Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

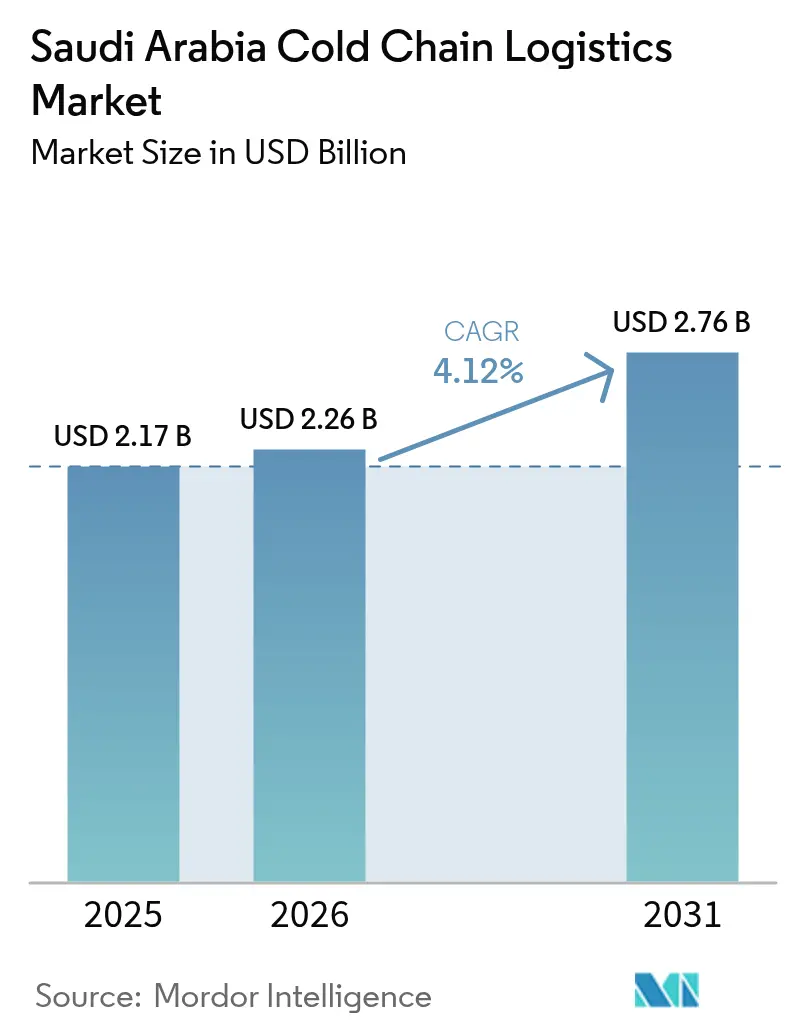

| Base Year Market Size (2025) | USD 2.17 Billion |

| Market Size (2026) | USD 2.26 Billion |

| Market Size (2031) | USD 2.76 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

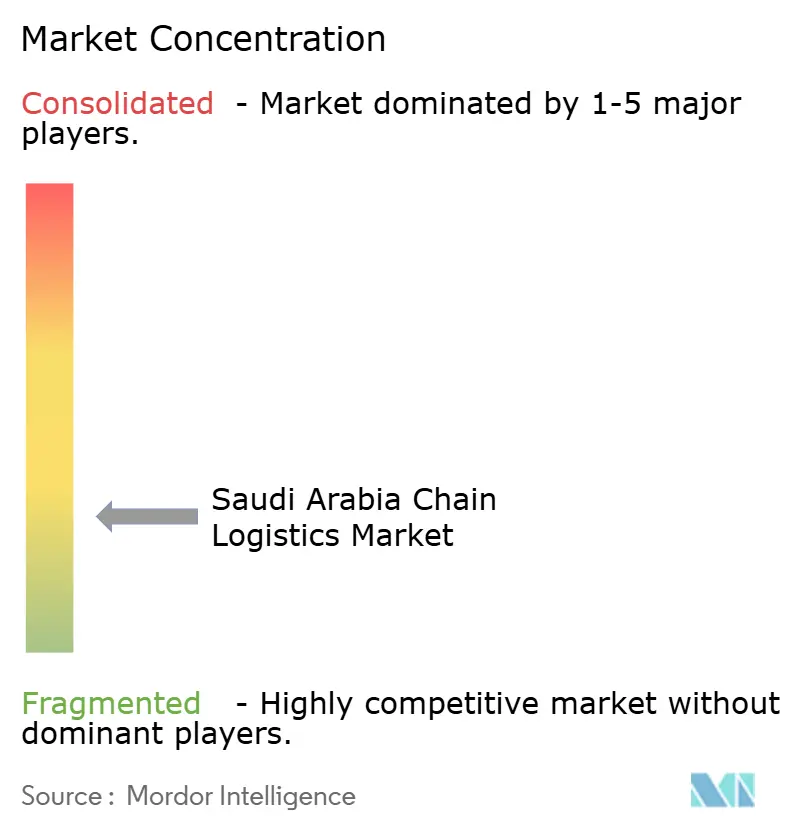

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Cold Chain Logistics Market Analysis by Mordor Intelligence

Saudi Arabia Cold Chain Logistics Market size in 2026 is estimated at USD 2.26 billion, growing from 2025 value of USD 2.17 billion with 2031 projections showing USD 2.76 billion, growing at 4.12% CAGR over 2026-2031.

The growth trajectory mirrors Vision 2030’s goal of economic diversification, which frames cold chain infrastructure as a cornerstone for safeguarding food security, modernizing healthcare distribution, and deepening regional trade integration. Government targets, such as achieving 80% poultry self-sufficiency by 2025, compel investment in temperature-controlled networks that can handle 950,000 MT (metric tons) of chicken production and simultaneously support imported protein flows[1]U.S. Department of Agriculture, “Poultry and Products Annual,” apps.fas.usda.gov. Regulatory tightening by the Saudi Food and Drug Authority (SFDA) stimulates specialized storage for biologics and vaccines, while AI/ML-enabled energy-optimization pilots cut refrigeration energy use by 20%, showing direct operating-cost advantages. Logistics corridors anchored on the 5,500 km rail network harness multimodal efficiencies, lowering long-haul costs by 15% versus road-only freight and improving service reliability for temperature-sensitive cargo.

Key Report Takeaways

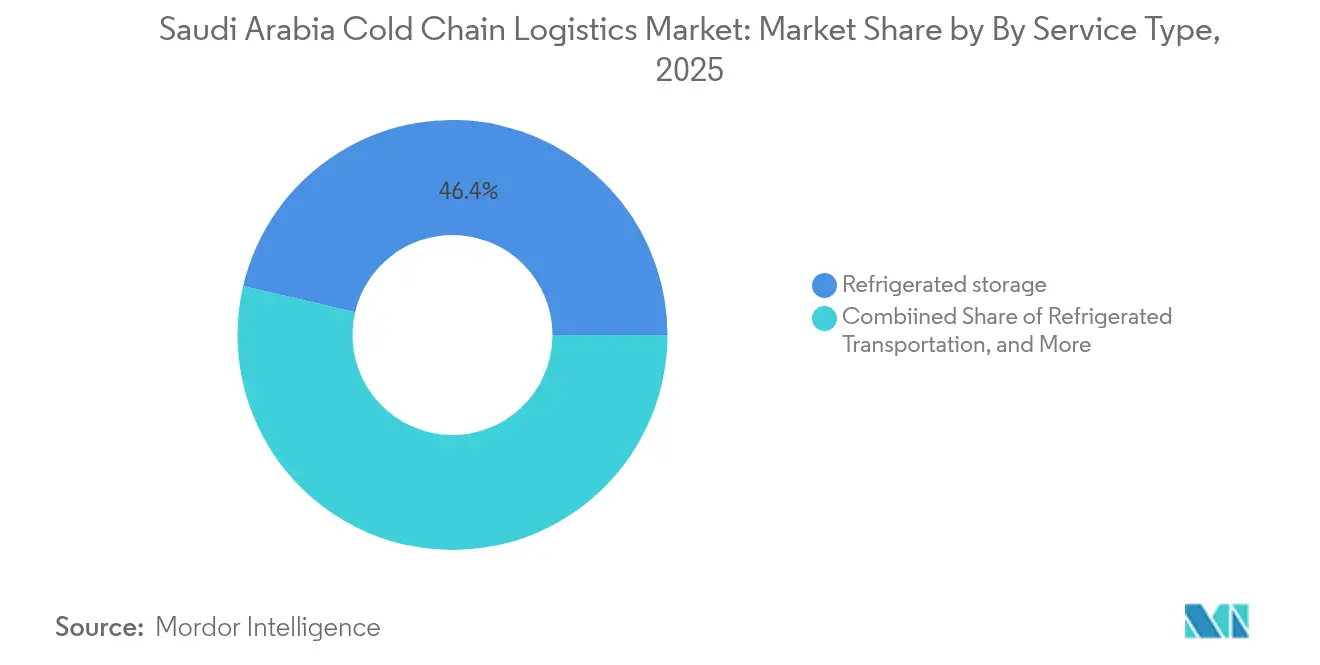

- By service type, refrigerated storage led with 46.35% of the Saudi Arabia cold chain logistics market share in 2025; value-added services are poised to grow at a 4.42% CAGR through 2031.

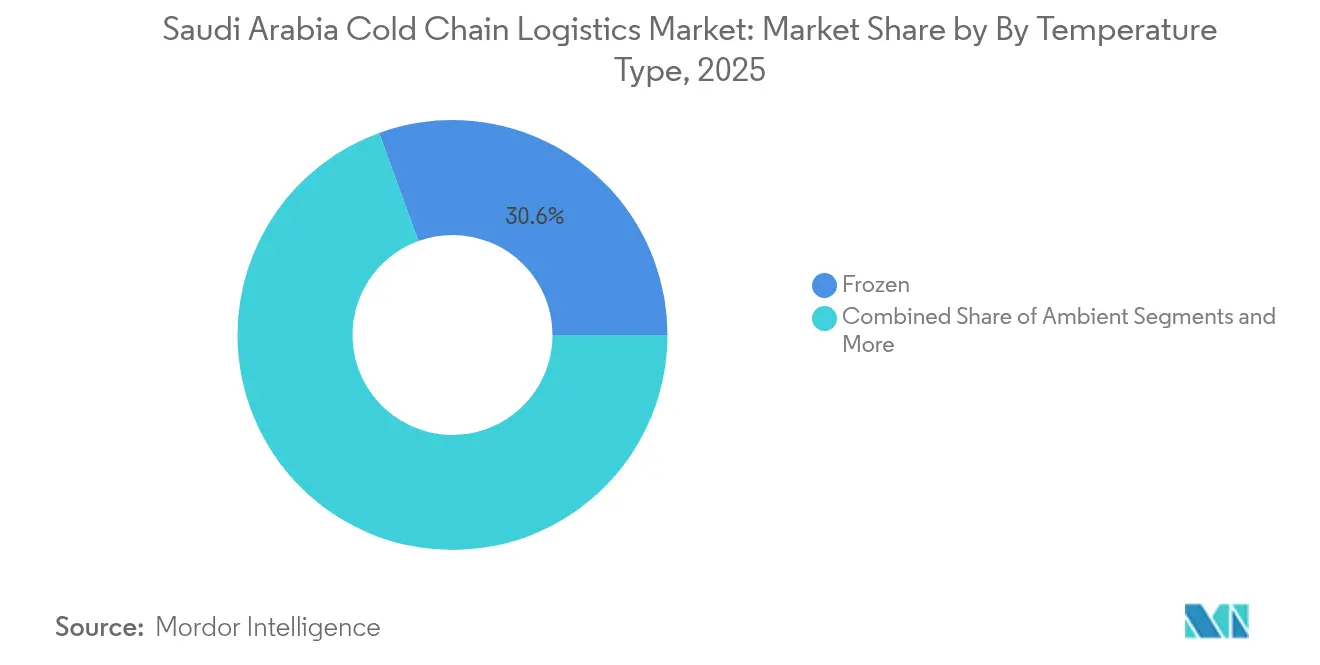

- By temperature range, frozen applications captured 30.55% share of the Saudi Arabia cold chain logistics market size in 2025, while deep-frozen/ultra-low operations are forecast to advance at a 4.68% CAGR to 2031.

- By application, meat & poultry held 23.60% of the Saudi Arabia cold chain logistics market share in 2025; pharmaceuticals & biologics will expand at a 5.22% CAGR through 2031.

- By region, Makkah accounted for a 28.65% share of the Saudi Arabia cold chain logistics market size in 2025, whereas Riyadh is projected to post the fastest 4.15% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pharma cold-chain requirements | +1.2% | Riyadh & Makkah | Medium term (2-4 years) |

| Online grocery & food delivery expansion | +0.8% | Riyadh, Jeddah, Dammam | Short term (≤ 2 years) |

| Vision 2030 logistics investments | +1.0% | National | Long term (≥ 4 years) |

| Stricter SFDA traceability rules | +0.6% | National | Medium term (2-4 years) |

| Poultry self-sufficiency push | +0.4% | Eastern production clusters | Medium term (2-4 years) |

| AI/ML-based energy optimization | +0.3% | Industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Logistics Infrastructure Investments Drive Capacity Expansion

The government has earmarked USD 133 billion for new roads, ports, airports, and 59 logistics centers spanning 100 million m² to be delivered by 2030[2]American Journal of Transportation, “Vision 2030 Logistics Investments,” ajot.com. Twenty-one of these centers are already in execution, and their integration with the Fasah customs portal will compress import dwell times that have historically jeopardized cargo integrity. Coupling these hubs with the national rail grid lowers inland transport costs and widens cold storage access for food importers and pharmaceutical distributors. As each hub comes online, small and mid-sized shippers gain entry to GDP-certified facilities without investing in proprietary assets, a dynamic expected to accelerate competitive intensity.

Pharmaceutical Cold Chain Requirements Accelerate Specialized Infrastructure Development

SFDA’s Breakthrough Medicine Program compels logistics firms to meet GDP standards, spurring EUR 500 million (USD 581.56 million) of regional spending under DHL’s global health-logistics initiative. NAQEL Express mirrors this focus with an SAR 200 million (USD 53.25 million) warehouse in Jeddah featuring multi-temperature zones dedicated to biologics and vaccines. These investments underpin the segment’s 5.40% CAGR, outstripping overall market growth, while also raising the entry bar for non-certified competitors. Future demand will intensify as Saudi Arabia positions itself as a regional clinical-trials center requiring ultra-low storage down to –80 °C.

Government Push for Poultry Self-Sufficiency Creates Domestic Cold Chain Demand

To reach 80% self-sufficiency, producers must handle 950,000 MT (metric tons) of chicken via temperature-controlled links from slaughterhouses to retailers, a logistical requirement accentuated by the Kingdom’s desert climate. Subsidized loans tethered to cold-chain compliance promote adherence to food-safety standards even among small growers. The coexistence of domestic and imported poultry elevates inventory complexity, driving uptake of warehouse-management systems capable of segregating different origin lots and expiry dates.

AI/ML-Driven Optimization Systems Enable Energy Efficiency Breakthroughs

Pilot sites deploying IoT sensors and machine-learning algorithms report 20% cuts in cooling energy and 31% reductions in cost without compromising temperature set-points. As energy charges constitute up to 35% of cold-storage OPEX, these savings directly widen margins. Wider adoption is aided by the Saudi Energy Efficiency Center’s SEER framework, which guides HVAC upgrades toward high-efficiency units. Integrating predictive analytics for demand forecasting further optimizes load profiles, reducing both waste and carbon intensity.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & energy intensity | –0.9% | National; acute in secondary cities | Long term (≥ 4 years) |

| Skilled-labor shortage | –0.7% | Eastern & Al-Medinah | Medium term (2-4 years) |

| Grid reliability issues | –0.5% | Secondary cities | Short term (≤ 2 years) |

| Refrigerant import licensing | –0.3% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Energy Intensity Constrain Market Entry for Smaller Players

Grade-A cold-storage projects can exceed USD 50 million, deterring smaller entrants without a deep balance sheet. Energy accounts for 25–35% of OPEX, and HVAC alone consumes 65% of facility electricity in peak summer months. Upgrading to SEER-compliant chillers raises up-front costs but reduces life-cycle expenses, creating a capital-versus-operating cost trade-off that many mid-tier operators find difficult to balance.

Skilled Workforce Shortage Threatens Operational Efficiency and Safety Standards

Saudization quotas amplify an already tight supply of refrigeration technicians and GDP-compliant drivers. TVET programs have not kept pace with digitalization, leaving skill gaps in data analytics, IoT troubleshooting, and hazardous-material protocols. Shortfalls elevate safety risks, particularly when handling biologics that can lose efficacy after minor temperature excursions. Larger players respond by launching in-house academies, but smaller firms struggle to fund similar initiatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Storage Infrastructure Dominance Meets Value-Added Growth

Refrigerated storage controlled 46.35% of the Saudi Arabian cold chain logistics market share in 2025 by virtue of the country’s heavy reliance on warehousing for both imported and domestically produced temperature-sensitive goods. Public warehouses capture smaller shippers seeking economies of scale, whereas private facilities like Almarai’s integrated network ensure quality control across vertically linked dairy and poultry lines. Road transport remains essential for last-mile delivery, yet rail is gaining favor as the rail grid extends its reach to inland consumption centers.

Value-added services, while holding a modest share today, are expanding at a 4.42% CAGR and encompass kitting, relabeling, and quality testing tailored to SFDA rules. Multi-temperature vehicles able to segregate SKUs within single trips lower transport costs and curb product spoilage. Intermodal solutions that stitch together sea-rail-road legs now differentiate full-service providers from asset-light competitors. Growing demand for e-commerce fulfillment accelerates take-up of cross-docking and pick-and-pack services that shorten delivery lead times to same-day or next-day standards in major cities.

By Temperature Type: Frozen Dominance Challenged by Ultra-Low Growth

Frozen operations held 30.55% of the Saudi Arabian cold chain logistics market size in 2025, reflecting strong imports of protein and expanding domestic poultry output. Latest UNEP guidelines favor low-GWP refrigerants, nudging operators toward CO₂ and propane systems that also improve energy efficiency. Chilled storage benefits from national food-waste reduction campaigns, creating new demand for produce and dairy chains.

Deep-frozen/ultra-low operations stand out with a 4.68% CAGR as pharmaceutical and biotech sectors install –20 °C to –80 °C rooms to accommodate vaccines and clinical-trial samples. Ambient storage remains relevant for temperature-stable drugs and acts as overflow for mixed-load facilities. Growing use of R-452A in transport refrigeration aligns fleets with Kigali Amendment timelines, future-proofing assets against regulatory risks associated with high-GWP blends.

By Application: Pharmaceuticals, Surge Challenges Meat & Poultry Leadership

Meat & poultry constituted 23.60% of the Saudi Arabia cold chain logistics market share in 2025, anchored by Vision 2030 support for domestic growers and ongoing imports from Brazil. Stringent food-safety norms increase demand for controlled-atmosphere chilling that lengthens shelf life in hot climates.

Pharmaceuticals & biologics, expanding at a 5.22% CAGR, capitalize on Riyadh’s role as a distribution hub and the proliferation of GDP-certified warehouses . Fruits & vegetables gain from public-private partnerships aimed at halving food waste, while dairy producers leverage brand premiumization to command refrigerated shelf space. Ready-to-eat meal logistics benefit from rising urban lifestyles requiring convenience foods, accelerating the adoption of small-format multi-temperature vehicles.

Geography Analysis

Makkah retained 28.65% of the Saudi Arabia cold chain logistics market size in 2025, thanks to Jeddah Port’s role as the Kingdom’s primary maritime gateway and the dense consumption profile of the western corridor. Planned multimodal hubs linking port, airport, and rail facilities reduce hand-off times for transshipped goods, ensuring the integrity of chilled and frozen cargo despite desert temperatures.

Riyadh posts the fastest 4.15% CAGR through 2031, propelled by King Salman International Airport’s cargo complex and SAL’s USD 215 million air-freight expansio. Pharmaceutical shippers gravitate to the capital because SFDA, customs, and major healthcare buyers are co-located, simplifying regulatory and tender processes. AI/ML pilots in Riyadh warehouses demonstrate 20% energy savings, positioning the region as a technology proving ground for the wider network.

The Eastern Region leverages Dammam Port and industrial cities to serve petrochemical and halal-certified food exports throughout the Gulf, while the Jubail-Dammam rail link boosts container throughput to 1.1 million annually, lowering inland freight costs. Al-Medinah and secondary markets trail in infrastructure, but targeted projects under the National Transport and Logistics Strategy aim to correct grid reliability and road-network gaps, unlocking latent demand for multi-temperature storage and last-mile services. United Warehousing’s BRC-certified site exemplifies rising standards even in emerging sub-markets.

Competitive Landscape

Competition is fragmented, with no single company exceeding a double-digit share, creating space for regional specialists and global integrators alike. Almajdouie and CEVA’s joint venture blends local fleet depth with international network reach, pooling more than 2,000 assets to serve end-to-end contracts that include GDP compliance and value-added packaging.

DHL leverages its EUR 2 billion (USD 2.32 billion) global health-logistics fund to scale ultra-low temperature hubs near Jeddah and Riyadh, while its ASMO venture with Aramco introduces blockchain-enabled procurement solutions for temperature-sensitive chemicals in the energy sector. Local contenders such as NAQEL Express raise the bar by integrating IoT sensors and AI-driven maintenance, allowing real-time intervention before temperature breaches occur.

Technology becomes the primary differentiator as providers deploy predictive analytics for demand planning, route optimization to minimize empty miles, and remote monitoring to satisfy SFDA’s documentation audits. Sustainability credentials increasingly influence bidding outcomes, with players touting lower carbon footprints through electric last-mile fleets and refrigerant upgrades to low-GWP gases.

Saudi Arabia Cold Chain Logistics Industry Leaders

Coldstores Group of Saudi Arabia

NAQEL Express

Mosanada Logistics Services

Agility Logistics

Tamer Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: DHL Group announced USD 570 million in Middle East logistics investments by 2030, prioritizing Saudi hub expansion.

- April 2025: DHL Group earmarked EUR 2 billion (USD 2.32 billion) globally for health-logistics infrastructure through 2030, including new GDP-certified pharma hubs that expand Saudi Arabia’s ultra-low-temperature warehousing network.

- January 2025: United Warehousing & Distribution Services upgraded its Makkah facility to full BRC certification and integrated an advanced warehouse-management system, adding ambient, chilled, and frozen capacity to better serve regional food and pharma clients.

- 2025: GFH and GWC revealed plans for 200,000 m² of Grade-A cold-chain facilities across Riyadh, Jeddah, and Dammam.

Saudi Arabia Cold Chain Logistics Market Report Scope

Cold chain logistics comprises establishments primarily engaged in operating refrigerated warehousing, storage facilities, and transportation of goods in temperature-controlled vehicles. The services provided by these establishments include blast freezing, tempering, and modified atmosphere storage services. A complete background analysis of the Saudi Arabia Cold Chain Logistics Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact, is covered in the report.

The Saudi Arabian cold chain logistics market is segmented by Service (Storage, Transportation, and Value-added Services), by Temperature (Chilled and Frozen), and by End User (Horticulture, Dairy Products, Meats, Fish, and Poultry, Processed Food Products, Pharma and Life Sciences, and Other End Users). The report offers the market sizes and forecasts for the Saudi Arabian cold chain logistics market in value (USD Million) for all the above segments.

By Service Type

| Refrigerated Storage | Public Warehousing |

| Private Warehousing | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

By Temperature Type

| Chilled (0–5 °C) |

| Frozen (-18–0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

By Application

| Fruits & Vegetables |

| Meat & Poultry |

| Fish & Seafood |

| Dairy & Frozen Desserts |

| Bakery & Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals & Biologics |

| Vaccines & Clinical Trial Materials |

| Chemicals & Specialty Materials |

| Other Applications |

By Region (Saudi Arabia)

| Makkah Region |

| Riyadh Region |

| Eastern Region |

| Al-Medinah Region |

| Others |

| By Service Type | Refrigerated Storage | Public Warehousing |

| Private Warehousing | ||

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0–5 °C) | |

| Frozen (-18–0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Application | Fruits & Vegetables | |

| Meat & Poultry | ||

| Fish & Seafood | ||

| Dairy & Frozen Desserts | ||

| Bakery & Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals & Biologics | ||

| Vaccines & Clinical Trial Materials | ||

| Chemicals & Specialty Materials | ||

| Other Applications | ||

| By Region (Saudi Arabia) | Makkah Region | |

| Riyadh Region | ||

| Eastern Region | ||

| Al-Medinah Region | ||

| Others | ||

Key Questions Answered in the Report

How big is the Saudi Arabia Chain Logistics Market?

The Saudi Arabia Chain Logistics Market size is expected to reach USD 2.26 billion in 2026 and grow at a CAGR of 4.12% to reach USD 2.76 billion by 2031.

What is the current Saudi Arabia Chain Logistics Market size?

In 2026, the Saudi Arabia Chain Logistics Market size is expected to reach USD 2.26 billion.

Who are the key players in Saudi Arabia Chain Logistics Market?

Coldstores Group of Saudi Arabia, NAQEL Express, Mosanada Logistics Services, Agility Logistics and Tamer Logistics are the major companies operating in the Saudi Arabia Chain Logistics Market.

What years does this Saudi Arabia Chain Logistics Market cover, and what was the market size in 2025?

In 2025, the Saudi Arabia Chain Logistics Market size was estimated at USD 2.26 billion. The report covers the Saudi Arabia Chain Logistics Market historical market size for years: 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Saudi Arabia Chain Logistics Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: