Africa Food Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

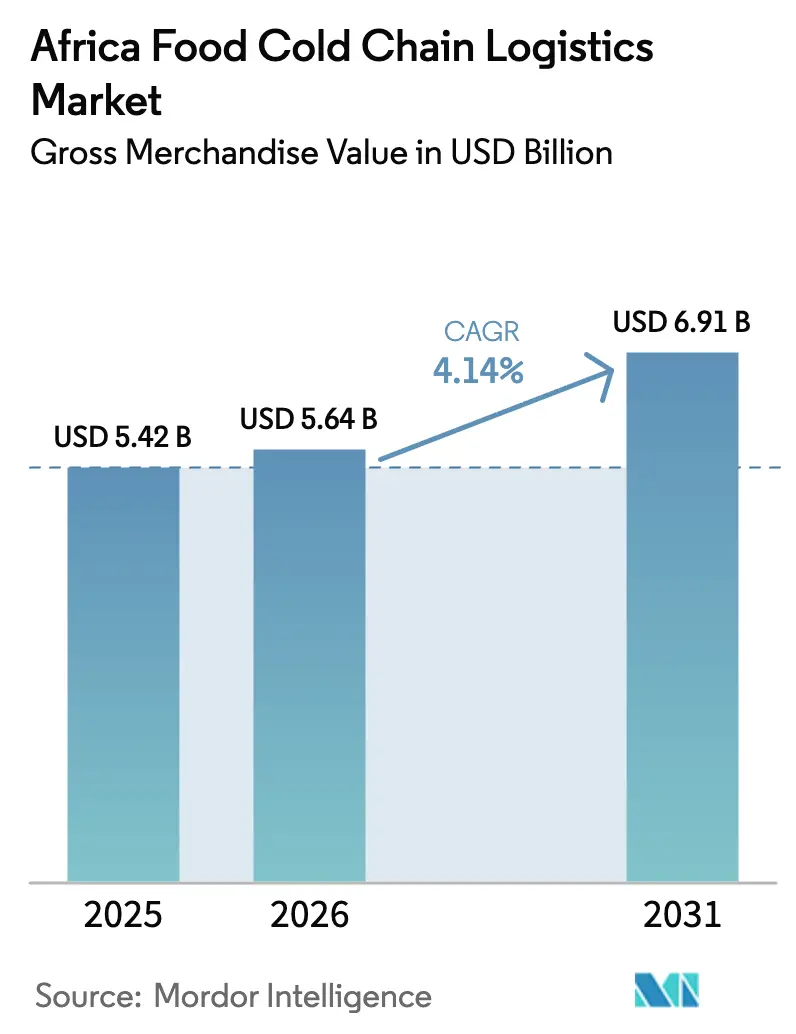

| Base Year Market Size (2025) | USD 5.42 Billion |

| Market Size (2026) | USD 5.64 Billion |

| Market Size (2031) | USD 6.91 Billion |

| Growth Rate (2026 - 2031) | 4.14% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Food Cold Chain Logistics Market Analysis by Mordor Intelligence

The Africa Food Cold Chain Logistics Market size was valued at USD 5.42 billion in 2025 and estimated to grow from USD 5.64 billion in 2026 to reach USD 6.91 billion by 2031, at a CAGR of 4.14% during the forecast period (2026-2031).

Rising investments in solar-powered storage, modern retail distribution centers, and corridor-wide digital traceability platforms continue to shrink the USD 4 billion in annual post-harvest losses that African economies recorded in 2024. South Africa’s port-anchored infrastructure, Ethiopia’s perishables-ready cargo terminals, and Nigeria’s off-grid micro-warehouses are converging to reshape route density, lower spoilage, and elevate service-level expectations across the Africa Food Cold Chain Logistics market. Regulatory modernization—anchored by AfCFTA-aligned phytosanitary protocols—shortens border dwell times, while pan-regional retail chains make year-round fresh produce availability the new consumer baseline. Competitive differentiation now hinges on AI-enabled dispatching that prevents load-shedding spoilage, and on blended finance structures that de-risk capital outlays for temperature-controlled fleets.

Key Report Takeaways

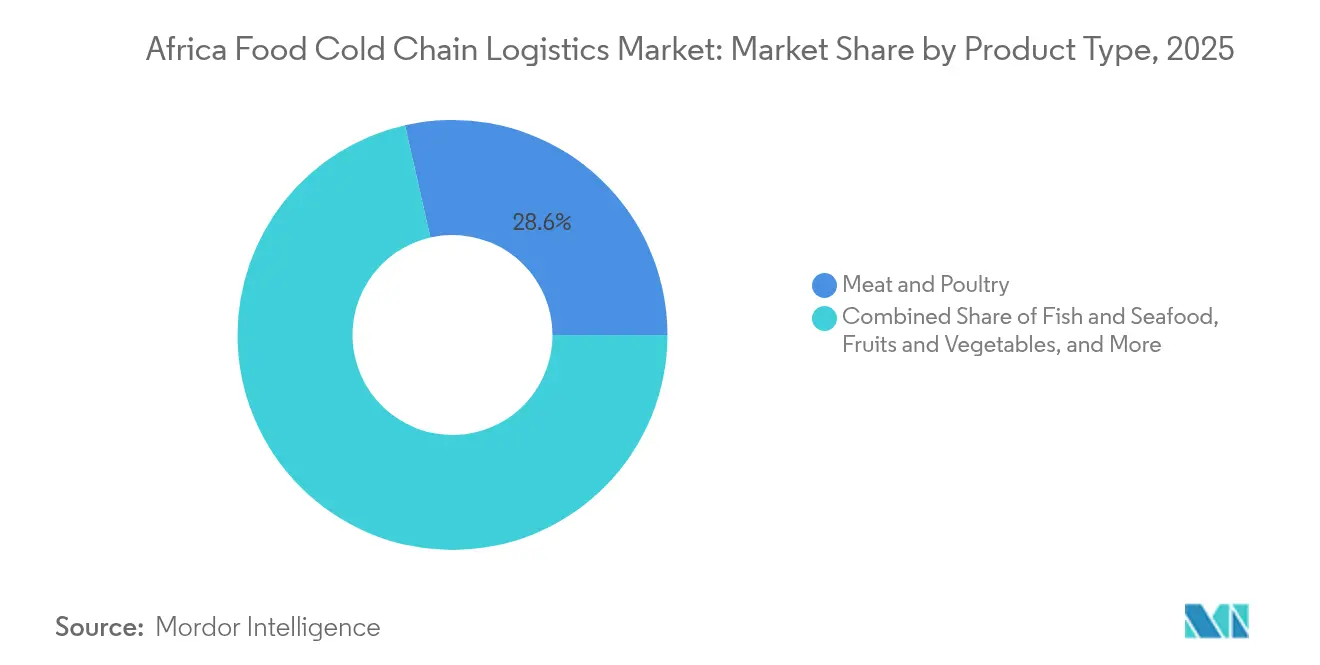

- By product type, Meat & Poultry led with 28.55% of Africa Food Cold Chain Logistics market share in 2025, while Fruits & Vegetables is forecast to advance at a 4.52% CAGR from 2026 to 2031.

- By service type, Refrigerated Storage accounted for a 37.60% share of the Africa Food Cold Chain Logistics market size in 2025, whereas Refrigerated Transportation is projected to grow at a 4.02% CAGR through 2031.

- By temperature type, frozen applications secured a 47.70% share of the Africa Food Cold Chain Logistics market size in 2025, and chilled applications are set to expand at a 4.75% CAGR between 2026-2031.

- By country, South Africa commanded 26.75% of the Africa Food Cold Chain Logistics market share in 2025, while Nigeria exhibits the fastest trajectory at 4.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Food Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing horticultural exports | +0.8% | Kenya, South Africa, Egypt | Medium term (2-4 years) |

| Retail expansion of modern grocery chains | +0.6% | Nigeria, South Africa, Kenya | Long term (≥ 4 years) |

| Stricter food-safety & traceability regulations | +0.5% | Export corridors continent-wide | Short term (≤ 2 years) |

| Pan-African free-trade corridors | +0.4% | SADC & EAC regions | Long term (≥ 4 years) |

| Mobile solar-powered micro-warehouses | +0.7% | Nigeria, Kenya, Rwanda | Medium term (2-4 years) |

| AI-driven route optimisation | +0.3% | South Africa, Nigeria | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Horticultural Exports Drive Infrastructure Investment

Kenya, South Africa, and Egypt have accelerated pack-house and airport cargo-terminal upgrades to unlock premium markets for blueberries, avocados, and cut flowers. Controlled-atmosphere containers now extend avocado shelf life to 50 days, allowing exporters to reach Europe by sea without quality degradation. Ethiopian Airlines Cargo scaled its perishables terminal to handle 450,000 tonnes annually, giving producers a reliable end-to-end cold chain that commands price premiums. Kenyan exporters have doubled their share of the USD 3.7 billion global flower trade in the last 20 years. This surge compels logistics providers to add blast-chillers, real-time humidity monitoring, and blockchain traceability modules that meet EU and Middle East phytosanitary rules.

Retail Modernization Accelerates Cold Storage Demand

Supermarket penetration has risen sharply in Lagos, Johannesburg, and Nairobi, pushing demand for distribution centers that sustain 0-5 °C for dairy, deli, and ready-meal categories. Modern retailers operate just-in-time inventory systems, reducing acceptable spoilage from 40-50% in informal markets to single digits[1]Food and Agriculture Organization, “Sustainable Food Cold Chains: Opportunities, Challenges and the Way Forward,” fao.org. Temperature-controlled last-mile networks—from insulated e-moped boxes to battery-electric delivery trucks—are emerging as cost-effective pathways to serve densely populated urban neighborhoods. As a result, the Africa Food Cold Chain Logistics market increasingly values integrated warehousing, transport, and order-management solutions over standalone assets.

Regulatory Harmonization Enhances Cross-Border Trade Efficiency

The East African Community has issued more than 50 harmonized food standards, while the World Bank’s ePhyto platform replaces paper certificates with digital equivalents, slashing border delays for perishables[2]World Bank, “Avoiding the ‘Harm’ in Harmonized Standards for Food Staples in Africa,” worldbank.org. Though strict aflatoxin limits initially raised compliance costs for maize, iterative policy dialogue now balances food-safety and trade-facilitation goals. Logistics firms leverage automated document upload and container-seal verification tools to shorten dwell times that once exceeded 72 hours at regional borders.

Pan-African Trade Integration Unlocks Logistics Synergies

AfCFTA’s tariff reductions are projected to lift intra-African freight demand by 28% and add nearly 2 million trucks by 2030. Cold-chain operators optimize back-haul utilization—sending citrus southbound and pharmaceuticals northbound—reducing empty-run kilometers. Special Agro-Industrial Processing Zones in Nigeria anchor produce aggregation, enabling route densities that warrant fleet electrification and solar-hybrid micro-hubs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic electricity shortages & load-shedding | -0.9% | South Africa, Nigeria, Ghana | Short term (≤ 2 years) |

| High capital intensity of refrigerated fleets | -0.6% | Continent-wide, land-locked states | Medium term (2-4 years) |

| Shortage of certified refrigeration technicians | -0.4% | Sub-Saharan Africa | Long term (≥ 4 years) |

| Complex cross-border phytosanitary inspections | -0.3% | Regional corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Load-Shedding Disruptions Threaten Supply-Chain Resilience

South Africa logged more than 280 days of scheduled blackouts in 2024, compelling cold-store operators to rely on diesel generators that elevate operating costs and carbon footprints. The Global Cold Chain Alliance warns that unplanned outages jeopardize vaccine efficacy and seafood integrity within hours[3]Global Cold Chain Alliance, “Urgent Action Needed to Mitigate Energy Blackout Threat to Food Supply Chain Resilience in Africa,” gcca.org. Operators adopt hybrid solar-diesel micro-grids, phase-change tiles, and remote temperature alarms to avert catastrophic spoilage, yet rising fuel prices tighten margins for SMEs.

Capital Intensity Barriers Limit Market Entry

Fleet electrification, multi-temperature trailers, and telematics add USD 60,000-80,000 per truck—outlays beyond reach for many local hauliers. DHL has earmarked EUR 2 billion (USD 2.08 billion) for global healthcare cold-chain projects through 2030, illustrating the scale advantages large incumbents wield[4]DHL Group, “DHL Group to Invest EUR 2 Billion in Health Logistics,” dhl.com. Impact investors step in with mezzanine debt and revenue-based financing, but credit-scoring challenges persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Meat Dominance Faces Fruit Revolution

Meat & Poultry generated 28.55% of Africa Food Cold Chain Logistics market size in 2025, reflecting high-value protein flows into the Middle East and EU markets. Frozen carcass exports from South Africa and live-animal shipments from Ethiopia demand -18 °C compliance, sophisticated haulage, and veterinary-approved cleaning protocols. Fruits & Vegetables post the fastest 4.52% CAGR as avocado, mango, and blueberry exports expand; controlled-atmosphere reefer liners extend shelf life, broadening shipping options. Dairy, Fish & Seafood, and niche Ready-Meals each occupy smaller shares yet benefit from urban consumption shifts and QSR expansion. Solar micro-hubs reduce on-farm pineapple and tomato losses, turning subsistence plots into cash-crop nodes across the Africa Food Cold Chain Logistics market.

Adoption of ethylene-absorbing sachets and digital ripeness sensors amplifies the competitive edge of fruit exporters. Meanwhile, halal-certified slaughterhouses and integrated cold stores near port zones reinforce South Africa’s beef leadership. Fish landings along West Africa’s coast increasingly ship under ultra-low-temperature (-50 °C) conditions, raising service-quality thresholds for carriers wishing to penetrate the Africa Food Cold Chain Logistics market.

By Service Type: Storage Infrastructure Leads Transportation Evolution

Refrigerated Storage captured 37.60% of Africa Food Cold Chain Logistics market share in 2025 as producers sought buffer capacity to smooth harvest-linked supply spikes. Operators deploy racking systems, blast freezers, and WMS software that provide SKU-level inventory accuracy essential for export compliance. Transportation is forecast at a 4.02% CAGR to 2031, underpinned by corridor upgrades and rail-sea modal shifts. CEVA Logistics’ adoption of reefer rail wagons between South Africa and Namibia illustrates new intermodal possibilities.

Value-Added Services—from kitting and pre-cooling to pallet re-configuration—register the quickest revenue climb as retailers outsource complex in-store preparation tasks. Telematics platforms now combine compressor diagnostics, door-open alerts, and CO₂-equivalent dashboards, letting shippers benchmark sustainability performance across the Africa Food Cold Chain Logistics market.

By Temperature Type: Frozen Applications Drive Technical Innovation

Frozen applications constituted 47.70% of Africa Food Cold Chain Logistics market size in 2025. -18 °C environments handle red-meat primals, pasteurized poultry, and ice-glazed shrimp bound for Asian markets. Chilled products, expanding at a 4.75% CAGR, ride the wave of fresh-cut salads, yogurt drinkables, and sushi-grade tilapia demanded by urban Millennials.

The International Institute of Refrigeration disseminates hot-climate cold-room blueprints, emphasizing insulation R-values and nocturnal condensate management. Ambient-controlled facilities bridge the gap for confectionery and grain derivatives sensitive to humidity but not requiring active refrigeration, seeding first-time cold-chain adoption in francophone West Africa.

Geography Analysis

South Africa’s mature asset base, anchored by Durban and Cape Town ports, buffers 70% of sub-Saharan refrigerated maritime exports. Retail consolidation fuels the expansion of cross-dock centers that synchronize rural poultry processors with urban hypermarkets. Load-shedding risks, however, force widespread solar-rooftop retrofits and LNG micro-turbine pilots to safeguard the Africa Food Cold Chain Logistics market.

Nigeria’s innovation centers on bridging a 40.66% food inflation shock through cold-chain efficiency gains. Solar micro-hubs aggregate peppers, okra, and catfish within 20 km of farms, integrating with Lagos’ tech-enabled B2B platforms that link producers to 7,000+ informal retailers daily. Government tax incentives for reefer truck imports lower entry hurdles, while digital duty-drawback systems accelerate customs clearance at Apapa port, shortening cycle times from 4 days to 36 hours.

Competitive Landscape

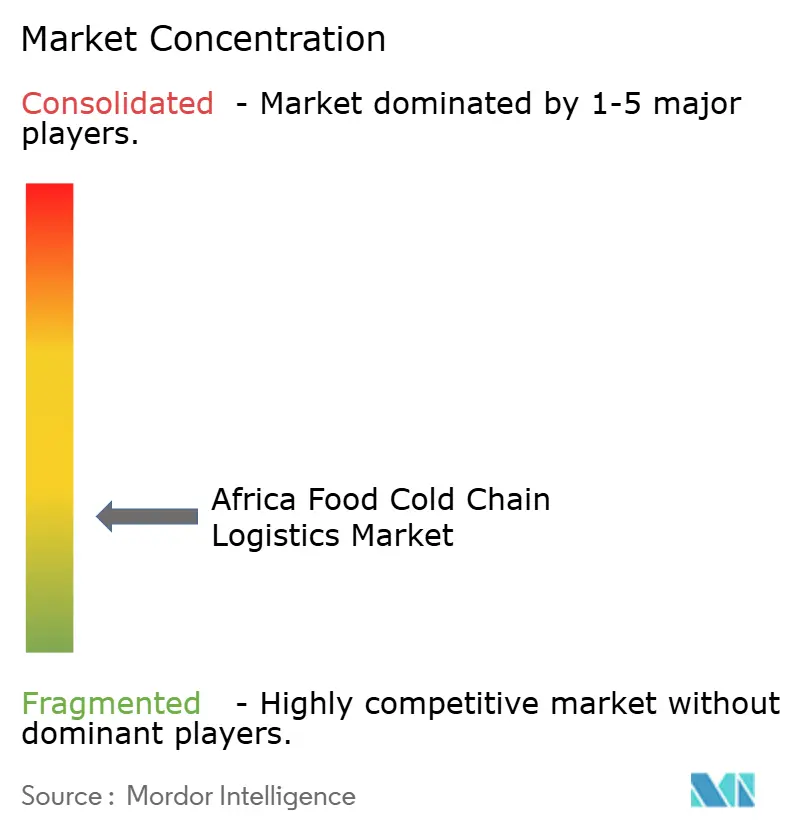

The Africa Food Cold Chain Logistics market remains fragmented. Imperial Logistics, DHL Supply Chain, and CEVA Logistics leverage borderless networks, sizable capex budgets, and ISO 22000 certifications to win multi-year contracts from retailers, QSR chains, and vaccine manufacturers. Imperial’s Abuja control tower integrates IoT data from 12,000 assets, enabling dynamic routing that trims 18% idle time and 0.5 °C average temperature variance. DHL’s GoGreen Plus program offers carbon-insetting options, tapping corporates’ ESG budgets.

Local innovators exploit white-space niches. ColdHubs scales pay-go, off-grid rooms that achieve 98.5% equipment uptime using GSM-enabled energy management. BigCold Kenya uses AI dispatch to consolidate cut-flower loads into Nairobi-Amsterdam freighters, reducing wait times that once jeopardized stem firmness. Keep IT Cool’s Markiti app collapses multi-tier produce trade into direct farmer-to-hotel transactions, slashing waste by 12 percentage points.

M&A intensity grows: Kuehne + Nagel acquired Morgan Cargo to fortify perishables links between South Africa, the UK, and Kenya. DSV’s USD 14.9 billion purchase of DB Schenker boosts warehouse density and client cross-selling potential. Strategic partnerships with sensor firms, autonomous-truck start-ups, and ag-tech platforms accelerate the digital maturity curve across the Africa Food Cold Chain Logistics market.

Africa Food Cold Chain Logistics Industry Leaders

CCS Logistics

Vector Logistics

Khold

African Perishables Logistics

Imperial Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSV completed the acquisition of DB Schenker for USD 14.9 billion, creating a 160,000-employee logistics leader.

- March 2025: Volvo Trucks South Africa delivered two battery-electric FH 6x4 tractors to Vector Logistics, marking the fleet’s first net-zero cold-chain rigs.

- June 2024: DP World earmarked USD 3 billion for African port and logistics upgrades, with USD 1 billion targeted at cold-chain capabilities.

- April 2024: Unitrans launched a Centre of Excellence to drive data-led safety and cost efficiencies across African freight corridors.

Africa Food Cold Chain Logistics Market Report Scope

A cold chain is a temperature-controlled supply chain. Cold chain logistics is a technology and process that enables the safe transportation of temperature-sensitive goods and products along the supply chain. The market size captures the revenue accrued by the logistics companies by providing services such as transportation, storage, and other value-added services. The current market report scope captures only cold chain logistics spending related to food cold chain and does not include other products such as pharmaceuticals and chemicals.

The African food cold chain logistics market is segmented by service (storage, transportation, and value-added services), temperature (chilled, frozen, and ambient), product category (horticulture, dairy products, meat, poultry, and seafood, processed food products, and other categories), and country (Egypt, Nigeria, South Africa, and other countries). The report offers market size and forecast in value (USD) for all the above segments.

| Meat & Poultry |

| Fish & Seafood |

| Dairy & Ice-cream |

| Fruits & Vegetables |

| Bakery & Confectionery |

| Ready Meals & Others |

| Refrigerated Storage | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

| Chilled (0–5 °C) |

| Frozen (-18–0 °C) |

| Ambient |

| Egypt |

| Nigeria |

| South Africa |

| Kenya |

| Ethiopia |

| Rest of Africa |

| By Product Type | Meat & Poultry | |

| Fish & Seafood | ||

| Dairy & Ice-cream | ||

| Fruits & Vegetables | ||

| Bakery & Confectionery | ||

| Ready Meals & Others | ||

| By Service Type | Refrigerated Storage | |

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0–5 °C) | |

| Frozen (-18–0 °C) | ||

| Ambient | ||

| By Country | Egypt | |

| Nigeria | ||

| South Africa | ||

| Kenya | ||

| Ethiopia | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the Africa Food Cold Chain Logistics market in 2026?

It is valued at USD 5.64 billion in 2026 with a forecast to reach USD 6.91 billion by 2031.

What CAGR is expected for Africa’s solar-powered cold-storage hubs?

Solar micro-warehouses underpin a 4.52% CAGR for the Fruits & Vegetables segment through 2031.

Which country leads in market share?

South Africa holds 26.75% of market share thanks to mature ports and dense distribution networks.

What is the fastest-growing service segment?

Refrigerated Transportation, driven by corridor upgrades, is projected at 4.02% CAGR to 2031.

How do power outages affect the cold chain?

Load-shedding can raise spoilage risk, prompting investment in hybrid solar-diesel systems and IoT alerts.

Page last updated on: