South America Feed Flavors and Sweeteners Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

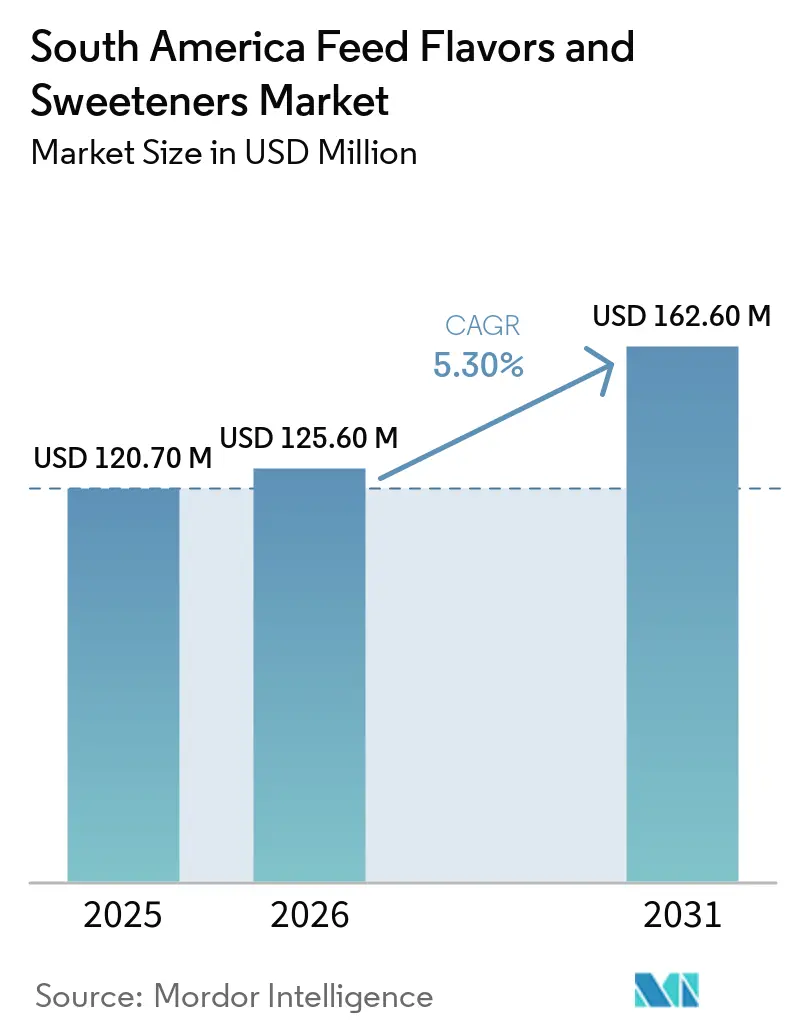

| Base Year Market Size (2025) | USD 120.70 Million |

| Market Size (2026) | USD 125.60 Million |

| Market Size (2031) | USD 162.60 Million |

| Growth Rate (2026 - 2031) | 5.30% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Feed Flavors and Sweeteners Market Analysis by Mordor Intelligence

The South America feed flavors and sweeteners market size was valued at USD 120.70 million in 2025 and estimated to grow from USD 125.60 million in 2026 to reach USD 162.60 million by 2031, at a CAGR of 5.30% during the forecast period (2026-2031). The ruminant and swine segments, bolstered by South America's robust livestock industry, primarily drive the market. As a one of the leader in beef and pork production, Brazil plays a pivotal role, producing over 54,500 thousand head of beef in 2024, as per the United States Department of Agriculture[1]Source: United States Department of Agriculture, “Exact Report Title,” usda.gov. This production surge, up from 53,750 thousand head, underscores the rising demand for high-performance feed additives. These additives, especially feed flavors and sweeteners, are being increasingly integrated into ruminant and swine diets. Their primary roles include enhancing feed palatability, boosting intake, and improving growth performance during crucial phases like weaning and dietary transitions. Major players in the region, such as ADM, Kerry Group plc, and Kemin Industries, are not only expanding their feed additive portfolios but also innovating in product development and tailoring flavor and sweetener solutions, further propelling market growth.

Key Report Takeaways

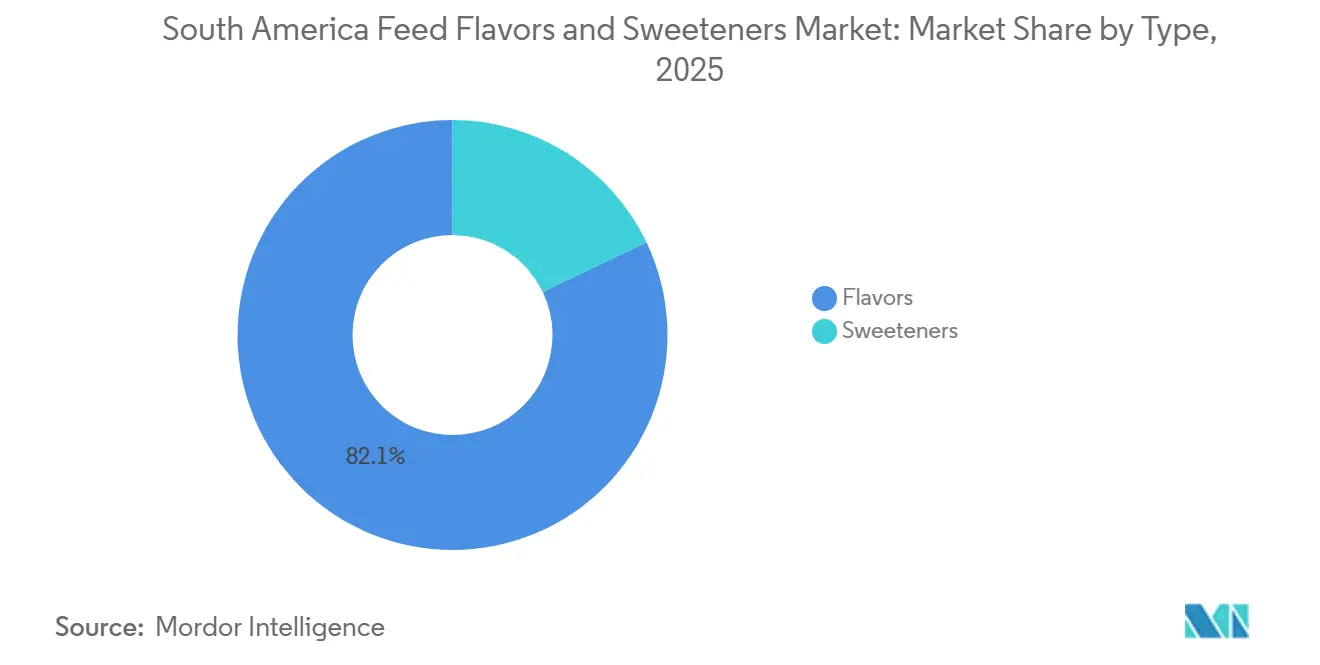

- By type, flavors accounted for the largest segment, represented 82.1% of the South America feed flavors and sweeteners market share in 2025. Sweeteners, however, are projected to be the fastest-growing segment, registering a CAGR of 4.3% from 2026 to 2031.

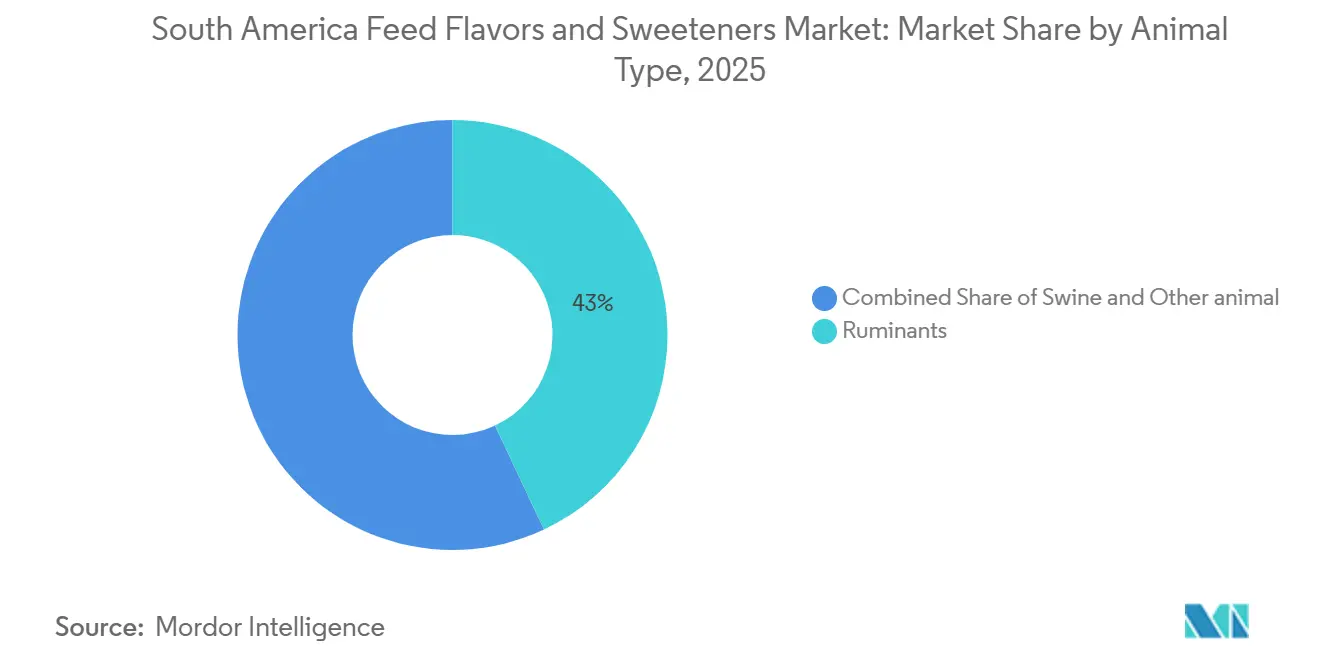

- By animal type, ruminants accounted for the largest share, at 43.0% of the South American feed flavors and sweeteners market size in 2025. While swine is projected to be the fastest-growing segment, registering a CAGR of 7.4% from 2026 to 2031.

- By geography, Brazil dominated the South American feed flavors and sweeteners market, accounted for 46.0% in 2025. Chile is projected to be the fastest-growing country market, registering a CAGR of 5.4% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Feed Flavors and Sweeteners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-led pork production growth | +0.8% | South America, with the highest concentration in Brazil and Argentina | Medium term (2-4 years) |

| Commercial feed volume expansion across Brazil and the broader region | +0.9% | South America core, particularly Brazil and Argentina | Short term (≤ 2 years) |

| Higher use of sweeteners in piglet and young-animal diets | +0.7% | Brazil, Argentina, and the rest of South America | Short term (≤ 2 years) |

| Increasing focus on feed efficiency and animal nutrition outcomes | +0.6% | Brazil primarily, with spillover into Argentina and Chile | Medium term (2-4 years) |

| Reformulation toward alternative protein sources increases demand for palatability solutions | +0.5% | South America core, with early gains in Brazil and Chile | Long term (≥ 4 years) |

| Antimicrobial phaseout raises demand for intake-preserving sensory reformulation | +0.5% | Brazil first, with secondary relevance in Argentina and Chile | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Export-Led Pork Production Growth

Brazil’s role as one of the world’s largest meat exporter and a leading pork exporter creates a strong volume base for the South America feed flavors and sweeteners market. According to the Brazilian Association of Animal Protein (ABPA), Brazil’s pork exports reached 1.5 million metric tons in 2025, up 11.6% from 2024, and export revenue rose to USD 3.619 billion[2]Source: Associação Brasileira de Proteína Animal, “Exportações de carne suína fecham 2025 com crescimento de 11,6%,” ABPA, abpa-br.org. At that scale, stable feed intake is commercially important, so flavors and sweeteners remain part of the routine formulation toolkit for integrated producers and contract growers. Brazil’s push into demanding export markets also raises attention to approved additives and residue-compliant formulations, which support sensory additive adoption over older intake-support tools.

Commercial Feed Volume Expansion Across Brazil and the Broader Region

South America produced 204.446 million metric tons of compound feed in 2025, up 2.8% year over year, and Brazil alone accounted for 89.904 million metric tons according to Alltech Agri Food Statistics. This wider production base expands the addressable market for South America feed flavors and sweeteners, as most inclusions occur at the feed mill level. Higher throughput at larger mills also improves the economics of precision palatability systems, since fixed application and service costs are spread across more tonnage. Brazil and the Southern Cone carried much of that stability, even as smaller subregional markets saw localized disruption. That makes regional distribution coverage and local technical support important competitive tools in the South America feed flavors and sweeteners market.

Higher Use of Sweeteners in Piglet and Young-Animal Diets

Sweeteners are the fastest-growing segment in the South America feed flavors and sweeteners market because producers are placing greater emphasis on intake support during weaning and early growth stages. Piglet weaning remains the most important use case, as the shift from sow milk to solid feed often reduces intake and increases the risk of performance. According to the Brazil Association of Animal Protein (ABPA), Brazil’s swine production reached 5.42 metric tons in 2025, an increase of 2.2% compared to 2024, providing this application with a large commercial base. The 2026 antimicrobial phaseout is also increasing reformulation work in swine diets, which supports the added use of sweeteners as intake-preserving tools in the South America feed flavors and sweeteners market.

Reformulation Toward Alternative Protein Sources Increases Demand for Palatability Solutions

As feed manufacturers in South America increasingly turn to alternative and locally sourced protein ingredients for livestock diets, they're facing heightened palatability challenges. These alternative proteins can introduce new tastes and aromas, potentially diminishing feed acceptance, especially in swine and ruminant diets. Industry experts, including Adisseo, highlight that diets with these alternative ingredients often necessitate specific flavor and sweetener solutions to ensure steady feed intake and optimal animal performance. This trend is particularly pronounced in Chile, where livestock producers are not only adopting more sustainable and cost-effective feed formulations but are also keen on maximizing productivity. While the immediate effect on feed volumes is modest, the potential value is substantial. Specialized solutions that mask or enhance the palatability of these novel feed ingredients tend to yield higher margins than traditional flavoring products. Consequently, this niche is rapidly becoming one of the most promising growth sectors in South America's feed flavors and sweeteners market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented feed-mill base slows premium additive penetration | -0.6% | South America broadly, with a stronger impact in Brazil’s smaller regional mills and the rest of South America | Long term (≥ 4 years) |

| Ministry of Agriculture, Livestock and Supply (MAPA) registration and compliance complexity for sensory additives | -0.5% | Brazil primarily, with secondary relevance in Argentina | Medium term (2-4 years) |

| Currency volatility raises the cost of imported micro-ingredients | -0.7% | Brazil and Argentina most exposed | Short term (≤ 2 years) |

| Disease outbreaks and export restrictions disrupt additive purchasing patterns | -0.4% | Brazil and Chile most exposed | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Feed-Mill Base Slows Premium Additive Penetration

The South America feed flavors and sweeteners market still operates through a widely dispersed feed manufacturing base outside the largest integrated protein companies. Smaller and mid-sized mills are often more price-sensitive and less able to run structured validation trials for premium sensory systems. That reduces the practical addressable market for high-specification products even when headline feed volume is large. Suppliers also face higher technical service costs per ton when accounts are scattered across many smaller customers. The result is slower premium penetration across parts of the South America feed flavors and sweeteners market, especially outside Brazil’s production clusters.

Ministry of Agriculture, Livestock and Supply (MAPA) Registration and Compliance Complexity for Sensory Additives

Brazil regulates feed additives through the Ministry of Agriculture, Livestock, and Supply (MAPA) framework, and that process can slow new launches in the South American feed flavors and sweeteners market. New or reformulated products must move through documentation, technical review, and product registration steps before commercialization. Imported specialty ingredients can face added time-to-market pressure when registration and import procedures overlap. Large multinationals are usually better equipped to manage those steps than smaller regional suppliers. That creates a measured pace of innovation even when customer demand for reformulation support is rising.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Sweeteners Gain Share as Flavors Anchor the Market

Flavors hold the largest segment, captured 82.1% of the South America feed flavors and sweeteners market share in 2025, confirming their widespread use across swine, and ruminant diets in the region. Their leading position reflects the broad set of problems they address, including masking bitter raw materials, improving first-feed acceptance, and supporting intake in high-performance production systems. Flavors also fit well into both large integrated feed programs and more standardized premix-based formulations, which supports repeat demand in the South America feed flavors and sweeteners market. This breadth makes the flavor category structurally harder to displace, even as adjacent solution types improve.

Sweeteners remain the fastest-growing segment, projected to expand at a 4.3% CAGR through 2026 to 2031. The strongest pull comes from piglet weaning diets, where intake support directly affects early growth and feed conversion. ADM's SUCRAM and Adisseo's Optisweet demonstrate the way suppliers have developed technical solutions tailored to specific use cases, rather than positioning sweeteners solely as general flavor enhancers. This approach provides sweeteners with a more defined growth trajectory within the South America feed flavors and sweeteners market, despite flavors maintaining a higher overall market value.

By Animal Type: Ruminants Lead Across Cattle Sub-Segments While Swine Accelerates

Ruminants held 43% of South America's feed flavors and sweeteners market size in 2025. This dominance stems from the region's vast cattle population and robust beef and dairy sectors, especially in Brazil and Argentina. Ruminants are increasingly being given feed flavors and sweeteners to enhance the taste of their compound feed, mineral supplements, and nutritional additives. This not only ensures a steady intake of feed but also optimizes animal performance. With a heightened emphasis on boosting milk yield, weight gain, feed conversion efficiency, and overall herd productivity, the demand for these additives in the ruminant sector is set to persist.

Swine is projected to be the fastest-growing segment, with a 7.4% CAGR from 2026 to 2031. This surge is fueled by the rising pork production, the growing commercialization of swine farming, and the widespread adoption of precision nutrition practices. In swine nutrition, feed flavors and sweeteners are pivotal, especially for piglets during weaning, when feed intake can dwindle under dietary and environmental stress. By enhancing palatability, these additives not only boost feed intake but also improve growth performance and feed conversion ratios. Responding to this burgeoning demand, industry giants such as ADM, Cargill, dsm-firmenich, and Kemin Industries are broadening their feed additive portfolios.

Geography Analysis

Brazil accounted for 46.0% of South America's feed flavors and sweeteners market in 2025. The country ranks third globally in compound feed production, providing additive suppliers with the region’s most extensive commercial base. Brazil's export-oriented ruminants and pork industries maintain the relevance of intake-support products across large integrated systems. Furthermore, the country's strong agricultural infrastructure and government support for the livestock sector reinforce its role as a significant market for feed additives.

Chile is projected to be the fastest-growing market, with a 5.4% CAGR from 2026 to 2031. This growth trajectory is primarily buoyed by the nation's burgeoning ruminant sector and a heightened emphasis on feed efficiency and livestock productivity. Data from Chile's National Institute of Statistics (INE) reveals that in 2025, the country's bovine cattle inventory was around 750,219 head[3]Source: National Institute of Statistics, “Exact Report Title,” ine.cl. As producers lean towards more intensive feeding practices, there's an increase in the use of feed flavors and sweeteners in ruminant diets. These additives not only enhance feed palatability but also bolster nutrient intake and overall production performance.

Argentina presents significant opportunities in the South American feed flavors and sweeteners market, but certain challenges persist. The prevalence of smaller, price-sensitive regional mills limits the rapid adoption of premium additives, despite Argentina's large swine population. In contrast, Colombia and other Andean countries, though currently smaller contributors, show potential for long-term growth. These markets are progressively aligning their feed standards with regional benchmarks while benefiting from investments in feed production infrastructure and improvements in ruminant management practices.

Competitive Landscape

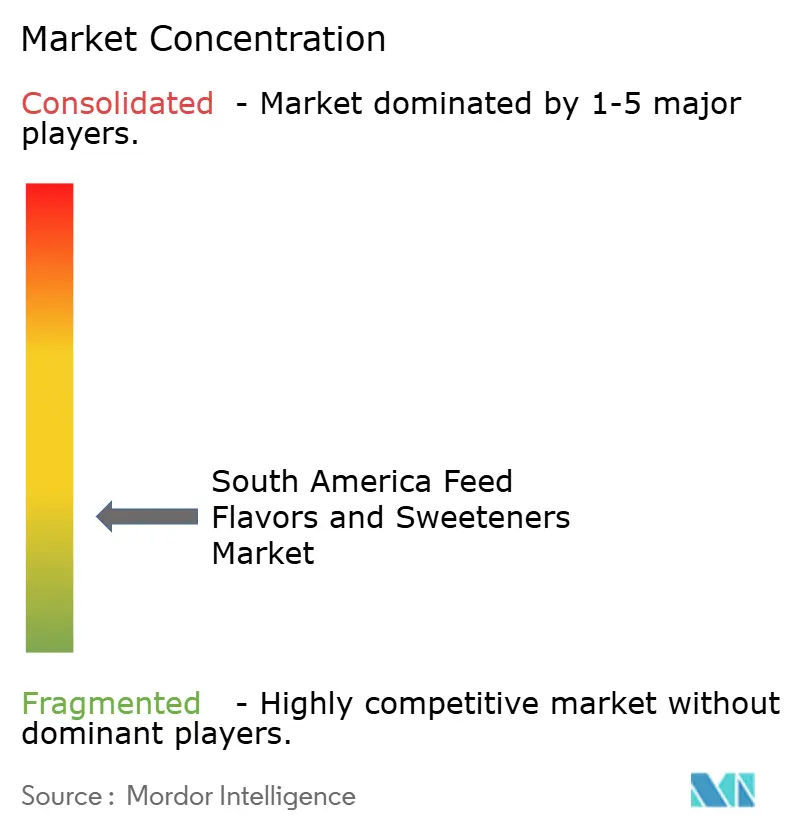

The South America feed flavors and sweeteners market was fragmented by 2025. The top five players in the market include ADM, Kerry Group plc, Symrise AG, Adisseo, and Kemin Industries, Inc. No single supplier holds a significant enough market share to influence pricing across the entire region. This market structure underscores the importance of local manufacturing, formulation support, and regulatory compliance as sustainable competitive advantages, rather than relying solely on portfolio breadth. Additionally, this fragmentation creates opportunities for specialized local companies to gain market share by offering faster service and aligning more closely with customer feed programs.

Recent strategic moves show where the leading players are allocating capital in the South American feed flavors and sweeteners market. In 2023, Symrise invested in local production in Chapecó, Brazil, and the site later achieved FSSC 22000 certification, strengthening both supply responsiveness and compliance credibility. Mid-tier companies are competing differently in the South America feed flavors and sweeteners market, often using formulation flexibility and species-specific positioning rather than scale.

Norel’s product positioning in Brazil and South America, along with species-focused offerings from specialist suppliers, shows that room still exists for targeted technical propositions. Bioaromas do Brasil is particularly well placed in plant-origin palatants for swine and other animals, where imported multinational products can be too expensive for some buyers. The biggest near-term opening is in validated non-antibiotic intake-support systems and specialized palatants for alternative-protein diets, where early movers can build durable customer relationships.

South America Feed Flavors and Sweeteners Industry Leaders

ADM

Kerry Group plc

Symrise AG

Kemin Industries, Inc.

Adisseo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: ADM has inaugurated a new premix and additives plant in Apucarana, Parana, Brazil, with an initial production capacity of 40,000 metric tons per year, which can potentially expand to 80,000 metric tons. The 7,500 m² facility boosts ADM's regional capacity by 40-50% and features advanced automation and traceability systems. This facility expansion strengthens the availability of specialty feed additives in the region, supporting growth in the feed flavors and sweeteners market through increased production capacity and enhanced regional market penetration.

- August 2025: Cargill, Incorporated expanded its Brazilian feed business through the acquisition of Mig-Plus, focusing on multiple species, particularly swine and ruminants. This acquisition strengthened the company's presence in Brazil by incorporating performance enhancers, vitamins, and specialty blends tailored to local production systems. It also improved the availability of advanced feed nutrition solutions in South America, thereby driving demand for feed flavors and sweeteners that enhance feed palatability and animal performance.

- October 2024: DSM-Firmenich has inaugurated a new animal nutrition facility in Brazil. The plant is designed to produce 100,000 metric tons of supplements annually, focusing on enhancing the health and nutrition of beef and dairy cattle. This facility expands the company's regional manufacturing capabilities for animal nutrition and promotes the wider use of value-added feed additive solutions in livestock production systems.

South America Feed Flavors and Sweeteners Market Report Scope

The feed flavors and sweeteners market encompasses the global industry focused on the production, formulation, distribution, and sale of flavoring agents and sweetening additives designed to enhance the palatability, aroma, taste, and overall intake of animal feed. The South America feed flavors and sweeteners market report is segmented by type (flavors and sweeteners), by animal (ruminants, swine, and other animal type), and by geography (Brazil, Chile, Argentina, And Rest of South America). The market forecasts are provided in terms of value (USD) and Volume (Metric Tons).

| Flavors |

| Sweeteners |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animal Type |

| Brazil |

| Argentina |

| Chile |

| Rest of South America |

| By Type | Flavors | |

| Sweeteners | ||

| By Animal Type | Ruminants | Beef Cattle |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animal Type | ||

| By Geography | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the South America feed flavors and sweeteners market in 2026?

The market is estimated to reach USD 125.60 million in 2026.

Which product type leads to demand across the region?

Flavors accounted for 82.1% of the market value in 2025.

Why is ruminant becoming more important for additive suppliers in Chile?

In Chile, as the emphasis on enhancing cattle productivity, feed efficiency, and beef and dairy yields intensifies, ruminants are emerging as a focal point for additive suppliers.

Why does Brazil matter more than any other country in this space?

Brazil leads the region in compound feed production, driven by substantial pork exports, which support a diverse demand base.

Page last updated on: