Middle East Feed Flavors and Sweeteners Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

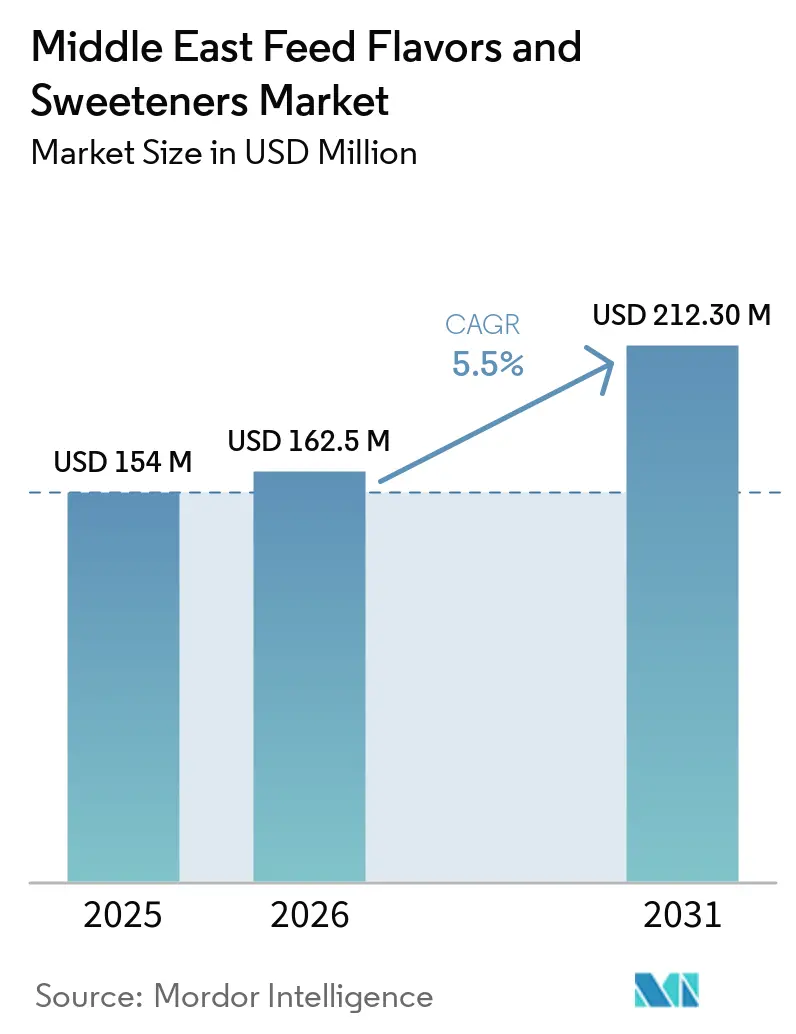

| Base Year Market Size (2025) | USD 154 Million |

| Market Size (2026) | USD 162.5 Million |

| Market Size (2031) | USD 212.30 Million |

| Growth Rate (2026 - 2031) | 5.50% CAGR |

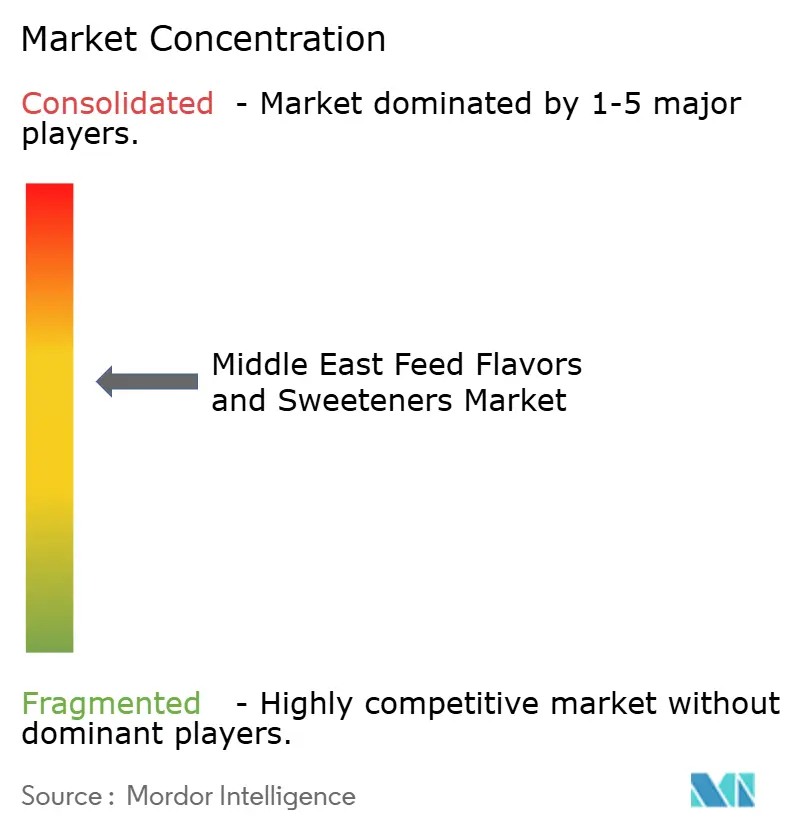

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Feed Flavors and Sweeteners Market Analysis by Mordor Intelligence

The Middle East feed flavors and sweeteners market was USD 154.0 million in 2025 and projected to grow from USD 162.5 million in 2026 to USD 212.3 million by 2031, registering a CAGR of 5.5% during the period from 2026 to 2031. This growth is driven by increased compound feed production in Saudi Arabia and Iran, greater use of sensory additives in commercial dairy and poultry feed, and the adoption of formulations designed to help animals maintain feed intake under heat and health-stress conditions. Regulatory changes are also influencing demand, with antibiotic-free feeding programs and the anticipated removal of saccharin from certain imported feed additive systems encouraging the adoption of reformulated sweetener and flavor solutions. Additionally, the region's ongoing investment in modern feed milling infrastructure presents opportunities, as advanced dosing systems facilitate the standardization of premium palatability additives across larger production volumes. The competitive landscape remains moderately fragmented. This market structure allows for product differentiation, local distribution partnerships, and application-focused strategies. The market is also benefiting from increased efforts to reformulate ruminant diets. Challenges such as silage off-notes, reduced roughage flexibility, and summer heat stress are driving demand for additives that enhance feed intake stability and acceptance.

Key Report Takeaways

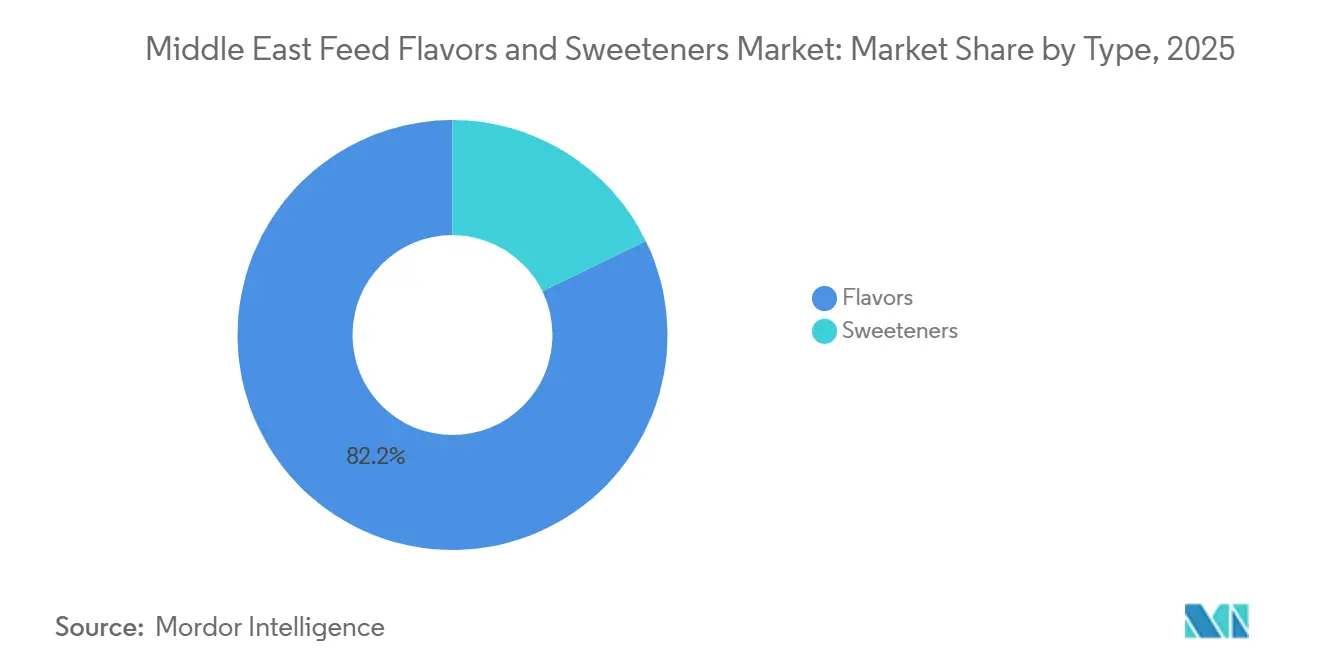

- By sub-additive, flavors accounted for 82.2% of the Middle East feed flavors and sweeteners market share in 2025, while sweeteners are projected to grow at a CAGR of 4.3% through 2031.

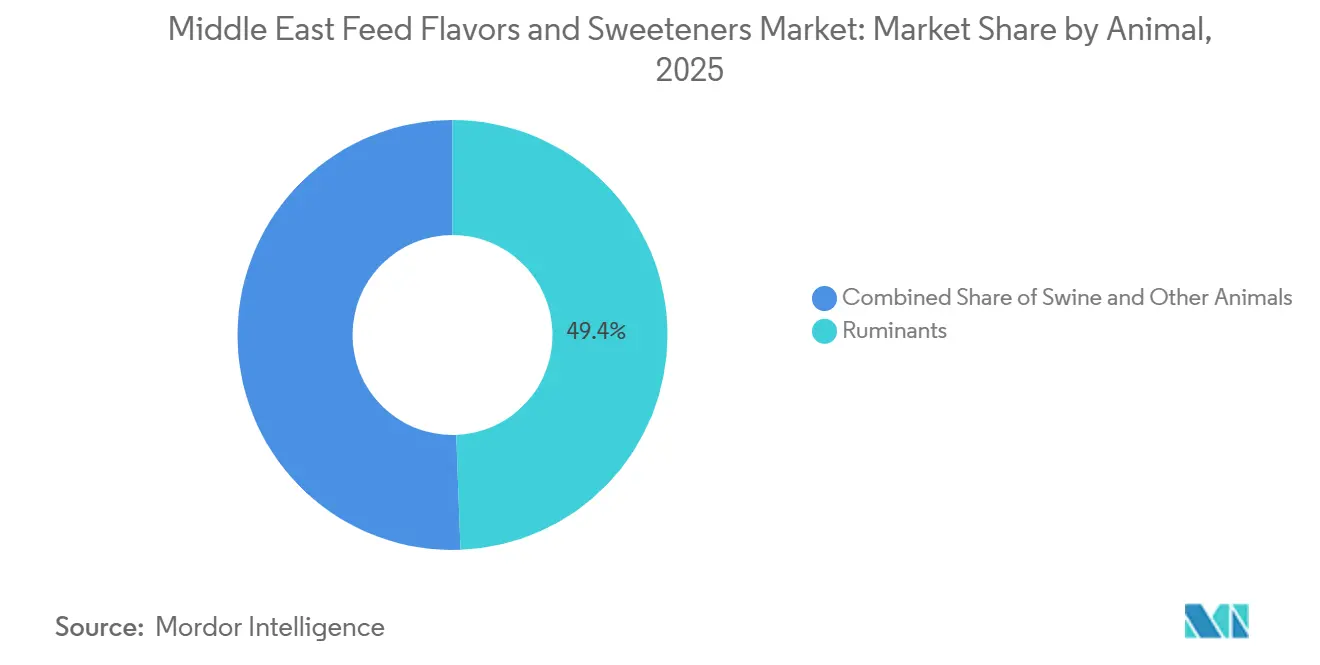

- By animal, ruminants accounted for 49.4% of the Middle East feed flavors and sweeteners market size in 2025 and also recorded the highest projected CAGR of 4.3% through 2031.

- By country, Saudi Arabia is the largest country, with a 45% market share in 2025, while Iran is also the fastest-growing, with a projected CAGR of 5.8% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East Feed Flavors and Sweeteners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Palatability Enhancement in Commercial Feed | +1.2% | Saudi Arabia, United Arab Emirates | Short term (≤ 2 years) |

| Growth in Poultry and Ruminant Feed Production | +1.0% | Saudi Arabia, Iran | Medium term (2-4 years) |

| Shift Toward Antibiotic-Free Feed Programs | +0.8% | Saudi Arabia, United Arab Emirates | Medium term (2-4 years) |

| Expansion of Modern Feed Milling Capacity | +0.7% | Saudi Arabia, Iran, United Arab Emirates | Medium term (2-4 years) |

| Increasing Use of Natural Feed Inputs | +0.5% | United Arab Emirates, Qatar, Bahrain | Long term (≥ 4 years) |

| Heat Stress Management in Livestock Nutrition | +0.6% | Saudi Arabia, United Arab Emirates, Qatar, and Oman | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Palatability Enhancement in Commercial Feed

Commercial feed production in the region is transitioning from basic commodity-style blends to denser, performance-oriented rations, leading to increased use of sensory additives in formulations. Feed mills incorporate flavors and sweeteners to maintain feed intake, as feed refusal negatively impacts conversion efficiency and raises the cost of producing meat and milk. In Saudi Arabia, large poultry and dairy systems already consider palatability as a standard component of feed formulation rather than an optional addition. According to the Alltech Feed survey 2026, global compound feed production reached 1.4 billion metric tons in 2025[2]Alltech, “2026 Alltech Agri-Food Outlook: Global Feed Production Survey,” Feed and Additive Magazine, https://www.feedandadditive.com/alltech-survey-global-feed-production-hit-1-44-billion-tons-in-2025 . The report also highlighted that Middle East feed output faces challenges, including disease pressure and raw material variability, making stable feed intake critical for producers. The value of these additives is further enhanced in modern mills, where continuous mixing and precise dosing improve the consistency of low-inclusion specialty ingredients. Consequently, the Middle East feed flavors and sweeteners market is benefiting from both increased feed demand and improved technical conditions for the use of premium additives. This trend fosters repeat purchasing behavior, as once intake-support systems are integrated into standard feed specifications, mills are less inclined to remove them from commercial formulations.

Growth in Poultry and Ruminant Feed Production

Increasing livestock production in Saudi Arabia and Iran is driving higher demand for compound feed incorporating flavors and sweeteners. On the ruminant side, the planned cessation of perennial forage cultivation in Saudi Arabia by November 2026 is anticipated to increase reliance on commercial feed and total mixed rations, thereby intensifying the need for additives to mask silage and formulation off-notes[1]Source: Okaz, “Halt of Perennial Forage Cultivation in Saudi Arabia,” Okaz, okaz.com.sa. Iran also contributes to this trend, with its substantial cattle population and a robust poultry industry supported by domestic feed manufacturing capabilities. In 2026, Saudi Arabia’s 13 livestock agreements with Russia, valued at SAR 4.8 billion (USD 1.3 billion), further indicate ongoing efforts to enhance protein production capacity across the value chain. As feed volumes expand in both poultry and ruminant systems, the Middle East feed flavors and sweeteners market benefits from a growing base of commercial formulas reliant on stable intake.

Shift Toward Antibiotic-Free Feed Programs

The shift away from antibiotic growth promoters is influencing feed formulation practices across poultry and livestock systems in the region. With reduced or eliminated antibiotic support, producers often require a targeted combination of gut health tools and sensory aids to sustain feed intake during periods of stress. Flavors and sweeteners play a significant role in this context, as they help mitigate off-notes and acceptance challenges that become more apparent with changes in feed programs. Research published in Frontiers in Animal Science in 2025 found that phytogenic and fermentation-based additives can maintain performance under heat-stress conditions following antibiotic removal, a finding particularly relevant to Middle Eastern production environments. Additionally, Saudi Arabia’s National Action Plan on Antimicrobial Resistance for 2023-2028 promotes the broader use of alternative functional ingredients in livestock feeding systems. Reflecting this trend, product development has adapted, with ADM introducing a monk fruit-based sweetener as a saccharin-free option tailored to species-specific sweet taste responses. Consequently, the Middle East feed flavors and sweeteners market is benefiting from regulatory and technical changes that align palatability solutions with broader feed health reformulation efforts.

Expansion of Modern Feed Milling Capacity

Feed mill modernization is one of the quieter but more durable growth drivers for the Middle East feed flavors and sweeteners market. Newer plants use automated dosing, more consistent batching, and better quality control, all of which make it easier to include specialty additives at repeatable levels. Saudi Arabia’s new high-capacity poultry mill projects show that the region is still adding industrial feed infrastructure rather than relying only on older, fragmented production assets. Iran also has a deep domestic feed manufacturing base, which supports a gradual move from legacy operations toward more standardized compound feed production. As mills scale up, it becomes easier for suppliers of flavors and sweeteners to justify technical service, on-site trials, and customized product placement across larger customer volumes. Better equipment also improves the economics of premium low-dose ingredients by reducing formulation variability and waste. This is important because the Middle East feed flavors and sweeteners market does not rely solely on herd growth, but it also relies on improved physical infrastructure that increases the share of feed output suitable for value-added additive systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on Imported Specialty Ingredients | -0.8% | Saudi Arabia, United Arab Emirates, and Bahrain | Short term (≤ 2 years) |

| Price Sensitivity Among Small Feed Producers | -0.6% | Iran, and Rest of Middle East | Medium term (2-4 years) |

| Limited Local Formulation and Testing Infrastructure | -0.5% | Rest of Middle East | Long term (≥ 4 years) |

| Supply Chain Disruptions and Trade Volatility | -0.6% | Saudi Arabia, United Arab Emirates, and Iran | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dependence on Imported Specialty Ingredients

The region heavily relies on imported specialty ingredients for advanced feed flavor and sweetener systems. Key components such as natural flavor bases, encapsulated palatants, and active sweetener compounds are predominantly sourced from Europe, the United States, and Asia, rather than domestic production. This reliance subjects feed mills to multiple cost pressures, including freight charges, currency fluctuations, and extended procurement cycles. The issue became particularly evident in early 2026, when military escalation near the Strait of Hormuz prompted major shipping lines to halt Gulf operations, resulting in significant delays in feed additive deliveries. Additionally, regulatory approval processes hinder emergency substitutions, as registration and cross-border acceptance are often too slow to address immediate shortages. Consequently, the Middle East feed flavors and sweeteners market exhibits structural vulnerability, such as demand remaining steady, but product availability can unexpectedly become constrained. This dependency also limits pricing flexibility for smaller buyers, who typically lack the capacity to maintain inventory or secure favorable logistics terms compared to larger, integrated customers.

Price Sensitivity Among Small Feed Producers

Price sensitivity remains a significant barrier for small and mid-sized producers outside the largest integrated feed and livestock companies. These producers often assess additives based on a short-term payback perspective, making it challenging to adopt higher-cost flavor and sweetener systems, even when their technical benefits are evident. This issue is particularly pronounced in cost-constrained markets, where feed ingredients already account for a substantial portion of production expenses. For instance, Jordan imports nearly 90% of its essential feed ingredients, such as corn and soy, leaving limited flexibility for discretionary formulation upgrades when raw material prices increase. In such scenarios, mills often reduce additive usage first when margins tighten, even if this decision negatively impacts feed intake or conversion efficiency over time. Consequently, the Middle East feed flavors and sweeteners market experiences uneven growth, with premium adoption concentrated among larger, well-capitalized operations, while smaller mills remain cautious about spending on specialty inputs. Unless suppliers can provide clearer cost-benefit positioning or develop lower-dose premium systems, this cautious approach is anticipated to continue, limiting broader market penetration in the region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Flavors Dominate the Market, Sweeteners Undergo Reformulation

Flavors account for 82.2% of the Middle East feed flavors and sweeteners market in 2025, maintaining their leading position. This dominance is attributed to the widespread use of flavor systems in broiler starter and grower feeds and in dairy total mixed rations, which help mask variations in raw material characteristics and ensure consistent feed acceptance. Additionally, flavor usage is often integrated into standard feed specifications at many poultry and dairy operations. Adisseo’s 2025 dairy nutrition partnership program in the Middle East and Africa highlights the increasing need to balance precision nutrition with reliable intake in dairy cattle, further supporting the use of flavor systems in controlled feeding programs. However, suppliers face challenges as mills increasingly prefer lower-dose, higher-potency systems that achieve similar sensory outcomes at reduced inclusion rates.

Sweeteners are projected to grow at a compound annual growth rate (CAGR) of 4.3% through 2031, positioning them as the fastest-growing subcategory despite their currently smaller market value. This growth is primarily attributed to the saccharin-free reformulation trend in imported European feed additives, driven by Regulation EU 2024/1727, which mandates compliance for compound feed by July 2026. The European Food Safety Authority’s (EFSA) 2025 assessment of NHDC safety has further clarified the pathway for saccharin replacements. Companies such as Phytobiotics and ADM have introduced saccharin-free alternatives utilizing natural or receptor-targeted sweetener systems. As this transition is influenced by imported feed reformulation rather than local bans, distributors in the Middle East feed flavors and sweeteners market face pressure to qualify alternative sweetener systems before broader changes are implemented in supplier formulations.

By Animal: Ruminants Dominate in Scale and Drive Growth

Ruminants accounted for 49.4% of the Middle East feed flavors and sweeteners market share in 2025 and are projected to grow at a compound annual growth rate (CAGR) of 4.3% through 2031. This makes ruminants both the largest and fastest-growing animal segment in the market. This dominance is attributed to the dairy and beef feeding practices prevalent across the Gulf region, where total mixed rations often include silage and fermented inputs. These inputs can reduce feed attractiveness if not effectively masked. In such systems, intake stability is critical, as daily dry matter consumption directly impacts milk yield, animal health, and feed efficiency. Saudi Arabia’s ongoing investment in livestock capacity, including SAR 4.8 billion (USD 1.3 billion) in agreements related to the livestock sector, supports the scale of this demand. Additionally, the planned cessation of perennial forage cultivation in Saudi Arabia by November 2026 is anticipated to increase reliance on commercial rations, further emphasizing the importance of palatability additives in dairy and beef feed.

Swine remains a minor segment in the Middle East due to religious and consumption constraints across much of the region. However, it plays a role in product development for sweetener innovation. Many of the most well-documented intake responses for advanced sweetener systems are derived from piglet and post-weaning trials. This technical knowledge can be applied to calf, lamb, and transitional rations, contributing to advancements in feed formulations for other animal categories.

The Other Animals category, which includes aquaculture and equine animals, constitutes the remainder of regional demand. Meanwhile, aquaculture is emerging as a new growth area, particularly following Saudi Arabia's approval of microbial protein use in aquaculture feed in early 2025. This development highlights opportunities for the Middle East feed flavors and sweeteners market to expand beyond its current focus on ruminants and swine, with potential growth in specialized aquaculture and young-animal feed programs.

Geography Analysis

Saudi Arabia holds a 45% market share in 2025, with a projected CAGR of 5.8% through 2031, making it the fastest-growing country segment in the Middle East feed flavors and sweeteners market. The country's growth is supported by strong policy initiatives focused on food security and local protein production under Vision 2030. Investments in the animal production chain, including livestock agreements worth SAR 4.8 billion (USD 1.3 billion), highlight continued development in this sector. The planned halt in forage cultivation in November 2026 is anticipated to significantly impact ruminant feed programs, shifting the focus toward commercial compound feed and related palatability systems.

Iran is anticipated to grow over the forecast period, supported by its extensive domestic feed production system, ample local grain availability, and a well-developed manufacturing base. These factors create a substantial market for feed flavors and sweeteners, despite historically lower penetration compared to some Gulf markets. As advancements in milling technology improve dosing precision, the use of additives is becoming more standardized in commercial feed production. However, trade restrictions and currency controls have limited access to imported specialty inputs, resulting in a market characterized by current limitations and future growth potential.

The United Arab Emirates is a significant market, driven by its focus on premium feed strategies, which are increasingly important in commercial operations. In contrast, Jordan faces cost constraints due to its reliance on imports for nearly 90% of core feed ingredients. This limits spending on additives but underscores the long-term value of solutions that enhance feed utilization. Additionally, common Gulf regulatory frameworks facilitate more efficient approval processes for suppliers across multiple neighboring markets.

Competitive Landscape

The Middle East feed flavors and sweeteners market was moderately concentrated in 2025, with the top 5 players, including Adisseo as the market leader, followed by Alltech, ADM, Cargill Incorporated, and Solvay S.A. The rest of the market remained split between smaller specialists and European niche suppliers that handle market access and customer service. This structure means large companies still influence product direction and premium pricing, but no single supplier has enough market share to gain a significant competitive advantage. The Middle East feed flavors and sweeteners market, therefore, still rewards technical service, local partnerships, and product positioning tied to ruminant feeding conditions.

Leading players are also broadening their role beyond simple ingredient supply. ADM expanded SINCRO data-driven services in October 2025, showing how major companies are linking additives with digital and advisory tools that make customer relationships harder to displace. Adisseo’s 2025 dairy partnership program in the Middle East and Africa pointed in the same direction, with additive suppliers moving closer to precision nutrition support. In parallel, the Middle East feed flavors and sweeteners industry is seeing more interest in natural sweeteners, phytogenic products, and application-led systems that combine sensory and functional claims.

Consolidation and portfolio reshaping have become more visible in 2025 and 2026. PAI Partners completed the acquisition of Innov Ad NV/SA in 2026, which highlighted investor interest in specialty feed additives with scalable international customer bases[3]Source: IK Partners, “PAI Partners Acquires Innovad Group from IK Partners,” IK Partners Press Release, ikpartners.com. ADM and Alltech also launched the Akralos Animal Nutrition joint venture in February 2026, bringing a large feed mill network under one platform. Solvay, meanwhile, faces a more specific portfolio shift as saccharin demand changes under new European rules, which increases the urgency of moving toward alternative sweetener chemistries

Middle East Feed Flavors and Sweeteners Industry Leaders

Adisseo

Cargill Incorporated

Alltech

ADM

Solvay S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Orffa inaugurated its Science Lab in Breda, the Netherlands, on June 1. This facility serves as a dedicated research and diagnostics center aimed at providing actionable insights into palatability and nutrition for customers. The lab enhances Orffa's applied science capabilities, supporting the development of targeted flavor and specialty additive solutions for ruminant and swine species in the Middle East region.

- April 2026: Alltech introduced Olerix, a phytogenic blend of essential oils, classified as a flavoring feed additive under EU feed regulations. The product is designed to enhance voluntary feed intake, feed conversion efficiency, and gut health resilience in swine nursery and finishing operations. It was developed through validated commercial trials, which demonstrated consistent improvements in growth performance and livability under real production conditions.

- April 2025: Phytobiotics developed and launched PhytoSense 2.5, a saccharin-free natural sweetener for weaned piglets and transitional livestock rations validated in a 42-day trial.

Middle East Feed Flavors and Sweeteners Market Report Scope

Feed flavors and sweeteners are palatability-enhancing additives mixed into animal feed to improve its smell and taste. The Middle East feed flavors and sweeteners market report is segmented by type (flavors and sweeteners), by animal (ruminants, swine, and other animals), and by country (Iran, Saudi Arabia, and the rest of the Middle East). The market forecasts are provided in terms of value (USD) and volume (metric tons).

| Flavors |

| Sweeteners |

| Swine | |

| Ruminants | Dairy Cattle |

| Beef Cattle | |

| Others | |

| Others |

| Iran |

| Saudi Arabia |

| Rest of Middle East |

| By Type | Flavors | |

| Sweeteners | ||

| By Animal | Swine | |

| Ruminants | Dairy Cattle | |

| Beef Cattle | ||

| Others | ||

| Others | ||

| By Country | Iran | |

| Saudi Arabia | ||

| Rest of Middle East | ||

Key Questions Answered in the Report

What is the projected value of the Middle East feed flavors and sweeteners market by 2031?

It is projected to reach USD 212.3 million by 2031, rising from USD 162.5 million in 2026 at a 5.5% CAGR over 2026-2031.

Which sub additive category leads demand in 2025?

Flavors lead demand with 82.2% of total value in 2025 because they are already embedded in aquaculture and dairy feed formulations across key regional markets.

Which animal segment has the strongest demand?

Ruminants lead with 49.4% share in 2025 and also post the fastest projected growth at 4.3% CAGR through 2031.

Why is Saudi Arabia important for future growth?

Saudi Arabia records the fastest projected CAGR at 5.8% through 2031, supported by feed mill expansion, livestock investment, and tighter forage availability.

What is driving faster growth in sweeteners?

Sweeteners are growing faster because imported feed additives are moving toward saccharin-free reformulation, which is increasing interest in NHDC, stevia, and monk fruit-based options.

Page last updated on: