Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

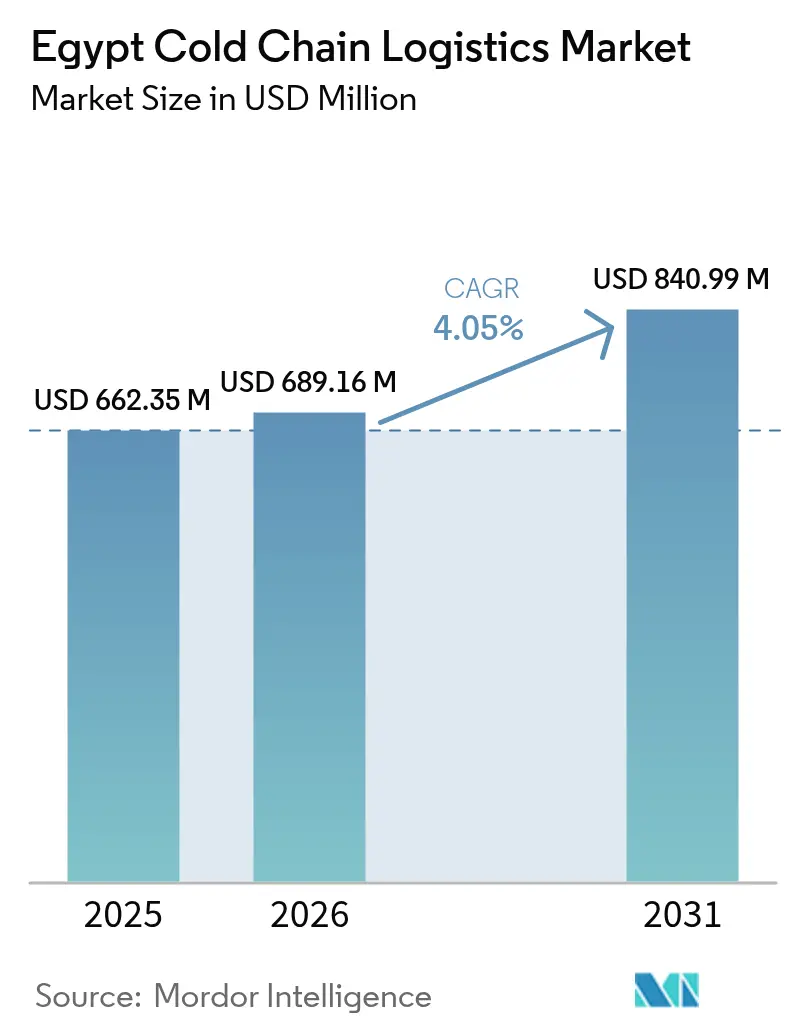

| Base Year Market Size (2025) | USD 662.35 Million |

| Market Size (2026) | USD 689.16 Million |

| Market Size (2031) | USD 840.99 Million |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Cold Chain Logistics Market Analysis by Mordor Intelligence

Egypt cold chain logistics market size in 2026 is estimated at USD 689.16 million, growing from 2025 value of USD 662.35 million with 2031 projections showing USD 840.99 million, growing at 4.05% CAGR over 2026-2031. This market size growth is powered by record processed-food exports, double-digit expansion in pharmaceuticals, and steady government investment in logistics corridors that connect Africa, Europe, and Asia. Egypt’s position on the Suez Canal, combined with the National Single Window for Foreign Trade Facilitation (Nafeza) that now covers 95% of imports and exports, shortens customs clearance times and attracts global logistics players[1]English Ahram, “President Sisi directs government to turn Egypt into int'l logistics hub,” Ahram.org.eg. Private operators are rapidly adding Grade-A refrigerated space, while adoption of IoT temperature-monitoring systems is driving real-time quality control and reducing spoilage rates. However, Red Sea disruptions that lowered Suez Canal revenues by 60% in 2024, volatile energy prices, and foreign-exchange shortages affecting imported refrigeration equipment temper the overall momentum.

Key Report Takeaways

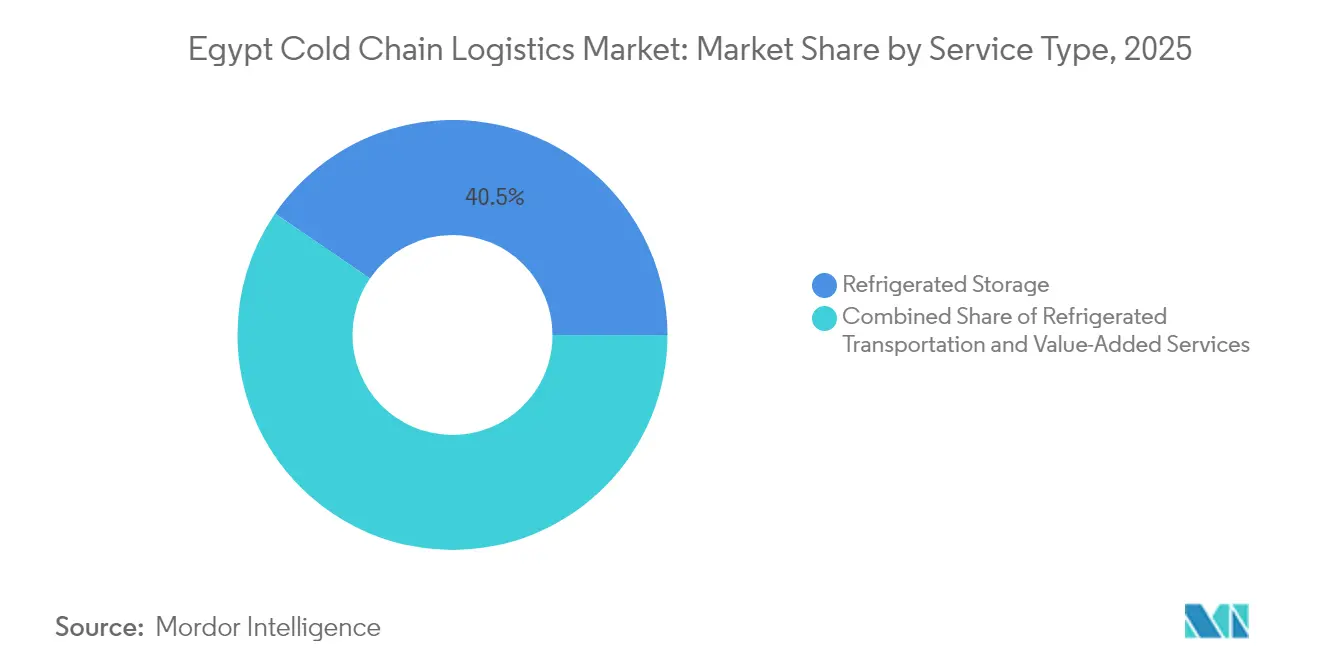

- By service type, refrigerated storage led with 40.45% of Egypt cold chain logistics market share in 2025, while value-added services are projected to register a 4.12% CAGR to 2031.

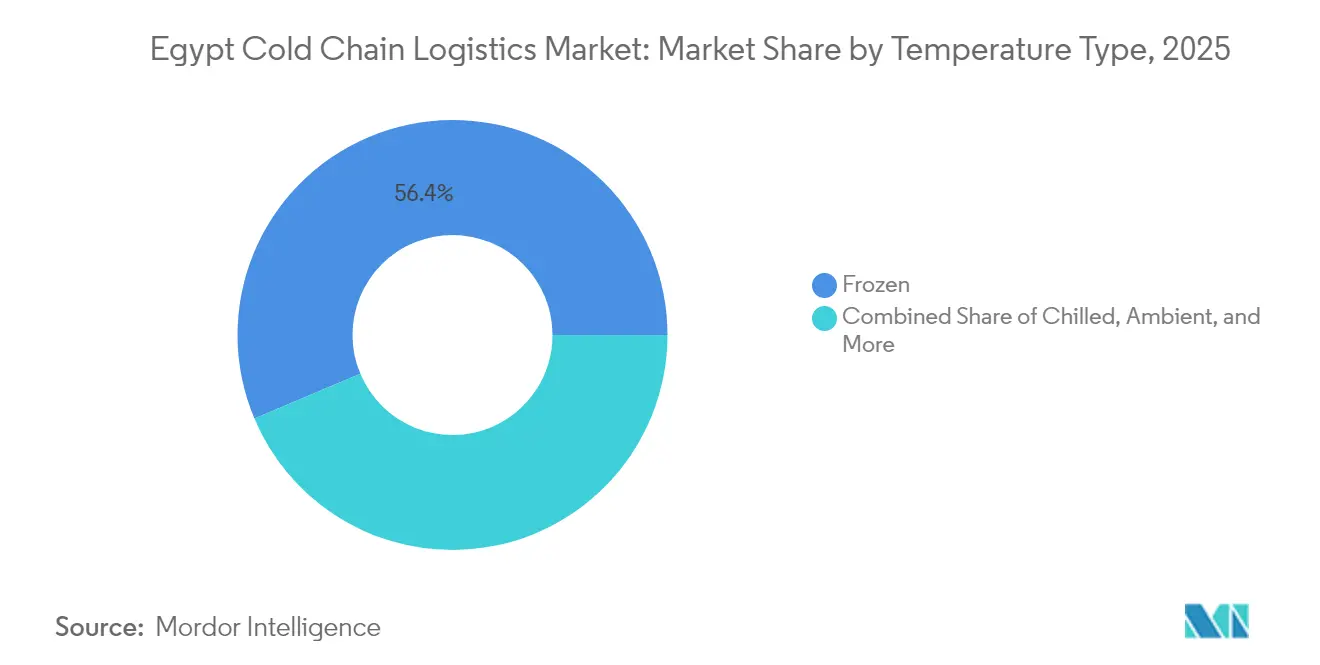

- By temperature type, the frozen (-18 °C to 0 °C) segment accounted for 56.35% of Egypt cold chain logistics market size in 2025; chilled (0 °C to 5 °C) applications are forecast to expand at a 4.88% CAGR through 2031.

- By application, meat & poultry held 27.45% of Egypt cold chain logistics market share in 2025; ready-to-eat meals are expected to post the quickest growth at a 4.11% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Evolving consumer preference for fresh & frozen foods | +0.8% | National—Cairo, Alexandria, Giza | Medium term (2-4 years) |

| Accelerating pharmaceutical cold-chain demand | +1.2% | Cairo and Alexandria | Short term (≤ 2 years) |

| Government investments in logistics corridors & inland ports | +0.9% | Suez Canal Economic Zone, Port Said | Long term (≥ 4 years) |

| Adoption of IoT-enabled temperature-monitoring systems | +0.6% | Major cities | Medium term (2-4 years) |

| Suez Canal Free-zone push to be MENA re-export hub | +0.7% | Suez Canal Economic Zone | Long term (≥ 4 years) |

| Surge in processed-food exports | +1.0% | Coastal export hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Evolving Consumer Preference for Fresh & Frozen Foods

Processed-food exports climbed to USD 6.1 billion in 2024, a 21% annual increase that underscores Egypt’s growing role as a food-processing hub. Frozen potato shipments alone surged 923%, demonstrating the reliability of the Egypt cold chain logistics market in meeting stringent quality standards. Arab countries absorb 54% of outbound volumes, while the European Union and the United States represent high-margin destinations. The “Future of Egypt” agricultural initiative is equipping new grain silos with cooling stages, signaling policy support for temperature-controlled infrastructure[2]State Information Service, “President El-Sisi Inaugurates 2024 Harvest Season of ‘Egypt’s Future’,” Sis.gov.eg. Urban consumers are also shifting toward convenience products with longer shelf lives, spurring demand for chilled and frozen distribution networks across secondary cities.

Accelerating Pharmaceutical Cold-Chain Demand

Pharmaceutical sales rose 42% year-on-year to EGP 292 billion (USD 5.7 billion) in 2024, aided by Egyptian Drug Authority price approvals and reduced drug shortages. Good Distribution Practice requirements mandate continuous temperature tracking for biologics and vaccines, elevating service standards within the Egypt cold chain logistics market. CACC Cargolinx secured IATA CEIV Pharma certification for its 10,000 m² terminal at Cairo International Airport, setting a benchmark for GDP-compliant facilities. DHL Group’s EUR 2 billion (USD 2.08 billion) global healthcare logistics plan earmarks new GDP hubs and temperature-controlled fleets that will boost local capacity. Rising biologics volumes and Egypt’s regional export ambitions are therefore translating into premium contract opportunities for specialized cold-chain operators.

Government Investments in Logistics Corridors & Inland Ports

The state allocated USD 153 million to develop grain handling and 20 high-capacity silos inside the Suez Canal Economic Zone, reinforcing its strategy to become a regional trans-shipment center. Hutchison Ports committed USD 700 million to new terminals at Sokhna and Alexandria, with Sokhna alone adding 1.7 million TEU of annual capacity. DP World is finalizing a USD 80 million logistics hub expected to streamline multimodal flows along the Red Sea corridor. These projects, combined with Nafeza’s end-to-end digital customs clearance, shorten dwell times for temperature-sensitive cargo and expand total Egypt cold chain logistics market capacity.

Adoption of IoT-Enabled Temperature-Monitoring Systems

Cloud-connected sensors now achieve 98.35% upload success and 0.64-second data latency, enabling real-time intervention when excursions occur[3]MDPI Authors, “Blockchain-Based Mobile IoT System with Configurable Sensor Modules,” Mdpi.com. Deep-learning algorithms executed on low-power microcontrollers deliver 92% accuracy in spotting cold-room anomalies that could threaten vaccine potency[4]Frontiers Researchers, “Real-time temperature anomaly detection in vaccine refrigeration systems,” Frontiersin.org. Cairo-based ReNile offers modular IoT platforms for agriculture and industry, proving domestic capability in high-tech monitoring solutions. Blockchain integration guarantees tamper-proof logs, satisfying regulator demands for traceability across the Egypt cold chain logistics market. These technologies are indispensable in a climate where summer temperatures frequently exceed 40 °C.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Grade-A cold-storage capacity in secondary cities | -0.7% | Upper Egypt & emerging urban centers | Medium term (2-4 years) |

| High electricity tariffs & diesel price volatility | -0.9% | National | Short term (≤ 2 years) |

| FX shortages inflating refrigerant & equipment costs | -1.1% | National | Short term (≤ 2 years) |

| Fragmented biosafety regulations for biologics | -0.5% | Pharmaceutical clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Grade-A Cold-Storage Capacity in Secondary Cities

Refrigeration assets cluster around Greater Cairo and Alexandria, forcing distributors to operate costly hub-and-spoke routes to underserved governorates. Capacity shortages in Upper Egypt raise last-mile costs, prolong transit times, and heighten temperature-excursion risk. Although private projects—such as Sharp Corporation’s joint venture that will add 400,000 refrigerator units annually from March 2026—address the gap, new facilities will not come online fast enough to fully satisfy emerging demand. The imbalance constrains the Egypt cold chain logistics market from realizing its full national footprint.

High Electricity Tariffs & Diesel Price Volatility

Rolling power cuts and LNG import needs highlight systemic energy stress. Diesel shortages have produced fuel queues and black-market premiums, lifting refrigerated-transport costs and eroding operator margins. Egypt aims to lift renewable-energy contribution to 42% by 2030, yet capital outlays during the transition could inflate tariffs. Continuous refrigeration loads limit providers’ ability to defer consumption, making the Egypt cold chain logistics market highly sensitive to utility pricing swings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Storage Dominates Infrastructure Investment

Refrigerated storage accounted for 40.45% of Egypt cold chain logistics market size in 2025, reflecting sustained capital flows into large, multi-temperature facilities positioned near ports and agro-processing clusters. Logistica’s 50,000 m² warehouse capable of –30 °C to +25 °C operations illustrates the scale of current assets. Operators leverage these hubs to consolidate seafood, meat, and pharma cargo before re-export through the Suez axis. Refrigerated transportation ranks second, supported by a road network spanning 30,000 km and strategic proximity to Mediterranean and Red Sea routes that allow multimodal hand-offs.

Value-added services—ranging from kitting and blast-freezing to GDP audit support—are projected to grow at a 4.12% CAGR (2026-2031), outpacing core storage and transport. Uptake of IoT track-and-trace, repacking for export, and quality-control analytics positions this niche as a profit center within the broader Egypt cold chain logistics market. Certified air-cargo handlers such as CACC Cargolinx use pharmaceutical handling accreditation to differentiate in a fragmented field. Small and midsize shippers increasingly outsource complex compliance tasks, deepening demand for bundled services.

By Temperature Type: Frozen Segment Leads Market Share

The frozen band (-18 °C to 0 °C) commanded 56.35% of Egypt cold chain logistics market share in 2025 on the back of robust poultry processing and the 923% jump in frozen potato exports. Frozen proteins ship to Gulf Cooperation Council countries with transit times under five days, requiring high-efficiency blast freezers and insulated trucks. Ultra-low (below –20 °C) demand is modest yet rising, led by cell-therapy inputs and mRNA-based vaccine research that require –70 °C or colder storage.

Chilled cargo is forecast to post a 4.88% CAGR (2026-2031), the fastest among temperature bands, as urban consumers favor fresh dairy, cut vegetables, and premium ready-to-eat meals. IoT anomaly detection that offers 92% predictive accuracy is critical for safeguarding chilled goods, which are more susceptible to short-term thermal shocks. Ambient storage retains strategic importance for packaging and buffer inventory, but contributes limited revenue to the total Egypt cold chain logistics market size.

By Application: Meat & Poultry Drives Volume Demand

Meat & poultry generated 27.45% of 2025 revenue, supported by expanded domestic livestock operations and regional export routes to North Africa and the Gulf. The “Future of Egypt” initiative earmarks modern slaughterhouses and feedlots, ensuring steady throughput for cold-chain nodes. Fish & seafood volumes are climbing as the Al Fayrouz aquaculture project ramps production to 150,000 tons annually, much of which requires frozen or chilled carriage.

Ready-to-eat meals are on track for a 4.11% CAGR (2026-2031). Growing middle-class employment, longer commutes, and the rise of e-grocery platforms are reshaping purchase habits toward convenience SKUs that rely on reliable chilled distribution to store shelves and homes. Pharmaceutical and biologics shipments, though smaller in tonnage, command premium yields and stringent compliance, reinforcing their strategic value inside the Egypt cold chain logistics market.

Geography Analysis

Greater Cairo, Alexandria, and the Suez Canal Economic Zone capture the lion’s share of Egypt cold chain logistics market size thanks to port connectivity, population density, and proximity to processing clusters. A USD 153 million grain hub with 20 silos in East Port Said strengthens northern corridor capacity and will hold up to 6 million tons of cereals annually. Despite the 2024 Red Sea crisis that shaved USD 7 billion from Suez Canal receipts, the Economic Zone still reported 38% revenue growth in 2025, proving resilience.

Coastal governorates, including Port Said and Suez, are focal points for export-oriented processors seeking fast maritime links to Europe and the Middle East. AD Ports Group’s 50-year concession to develop KEZAD East Port Said underscores long-term investor confidence in Egypt’s logistics throughput potential. Together, these geographic nodes reinforce Egypt’s role as a gateway for temperature-sensitive trade between three continents.

Competitive Landscape

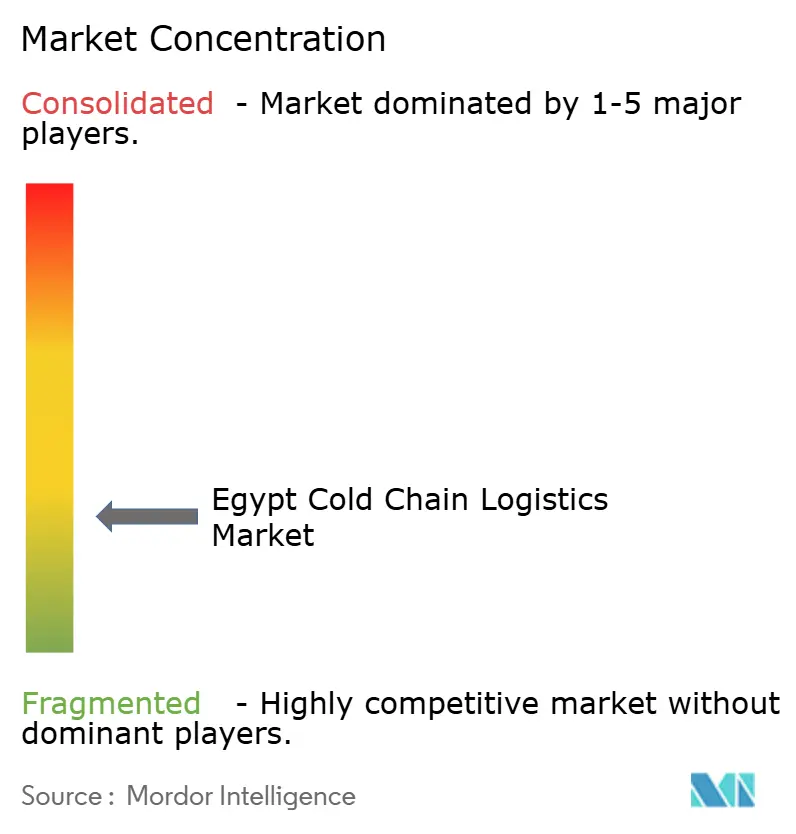

Domestic specialists, multinational integrators, and niche technology vendors collectively shape a moderately fragmented Egypt cold chain logistics market. Logistica dominates large-scale storage through its 50,000 m² multi-temperature complex outside Cairo, catering to FMCG and pharma clients alike. CACC Cargolinx differentiates through IATA CEIV Pharma certification, granting preferred-carrier status for vaccine imports and exports.

Global heavyweights are injecting capital and know-how. DHL Group earmarked EUR 2 billion (USD 2.08 billion) for health-care logistics upgrades that include GDP-certified hubs and an expanded fleet of dual-temperature vehicles. Kuehne + Nagel posted 19% turnover growth in Q3 2024 as Egyptian shippers sought flexible routings during Suez disruptions. These players couple global networks with local partnerships to secure end-to-end control across ocean, air, and last-mile modes.

Technology adoption is an emerging battleground. IoT sensors with blockchain-verified data are gaining traction among compliance-intensive pharmaceutical clients. Local start-up ReNile supplies customizable IoT modules, giving smaller operators an affordable entry to digital monitoring. In secondary cities where capacity lags, regional operators with first-mover cold storage have the potential to cement strongholds before global entrants scale inland.

Egypt Cold Chain Logistics Industry Leaders

Logistica

Logistics for Storage Services (S.A.E)

Custom Storage Company (CSC)

SulleX

EPx Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: EPX partnered with Smartlog to automate its new pharma logistics center, integrating advanced WMS for secure, temperature-sensitive handling.

- April 2025: DHL Group confirmed a EUR 2 billion (USD 2.08 billion) commitment to health-care logistics that expands GDP-certified cold-chain hubs and temperature-controlled vehicle fleets.

- February 2025: DP World neared completion of a USD 80 million logistics hub designed to streamline temperature-controlled flows along the Red Sea corridor.

- February 2024: Sullex broke ground on SulleX-TRC, a USD 150 million smart temperature-controlled logistics city covering 510,000 m² in Giza.

Egypt Cold Chain Logistics Market Report Scope

The technology and mechanism that allows for the secure delivery of temperature-sensitive goods and items along the supply chain are known as cold chain logistics. Any product that is perishable or is branded as such would almost certainly need cold chain management. Foods, including meat and fish, produce, medical supplies, and pharmaceuticals, could all fall under this category.

A comprehensive background analysis of the Egypt cold chain logistics market covering the current market trends, restraints, technological updates, and detailed information on various segments and the competitive landscape of the industry. The impact of COVID-19 has also been incorporated and considered during the study.

The Egypt cold chain logistics market is segmented by service (storage, transportation, and value-added services (blast freezing, labeling, and inventory management), by temperature (chilled and frozen), and by end-user (horticulture (fresh fruits and vegetables), dairy products (milk, ice-cream, and butter), meats, fish, poultry, processed food products, pharma, life sciences, and chemicals, and other end users). the report offers market size and forecasts for the Egypt cold chain logistics market in value (USD) for all the above segments.

By Service Type

| Refrigerated Storage | Public Warehousing |

| Private Warehousing | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

By Temperature Type

| Chilled (0–5 °C) |

| Frozen (-18–0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

By Application

| Fruits & Vegetables |

| Meat & Poultry |

| Fish & Seafood |

| Dairy & Frozen Desserts |

| Bakery & Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals & Biologics |

| Vaccines & Clinical Trial Materials |

| Chemicals & Specialty Materials |

| Other Application |

| By Service Type | Refrigerated Storage | Public Warehousing |

| Private Warehousing | ||

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0–5 °C) | |

| Frozen (-18–0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Application | Fruits & Vegetables | |

| Meat & Poultry | ||

| Fish & Seafood | ||

| Dairy & Frozen Desserts | ||

| Bakery & Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals & Biologics | ||

| Vaccines & Clinical Trial Materials | ||

| Chemicals & Specialty Materials | ||

| Other Application | ||

Key Questions Answered in the Report

How big is the Egypt cold chain logistics market in 2026?

The market stands at USD 689.16 million in 2026 and is projected to grow at a 4.05% CAGR through 2031.

Which service segment leads revenue?

Refrigerated storage accounts for 40.45% of 2025 revenue due to heavy investment in multi-temperature warehouses.

What temperature range is expanding fastest?

Chilled cargo (0 °C–5 °C) is forecast to grow at 4.88% annually, driven by fresh-food and biologics demand.

How are Red Sea disruptions affecting operators?

Suez Canal revenue declines have lengthened transit loops, prompting carriers to reroute and raising freight costs.

Which application segment offers the highest growth?

Ready-to-eat meals will advance at a 4.11% CAGR as urban consumers favor convenience foods requiring reliable cold chains.

What technology is most transformative?

IoT sensors with blockchain-backed data provide real-time temperature tracking, reducing spoilage and supporting GDP compliance.

Page last updated on: