Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

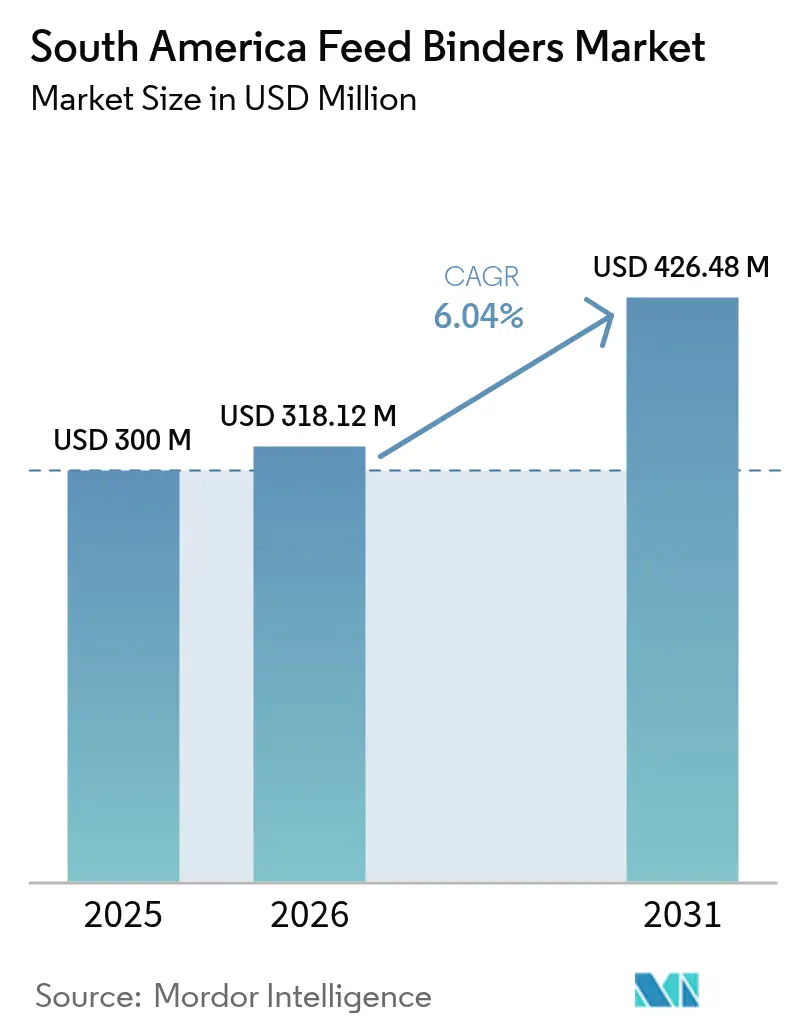

| Base Year Market Size (2025) | USD 300 Million |

| Market Size (2026) | USD 318.12 Million |

| Market Size (2031) | USD 426.48 Million |

| Growth Rate (2026 - 2031) | 6.04% CAGR |

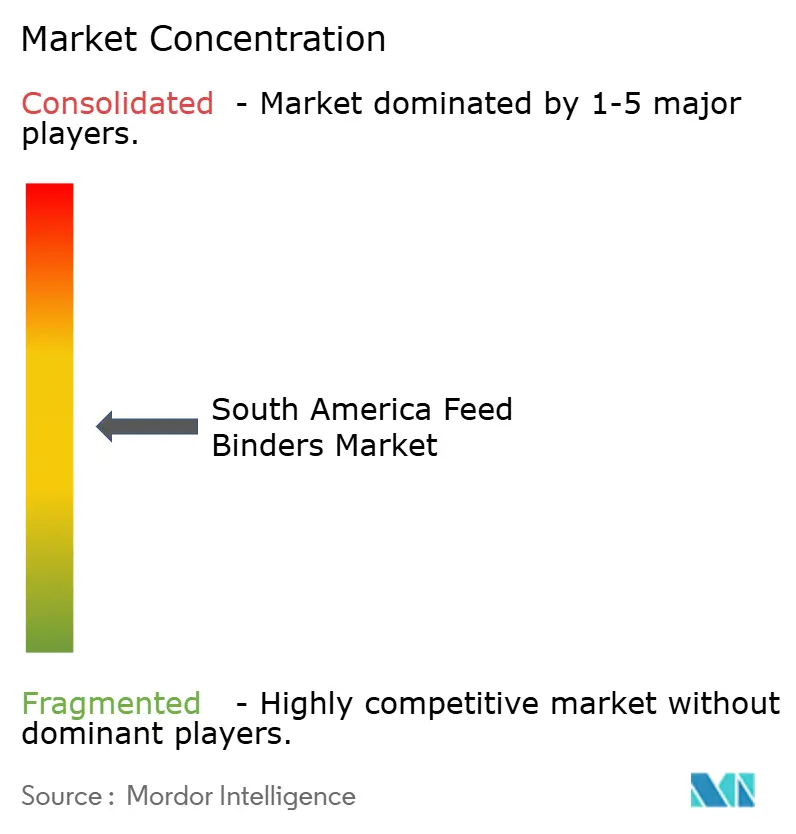

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Feed Binders Market Analysis by Mordor Intelligence

The South America Feed Binders Market size is expected to grow from USD 300 million in 2025 to USD 318.12 million in 2026 and is forecast to reach USD 426.48 million by 2031 at 6.04% CAGR over 2026-2031. This growth trajectory reflects the region's expanding livestock meat production base and increasing adoption of precision feed manufacturing technologies that require advanced binding solutions to maintain pellet integrity and nutritional consistency. For instance, according to FAOSTAT, South America's poultry meat production was 22.6 million metric tons in 2021, increasing to 23.4 million metric tons in 2023 [1]Source: Food and Agriculture Organization of the United Nations, “FAOSTAT: Livestock and Fishery Production Domain,” fao.org. Natural binders already command a dominant position, reflecting corporate sustainability pledges and consumer pressure to reduce synthetic ingredients. Aquaculture producers in Brazil’s Amazon Basin and Chile’s salmon industry are adopting water-stable plant and marine hydrocolloids, while poultry integrators across Brazil and Colombia specify dual-function binders that offer structural integrity and gut health benefits. Investment momentum remains robust, as illustrated by ADM’s 40% capacity expansion in Paraná and Cargill, Incorporated recent mill acquisitions, which expand the regional reach. Despite these positives, the volatility of raw material costs and the capital intensity of modern pellet mills continue to temper adoption among smaller feed manufacturers.

Key Report Takeaways

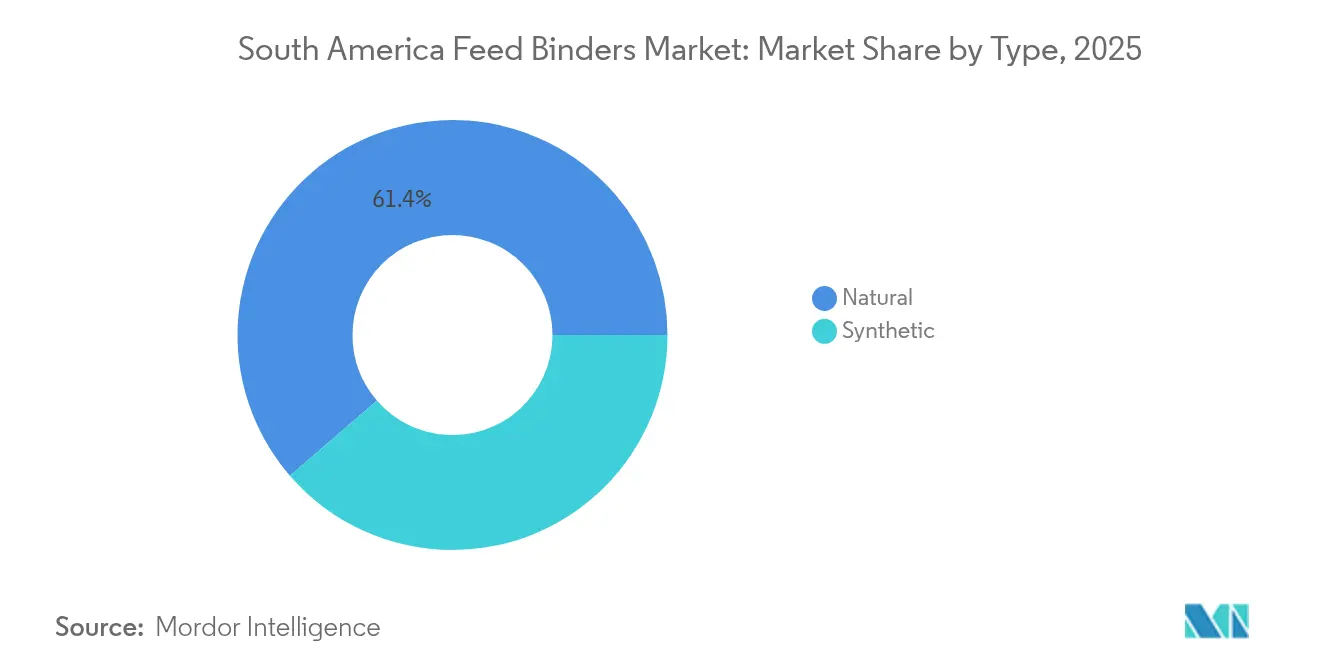

- By type, natural binders led the South America feed binders market with a 61.35% market size in 2025 and are forecast to expand at a 7.34% CAGR through 2031.

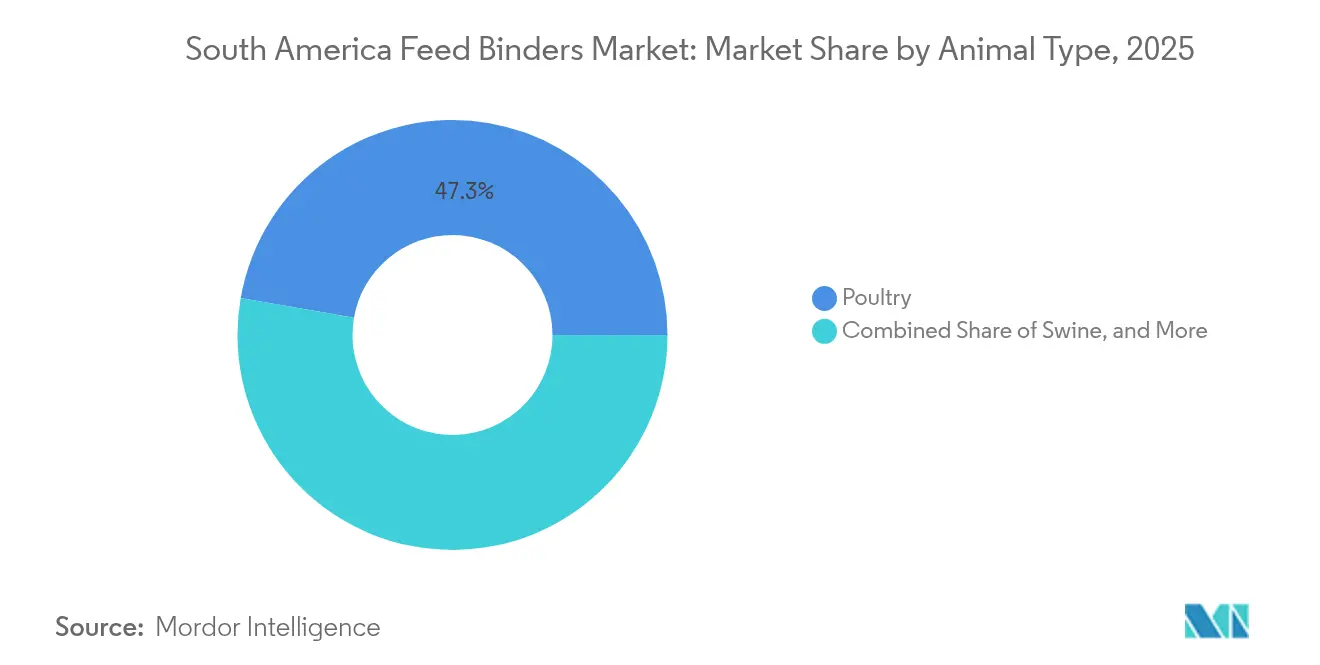

- By animal type, Poultry applications dominate the South America feed binders market, with a 47.25% share in 2025, while aquaculture feed is projected to record the highest growth at a CAGR of 8.52% through 2031.

- By country, Brazil commanded 44.20% of the South America feed binders market size in 2025, while Colombia is forecast to grow fastest at 7.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Feed Binders Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Livestock Production | +1.8% | Brazil and Colombia with moderate effect in Argentina and Peru | Medium term (2-4 years) |

| Focus on Animal Health and Nutrition | +1.5% | Region-wide with strongest traction in Brazil and Chile | Long term (≥ 4 years) |

| Sustainability and Natural Feed Additives | +1.2% | Brazil, Argentina and Chile leading adoption | Long term (≥ 4 years) |

| Expansion of Precision Pelletization and Micro-Batch Feed Mills | +1.1% | Brazil core, spreading to Colombia and Argentina | Medium term (2-4 years) |

| Surging Aquaculture Intensification along Amazon Basin | +0.9% | Brazil Amazon, spillover to Peru and Colombia | Short term (≤ 2 years) |

| Government Carbon-Intensity Programs Driving Methane-Reducing Binders | +0.8% | Brazil and Argentina with pilot work in Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Livestock Production

Commercial animal numbers continue to climb in Brazil and Colombia, lifting compound feed output and creating a sustained pull for durable binders that cut fines and improve pellet density. According to FAOSTAT, Brazil's production of poultry meat was 14.9 million metric tons in 2022, which increased by 15.0 million metric tons in 2023[2]Source: Food and Agriculture Organization of the United Nations, “FAOSTAT: Livestock and Fishery Production Domain,” fao.org. Even in Argentina, where cattle numbers slipped in 2024, export-oriented feedlots still rely on consistent binder performance to secure premium carcass yields. Peru’s cash-positive broiler and swine operators are also shifting from mash to pelleted formulations, opening opportunities for specialized binding systems compatible with lower-throughput mills.

Focus on Animal Health and Nutrition

The regional shift toward antibiotic-free production systems has elevated the importance of functional feed binders that deliver gut health benefits beyond mechanical pellet integrity. Argentina's Resolution 445/2024 prohibits antimicrobial use for growth promotion and sub-therapeutic dosing, creating immediate market opportunities for binders incorporating prebiotics, organic acids, or botanical extracts. Brazilian broiler integrators now ask for plant tannin or yeast-derived binders that combine physical cohesion with microbiome modulation. Chilean salmon producers pursue kelp-based hydrocolloids enriched with prebiotics to enhance disease resistance during warm-water stress events. These multifaceted requirements favor suppliers that can deliver turnkey technical advice alongside the product.

Sustainability and Natural Feed Additives

Corporate sustainability commitments and consumer pressure have accelerated the transition from synthetic to natural binding solutions across major South American feed manufacturers. Borregaard's LignoBond lignin-based binders demonstrate this shift, with field trials in Brazil showing improved dairy pellet quality while meeting organic certification requirements. CP Kelco's Brazilian manufacturing operations for pectin, carrageenan, and xanthan gums position the company to capitalize on marine-derived hydrocolloid demand, particularly for aquaculture applications where water stability and biodegradability provide competitive advantages. Natural binder adoption faces technical challenges, including variable raw material quality and higher costs compared to synthetic alternatives, and regulatory frameworks increasingly favor bio-based solutions.

Expansion of Precision Pelletization and Micro-Batch Feed Mills

High-speed conditioners, liquid dosing systems, and automated mixing platforms permit binder application within narrow moisture and temperature windows, resulting in tighter pellet quality targets. Brazilian integrators are retrofitting mills with micro-batch lines that craft flock-specific ratios and permit on-the-fly binder dosage changes. Colombia’s newest broiler complex integrates real-time NIR sensors that feed back to a programmable logic controller managing lignosulfonate sprays. These investments heighten demand for binders with predictable viscosity, rapid dispersion, and compatibility with online viscosity tracking devices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Raw-Material Price Volatility | -1.2% | Region-wide with highest stress in Argentina | Short term (≤ 2 years) |

| Capital Requirement for Modern Pellet Mills | -0.8% | Small and medium mills across all countries | Medium term (2-4 years) |

| Low Density of Cold-Chain and Humidity Control in Remote Ports | -0.7% | Coastal export corridors | Medium term (2-4 years) |

| Regulatory Uncertainty on Secondary-Metabolite Residue Limits | -0.5% | Cross-border trade linked to Europe Union and United States standards | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Raw-Material Price Volatility

Commodity price fluctuations for key binder ingredients create significant margin pressure and formulation instability for regional feed manufacturers. Corn-based starch prices, fundamental to many binding systems, experience seasonal variations exceeding 25% annually, while guar gum imports from India face currency exchange risks and supply chain disruptions. Currency devaluation in Argentina magnifies import bills for specialty polymers while Brazilian mills fight freight surcharges tied to river droughts. Contracting long-term supply and diversifying toward locally available lignocellulosic sources are the main mitigation strategies, and supplier consolidation limits bargaining leverage.

Capital Requirement for Modern Pellet Mills

Infrastructure investment barriers limit advanced binder technology adoption among smaller and medium-sized feed operations throughout the region. Modern conditioning and pelleting systems essential for optimal binder performance require capital investments ranging from USD 200,000 to USD 1 million, depending on capacity and automation levels. Rural cooperatives and mid-tier swine mills often delay upgrades, restricting them to dry powders or suboptimal binder inclusion levels. Absence of concessional lending in parts of Peru and Colombia slows modernization, preserving a structural gap between large integrators and legacy mills.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Natural Solutions Dominate Sustainability Drive

Natural binders command 61.35% South America feed binder market size in 2025 and are forecast to expand at a 7.34% CAGR, reflecting the region's accelerating transition toward sustainable feed additive solutions. Clay-based binders, particularly bentonite and kaolin, maintain strong positions in traditional livestock applications due to their cost-effectiveness and proven durability in pellet performance. Plant-based solutions, including guar gum and starch derivatives, are gaining traction in premium feed formulations, supported by local production capabilities and compatibility with organic certification. Hydrocolloids such as carrageenan and xanthan demonstrate particular strength in aquaculture applications where water stability requirements favor marine-derived binding agents over terrestrial alternatives.

Synthetic alternatives primarily serve cost-sensitive applications and specialized industrial feed requirements. Polyvinyl acetate and acrylic polymers maintain relevance in high-throughput commercial operations where consistent binding performance outweighs sustainability considerations. Regulatory pressure and consumer preferences are increasingly constraining the adoption of synthetic binders, particularly in export-oriented livestock operations serving European and North American markets with stringent residue standards.

By Animal Type: Aquaculture Emerges as Growth Engine

Poultry applications dominate the South America feed binders market with a 47.25% share in 2025, reflecting the sector's industrial maturation and focus on feed conversion optimization across broiler and layer operations. Broiler feed represents the largest single application due to its high feed volumes and stringent pellet quality requirements, which minimize waste and maximize growth performance. Layer feed applications emphasize calcium binding and shell quality enhancement, driving demand for specialized binder formulations that improve mineral availability and reduce dust generation in automated feeding systems. Swine applications maintain steady demand patterns, particularly in Brazil's integrated pork production systems, where feed conversion efficiency has a direct impact on profitability margins.

Aquaculture emerges as the fastest-growing segment with an 8.52% CAGR through 2031, driven by Amazon Basin intensification and Chilean salmon industry expansion. Fish feed applications, particularly for tilapia and tambaqui, require water-stable binders that prevent nutrient leaching and maintain pellet integrity in aquatic environments. Shrimp feed represents a premium application segment where specialized marine polysaccharides command higher prices due to their superior water stability and digestibility characteristics.

Geography Analysis

Brazil’s 44.20% share of the South American feed binders market is based on its ranking as the world’s third-largest compound feed producer and its broad species mix, which spans broilers, layers, pigs, cattle, and an expanding tilapia sector. The country's feed production is expected to grow by 2% in 2025, driven by the resilience of the poultry sector and emerging aquaculture opportunities in the Amazon Basin, where tilapia and tambaqui production is intensifying. In 2024, ADM's new capacity expansion in Paraná, which boosts production by 40%, demonstrates the multinational's confidence in Brazilian market fundamentals and regional export potential to Chile, Peru, and Bolivia .

Argentina holds the second slot, yet its path diverges. Herd downsizing and high inflation suppress feed tonnage, but value-added beef export channels keep binder demand steady in feedlots targeting European certifications. SENASA’s (National Service of Agri-Food Health and Quality) antibiotic ban sparks a rapid pivot to multifunctional natural binders, positioning local starch processors as new entrants. Currency depreciation increases the USD cost of imported acrylic polymers, indirectly encouraging formulators to consider domestic lignocellulosic options.

Colombia is forecast to grow fastest at a 7.22% CAGR through 2031. Colombian poultry output is rising, stimulating micro-batch mill installations near Bogotá and Cali that favor premium binder inclusion. Peru’s frontier markets in La Libertad and Piura pivot toward pelleted dairy rations, unlocking sales for guar blends that improve pellet hardness in humid coastal climates. Remaining South American nations contribute niche demand but promise upside once political and macroeconomic stability returns.

Competitive Landscape

The South American feed binders market is moderately consolidated, with players contributing to this sector including Cargill, Incorporated, Archer-Daniels-Midland Company, Evonik Industries AG, BASF SE, and Adisseo Nutrition. These players are known for focusing on R&D, broadening their product portfolios, maintaining a wide geographical presence, and employing an aggressive acquisition strategy.

Technical service emerges as the main differentiator. Leading firms conduct on-site pelleting audits, adjust steam profiles, and supply data loggers to track durability. Middle-tier regional companies such as Nutron and Guarany compete by bundling vitamin premixes and mycotoxin adsorbents with binders to create one-stop nutritional packages. Local starch producers in Brazil and Argentina are scaling up their capacity to meet the demand for natural binders, while forming alliances with hydrocolloid importers to offer hybrid solutions. Mergers and acquisitions concentrate on securing regional manufacturing footprints, exemplified by Innovad’s purchase of Oligo Basics in 2024, which adds South American distribution rights for plant gum binders.

Integration with digital manufacturing is a rising frontier. Suppliers develop cloud dashboards that correlate binder inclusion, pellet durability, and feed conversion ratios across customer sites. Automated viscosity sensors linked to programmable logic controllers allow mills to fine-tune inclusion rates, cutting over-application wastage. Companies offering both the binder and the software enjoy higher switching costs and customer stickiness.

South America Feed Binders Industry Leaders

Archer-Daniels-Midland Company

Evonik Industries AG

BASF SE

Adisseo Nutrition

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Cargill, Incorporated acquired the remaining 50% stake in SJC Bioenergia South Africa, which increased its dried distillers' grains (DDG) production capacity and enhanced its position in alternative protein ingredients for livestock feed applications in the South African market.

- October 2024: DSM-Firmenich has opened a new animal nutrition factory in Minas Gerais, Brazil’s largest state in the Southeast. The company stated that the plant will produce 100,000 metric tons of supplements, including feed binders, annually for the health and nutrition of beef and dairy cattle.

- May 2024: Innova Group acquired Brazilian feed additive supplier Oligo Basics, combining Innova's diverse portfolio with local manufacturing expertise to offer natural, sustainable solutions tailored to Brazilian and South American market requirements.

South America Feed Binders Market Report Scope

Animal feed binders are used for durability and resistance to physical breakdown during handling and storage of feeds. Some binders also have additional nutritional value. Unlike feed for livestock, feed for aquaculture requires an adequate level of processing to guarantee good stability in water, long enough for animals to consume it. For this reason, the role of the binder is crucial in determining variable levels of firmness adequate to specific feeding behavior. South American feed Binders Market is Segmented by Type (Natural and Synthetic), by Animal (Ruminant, Poultry, Swine, Aquaculture, and Other Animal Types), Geography (Brazil, Argentina, and the Rest of South America).

By Type

| Natural |

| Synthetic |

By Animal Type

| Poultry |

| Swine |

| Ruminants |

| Aquaculture |

| Other Animal Types |

By Country

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Type | Natural |

| Synthetic | |

| By Animal Type | Poultry |

| Swine | |

| Ruminants | |

| Aquaculture | |

| Other Animal Types | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the current value of the South America feed binders market?

It is valued at USD 318.12 million in 2026 and is projected to reach USD 426.48 million by 2031.

Which country leads demand for feed binders in South America?

Brazil accounts for 44.20% of regional demand, driven by its large poultry and aquaculture sectors.

Which binder type is growing fastest?

Natural binders are forecast to grow at 7.34% CAGR, fueled by sustainability initiatives and regulatory support.

Why are feed binders important for aquaculture?

They improve water stability of pellets, reduce nutrient leaching and help fish and shrimp achieve better feed conversion.

How is regulation influencing binder formulation in South America?

Bans on antibiotic growth promoters and emerging carbon-intensity programs are pushing demand toward multi-functional and natural binder solutions.

Page last updated on: