Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

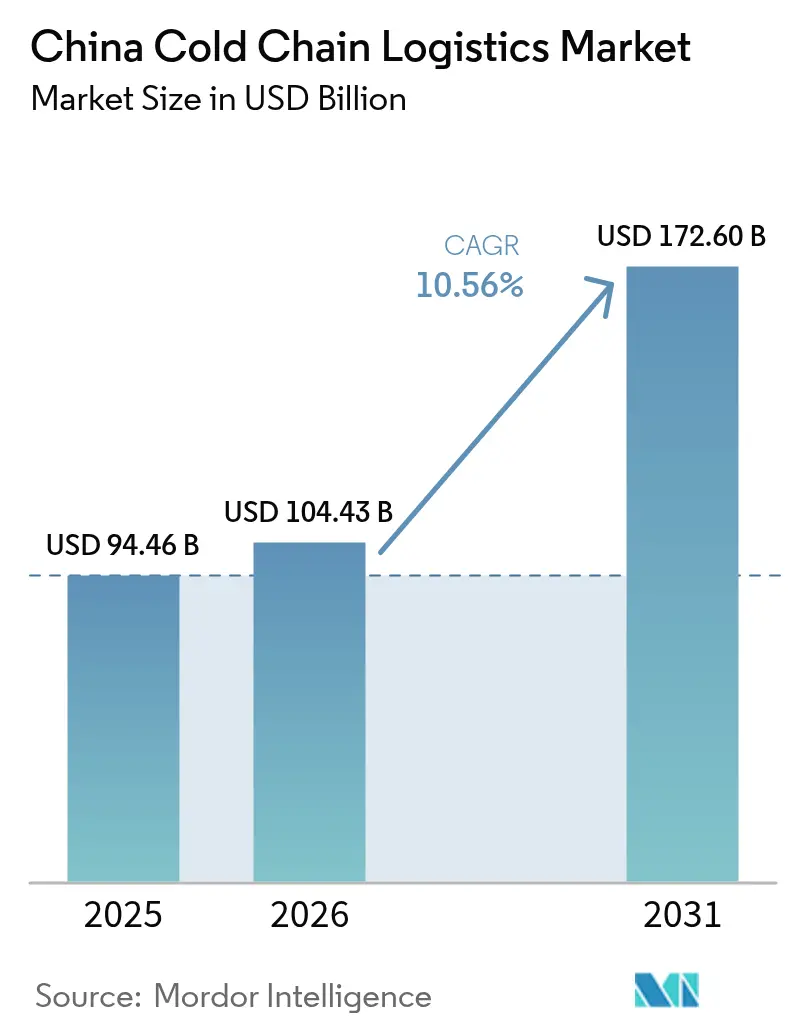

| Base Year Market Size (2025) | USD 94.46 Billion |

| Market Size (2026) | USD 104.43 Billion |

| Market Size (2031) | USD 172.6 Billion |

| Growth Rate (2026 - 2031) | 10.56% CAGR |

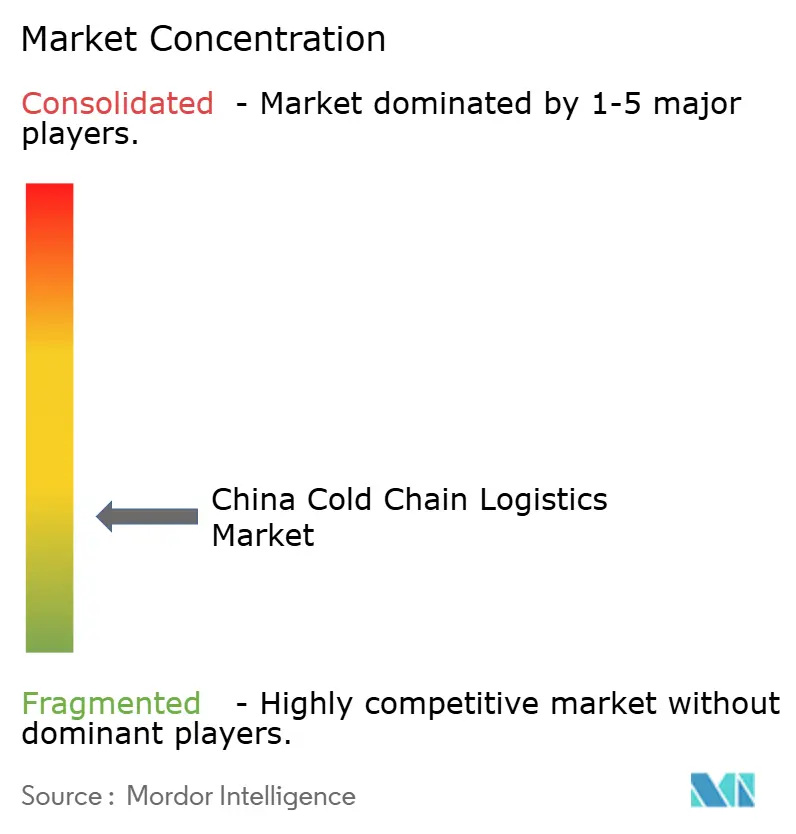

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Cold Chain Logistics Market Analysis by Mordor Intelligence

The China Cold Chain Logistics Market size is expected to grow from USD 94.46 billion in 2025 to USD 104.43 billion in 2026 and is forecast to reach USD 172.6 billion by 2031 at 10.56% CAGR over 2026-2031.

Investment flowing from the 14th Five-Year Plan continues to add modern, multi-temperature depots across inland provinces, reducing the sector’s historic coastal bias and opening fresh revenue streams for integrated providers. At the same time, the proliferation of fresh-food e-commerce keeps compressing delivery windows, nudging operators to weave micro-fulfilment hubs into existing long-haul networks. Demand for GDP-compliant, ultra-low temperature lanes is rising in parallel with China’s biopharma export ambitions, which lifts average yields per tonne and accelerates technology upgrades. Middle-income households are buying more imported chilled meat and seafood, pulling volume through port-centric corridors that already benefit from scale. Last-mile fragmentation and a shortage of certified refrigeration technicians persist, yet the broader trajectory remains one of scale, digitisation, and gradual consolidation.

Key Report Takeaways

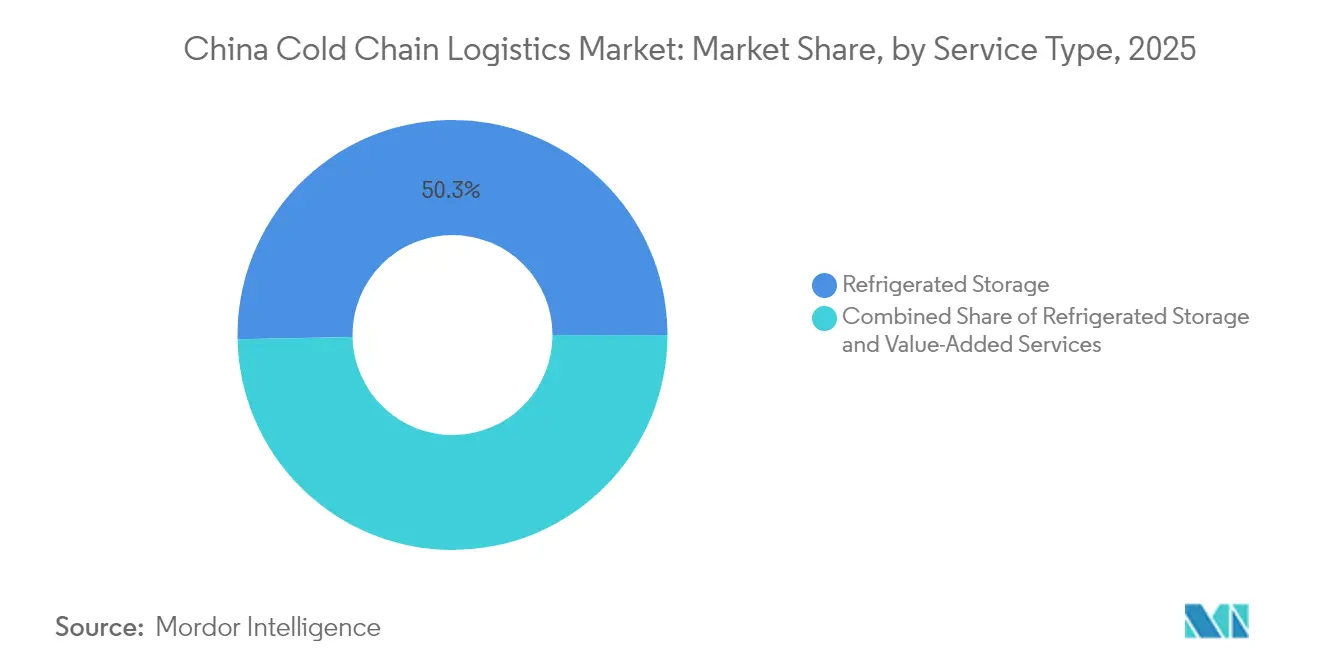

- By service type, refrigerated storage retained 50.32 % market share in 2025, while value-added services is pacing the field at a 11.90 % CAGR through 2031.

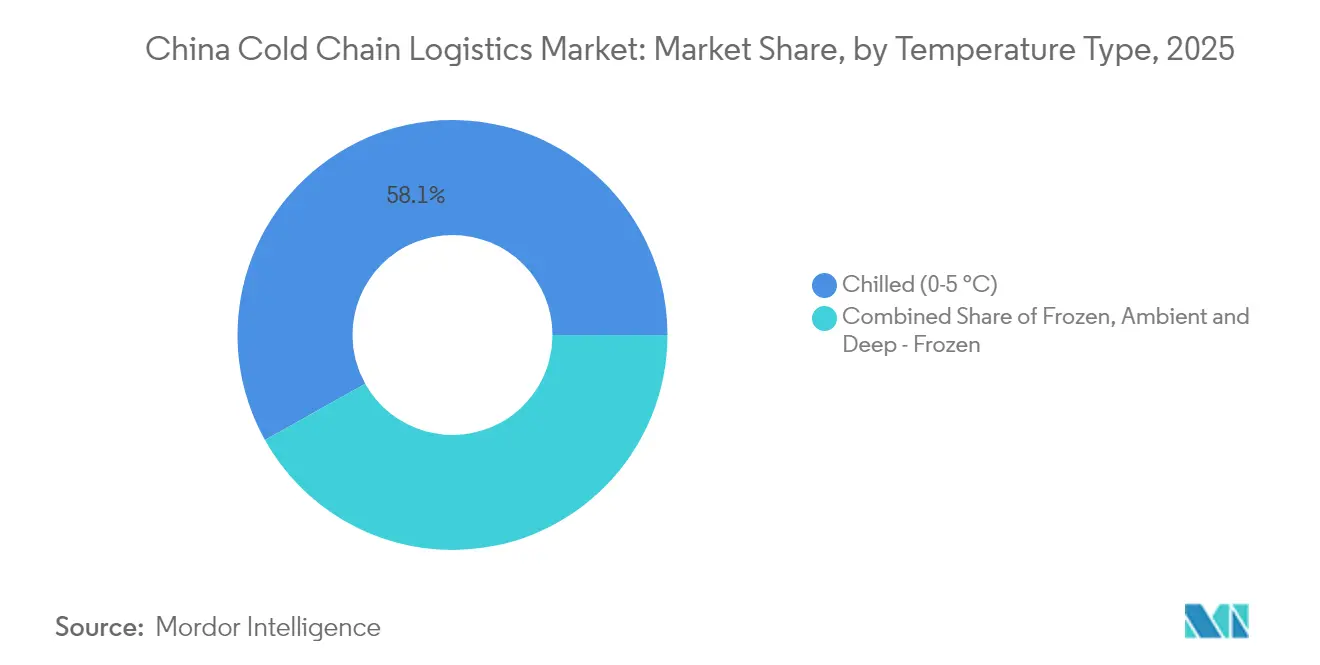

- By temperature range, chilled handling (0–5 °C) dominated with 58.12 % share in 2025; frozen logistics (–18–0 °C) is expanding fastest at an 11.01 % CAGR to 2031.

- By application, fruits & vegetables contributed 28.38 % of demand in 2025, whereas pharmaceuticals & biologics are projected to grow at a 14.12 % CAGR to 2031.

- By region, East China accounted for 33.74 % of the market in 2025, while Southwest China leads in growth with a 12.42 % CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Cold Chain Infrastructure under 14th FYP Accelerating Warehouse Build-out | +2.1% | National, with inland priority | Long term (≥ 4 yrs) |

| Rapid Fresh E-commerce | +1.5% | Urban nationwide | Short term (≤ 2 yrs) |

| Biopharma Export Boom Driving GDP-compliant Ultra-low Cold Chain | +1.3% | East and North China | Medium term (2-4 yrs) |

| Rising Middle-class Appetite for Imported Chilled Meat & Seafood | +0.8% | National, with higher penetration in coastal cities | Medium term (2-4 years) |

| Dairy-safety Modernization Programs Stimulating Temperature-controlled Milk Logistics | +0.6% | National, with focus on dairy production regions | Long term (≥ 4 years) |

| Energy-efficiency Subsidies for CO₂/Ammonia Systems Lowering Capex Barriers | +0.4% | National, with emphasis on industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National Cold Chain Infrastructure under 14th FYP Accelerating Warehouse Build-out

Central government plans earmark significant capital for cold chain highways that connect production zones to city markets, targeting a 25 % chilled distribution rate for fruit and 45 % for meat by 2027[1]National Development and Reform Commission, “14th Five-Year Plan for Cold Chain Logistics Development,” ndrc.gov.cn. Inland hubs in Henan, Hunan, and Sichuan now account for a larger share of new cubic metres than coastal hubs, closing historical gaps and reducing transport distances[2]Sichuan Provincial Government, “Implementation Plan for Cold Chain Logistics Bases,” sc.gov.cn. This build-out is already cutting produce spoilage and encouraging planting of higher-value crops, a development that expands product diversity in retail channels.

Rapid Expansion of Fresh E-commerce

Same-day delivery promises from platforms such as JD Fresh and Freshippo have forced traditional carriers to install micro-fulfilment nodes inside city rings. Each node typically supports three temperature bands, allowing orders to be picked within minutes of confirmation. Route-optimisation software is cutting empty kilometres, meaning urban reefer vans can run more stops per shift. Consumers respond with larger basket sizes once they trust temperature integrity, reinforcing the platform’s competitive moat.

Biopharma Export Boom Driving GDP-Compliant Ultra-Low Cold Chain

China’s biologics manufacturers now ship therapies that require −20 °C to −70 °C handling, a process governed by the National Medical Products Administration’s GDP rules that align with EU standards. Providers that validate containers and log chain-of-custody data can price loads at two to three times the yield of food cargo. Those premiums justify investments in liquid-nitrogen systems that will later serve niche seafood and lab research markets, thereby raising industry-wide technical competence.

Rising Middle-Class Appetite for Imported Chilled Protein

Affluent households are spending more on Australian beef and Norwegian salmon, products that must stay between 0 °C and 4 °C from port to plate. Import corridors through Shanghai and Ningbo now embed real-time trackers in every reefer, making temperature compliance a visible marketing claim. Domestic beef suppliers are responding by upgrading their own logistics, so improvements spill back into local supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Last-mile Reefer Network Causing High Spoilage Rates | -1.2% | Tier-3 cities | Short term (≤ 2 yrs) |

| Shortage of Certified Industrial Refrigeration Technicians | -0.8% | Inland regions | Medium term (2-4 yrs) |

| High Electricity Tariffs & Grid Instability in Tier-3 Cold Stores | -0.7% | Tier-3 cities and rural areas | Medium term (2-4 years) |

| China VI Truck Emission Rule Inflating Reefer Fleet Retrofit Costs | -0.5% | National, with higher impact on smaller operators | Short term (≤ 2 yrs) |

| Source: Mordor Intelligence | |||

Fragmented Last-Mile Reefer Network

China Cold Chain Logistics market study data show spoilage rates for leafy greens exceed 10 % in some tier-three cities because many delivery firms use non-insulated vans. Insurance underwriters increasingly demand temperature logs for claims, leading to higher premiums for carriers without monitoring equipment. Technology-enabled entrants that pool orders across stores are winning share, foreshadowing consolidation in urban distribution.

Shortage of Certified Refrigeration Technicians

A national shortfall of tens of thousands of qualified technicians constrains the roll-out of natural-refrigerant systems. Operators in western provinces often wait days for repairs, lowering equipment uptime and raising electricity bills. Leading equipment vendors now bundle training with installation, monetising the skills gap while improving service quality. Facilities that secure certified staff quickly report lower maintenance costs and improved carbon footprints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Service Type: Storage Dominance Masks Transportation Opportunity

Refrigerated storage accounted for 50.32 % China Cold Chain Logistics market share in 2025, underscoring the need for fixed capacity. Growth in value-added services is faster at a forecast 11.90 % CAGR through 2031, showing that shippers increasingly pay for tasks like relabelling, inspection, and kitting. Operators that combine warehousing with these services improve their revenue per square metre, creating a buffer against price competition in basic pallet storage. Integrated models also lower handling errors because goods remain within one digital ecosystem from inbound to outbound.

Refrigerated transportation remains the second-largest category and continues to benefit from e-commerce timelines that compress order-to-delivery cycles. Sensor-equipped trailers now stream temperature and door-open data every two minutes, reducing claims and supporting dynamic route changes when traffic builds. Small hauliers unable to finance such upgrades risk losing contracts to asset-light tech intermediaries that can guarantee visibility without owning trucks. The landscape therefore tilts toward fewer but larger fleets partnered with software platforms.

Temperature Type: Chilled Segment Expansion Driven by Fresh Produce Revolution

Chilled logistics (0 °C–5 °C) captured 58.12 % China Cold Chain Logistics market size in 2025 as fresh produce and dairy remained central to household diets. Frozen lanes (−18 °C–0 °C) are expanding at more than 11 % CAGR thanks to convenience foods and longer-haul meat imports. The deep-frozen and ultra-low segment grows quickest, driven by biologics and some premium desserts that need −40 °C or colder. Facilities capable of handling three bands under one roof can switch chambers as demand shifts, maximising utilisation and reducing payback periods.

Energy-efficient hardware is spreading across all bands. Carbon-dioxide systems, supported by central grants, cut power bills and avoid synthetic refrigerant quotas. Users report that the higher upfront cost is recouped within five years through lower electricity and maintenance outlays, suggesting a clear financial case for green technology in the China Cold Chain Logistics industry.

Application: Fruits & Vegetables Lead While Pharmaceuticals Accelerate

Fruits and vegetables held 28.38 % China Cold Chain Logistics market share in 2025, reflecting the scale of domestic horticulture. Direct sourcing models that truck produce within hours of harvest have reduced shrinkage and expanded shelf life, so supermarkets can now stock more SKUs and reduce mid-week replenishment trips. Meat and poultry is the next-largest segment, with stricter import inspections driving demand for certified storage space.

Pharmaceuticals and biologics form the fastest-growing segment at over 14 % CAGR through 2031. Stringent GDP rules mean zero tolerance for temperature excursions, so loads earn premium yields that cover extra compliance costs. Vaccine makers sign multi-year contracts to lock in capacity, giving providers predictable revenue streams. Precision monitoring tools developed for pharma are now crossing over to high-value food categories, a trend that elevates industry-wide service expectations.

Geography Analysis

East China retained 33.74 % China Cold Chain Logistics market share in 2025, underpinned by dense consumer markets and port access. Container throughput at Shanghai supports fast transshipment of chilled salmon flown in from Europe, reinforcing the region’s role as gateway for premium imports. Pharmaceutical clusters in Jiangsu and Zhejiang generate steady demand for 2 °C–8 °C storage, providing counter-seasonal revenue that balances produce peaks. Operators describe energy tariffs as the main cost headwind, prompting heavy investment in rooftop solar and high-efficiency insulation.

Southwest China posts the industry’s highest regional CAGR at 12.42 % through 2031. Government incentives attract logistics parks to Chengdu and Chongqing, creating an alternative corridor that links to Southeast Asia by rail-sea service. The region’s mild winters lower refrigeration power loads, giving cost advantages for long-term storage. Citrus growers in Sichuan now pre-cool fruit on farm, cutting loss rates and enabling export to northern markets. Early entrants enjoy first-mover advantages in land availability and local labour, positioning them to scale alongside rising consumption.

North China combines the national capital area with grain-producing hinterlands. Cooler ambient temperatures reduce energy use in half the year, yet hot, humid summers strain legacy insulation. Large distribution centres around Tianjin employ smart ventilation to manage condensation, improving safety and reducing mould risk. Cross-border lanes with Mongolia handle frozen beef and ice cream, using electrified reefers that plug into trackside power to cut diesel costs. Local authorities offer toll rebates for low-emission trucks, nudging fleets toward cleaner engines earlier than in other regions.

Competitive Landscape

Roughly 70 % of China Cold Chain Logistics market share is split among the top fifteen companies, yet hundreds of local firms keep pricing fluid. Scale players such as Sinotrans and China Merchants deploy capital into national parks, locking in electricity contracts that damp energy volatility. Technology-centric operators including SF Cold Chain and JD Logistics focus on same-day fulfilment and data transparency, often commanding higher unit rates. Foreign specialists like Lineage partner with domestic firms to navigate equity caps, importing warehouse automation that boosts throughput.

Competitive edges increasingly come from software, not just cubic metres. AI tools predict peak loads during festival seasons, allowing carriers to pre-position trailers and avoid surge costs. Blockchain pilots give shippers immutable temperature records, reducing dispute resolution time. Smaller firms without these tools may either license platforms or exit niche markets. The technician shortage magnifies the divide because large players can run in-house training academies, ensuring uptime and client confidence.

China Cold Chain Logistics Industry Leaders

Sinotrans Limited

SF Express

Beijing Ershang Group

NICHIREI CORPORATION

Shanghai Jin Jiang International Industrial Investment Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: JD Logistics opened a 120 000 m² automated multi-temperature centre in Suzhou with five climate zones ranging from −30 °C to ambient, enabling 200-city coverage within 24 hours.

- March 2025: Sinotrans committed CNY 2.8 billion (USD 433 million) to build 15 cold chain parks in central and western provinces, each designed for rail-road interchanges.

- February 2025: SF Express bought Chengdu Silverplow Low-Temperature Logistics for CNY 1.2 billion (USD 185 million), adding 500 specialised vehicles to its Southwest fleet.

- January 2025: China Merchants Americold Logistics secured CNY 3.5 billion (USD 541 million) to develop 20 GDP-compliant stores by 2027, focusing on biologics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study regards the China cold-chain logistics market as the full value generated within the country by specialized storage sites, temperature-controlled vehicles, containers, and related monitoring or handling services used to keep food, pharmaceutical, and other perishable cargos within their mandated thermal bands from farm or factory through final distribution.

Scope expressly omits generic dry-goods trucking, ambient third-party warehousing, and in-house corporate cold rooms that never enter the commercial logistics stream.

Segmentation Overview

- By Service Type

- Refrigerated Storage

- Public Warehousing

- Private Warehousing

- Refrigerated Transportation

- Road

- Rail

- Sea

- Air

- Value-Added Services

- Refrigerated Storage

- By Temperature Type

- Chilled (0–5 °C)

- Frozen (-18–0 °C)

- Ambient

- Deep-Frozen / Ultra-Low (More than -20 °C)

- By Application

- Fruits & Vegetables

- Meat & Poultry

- Fish & Seafood

- Dairy & Frozen Desserts

- Bakery & Confectionery

- Ready-to-Eat Meals

- Pharmaceuticals & Biologics

- Vaccines & Clinical Trial Materials

- Chemicals & Specialty Materials

- Other Perishables

- By Region (China)

- East China

- North China

- South-Central China

- Southwest China

- Northeast China

- Northwest China

Detailed Research Methodology and Data Validation

Primary Research

We validated desk findings through interviews with fleet managers in Beijing, cold-store developers in Jiangsu, chilled-food e-commerce operators in Guangdong, and procurement heads at multinational pharma importers. Conversations clarified typical haul lengths, average storage tariffs, and emerging IoT sensor adoption rates, helping us tighten utilization and asset-life assumptions.

Desk Research

Analysts began with customs records, Ministry of Transport fleet statistics, and the Cold Chain Logistics Committee's annual bulletins, which quantify refrigerated truck registrations, cold storage capacity, and commodity throughput. Trade associations such as the China Meat Association and Dairy Industry Association, National Bureau of Statistics retail datasets, and peer-reviewed journals on vaccine distribution added volume, weight, and spoilage rates. Company 10-Ks, IPO prospectuses, and provincial tender portals supplied pricing clues, while D&B Hoovers and Dow Jones Factiva offered firm-level financials. These sources, alongside other public and paid datasets, informed the foundational supply-demand matrix.

Market-Sizing & Forecasting

The model starts with a top-down rebuild. Cold storage cubic-meter inventory and refrigerated vehicle ton-kilometers are multiplied by average lease or freight rates, then adjusted for utilization seasonality. Select bottom-up checks, sampled operator revenue roll-ups and temperature-controlled shipment counts, calibrate the totals before results are locked. Key variables include fresh food e-commerce penetration, refrigerated truck sales, pharmaceutical cold chain compliance expenditure, average cold-store rental, and urban household protein consumption. A multivariate regression with these drivers, refined by expert consensus, projects values to 2030. ARIMA smoothing resolves short-term shocks. Gaps in operator disclosures are bridged with proxy ratios from closely matched listed peers.

Data Validation & Update Cycle

Outputs undergo variance scans against historical NBS and customs series; anomalies trigger re-checks with subject experts before sign-off. Mordor refreshes the dataset annually and revisits the model whenever regulatory shifts or major capacity additions exceed preset thresholds, ensuring clients always receive the latest view.

Why Mordor's China Cold Chain Logistics Baseline Commands Reliability

Published estimates often diverge because firms slice the market differently, choose varied price decks, or refresh on unequal calendars.

Key gap drivers stem from scope breadth, as some exclude value-added services, currency conversions, and whether e-commerce last-mile legs are counted. Mordor captures the full logistics chain and updates right after mid-year CFLP releases; others frequently rely on older inventory surveys or assume flat tariffs through the horizon.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 94.46 B (2025) | Mordor Intelligence | - |

| USD 17.20 B (2024) | Regional Consultancy A | Omits intra-city last-mile legs; uses listed-company revenue only |

| USD 51.10 B (2024) | Industry Association B | Excludes monitoring equipment revenue; applies constant RMB-USD rate across forecast |

Taken together, the comparison shows that when the full service stack and up-to-date pricing are applied, Mordor delivers a balanced, transparent baseline that decision-makers can confidently rely on.

Key Questions Answered in the Report

What is the expected size of the China Cold Chain Logistics market by 2031?

The market is projected to reach USD 172.6 billion by 2031.

Which region currently holds the largest China Cold Chain Logistics market share?

East China leads with just over one-third of national revenue.

Which service segment is growing fastest within the China Cold Chain Logistics industry?

Value-added services, such as packaging and quality inspection, are expanding more quickly than basic storage or transport.

Why is the pharmaceutical cold chain becoming more prominent?

Stringent GDP rules and growth in biologics exports require ultra-low temperature control, creating higher-margin lanes for compliant providers.

What challenge most affects last-mile cold deliveries?

A fragmented network of small carriers lacking temperature-controlled vans leads to higher spoilage rates in tier-three cities.

How does the 14th Five-Year Plan influence cold chain investment?

The plan funds new hubs across central and western provinces, accelerating infrastructure growth beyond coastal regions.

Page last updated on: