Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

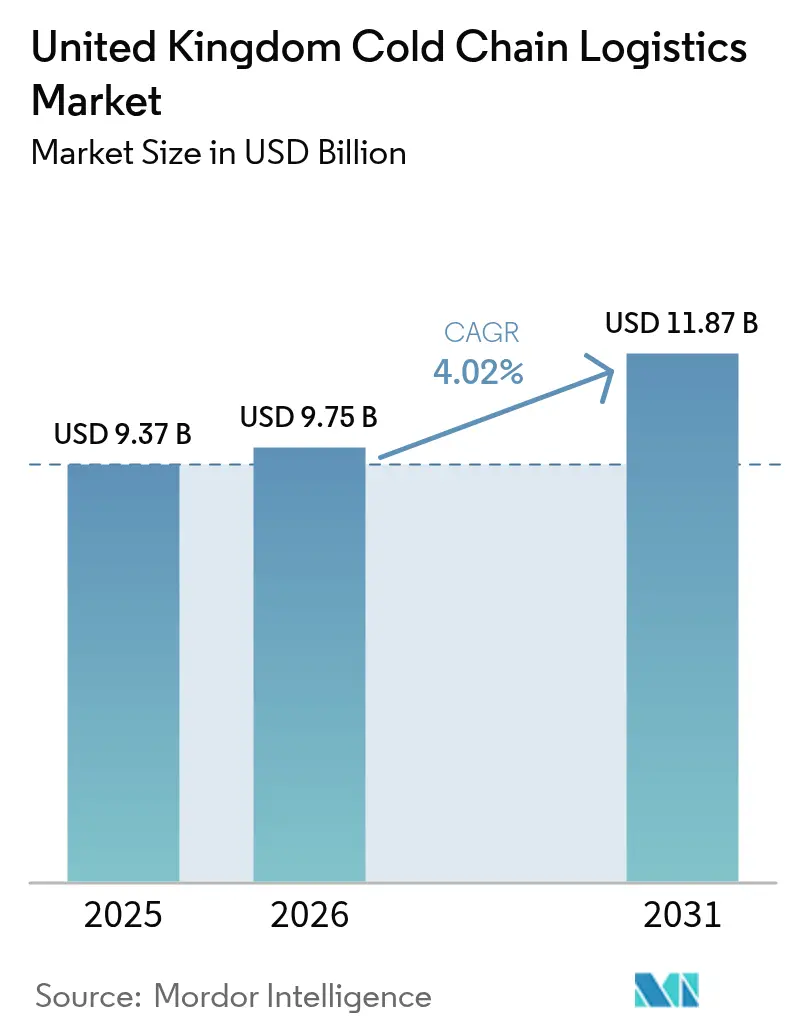

| Base Year Market Size (2025) | USD 9.37 Billion |

| Market Size (2026) | USD 9.75 Billion |

| Market Size (2031) | USD 11.87 Billion |

| Growth Rate (2026 - 2031) | 4.02% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Cold Chain Logistics Market Analysis by Mordor Intelligence

The United Kingdom Cold Chain Logistics Market size was valued at USD 9.37 billion in 2025 and estimated to grow from USD 9.75 billion in 2026 to reach USD 11.87 billion by 2031, at a CAGR of 4.02% during the forecast period (2026-2031).

The market size growth is driven by rising pharmaceutical exports, stricter food-safety laws, and a steady shift toward e-grocery purchases. Consolidation among third-party logistics providers adds scale efficiencies, while sustainability mandates accelerate investment in energy-efficient warehouses and low-emission fleets. Regulatory clarity after Brexit has lengthened customs lead-times but also compelled operators to upgrade traceability systems, reinforcing service demand in the United Kingdom cold chain logistics market. Technology adoption, especially IoT sensors and digital twins, enhances temperature compliance and cost visibility across the supply chain.

Key Report Takeaways

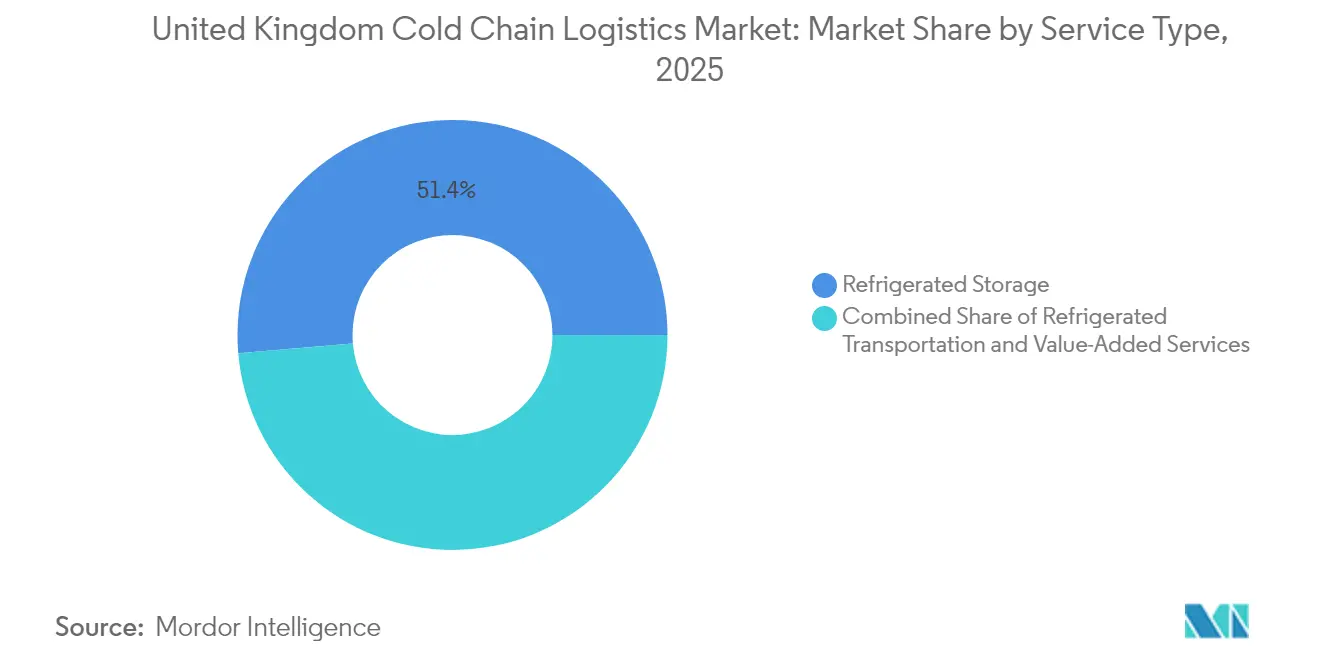

- By service type, refrigerated storage held 51.35% of United Kingdom cold chain logistics market share in 2025; value-added services are projected to expand at a 4.37% CAGR through 2031.

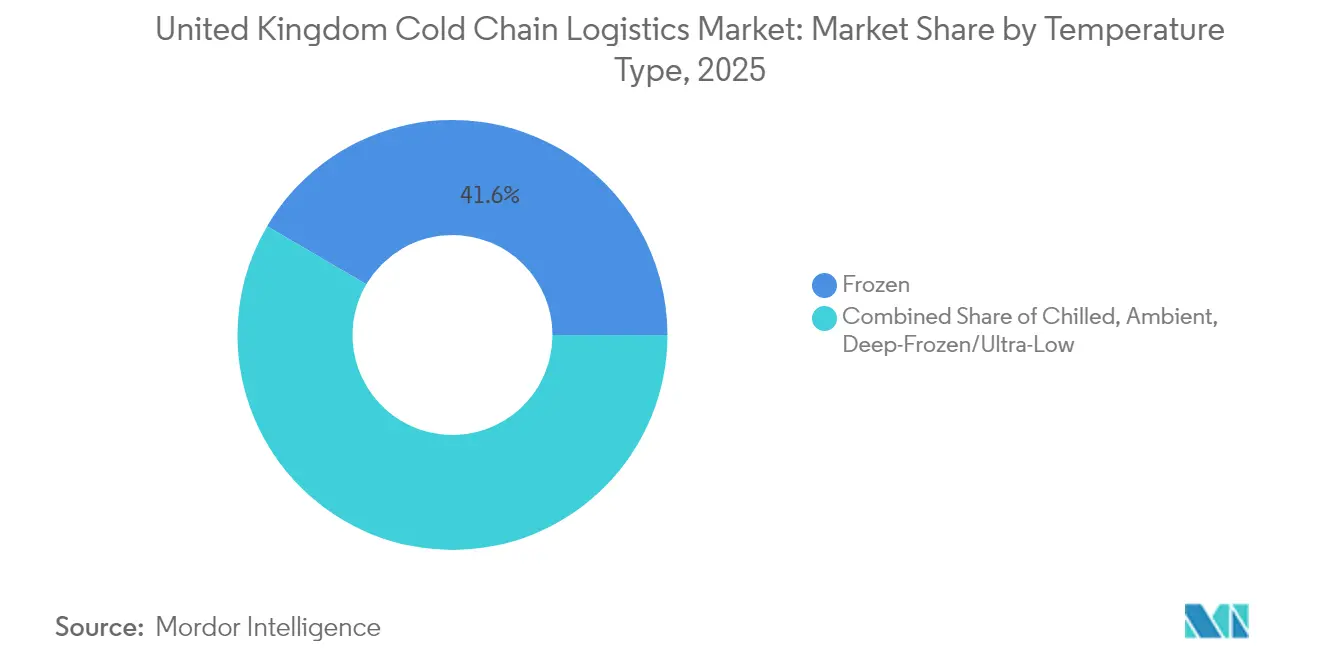

- By temperature type, frozen applications accounted for 41.55% share of the United Kingdom cold chain logistics market size in 2025, while chilled services are poised to grow at a 4.08% CAGR over 2026-2031.

- By application, meat and poultry controlled 23.65% of the United Kingdom cold chain logistics market share in 2025; pharmaceuticals and biologics exhibit the fastest trajectory at 5.26% CAGR to 2031.

- By geography, the South East corridor that includes Dover and London Gateway handled 47.60% of inbound temperature-sensitive import volumes in 2025 and is advancing at a 4.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in online grocery and meal-kit demand | +0.8% | London, Manchester, Birmingham, Edinburgh | Medium term (2-4 years) |

| Expansion of pharmaceutical and biotech exports | +0.7% | Clusters in Cambridge, Oxford, London | Long term (≥ 4 years) |

| Stricter UK food-safety and traceability rules | +0.5% | National, reinforced at border control posts | Short term (≤ 2 years) |

| Rising frozen and convenience-food consumption | +0.4% | Metropolitan regions nationwide | Medium term (2-4 years) |

| On-site renewable-energy microgrids cut OPEX | +0.3% | Industrial estates across the country | Long term (≥ 4 years) |

| Urban micro-fulfilment cold hubs | +0.6% | Major urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in online grocery and meal-kit demand

Post-pandemic purchasing habits have cemented double-digit e-grocery penetration. Large retailers widened distribution footprints, and dark-store conversions inside existing supermarkets reduced capital intensity while sustaining rapid fulfilment. Purpose-built hubs such as a 500,000 sq ft warehouse opened by a leading frozen specialist streamline last-mile chilled delivery[1]“Import food and drink from the EU to Great Britain,” UK Government, gov.uk. Sensor-driven stock-monitoring platforms further improve accuracy and minimize spoilage, reinforcing service uptake within the United Kingdom cold chain logistics market.

Expansion of pharmaceutical and biotech exports

Government backing of GBP 1 billion (USD 1.3 billion) for life-sciences innovation and a sustained 22% rise in temperature-controlled airfreight volumes underscore the export opportunity. Advanced packaging that maintains 2-8 °C or ultra-low parameters for 36 hours without polystyrene positions the United Kingdom cold chain logistics market as a preferred hub for biologics distribution.

Stricter UK food-safety and traceability rules

The Border Target Operating Model mandates health certificates and pre-notifications for medium-risk imports, triggering investment in blockchain-ready traceability platforms able to process 207 transactions per second without data discrepancies. Enhanced compliance costs favor operators with digital capacity, fostering market consolidation.

Rising frozen and convenience-food consumption

Energy-efficient initiatives, including raising freezer settings from −18 °C to −15 °C, lower electricity use by 10-11% while keeping food safe. These savings amplify profitability for frozen storage providers and support steady demand in the United Kingdom cold chain logistics market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and energy costs of facilities | -0.9% | Nationwide, acute where power prices are highest | Short term (≤ 2 years) |

| HGV and reefer-driver labor shortage | -0.7% | Main logistics corridors and ports | Medium term (2-4 years) |

| Limited electric-vehicle charging infrastructure | -0.5% | Predominantly outside major urban areas | Medium term (2-4 years) |

| Supply bottlenecks for refrigeration equipment | -0.4% | National, most severe at new build projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CAPEX and energy costs of facilities

Cold storage consumes 1.54 kWh per cubic foot annually and electricity accounts for 70% of a warehouse’s total energy bill. Reaching best-practice intensity of 10 kWh/m³/yr in a 100,000 m³ site requires automation and heat-recovery systems, inflating upfront budgets. Grid volatility during the renewable transition exposes operators to price spikes, yet liquid-air energy storage due online near Manchester in 2026 promises long-duration backup, reducing exposure to curtailments.

HGV and reefer-driver labor shortage

A deficit of 50,000 qualified drivers elevates transport wages and jeopardizes on-time deliveries. Median hourly pay climbed to GBP 15.00 (USD 19.5) in 2025 but demographics remain skewed; half the workforce is over 50 years old and female representation is 2%. Government grants of GBP 100 million (USD 130 million) fund roadside amenities and training, yet annual demand for 40,000 new licenses through 2029 keeps pressure on recruitment pipelines[2]“The Border Target Operating Model,” UK Government, gov.uk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Storage Dominates, Services Accelerate

Refrigerated storage generated 51.35% of the United Kingdom cold chain logistics market size in 2025, underpinning import-heavy food and pharmaceutical flows. Investments such as a GBP 2 million (USD 2.6 million) chilled consolidation center add capacity close to retail distribution hubs. Over 2026-2031, value-added services grow at 4.37% CAGR as shippers seek integrated customs clearance, repacking, and temperature validation in a single contract. Sensor networks and digital twins cut stock-holding days, lifting return on invested capital for service providers.

A wave of mergers, including a USD 719 million takeover of Wincanton, enables scale purchasing of renewable electricity and advanced warehouse automation. The resulting footprint allows firms to flex space between frozen and chilled slots, an advantage as the United Kingdom cold chain logistics market absorbs shifting consumer demand.

By Temperature Type: Frozen Leads, Chilled Accelerates

Frozen logistics maintained 41.55% share of the United Kingdom cold chain logistics market in 2025, supported by stable protein imports and national frozen-food brands. Innovations such as variable-speed compressors and high-efficiency insulation reduce per-pallet energy draw, sustaining margins.

Chilled services register the quickest expansion at 4.08% CAGR, buoyed by fresh meal solutions and biologic medicines. Radiopharmaceutical exports that require deep-frozen holding spur niche demand for -70 °C capacity compliant with Good Distribution Practice. Recyclable fiber-based boxes that safeguard 2-8 °C payloads for 36 hours enhance sustainability credentials while minimizing landfill.

By Application: Meat Dominates, Pharma Surges

Meat and poultry retained 23.65% of United Kingdom cold chain logistics market share in 2025 due to steady domestic consumption and EU sourcing rules. Customs documentation now involves advance veterinary certification, making real-time data platforms critical for just-in-time delivery.

Pharmaceuticals and biologics lead growth at 5.26% CAGR. A government-backed GMP cluster across Cambridge and Oxford elevates export volumes of cell-and-gene therapies that must remain at cryogenic temperatures. Airlines and freight forwarders partner on lane-specific monitoring tools that alert shippers when deviations exceed 0.5 °C, protecting high-value cargo.

Geography Analysis

The South East corridor, anchored by Dover, Felixstowe, and London Gateway, processed almost half of inbound temperature-sensitive EU goods in 2025 and is projected to log a 4.05% CAGR through 2031. New border control posts equipped with on-site refrigeration limit dwell-time increases to under 8 hours even as paperwork expands.

The Midlands leverage central positioning and motorway connectivity, allowing next-day coverage of 90% of UK postcodes. Automated campuses in Northampton and Leicester use renewable-powered microgrids to cut grid draw by 30% in peak summer. Scotland advances with seafood exports and whiskey maturation requiring bonded cold rooms; investments in port chilled tunnels at Grangemouth shorten clearance for live shellfish.

Wales and Northern Ireland remain smaller but strategic. The Windsor Framework permits qualifying goods to move from Northern Ireland to Great Britain without extra animal-health declarations, sustaining cold-store throughput. Local EV Infrastructure Fund support of GBP 381 million (USD 495.3 million) prioritizes high-capacity chargers at Cardiff, Swansea, and Belfast to prepare for mandatory zero-emission heavy vehicles by 2035.

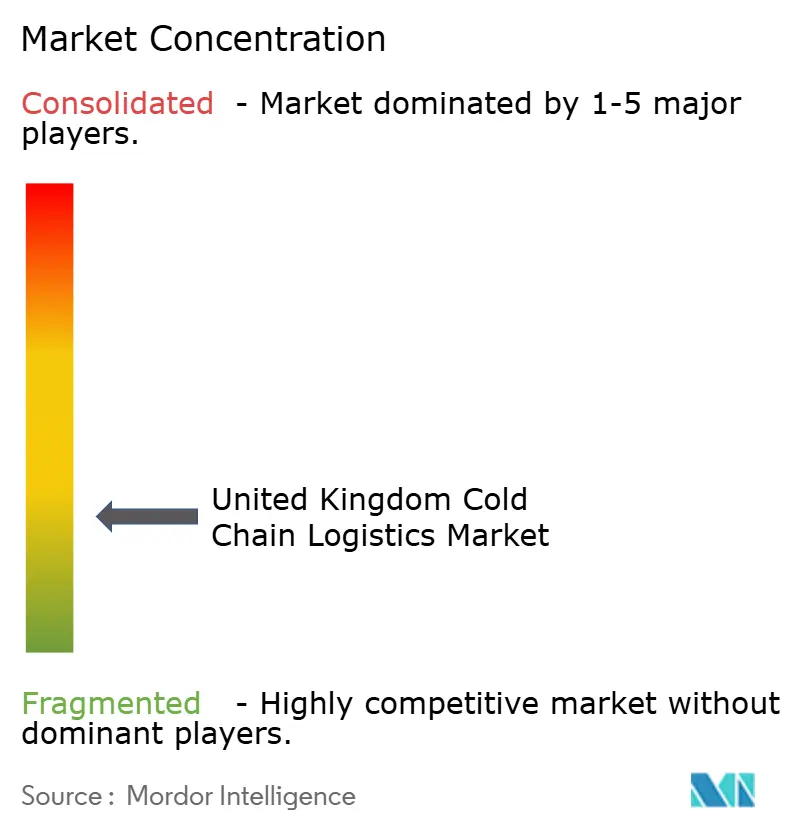

Competitive Landscape

The market remains moderately fragmented, yet recent M&A signals accelerating consolidation. DSV closed a EUR 14.3 billion (USD 15.78 billion) purchase of DB Schenker, adding capacity in pharmaceuticals and life-science handling. CMA CGM’s logistics arm acquired Wincanton for USD 719 million, securing access to 8 million sq ft of chilled warehousing.

Lineage Logistics and Americold expand via automation, employing high-bay cranes and shuttle systems that raise pallet density by 30%. Lineage’s USD 18 billion IPO valuation evidences investor appetite for scalable cold storage networks. Smaller operators differentiate with renewable-energy retrofits, winning contracts from retailers that pledge carbon-neutral deliveries by 2030.

Technology adoption is a primary battleground. Operators deploy IoT nodes every 10 meters inside trailers to report temperature and door status in real time. Blockchain pilots with meat processors confirm provenance within 2 seconds, reducing fraud risk. Companies occupying the top five revenue positions jointly held 46% share in 2024, indicating moderate concentration in the United Kingdom cold chain logistics market.

United Kingdom Cold Chain Logistics Industry Leaders

Lineage Logistics

Culina Group

Reed Boardall

NewCold

Gist Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSV finalized its EUR 14.3 billion (USD 15.7 billion) takeover of DB Schenker, creating one of the world’s largest logistics groups. The deal deepens cold-chain capabilities, targets DKK 9 billion in annual synergies by 2028, and boosts the company’s service breadth in the United Kingdom.

- September 2024: MSC’s inland-logistics arm, Medlog, acquired Maritime Transport, the country’s biggest haulier with more than 2,500 vehicles. The transaction links port handling and inland distribution, improving temperature-controlled cargo flows through key U.K. gateways.

- June 2024: DP World committed GBP 34 million (USD 44.2 million) to a 598,000 sq ft warehouse in Coventry, enlarging its U.K. logistics footprint and adding chilled capacity for automotive and consumer-goods clients amid shifting post-Brexit trade patterns.

- March 2024: DFDS ordered 100 Volvo heavy-duty electric trucks, taking its battery-electric fleet to 225 vehicles. The carrier aims for 25% fleet electrification by 2030 to support lower-carbon refrigerated transport across Europe.

United Kingdom Cold Chain Logistics Market Report Scope

The technique and procedure, known as "cold chain logistics," enable the secure transportation of temperature-sensitive commodities and products throughout the supply chain. It mainly relies on science to assess and account for the relationship between temperature and perishability.

The report provides a comprehensive background analysis of the United Kingdom Cold Chain Logistics Market, covering the current market trends, restraints, technological updates, and detailed information on various segments and the competitive landscape of the industry. Additionally, the COVID-19 impact has been incorporated and considered during the study. The United Kingdom cold chain logistics market is segmented by service (storage, transportation, and value-added services), temperature type (chilled, frozen and ambient), and application (horticulture, dairy products, meats, fish, poultry, processed food products, pharmaceuticals, life sciences, chemicals, and other applications). The report offers market size and forecasts for the United Kingdom cold chain logistics market in value (USD) for all the above segments.

By Service Type

| Refrigerated Storage | Public Warehousing |

| Private Warehousing | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

By Temperature Type

| Chilled (0-5°C) |

| Frozen (-18-0°C) |

| Ambient |

| Deep-Frozen/Ultra-Low (less than -20°C) |

By Application

| Fruits and Vegetables |

| Meat and Poultry |

| Fish and Seafood |

| Dairy and Frozen Desserts |

| Bakery and Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals and Biologics |

| Vaccines and Clinical Trial Materials |

| Chemicals and Specialty Materials |

| Other Perishables |

| By Service Type | Refrigerated Storage | Public Warehousing |

| Private Warehousing | ||

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0-5°C) | |

| Frozen (-18-0°C) | ||

| Ambient | ||

| Deep-Frozen/Ultra-Low (less than -20°C) | ||

| By Application | Fruits and Vegetables | |

| Meat and Poultry | ||

| Fish and Seafood | ||

| Dairy and Frozen Desserts | ||

| Bakery and Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals and Biologics | ||

| Vaccines and Clinical Trial Materials | ||

| Chemicals and Specialty Materials | ||

| Other Perishables | ||

Key Questions Answered in the Report

What value will United Kingdom cold chain logistics reach by 2031?

The sector is forecast to hit USD 11.87 billion in 2031, up from USD 9.75 billion in 2026 at a 4.02% CAGR.

Which service type is expanding the fastest in temperature-controlled logistics?

Value-added services such as specialized packaging, relabeling, and customs support are growing at a 4.37% CAGR through 2031, outpacing storage and transportation.

Why are chilled operations gaining momentum versus frozen capacity?

Rising e-grocery volumes and growth in biologics that must stay between 2 °C and 8 °C are pushing chilled services to a 4.08% CAGR, the highest among temperature bands.

How severe is the driver shortage for refrigerated haulage?

The United Kingdom needs 40,000 new HGV drivers annually through 2029, while a current shortfall of about 50,000 licensed operators is inflating wages and straining delivery schedules.

What sustainability actions are companies taking to curb energy bills?

Operators are raising freezer settings from –18 °C to –15 °C, installing solar roofs, and trialing electric trucks; these steps can cut warehouse electricity use by 10-11% and slash fleet emissions.

How do post-Brexit food-safety rules influence cold-chain demand?

Mandatory health certificates, pre-notifications, and new border inspection posts require traceable, temperature-secure transit, prompting shippers to rely more heavily on compliant cold-chain specialists.

Page last updated on: