Human Enhancement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

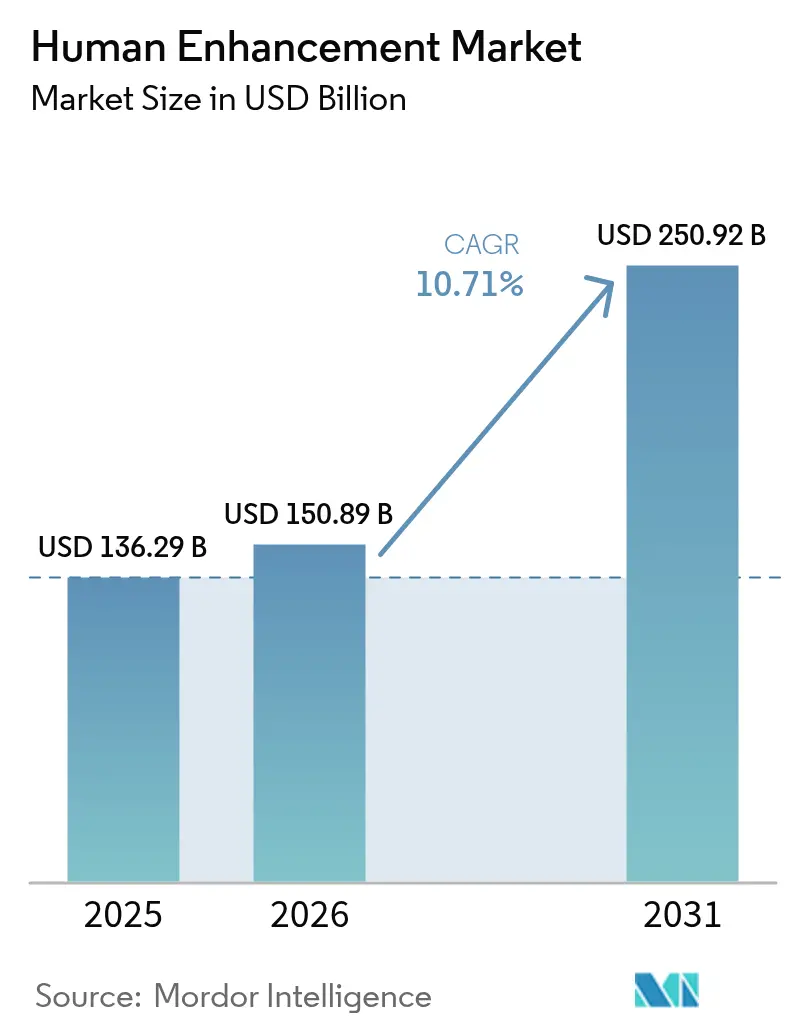

| Market Size (2026) | USD 150.89 Billion |

| Market Size (2031) | USD 250.92 Billion |

| Growth Rate (2026 - 2031) | 10.71% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Human Enhancement Market Analysis by Mordor Intelligence

The human enhancement market size was valued at USD 136.29 billion in 2025 and estimated to grow from USD 150.89 billion in 2026 to reach USD 250.92 billion by 2031, at a CAGR of 10.71% during the forecast period (2026-2031). A decisive pivot from reactive treatment to proactive augmentation is unfolding as edge-AI chips run health algorithms locally, exoskeletons move from trial to procurement, and wearable batteries last long enough for continuous monitoring. U.S. Food and Drug Administration clearances for sleep-apnea detection on Apple Watch and for Abbott’s FreeStyle Libre 3 Plus illustrate how miniaturized sensors and efficient firmware are collapsing the gap between wellness gadgets and regulated medical devices. Chronic diseases now drive 74% of global mortality, while the cohort aged 60 and above is forecast to exceed 1.4 billion by 2030, putting mobility and metabolic tracking devices into mainstream retail channels. Defense ministries view powered exoskeletons as force multipliers and are issuing multi-year contracts that reduce manufacturer risk. At the same time, data-privacy mandates such as the EU General Data Protection Regulation compel on-device processing to keep biometric streams local.

Key Report Takeaways

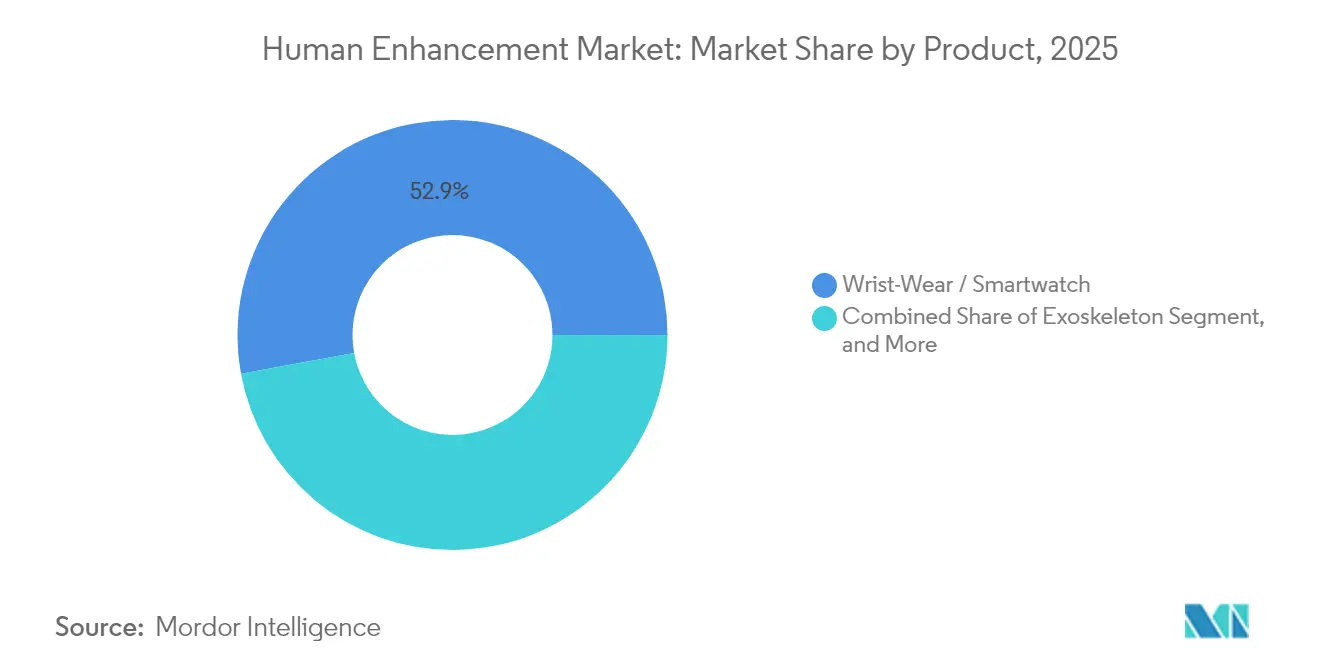

- By product type, wrist-wear and smartwatches led with 52.88% revenue share in 2025, while exoskeletons are projected to expand at an 11.39% CAGR through 2031.

- By application, healthcare and rehabilitation accounted for 41.96% of 2025 revenue, whereas military and defense applications are poised for the fastest 12.43% CAGR to 2031.

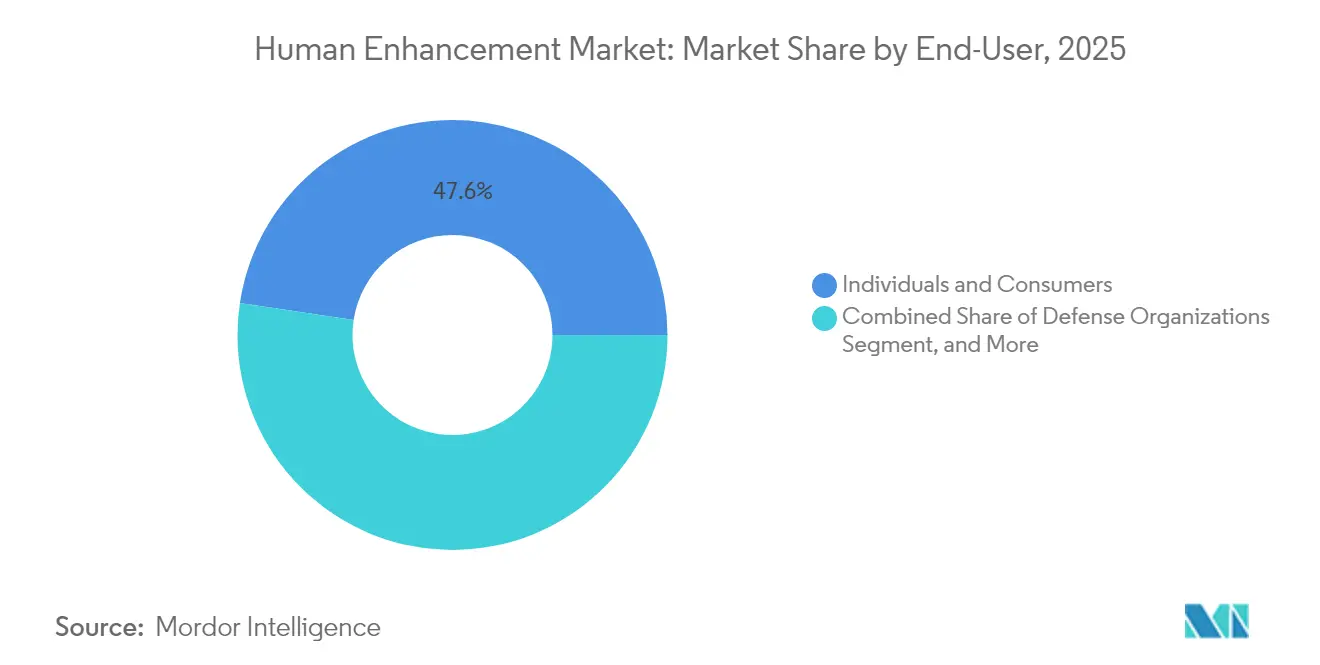

- By end-user, individuals and consumers commanded 47.62% of spending in 2025, yet defense organizations will grow at an 11.63% CAGR during the forecast window.

- By technology, wearable electronics held 54.45% of 2025 revenue, and brain-computer interfaces are projected to post a 11.98% CAGR through 2031.

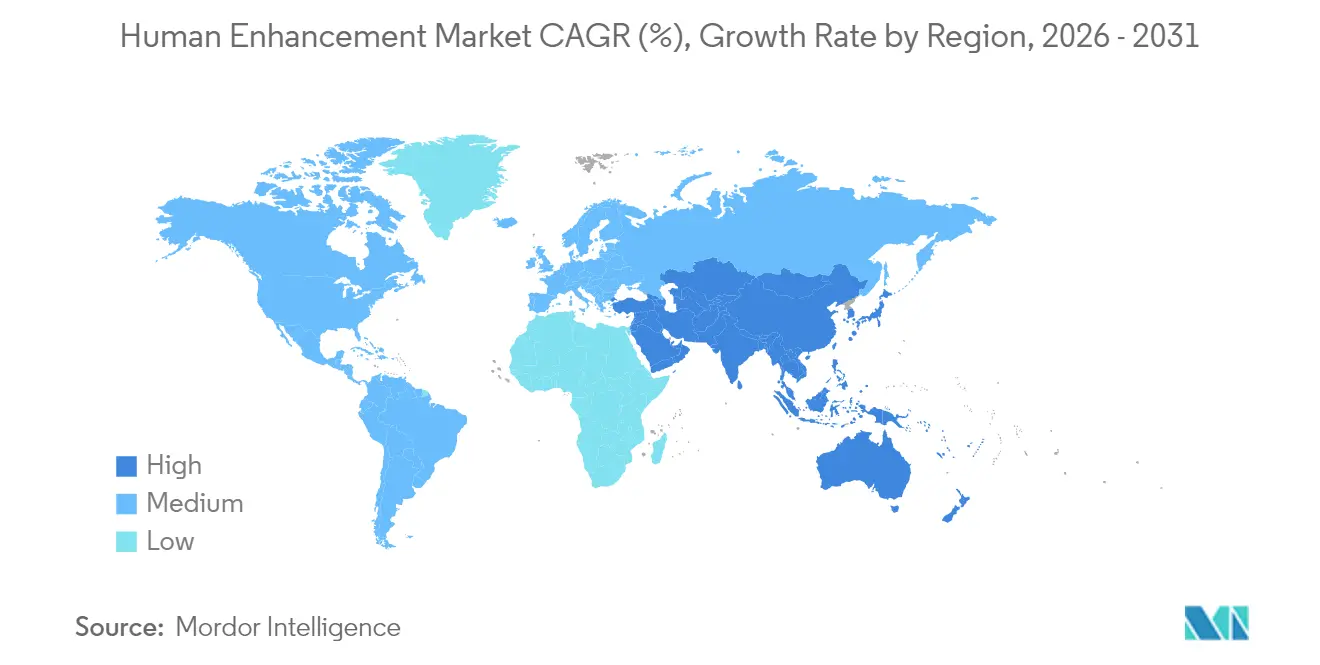

- By geography, North America captured 48.36% of 2025 revenue, but Asia-Pacific is set to record the highest 12.64% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Human Enhancement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancements in Wearable Sensor Miniaturization and Battery Life | +1.80% | Global, with early commercial deployment in North America and Asia-Pacific | Medium term (2-4 years) |

| Rising Prevalence of Chronic Diseases Boosting Demand for Assistive Devices | +2.10% | Global, particularly acute in North America, Europe, and aging Asia-Pacific markets | Long term (≥ 4 years) |

| Increasing Consumer Health and Fitness Awareness | +1.50% | Global, strongest in North America, Western Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Growing Aging Population Requiring Mobility and Cognitive Support | +1.90% | Global, most pronounced in Japan, South Korea, Germany, and Italy | Long term (≥ 4 years) |

| Integration of On-Device Edge AI Enabling Real-Time Personalized Assistance | +2.00% | Global, led by North America and China for AI chip production | Medium term (2-4 years) |

| Government Defense Programs Funding Soldier Augmentation Pilots | +1.20% | North America, Europe, and select Middle East nations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Advancements in Wearable Sensor Miniaturization and Battery Life

Sub-5-gram sensor stacks now combine accelerometers, microcontrollers, and solid-state batteries, allowing multi-day operation without recharging. MIT researchers embedded a 32-bit microcontroller and rechargeable cell into a single elastic fiber, proving garments can perform distributed inference at 95% accuracy. Apple’s sleep-apnea approval rides on the same trend, with edge algorithms parsing wrist motion locally to eliminate cloud latency.[1]U.S. Food and Drug Administration, “FDA Authorizations and Clearances,” fda.gov Higher energy densities, plus body-heat or kinetic energy harvesting prototypes, promise runtimes that make daily charging obsolete. As hardware friction dissolves, the human enhancement market integrates sensors into textiles, shoes, and helmets, extending addressable use cases. Component suppliers that co-optimize power and signal integrity now capture design-win premiums across consumer and clinical buyers.

Rising Prevalence of Chronic Diseases Boosting Demand for Assistive Devices

Noncommunicable ailments kill 41 million people each year, spurring payers and employers to subsidize continuous monitors that avert costly hospitalizations.[2]World Health Organization, “Noncommunicable Diseases,” who.int Abbott’s FreeStyle Libre 3 Plus delivers 14-day glucose streams and smartphone alerts, shifting diabetes care toward predictive intervention. Smartwatches with photoplethysmography and electrocardiogram sensors detect atrial fibrillation, nudging users to seek evaluation before stroke occurs. Regulatory sandboxes, such as the FDA Digital Health Center of Excellence, shorten review cycles for hybrid wellness-medical products, favouring firms with robust compliance teams. Economic modelling by health insurers shows remote monitoring lowers readmission penalties, fuelling enterprise bulk purchases that swell unit volumes in the human enhancement market.

Growing Aging Population Requiring Mobility and Cognitive Support

The world will host 1.4 billion people aged 60 plus by 2030, and nations with super-aged demographics already subsidize rehab robotics to offset caregiver shortages. Cyberdyne’s small-size HAL won Japanese clearance in 2025, opening pediatric and smaller-stature indications.[3]CYBERDYNE Inc., “Medical HAL Approval,” cyberdyne.jp Exoskeleton-aided gait therapy reduces fall risk and hospital stays, outcomes that resonate with cost-conscious health ministries. Hearing aids with AI noise-cancellation tackle age-related hearing loss, a condition projected to affect 900 million people by 2050. Brain-computer interfaces such as Synchron’s Stentrode give paralyzed patients cursor control, signalling future value for neurodegenerative care. As longevity rises, policy incentives, reimbursement codes, and caregiver relief accelerate device penetration across the human enhancement market.

Integration of On-Device Edge AI Enabling Real-Time Personalized Assistance

Edge inference slashes latency to milliseconds and keeps biometric data local, a compliance win under stringent privacy laws. SensorLM neuromorphic chips consume one-tenth the power of standard microcontrollers, enabling always-on anomaly detection without battery drain. Apple shifted atrial-fibrillation analysis onto the watch processor, freeing users from constant phone pairing. Defense programs layer augmented-reality overlays on soldier visors, where sub-100 ms response times are mission critical.[4]U.S. Department of Defense, “Defense Research Programs,” defense.gov Commercial players replicate the architecture for fall detection, glucose-trend warnings, and fatigue alerts, expanding the human enhancement market into environments with patchy connectivity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Costs of Advanced Enhancement Devices | -1.30% | Global, most acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Data Privacy and Security Concerns Around Biometric and Neural Data | -1.10% | Global, particularly stringent in EU under GDPR and forthcoming AI Act | Medium term (2-4 years) |

| Regulatory Uncertainty for Hybrid Wellness-Medical Devices | -0.90% | Global, with divergent pathways in FDA (US), EMA (EU), and PMDA (Japan) | Medium term (2-4 years) |

| Supply Chain Constraints for High-Performance Flexible Electronics Materials | -0.80% | Global, concentrated in graphene and rare-earth supply chains dominated by China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Costs of Advanced Enhancement Devices

Powered exoskeletons list between USD 40,000 and USD 100,000, restricting adoption to defense buyers and reimbursed rehab centers. Robotics-as-a-Service spreads cost over monthly fees but raises lifetime expenses and embeds vendor lock-in. Fitness wearables face opposite pressures: Xiaomi retails trackers below USD 50, eroding margins for mid-tier brands. Medicare funds continuous glucose monitors but not wellness devices, creating reimbursement gaps that slow uptake. In emerging markets, out-of-pocket healthcare spending caps demand, meaning premium devices must either drop price or prove multi-year payback.

Data Privacy and Security Concerns Around Biometric and Neural Data

Biometric data reveal intimate health and behavioural insights, so breaches erode trust and invite fines that smaller vendors cannot absorb. GDPR treats health data as a special category, mandating explicit consent and strict storage controls. Neural interfaces amplify worries by capturing brain signals that could infer intent, prompting neuro-rights legislation debates. On-device processing mitigates exposure but ups the silicon bill of materials. Companies that architect privacy by design gain competitive advantage, yet the compliance overhead tempers the overall CAGR for the human enhancement market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smartwatches Dominate, Exoskeletons Surge

Smartwatches anchored 52.88% of 2025 revenue, reinforcing their role as the core gateway to the human enhancement market share. Exoskeleton revenue, although lower in absolute terms, is on an 11.39% growth trajectory that could materially shift the product mix by 2031. Head-mounted displays cater to surgical visualization and industrial maintenance but battle user comfort and battery limits. Smart clothing prototypes show promise through conductive fibers that power sensors without bulky packs, yet mass production remains elusive. Ear-worn devices combine hearing assistance and real-time translation, appealing to aging and cross-border workforces. Body-worn cameras, funded by law-enforcement grants, illustrate that enhancement extends beyond health to accountability. Neural interface devices are pre-commercial but have secured breakthrough FDA pathways, signalling future inclusion in the broader product portfolio.

The product landscape reflects a continuum from consumer price points under USD 50 for basic trackers to six-figure therapeutic robots. As premium smartwatches fold in FDA-cleared features, they blur lines with medical-grade equipment and pull diagnostic revenues into the consumer channel. Exoskeletons shift from experimental prototypes to pallet-lifting workhorses on factory floors, where injury reduction delivers tangible return on investment. Smart clothing could leapfrog wrist devices once durability and washability challenges drop. Ear-worn form factors ride an audio-first trend, integrating voice assistants and potential cognitive augmentation. In aggregate, these dynamics anchor the human enhancement market as a multiproduct arena in which overlap rather than substitution drives growth.

By Application: Healthcare Leads, Defense Accelerates

Healthcare and rehabilitation applications commanded 41.96% of 2025 spending, underlining their foundational influence on the human enhancement market size for clinical use. Military and defense are the fastest climbers, set to expand at 12.43% CAGR as governments validate exosuits for soldier load carriage and tactical awareness. Industrial safety deployments scale in warehousing and construction, where exoskeleton leasing models compress payback periods to under 12 months. Consumer fitness devices mature into holistic wellness platforms that integrate sleep, stress, and recovery scores, but saturation in developed economies pushes brands toward emerging-market expansion. Cognitive enhancement applications remain nascent yet attract venture funding as neural-gaming pilots showcase thought-controlled interfaces.

The application breakout shows convergence between medical and non-medical domains. Hospitals deploy continuous glucose monitors for at-home management to free bed capacity, while defense labs spin off tech later adopted by sports-memory coaches. Industrial buyers weigh assistive robotics against workers’ compensation and retention costs, creating data-driven procurement criteria. As consumer devices integrate approved diagnostics, the line between fitness and medical narrows, potentially unlocking reimbursement. Defense projects generate ruggedization standards that industrial exoskeleton manufacturers reuse, accelerating commercial reliability.

By End-User: Consumers Prevail, Defense Organizations Climb

Individuals accounted for 47.62% of 2025 purchases, confirming the retail pull that keeps human enhancement market demand diversified. Defense organizations, though smaller in value, register an 11.63% CAGR, reflecting formal procurement cycles and confidentiality clauses that ensure volume commitments. Healthcare providers adopt powered exoskeletons and glucose monitors under reimbursement codes, yet budget scrutiny slows experimental trials. Industrial enterprises rely on injury-reduction metrics to justify exosuit rentals, often bundling vendor training into service contracts. Academia and research institutions function as crucibles, generating evidence that converts early adopters into mainstream buyers.

Consumer segments bifurcate premium ecosystems by Apple and Samsung lock users in with proprietary services, while value brands like Xiaomi push affordable pools of basic functionality. Defense entities demand domestic supply chains and cybersecurity certifications, effectively narrowing the vendor field. Hospitals prioritize scalable, interoperable data platforms to ease electronic medical record integration. Industrial firms compare productivity gains against subscription costs, sometimes negotiating usage-based pricing. The resulting mosaic keeps the human enhancement market resilient to shocks in any single buyer group.

By Technology: Wearables Lead, Brain-Computer Interfaces Gain

Wearable electronics represented 54.45% of 2025 revenue, anchoring the human enhancement market as the most mature technology stack. Brain-computer interfaces, though early stage, hold a 11.98% growth outlook thanks to breakthrough device designations and encouraging clinical pilots. Exoskeleton robotics straddle hardware and software, merging actuators with biomechanical sensing for precise torque delivery. Gene editing and cell therapies aim at curative interventions but face ethical scrutiny when framed as enhancement. Implantable stimulators and cochlear devices deliver sensory restoration yet require surgical implantation, limiting uptake to patients with clear clinical indications.

Supply-chain dynamics favour vertically integrated wearables suppliers that control displays, batteries, and health silicon, letting them iterate features at smartphone cadences. Brain-computer interface firms solve electrode longevity and wireless power to transition from lab to living room. Exoskeleton designers hunt for lightweight composite materials and high-density batteries that reconcile torque with user comfort. Gene-editing ventures prioritize therapy but maintain intellectual property and tooling applicable to future augmentation. Implantable device makers explore less invasive insertion techniques to broaden candidacy, potentially adding elective enhancement procedures to their roadmaps.

Geography Analysis

North America held 48.36% of 2025 human enhancement market share due to early FDA approvals, high healthcare spend, and robust defense R and D pipelines. Asia-Pacific is forecast to post a 12.64% CAGR to 2031 as China leverages manufacturing economies of scale and Japan subsidizes mobility aids for its super-aged society. Europe benefits from universal healthcare reimbursements, yet GDPR compliance and multilingual labelling prolong launches and increase costs. The Middle East funds exoskeleton pilots within smart-city and border-security projects, while Africa adopts mobile health integrations that piggyback on high smartphone penetration.

The United States leads brain-computer interface research under DARPA grants, creating a spillover talent pool for private startups. Canada’s reimbursement for continuous glucose monitoring broadens addressable diabetic populations. China delivers over 60% of global smartwatch shipments through contract manufacturers in Shenzhen and Guangdong. Japan’s January 2025 clearance of Cyberdyne’s small-size HAL cements its rehabilitation robotics leadership. India’s Ayushman Bharat Digital Mission lays groundwork for integrating wearable feeds into national health records, yet rural bandwidth gaps slow real-time uploads.

Europe’s Medical Device Regulation demands post-market surveillance, raising compliance costs but improving patient safety. Germany and Italy, facing high dependency ratios, subsidize homecare exoskeleton rentals. Saudi Arabia and the United Arab Emirates funnel Vision 2030 budgets into telehealth and exoskeleton supply chains. South Africa pilots smart-clothing kits for mining safety, adding an industrial dimension to adoption. These varied regional priorities diversify revenue streams, reducing concentration risk and sustaining global growth in the human enhancement market.

Competitive Landscape

Competition remains fragmented as consumer-electronics giants extend health stacks, while specialized robotics and neural firms cultivate regulatory moats. Apple and Samsung design custom silicon, integrate operating systems, and monetize health subscriptions to deepen ecosystem lock-in. Garmin and Oura target endurance athletes and sleep optimizers, respectively, yet tolerance for premium pricing narrows as incumbents clone features. Ekso Bionics, ReWalk Robotics, and Cyberdyne differentiate through peer-reviewed clinical trials and multijurisdictional approvals, a barrier that consumer brands cannot quickly replicate.

Neuralink, Synchron, and Precision Neuroscience race to prove safe, reliable brain implants that deliver functional gains for paralysis. The first to secure pivotal trial success and scalable manufacturing could command disproportionate human enhancement market influence. Industrial exoskeleton suppliers such as German Bionic partner with KULR Technology Group to localize U.S. assembly, cutting lead times and qualifying for federal procurement. Zimmer Biomet’s July 2025 acquisition of Monogram Technologies evidences consolidation, knitting autonomous robotic surgery into legacy orthopedic portfolios. Meanwhile, privacy legislation and supply-chain shocks around graphene and rare earths favour vertically integrated manufacturers that can buffer materials volatility.

White-space opportunities persist in smart clothing, where academic breakthroughs await commercial scaling. Gene-editing firms such as CRISPR Therapeutics own patents that could pivot from therapy to elective enhancement if ethics boards loosen. Body-worn camera vendors leverage Department of Justice grants, anchoring a non-medical revenue stream rooted in transparency mandates. As defense prototypes mature, dual-use technology flows into consumer and industrial lines, blurring sector boundaries and fuelling competitive churn that keeps prices in check and innovation cycles short.

Human Enhancement Industry Leaders

Vuzix Corporation

Ekso Bionics Holdings Inc.

Google LLC

B-Temia Inc.

Samsung Electronics Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Zimmer Biomet announced a definitive agreement to acquire Monogram Technologies for USD 177 million upfront and contingent value rights tied to regulatory milestones.

- April 2025: KULR Technology Group secured exclusive North American distribution rights for German Bionic’s Apogee ULTRA exoskeleton and will localize assembly in the United States.

- January 2025: Cyberdyne obtained Japanese certification to sell its small-size Medical HAL Lower Limb Type B, expanding access to patients 100-150 cm tall.

- October 2024: Oura acquired Sparta Science, adding force-plate analytics to its sleep-tracking ecosystem for enterprise wellness clients.

Global Human Enhancement Market Report Scope

The Human Enhancement Market Report is Segmented by Product Type (Smartwatch, Head-Mounted Display, Smart Clothing, Ear-Worn Devices, Fitness Tracker, Body-Worn Camera, Exoskeleton, Neural Interface Device, Medical Enhancement Device), Application (Healthcare and Rehabilitation, Industrial and Workplace Safety, Consumer Fitness and Wellness, Military and Defense, Cognitive Enhancement and Neuro-Gaming), End-User (Individuals and Consumers, Healthcare Providers, Industrial Enterprises, Defense Organizations, Research and Academia), Technology (Wearable Electronics, Exoskeleton Robotics, Brain-Computer Interfaces, Gene Editing and Cell Therapy, Implantable Devices), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Smartwatch |

| Head-Mounted Display |

| Smart Clothing |

| Ear-Worn Devices |

| Fitness Tracker |

| Body-Worn Camera |

| Exoskeleton |

| Neural Interface Device |

| Medical Enhancement Device |

| Healthcare and Rehabilitation |

| Industrial and Workplace Safety |

| Consumer Fitness and Wellness |

| Military and Defense |

| Cognitive Enhancement and Neuro-Gaming |

| Individuals and Consumers |

| Healthcare Providers |

| Industrial Enterprises |

| Defense Organizations |

| Research and Academia |

| Wearable Electronics |

| Exoskeleton Robotics |

| Brain-Computer Interfaces |

| Gene Editing and Cell Therapy |

| Implantable Devices |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Middle East | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| Africa | South Africa |

| Nigeria | |

| Egypt |

| By Product Type | Smartwatch | |

| Head-Mounted Display | ||

| Smart Clothing | ||

| Ear-Worn Devices | ||

| Fitness Tracker | ||

| Body-Worn Camera | ||

| Exoskeleton | ||

| Neural Interface Device | ||

| Medical Enhancement Device | ||

| By Application | Healthcare and Rehabilitation | |

| Industrial and Workplace Safety | ||

| Consumer Fitness and Wellness | ||

| Military and Defense | ||

| Cognitive Enhancement and Neuro-Gaming | ||

| By End-User | Individuals and Consumers | |

| Healthcare Providers | ||

| Industrial Enterprises | ||

| Defense Organizations | ||

| Research and Academia | ||

| By Technology | Wearable Electronics | |

| Exoskeleton Robotics | ||

| Brain-Computer Interfaces | ||

| Gene Editing and Cell Therapy | ||

| Implantable Devices | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

Key Questions Answered in the Report

What is the current value of the human enhancement market?

The market is valued at USD 150.89 billion in 2026.

How fast is the human enhancement market expected to grow?

It is forecast to expand at a 10.71% CAGR, reaching USD 250.92 billion by 2031.

Which product category holds the largest share?

Smartwatches account for 52.88% of 2025 product revenue.

Which region will grow the fastest through 2031?

Asia-Pacific is projected to register a 12.64% CAGR, outpacing all other regions.

What technology shows the highest growth rate?

Brain-computer interfaces are expected to grow at a 11.98% CAGR through 2031.

Which application segment is expanding most rapidly?

Military and defense enhancement is forecast to grow at a 12.43% CAGR to 2031.

Page last updated on: