Africa Feed Binders Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

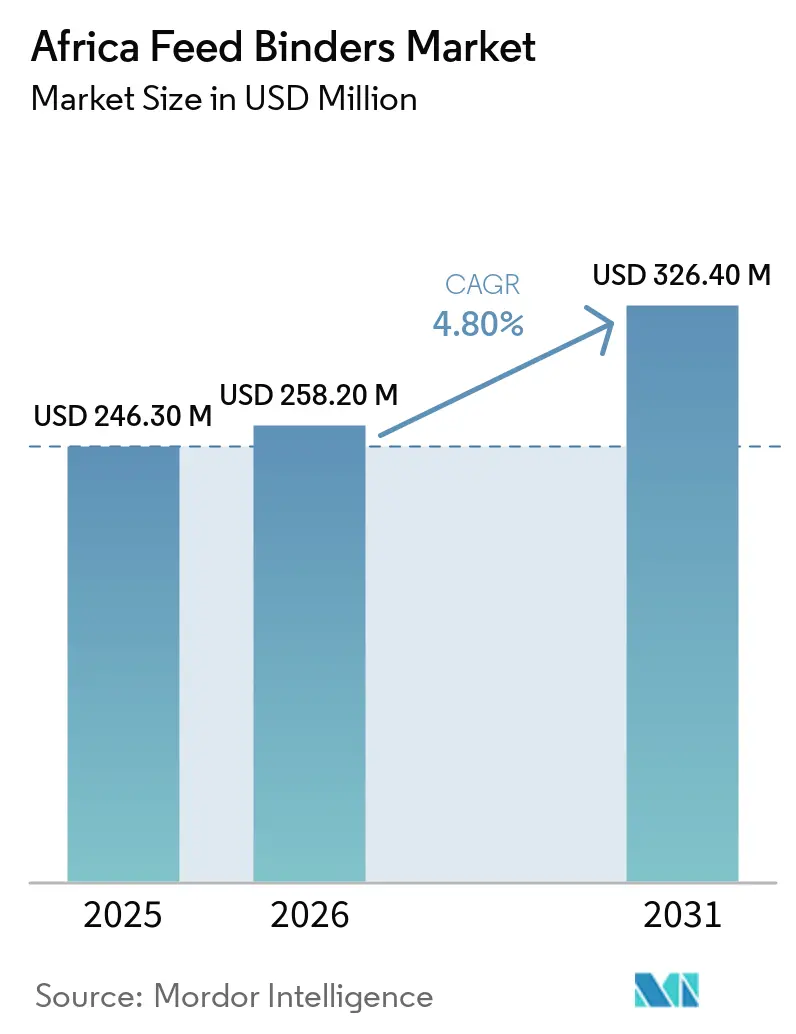

| Base Year Market Size (2025) | USD 246.30 Million |

| Market Size (2026) | USD 258.20 Million |

| Market Size (2031) | USD 326.40 Million |

| Growth Rate (2026 - 2031) | 4.80% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Feed Binders Market Analysis by Mordor Intelligence

The Africa feed binders market size is anticipated to grow from USD 246.30 million in 2025 to USD 258.20 million in 2026 and is forecast to reach USD 326.40 million by 2031 at 4.80% CAGR over 2026-2031. The Africa feed binders market is expanding as commercial feed production scales across the region and feed mills move away from informal mixing toward standardized pelleting systems that depend on consistent binder performance. Urbanization and rising protein consumption in countries such as Nigeria, Egypt, South Africa, and Kenya are increasing demand for higher pellet quality, stronger feed conversion, and lower rework in large mills, keeping the Africa feed binders market closely tied to broader livestock modernization trends. The market is also being shaped by a split between mills that can justify premium formulations and mills that remain exposed to imported input costs, exchange-rate pressure, and uneven raw material quality. South Africa remains central because it combines a mature compound feed base with domestic lignosulfonate production, while other countries still rely more heavily on imports for specialty and mineral binder grades. Mills that connect binder use with lower pellet fines, lower energy use, and better throughput are likely to move faster on adoption than mills that assess binders only as an additive cost line.

Key Report Takeaways

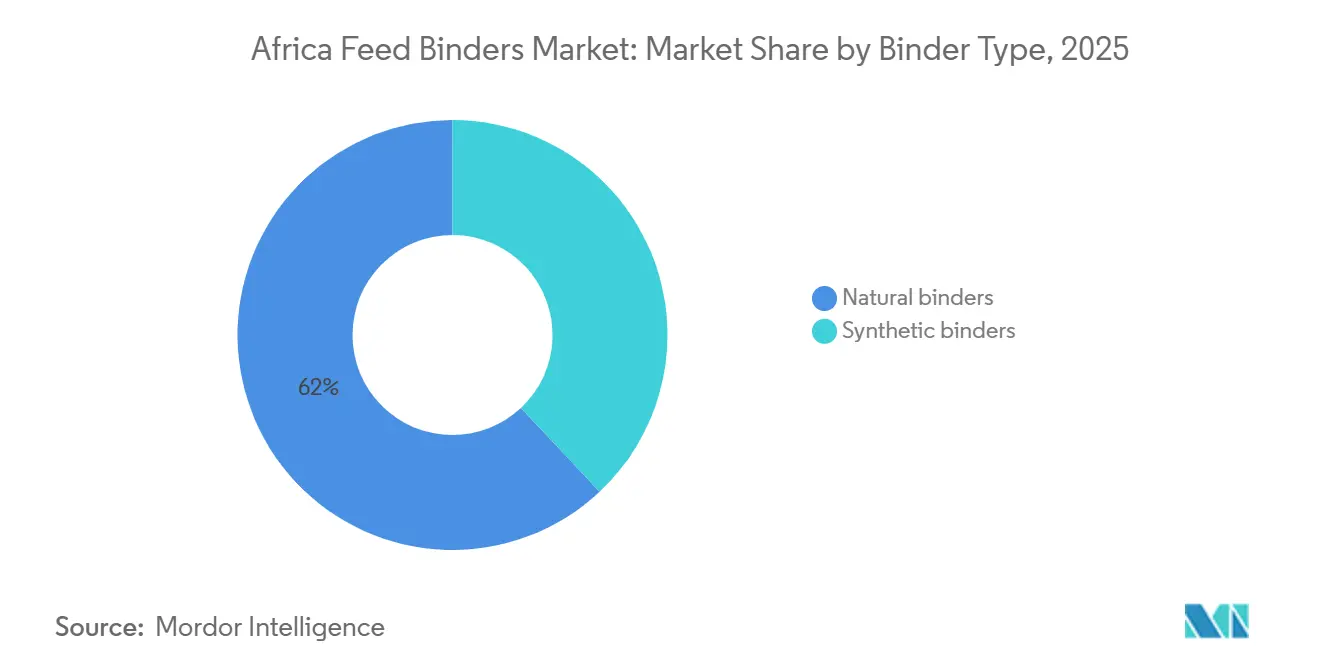

- By sub additives, natural binders held the largest share of the Africa feed binders market in 2025, at 62%, while the fastest-growing binder type is natural binders, with a CAGR of 4.8% from 2026 to 2031.

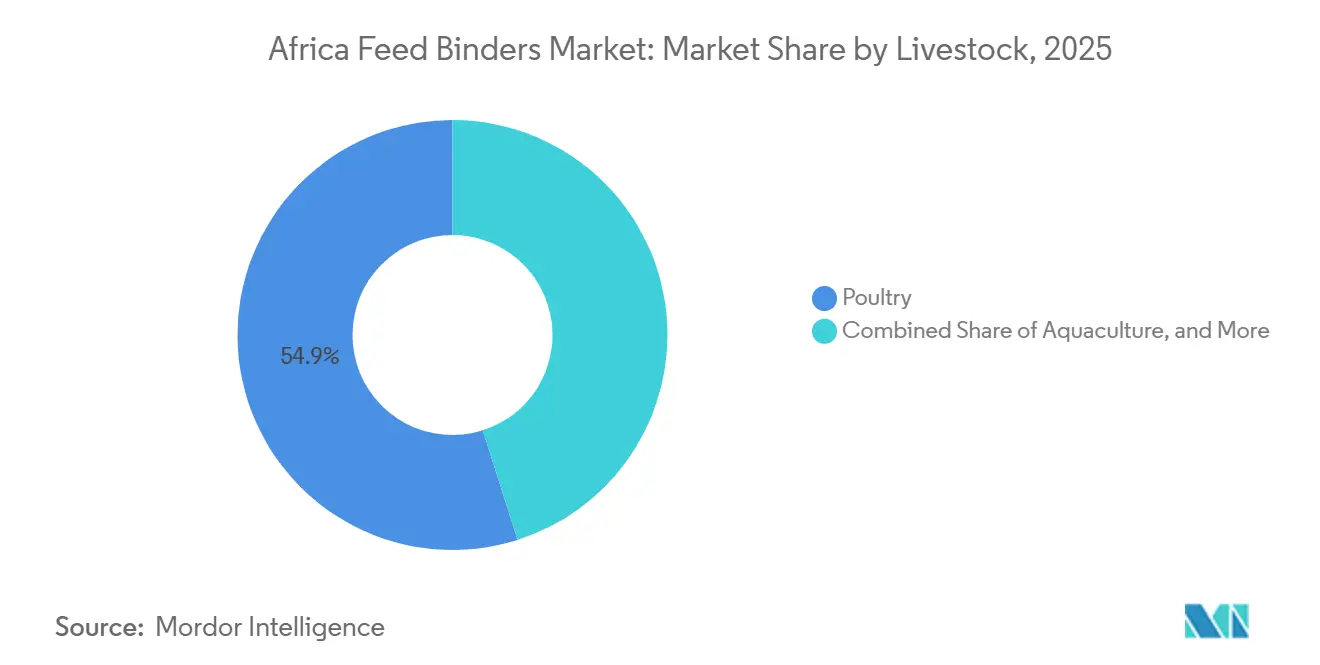

- By animal, poultry account for the largest segment, 54.9% of the Africa feed binders market size in 2025, while aquaculture is projected to be the fastest-growing segment, at a 6.8% CAGR through 2026 to 2031.

- By geography, South Africa accounted for 45.5% of the Africa feed binders market share in 2025, while Ethiopia is the fastest-growing geography, with a 7.64% CAGR through 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Feed Binders Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising compound feed output in Africa | +1.3% | Africa-wide, led by South Africa, Nigeria, Egypt, and Kenya | Short term (≤ 2 years) |

| Poultry feed pelletization demand | +1.2% | South Africa, Nigeria, Egypt, Kenya, and Morocco | Medium term (2-4 years) |

| Aquaculture feed expansion and water-stability needs | +0.9% | Nigeria, Kenya, Uganda, Tanzania, and Zambia | Medium term (2-4 years) |

| Fines reduction and nutrient retention gains | +0.7% | Africa-wide, strongest in large-scale mills in South Africa and Egypt | Short term (≤ 2 years) |

| Shift toward natural lignin-based binders | +0.6% | South Africa and import-dependent African markets | Long term (≥ 4 years) |

| Energy-cost savings from stronger pellets | +0.5% | South Africa, Kenya, and Nigeria | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Compound Feed Output in Africa

Rising compound feed output remains one of the clearest demand anchors for the Africa feed binders market. Commercial feed production creates a direct need for binding chemistry because pelleted output depends on durability, lower fines, and stable throughput, whereas on-farm loose feed does not. Africa's feed production is estimated to reach 64.2 million metric tons annually by 2025, including compound feed. South Africa, Nigeria, Egypt, and Kenya are projected to lead in terms of installed mill capacity capable of accommodating higher binder volumes. Government-backed plans in Nigeria and regulatory testing activity in Egypt also indicate that feed production is being organized more formally, improving the conditions for additive qualification and repeat procurement. As more feed volume moves into standardized mill systems, the Africa feed binders market gains from every new pelleting line, every mill upgrade, and every shift from informal mixing to industrial production.

Poultry Feed Pelletization Demand

Poultry remains the most dependable volume base for the Africa feed binders market because it combines scale, commercial structure, and tight pressure on feed efficiency. Broiler and layer operations depend heavily on pellet consistency, which makes binders important not only for pellet integrity but also for feed conversion, handling performance, and reduced nutrient loss during transport. According to the United States Department of Agriculture (USDA), South Africa's poultry chicken meat production reached 1,645 thousand metric tons in 2025[1]Source: USDA Foreign Agricultural Service, “The South African Animal Feed Industry,” USDA FAS, apps.fas.usda.gov. Recovery efforts and Nigeria's emphasis on stronger feed and fodder policy frameworks have supported the continued use of pellet-oriented additives in the region's largest feed-consuming livestock system.

Aquaculture Feed Expansion and Water-Stability Needs

Aquaculture is the fastest-growing end-use for the Africa feed binders market because fish feed places a much higher premium on water stability than land-animal feed. Floating and sinking pellets must retain their shape long enough to limit nutrient loss and avoid water contamination, making binder performance a technical requirement rather than a formulation preference. The opening of De Heus’s fish feed factory in Uganda in September 2025 added 100,000 metric tons of annual capacity in East and Central Africa, which immediately widened demand for aquafeed-grade binders[2]Source: De Heus Animal Nutrition, “De Heus Opens State-of-the-Art Fish Feed Factory in Uganda,” De Heus Uganda, deheus.ug. In 2025, the planned DiscoverAqua facility in Kenya and Kenya’s broader aquaculture output target reinforce the same direction of travel in East Africa, while Nigeria and other freshwater farming centers continue to expand their fish feed base. This keeps aquaculture central to the forward growth profile of the Africa feed binders market through 2031.

Fines Reduction and Nutrient Retention Gains

Lower fines and better nutrient retention support the Africa feed binders market because mills lose value whenever pellets break down in the line, in storage, or in transport. Better binding performance reduces rework, protects formulation consistency, and improves the odds that animals consume the intended nutrient mix rather than a separated ration. In large mills, the commercial effect is visible in throughput stability and fewer interruptions around conditioning and pelleting. In smaller mills, the benefit is simpler but still important because lower dust and lower pellet breakage can reduce waste even when technical instrumentation is limited. Suppliers that frame the value of the Africa feed binders market around measurable operating outcomes rather than abstract pellet metrics are likely to improve adoption, especially in mills where every tonne of finished feed must move quickly through constrained equipment

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported specialty binder costs and currency volatility | -0.9% | Nigeria, Egypt, Kenya, Algeria, and Ethiopia | Medium term (2-4 years) |

| Price sensitivity among small and mid-sized feed mills | -0.7% | Nigeria, Ethiopia, Tanzania, and Zambia | Long term (≥ 4 years) |

| Unstable power and steam availability | -0.5% | Nigeria, South Africa, and Ethiopia | Medium term (2-4 years) |

| Grain-quality variability and mycotoxin-heavy raw materials | -0.3% | Sub-Saharan Africa, with strong exposure in Kenya, Nigeria, and Zambia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Imported Specialty Binder Costs and Currency Volatility

Import dependency continues to be a significant constraint on the African feed binders market. The majority of synthetic and premium mineral binders used across the region still come from Europe and North America, which means freight costs, tariffs, and currency weakness feed directly into landed prices. Local currencies in several Africa markets are projected to depreciate significantly against the United States dollar in 2024 and 2025. This depreciation has led mills to shorten their purchasing cycles and reduce stock levels. As a result, the adoption of premium binders becomes more challenging, as they must demonstrate value not only through technical performance but also within a rapidly changing budgeting environment influenced by fluctuating exchange rates. Suppliers with local production facilities or distributor-held stock, such as Sappi in South Africa, are better positioned to navigate currency-related challenges in the African feed binders market.

Grain-Quality Variability and Mycotoxin-Heavy Raw Materials

Grain-quality variability and mycotoxin pressure create a more subtle but persistent obstacle for the Africa feed binders market. Maize, sorghum, and groundnut meal form a large part of the region’s feed base, and variable crop quality changes pellet behavior and binder response from batch to batch. This makes optimization harder because the same dose rate may not perform consistently across different raw material conditions. Additionally, recurring mycotoxin contamination prolongs trial cycles for premium binders, creating adoption challenges for mills already facing cost pressures. In cases where mills require ingredients that enhance both pelleting performance and overall feed safety, traditional binder-only solutions often struggle to gain acceptance in the African feed binders market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Additives: Natural Binders Sustain Lead, Mineral Variants Gain Ground in Aquafeed

Natural binders accounted for 62% of the Africa feed binders market in 2025 and are projected to grow at a CAGR of 4.8% between 2026 and 2031, maintaining their leading position across poultry, ruminant, and aquaculture applications. Their dominance is attributed to effective binding performance, familiarity among feed manufacturers, and broader regulatory acceptance. In South Africa, Sappi’s Pelletin production at the Tugela Mill provides a competitive advantage by ensuring a reliable local supply of binder products, which are still imported in many other African markets. This domestic availability enhances supply security and reduces exposure to currency fluctuations and freight-related costs associated with specialty feed additives. Starches, dextrins, and molasses-based products remain the cornerstone of the natural binder segment, with molasses playing a particularly significant role in Southern African ruminant feed formulations, contributing to palatability and feed intake.

Synthetic binders continue to serve specialized applications within the Africa feed binders market, particularly where feed mills require enhanced water stability, stronger pellet integrity, or tighter process control. However, the adoption of synthetic binders remains limited due to higher costs and continued reliance on imports across much of the continent. Meanwhile, mineral-based binders such as bentonite, kaolin, and sepiolite are gaining traction in countries like Kenya, Uganda, and Tanzania, where feed producers are increasingly focusing on pellet durability and mycotoxin management. Consequently, the market is becoming more diversified than the overall share distribution suggests, although natural binders continue to dominate volume demand and remain the primary growth driver of the Africa feed binders industry.

By Animal: Poultry Dominates, Aquaculture Captures the Growth Premium

Poultry remained the largest share of livestock demand in the Africa feed binders market in 2025, representing 54.9% of the market. That position reflects the scale of poultry feed output, the standard use of pellet formats, and the role of integrated producers in setting pellet-quality expectations across their supply chains. Poultry feed buyers place constant pressure on conversion, waste reduction, and cost control, so binders stay relevant even when mills remain cautious on additive spending. Commercial poultry systems in South Africa, Nigeria, Egypt, Morocco, and Kenya provide the largest recurring binder volumes because these are the markets where pelleting is most standardized. The Africa feed binders market, therefore, continues to rely on poultry for base demand, even as its strongest growth moves elsewhere.

Aquaculture is the fastest-growing livestock segment in the Africa feed binders market, with a projected 6.8% CAGR through 2031. In 2025, the opening of De Heus’s Ugandan plant and the planned DiscoverAqua mill in Kenya were significant as they introduced modern extruded-feed capacity in markets where water stability was a necessity rather than an option. Ruminants provide a broad but fragmented base, while swine feed remains a smaller, more organized market centered mainly in South Africa and Morocco. This mix means the Africa feed binders market is still volume-led by poultry but is being pushed forward by aquaculture, which carries more demanding technical standards and stronger willingness to specify performance at the formula level.

Geography Analysis

In 2025, South Africa accounted for 45.5% of the Africa feed binders market share, positioning itself as the primary regional hub for supplier activity and product qualification. The country benefits from a well-developed compound feed sector and hosts Africa's only commercially established domestic lignosulfonate supply chain, operated through Sappi’s Tugela Mill. Additionally, South Africa has a concentrated base of industrial feed producers that prioritize pellet durability, mill efficiency, and procurement reliability over cost considerations. The United States Department of Agriculture has described the South African feed industry as one of the most advanced on the continent, underscoring its critical role in the regional procurement structure for feed binders.

Nigeria and Egypt present significant growth opportunities within the Africa feed binders market, driven by distinct factors. Nigeria's potential lies in its large-scale poultry feed production and policy initiatives to accelerate feed and fodder development, which could increase the adoption of standardized additives. Conversely, Egypt's strength lies in its regulatory framework and the scale of its feed manufacturing system, which supports the consistent use of additives in controlled commercial environments. Meanwhile, Kenya, Morocco, and Algeria maintain steady demand through organized poultry and dairy systems. Morocco and Algeria rely on larger commercial mills, while Kenya contributes additional growth momentum through its expanding aquaculture sector.

Ethiopia is the fastest-growing market in the region, with a projected CAGR of 7.64% from 2026 to 2031. This growth is driven by Ethiopia's large livestock herd, the largest in Africa, which includes cattle, sheep, goats, poultry, and camels. As livestock production becomes more commercialized, demand for compound feed increases, directly driving the use of feed binders to improve pellet durability, reduce feed waste, and enhance feed quality. According to the International Livestock Research Institute, Ethiopia's livestock population in 2025 included over 70 million cattle, 52.5 million goats, and 42.9 million sheep, which significantly drives the demand for feed binders.

Competitive Landscape

The Africa feed binders market is fragmented, with key players such as BASF SE, Borregaard ASA, Kemin Industries, Inc., Alltech, Inc., and Sappi Limited collectively accounting for significant revenue in 2025. A substantial portion of the market remains accessible to regional specialists, local distributors, and smaller additive suppliers, who compete based on factors such as availability, packaging sizes, and market coverage. Sappi benefits from a structural local advantage due to its connection to Africa’s only commercially established domestic lignosulfonate production base for feed applications. Borregaard maintains strong technical credibility through its LignoBond product and the regulatory reauthorization in March 2024, which enhances its position with mills monitoring European Union-linked compliance standards.

A clear gap in the African feed binder market remains the lack of products and dosing systems designed specifically for smaller mills. Another open space lies in solutions that combine pellet performance with mycotoxin-related value, as many mills face both problems simultaneously. Companies that can localize mineral binder supply or simplify liquid dosing stand to gain from this unmet need. The market is also likely to reward suppliers that can meet certification filters such as GMP+ as multinational feed and protein buyers tighten vendor qualification standards in African procurement chains.

Competitive positioning in the market is increasingly shaped by suppliers' ability to deliver technical support and measurable production outcomes, rather than solely focusing on binder performance. Many feed mills in Africa, particularly in emerging livestock markets, operate with limited process optimization capabilities. As a result, these mills place significant value on suppliers that can assist with pellet mill efficiency, formulation adjustments, and quality assurance. Companies that combine binder products with on-site technical services, training programs, and performance monitoring are likely to enhance customer retention and distinguish themselves in a market where product offerings are often similar. As feed manufacturers prioritize reducing production costs while maintaining pellet quality, solution-oriented suppliers are projected to strengthen their presence across the region.

Africa Feed Binders Industry Leaders

BASF SE

Borregaard ASA

Kemin Industries, Inc.

Alltech, Inc.

Sappi Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: De Heus established a fish feed factory in Uganda with a production capacity of up to 100,000 metric tons annually to support aquaculture growth in East Africa. This development is significant for the Africa feed binders market, as the expansion of aquafeed production is anticipated to drive demand for pellet-binding solutions that enhance feed durability, water stability, and nutrient retention in fish feed.

- July 2024: Morocco implemented Decree No. 2-23-557, introducing updated standards for the quality, health safety, and labeling of animal feed intended for food-producing animals. This regulatory change is significant for the Africa feed binders market, as stricter requirements for feed manufacturing and additive compliance are anticipated to drive demand for certified technological additives, such as pellet binders, which enhance feed consistency and durability.

- April 2024: Sappi Southern Africa obtained the GMP+ Feed Safety Assurance certification for its Pelletin product range, produced at the Tugela Mill in South Africa. This development is significant for the Africa feed binders market, as Pelletin, a lignosulphonate-based pellet binder used in animal feed, enhances the availability of locally certified feed binder solutions and improves supply reliability for feed manufacturers in the region.

Africa Feed Binders Market Report Scope

Feed binders are additives incorporated into animal feed formulations to enhance the physical integrity and durability of feed pellets, crumbles, or mash. The Africa feed binders market report is segmented by binder type (natural binders, synthetic binders, and mineral binders), by animal (aquaculture, poultry, ruminants, swine, and other animals), and by geography (South Africa, Nigeria, Egypt, Kenya, Morocco, and Others). The market forecasts are provided in terms of Value (USD) and Volume (Metric Tons).

| Natural binders |

| Synthetic binders |

| Poultry | ||

| By Sub Animal | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | ||

| Beef Cattle | ||

| Dairy Cattle | ||

| Other Ruminants | ||

| Aquaculture | By Sub Animal | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Swine | ||

| Other Animal | ||

| South Africa |

| Nigeria |

| Egypt |

| Kenya |

| Morocco |

| Rest of Africa |

| By Binder Type | Natural binders | ||

| Synthetic binders | |||

| By Animal | Poultry | ||

| By Sub Animal | Broiler | ||

| Layer | |||

| Other Poultry Birds | |||

| Ruminants | |||

| Beef Cattle | |||

| Dairy Cattle | |||

| Other Ruminants | |||

| Aquaculture | By Sub Animal | Fish | |

| Shrimp | |||

| Other Aquaculture Species | |||

| Swine | |||

| Other Animal | |||

| By Geography | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Kenya | |||

| Morocco | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and outlook for feed binders in Africa?

The Africa feed binders market stood at USD 258.20 million in 2026 and is forecast to reach USD 326.40 million by 2031, growing at a 4.80% CAGR over 2026-2031.

Which livestock category creates the largest demand for binders across Africa?

Poultry is the largest demand base because it represented 54.9% of Africa's feed additive demand in 2025 and depends heavily on pellet quality and feed efficiency.

Which livestock category is growing the fastest for binder demand?

Aquaculture is the fastest-growing end use, with a projected 6.8% CAGR through 2031, supported by new fish feed capacity in Uganda and Kenya.

Why does South Africa lead regional demand?

South Africa held 45.5% of regional revenue in 2025 because it combines a mature feed industry, large integrated producers, and domestic lignosulfonate production through Sappi's Tugela Mill.

Page last updated on: