United States EHealth Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

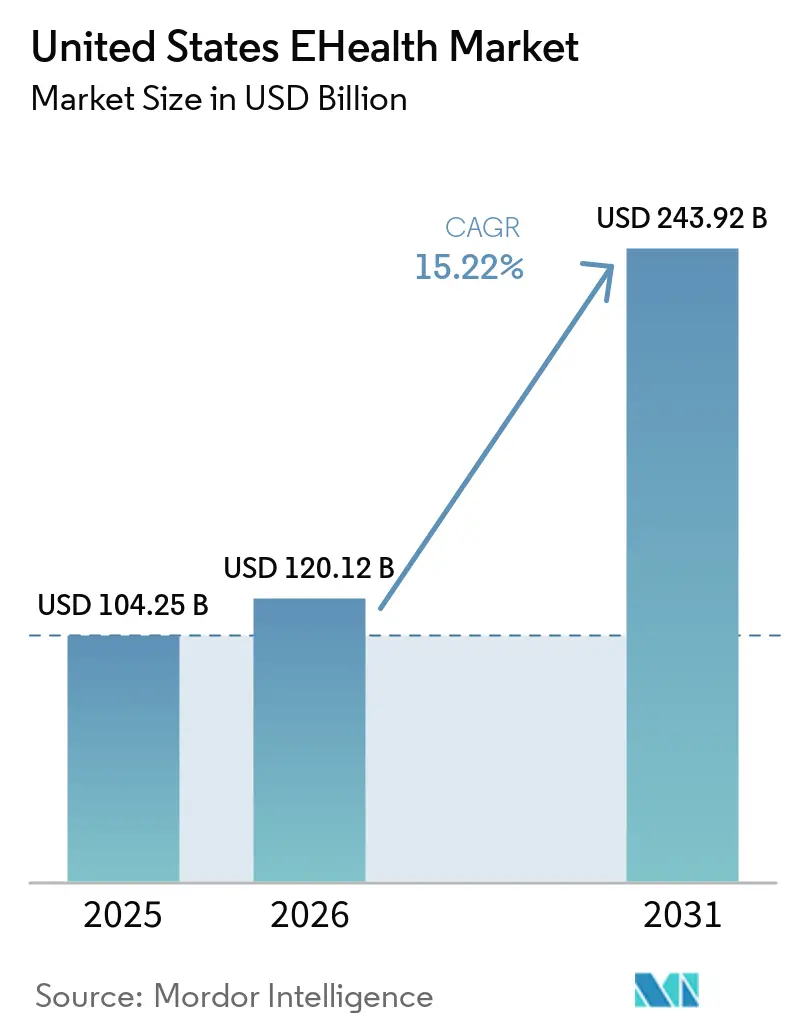

| Base Year Market Size (2025) | USD 104.25 Billion |

| Market Size (2026) | USD 120.12 Billion |

| Market Size (2031) | USD 243.92 Billion |

| Growth Rate (2026 - 2031) | 15.22% CAGR |

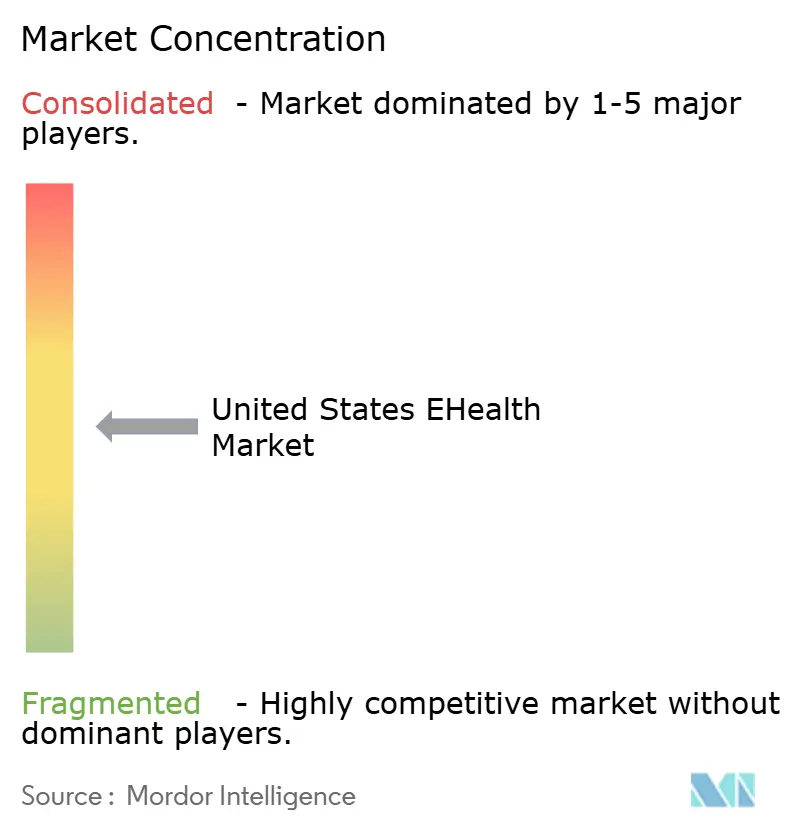

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States EHealth Market Analysis by Mordor Intelligence

The United States EHealth Market size is expected to grow from USD 104.25 billion in 2025 to USD 120.12 billion in 2026 and is forecast to reach USD 243.92 billion by 2031 at 15.22% CAGR over 2026-2031.

The market is moving into a more durable phase because the CMS ACCESS model turns selected AI-enabled chronic care tools into reimbursable care delivery channels for Original Medicare, which changes how providers and vendors plan recurring revenue. That shift matters because outcome-aligned payments reward measurable patient results instead of simple service volume, which gives the United States eHealth market a steadier payment framework than the earlier telehealth expansion cycle. Cloud maturity, wider use of interoperable exchange frameworks, and stronger patient demand for convenient digital care are also raising the operating value of scalable platforms across health systems and payer networks in the United States eHealth market. Competitive conditions remain balanced rather than extreme because a limited group of enterprise platform vendors controls core clinical workflow layers, while many specialized digital health providers still compete across narrow use cases, disease programs, and employer or insurer channels in the United States eHealth market. Growth is still constrained by cybersecurity exposure and slow migration away from legacy interoperability infrastructure, which means the United States eHealth market must expand while providers and vendors absorb higher security scrutiny and more complex data architecture transitions.

Key Report Takeaways

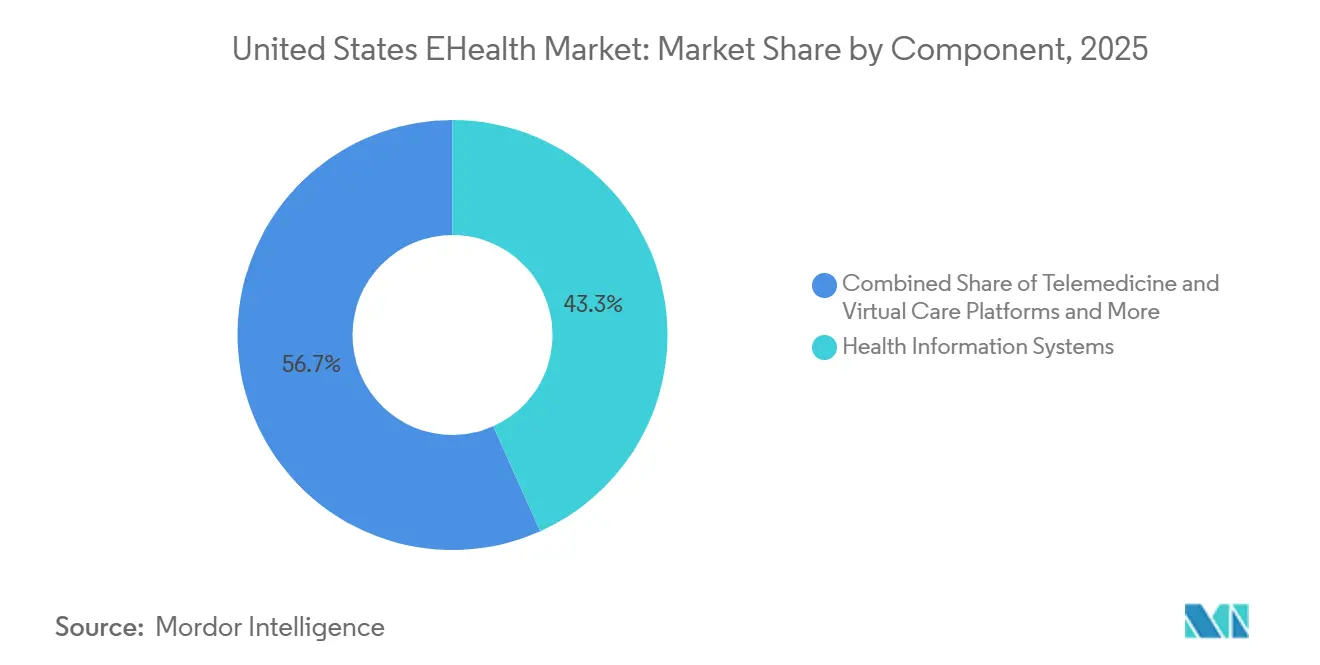

- By component, Health Information Systems accounted for 43.31% of the United States eHealth market size in 2025, while Telemedicine & Virtual Care Platforms is projected to expand at a 19.38% CAGR through 2031.

- By delivery mode, Cloud-based Solutions held 52.24% of the United States eHealth market share in 2025, while Hybrid Solutions is projected at a 20.52% CAGR through 2031.

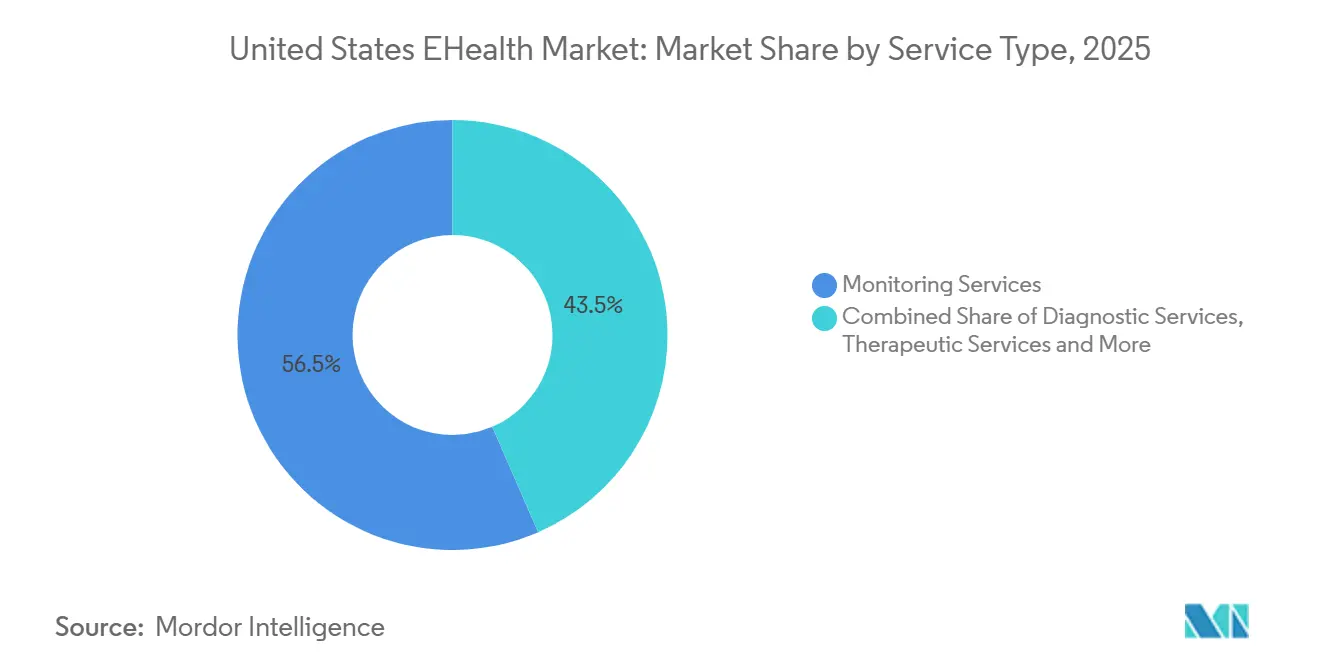

- By service type, Monitoring Services commanded 56.52% share of the United States eHealth market size in 2025, while Diagnostic Services is projected to grow at an 18.25% CAGR through 2031.

- By end user, Healthcare Providers held 48.24% of the United States eHealth market share in 2025, while Patients & Individual Consumers is forecast to expand at an 18.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States EHealth Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement and Federal Digital-Health Incentives | +2.8% | National, acute in rural and underserved markets where Medicare and Medicaid are dominant payers | Medium term (2-4 years) |

| Chronic Disease and Home-Monitoring Demand | +2.5% | National, with highest pressure in the South, Midwest, and Appalachia | Long term (≥ 4 years) |

| Cloud Migration of Virtual-Care Stacks | +2.2% | National, led by Northeast and West Coast integrated delivery networks | Medium term (2-4 years) |

| Value-Based Care and Patient-Engagement Analytics | +2.0% | National, led by ACO-dense Northeast and Midwest integrated health systems | Long term (≥ 4 years) |

| TEFCA and Information-Blocking Enforcement | +1.5% | National | Short term (≤ 2 years) |

| Ambient AI Documentation Copilots | +2.0% | National, with early adoption concentrated in large academic and multisite hospital systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reimbursement and Federal Digital-Health Incentives

Federal reimbursement design is changing the operating base of the United States eHealth market because the current policy shift reaches beyond small pilot programs and into recurring care delivery economics. The CMS Innovation Center's ACCESS model became active on July 5, 2026, and it introduced outcome-aligned payments across hypertension, type 2 diabetes, chronic musculoskeletal pain, and depression for Original Medicare beneficiaries over a 10-year period. That payment structure matters because it ties revenue to measurable clinical outcomes instead of service volume, which raises the value of platforms that can document performance at the population level. The United States eHealth market also benefits when those platforms can connect data across settings, since enforcement against information blocking and TEFCA-backed exchange growth make measurable outcomes easier to document and transmit. This pushes vendors to build around auditability, interoperability, and payment performance instead of one-time software deployment. It also makes partnerships with providers and payers more durable because the commercial case now rests on reimbursed clinical value rather than on convenience alone in the United States eHealth market[1]Centers for Medicare & Medicaid Services, “ACCESS (Advancing Chronic Care with Effective, Scalable Solutions) Model,” CMS Innovation Center, cms.gov.

Chronic Disease and Home-Monitoring Demand

Chronic disease remains one of the clearest demand anchors for the United States eHealth market because remote monitoring is directly tied to conditions that require continuous follow-up instead of occasional visits. A peer-reviewed, EHR-integrated remote patient monitoring program for hypertension and multiple chronic conditions delivered systolic blood pressure reductions of up to 16.01 mmHg, which supports continued provider investment in structured monitoring workflows. More than two-thirds of Medicare beneficiaries carry at least one condition targeted by the ACCESS model, so the United States eHealth market already has a built-in population base for home monitoring services. This demand is wider than device adoption alone because providers need workflows, escalation pathways, and reimbursement pathways that can sustain long-term use. As a result, monitoring is becoming less of an optional digital add-on and more of a core layer in chronic care management for health systems, payers, and patient-facing programs in the United States eHealth market. The strongest opportunity sits where provider demand already exists but payment stability has only recently improved, because those organizations can move faster than groups that still need to build operating processes from scratch.

Cloud Migration of Virtual-Care Stacks

Cloud migration is shaping competitive position in the United States eHealth market because AI-enabled care tools depend on scalable compute, storage, and integration layers that are hard to support through isolated on-premise stacks. WellSpan Health stated in January 2026 that it is migrating its full technology portfolio to AWS, and the system linked that move directly to AI-powered tools intended to return time to clinical and corporate teams. The logic goes beyond cost because cloud-native environments are better positioned to support modern API exchange, multi-site workflows, and the inference demands of ambient AI and imaging support tools. Hippocratic AI's Polaris system reached 10 million patient calls with a 99.9% clinical safety score on DigitalOcean's AI-native cloud, which shows how large-scale healthcare AI workloads are already being run in cloud environments rather than only in test settings. This gives cloud migration a direct bearing on service quality, deployment speed, and vendor relevance across the United States eHealth market. It also strengthens the position of vendors that can manage hybrid reality during transition instead of treating migration as a one-step event.

Value-Based Care and Patient-Engagement Analytics

The United States eHealth market is also gaining support from platforms that link patient engagement more directly to financial performance, especially in settings where reimbursement depends on documented care quality and patient follow-through. IKS Health introduced MyCareHub in April 2026 as an agentic AI platform that uses behavioral modeling, longitudinal patient memory, and orchestration logic to personalize outreach. The platform reported a 4.7% increase in total patient collections and a 9.4% increase in patient payments per visit, which shows why providers are starting to view engagement analytics as operating leverage rather than as a reporting expense. The shift is important because it broadens the buying case beyond compliance teams and pulls finance, operations, and clinical leadership into the same decision cycle. It also fits the United States eHealth market where value-based programs increasingly reward measurable engagement, timely follow-up, and reduced gaps in care. Over time, that makes predictive outreach and workflow automation more central to revenue protection, especially for organizations managing large attributed populations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity and HIPAA Exposure | -1.5% | National, acute in health systems with high third-party vendor dependencies | Short term (≤ 2 years) |

| Legacy Interoperability Bottlenecks | -1.0% | National, amplified in rural and smaller health systems with aging infrastructure | Medium term (2-4 years) |

| Clearinghouse Concentration and Cyber Single-Point Failure | -0.9% | National | Short term (≤ 2 years) |

| AI Liability and Malpractice Coverage Gaps | -0.9% | National, with earliest compliance pressure in California and Utah | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity and HIPAA Exposure

Cybersecurity is one of the clearest limiting factors for the United States eHealth market because the same connectivity that enables digital care also widens exposure to shared vendors, clearinghouses, and cloud-linked workflows. The Change Healthcare ransomware attack confirmed 192.7 million affected individuals, making it the largest healthcare data breach on record in the material provided. The same event hit a clearinghouse that processes nearly 15 billion transactions annually, which showed how concentration at a single infrastructure layer can disrupt much broader care and payment activity. The operational effect was severe because 74% of hospitals reported direct patient care disruptions and 94% reported economic strain after the incident. That experience raises diligence costs across vendor selection, supply chain oversight, and business continuity planning for participants in the United States eHealth market[2]Julia Adler-Milstein et al., “Lessons From the Change Healthcare Ransomware Attack,” JAMA Health Forum, jamanetwork.com. It also keeps buyers focused on resilience and vendor dependency risk, even when a platform has strong clinical or workflow advantages.

Legacy Interoperability Bottlenecks

Legacy interoperability remains a practical brake on the United States eHealth market because many digital tools still have to operate alongside older architectures rather than in a fully modern exchange environment. TEFCA exchange volumes reached nearly 500 million records by February 2026, which proves national data sharing is scaling, but it also raises the pressure on providers and vendors whose systems still depend on older interface structures. In practice, the transition stretches timelines because organizations must map data, preserve workflows, and maintain mixed environments while they move toward FHIR-native operations. This slows implementation of AI-enabled tools that depend on timely and normalized data inputs, which weakens some of the speed advantages that vendors promote in the United States eHealth market. The issue is not only technical because state-level scrutiny of AI-supported clinical decisions is also rising, with California's AB-2575 making it harder for developers of AI-based clinical decision support systems to shift responsibility entirely onto clinicians who do not override AI output. That means vendors face a longer path to scaled adoption when integration burdens and accountability expectations rise at the same time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Health Information Systems Anchor Revenue While Virtual Platforms Redefine Growth

Health Information Systems retained 43.31% of 2025 revenue, which reflects the entrenched role of EHR and EMR platforms, health information exchange tools, population health systems, and patient engagement software across the United States eHealth market. The segment remained durable because replacement decisions still carry high disruption costs for providers, even when newer tools enter with stronger AI features. Oracle launched a new AI-driven EHR for ambulatory providers in August 2025 with voice-first and contextual AI functions, and the company stated that acute care expansion is planned in 2026[3]Oracle Corporation, “Oracle Ushers in New Era of AI-Driven Electronic Health Records,” Oracle Newsroom, oracle.com. That move raises the competitive bar for vendors trying to win enterprise clinical workflow positions because core systems are now expected to add intelligence directly into the record environment rather than through bolt-on products. Population health management remains a meaningful spending pocket because organizations increasingly need broader risk visibility, including data that supports contract performance and coordinated care.

Health Information Exchange is also gaining more strategic importance because TEFCA exchange volume climbed to nearly 500 million records by February 2026 from a far smaller base in January 2025, which supports the business case for interoperable data infrastructure as a long-term moat. Telemedicine & Virtual Care Platforms are the fastest-growing component segment and are projected at a 19.38% CAGR through 2031, reflecting their central role in access expansion across employer programs, mental health delivery, and chronic care support in the United States eHealth industry. Omada Health reported Q1 2026 revenue of USD 78 million and 1.02 million total members, with all 3 leading U.S. pharmacy benefit managers as partners, which shows how virtual platforms are scaling through payer and benefit channels rather than only through traditional provider contracts. mHealth applications and ambient AI documentation are also moving closer together, and Suki's ambient notes reached general availability across athenahealth's network in May 2025 after use in more than 60,000 encounters during beta. This pattern suggests the United States eHealth market is rewarding components that can fit naturally into existing provider and patient channels instead of remaining standalone tools.

By Delivery Mode: Cloud Consolidates Its Lead While Hybrid Architectures Outpace Both Extremes

Cloud-based Solutions accounted for 52.24% of revenue in 2025, which reflects how strongly the United States eHealth market has shifted toward scalable infrastructure for storage, analytics, interoperability, and AI processing. The lead is tied to practical operating needs because systems that want to run virtual care, ambient documentation, and multi-site analytics at scale need infrastructure that can expand without constant hardware refresh cycles. WellSpan Health's January 2026 decision to migrate its full technology portfolio to AWS shows that cloud transition is now being treated as institutional strategy rather than a narrow IT upgrade. That decision also reflects how cloud environments support broader AI adoption, since organizations can pair data movement with new clinical and administrative tools instead of managing those efforts separately. For the United States eHealth market, this keeps cloud at the center of delivery strategy even when providers still retain some sensitive or deeply embedded systems on site.

Hybrid Solutions are projected to grow at a 20.52% CAGR through 2031, which makes them the fastest-growing delivery mode because mixed architectures are becoming the normal operating state rather than a short temporary bridge. Health systems still need to connect regulated clinical applications, legacy interfaces, and newer AI layers, so full migration rarely occurs in one cycle. On-premise Solutions continue to hold a smaller but persistent role in federal systems and organizations with tighter deployment constraints, which prevents a simple cloud-only transition path. The ONC's HTI-5 proposed rule published in December 2025 proposed removal of 34 certification criteria and estimated USD 1.53 billion in compliance cost savings for certified developers, which could reduce transition burdens for smaller health IT vendors over time. Taken together, these conditions mean the United States eHealth industry is likely to keep favoring cloud-led models, while hybrid deployment remains the fastest route for real-world scaling.

By Service Type: Monitoring Services Dominate As AI-Driven Diagnostics Accelerates

Monitoring Services commanded 56.52% of 2025 service-type revenue, which shows that the largest revenue base in the United States eHealth market still comes from ongoing observation of patients rather than one-time interactions. Remote patient monitoring, chronic disease management, and wellness monitoring have all benefited from the simple fact that large patient groups need repeated follow-up across Medicare, Medicaid, and commercial populations. A peer-reviewed program for hypertensive patients with comorbidities delivered systolic blood pressure reductions of up to 16 mmHg, reinforcing the clinical value of structured monitoring models. Wellness monitoring is also broadening because GLP-1 care programs now combine medication adherence, biometric tracking, and coaching in ways that move consumer health activity closer to formal chronic care management. The ACCESS model adds a longer operating horizon for selected chronic conditions, which better matches the recurring workflow and review cycles that monitoring platforms need to plan staffing and technology investment.

Diagnostic Services is the fastest-growing service segment and is projected to expand at an 18.25% CAGR through 2031, driven by AI-supported triage, tele-radiology, and tele-pathology that improve turnaround without always requiring specialist co-location. The FDA reported that more than 1,000 AI-enabled medical devices have been authorized, which shows that the regulatory path for clinical AI tools is moving further into routine use. Therapeutic Services are also drawing strategic interest, especially in behavioral health, where Universal Health Services agreed to acquire Talkspace for USD 835 million in March 2026. Administrative & Workflow Services remain important because HHS projected USD 19.2 billion in administrative savings over the next decade from real-time prior authorization standards, which supports ongoing demand for digital workflow tools alongside direct care services. This mix keeps the United States eHealth market balanced between mature recurring-monitoring revenue and faster-growing AI-enabled clinical support areas.

By End User: Healthcare Providers Lead by Share While Consumer-Facing Models Accelerate

Healthcare Providers retained 48.24% of 2025 end-user revenue, which confirms that the largest spending base in the United States eHealth market still sits with hospitals, health systems, clinics, and physician organizations. Providers remain the main buyers of EHR platforms, ambient documentation tools, clinical decision support systems, and population health infrastructure because these tools are most valuable when they connect directly with workflow and reimbursement operations. The direction of spend is shifting from isolated department tools toward enterprise AI orchestration, and Epic's HIMSS 2026 rollout of Agent Factory and Curiosity supports that move by giving health systems a way to build and deploy autonomous AI agents within existing environments. Epic also stated that more than 85% of its customer base now actively uses its AI tool suite, which suggests adoption has moved beyond experimentation in a large installed base. Payers remain the second-largest end-user group because they continue to invest in prior authorization automation, risk stratification, and member engagement tools that can influence utilization and quality performance.

Patients & Individual Consumers are the fastest-growing end-user segment, with projected growth of 18.83% through 2031, as direct-to-consumer telehealth, mental health applications, wearable-linked monitoring, and GLP-1 programs keep shifting more decision power toward individuals in the United States eHealth market. Hims & Hers announced in February 2026 that it agreed to acquire Eucalyptus, which extends its digital health platform into additional countries while building on U.S. consumer care economics. At the same time, Omada Health's relationships with the 3 leading U.S. pharmacy benefit managers show that consumer-facing digital care is often distributed through employer and insurer channels instead of only through direct app marketing. This means the United States eHealth market is expanding consumer reach without removing the influence of institutional buyers, which keeps hybrid B2B2C distribution central to growth.

Geography Analysis

The United States eHealth market does not expand evenly across the country because regional differences in infrastructure, clinical capacity, and regulatory pressure shape adoption patterns in distinct ways. The Northeast remains one of the most advanced areas for enterprise digital health deployment because it combines dense academic medical center networks with stronger health IT maturity and value-based contracting activity. That environment makes the region a frequent early buyer of health information exchange tools, population health analytics, and patient engagement platforms that depend on mature workflows and data-sharing discipline. Leading health systems in digitally advanced regions are also moving earlier on ambient AI documentation, and the American Medical Association reported that University of Iowa Health Care reached 220,000 patient encounters with Nabla's platform within roughly 6 months of system-wide use, while clinician burnout was estimated to have fallen by 30%. California adds another important layer because AB-2575 establishes that developers of AI-based clinical decision support systems cannot rely on clinician failure to override AI output as a complete break in liability, which influences product design choices well beyond one state.

The South and Midwest show a different growth pattern in the United States eHealth market because chronic disease burden, care access gaps, and large Medicare and Medicaid populations create stronger demand for remote care and monitoring. The ACCESS model focuses on hypertension, diabetes, chronic musculoskeletal pain, and depression, which aligns closely with demand conditions in many Southern and mid-Atlantic care settings as the model begins in the second half of 2026. Rural and frontier parts of the Midwest and Mountain West also depend more heavily on telehealth for psychiatry follow-up, dermatology, and chronic disease management because specialist supply is structurally limited. Those patterns give the United States eHealth market a durable base in areas where virtual care is tied to necessity and payer support, not just convenience.

Smaller regional markets, including the Mountain West, Pacific Northwest, and rural Mid-Atlantic, are gaining from federal support that extends beyond the largest urban systems in the United States eHealth market. ASTP and ONC highlighted 9 Behavioral Health IT pilot programs supported by more than USD 20 million across 45 exchange partners in 9 states, which shows that federal investment is helping bring exchange capability into underserved areas. That funding reduces the interoperability gap between community providers and large systems, which makes more regional providers reachable for eHealth vendors over time. In practical terms, this widens future demand by bringing previously under-connected geographies closer to the national exchange and digital care ecosystem.

Competitive Landscape

The United States eHealth market is medium concentrated at the platform layer because a relatively small set of enterprise vendors anchors clinical workflow, data infrastructure, and large-scale provider relationships, while the application layer remains more fragmented across specialized use cases. Epic Systems, Oracle Health, Optum, and Microsoft shape much of the infrastructure conversation, but competition is increasingly being decided by native AI integration rather than by traditional feature expansion alone. Oracle Health said in March 2026 that its Clinical AI Agent had already saved more than 200,000 physician-hours across U.S. providers since launch, which shows how incumbent platforms are using automation to deepen their position inside the care workflow. Epic is taking a similar path, with Agent Factory and Curiosity extending its AI footprint and with a public roadmap that spans at least 200 AI feature categories across clinical, patient-facing, and administrative domains. This puts clear pressure on mid-tier vendors that do not have similar scale, data depth, or development capacity in the United States eHealth market.

Disruptors are still finding room to grow, but many are entering through employer, payer, and pharmacy benefit channels instead of waiting for slower health system procurement cycles. Spring Health completed its acquisition of Alma in May 2026, creating what it described as the first AI-native lifelong mental health platform that combines employer benefit coverage with an independent clinician network. Hims & Hers is also expanding its digital care reach through acquisition, with the planned purchase of Eucalyptus strengthening its multi-country consumer platform strategy. Omada Health's PBM-linked distribution shows that scaled growth can come from embedded benefit channels, which lets specialized vendors reach large covered populations without first winning full enterprise EHR control.

The most open areas in the United States eHealth market sit where buyer urgency is high but incumbent control is less complete. Clearinghouse diversification remains relevant after the Change Healthcare attack exposed how concentrated infrastructure can create national operating risk. AI-native mental health platforms, administrative automation, and ambient documentation tools that work with non-dominant EHRs also retain room for specialized vendors that can move faster than the largest platforms. Even so, the longer-term direction of competition favors companies that can combine workflow access, measurable outcomes, interoperable data exchange, and credible security posture into one operating model.

United States EHealth Industry Leaders

Epic Systems Corporation

Oracle Health

Optum

athenahealth Inc.

Teladoc Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Spring Health completed the acquisition of Alma, creating the first AI-native lifelong mental health platform combining employer benefit coverage with an independent clinician membership network; the combined entity positions itself as the dominant vertically integrated digital mental health provider across commercial and employer-sponsored markets.

- August 2025: Oracle launched an all-new AI-driven EHR for ambulatory providers in the US with voice-first interactions, contextual AI, and a roadmap to introduce full acute care functionality in 2026, a full-stack interface replacement positioning Oracle to compete directly with Epic's ambulatory industry.

United States EHealth Market Report Scope

As per the scope of the report, eHealth refers to the use of digital technology, electronic communication, and information technology to support and improve healthcare services, health information management, and health education. It encompasses a wide range of tools such as electronic health records (EHRs), telemedicine, mobile health apps, health information systems, and other digital innovations aimed at enhancing healthcare delivery, patient engagement, and health outcomes.

The segmentation for the United States eHealth market is categorized by component, delivery mode, service type, and end user. By component, it includes health information systems, electronic health records/electronic medical records, health information exchange, population health management, patient engagement solutions, telemedicine and virtual care platforms, mHealth applications, clinical decision support and ambient AI, e-prescribing and e-pharmacy, and other components. By delivery mode, the market is segmented into cloud-based solutions, hybrid solutions, and on-premise solutions. By service type, it covers monitoring services (remote patient monitoring, chronic disease management, and wellness monitoring), diagnostic services (tele-radiology, tele-pathology, and AI-enabled triage and decision support), therapeutic services (teleconsultation, digital therapeutics, virtual rehabilitation, and telepsychiatry and behavioral therapy), and administrative and workflow services (e-prescribing, e-prior authorization, patient scheduling and intake, and patient engagement and messaging). By end user, the market is divided into healthcare providers, payers, patients and individual consumers, and other end users. For each segment, the market size and forecast are provided in terms of value (USD).

| Health Information Systems | Electronic Health Records / Electronic Medical Records |

| Health Information Exchange | |

| Population Health Management | |

| Patient Engagement Solutions | |

| Telemedicine & Virtual Care Platforms | |

| mHealth Applications | |

| Clinical Decision Support & Ambient AI | |

| e-Prescribing & e-Pharmacy | |

| Other Components |

| Cloud-based Solutions |

| Hybrid Solutions |

| On-premise Solutions |

| Monitoring Services | Remote Patient Monitoring |

| Chronic Disease Management | |

| Wellness Monitoring | |

| Diagnostic Services | Tele-radiology |

| Tele-pathology | |

| AI-enabled Triage & Decision Support | |

| Therapeutic Services | Teleconsultation |

| Digital Therapeutics | |

| Virtual Rehabilitation | |

| Telepsychiatry & Behavioral Therapy | |

| Administrative & Workflow Services | e-Prescribing |

| e-Prior Authorization | |

| Patient Scheduling & Intake | |

| Patient Engagement & Messaging |

| Healthcare Providers |

| Payers |

| Patients & Individual Consumers |

| Other End Users |

| By Component | Health Information Systems | Electronic Health Records / Electronic Medical Records |

| Health Information Exchange | ||

| Population Health Management | ||

| Patient Engagement Solutions | ||

| Telemedicine & Virtual Care Platforms | ||

| mHealth Applications | ||

| Clinical Decision Support & Ambient AI | ||

| e-Prescribing & e-Pharmacy | ||

| Other Components | ||

| By Delivery Mode | Cloud-based Solutions | |

| Hybrid Solutions | ||

| On-premise Solutions | ||

| By Service Type | Monitoring Services | Remote Patient Monitoring |

| Chronic Disease Management | ||

| Wellness Monitoring | ||

| Diagnostic Services | Tele-radiology | |

| Tele-pathology | ||

| AI-enabled Triage & Decision Support | ||

| Therapeutic Services | Teleconsultation | |

| Digital Therapeutics | ||

| Virtual Rehabilitation | ||

| Telepsychiatry & Behavioral Therapy | ||

| Administrative & Workflow Services | e-Prescribing | |

| e-Prior Authorization | ||

| Patient Scheduling & Intake | ||

| Patient Engagement & Messaging | ||

| By End User | Healthcare Providers | |

| Payers | ||

| Patients & Individual Consumers | ||

| Other End Users | ||

Key Questions Answered in the Report

What is driving growth in United States eHealth through 2031?

Growth is being supported by CMS reimbursement changes, chronic disease management demand, cloud migration, and wider use of AI-enabled virtual care and workflow tools. The sector is projected to reach USD 243.92 billion by 2031 at a 15.22% CAGR.

Which service area holds the largest revenue base in this space?

Monitoring Services led with 56.52% of 2025 revenue, supported by remote patient monitoring, chronic disease management, and wellness monitoring programs.

Which component is expanding the fastest in digital care platforms?

Telemedicine & Virtual Care Platforms are the fastest-growing component, with a projected 19.38% CAGR through 2031, helped by employer channels, mental health care, and chronic care programs.

Why are cloud deployments leading adoption across providers?

Cloud-based Solutions held 52.24% of 2025 delivery-mode revenue because health systems need scalable infrastructure for AI workloads, interoperability, and virtual care operations.

Who spends the most on eHealth solutions in the United States?

Healthcare Providers remained the largest end-user group with 48.24% of 2025 revenue, as they continue to buy EHR systems, ambient AI tools, decision support platforms, and population health systems.

What is the biggest risk facing digital health platforms in the United States?

Cybersecurity remains the sharpest near-term risk. The Change Healthcare attack affected 192.7 million individuals and showed how failures at one infrastructure layer can disrupt care delivery and payments nationwide.

Page last updated on: