Africa Feed Prebiotics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

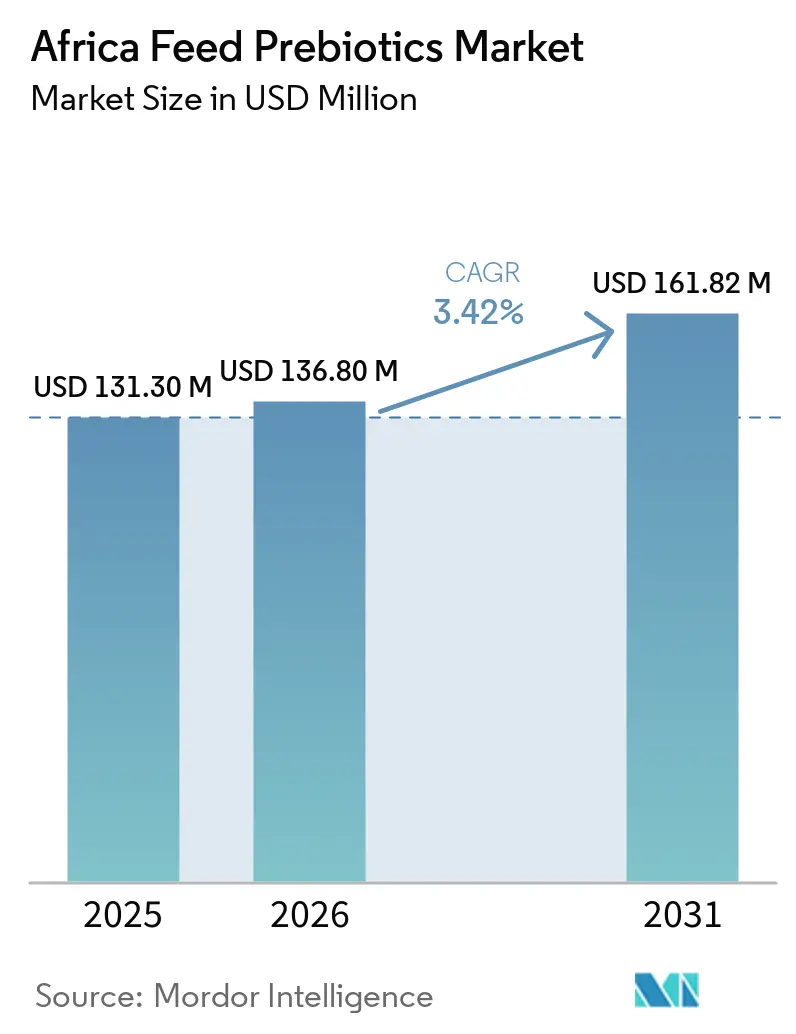

| Base Year Market Size (2025) | USD 131.30 Million |

| Market Size (2026) | USD 136.80 Million |

| Market Size (2031) | USD 161.82 Million |

| Growth Rate (2026 - 2031) | 3.42% CAGR |

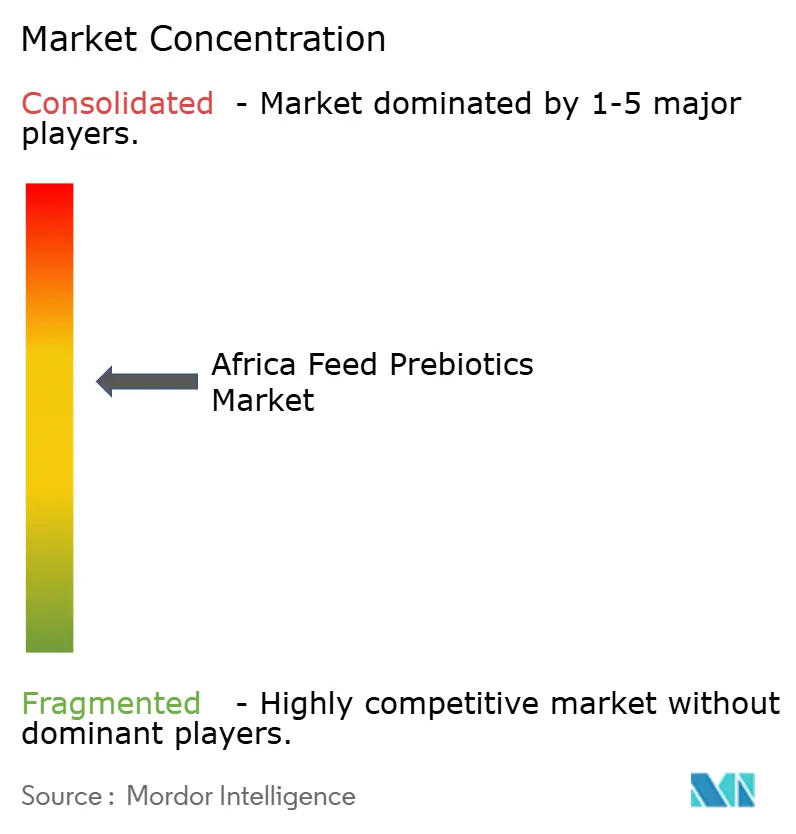

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Feed Prebiotics Market Analysis by Mordor Intelligence

The Africa feed prebiotics market size is anticipated to grow from USD 131.30 million in 2025 to USD 136.80 million in 2026 and is forecast to reach USD 161.82 million by 2031 at 3.42% CAGR over 2026-2031. The Africa feed prebiotics market is expanding through a steady shift away from antibiotic growth promoters (AGPs) in formal feed systems, even though adoption remains uneven across countries. Poultry and aquaculture feed demand continues to create a broad volume base, while export-facing livestock producers are also pushing feed mills toward safer and more consistent additive programs. The Africa feed prebiotics market also benefits from the need to protect gut health under variable grain quality and repeated contamination pressure in tropical feed chains. Competition in the Africa feed prebiotics market is still centered more on technical support, local validation, and regulatory readiness than on price alone. This leaves room for suppliers that can combine scientific proof, registration discipline, and dependable cross-border supply into a practical value proposition.

Key Report Takeaways

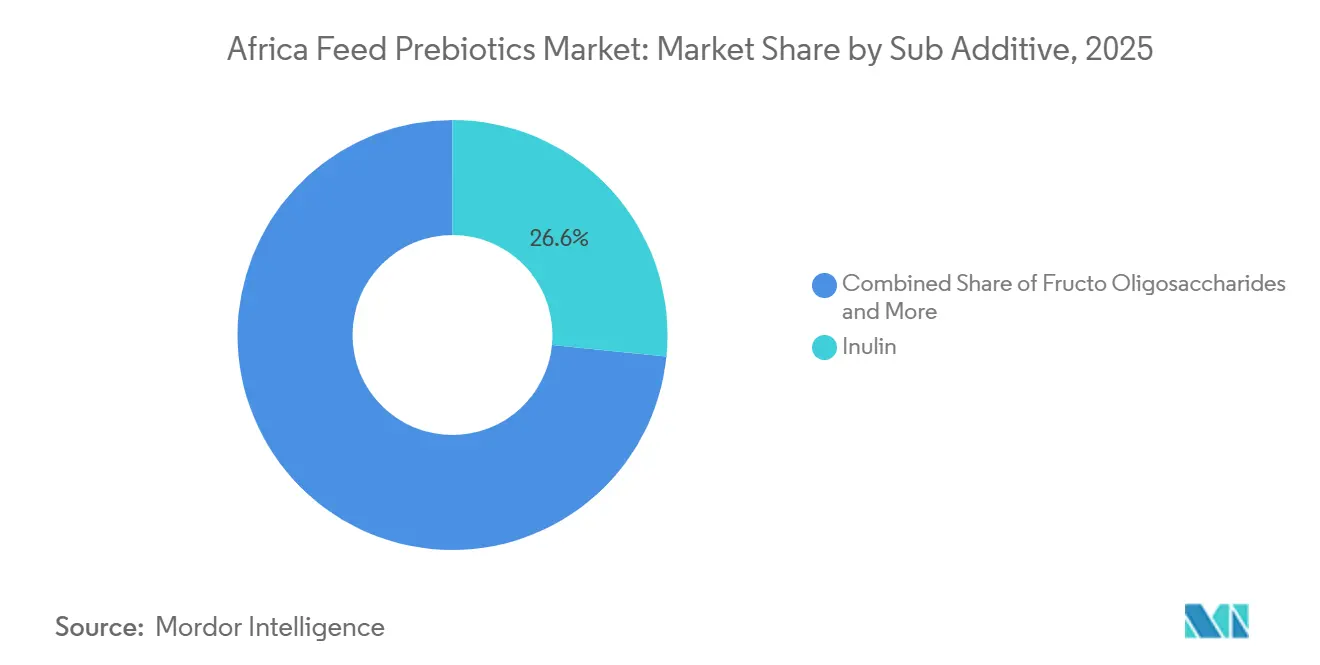

- By sub additive, inulin was the largest segment with 26.6% of the Africa feed prebiotics market share in 2025, and it is also the fastest segment with a projected 3.6% CAGR through 2031.

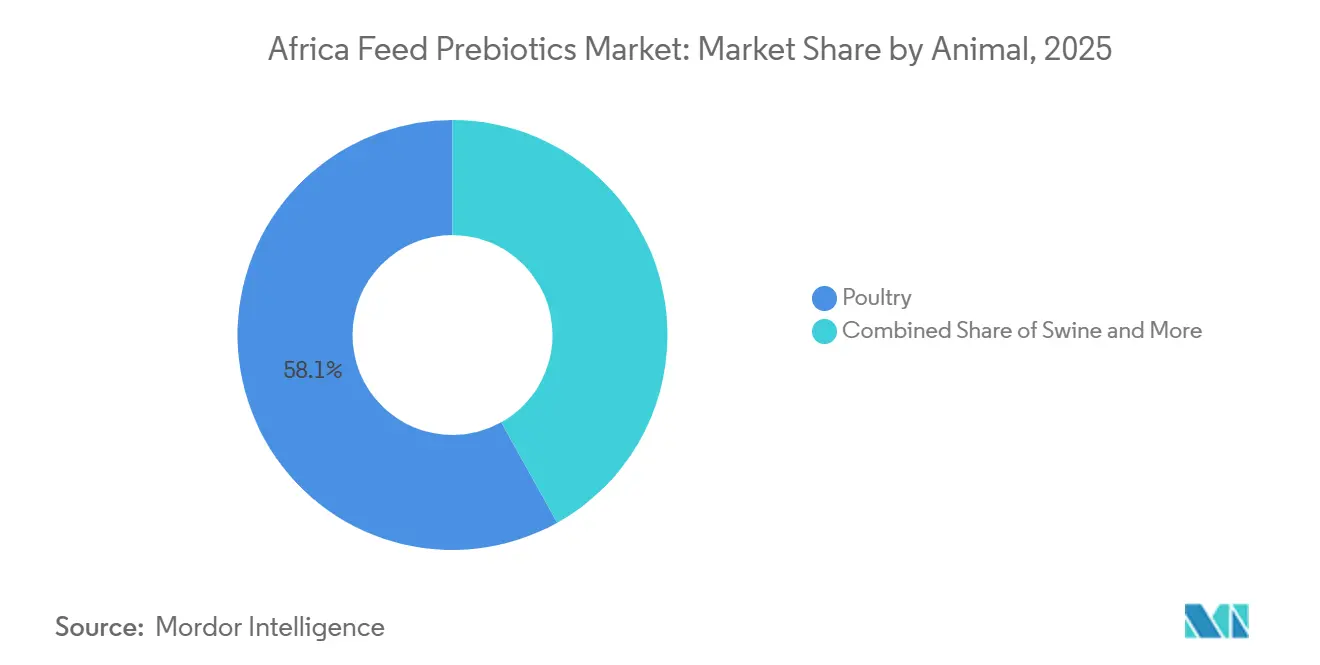

- By animal, poultry was the largest segment with 58.1% of the Africa feed prebiotics market size in 2025, while swine is the fastest segment with a projected 4.0% CAGR through 2031.

- By geography, South Africa was the largest segment with 48.4% share in 2025, and it is also the fastest segment with a projected 4.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Feed Prebiotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Poultry feed industrialization and rising antibiotic-alternative demand | +1.1% | South Africa, Nigeria, Kenya, Ghana | Short term (≤ 2 years) |

| Aquaculture scale-up in Egypt, Nigeria, and East Africa | +0.8% | Egypt, Nigeria, Kenya, Tanzania | Medium term (2-4 years) |

| Rising focus on gut health, feed efficiency, and flock resilience | +0.5% | South Africa, East Africa | Medium term (2-4 years) |

| Mycotoxin pressure raises demand for microbiome-supporting additives | +0.4% | Sub-Saharan Africa, North Africa | Short term (≤ 2 years) |

| Local premix and additive manufacturing improves product access | +0.3% | South Africa, Nigeria, Egypt | Long term (≥ 4 years) |

| Export-oriented integrators need tighter food safety programs | +0.2% | South Africa, Kenya, Egypt | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Poultry Feed Industrialization and Rising Antibiotic-Alternative Demand

The market is closely tied to the part of the poultry sector that is moving into formal, integrated production. Demand is strongest where broiler and layer operations are linked to retail chains, large processors, and buyers that require tighter residue control and documented feed practices. Uganda’s Animal Feeds Act 2024 shows how regulatory systems in East Africa are beginning to formalize oversight of additives and create a clearer path for compliant suppliers. This shift matters because the Africa feed prebiotics market is not growing evenly across all farm sizes, and verified volumes still sit mostly with larger integrators. Suppliers that can support trials, application guidance, and buyer-facing documentation are therefore better placed than suppliers competing only on ingredient price.

Aquaculture Scale-Up in Egypt, Nigeria, and East Africa

It is gaining support in aquaculture, where intestinal stability directly affects survival, feed use, and disease control in dense systems. A 2025 review in Aquaculture showed that sustainable aquafeed development in Africa is increasingly linked to bioactive ingredients that support resilience and performance[1]Source: Stanley Iheanacho et al., “Toward Resilient Aquaculture in Africa, Innovative and Sustainable Aquafeeds Through Alternative Protein Sources,” onlinelibrary.wiley.com. WorldFish also described how local feed innovation in Nigeria is being used to improve fish farming outcomes and reduce reliance on inferior feed practices. The Africa feed prebiotics market benefits from this trend because aquaculture producers make additive decisions on operational loss prevention rather than on branding or welfare messaging alone. That economic logic gives prebiotic suppliers a clearer path into value-based selling when performance can be shown under local water, feed, and stocking conditions.

Rising Focus on Gut Health, Feed Efficiency, and Flock Resilience

The market is driven by the need to address a key commercial challenge, ensuring consistent animal performance despite variability in feed ingredients. In 2025, AFGRI Animal Feeds reported that prebiotics, including fructo-oligosaccharides (FOS), mannan-oligosaccharides (MOS), inulin, and galacto-oligosaccharides (GOS), support the production of short-chain fatty acids, lower intestinal pH, and help restrict pathogen activity in poultry[2]Source: AFGRI Animal Feeds, “Enhancing Poultry Gut Health, The Roles of Prebiotics, Probiotics, and Postbiotics,” afgrianimalfeeds.co.za. A 2025 Scientific Reports highlighted that synbiotic supplementation enhanced performance and gut health in broiler chickens. In the Africa feed prebiotics market, this evidence supports purchasing decisions focused on feed conversion ratio (FCR) protection, flock consistency, and reduced response time to gut challenges, rather than broad health claims. Consequently, the highest demand is expected to come from commercial producers who view nutrition programs as a key factor in maintaining profit margins.

Mycotoxin Pressure Raises Demand for Microbiome-Supporting Additives

It is influenced by chronic grain quality risk, especially where storage and handling conditions support repeated fungal contamination. The International Livestock Research Institute documented multi-mycotoxin co-occurrence in semi-intensive broiler farms in Kenya in 2025, showing that feed exposure is not limited to a single toxin or commodity[3]Source: International Livestock Research Institute, “Multi-mycotoxin Occurrence and Their Risk to Poultry Health in Semi-intensive Broiler Farms in Kenya,” ilri.org. A 2025 study in Discover Applied Sciences also reported aflatoxin B1 contamination in dairy animal feeds in Ethiopia above Food and Agriculture Organization and World Health Organization limits. In the Africa feed prebiotics market, this keeps yeast-based solutions relevant because they sit at the intersection of gut support, contamination management, and day-to-day feed risk control.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity in low-margin feed formulations | -0.9% | Sub-Saharan Africa broadly, rural smallholder zones | Short term (≤ 2 years) |

| Dollar-linked import dependence and currency volatility | -0.7% | Nigeria, Egypt, Kenya, South Africa | Short term (≤ 2 years) |

| Patchy technical adoption beyond large integrators | -0.5% | West Africa, East Africa non-commercial tier | Medium term (2-4 years) |

| Fragmented registration and label-compliance rules | -0.4% | Pan-African, most acute outside South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity in Low-Margin Feed Formulations

It still faces a hard cost ceiling outside the most organized feed operations. Many mid-sized mills and informal producers review additives through an immediate payback lens, and that slows uptake when local efficacy data are limited or scattered. A 2025 review in Ruminants found that the body of quantitative evidence on the performance of natural feed additives in sub-Saharan Africa remains narrow, which helps explain why confidence remains weak among cautious buyers. This means the Africa feed prebiotics market grows much faster in export-linked or retail-linked systems than in broad informal feed channels. Until more local field data are visible and commercially relevant, price-sensitive buyers will continue to favor minimum-cost formulations over preventive gut health programs.

Dollar-Linked Import Dependence and Currency Volatility

The market remains dependent on imports because key active materials and fermentation-based ingredients are still sourced from outside the continent. Feed manufacturers carry that currency risk directly, and cost swings are difficult to absorb in domestic livestock systems where selling prices do not reset quickly. A 2025 review in Animal Feed Science and Technology identified agro-industrial residues, such as cassava processing waste, as possible prebiotic feedstocks, but it also makes clear that local conversion into scaled commercial products remains an emerging path rather than a present substitute. The Africa feed prebiotics market, therefore, remains vulnerable to procurement timing, exchange rate pressure, and slower ordering cycles when import economics become unstable. This constraint is strongest in countries where mills depend on imported specialty ingredients but sell into highly price-sensitive poultry, swine, and aquaculture sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Additive: Inulin Holds the Largest Position While Yeast Variants Extend Product Utility

Market share in this segment remained concentrated in inulin, which held 26.6% of Africa feed prebiotics market share in 2025, and maintained the clearest commercial lead across formal feed channels. Inulin also posted the fastest forecast in this category, at 3.6% through 2031, suggesting continued preference rather than a mature ceiling. Afrikaanse Bedryfsontwikkeling (AFGRI) Animal Feeds described how inulin and related prebiotics support beneficial microbial activity and reduce intestinal conditions that favor pathogen growth. In the Africa prebiotics industry, this matters because poultry producers tend to choose solutions that support both gut consistency and usable field performance despite uneven ingredient quality.

Market size in this segment continues to rest on a wider portfolio than inulin alone, because yeast derivatives, live yeast, spent yeast, torula dried yeast, selenium yeast, and whey yeast each address different buyer priorities. Yeast derivatives remain the second-largest commercial group because they support microbiome function and fit well into contamination-management programs where mills want more than one layer of protection. The European Commission renewed authorization in 2026 for the Saccharomyces cerevisiae CBS 493.94 preparation from Alltech Ireland as a zootechnical additive and gut flora stabilizer for ruminants, thereby strengthening global scientific confidence in live yeast use. In the Africa feed prebiotics industry, this creates room for a tiered supplier strategy, with premium inulin at one end and more cost-accessible yeast-based options at the other.

By Animal: Poultry Delivers the Largest Base While Swine Posts the Fastest Growth

Market share by animal remained heavily led by poultry, which accounted for 58.1% of Africa feed prebiotics market size in 2025 and set the direction for ingredient demand across the region’s formal livestock feed systems. Poultry remained the largest segment because broiler and layer operations absorb feed additives more consistently than other animal groups and respond faster to changes in food safety expectations. A 2025 review published in Poultry Science through PubMed Central found that prebiotic supplementation improved gut microbiota balance and supported stronger zootechnical and health performance in broiler chickens. That evidence aligns with how the Africa feed prebiotics market is actually bought, where poultry producers prioritize repeatable flock outcomes and practical risk reduction.

Market size expansion by animal is projected to be fastest in swine, which is projected to grow at 4.0% through 2031 as commercial pig production expands and gut stability at weaning remains a key production issue. A 2025 review in Metabolites noted that synbiotic strategies combining prebiotics and probiotics deliver strong gut health outcomes during the swine weaning transition. Aquaculture is also gaining ground, supported by the search for more resilient feeding programs in intensive fish systems. Ruminants remain relevant where yeast culture and live yeast products are already familiar, and in Veterinary Science found improved growth, immune function, and intestinal microbiota structure in supplemented beef cattle. Other animals remain smaller in volume, but they support specialized nutrition programs where higher additive inclusion can still be justified.

Geography Analysis

South Africa held 48.4% of Africa feed prebiotics market share in 2025, making it the largest country market and the main anchor for formal additive demand on the continent. South Africa is also projected to be the fastest geographic segment, with 4.0% growth through 2031, which reflects an expanding shift toward non-antibiotic feed strategies rather than a mature replacement cycle. The country’s regulatory setting remains the most structured in the region under the Fertilizers, Farm Feeds, Agricultural Remedies and Stock Remedies Act, Act No. 36 of 1947, and that gives registered suppliers a clearer route to commercial scale. Kemin Industries stated in 2025 that regulatory work for its feed biosecurity solution was underway in South Africa, which shows how seriously global suppliers view the country’s approval pipeline.

Egypt and Nigeria form the next important layer of the Africa feed prebiotics market because each country combines expanding animal protein demand with a stronger move toward commercial feed systems. Egypt’s position comes largely from freshwater aquaculture and the need for ingredients that can support intestinal stability in dense production environments. Nigeria matters through poultry and fish feed demand, while local innovation programs continue to improve the technical base for more advanced feed formulations. WorldFish highlighted in 2025 that resilient fish farming in Nigeria depends on local feed innovation and better formulation capability, which creates a more credible route for specialty ingredients over time.

The Rest of Africa remains smaller in immediate value, but it carries much of the future expansion potential for the Africa feed prebiotics market. Kenya stands out because documented multi-mycotoxin risk in broiler systems creates a direct reason to adopt microbiome-supporting additives in formal feed programs. East African aquaculture systems in Kenya, Uganda, Tanzania, and Rwanda are also becoming more relevant as feed quality and productivity receive more attention from producers and development-linked technical programs. As these markets formalize, supplier advantage is likely to depend on registration readiness, application support, and the ability to translate science into affordable local use.

Competitive Landscape

The Africa feed prebiotics market is moderately concentrated in 2025 in the formal supplier layer, with a small group of global fermentation, yeast, and functional fiber companies controlling much of the technically serviced business. The market is not fully consolidated because regional distributors and local blenders still serve the lower-priced middle of the market, especially where buyers prefer bundled premixes and flexible pack sizes. Even so, the Africa feed prebiotics market rewards suppliers that can provide evidence under African production conditions, not just global product catalogs. This keeps technical service, formulation support, and regulatory discipline at the center of competition.

A major strategic move came in February 2026, when DSM-Firmenich announced an agreement to divest its Animal Nutrition and Health business to CVC Capital Partners for EUR 2.2 billion (USD 2.6 billion). Another important step came in 2025, when Novonesis agreed to acquire DSM-Firmenich’s share of the Feed Enzyme Alliance for EUR 1.5 billion (USD 1.65 billion), broadening its animal biosolutions portfolio. These deals matter to the Africa feed prebiotics market because African feed mills often prefer suppliers with wider solution sets, stronger documentation, and a single technical contact across multiple additive categories. Portfolio breadth is therefore becoming a real commercial advantage in larger feed accounts.

Competitive activity also shows up in partnership and platform expansion. Lesaffre expanded its capacity for yeast derivatives through its 2025 joint venture with Zilor, enhancing its global position in specialty fermentation ingredients. The company also has a significant industrial and commercial presence in Africa, with major production, distribution, and blending facilities in countries such as Egypt, Algeria, Ivory Coast, and South Africa.. In the Africa feed prebiotics market, these moves support a competitive pattern where scale, science, and application depth matter more than commodity pricing. Suppliers still have room to grow in aquaculture, mid-tier premix systems, and integrated solutions linked to mycotoxin management.

Africa Feed Prebiotics Industry Leaders

Alltech, Inc.

DSM-Firmenich AG

Lesaffre et Compagnie

Orffa International Holding B.V.

Lallemand Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DSM-Firmenich has agreed to sell its Animal Nutrition and Health business to CVC Capital Partners for EUR 2.2 billion (USD 2.6 billion). projected to close by 2026, the deal will create two specialized entities under CVC. One for premix and performance solutions, and another for vitamins and carotenoids. This may impact global additives and Africa feed prebiotics supply dynamics.

- January 2026: The European Union renewed authorization for Saccharomyces cerevisiae CBS 493.94, Alltech's preparation, as a zootechnical feed additive and gut flora stabilizer for ruminants under Commission Implementing Regulation 2026/168. This reinforces the credibility of live yeast in ruminant applications within the Africa feed prebiotics market.

- February 2025: Novonesis signed an agreement with DSM-Firmenich to acquire the Feed Enzyme Alliance's sales and distribution activities for EUR 1.5 billion (approximately USD 1.55 billion), with the transaction expected to be completed by 2025. The acquisition expands Novonesis' animal biosolutions portfolio from probiotics and prebiotics into feed enzymes, creating a more comprehensive offering for African feed mill customers.

Africa Feed Prebiotics Market Report Scope

Feed prebiotics are specialized, non-digestible plant fibers or carbohydrates added to animal diets to serve as food for beneficial gut bacteria. By selectively nourishing these microbes, they improve gut health, enhance digestion, and boost immunity and overall livestock performance.

The Africa Feed Prebiotics Market Report is Segmented by Sub Additive (Fructo-Oligosaccharides, Galacto-Oligosaccharides, Inulin, Lactulose, Mannan Oligosaccharides, Xylo Oligosaccharides, and Other Prebiotics), Animal (Aquaculture, Poultry, Ruminants, and Swine), and Geography (South Africa, Kenya, Egypt, Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Inulin |

| Fructo Oligosaccharides |

| Galacto Oligosaccharides |

| Xylo Oligosaccharides |

| Lactulose |

| Mannan Oligosaccharides |

| Other Prebiotics |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

| South Africa |

| Kenya |

| Egypt |

| Rest of Africa |

| By Sub Additive | Inulin | |

| Fructo Oligosaccharides | ||

| Galacto Oligosaccharides | ||

| Xylo Oligosaccharides | ||

| Lactulose | ||

| Mannan Oligosaccharides | ||

| Other Prebiotics | ||

| Animal Type | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| Country | South Africa | |

| Kenya | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the Africa feed prebiotics sector?

The Africa feed prebiotics market is valued at USD 136.80 million in 2026 and is projected to reach USD 161.80 million by 2031, growing at 3.42% over the forecast period.

Which sub additive leads demand across Africa?

Inulin is the largest and fastest sub additive category, holding 26.6% share in 2025 and advancing at 3.6% through 2031.

Why does poultry dominate feed prebiotic use in Africa?

Poultry accounts for the largest share at 58.1%, as large broiler and layer systems consistently adopt additives. Producers prioritize prebiotics for gut stability, pathogen control, and improved feed conversion.

Which animal group is expanding fastest?

Swine is the fastest-growing animal segment, with projected growth of 4.0% through 2031, supported by commercial piggery expansion and the need to manage weaning stress.

Which country is most important in African demand?

South Africa accounts for 48.4% of the market and has the fastest-growing CAGR of 4.0%. This growth is driven by structured feed regulations, well-established formal feed channels, and increasing interest in non-antibiotic nutrition programs.

What are the main barriers to stronger adoption?

The main barriers are price sensitivity outside formal integrators, imported ingredient dependence, currency pressure, uneven technical adoption, and fragmented registration rules across countries.

Page last updated on: