Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

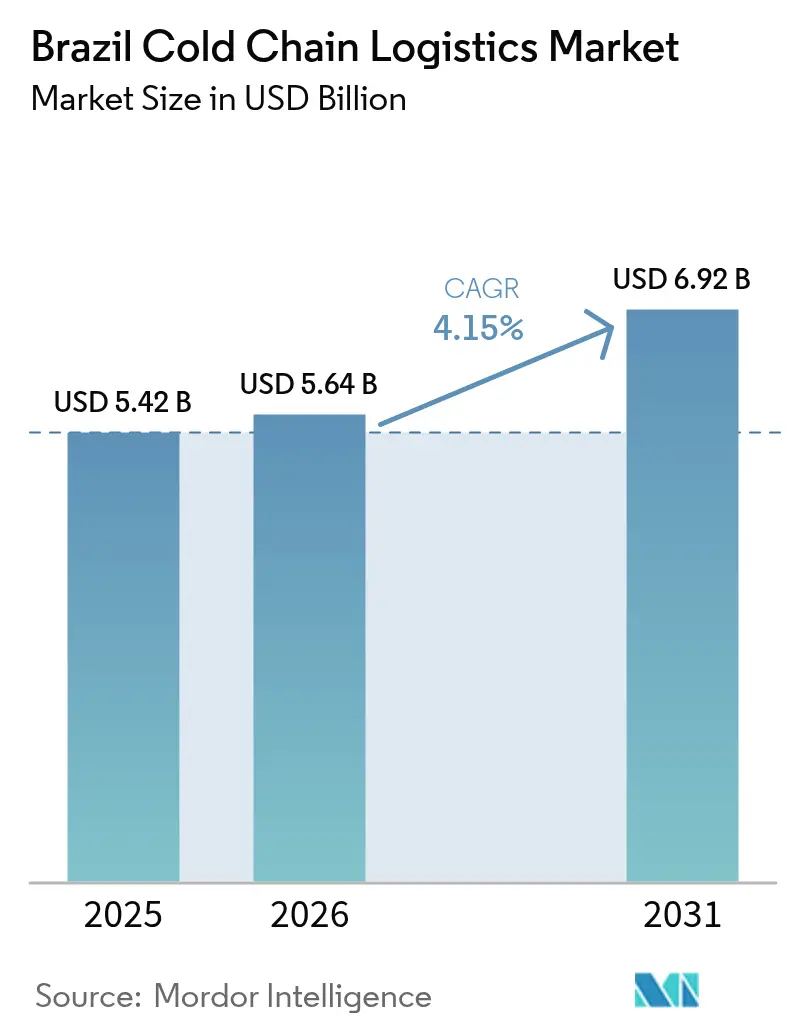

| Base Year Market Size (2025) | USD 5.42 Billion |

| Market Size (2026) | USD 5.64 Billion |

| Market Size (2031) | USD 6.92 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

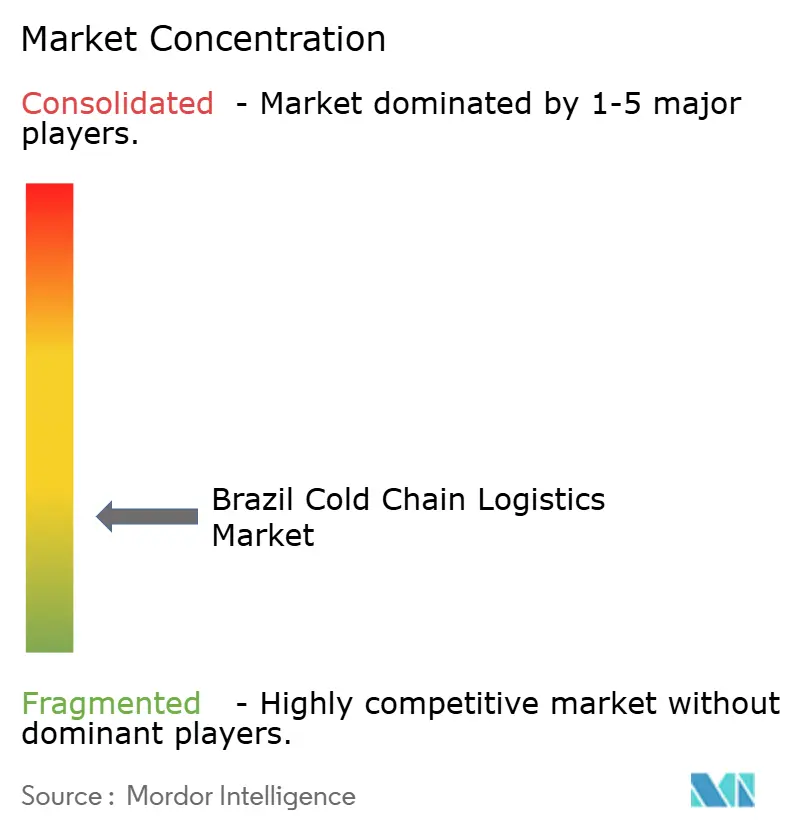

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Cold Chain Logistics Market Analysis by Mordor Intelligence

The Brazil Cold Chain Logistics Market size is expected to grow from USD 5.42 billion in 2025 to USD 5.64 billion in 2026 and is forecast to reach USD 6.92 billion by 2031 at 4.15% CAGR over 2026-2031.

The growth trajectory is supported by the country’s role as a high-volume agricultural exporter, the rapid scale-up of domestic vaccine production, and rising urban demand for convenience foods. Investments in multimodal infrastructure, digitalized warehouse management, and ultra-low-temperature storage continue to lift service quality, even as chronic electricity price volatility and driver shortages elevate operating costs. International entrants are accelerating technology transfer and ESG standards, while local specialists defend market share through geographic coverage and long-term customer contracts. Although the economy faces cyclical headwinds, the structural drivers behind temperature-controlled logistics food safety rules, e-commerce fulfillment expectations, and the reshoring of biopharma manufacturing remain intact, anchoring medium-term opportunities in the Brazil cold chain logistics market.

Key Report Takeaways

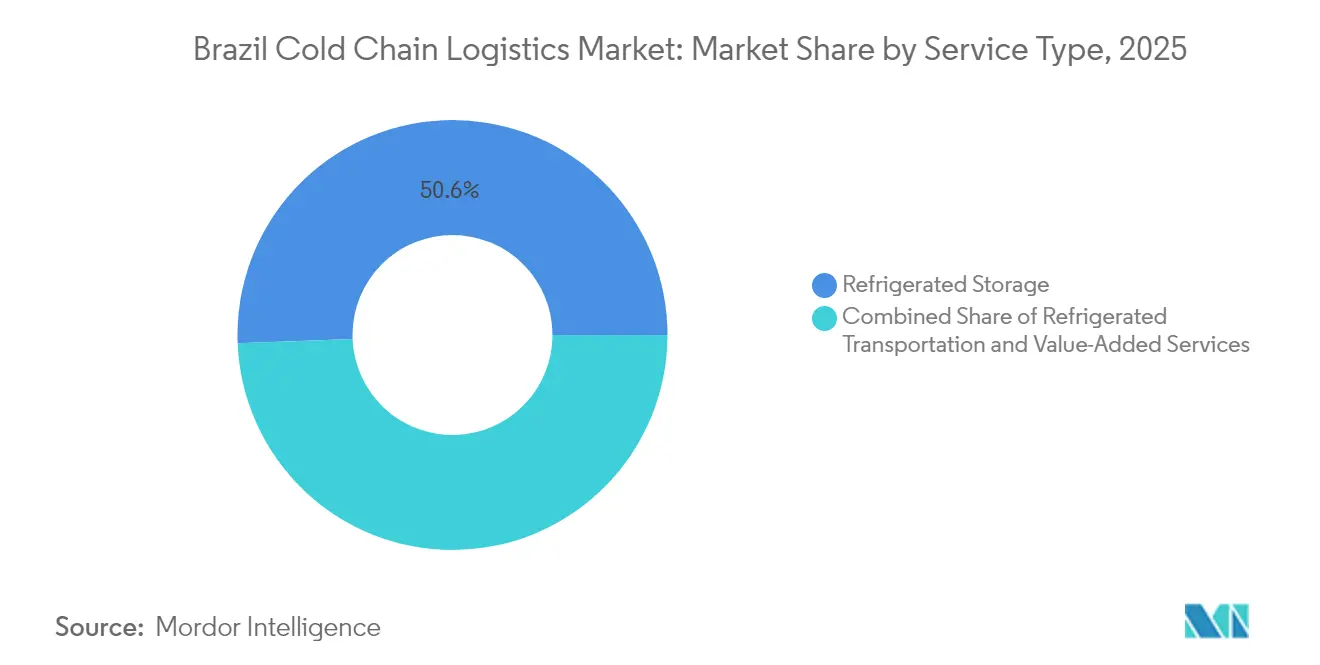

- By service type, Refrigerated Storage led with 50.62% revenue share in 2025, while Value-Added Services is forecast to expand at a 4.16% CAGR through 2031.

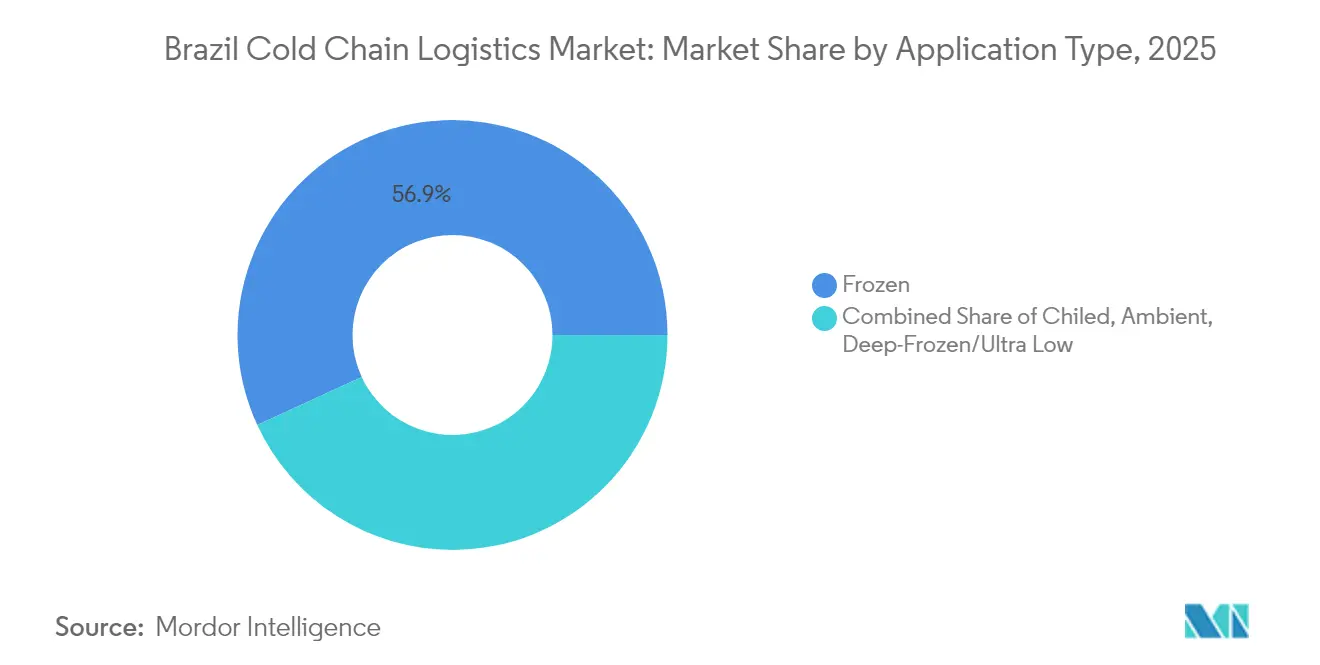

- By temperature range, Frozen (-18 °C–0 °C) captured 56.88% of Brazil cold chain logistics market share in 2025; Chilled (0 °C–5 °C) is advancing at a 3.58% CAGR to 2031.

- By application, Meat & Poultry accounted for 29.05% of the Brazil cold chain logistics market size in 2025, whereas Ready-to-Eat Meals is projected to grow at 4.26% CAGR between 2026 and 2031.

- By geography, the Southeast corridor commanded the largest slice of the Brazil cold chain logistics market in 2025, and the North–Northeast cluster is the fastest-growing area at a mid-single-digit CAGR, supported by PAC-funded distribution centers.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming national demand for frozen ready-to-eat meals | 0.8% | National, concentrated in São Paulo, Rio de Janeiro, Brasília | Medium term (2-4 years) |

| Rapid growth of pharmaceutical biologics & vaccines | 1.2% | National, with manufacturing hubs in São Paulo, Rio de Janeiro | Long term (≥ 4 years) |

| Acceleration of supermarket e-commerce fulfilment | 0.9% | National, urban centers leading adoption | Short term (≤ 2 years) |

| Government-funded expansions of regional distribution centres | 0.7% | North & Northeast regions, secondary cities | Long term (≥ 4 years) |

| On-port pre-cooling incentives for perishable exporters | 0.4% | Coastal regions, Santos, Rio Grande, Paranaguá ports | Medium term (2-4 years) |

| Emergence of carbon-credit-linked refrigeration financing | 0.3% | National, industrial zones prioritized | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Booming Frozen Ready-to-Eat Meal Demand

Brazilian urban households are reallocating disposable income toward convenience, lifting frozen entrée volumes across modern retail and food-service channels. Rising female workforce participation shortens cooking times, and dual-income families intensify weekday demand for portion-controlled frozen options. National restaurant-to-home delivery platforms are adding chilled lockers inside residential complexes to preserve temperature integrity until pick-up, reinforcing the need for short-haul urban refrigerated fleets. Retail groups have responded by designating expanded freezer aisles for premium protein-rich dishes, requiring additional back-of-store blast-freezing capacity. Cold storage operators are monetizing the trend by renting pallet positions on seasonal contracts aligned to holiday peaks. Importantly, mid-sized regional processors prefer outsourcing value-added services, such as in-line IQF glazing and nitrogen tunnel freezing, to mitigate capital outlays on specialized equipment[1]“Governo Federal anuncia primeira vacina 100% nacional e de dose única contra a dengue,” Government of Brazil, gov.br.

Rapid Growth of Pharmaceutical Biologics and Vaccines

Federal incentives for on-shore vaccine sovereignty have triggered unprecedented upgrades in ultra-low-temperature storage. Instituto Butantan’s facility expansion to supply 60 million dengue doses per year starting in 2026 demands consistent -60 °C to -80 °C lanes from plant to public clinic. Similar conditions apply to mRNA investigational products handled by private CROs at hub sites in Campinas and Rio[2]“How Brazil’s 2035 logistics plan could transform crop production and global trade,” Purdue University Agribusiness, agribusiness.purdue.edu. Multinationals have responded: DHL is rolling out GDP-certified pharma hubs calibrated for lane risk mapping and active container staging. Smart-probe IoT devices integrated with digital control towers transmit location and temperature every fifteen minutes, enabling predictive hold-over power management during blackouts. Insurance providers now price premium reductions for validated data trails, reinforcing adoption.

Acceleration of Supermarket E-commerce Fulfillment

Online grocery share accelerated post-pandemic and continues to expand as retailers promise two-hour delivery windows under dynamic pricing. Mercado Libre’s plan to lift national DC count from 10 to 21 by end-2025 adds 880,000 m² of multizone climate-controlled capacity. Mixed-temperature orders require mathematically optimized pick sequencing, and retailers are investing in shuttle systems that combine frozen, chilled, and ambient items into insulated totes. Autonomous routing software increases truck fill factors while minimizing door-open events, lowering spoilage. The shift toward e-commerce elevates demand for city micro-fulfillment nodes with cross-docking functions that can reset pack temperatures before last-mile dispatch.

Government-Funded Regional Distribution Centers

The Growth Acceleration Program channels concessional credit toward hinterland DCs, aiming to bridge north–south logistics cost gaps. The Transnordestina railway revival captures grain and meat flows from interior producing belts, offering energy-efficient alternatives to diesel road hauls. Cold-chain investors gain multi-year property-tax abatements conditional on deploying solar-assisted refrigeration and training local technicians. Regional cooperatives use the new facilities to consolidate fruit exports, cutting pre-cooling time at ports and raising product premiums. The initiatives also seed retail expansion as modern supermarkets follow infrastructure upgrades[3]“A Brazilian breakthrough in eco-friendly refrigeration,” United Nations Industrial Development Organization, unido.org.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic electricity price volatility | -0.6% | National, industrial regions most affected | Short term (≤ 2 years) |

| Truck driver shortage & restrictive driving-time rules | -0.4% | National, long-haul routes severely impacted | Medium term (2-4 years) |

| Fragmented last-mile infrastructure in North & Northeast | -0.3% | North & Northeast regions, rural areas | Long term (≥ 4 years) |

| Lack of uniform GDP-compliant quality audits | -0.2% | National, pharmaceutical sector priority | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic Electricity Price Volatility

Aging grid assets and extreme-weather-related outages forced cold-store operators to activate diesel gensets eleven times on average in 2024. Each event added unbudgeted fuel cost and compressor restart stress, cutting equipment life. Grid planners foresee 50% distributed-generation penetration by 2029 without matching transmission upgrades, implying continued tariff fluctuation. Operators are countering through variable-frequency drives, phase-change buffer walls, and rooftop solar arrays with lithium-ion storage sized for four-hour autonomy. While capex is high, loan guarantees under the BRL 186.6 billion (USD 38.44 billion) industrial digitalization program lower financing costs. However, small warehousing cooperatives still struggle to self-fund resiliency measures, limiting overall industrywide impact.

Truck Driver Shortage & Restrictive Driving-Time Rules

Long-haul refrigerated carriers operate with a vacancy rate near 12%, driven by demographic attrition and regulatory limits capping consecutive hours behind the wheel. Cold chain timetables are particularly exposed because temperature deviation risk heightens with unplanned layovers. Spot freight rates on the North-South corridor rose in mid-2025 as shippers competed for compliant capacity. Fleet operators try to retain drivers via profit-sharing and cab comfort upgrades, but training throughput lags retirements. Logistics associations lobby for modular road-train allowances to move larger volumes per driver, yet infrastructure readiness (bridge weight limits, turn radii) remains patchy. Autonomous platooning pilot projects by Volvo and Scania offer a long-term pathway, though commercial deployment is several years away.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Storage Dominates, Services Differentiate

Refrigerated Storage accounted for 50.62% of Brazil cold chain logistics market share in 2025, reflecting the need to buffer protein exports and synchronize farm output with vessel schedules. Value-Added Services registered the fastest 4.16% CAGR forecast, propelled by client outsourcing of labeling, blast-freezing, kitting, and GDP compliance audits. Multinational 3PLs leverage standardized SOPs to win pharmaceutical contracts, while domestic warehouse specialists such as SuperFrio add bespoke chambers sized for butchered carcasses and IQF berries. Brazil cold chain logistics market size tied to private storage is widening faster than public facilities because producers prefer dedicated racking heights, ammonia-glycol systems, and integrated WMS interfaces. On the transport front, road continues to dominate, but double-stack reefer railcars on the Ferrovia Norte-Sul corridor demonstrate early proof of concept for lower-carbon long-haul moves.

The rise of value-added outsourcing opens ancillary revenue streams around KPI analytics, pallet-level RFID, and in-house customs brokerage. DHL’s announced EUR 2 billion (USD 2.20 billion) global health-logistics program directs 50% of capex to the Americas, including Brazil, to establish validated pharma hubs and first-to-final-mile cryogenic lanes. Local operators counter by pooling resources; Emergent Cold LatAm’s Rio acquisition delivered convertible chambers that switch between freezer and chiller mode within eight hours, maximizing utilization. These moves illustrate how service breadth and asset flexibility increasingly dictate competitive positioning within the Brazil cold chain logistics market.

By Temperature Type: Frozen Still Leads but Chilled Climbs

Frozen lanes preserved 56.88% of 2025 revenue as Brazil exported high-volume beef, poultry, and seafood under World Organization for Animal Health guidelines. Yet chilled throughput is expanding at a 3.58% CAGR on the back of domestic dairy, craft beverage, and fresh-produce trade. Retailers run category management resets that shrink ambient center-store space in favor of expanded chilled assortments, pushing DC operators to invest in high-humidity dock areas and rapid-cool alcoves. Brazil cold chain logistics market size tied to vaccines also lifts demand for deep-frozen gear: Instituto Butantan’s dengue output needs -60 °C freezers and dual-redundant liquid nitrogen backup. Although ultra-low volumes remain modest, margins are superior because of specialized packaging and validation requirements.

Technological progress accelerates the chilled segment’s momentum. Brazilian OEMs such as Eletrofrio introduced microchannel condensers that cut refrigerant charge by 93% and drop kWh draw 15%, enhancing ROI. Start-ups collaborate with universities on phase-change composite panels that hold 2 °C, -4 °C for 24 hours, enabling non-mechanical last-mile delivery in regions with unstable power. Looking ahead, statewide carbon-credit programs are expected to lower payback periods on hydrocarbon-based chillers, tilting capex decisions toward greener specifications.

By Application: Protein Legacy Meets Convenience Revolution

Meat & Poultry commanded 29.05% of Brazil cold chain logistics market size in 2025 and remains foundational to export receipts. Plants in Mato Grosso spread output across multi-temperature networks, linking grow-out farms to slaughterhouses, distribution centers, and port pre-coolers. Fruits & Vegetables follow as a key user of quick-turnaround chilled storage, with mango, papaya, and melon exporters embracing ethylene scrubber technology to reduce spoilage. Ready-to-Eat Meals, though smaller today, is the fastest-growing category at 4.26% CAGR as lifestyle shifts reinforce single-serve frozen entrée adoption. This segment leans heavily on IQF tunnels, nitrogen dosing, and portion-controlled packaging lines, spurring demand for warehouse zoning that keeps cook-freeze workflows separate from raw protein docks.

Pharmaceuticals & Biologics, including vaccines, post double-digit revenue gains and require precise lane validation, datalogger analytics, and dedicated loading bays with HEPA filtration. Dairy & Frozen Desserts benefit from Nestlé’s USD 1.4 billion investment that modernizes confectionery plants and raises freezer demand for chocolate transport. Chemicals & Specialty Materials remain a niche slice, yet stringent REACH-equivalent regulations motivate chemical shippers to outsource GDP-equivalent audits, bolstering premium margin stacks for certified 3PLs. Collectively, the plural application mix highlights why operators seek modular builds allowing rapid repurposing among protein, produce, and pharma flows hallmarks of a resilient Brazil cold chain logistics market.

Geography Analysis

The Southeast corridor, anchored by Sao Paulo and Rio de Janeiro, captures the lion’s share of Brazil cold chain logistics market activity, owing to port connectivity at Santos and proximity to pharma manufacturing clusters. Sao Paulo’s USD 6 billion infrastructure outlay in 2025 expands highway interchanges and last-mile cold warehouses, amplifying throughput for intra-regional groceries and export-bound proteins. The region also hosts Merck’s USD 21.7 million distribution hub that brings GDP-validated secondary packaging lines under one roof. Dense urban populations further accelerate e-commerce grocery growth, pushing demand for chilled cross-docks within 30 km of high-rise neighborhoods.

Southern states such as Rio Grande do Sul and Paraná rank second in revenue, backed by integrated meat-packing complexes and grain export channels. Flood damage in 2024 exposed vulnerabilities, but utilities subsequently earmarked BRL 1.8 billion (USD 370.82 million) to harden electricity infrastructure, preserving cold-store uptime. Marine gateways at Paranaguá leverage new on-dock pre-cooling incentives that shorten cycle times for fruit exporters and reduce reefer plug queues. Cross-border flows into Uruguay and Argentina use bonded reefer trucks, benefiting from unified sanitary protocols ratified in early 2025.

The North and Northeast, though currently underpenetrated, register the fastest expansion. PAC-financed DCs open capacity pockets in secondary cities such as Feira de Santana, serving as consolidation nodes for tropical fruit and seafood. The Transnordestina railway’s phased activation lowers inland freight costs up to 15% versus road, making chilled melon exports more competitive. Still, fragmented roadways and intermittent power supply mean operators must deploy diesel-backup gensets and mobile data loggers to satisfy importer audit trails. Government ESG policy encourages photovoltaic cold rooms at regional airports, signaling greener growth for the Brazil cold chain logistics market.

Competitive Landscape

Brazil cold chain logistics industry hosts a mixture of domestic specialists and global multinationals, producing a moderately consolidated environment. DHL, Kuehne + Nagel, and Nippon Express leverage global networks, standardized SOPs, and proprietary TMS platforms to court high-value pharma customers. DHL’s takeover of CRYOPDP in March 2025 folds niche cryogenic capabilities into its Brazilian franchise, widening its moat in biologics and clinical-trial support. Emergent Cold LatAm expands footprint by acquiring a Rio facility optimized for multi-temperature switching, signaling rising M&A momentum.

Local champions such as SuperFrio and Brasfrigo lean on extensive hinterland coverage and multi-decade commodity relationships to defend share. Joint-venture models with agribusiness cooperatives enable them to pre-book storage volumes before harvest cycles, ensuring asset utilization. Technology adoption differentiates players: IoT probes, AI-led inventory forecasts, and automated shuttle systems raise throughput per square foot by 18% on average. Sustainability credentials now influence bid awards; fleets with Euro-VI or electric rigid trucks, like Scania’s first 300 km-range unit sold to Reiter Log in late 2024, gain access to low-emission zones.

Regulatory harmonization also shapes rivalry. The advancement of PL 3757/2020 sets baseline obligations for traceability, driver training, and incident reporting, which larger firms absorb with minor incremental cost, while smaller incumbents struggle to upgrade IT systems. As a result, analysts anticipate a gradual rise in market concentration over the next five years, particularly in the pharmaceutical and ready-meal verticals where audit overhead favors scale.

Brazil Cold Chain Logistics Industry Leaders

Friozem Armazens Frigorificos Ltda.

Emergent Cold LatAm

Comfrio Logística

Brado Logistics SA

Movecta

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Nestle announced a BRL 7 billion (USD 1.44 billion) program from 2025 to 2028 to expand production capacity and modernize Brazilian factories in confectionery and coffee segments, enhancing the demand for temperature-controlled distribution.

- April 2025: BNDES, Instituto Butantan, and Finep agreed to invest BRL 200 million (USD 40 million) in health-sector start-ups to strengthen domestic supply chains for the Unified Health System.

- April 2025: DHL Group earmarked EUR 2 billion (USD 2.20 billion) by 2030 for DHL Health Logistics, with half devoted to the Americas, introducing new GDP-certified pharma hubs and extra cryogenic capacity.

- April 2025: The Brazilian Ministry of Health and Gavi signed an MoU to advance local vaccine production and equitable distribution, underscoring reliance on high-specification cold chain corridors.

Brazil Cold Chain Logistics Market Report Scope

The cold chain logistics market involves the transportation of temperature-sensitive products along a supply chain through thermal and refrigerated packaging methods and the logistical planning to protect the integrity of these shipments. Transportation modes used are refrigerated trucks, refrigerated railcars, refrigerated cargo, and air cargo. The report provides key insights into Brazil's cold chain logistics market, including technological developments, trends, and government regulations in the sector. It also focuses on market dynamics, the competitive landscape. and profiles of active key players.

Brazil's cold chain logistics market is segmented by service (storage, transportation, and value-added services), temperature type (chilled and frozen), application (horticulture, meat, fish, poultry, processed food products, pharmaceuticals, life sciences, and chemicals, and other applications), and key cities (Sao Paulo, Rio de Janeiro, and Salvador). The report also covers the impact of COVID-19 on the market. The report offers market size and forecasts in value (USD billion) for all the above segments.

By Service Type

| Refrigerated Storage | Public Warehousing |

| Private Warehousing | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

By Temperature Type

| Chilled (0-5 °C) |

| Frozen (-18-0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

By Application

| Fruits and Vegetables |

| Meat and Poultry |

| Fish and Seafood |

| Dairy and Frozen Desserts |

| Bakery and Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals and Biologics |

| Vaccines and Clinical Trial Materials |

| Chemicals and Specialty Materials |

| Other Perishables |

| By Service Type | Refrigerated Storage | Public Warehousing |

| Private Warehousing | ||

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0-5 °C) | |

| Frozen (-18-0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Application | Fruits and Vegetables | |

| Meat and Poultry | ||

| Fish and Seafood | ||

| Dairy and Frozen Desserts | ||

| Bakery and Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals and Biologics | ||

| Vaccines and Clinical Trial Materials | ||

| Chemicals and Specialty Materials | ||

| Other Perishables | ||

Key Questions Answered in the Report

How large is the Brazil cold chain logistics market in 2026?

Brazil cold chain logistics market size equals USD 5.64 billion in 2026 and is forecast to grow at a 4.15% CAGR to 2031.

Which segment grows fastest through 2031?

Value-Added Services posts the highest 4.16% CAGR as shippers outsource packaging, labeling, and quality audits.

What drives investment in ultra-low-temperature storage?

Domestic vaccine production, led by Instituto Butantan’s dengue program, requires -60 °C to -80 °C capacity and end-to-end traceability.

Why is the Southeast region dominant?

It combines port infrastructure at Santos, dense urban consumption, and the largest pharmaceutical manufacturing base, concentrating demand for temperature-controlled services.

Which restraint pressures margins most?

Volatile electricity pricing raises operating costs for cold warehouses and necessitates expensive backup power systems.

Page last updated on: