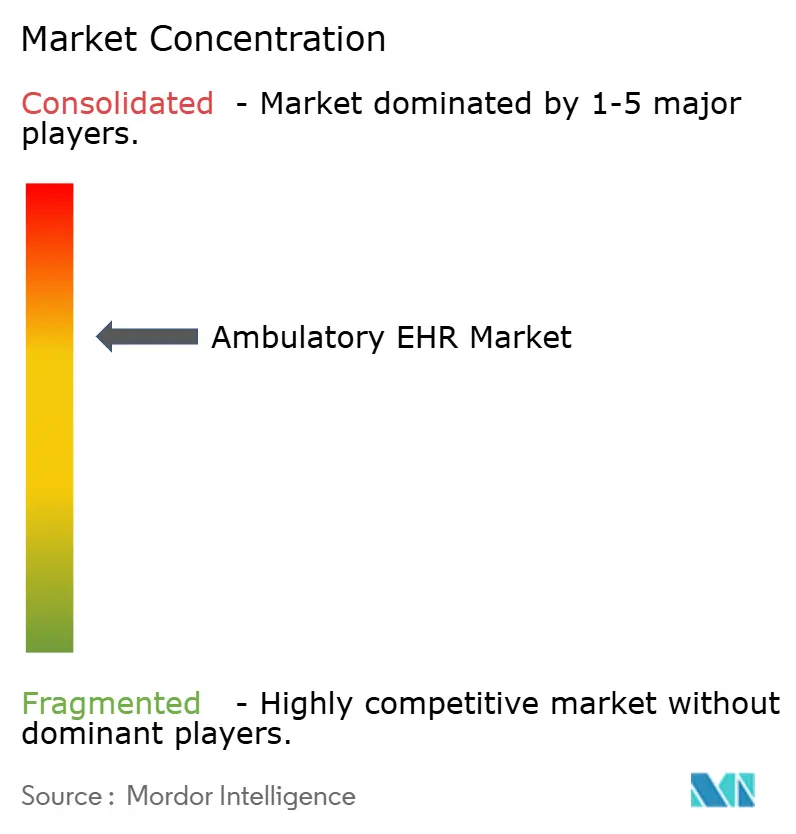

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ambulatory EHR Market Analysis by Mordor Intelligence

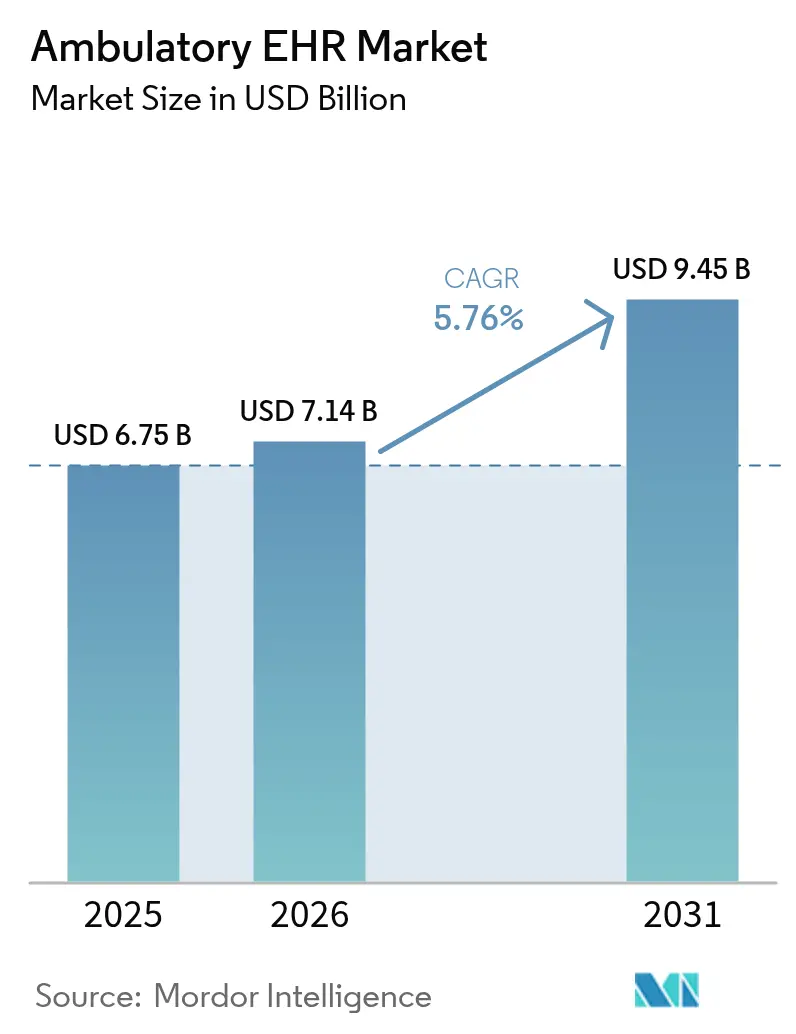

Ambulatory EHR market size in 2026 is estimated at USD 7.14 billion, growing from 2025 value of USD 6.75 billion with 2031 projections showing USD 9.45 billion, growing at 5.76% CAGR over 2026-2031. Accelerating regulatory penalties for information blocking, new Advanced Primary Care Management billing codes, and expansion of accountable-care contracts raise the stakes for providers that still rely on legacy record systems. Cloud migration remains the dominant deployment choice, delivering rapid scalability and lower capital outlays even as high-profile breaches expose security gaps. Artificial-intelligence modules that shorten documentation time and improve risk stratification now influence buying decisions more than classic feature sets. Competitive intensity is sharpening, with vendors racing to combine interoperability, telehealth workflows, and ambient listening tools into cohesive platforms that serve both large health systems and small independent practices.

Key Report Takeaways

- By delivery mode, cloud-based solutions led with 77.12% of the ambulatory EHR market share in 2025, while the cloud segment is expanding at a 6.09% CAGR through 2031.

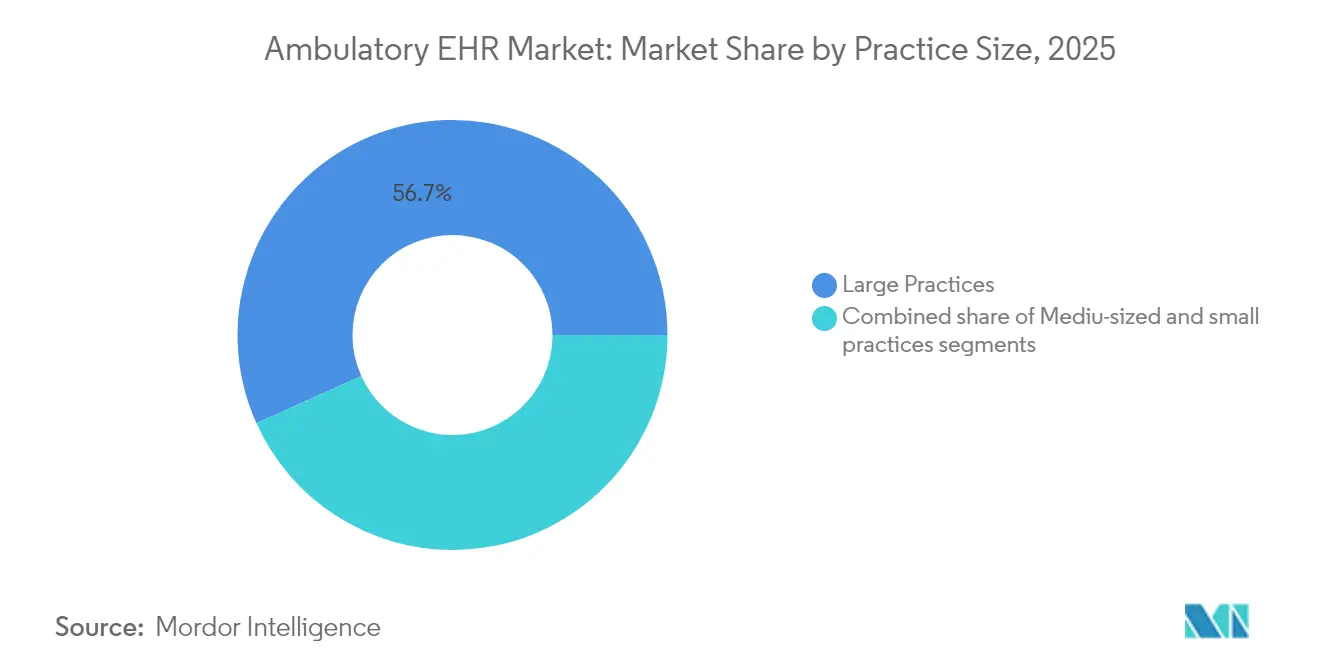

- By practice size, large practices accounted for 56.74% of the ambulatory EHR market share in 2025; small practices to record the fastest growth at 7.84% CAGR to 2031.

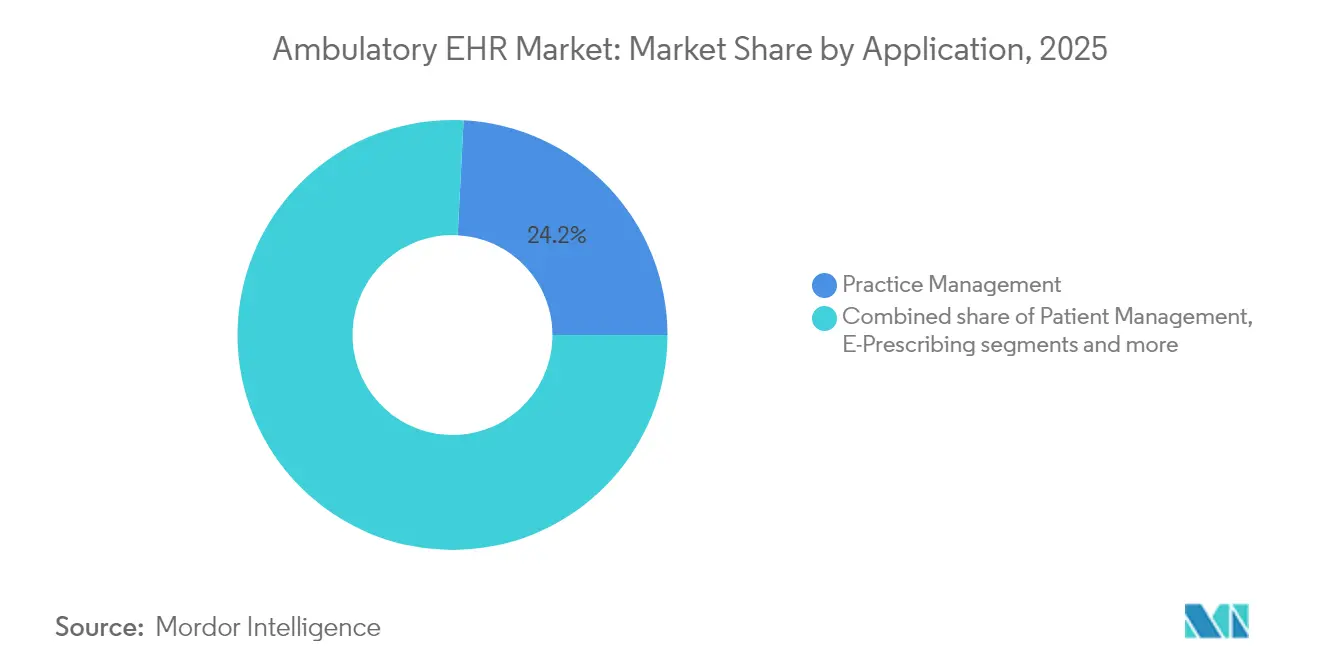

- By application, practice-management modules held 24.18% of the ambulatory EHR market size in 2025, whereas population-health management is advancing at a 6.32% CAGR.

- By end-user, hospital-owned ambulatory centers controlled a 63.58% share of the ambulatory EHR market in 2025, but independent centers are growing at a 7.41% CAGR to 2031.

- By geography, North America represented 39.88% of the ambulatory EHR market share in 2025; Asia Pacific is projected to post the highest 6.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ambulatory EHR Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government incentives & compliance mandates | +1.8% | Global, strongest in North America & Europe | Medium term (2-4 years) |

| Accelerated shift to cloud-hosted EHRs | +1.5% | Global, led by developed markets | Short term (≤ 2 years) |

| Value-based-care push for interoperable data | +1.2% | North America core, expanding to APAC | Long term (≥ 4 years) |

| Specialty-specific AI modules boosting upgrades | +0.9% | North America & Europe early adoption | Medium term (2-4 years) |

| Integration of telehealth workflows into EHR platforms | +0.8% | Global, accelerated in rural and underserved areas | Short term (≤ 2 years) |

| Reimbursement for remote monitoring & outpatient data capture | +0.7% | North America primary, Europe emerging | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Incentives & Compliance Mandates Drive Market Expansion

Penalties now outweigh rewards in EHR policy. Under the 21st Century Cures Act, providers that block information risk up to a 5% Medicare payment cut, potential removal from the Shared Savings Program, and reputational harm. The 2025 Quality Payment Program introduces seven new quality measures that demand deeper electronic clinical-quality reporting. CMS also requires FHIR-enabled APIs for patient access, a rule already met by 73% of digital-health firms[1]Wesley Barker, “A National Survey of Digital Health Company Experiences With Electronic Health Record Application Programming Interfaces,” Journal of the American Medical Informatics Association, academic.oup.com but still burdened by high implementation fees. As a result, the ambulatory EHR market benefits from a compliance-driven replacement cycle among laggard practices and smaller specialty clinics.

Cloud Migration Momentum Offset by Escalating Security Imperatives

Cloud environments lower hardware costs and speed updates, yet they expand the attack surface. The HHS Office for Civil Rights logged 626 significant breaches in 2024, affecting 41.7 million individuals; hacking accounted for 74% of incidents and network servers were the prime vector. The February 2024 Change Healthcare ransomware attack, which disrupted half of U.S. claims traffic, underscored the systemic risks of centralized data processing. Providers now demand multi-factor authentication, continuous monitoring, and zero-trust architectures as non-negotiables in vendor contracts, supporting a higher-margin security-services layer that adds stickiness to leading platforms.

Value-Based Care Integration Accelerates Interoperability Demands

CMS aims to place every Traditional Medicare beneficiary under an accountable-care arrangement by 2030, forcing ambulatory sites to exchange clinical data seamlessly across payers and hospitals. Shared-Savings ACOs now number 480, serving 10.8 million beneficiaries[2]Centers for Medicare & Medicaid Services, “Calendar Year 2025 Medicare Physician Fee Schedule Final Rule (CMS-1807-F): Medicare Shared Savings Program,” cms.gov , while new Primary-Care Management codes deliver USD 15–110 per patient each month for risk-tiered care coordination. These policy shifts push demand for population-health dashboards and closed-loop referral workflows, cementing interoperability as a decisive purchasing criterion in the ambulatory EHR market.

AI-Powered Clinical Documentation Transforms Workflow Economics

Ambient listening and generative-AI triage models are moving from pilot to production. Kaiser Permanente cut clinician documentation time by as much as two hours per day and registered patient-satisfaction scores above 92% after rolling out an AI scribe. Epic has built more than 100 AI functions, including automated MyChart messaging and order prediction, while Oracle embeds voice recognition throughout its Cerner-derived platform. These capabilities alter cost-benefit analyses for small practices that lacked staff to manage legacy documentation loads, unlocking a new addressable cohort for the ambulatory EHR market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security & privacy breach concerns | -0.8% | Global, acute in developed markets | Short term (≤ 2 years) |

| Uneven infrastructure in emerging economies | -0.6% | APAC, MEA, South America | Long term (≥ 4 years) |

| Complex multi-jurisdiction regulatory compliance | -0.6% | Global, particularly Europe-US-APAC | Medium term (2-4 years) |

| Rising pay-per-use API costs for third-party integrations | -0.5% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cyber-Security Vulnerabilities Constrain Cloud Adoption Velocity

The ALPHV ransomware breach at Change Healthcare triggered revenue losses for 80% of U.S. physician practices and required a USD 22 million ransom payment, yet still produced multi-week payment delays. Such events spur calls for distributed-ledger data storage and multi-cloud fail-over strategies, but smaller providers often lack the budgets or staff to implement them fully. As a result, some organizations postpone cloud migrations, opting for incremental hybrid architectures that slow overall ambulatory EHR market growth trajectory.

Infrastructure Disparities Limit Emerging-Market Penetration

India’s Ayushman Bharat Digital Mission issued 568 million health IDs, but rural adoption lags due to unreliable internet and scarce IT support. Urban EHR adoption[3]A. Jerrod Anzalone, “Lower Electronic Health Record Adoption and Interoperability in Rural Versus Urban Physician Participants: A Cross-Sectional Analysis From the CMS Quality Payment Program,” BMC Health Services Research, bmchealthservres.biomedcentral.com stands at 74%, while rural clinics reach only 64%. Language localization, limited funding, and provider training gaps compound the issue. Similar patterns appear across Southeast Asia and parts of Africa, tempering otherwise robust growth projections for the ambulatory EHR industry in the developing world.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Practice-Management Dominance Challenged by Population-Health Innovation

Practice-management modules captured 24.18% of the ambulatory EHR market share in 2025, reflecting their vital role in billing, scheduling, and eligibility checks. However, the ambulatory EHR market size for population-health management is projected to expand at 6.32% CAGR through 2031, spurred by risk-based reimbursement that rewards proactive chronic-care oversight. Vendors now embed AI-driven risk stratification into population dashboards, enabling small groups to manage complex patient panels without adding staff. Referral-management tools now integrate with health-information exchanges via the Trusted Exchange Framework and Common Agreement, positioning them to capture cross-network patient journeys. Specialty modules ranging from cardio-oncology to dermatology are emerging as AI-ready add-ons that can be switched on without major code rewrites, laying fresh revenue tracks for platform vendors.

Population-health dashboards benefit directly from Advanced Primary Care Management reimbursements that scale from USD 15 to USD 110 per patient per month. Clinics that demonstrate risk-based outreach and follow-up protocols see near-immediate return on investment, making this application segment the strongest pull for upgrades inside the ambulatory EHR market. As cloud hosting trims infrastructure costs, even single-site physician groups gain affordable access to analytics engines once reserved for enterprise systems, deepening market diffusion over the forecast horizon.

By Delivery Mode: Cloud Supremacy Accelerates Yet Security Doubts Persist

Cloud-hosted deployments accounted for 77.12% of the ambulatory EHR market size in 2025, and the segment is set to advance at a 6.09% CAGR. Public-cloud instances from Epic, Oracle, and athenahealth offer consumption-based pricing, rolling version updates, and turnkey analytics, but 2024’s ransomware events forced customers to scrutinize shared-responsibility clauses, conduct external penetration tests, and demand cyber-liability riders in contracts. On-premise solutions remain relevant to a minority of providers with heightened data-sovereignty needs, particularly academic medical groups that manage clinical-research data. Still, their share will keep eroding as cloud security controls mature.

Hybrid models are rising quickly among large health systems that want the elasticity of cloud analytics while retaining a local copy of core health records. This architecture mitigates single-point-of-failure risk and enables rapid disaster-recovery options. It also supports “edge-AI” inference at the point of care, reducing latency for decision support tools. These structural shifts reinforce a winner-takes-most dynamic that favors vendors with proven cloud security track records, deep interoperability credentials, and global scale.

By Practice Size: Vendor Accessibility Initiatives Boost Small-Practice Uptake

Large practices controlled 56.74% of the ambulatory EHR market share in 2025, yet growth momentum is clearly shifting to offices with fewer than 10 physicians. Epic’s Garden Plot, Oracle’s CommunityWorks, and NextGen Office specifically target this cohort with templated implementations, API marketplaces, and bundled rev-cycle services. Improving usability is crucial; 60% of small clinics state that core vendors still miss essential functions such as patient self-scheduling and integrated telehealth. The ambulatory EHR market is therefore responding with modular UI frameworks that clinicians can reconfigure without code, cutting go-live cycles to weeks rather than months.

Mid-size practices occupy a middle ground where they need enterprise-grade functionality but lack the budget of big networks. Partnership ecosystems that pool DevOps, data analytics, and network administration support are emerging to serve this group. Rural clinics wrestle with broadband deserts and staffing shortages, conditions that intensify the appeal of managed cloud offerings and voice-enabled navigation. As these accessibility hurdles are lowered, small-practice penetration will continue to outpace every other cohort, reshaping total addressable demand across the ambulatory EHR industry.

By End-User: Independent Centers Move Swiftly as Hospital-Owned Sites Consolidate

Hospital-owned ambulatory facilities commanded 63.58% of the ambulatory EHR market size in 2025, thanks to integrated systems that span inpatient, emergency, and outpatient units. Yet independent centers are growing at 7.41% CAGR, fueled by entrepreneurial models that specialize in orthopedics, gastroenterology, and women’s health. These groups require nimble EHR deployments that interoperate with multiple payers and hospital partners while supporting clinic-run ancillary services such as imaging or pharmacy. Vendor roadmaps now emphasize open, FHIR-compliant APIs and ambient documentation so that independent physicians can maintain patient throughput without heavy IT overhead.

Health-system-affiliated physician groups face distinctive pressures. They must comply with enterprise governance yet still chase local patient growth. Their wish list combines enterprise analytics, consumer-grade patient portals, and flexible billing engines that handle direct-to-employer contracts. Vendors supplying configurable workflow engines and analytics connectors are positioned to capture expansion budgets inside this segment, adding another driver to overall ambulatory EHR market growth.

Geography Analysis

North America accounted for 39.88% of 2025 revenue and will grow at 5.44% CAGR as the market transitions from digitization to optimization. New CMS rules mandate a 180-day EHR-reporting window and expanded eCQM submissions, compelling providers to replace bolt-on modules with natively interoperable alternatives. AI uptake is particularly robust; more than 30 health systems have deployed ambient listening at scale, shaving physician documentation time and elevating the ROI calculus for system refreshes. Smaller U.S. practices gain fresh incentives from codes that reimburse longitudinal care-coordination activities, widening market participation across rural states.

Asia-Pacific is the fastest-growing region at 6.96% CAGR, underpinned by India, Australia, and Japan. India’s Ayushman Bharat Digital Mission registered 568 million health accounts, yet only a fraction translates to active EHR utilization because of patchy connectivity and language diversity. Government subsidies for network upgrades and device procurement are beginning to bridge this gap. China and South Korea aggressively subsidize AI-based medical analytics, creating green-field demand for cloud-hosted ambulatory systems that ship with built-in machine-learning pipelines. These trends position the region as the largest incremental revenue pool for the ambulatory EHR market during the forecast period.

Europe shows a 5.80% CAGR, supported by national e-health plans in Germany, France, and the Nordics that emphasize cross-border data sharing. GDPR compliance imposes rigid access controls and audit logging, tilting procurement toward established vendors with robust privacy frameworks. Middle East & Africa follow at 6.28% CAGR, helped by telemedicine programs in Saudi Arabia and the UAE that funnel patient-generated data directly into ambulatory records. South America is growing 5.92% CAGR, with Brazil leading investments in cloud-native EHRs that integrate with public-health reporting portals. Infrastructure gaps remain a constraint throughout emerging markets. Still, multi-tenant public-cloud deployments and mobile-first front ends offer cost-effective workarounds, bolstering long-run prospects for the ambulatory EHR market.

Competitive Landscape

Epic Systems expanded its share of U.S. hospital installations in 2024 by signing 176 new facilities and adding 29,399 beds. Its continued dominance stems from aggressive product releases—over 100 new AI features—and a reputation for deep-link interoperability. Oracle Health, the rebranded Cerner acquisition, lost 74 hospital sites despite refreshed cloud architecture, illustrating integration friction that can erode share even for well-capitalized players. MEDITECH Expanse, athenahealth, and NextGen pivot to niche plays, emphasizing physician delight, fast go-lives, and low total cost of ownership, strategies that resonate in the ambulatory EHR market’s under-served small-practice tier.

AI remains the headline differentiator. Epic’s GPT-powered MyChart Compose drafts patient messages, while Oracle embeds real-time prior-authorization checks. InterSystems unveiled IntelliCare, layering generative AI onto its global TrakCare base to accelerate note generation. Start-up challengers such as Elation and Canvas flaunt API-first architectures that let digital health builders spin up new care-delivery models quickly. Still, buyers gravitate toward vendors demonstrating proven cyber-resilience; the Change Healthcare saga sharpened this filter, making tabletop-tested incident-response plans a key selection criterion.

Partnership ecosystems are mushrooming. Veradigm’s Ambient Scribe injects AI transcription into any EHR via a standards-based API, while its Insiteflow deal pipes payer coverage rules into Epic workflows. Large cloud providers—Microsoft, Google, and AWS—offer health-data services that underlie many mid-tier vendor stacks. The resulting landscape is increasingly barbell-shaped: a handful of mega-platforms at one end and specialized best-of-breed apps at the other, all vying to aggregate the next billion clinical interactions in the ambulatory EHR market.

Ambulatory EHR Industry Leaders

Epic Systems Corporation

Medical Information Technology, Inc. (Meditech)

Oracle Corporation

TruBridge, Inc.

Veradigm Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Epic Systems unveiled a healthcare-specific ERP suite spanning workforce, finance, and supply management, positioning itself against Oracle and Workday.

- March 2025: InterSystems launched IntelliCare, an AI-powered EHR overlay built on TrakCare that automates encounter notes and supports natural-language commands.

- November 2024: Veradigm released Ambient Scribe, an AI tool that captures patient conversations and populates structured notes inside Veradigm EHR.

- April 2024: eClinicalWorks integrated Sunoh.ai ambient listening across its install base, enabling Canyonville Health to expand chronic-care services.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the ambulatory electronic health record (EHR) market as all license, subscription, and support revenues earned from purpose-built EHR software deployed in physician offices, urgent-care clinics, and freestanding outpatient centers worldwide. These totals cover core charting modules, billing add-ons, patient portals, and cloud hosting that accompany the primary record system.

Scope exclusion: inpatient hospital EHR suites and stand-alone practice-management tools without clinical documentation are not counted.

Segmentation Overview

- By Application

- Practice Management

- Patient Management

- E-Prescribing

- Referral Management

- Population Health Management

- Others

- By Delivery Mode

- Cloud-based Solutions

- On-premise Solutions

- Hybrid Solutions

- By Practice Size

- Large Practices

- Medium-sized Practices

- Small Practices

- By End-User

- Hospital-owned Ambulatory Centers

- Independent Ambulatory Centers

- Health-system Affiliated Physician Groups

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed EHR product managers, clinic administrators, and health-IT regulators across North America, Europe, Asia, and the Gulf to validate usage intensity, cloud pricing tiers, and integration pain points. Structured surveys with small-practice physicians helped refine average seats per facility and upgrade cycles that are hard to spot in filings.

Desk Research

We begin by mapping the addressable universe through public datasets such as the U.S. Office of the National Coordinator's Certified Health IT list, CMS Physician Compare, OECD Health Statistics, and World Health Organization digital-health compendia. Trade bodies like HIMSS and the American Medical Association supply clinic counts and adoption ratios, while patent and tender feeds from Questel and Tenders Info flag pipeline activity. Financial clues come from SEC 10-Ks, IPO filings, and voluntary disclosures on vendor websites, all parsed inside Dow Jones Factiva. These inputs set the outer guardrails for volume, price, and regional spread.

Because many nations lack granular outpatient software data, we lean on shipment-level customs records from Volza, peer-reviewed journals that benchmark EHR penetration, and country eHealth strategy documents to plug data gaps. The sources noted here are illustrative; analysts reviewed additional government, academic, and industry material to cross-check every figure.

Market-Sizing & Forecasting

A top-down "clinic head-count × penetration rate × average annual spend" build provides the first pass, which is then stress-tested with selective bottom-up vendor revenue rolls and channel checks. Key variables like the number of ambulatory visits, share of cloud deployments, average subscription per physician, regulatory incentive timelines, and refresh frequency drive the model. Multivariate regression aligns historical spend with these indicators and projects through 2030, with scenario analysis applied where policy shifts are material.

Data Validation & Update Cycle

Before sign-off, outputs are reconciled against independent adoption trackers and currency movements; anomalies trigger a recheck call with experts, and a senior reviewer signs the workbook. Reports refresh annually; material vendor mergers or policy moves prompt an interim update, ensuring clients receive our latest view.

Why Mordor's Ambulatory EHR Baseline Stands Firm

Published estimates often diverge because firms pick different product baskets, price assumptions, and refresh cadences. Our disciplined scope selection and yearly re-benchmarking narrow those gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.75 B (2025) | Mordor Intelligence | - |

| USD 6.56 B (2024) | Global Consultancy A | Excludes embedded analytics modules and uses blended regional ASPs |

| USD 6.50 B (2023) | Industry Research Group B | Relies on clinic count projections without validating active user licenses |

The comparison shows differences stem less from market reality and more from scope trimming and untested assumptions. By anchoring our baseline to validated clinic inventories, real subscription pricing, and an annual review cycle, Mordor Intelligence offers decision-makers a balanced, transparent starting point they can trace and replicate.

Key Questions Answered in the Report

How are value-based care models shaping EHR feature priorities?

Tools that enable population-health dashboards, closed-loop referrals, and device-sourced patient-generated data have become essential as reimbursement increasingly rewards coordinated, outcome-focused care.

What makes hybrid deployment architectures attractive to large health systems?

Hybrid models keep sensitive clinical records on-premise for control and resiliency while leveraging cloud resources for analytics and patient engagement, balancing data sovereignty with scalability.

What regulatory changes are most influencing ambulatory EHR purchasing decisions in 2025?

Providers are prioritizing systems that natively meet new information-blocking penalties, FHIR-enabled patient-access rules, and expanded electronic clinical-quality reporting requirements, making regulatory ready-made compliance a top selection factor.

How is artificial intelligence redefining clinician workflows in ambulatory settings?

Ambient listening and generative-text modules now convert doctor-patient conversations into structured notes, while predictive analytics surface next-best actions, reducing documentation burdens and enhancing clinical decision support

Which security strategies are healthcare organizations adopting after recent ransomware incidents?

Providers are moving toward zero-trust network designs, multi-factor authentication, continuous monitoring, and contractual shared-responsibility models with vendors to mitigate centralized cloud-data risks.

Why are small physician practices accelerating their shift to modern EHR platforms?

Subscription-based cloud offerings, templated implementations, and bundled revenue-cycle services lower upfront costs and IT complexity, letting small offices access capabilities once reserved for large health systems.

Page last updated on: