EHealth Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 317.64 Billion |

| Market Size (2031) | USD 661.35 Billion |

| Growth Rate (2026 - 2031) | 15.78% CAGR |

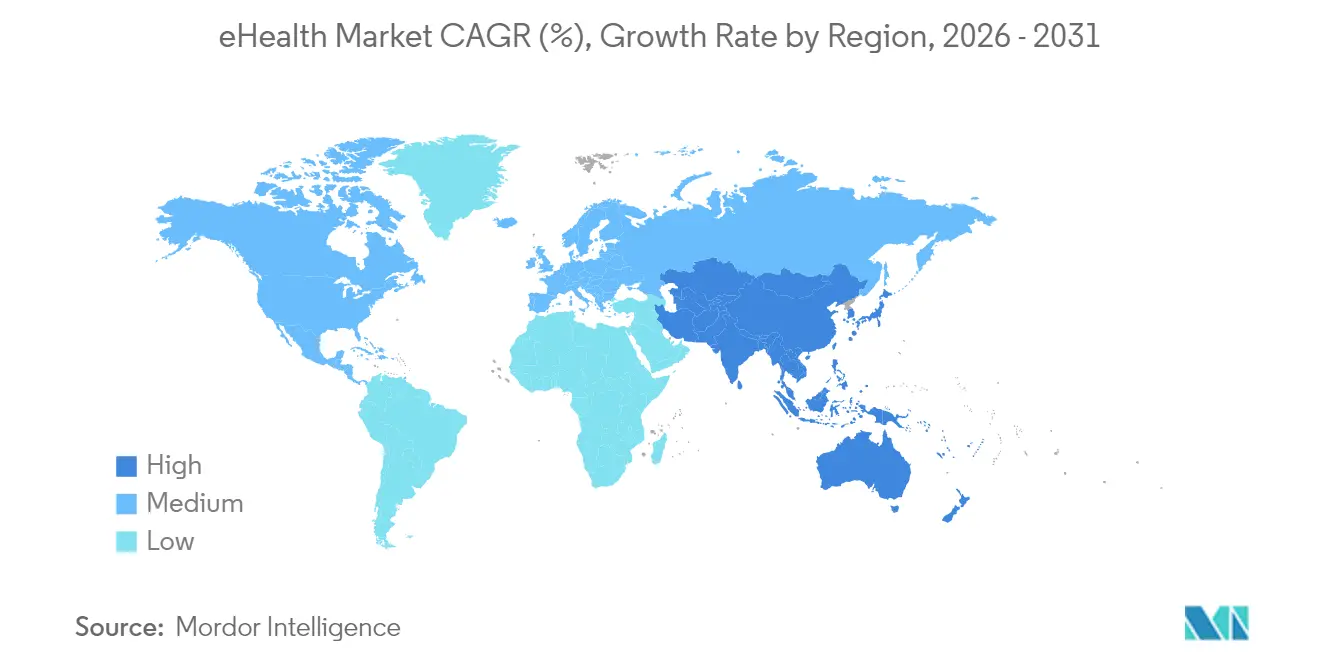

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

EHealth Market Analysis by Mordor Intelligence

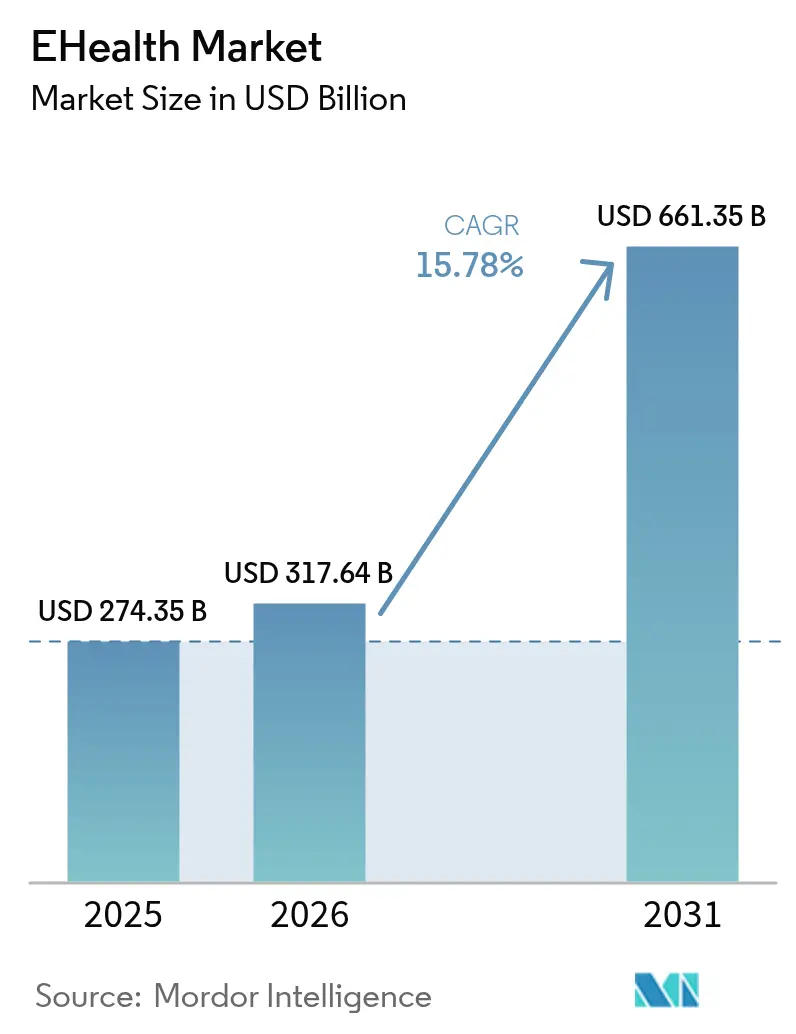

The eHealth market size was valued at USD 274.35 billion in 2025 and estimated to grow from USD 317.64 billion in 2026 to reach USD 661.35 billion by 2031, at a CAGR of 15.78% during the forecast period (2026-2031). This performance stems from rapid gains in connectivity, favorable legislation, and sustained investment in digital-first care pathways that let providers scale services without proportional increases in staff or physical infrastructure. Rising reimbursement for remote monitoring, wider 5G rollouts, and the integration of generative-AI assistants into clinical workflows further expand the addressable patient base, while growing consumer acceptance anchors long-run demand. Health-system mergers now dedicate high capital to IT modernisation, illustrating that digital capabilities have shifted from “nice to have” to “mission critical.” Still, data-security incidents and interoperability gaps temper near-term growth ambitions and oblige new spending on cyber-risk mitigation and data-exchange standards.

Key Report Takeaways

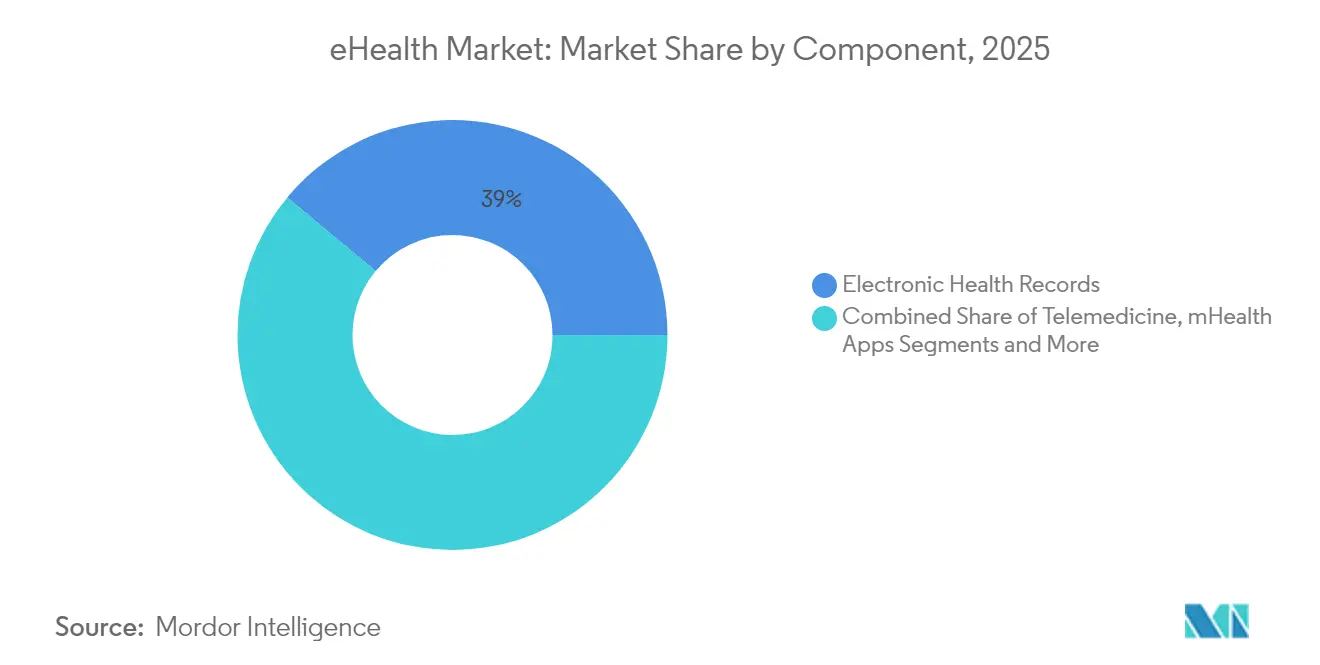

- By component, Electronic Health Records led with 38.95% revenue share in 2025; Telemedicine is poised for a 19.89% CAGR through 2031.

- By delivery mode, cloud-based platforms captured 52.10% of 2025 revenue, while hybrid solutions are projected to expand at 22.20% CAGR to 2031.

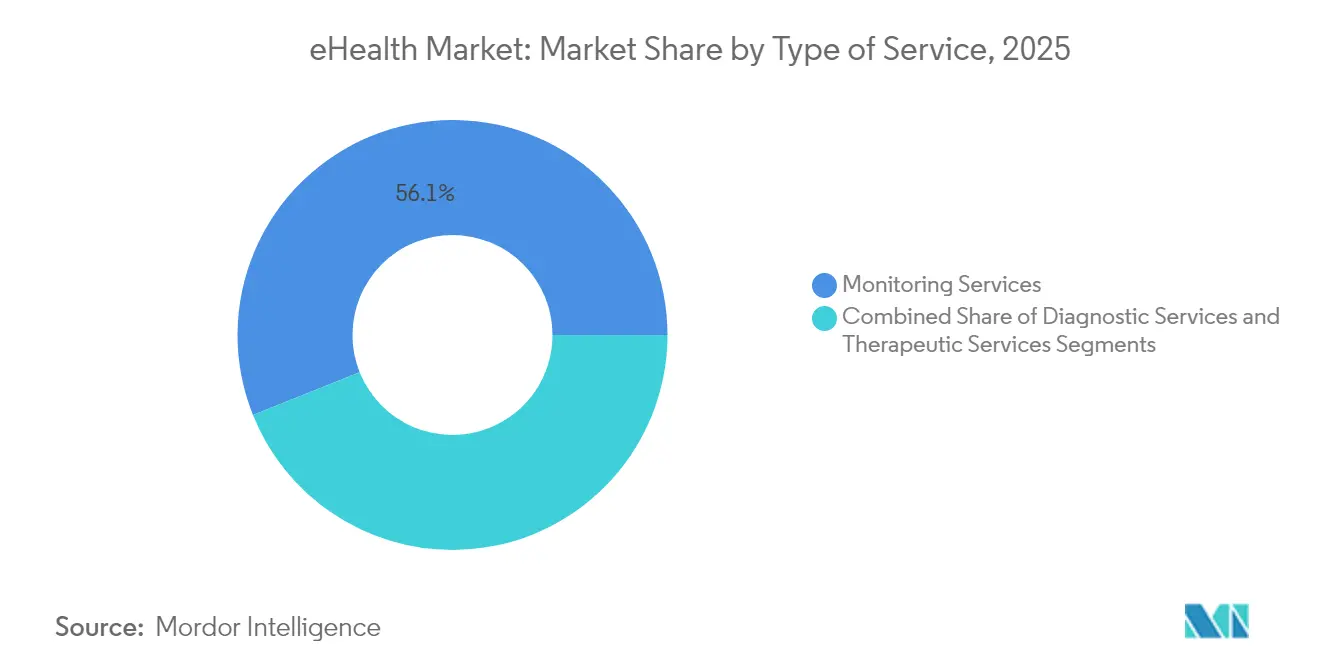

- By service type, monitoring accounted for 56.07% of 2025 revenue; diagnostic services are forecast to rise at an 18.28% CAGR to 2031.

- By end user, hospitals and health systems held 52.30% of 2025 revenue, yet patients and individual consumers are set for 19.32% CAGR through 2031.

- By geography, North America commanded 42.35% 2025 revenue, whereas Asia-Pacific is expected to deliver the fastest 20.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global EHealth Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Incentives For Digital Health Adoption | +4.2% | Global, with early gains in US, EU, Australia | Medium term (2-4 years) |

| Growing Prevalence Of Chronic Diseases Demanding Remote Monitoring | +3.8% | Global, concentrated in aging populations | Long term (≥ 4 years) |

| Expansion Of High‐Speed Connectivity (5G) Enabling Telehealth | +2.9% | APAC core, spill-over to North America & EU | Short term (≤ 2 years) |

| Integration Of Generative-AI Copilots Into EHR Workflows | +3.1% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Emergence Of Retail & Big-Tech Virtual Clinics | +2.3% | North America, selective expansion globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Incentives For Digital Health Adoption

Financial carrots and regulatory sticks continue to accelerate eHealth market penetration. The HTI-2 rule finalized by the U.S. Department of Health and Human Services penalizes information blocking and forces tighter interoperability, spurring hospital demand for standards-compliant upgrades[1]U.S. Department of Health and Human Services, “HHS Finalizes Rule Establishing Disincentives for Health Care Providers That Have Committed Information Blocking,” hhs.gov. Meanwhile, the European Health Data Space secured EUR 810 million to harmonize data exchange across 27 member states, offering vendors a single continental entry point. Australia’s 2023-2028 National Digital Health Strategy funds interoperability layers that link federal registries to state systems. Collectively, these programs shorten sales cycles, provide direct subsidy pools, and cement the convening power of governments in setting technical baselines. As compliance dates approach, provider budgets increasingly prioritize certified platforms, creating a pull-through effect for integration consultancies and cybersecurity vendors. The visible policy pipeline increases investor confidence, keeping capital flows robust even in tighter macro conditions.

Growing Prevalence Of Chronic Diseases Demanding Remote Monitoring

Rising incidence of diabetes, hypertension, and COPD shifts care toward continuous at-home oversight and generates recurring device and analytics revenues. Remote patient monitoring adoption reached 81% of U.S. clinicians by 2023 and delivered a 76% drop in 30-day readmissions among high-risk cohorts. Teladoc Health reports a threefold rise in diabetes-member engagement and a 0.4 reduction in A1c through predictive nudges, underscoring clinical validity. Wearable shipments are tracking 55% annual growth as sensors graduate from fitness tracking to FDA-cleared medical functionality. As insurers expand reimbursement codes, device makers bundle AI-powered triage layers that flag deterioration early and escalate only when clinically necessary, trimming utilization costs. High-speed cellular connectivity broadens eligible populations in rural areas, while cloud-native dashboards lower IT overhead for small practices, opening fresh sub-segments of the eHealth market.

Expansion Of High-Speed Connectivity (5G) Enabling Telehealth

Ultra-reliable low-latency networks unlock real-time use cases such as telesurgery and edge-based imaging analysis. The world’s first 5G remote robotic transcervical thyroidectomy linked surgeons 1,500 km apart with 99 ms latency, validating clinical safety thresholds[2]BMC Surgery, “5G Remote Robotic-Assisted Transcervical Thyroidectomy: The First Case Report in the World,” doi.org. University hospitals in Düsseldorf and Boston deployed private 5G to reduce packet loss that can jeopardize patient monitoring. Europe’s federally funded 6G Health consortium now tests augmented-reality assisted rounds, indicating a longer-run roadmap beyond current commercial networks. As spectrum auctions widen, rural broadband pilots in India and Indonesia demonstrate cost-effective tele-ICU models, reducing urban overflow. Vendors able to certify medical-grade network equipment gain a defensible niche while cloud platforms race to localize edge nodes for compliance. Collectively, improved bandwidth raises service quality thresholds and cements video consultation as a mainstream care modality rather than an emergency substitute.

Integration Of Generative-AI Copilots Into EHR Workflows

Large-language models embedded in clinical systems promise to convert onerous documentation into short voice commands and auto-drafted encounter notes. Stanford Health Care’s ChatEHR lets clinicians query patient histories conversationally, an early proof that search and summarization can shave hours off charting time. Oracle’s Clinical Digital Assistant integrates ambient voice capture to populate structured fields, tackling a pain-point cited by 41% of providers who spend over four hours daily on paperwork. GE HealthCare is co-building foundation models on AWS to accelerate imaging-workflow coding and reduce development cycles. Early pilots show documentation time savings near three hours per shift and improved accuracy, indirectly expanding appointment capacity. Regulatory sandboxes in the UK and Singapore fast-track clinical validation, pushing vendors to bake in bias-mitigation and audit trails from day one. These copilots are now a primary differentiator in EHR renewals, shaping a new competitive frontier across the eHealth market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Security & Privacy Concerns | -2.1% | Global, heightened in EU due to GDPR | Long term (≥ 4 years) |

| Interoperability Challenges Among Disparate Systems | -1.8% | Global, acute in fragmented markets | Medium term (2-4 years) |

| AI Algorithm Liability & Malpractice Insurance Gaps | -1.4% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Security & Privacy Concerns

Cyber incidents reached a record 677 major breaches in 2024, affecting 182.4 million individuals and highlighting persistent attack-surface expansion as devices proliferate. The Change Healthcare ransomware event alone disrupted claims processing nationwide, underscoring the systemic nature of third-party dependencies. Health records command premium dark-web prices because they carry immutable personal identifiers, attracting both cybercriminals and nation-state actors. The HHS cybersecurity strategy now proposes new HIPAA Security Rule standards, while the Health Care Cybersecurity Improvement Act offers funding for small practices to upgrade tools. EU regulators impose heavy fines for GDPR lapses, forcing multinationals to engineer data-minimization workarounds. Ongoing vulnerability management costs and rising cyber-insurance premiums erode margins, causing some providers to defer non-critical digital projects and slowing overall eHealth market adoption.

Interoperability Challenges Among Disparate Systems

A decade of policy pushes lifted U.S. hospital participation in data exchange from 23% to 70%, yet only 47% of clinicians report easy access to external patient information. Data-standard inconsistencies, vendor-specific APIs, and cost barriers hamper smaller practices more severely, perpetuating information silos. The Draft Federal FHIR Action Plan outlines a common interface approach, but implementation requires skilled development resources in short supply[3]HealthIT.gov, “Raising the Bar on Interoperability – A Decade of Data,” healthit.gov. Internationally, the European Health Data Space sets ambitious unification goals, yet cross-border data portability still confronts linguistic, ethical, and consent hurdles. Fragmentation complicates longitudinal analytics and undermines AI model accuracy, prompting payers and life-science companies to invest in data-normalization layers that inflate project costs. Until harmonization improves, the friction-filled ecosystem will clip a portion of the forecast CAGR for the eHealth market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: EHR Dominance Meets Telemedicine Acceleration

Electronic Health Records generated the largest 38.95% share of the eHealth market in 2025 as regulatory compliance, incentives, and enterprise-grade functionality kept procurement pipelines robust. Cloud-enabled upgrades bundled with analytics and population-health modules have renewed growth, while embedded generative-AI copilots from Epic and Oracle compress documentation time and attract multi-year license renewals. The component’s lead positions vendors to cross-sell revenue-cycle and clinical-decision add-ons, sustaining average deal sizes. Telemedicine posted the fastest 19.89% CAGR outlook because post-pandemic consumer familiarity, payment parity laws, and scalable video infrastructure lowered adoption barriers. Amazon’s consolidation of Clinic into One Medical signals that platform integration and national brand trust will dictate competitive advantage going forward.

Fast-moving mHealth apps combine smartphone cameras, edge AI, and low-cost sensors to support dermatology, ophthalmology, and mental-health triage, deepening consumer engagement. Clinical Decision Support tools embedded in imaging platforms record higher sensitivity and specificity, reinforcing demand for algorithm training datasets. e-Prescribing exhibits steady expansion under mandatory electronic-controlled-substance regulations, but remains hampered by inconsistent pharmacy system upgrades. Together, diversified component innovation keeps the eHealth market vibrant and spurs ecosystem partnerships.

By Delivery Mode: Cloud Leadership Drives Hybrid Innovation

Cloud platforms supplied 52.10% of 2025 revenue and anchor modernization roadmaps because they eliminate capital-intensive data centers and power automatic patching, essential to cyber-risk management. Microsoft Cloud for Healthcare exemplifies how shared responsibility models and responsible-AI toolchains de-risk adoption while compressing deployment timelines. Hybrid solutions, however, hold the fastest 22.20% CAGR forecast, reflecting provider desire to retain sensitive workloads on-premise while off-loading non-PHI analytics to hyperscale services. Vendors now pre-package connectors that let organizations shuttle data across environments without refactoring legacy code, smoothing migration trajectories.

On-premise deployments persist in military hospitals, genomic research institutes, and jurisdictions mandating data localization, though their eHealth market share continues to erode as total cost of ownership rises. The hybrid paradigm also aids multi-cloud strategies, preventing lock-in and aligning compute location with regulatory risk profiles. As cloud regions proliferate and sovereign-cloud offerings mature, the addressable base for fully managed subscriptions expands further, reinforcing a long-run shift toward consumption-based pricing models.

By Type of Service: Monitoring Prevalence Supports Diagnostic Expansion

Monitoring services represented 56.07% revenue in 2025, propelled by Medicare reimbursement and chronic-condition prevalence. Remote Patient Monitoring platforms demonstrated a 76% fall in 30-day readmissions, underscoring economic value to payers and hospitals. The segment’s dominance anchors the largest eHealth market size contribution among all service categories. AI-powered dashboards triage alerts, enabling clinicians to oversee larger patient panels without quality loss.

Diagnostic services hold the fastest 18.28% CAGR as AI models shorten radiology turnaround and boost detection accuracy. Tele-radiology benefits from 5G transfer speeds that support high-resolution imaging, while tele-pathology leverages digital microscopy for expert remote reads. Therapeutic and other services, including digital therapeutics and virtual rehabilitation, grow from a small base amid reimbursement uncertainties but gain credibility from FDA clearances. Balanced growth across service lines diversifies revenue sources and improves the resilience of the overall eHealth market.

By End User: Hospital Systems Anchor Consumer Growth

Hospitals and health systems contributed 52.30% of 2025 revenue and remain the backbone customers because they control large budgets and must meet statutory data-sharing obligations. M&A activity, such as Sanford-Marshfield’s USD 500 million IT modernization, showcases capital allocation toward integrated platforms that consolidate clinical, revenue-cycle, and population-health modules. Their scale requirements sustain multi-year enterprise deals and service contracts.

Patients and individual consumers post a 19.32% CAGR, the fastest among end users, propelled by subscription telehealth, home-testing kits, and wellness ecosystems. Retailers like Costco and Best Buy bundle primary-care visits and connected devices, illustrating shifting power toward consumer-directed channels. Payers invest in digital engagement portals that integrate benefits navigation with condition-management programs, while pharma sponsors digital endpoints to accelerate decentralized trials. The expanding consumer base spreads the eHealth market’s risk profile and compels interface simplicity and omni-channel access.

Geography Analysis

North America produced 42.35% of 2025 revenue, driven by mature reimbursement frameworks, a high clinician-to-patient ratio, and aggressive investment in AI-enabled clinical decision support. The HTI-2 rule and federal AI strategic plan signal long-term regulatory stability, encouraging provider spending and venture capital inflows. Canada advances provincial interoperability initiatives, and cross-border telehealth partnerships allow winter-surge overflow management, while Mexico scales cloud-hosted records to underserved regions. Ongoing cyber-attacks remain a regional restraint, prompting higher security budgets that inflate total cost of ownership for eHealth deployments.

Asia-Pacific delivers the highest 20.22% CAGR, with China’s 5G medical pilots, India’s insurance-backed digital health stack, and Australia’s federally funded interoperability plan as key accelerants. Successful remote robotic surgery across 1,500 km in China validates ultra-low-latency care models and burnishes national AI ambitions bmc. Singapore embeds IoT sensors into public-hospital wards for predictive analytics, while Thailand pursues virtual-care to bridge specialist shortages. Government-led sandbox programs streamline approvals and shorten commercial lead times, sustaining investor confidence in the region’s eHealth market.

Europe maintains steady expansion anchored by EUR 810 million earmarked for the European Health Data Space and the risk-based EU AI Act slated for phased compliance by 2027. Germany’s 6G Health project positions Europe at the forefront of next-generation connectivity, and the UK’s sector-specific AI governance introduces differentiated oversight paths for clinical algorithms. Nordic nations pilot personal-data wallets that give citizens granular consent controls, while Southern European providers upgrade cloud capacity to offset clinician shortages. The regulatory push for trust and safety enhances adoption intent but also raises compliance costs, compelling smaller vendors to seek partnership or acquisition.

Competitive Landscape

The eHealth market features a converging field where legacy EHR vendors, big-tech entrants, and AI-first start-ups vie for platform primacy. Incumbents like Epic, Oracle Cerner, and athenahealth defend share through broad functionality and entrenched client bases, layering generative-AI assistants to modernize user experience. Amazon reorganized its health arm into six focused units, showcasing strategic pivot toward an integrated virtual-first offering and signaling that platform breadth, not physical footprint, will dictate future dominance. Walmart’s exit from clinic build-outs and CVS’s telehealth emphasis confirm that retail players prioritize scalable digital touchpoints over brick-and-mortar risk.

White-space opportunities abound in cross-vendor data-exchange middleware, algorithm-liability insurance, and home-based acute-care orchestration. Transcarent absorbed Accolade in a USD 621 million merger to assemble an AI-powered advocacy engine covering 20 million members, illustrating a shift toward navigation-centric value propositions. GE HealthCare collaborates with AWS to train imaging foundation models, while Cognizant pairs with Google Cloud on sector-specific LLM toolkits, underscoring the premium placed on cloud GPU access and model-lifecycle governance. Mid-tier players differentiate through narrow clinical specialties, such as Zimmer Biomet’s co-marketing with RevelAi for ortho-outcomes management, proving that vertical depth can counter horizontal platform scale.

Competition also unfolds in cybersecurity posture and regulatory readiness. Vendors that offer turnkey HIPAA and GDPR compliance, zero-trust architectures, and auditable AI pipelines win RFP points and shorten sales cycles. As the EU AI Act deadlines near, compliance services become bundled differentiators. Overall, the pace of innovation forces continuous road-mapping, while capital markets reward firms able to balance revenue growth with disciplined go-to-market spending in the expanding eHealth market.

EHealth Industry Leaders

athenahealth Inc.

Veradigm LLC

Oracle Cerner

Epic Systems Corporation

Teladoc Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Emory Healthcare invested USD 10 million in Guidehealth to advance AI-driven care solutions.

- June 2025: Stanford Health Care launched ChatEHR, allowing clinicians to converse with medical records during pilot deployment.

- January 2025: Teladoc Health partnered with Amazon’s Health Benefits Connector for cardiometabolic programs, letting eligible users enroll in diabetes and hypertension services.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the eHealth market as the aggregate spending on software platforms, connected devices, and cloud-enabled services that let licensed clinicians, payers, and patients exchange medical data, manage workflows, and deliver virtual care outside traditional in-person encounters. Values are reported in USD at end-user price levels, covering solutions such as electronic health records, telemedicine portals, mHealth apps, e-prescriptions, clinical decision support, and related implementation services across 17 countries tracked by Mordor Intelligence.

Scope exclusion: Stand-alone wellness wearables or fitness apps that never interface with regulated healthcare systems sit outside this sizing.

Segmentation Overview

- By Component

- Electronic Health Records

- Telemedicine

- mHealth Apps

- Clinical Decision Support

- e-Prescribing

- Other Components

- By Delivery Mode

- Cloud-based Solutions

- On-premise Solutions

- Hybrid Solutions

- By Type of Service

- Monitoring Services

- Remote Patient Monitoring

- Chronic Disease Management

- Diagnostic Services

- Tele-radiology

- Tele-pathology

- Therapeutic Services

- Digital Therapeutics

- Virtual Rehabilitation

- Monitoring Services

- By End User

- Hospitals & Health Systems

- Insurance Companies & Payers

- Patients & Individual Consumers

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts then conduct expert interviews with hospital CIOs, telehealth insurers, and digital therapeutics start-ups across North America, Europe, Asia-Pacific, and GCC markets. These conversations validate unit economics, reveal reimbursement inflection points, and surface regional nuances that raw desk data misses, letting us tighten every assumption.

Desk Research

We begin by harvesting public datasets from tier-1 sources such as WHO Digital Health Observatory, OECD Health Stats, US ONC interoperability dashboards, European eHealth Network reports, and national telecom regulators that publish broadband and smartphone penetration. Regulatory filings, 10-Ks, and investor decks enrich pricing and rollout timelines, while peer-reviewed journals highlight adoption barriers. Paid repositories including D&B Hoovers and Dow Jones Factiva help verify revenue splits and funding flows for key vendors. The sources listed illustrate our coverage; many additional publications informed the evidence base.

Market-Sizing & Forecasting

A top-down model converts national health expenditure into the addressable digital share through metrics such as EHR penetration, average teleconsults per capita, 4G/5G coverage, remote monitoring enrollment, and cloud pricing trends, which are then benchmarked against selective bottom-up checks on supplier revenues and sampled ASP × volume data. Gaps in bottom-up inputs are bridged by interpolation using adoption curves aligned to comparable country clusters. Multivariate regression, refreshed annually, projects each driver and feeds scenario analysis that yields our 2025-2030 outlook.

Data Validation and Update Cycle

Outputs face variance screens against external spending indices, after which a senior reviewer signs off. Reports refresh every year, with mid-cycle updates if major policy or funding shocks arise, and an analyst re-runs the model before each client delivery to keep insights current.

Why Our Ehealth Baseline Earns Trust

Published estimates often diverge because firms pick different product baskets, exchange-rate dates, and refresh cadences.

Key gap drivers include whether home-grown patient portals are counted, how aggressively unproven AI tools are projected, and if subsidies announced but not appropriated find their way into revenue pools, which can inflate numbers beyond realistic spending.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 274.35 B (2025) | Mordor Intelligence | - |

| USD 411.04 B (2024) | Global Consultancy A | Includes consumer fitness apps and counts booked telehealth reimbursements twice |

| USD 484.83 B (2025) | Research Firm B | Uses list prices without regional ASP adjustment and applies uniform 18% CAGR across all regions |

| USD 176.29 B (2025) | Industry Association C | Excludes cloud implementation services and small-practice EHR upgrades |

The comparison shows that when scope creep or overly narrow definitions shift totals, decision-makers can rely on Mordor's carefully bounded variables, transparent driver logic, and annual refresh cycle for a balanced, reproducible baseline.

Key Questions Answered in the Report

How large is the eHealth market today?

The eHealth market size reached USD 317.64 billion in 2026 and is forecast to climb to USD 661.35 billion by 2031 at a 15.78% CAGR.

Which component leads the eHealth market?

Electronic Health Records command the largest 38.95% share, reflecting their central role in digitizing clinical workflows.

Which region is growing the fastest in eHealth adoption?

Asia-Pacific is projected to post the highest 20.22% CAGR through 2031, propelled by 5G rollouts and national digital-health programs.

Which is the fastest growing region in EHealth Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

What service type generates most revenue in the eHealth market?

Monitoring services account for 56.07% of 2025 revenue, underpinned by expanding remote patient monitoring reimbursement.

What is the biggest restraint to eHealth market growth?

Data security and privacy concerns exert the strongest negative impact, clipping the forecast CAGR by an estimated 2.1%.

How will generative AI influence the eHealth industry?

Generative-AI copilots integrated into EHRs are already saving clinicians several hours of documentation per day and will become a major buying criterion in system renewals.

Page last updated on: